electronic trading under mifid-ii - norton rose · pdf file•mifid-ii work at esma: level...

TRANSCRIPT

Electronic trading under MiFID-II

Piebe B. Teeboom December 1, 2015

• MiFID-II work at ESMA: level 2 & 3 • Algo trading: Recap key points from level-1 • Overview of MiFID-II initiatives regarding algo trading / HFT / market

microstructure

• Focus on: – Definition of algo trading and DEA – Systems & Controls – Market making

Agenda

NortonRose - Electronic trading under MiFID-II

Board of Supervisors (BoS)

Standing Committees (SC)

Taskforces (TF)

SMSC: Secondary Markets Standing Committee

CDTF: Commodities Derivatives TF (position limits, position reporting, ancillary activity)

MDRWG: Markets Data Reporting Working Group (transaction reporting)

IPISC: Investor Protection and Intermediaries Standing Committee

Interaction with:

MISC: Market Integrity Standing Committee (=MAD-II/MAR)

PTSC: Post-trading Standing Committee (=EMIR)

Internal organisation of ESMA work

NortonRose - Electronic trading under MiFID-II

Drafting of L2/L3 work is collaborative effort

of ESMA Staff and NCA representatives

Secondary Markets Standing Committee (SMSC)

TF Transparency and the trading obligation for derivatives (TTF)

TF Microstructural issues (TF MSI)

TF Organisational requirements for trading venues

TF Data publication and access (TF DPA)

Market Data Reporting Working Group (MDRWG) Sub groups

SG1 : EMIR Trade Reporting

SG2 : MiFIR Transaction Reporting

SG3 : Instrument Reference Data

SG4 : Orderbook Data

Investor Protection and Intermediaries Standing Committee (IPISC)

TF1: Conduct Rules

TF2: Licensing

TF3: Organisational Requirements

MiFID Level-2 Task Forces

NortonRose - Electronic trading under MiFID-II

Policy objective: Regulating risks arising from algorithmic trading, with particular (but not exclusive) attention to HFT Risks: o Overloading of the systems of trading venues; o Creating a disorderly market (i.e. generating duplicative or erroneous

orders or otherwise malfunctioning); o Overreacting to other market events which can exacerbate volatility; o Market abuse / market manipulation o Prompting other investors to move to dark pools

Scope: o IFs that engage in algorithmic trading or high-frequency algorithmic

trading techniques; o IFs that provide direct electronic access (DEA); o DEA users; o General clearing members; o Trading venues (RM, MTF, OTF) o Members of trading venues (incl. insurance undertakings, UCITS

managers, dealers-on-own account in emissions allowances & commodities)

Algo trading: recap key points from Level 1

NortonRose - Electronic trading under MiFID-II

A. Licensing and organisational requirements • Defining HFT, DEA, algorithmic trading • Regulating HFT firms, members of trading venues, and clients of DEA providers • Systems and controls for investment firms, DEA providers, clearing members, and trading venues

B. Reporting, documentation and standards • Notification and documentation of algorithmic and HFT trading activity • Algo flagging • Exchange of order book data • Synchronisation of business clocks • Algo ID in transaction reporting

C. Market microstructure • Volatility management (i.a. circuitbreakers) • Tick sizes • Order to trade ratios (OTRs) • Fee structures • Co-location

D. Liquidity provision • Requirements for algo firms that undertake MM strategies (and market making schemes for TVs)

MiFID-II treatment of market microstructure can be distinguished in four main buckets

NortonRose - Electronic trading under MiFID-II

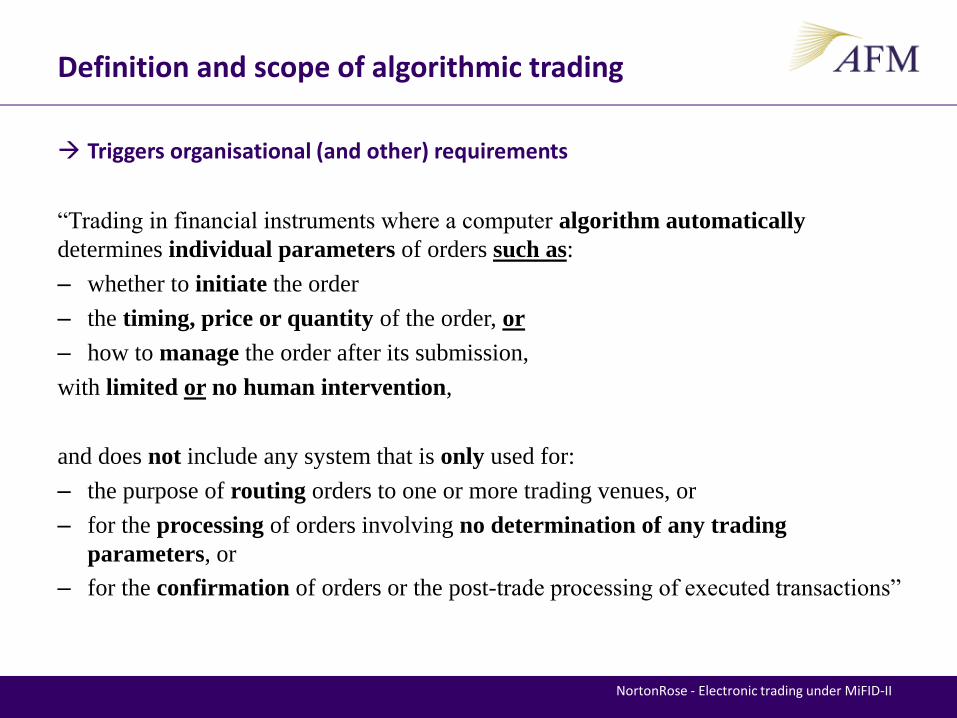

Triggers organisational (and other) requirements

“Trading in financial instruments where a computer algorithm automatically

determines individual parameters of orders such as:

– whether to initiate the order

– the timing, price or quantity of the order, or

– how to manage the order after its submission,

with limited or no human intervention,

and does not include any system that is only used for:

– the purpose of routing orders to one or more trading venues, or

– for the processing of orders involving no determination of any trading

parameters, or

– for the confirmation of orders or the post-trade processing of executed transactions”

Definition and scope of algorithmic trading

NortonRose - Electronic trading under MiFID-II

Clarifying the definition of algorithmic trading (ESMA’s technical advice for delegated acts)

• Optimisation of order execution processes by automated means (=smart order routers, SORs) are included in the definition of algorithmic trading

• Arrangements are considered as algorithmic trading if the system makes independent decisions at any stage of the processes on either initiating, generating, routing or executing orders

• Definition excludes automated order routers that only determine the venue(s) where the order should be submitted without changing any other parameters of

the order.

NortonRose - Electronic trading under MiFID-II

Relevance:

• Systems and controls requirements for DEA providers and trading venues allowing DEA

• DEA users will be regulated as investment firms

Conditions for DEA:

• Broker (= member of trading venue) provides clients with access to that trading venue through the use of its trading code;

• Clients can exercise discretion regarding the exact fraction of a second of order entry and regarding the lifetime of order within that timeframe

• Orders of clients are routed to the venue by deploying a SOR which is embedded into the clients' systems.

NB:

• DEA is not mutually exclusive from algo trading or HFT (i.e. a person can be covered by all three definitions)

• Use of SOR embedded into broker’s system = agency algorithmic trading, but not DEA Client has no full control over all order parameters, exact moment of order entry, and order lifetime.

Refining the definition of Direct Electronic Access (DEA)

NortonRose - Electronic trading under MiFID-II

RTS: Systems and controls for investment firms & trading venues

• Further specification of ESMA Guidelines (2012) • Scope: undertaking algorithmic trading activities or facilitating them

(trading venues / DEA providers / clearing members) • Less discretion on basis of proportionality

Key themes:

– Development, testing, deployment, and review of algos and trading systems

– Systems capacity and resilience – Pre-trade/post-trade controls – Monitoring and alerting (disorderly trading and market manipulation) – Kill switches – Systems security – Outsourcing – Governance framework

NortonRose - Electronic trading under MiFID-II

Scope:

o Firms that engage in algorithmic trading to pursue a market making strategy

o Venues for which it is appropriate to offer market making schemes

When? “Continuously” (=during specified proportion of trading hours, except under exceptional

circumstances)

What?

Firms

o Enter into a binding written agreement with the trading venue

o Provide liquidity on a regular and predictable basis to the trading venue

o Have in place effective systems and controls

Venues

o Have written agreements with all investment firms pursuing a market making strategy

o Offer schemes to ensure that a sufficient number of IFs participate in agreements

o Specifying the obligations of the IF and incentives offered

o Monitor and enforce compliance

o Inform NCA of content of agreements

RTS: Market making strategies and schemes

NortonRose - Electronic trading under MiFID-II

Defining “market making strategy”

[W]hen, as a member or participant of one or more trading venues, [the firm’s] strategy, when dealing on own account, involves posting firm, simultaneous two-way quotes of comparable size and at competitive prices relating to one or more financial instruments on a single trading venue or across different trading venues, with the result of providing liquidity on a regular and frequent basis to the overall market.

RTS 8 specifies:

• regular and frequent basis:

– 50% of trading hours (excluding opening/closing auction)

– for half of trading days

– during 1 month period

• ‘simultaneous’: both sides present in order book at the same time

• ‘comparable size’: sizes within 50% of each other

• ‘competitive prices’: at or within maximum bid-ask spread set by trading venue

Pragmatic approach: in at least one financial instrument on a single trading venue

NortonRose - Electronic trading under MiFID-II

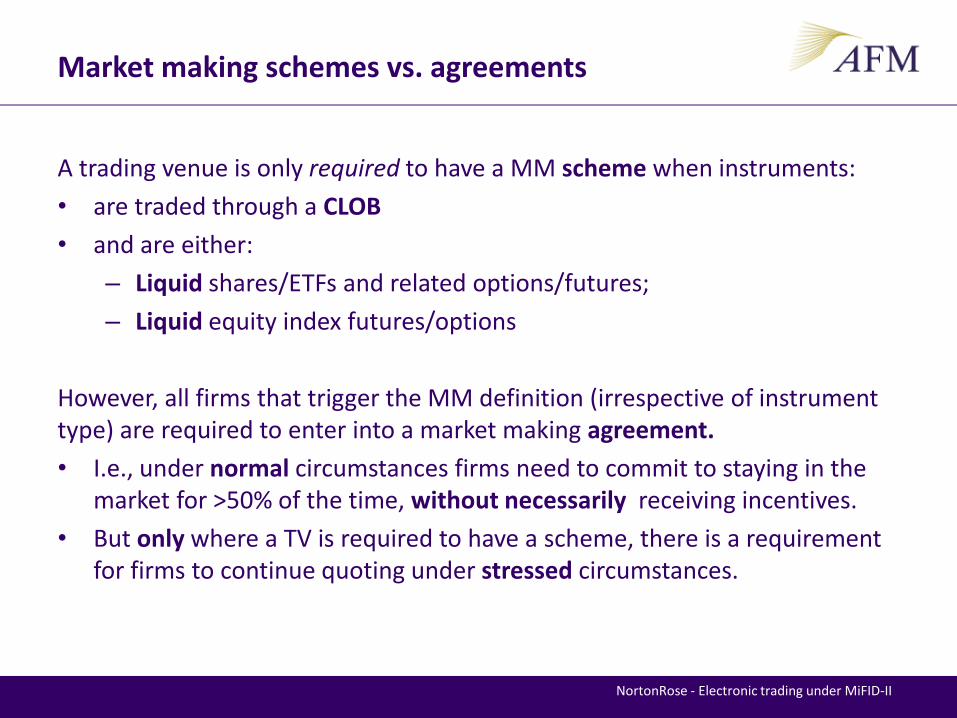

Market making schemes vs. agreements

A trading venue is only required to have a MM scheme when instruments:

• are traded through a CLOB

• and are either:

– Liquid shares/ETFs and related options/futures;

– Liquid equity index futures/options

However, all firms that trigger the MM definition (irrespective of instrument type) are required to enter into a market making agreement.

• I.e., under normal circumstances firms need to commit to staying in the market for >50% of the time, without necessarily receiving incentives.

• But only where a TV is required to have a scheme, there is a requirement for firms to continue quoting under stressed circumstances.

NortonRose - Electronic trading under MiFID-II

Market circumstances and market making requirements/incentives

NortonRose - Electronic trading under MiFID-II

VOLATILITY

Type of circumstance

Characteristics Required presence time

Incentives Scope in terms of instruments

Exceptional • Made public by Trading venue; includes:

a. Extreme volatility (interruption of trading) b. Political events & cybersabotage c. Disorderly trading conditions d. Investment firm unable to maintain prudent risk

management: a. Technological issues b. Risk management issues (capital, clearing,

or hedging problems) e. (for non-equity:) Suspension of pre-trade

transparency by NCA Exceptional circumstances do not include regular or pre-planned information events (e.g. publication of macroeconomic statistics)

0% -- • Liquid shares/ETFs and related options/futures;

• Liquid equity index futures/options

Stressed • Declared by trading venue

• Significant short-term change of price and volume

• Includes “fast markets” and resumption of trading after volatility interruptions

>50% • Required as per MM scheme

• Should be higher (taking into account additional risk under stressed circumstances)

• Liquid shares/ETFs and related options/futures;

• Liquid equity index futures/options

Normal >50% • Optional • Lower (but: no

incentives w/o MM scheme)

All