electricity and new zealand’s low-carbon future - bell gully...

TRANSCRIPT

W W W. B E L L G U L LY. C O M

December 2017

THE BIG PICTURE: Electricity and New Zealand’s low-carbon future

Contents

1 Introduction

2 Strong in renewable generation

3 The key to the future

4 Are regulations fit for purpose?

5 Structuring the electricity industry

6 An opportunity to look forward

7 The law of unintended consequences

8 New technologies, new services

11 From climate change to renewable energy

12 Endnotes

13 Bell Gully’s Energy Practice

14 Bell Gully’s Energy team

ELECTRICITY INDUSTRY REPORT

W W W. B E L L G U L LY. C O M

1 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

An ambitious new target lies ahead for the electricity industry. The new Labour-led Government aims to

achieve 100% renewable energy by 20351 in a year of normal rainfall. It will charge the to-be-formed Climate Commission with planning that transition2, which builds on the country’s previous target of producing at least 90 per cent of electricity from renewable sources by 2025 in a year of average rainfall, providing supply security is maintained3.

But how realistic are these figures? Are they achievable?

It should be possible, at least, to get to 90 per cent. Political momentum favouring renewable energy is intersecting with the increasing emergence of new technologies such as the use of solar power and battery storage. These technologies are becoming economic. The roll-out of smart meters

100%

of electricity from renewable sources by 2035

AIM

in New Zealand is nearly complete. That means increased short-to-medium term opportunities for both business and individuals to produce some of their daily electricity needs to supplement their use of electricity from the national distribution system. Existing distribution networks may also be able to take advantage of large scale battery storage to augment the efficiency of their existing network. This potentially offsets the need to spend additional capital, and may result in cost and efficiency savings for consumers.

These factors mean New Zealand is uniquely placed over the next 10 to 20 years to have nearly all of its electricity produced from renewable energy sources in a normal rainfall year. New Zealand is in line to continue to build on its reputation as having a world leading electricity industry, an industry that in turn may prove critical to assisting New Zealand to achieve a low carbon future.

Introduction

2 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

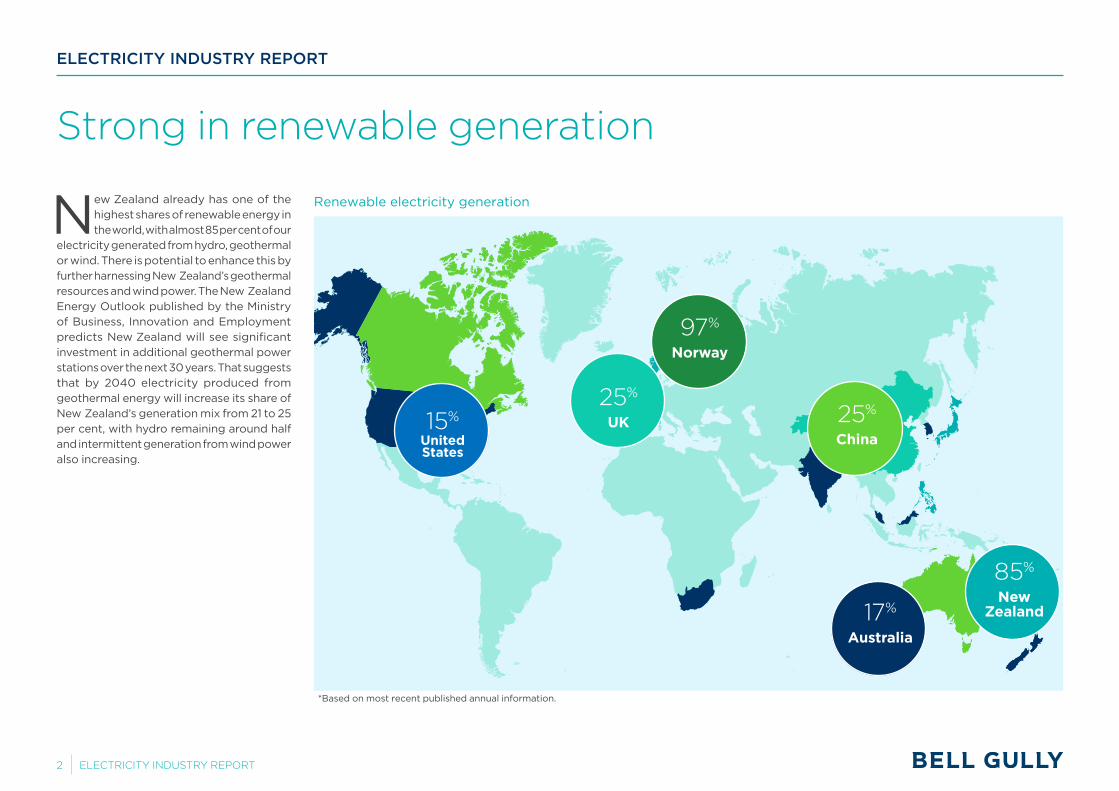

Strong in renewable generation

New Zealand already has one of the highest shares of renewable energy in the world, with almost 85 per cent of our

electricity generated from hydro, geothermal or wind. There is potential to enhance this by further harnessing New Zealand’s geothermal resources and wind power. The New Zealand Energy Outlook published by the Ministry of Business, Innovation and Employment predicts New Zealand will see significant investment in additional geothermal power stations over the next 30 years. That suggests that by 2040 electricity produced from geothermal energy will increase its share of New Zealand’s generation mix from 21 to 25 per cent, with hydro remaining around half and intermittent generation from wind power also increasing.

25%

UK15%

United States

97%

Norway

17%

Australia

85%

New Zealand

25%

China

*Based on most recent published annual information.

Renewable electricity generation

3 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

A low-carbon economy is a highly desirable goal for New Zealand. It would help to ensure New Zealand

remains an attractive place to live, work and invest. A well-functioning renewables-based electricity industry is not the only initiative driving New Zealand towards becoming a low carbon economy, but it is an important one. Others include:

• the strong emphasis by the new Government on climate change policies which will see New Zealand introduce a Zero Carbon Act, with a target of net zero carbon emissions by 2050,

• incremental enhancements to New Zealand’s Emissions Trading Scheme to incentivise all sectors of New Zealand’s economy (potentially including the agricultural sector) to reduce carbon emissions, and

• continued demand-side management of energy usage through energy efficiency programs in the transport sector, including by the switch to electric vehicles, and in the industrial heat sector, including converting coal-fired heating to natural gas and electric heating.

Together, these initiatives will work towards a low-carbon economy.

The key to the future

POLICY GOALS AND THE PRE-ELECTION MANIFESTOLabour’s election policy manifesto shows energy policies that are closely aligned with (and overlapping) its environmental policies. Planning for what is termed ‘the clean energy revolution and the just transition to a sustainable low-emissions economy’ is at the heart of this. Some of these policies have been confirmed in the agreements between parties that formed the Government.

The coalition agreement and supply and confidence agreement include plans to:

• Request the new independent Climate Commission to plan the transition to 100 per cent renewable electricity by 2035 (which includes geothermal) in a normal rainfall year.

• Undertake a full review of retail electricity pricing.

• Ensure the government’s vehicle fleet where practicable, becomes emissions-free by 2025/26.

Labour’s pre-election manifesto says it will:

• Ensure that at least 90 per cent of electricity being generated from renewable sources by 2025 with close to 100 per cent being renewably generated by 2040 (while recognising some geothermal backup may be necessary to meet peak seasonal demand, especially in dry years that affect hydro).

• Ensure a coherent plan to manage and maximise the benefits of disruptive energy technologies, and convening a cross-agency and cross-interest working group to undertake a wide-ranging review of the electricity sector.

• Add climate change mitigation and emissions reduction to the objectives of the Electricity Authority, in order to promote an increased uptake of renewable electric and, as part of the cross-sector review, determine whether responsibility for an overarching transitional plan should be placed with the Electricity Authority, as the regulator of the overall electricity system.

• Ensure that assessment of any new generation plant or energy infrastructure includes all environmental costs involved.

• Reinstate a moratorium on any new fossil-fuelled baseload electricity generation until 2028.

• Work in partnership with rural communities, distributors and generators to identify and promote opportunities for localised alternative sources of electricity generation.

• Ensure that households and other distributed generators can be grid-connected at a fair rate, and sell surplus electricity back into the power grid at a fair price (linked to the wholesale price).

• Investigate and develop new electricity system structures that can deal with higher proportions of variable renewable energy from sources such as wind and solar power.

• Work with the electric vehicle industry to encourage the uptake of electric vehicles and the provision of charging infrastructure.

• Promote energy efficiency initiatives, including through EECA.

• Promote the use of smart grids and meters to empower consumers to best manage their electricity requirements.

• Promote clean industrial heat and a move away from the use of thermal coal.

• Encourage the use of biomass as a way of making industrial heat.

• Review the low user tariff to ensure it, or an alternative, addresses energy poverty.

4 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

Are regulations fit for purpose?

Between the vision and the reality of a low carbon future stands a robust discussion. Do the current regulatory

settings for the electricity industry remain fit for purpose as new technologies emerge? Or are new regulations needed to enhance the use and take-up of new technologies which will play a significant role in a low-carbon economy, while preserving the essential functioning of an industry vital to the nation’s economic health?

During the election Labour proposed the development of a coherent plan to manage and maximise the benefits of the transformation that disruptive energy technologies will bring. Labour proposed a cross-agency and cross-interest working group to undertake a wide ranging review of the electricity sector and address issues including:

Electricity Authority consultation on mass participation

Any such review would dovetail well with the recent consultation undertaken by the Electricity Authority on whether the current regulatory settings for the electricity industry remain fit for purpose. Is the electricity industry responding to the opportunities created by new technologies and business models, and in turn the possibility of increased competition? The Electricity Authority calls the new development “mass participation” in the electricity market and expects it to result in a change to the decades-old electricity supply model with large scale and specialised electricity businesses.

• the optimal role

for the electricity

sector in making

a just transition

to a low-carbon

economy

• whether in achieving

this, any changes need

to be made to current

electricity industry

arrangements, or any

policy inconsistencies

across the wider

economy addressed

• any barriers that

currently exist to

improving energy

productivity

• whether responsibility

for an overarching

transitional plan should

be placed with the

Electricity Authority,

as the regulator of

the overall electricity

system

• regulatory and

equity issues

arising from the

impact of the new

technologies

5 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

Structuring the electricity industry

Industry’s strong interest in the potential for reform is reflected in the 39 submissions received during the “enabling mass

participation” consultation. Electricity companies, major users and other interested stakeholders put significant effort into providing their submissions. That’s no surprise. Significant structural issues are at stake, including:

• whether the distribution companies should be able to participate in technology such as offering solar power and battery storage, without ring-fencing this consumer-facing business from their core electricity distribution network business,

• the potential for the introduction of further liquidity into the wholesale electricity hedge market,

• whether a ‘level-playing field’ exists to best enable the take-up of new technology, and

• the basis on which customer data can be accessed by industry participants.

In November, the Electricity Authority released its summary of submissions and revised work plan. A number of themes emerged. One was the need for a ‘level playing field’ for entry into, and participation in, the electricity industry. Some submitters highlighted the current division between

network monopoly services and contestable services as a hurdle in favour of network distribution companies, while an alternative view was put forward by network distribution companies, who see themselves as legitimate participants in emerging contestable markets. Other submissions included the need for the Electricity Authority and the Commerce Commission to work together to ensure a consistent regulatory framework for the industry to support a ‘level playing field’ and access to the network support markets. Participants also highlighted the desirability of a process of consumer authorisation for releasing smart meter data to third parties. Details can be accessed here.

The drive to ensure future-fit regulation is ongoing. The Electricity Authority is currently consulting on the significance of barriers to ‘multiple trading relationships’, hurdles that hinder consumers’ ability to use electricity or electricity services provided by more than one party at the same time, at the same location. That consultation is open until 5pm on 27 February 2018. The consultation paper and submission form can be accessed here.

Following its consultation on enabling mass participation in the electricity industry, the Electricity Authority has also recently put in place a new ‘equal access framework’ project through which it seeks to ensure current open access arrangements to facilitate equal access and provide confidence to

parties accessing New Zealand’s electricity networks. An overview of the project can be found here.

A review of retail pricing

The coalition agreement between Labour and the New Zealand First Party commits the Government to a review of retail pricing in the electricity sector.

A combined review

We believe it would make sense to link this to the results of the Electricity Authority’s consultation on mass participation and any potential cross sector review, rather than having separate reviews. These are complex issues and they tend to interrelate. It is desirable to have a single, holistic review, framed around what is needed to deliver a world-leading industry, with the best interests of business and retail consumers at its heart.

GENERATION

SMART METERSHEDGING

LINE NETWORKS

DISTRIBUTION

6 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

An opportunity to look forward

1987• Corporatisation of ECNZ

1996• Establishment

of wholesale electricity market

1993• Electricity Act

1992 enacted

2008• Introduction of price, quality

regulation of non-community owned line network companies

1994-1999• Separation of ECNZ into generator retailers:

Meridian, Contact, Mercury, Genesis

1998-1999• Bradford reforms = split

of generation / retail from lines companies

2010• Enactment of Electricity

Act 2010• Development of industry

rule book - Electricity Participants Code

The current structure of the electricity industry has served New Zealand well for the last 30 years. The International

Energy Agency’s 2017 review of New Zealand’s energy policies stated that “New Zealand is a world leading example of a well-functioning electricity market which continues to work effectively”.

In this time, we have seen the corporatisation of the local power boards, the separation and corporatisation of the Electricity Corporation of New Zealand (ECNZ) into the now majority state owned generator retailers, the establishment of the wholesale electricity market, the split of generation and retail from lines networks (known as the

Bradford reforms), the introduction of price and quality regulation of non-community owned line network companies, the enactment of the Electricity Industry Act in 2010 (which liberalised the Bradford reforms to a significant extent) and the development of the industry rulebook in the form of the Electricity Industry Participation Code 2010.

The Electricity Authority and many of the submitters agree it is time to review the structure of the industry to account for the benefits and potential new challenges of new technologies. Many also agree the review must encompass whether the industry structure remains fit-for-purpose.

7 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

The law of unintended consequences

The Government, the Electricity Authority and the industry need to determine the optimal structure to

take the sector forward for the next 20 plus years. The industry is complex, yet there are justifiable reasons for this complexity. Billions of dollars of investment has been made by stakeholders. There is a physical component which requires the supply of available generation and demand for electricity usage to be in constant balance. Security of supply remains critical and New Zealand must retain backup of gas-fired peaking plants to ensure New Zealanders have a secure supply of electricity in periods of low rainfall affecting hydro lakes. New technologies have the potential to significantly change the way electricity is supplied, transmitted and consumed in New Zealand.

If any change to the industry and its current structure is proposed, it will be important to keep in mind the law of unintended consequences. Any change to the industry will need to be carefully examined so that any changes don’t unintentionally restrict the positive growth and development of the industry in the interests of consumers.

Changes will require detailed economic, regulatory, commercial and policy review.

New regulatory settings will also need to address the blurring of the traditional divide between monopoly network services and generation/retail activities. For example, a battery can be embedded on a distribution network to improve network resilience, but also to provide peak supply. Regulations will need to ensure a level playing field between market participants, allow for competition for the provision of such services where possible and drive efficient investment.

The starting point for any review should be the best interests of business and household consumers. Consumers must continue to have security of supply at a reasonable price, as well as access to the new technologies and services that are and will become available in the industry. Coupled with this, the regulatory settings should allow any investor who wishes to provide new technology the ability to do so without any structural impediment: a level playing field. Ideally, a combined Government and Electricity Authority review would also examine whether any simplification can be made to the industry.

NEXT 20 YEARS

8 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

New technologies, new services

There is good potential to also utilise new technology such as solar, bio energy and marine energy for future renewable

electricity generation sources and direct heat production. The current New Zealand Energy Strategy 2011 – 2021 (NZES) recognises that New Zealand is in a good position to trial, develop and integrate new technologies and be at the forefront of potentially far reaching electricity system development in the 21st century.

The stated goal is a responsive and future-focused electricity industry taking advantage of new technology opportunities and welcoming new investors. It wants the electricity system to take advantage of new smart technologies to promote energy conservation to consumers and to improve energy efficiency. The availability of a number of new and innovative offerings in solar power and battery storage to consumers in New Zealand, as set out in this section, show the sector’s readiness to step forward.

Maintaining security of supplyTargets for renewable energy must be set against the need to retain security of electricity supply. This is critical to the life blood of the economy and the functioning of households. The sector needs to maintain strong use of gas-fired generation in the mix, in particular through peaking plants which can be brought on to the electricity system quickly in times of low rainfall into the hydro lakes.

9 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

New technologies, new services

New technologies have the potential to change fundamental aspects of New Zealand’s electricity industry.

They will offer consumers many new options for generating and storing energy for their homes and businesses, and choices over how and when they buy their power. They have the potential to allow consumers to sell electricity back to the grid directly or through peer-to-peer buying and selling platforms. Battery storage may allow energy generated from solar power during the day to be stored for night time use, which in turn offers line network owners support for grid availability and reliability without the spending usually required to provide that support. A number of New Zealand’s leading energy companies are trialling solar and battery storage initiatives.

As solar power systems have become increasingly affordable, a wide range of solar panel providers have emerged including Solar King, Vector, PowerSmart, solarcity and Harrisons Energy. They offer a variety of deals which range from full installation and ownership (with some companies such as Vector also providing mechanisms for consumers to spread purchase costs over time), to supply only packages for self-installation. Meridian offers a solar buyback rate for excess energy that members generate9 while Contact offers customers a distributed generation meter if their local Network company approves a connection, with the opportunity to sell excess energy back to Contact10. Some solar providers offer long-term service agreements to consumers for the provision of solar energy systems and services.

Solar powered systems

There has been a rapid emergence to the market of smart technologies aimed at helping consumers better manage their energy usage and efficiency. StorEdge™ and SolarEdge are two of the ‘Smart Monitoring’ systems provided by Harrisons Energy Solutions, which provide users with real-time alerts about system performance via a cloud-based monitoring system4. Genesis Energy has recently announced its ‘Genesis Energy Mobile App’ which allows its customers to view a breakdown of their power usage, compare their usage to similar households and allows them to obtain estimates of future power bills5. Mercury is providing ‘plugged-in’ electric vehicle owners who are also their residential customers with a fuel package that enables them to save 20 per cent when they charge their car overnight6. Meridian offers electric vehicle owners low overnight charging rates and free charging stations7. Australian energy retailer Origin Energy has also recently announced a “sales trial” of its smart home kit, Home HQ, which seeks to help provide consumers with greater visibility over their energy consumption. Using the Home HQ mobile app, consumers will be able to control smart devices remotely, including checking if appliances are switched on or off or setting alerts for when motion is undetected in a household8. Coupled with developing energy storage solutions, the introduction and uptake of smart technologies will allow consumers to use energy more efficiently, maximise self-consumption and will have the capacity to transform energy use.

Smart technologies

10 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

New technologies, new services

Batteries allow consumers to use energy when and how they want to, maximising savings on power bills. Rather than sending electricity back to the grid and receiving a low cost per kilowatt hour (kWh), consumers can store surplus electricity generated during the day and use it to power their homes during the evening or when their solar power system can’t meet demand. Most solar power installers also offer battery installation. Solar storage batteries currently available in New Zealand include the sonnenBatterie, the LG Chem RESU, the Tesla Powerwall, the SolaXBox and the Enphase AC battery11. Vector is a New Zealand stockist of the Tesla Powerwall 2 Battery, which has the capacity to power an average two-bedroom home for a full day and can be used as a backup power source for some appliances in homes or small businesses12.

The improving capabilities and falling costs of batteries means it will become more feasible for consumers to self supply their electricity needs, and for other parties to provide aspects of the network service. Batteries can be used to provide network support by discharging generated electricity into the network at times of high demand. Importantly, control of the battery in this instance does not need to rest with the distributor. Anyone can own and control a battery that is being used to help support network reliability13. These sorts of models reflect the fundamental change in the industry the Electricity Authority has recently highlighted in its 28 November 2017 Consultation Paper ‘Multiple Trading Relationships’. That says there is a move to a more dispersed model that is driven by technology and new business models, and which challenges the assumption that consumers want or need a single retailer14.

BatteriesPeer-to-peer platforms

Solarcity’s solarZero® enables consumers to power 100 per cent of their home’s electricity needs without buying a solar power system. Consumers pay a fixed, monthly fee for a 20-year period that provides them with solar power and energy efficient services. The solarZero® buyback guarantee ensures the rate consumers pay to buy energy off the grid (not including network charges or GST) matches what they get paid for any surplus solar energy generated by their solar system that is fed back into the grid.

Solar services: a case study

Peer-to-peer platforms enable households and businesses to directly trade power from solar panels and battery storage with one another. A domestic example is P2 Power, a peer-to-peer energy provider service through SolarShare™, available to consumers connected to the Vector network. P2 Power enables local buyers to directly purchase excess power from others in their community through a service which matches buyers and sellers every half hour. Traditional grid power is only used when there is not enough local power to meet consumer demand. During summer P2 Power has also guaranteed to buyers that at least 7 per cent of their power usage will be charged at the then-prevailing ‘P2P’ rate15. Australian blockchain energy technology firm Power Ledger has also recently completed its trial of its peer-to-peer trading platform with Vector in New Zealand16.

11 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

New Zealand ENERGY EFFICIENCY AND

CONSERVATION STRATEGY 2017-2022

THE UNITED NATIONS FRAMEWORK CONVENTION ON CLIMATE CHANGE

From climate change to renewable energy

THE KYOTO PROTOCOL

(ratified December 2002)

NEW ZEALAND ENERGY STRATEGY 2011-2021 (NZES)

ELECTRICITY Innovative and efficient use of electricityTARGET 90% electricity will be generated from renewable sources by 2025

TRANSPORT Efficient and low-emissionsTARGET Electric vehicles make up 2% of the vehicle fleet by the end of 2021

PROCESS HEAT Renewable and efficient useTARGET Decrease in industrial emissions intensity of at least 1% per annum on average between 2017-2022

New Zealand EMISSIONS TRADING SCHEME (NZETS)

THE PARIS AGREEMENT

(ratified 4 October 2016, taking effect from 2020)

ENERGY EFFICIENCY AND CONSERVATION ACT 2000

The renewable energy target the industry must work towards is inextricably linked to New Zealand’s response to

climate change.

The policy establishing this target starts at the international level, with New Zealand’s ratification of the Paris Agreement on climate change. Nationally, the Government’s overarching energy policy is the New Zealand

Energy Strategy. The 90 per cent renewable energy target is included in this as well as the New Zealand Energy Efficiency and Conservation Strategy 2017-2022. Complementing these policy objectives is the

Emissions Trading Scheme, which incentivises industries to reduce carbon emissions. This may soon be allied with a Zero Carbon Act, setting a target of net zero carbon emissions by 2050, with associated mechanisms to achieve this target.

INTERNATIONAL NATIONAL

12 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

1 National Statement from New Zealand to 23rd Conference of the Parties to the UNFCCC (17 November 2017) https://www.beehive.govt.nz/speech/national-statement-new-zealand-23rd-conference-parties-unfccc

2 Confidence and Supply agreement between New Zealand Labour Party and the Green Party of Aotearoa New Zealand (24 October 2017) https://d3n8a8pro7vhmx.cloudfront.net/nzlabour/pages/8637/attachments/original/1508818771/NZLP___GP_C_S_Agreement.pdf?1508818771

3 New Zealand Energy Strategy 2011–2021, page 25 (30 August 2011) https://www.mbie.govt.nz/info-services/sectors-industries/energy/documents-image-library/nz-energy-strategy-lr.pdf

4 https://www.harrisonsenergy.co.nz/solar/smart-monitoring 5 https://www.genesisenergy.co.nz/app 6 https://www.mercury.co.nz/Products/electric-vehicles

7 https://www.meridianenergy.co.nz/your-home/sustainability/electric-cars-vehicles

8 https://originhomehq.com.au/

9 https://www.meridianenergy.co.nz/your-home/pricing-and-rates/solar-buy-back-rate

10 https://contact.co.nz/residential/electricity/electricity/alternative-energy

11 https://www.mysolarquotes.co.nz/about-solar-power/residential/solar-battery-storage---product-comparison/

12 https://www.vector.co.nz/personal/batteries

13 ‘Enabling mass participation in the electricity market: How can we promote innovation and participation?’ Electricity Authority Consultation Paper (30 May 17) https://www.ea.govt.nz/development/work-programme/evolving-tech-business/enabling-mass-participation/

14 ‘Multiple Trading relations: How can consumers choose multiple electricity providers?’ Electricity Authority Consultation Paper (28 November 2017) https://www.ea.govt.nz/development/work-programme/evolving-tech-business/multiple-trading-relationships/consultations/#c16922

15 https://p2power.co.nz/#pricing

16 https://renewablesnow.com/news/interview-power-ledger-sees-infinite-opportunities-for-blockchain-enabled-energy-trading-590633/

Endnotes

13 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

Bell Gully’s Energy Practice

New Zealand. Our energy team is consistently recognised in the top tier by leading legal directories. We have a detailed knowledge and understanding of the energy sector and the legal issues that are relevant to it.

The energy team works closely with our climate change experts.

Our team incorporates:

• Specialist energy sector expertise, transactional and advisory experience based on extensive work in the sector over many years.

Bell Gully has been an active advisor to the energy sector over the last 30 years. During this time, Bell Gully has worked on some of the most significant projects and transactions in New Zealand’s energy sector. Our energy practice comprises lawyers with specialist expertise in corporate, commercial, litigation, regulatory, and environmental matters. This group of lawyers acts for electricity generators, retailers and line network companies, a number of major industry participants in the oil and gas transmission and upstream mining sectors, and for large industrial market participants operating in

• The market-leading corporate team undertaking M&A and other corporate and commercial transactions for a wide range of industry participants, and providing market-leading advice on energy projects and overseas investment issues.

• Particular expertise and experience in regulatory work, investigations and prosecutions in the energy sector, including high hazard industries.

• A property team with full environmental, resource management, land purchase, sale and access and construction capability.

• A litigation team with extensive experience in energy sector disputes, and a proven ability to win complex and high profile cases.

• A leading tax team.

• Recognised climate change experts.

14 | ELECTRICITY INDUSTRY REPORT

ELECTRICITY INDUSTRY REPORT

Bell Gully’s Energy team

Andrew BeatsonPARTNER

DDI +64 9 916 8754 MOB +64 21 223 9170

Jane HollandPARTNER

DDI +64 9 916 8983 MOB +64 21 706 129

For further information, please contact our Energy team or your usual Bell Gully adviser:

If you have any questions about this report, please contact the author:

David CoullPARTNER

DDI +64 4 915 6863 MOB +64 21 800 308

Chris GordonPARTNER AND CHAIR

DDI +64 4 915 6836 MOB +64 21 614 522

Glenn ShewanSENIOR ASSOCIATE

DDI +64 9 916 8726 MOB +64 21 828 926

Garry DownsPARTNER

DDI +64 9 916 8932 MOB +64 21 761 601

Amon NunnsPARTNER

DDI +64 4 915 6741 MOB +64 21 687 368

Angela HarfordSENIOR ASSOCIATE

DDI +64 4 915 6764 MOB +64 21 875 905

David McPhersonPARTNER

DDI +64 9 916 8988 MOB +64 21 621 623

Natasha GarvanSENIOR ASSOCIATE

DDI +64 9 916 8956 MOB +64 27 420 0561

W W W. B E L L G U L LY. C O M

Disclaimer: This publication is necessarily

brief and general in nature. You should seek

professional advice before taking any further

action in relation to the matters dealt with

in this publication. The views expressed are

our own. No client views are represented in

this publication.

All rights reserved © Bell Gully 2017

WELLINGTON

ANZ CENTRE171 FEATHERSTON STREETNEW ZEALAND

AUCKLAND

VERO CENTRE48 SHORTLAND STREETNEW ZEALAND