edible oil - pacra research - jan'21

TRANSCRIPT

Edible OilAn Overview

February 2021© The Pakistan Credit Rating Agency Limited1

TABLE OF CONTENTS

Contents Page No.

Snapshot 1

Process Flow 2

Global Oil Seed 3

Edible Oil |Global 5

Global Price Dynamics 7

Domestic Overview 8

Domestic | Supply Side 9

Domestic |Demand Side 11

Domestic | Price Dynamics 12

Business Risk 13

Financial Risk 15

Duty Structure 16

Contents Page No.Rating Curve 17

SWOT Analysis 18

Conclusion / Outlook 19

Snapshot

EDIBLE OIL | OVERVIEW

Source: USDA, WB

Edible Oil is one of the essential items for cooking and food preparation. The product is being consumed by almost all classes of society, although per capita consumption patterns vary across the globe.

Edible oil can be obtained from a number of vegetables. The most commonly used edible oil products are soybean oil, palm oil,sunflower oil and rapeseed oil.

USA is the largest producer of soybean seeds in the world whereas Malaysia and Indonesia are largest exporter of Palm oil whereas India is the largest importer of edible oil.

Parameters FY19 FY20Turnover – Global (USD bln) 150 163

Turnover – Domestic (PKR bln) 1,025 1,229

Turnover per Capita – Global (USD) 19.7 21.2

Turnover per Capita‐ Domestic (PKR) 4,726 5,586

Share in GDP‐ Global 0.17% 0.19%

Share to GDP‐ Domestic (Nominal) 2.6% 2.9%

Growth Rate (Annual) – Global 1% 9%

Growth Rate (Annual) – Domestic 12% 22%

1

EDIBLE OIL| PROCESS FLOW

Refined Bulk Edible Oil

Seed Extraction Oil Refinery

Branded Oil

Oil Seeds

Process Flow

Source: PACRA Internal Database 2

Consumer

Packing UnitPoultry Feed

Production of Oil seeds

EDIBLE OIL | GLOBAL

Source: USDA, PACRA Internal Database

Global Oil seeds production was recorded at 576mln MTs during FY20 down by 3% YoY (FY19: 597mln MTs). A decline of almost ~18%YoY in USA crops led to drop in global production in FY20. This decline was majorly owed to supply chain disruptions being caused bythe Covid‐19 lockdown and high opening inventory levels in the USA.

During FY21, global oil seed production is estimated to be 596mln MTs, YoY growth of 3%. USA production is expected to reach 124mlnMTs from a historical low production of 107mln MTs in FY20, expecting a growth of 16% YoY.

3

0

20

40

60

80

100

120

140

160

180

200

FY16 FY17 FY18 FY19 FY20

Country wise Production (MMT)

United States Brazil Argentina China India Other

0

50

100

150

200

250

300

350

400

FY16 FY17 FY18 FY19 FY20

Oil Seed Production (MMT)

Soybean Seed Rapeseed Sunflower Seed Cottonseed Palm Kernel Others

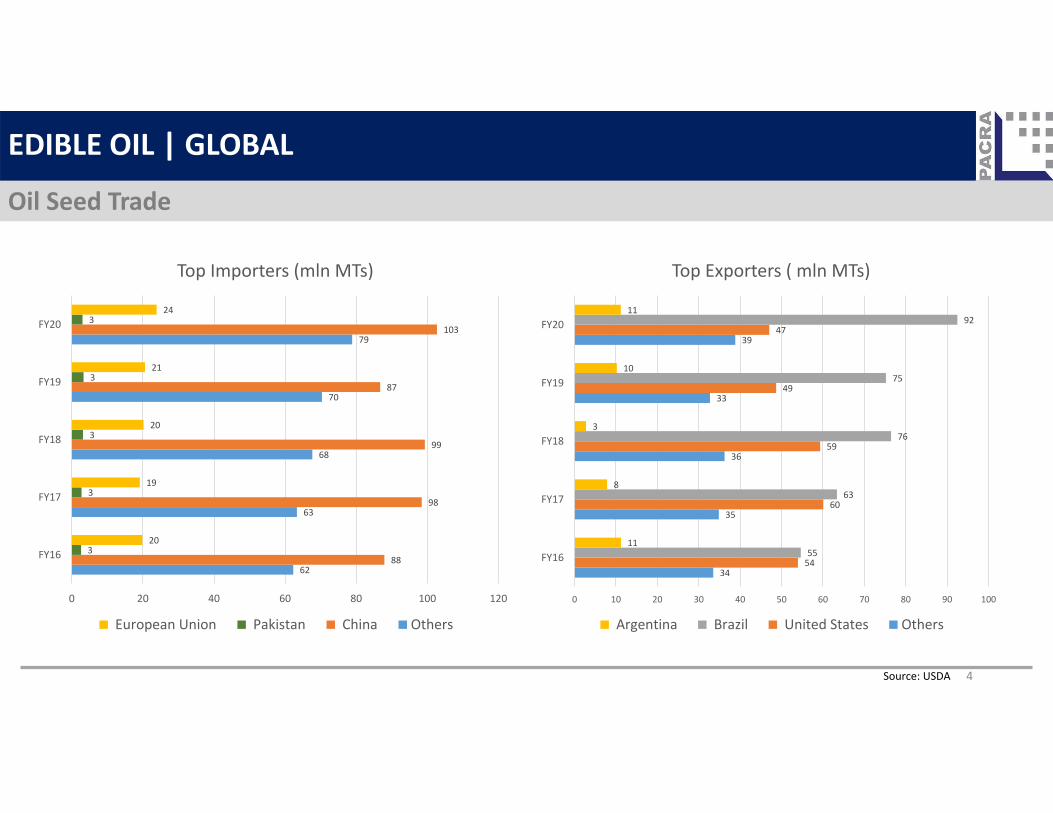

Oil Seed Trade

EDIBLE OIL | GLOBAL

Source: USDA 4

62

63

68

70

79

88

98

99

87

103

3

3

3

3

3

20

19

20

21

24

0 20 40 60 80 100 120

FY16

FY17

FY18

FY19

FY20

Top Importers (mln MTs)

European Union Pakistan China Others

34

35

36

33

39

54

60

59

49

47

55

63

76

75

92

11

8

3

10

11

0 10 20 30 40 50 60 70 80 90 100

FY16

FY17

FY18

FY19

FY20

Top Exporters ( mln MTs)

Argentina Brazil United States Others

Global Oil Production

EDIBLE OIL | GLOBAL

Global oil production was recorded at 207mln MTs during FY20 – a YoY growth of 2% (FY19: 203mln MTs).

Palm oil has the largest share in global oil production.

Growth in global oil production is expect to remain flat, going forward.

Source: USDA 5

0

10

20

30

40

50

60

70

80

FY17 FY18 FY19 FY20

Variant wise Oil Production (MMT)

Palm Oil Soybean Oil Rapeseed Oil Others

0

20

40

60

80

100

120

FY17 FY18 FY19 FY20

Country wise Oil Production (MMT)

China United States Malaysia Indonesia Others

Oil Trade

EDIBLE OIL | GLOBAL

Source: USDA 6

35

38

38

40

38

15

15

14

16

14

10

11

11

12

12

3

3

3

3

3

0 5 10 15 20 25 30 35 40 45

FY16

FY17

FY18

FY19

FY20

Top Importer (mln MTs)

Pakistan European Union China India Others

26

28

27

28

32

25

30

29

32

29

18

17

18

20

19

5

6

6

7

7

0 5 10 15 20 25 30 35

FY16

FY17

FY18

FY19

FY20

Top Exporters ( mln MTs)

Ukraine Malaysia Indonesia Others

Price Dynamics

EDIBLE OIL | GLOBAL

Prices of edible oil during FY19 were at their lowest in several years, a reflection of the slowdown in global demand for oils and proteinmeals, as well as the uncertainties stemming from US‐China trade disputes.

Since Dec‐2020 the price of Soyabean oil increased by 12%. Prices continued to rise post covid‐19 lockdown amid supply uncertaintiesand historically low global inventory levels.

7

22

2323

23

20

18

19

20

21

22

23

24

FY16 FY17 FY18 FY19 FY20

Closing Inventory Oil (mln MTs)

Source: USDA, PACRA Internal database

‐ 200 400 600 800

1,000 1,200 1,400

FY16 FY17 FY18 FY19 FY20

Price Trend (US$/MT)

Soybean Oil Sunseed Oil Palm Oil Rapeseed Oil

An Overview

EDIBLE OIL | DOMESTIC

• Pakistan’s edible oil market was recorded at PKR 1,161 million in FY20 registering a YoY growth of 22% (FY19: PKR~950 million).

• Local consumption was recorded at ~4.9mln MTs in FY20 up ~3% YoY, as (FY19: ~4.7mln MTs). This reflects that the growth in revenue was majorly contributed by a spike in prices. Average price of edible oil during FY20 was recorded at PKR~238/kg as compared to PKR~201/kg during FY19 (YoY Growth: 19%).

• With a per capita consumption of 22kg, Pakistan is the world’s 8th largest consumer of edible oil.

• The sector is highly dependent on imported oil seeds and refined palm oil to meet the local demand. Hence the exposure to exchange rate and International price fluctuations is high.

Source: USDA, WB, IMF 8

FY18 FY19 FY20

Turnover ( PKR bln)

845 950 1,161

Growth Rate 1.91% 12.47% 22.13%

Turnover Per Capita (PKR) 3,985 4,379 5,275

Share to GDP 2.46% 2.46% 2.78%

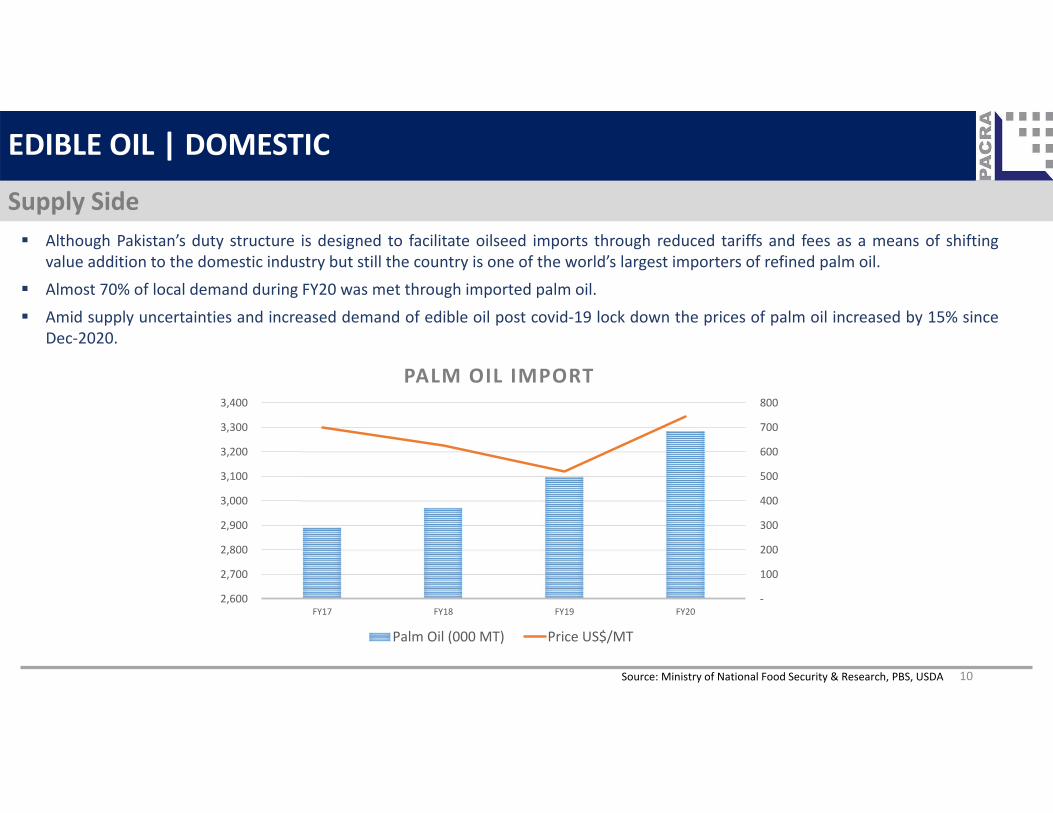

Supply Side

EDIBLE OIL | DOMESTIC

Source: Ministry of National Food Security & Research, PBS, USDA

Local edible oil demand is met through both crushing of oil seeds and import of cooking oil.

Local industry relies entirely on imports to meet its demand of soybean seed whereas cottonseed demand is met through localproduce only. Meanwhile, rapeseed and sunflower seeds are both produced locally as well as imported.

9

3,31

8

3,55

2

3,29

2

2,90

0

200

225

346

410

75

90

144

145

2 2 2 2

FY17 FY18 FY19 FY20

PRODUCTION (000MT)

Cottonseed Rapeseed Sunflower seed Soybean seed

1,60

0

2,17

9

1,99

7

1,70

4

1,18

0

821 907

781

102

41

‐ ‐

FY17 FY18 FY19 FY20

IMPORT (000MT)

Soybean seed Rapeseed Sunflower seed

Supply Side

EDIBLE OIL | DOMESTIC

Source: Ministry of National Food Security & Research, PBS, USDA

Although Pakistan’s duty structure is designed to facilitate oilseed imports through reduced tariffs and fees as a means of shiftingvalue addition to the domestic industry but still the country is one of the world’s largest importers of refined palm oil.

Almost 70% of local demand during FY20 was met through imported palm oil.

Amid supply uncertainties and increased demand of edible oil post covid‐19 lock down the prices of palm oil increased by 15% sinceDec‐2020.

10

‐

100

200

300

400

500

600

700

800

2,600

2,700

2,800

2,900

3,000

3,100

3,200

3,300

3,400

FY17 FY18 FY19 FY20

PALM OIL IMPORT

Palm Oil (000 MT) Price US$/MT

Demand Side

EDIBLE OIL | DOMESTIC

Being the essential food item the demand of edible oil always remains robust.

During FY20 the local consumption of edible oil was recorded at 4.871 MMT up 3% YOY. Palm oil has largest share in overall edible oilconsumption followed by soybean oil, rapeseed oil and sunflower oil.

The demand of the edible oil is expected to remain robust and expected to increase more in coming Ramzan month.

11

3,070 3,095 3,245 3,390

470 485 490 480

471 374 472 491 445 480 470 450

‐ 500

1,000 1,500 2,000 2,500 3,000 3,500 4,000

FY17 FY18 FY19 FY20

Edible Oil Consumption (000 MT)

Palm Oil Soybean Oil Canola Oil Cottonseed Oil Sunflower Oil

Source: Ministry of National Food Security & Research, PBS, USDA

Price Dynamics

EDIBLE OIL | DOMESTIC

Source: USDA, PBS.

Pakistan is heavily dependent on import of oil seed and edibleoil to meet local consumption.

Further the exposure to exchange rate movement is also high.

It is the market norm to pass in entirety the impact of increasedcost of purchase to end consumers.

International stock of edible oil and oil seed is at historically lowlevel. Amid tight supplies, the prices of imported edible oil arealso expected to increase further and hence the local prices ofthe products.

Further, demand side push to prices is expected from anincrease in demand due to eased lockdown and upcomingmonth of Ramazan.

12

189201

238 258

2%

7%

19%

8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

50

100

150

200

250

300

FY18 FY19 FY20 6MFY21

Price Dynamics

Price (PKR/kg) Change

EDIBLE OIL | DOMESTIC

Business Risk | Demand Side

Source: PACRA Internal database

The business risk of edible oil sector can be divided into operating risk and sales risk.

Operating Risk: This risk particularly refers to the difficulties relating to the operations of the edible oil playerswhich can hamper the profitability and performance of the sector. Major inputs include both local inputs andimported inputs although the proportion of local input is significantly low. The sector’s costs are therefore subjectto Exchange Rate volatility and International prices of oil seed and refined oil. Although tariff structure of thecountry is designed in way to promote local production of edible oil but still the major portion of demand is metthrough import of refined oil.

. Sales Risk: This risk is focused on the demand side of edible oil. Being the essential food item demand of edible oil

remains robust. But the slight variation in demand is related to price movement as well. As the customer switchedfrom branded edible oil to low cost products.

13

EDIBLE OIL | DOMESTIC

14

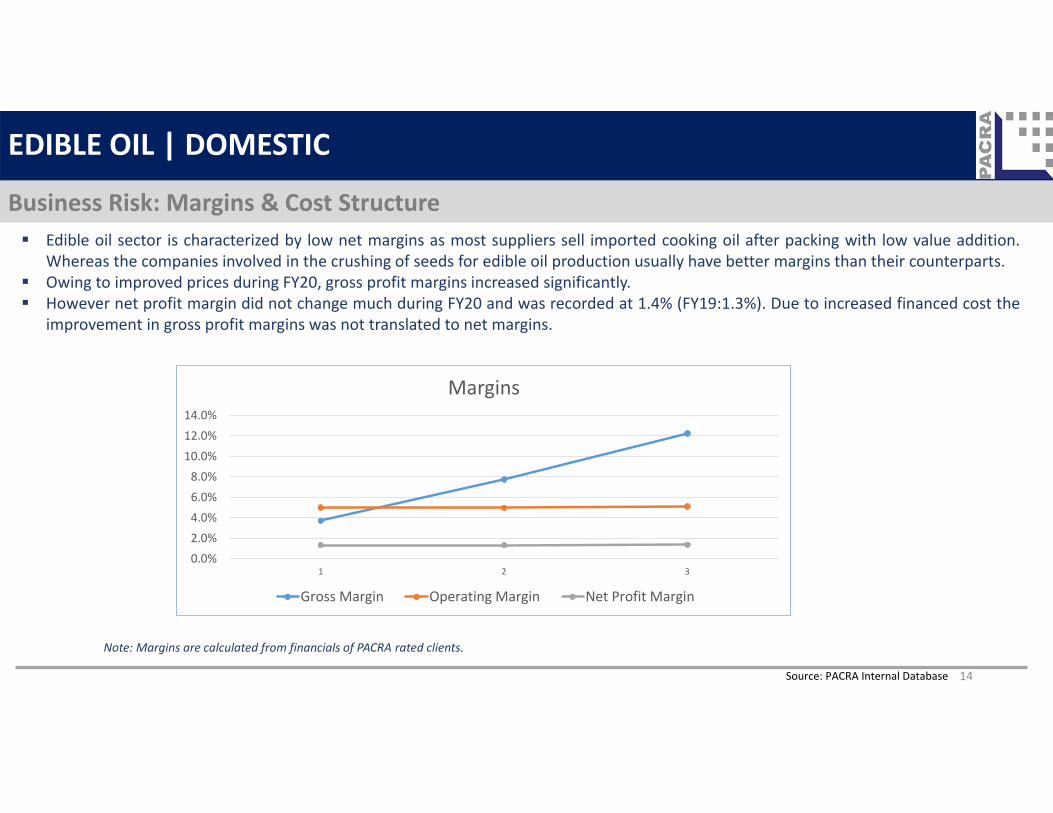

Business Risk: Margins & Cost Structure

Source: PACRA Internal Database

Edible oil sector is characterized by low net margins as most suppliers sell imported cooking oil after packing with low value addition.Whereas the companies involved in the crushing of seeds for edible oil production usually have better margins than their counterparts.

Owing to improved prices during FY20, gross profit margins increased significantly. However net profit margin did not change much during FY20 and was recorded at 1.4% (FY19:1.3%). Due to increased financed cost the

improvement in gross profit margins was not translated to net margins.

Note: Margins are calculated from financials of PACRA rated clients.

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%

1 2 3

Margins

Gross Margin Operating Margin Net Profit Margin

EDIBLE OIL | DOMESTIC

Financial Risk Net working capital days of the sector increased due to increase in inventory days. The suppliers keeps considerable inventory levels to

support demand during lead time required to import inputs. The need to maintain back up stock increased during FY20 owing to supplychain destructions caused by covid‐19 lockdown. As mentioned in below graph the working capital need of the sector are high owing tolow payable days.

To finance the working capital needs, the companies resorts to short term borrowing as the short term borrowing constitute 98% of thetotal outstanding debt. High reliance on short term financing is a depiction of aggressive working capital policy which increases therepayment risk. Gearing ratio of the sector was recorded at 54% during FY20 (FY19:64%).

Source: PACRA Internal Database 15

‐

50.00

100.00

150.00

200.00

FY18 FY19 FY20

Working Capital

Inventory Days Trade Receivable Days

Trade Payable Days Net Working Capital Days

95% 96% 98%5% 4% 2%

50%

60%

70%

80%

90%

100%

FY18 FY19 FY20

Debt Structure

Short Term Borrowing Long Term Borrowing

Note: Margins are calculated from financials of PACRA rated clients.

EDIBLE OIL | DOMESTIC

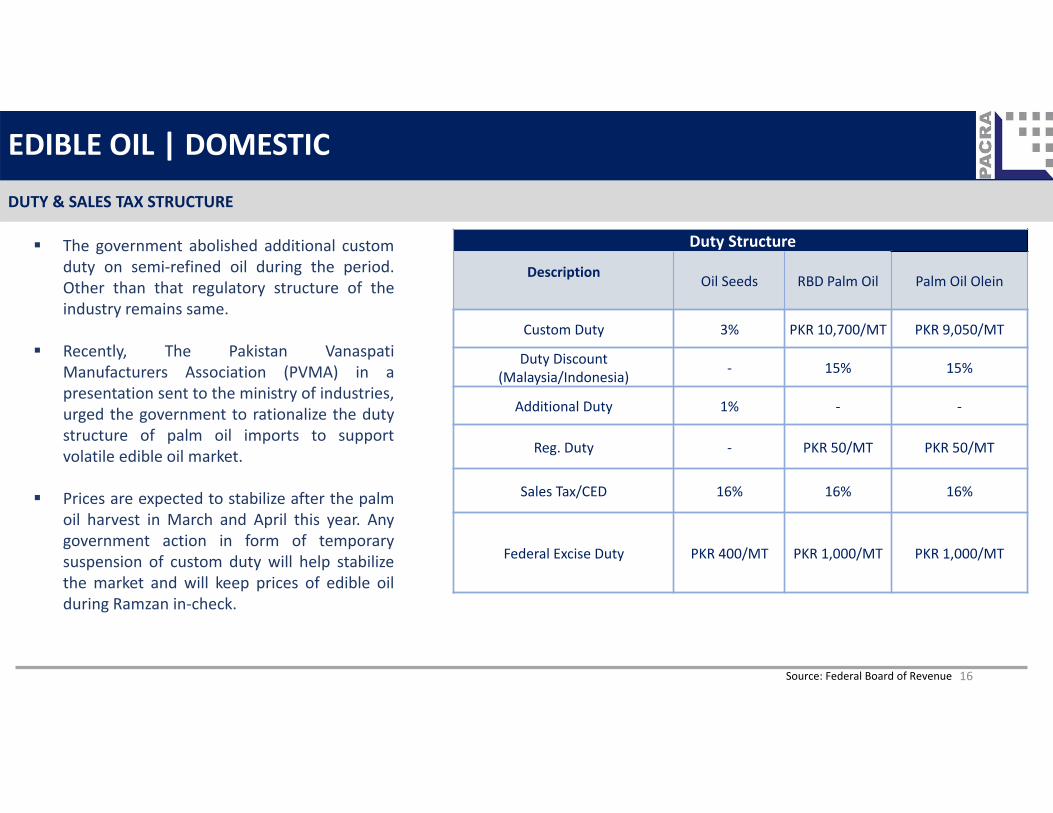

DUTY & SALES TAX STRUCTURE

Source: Federal Board of Revenue 16

Duty Structure

Description Oil Seeds RBD Palm Oil Palm Oil Olein

Custom Duty 3% PKR 10,700/MT PKR 9,050/MT

Duty Discount (Malaysia/Indonesia) ‐ 15% 15%

Additional Duty 1% ‐ ‐

Reg. Duty ‐ PKR 50/MT PKR 50/MT

Sales Tax/CED 16% 16% 16%

Federal Excise Duty PKR 400/MT PKR 1,000/MT PKR 1,000/MT

The government abolished additional customduty on semi‐refined oil during the period.Other than that regulatory structure of theindustry remains same.

Recently, The Pakistan VanaspatiManufacturers Association (PVMA) in apresentation sent to the ministry of industries,urged the government to rationalize the dutystructure of palm oil imports to supportvolatile edible oil market.

Prices are expected to stabilize after the palmoil harvest in March and April this year. Anygovernment action in form of temporarysuspension of custom duty will help stabilizethe market and will keep prices of edible oilduring Ramzan in‐check.

EDIBLE OIL | RATING CURVE

Source: PACRA Internal data

0

1

BBB+ BBB BBB‐

Ratings ‐ PACRA

PACRA rates two of the players ofpoultry sector ‐ Sadiq Poultry &Islamabad Farms.

No change has occurred in the ratingsof both of the players.

17

POULTRY | SWOT ANALYSIS

Increased research and development Economic recovery Increase income per capita Evolving consumer taste palette Change in eating habits No brand loyalty Vast distribution

Artificial breeding of broilers Lack of research and development

initiatives Outdated technology used for hatchery

and breeding Highly fragmented sector Perishable Items Prevailing uncertainty due to COVID‐19•High raw material costs• Low contribution margins•High waste production levels

Continuous availability of raw material and labor Reduction of policy rate Stability of exchange rate for raw material Simple to operate controlled shed Available capacity Government incentives and ease policies Increasing income levels and restaurants Wide range of target market•Approx.40% market occupied by unorganized sector

Strengths Weaknesses

Threats Opportunities

Fluctuations in economic conditions Lack of Required Regulation by the

Government of Pakistan Poor Infrastructure High competition Virus and disease in Parent stocks i.e. Bird

Flu Accessibility of inputs

18

Sector Outlook: Negative

POULTRY | CONCLUSION

The first wave of Covid‐19 had hit hard on poultry prices, due to lockdown situation creating a supply glut as marriage halls andrestaurants were closed across the country. Prices of day‐old chick (DOP), eggs and broiler posted a dip (down by over 20%) duringMar’20‐June’20 period.

However, in 1HFY21, poultry prices have spiked rapidly due to recovered demand, supply dip (many farmers who suffered losses inthe previous three months, did not replenish their sheds) and increase in input prices.

Maize prices are expected to rise further due to hoarding of maize by farmers. International soybean and soybean meal prices arealso expected to continue growth due to lower USA stocks and increasing demand from China.

The Sector is highly leveraged, while average net margins of the sector are around ~4% in normal circumstances. Therefore, thecredit risk of sector players is expected to remain on the higher side on the backdrop of declining inventories and cash flows amidincreasing prices and demand uncertainty. On the contrary, an interest rate cut by 625bps is expected to provide relief to the Sector’sbottom‐line margins through reduction in finance cost.

In the absence of any reforms or package scheme, the increasing input prices of poultry feed with the current duty and tax regimemay continue to pressure the margins of the Sector players, particularly of the small farmers whose buying power is limited.

Despite the prevailing challenges, Pakistan’s overall economic position is on a trajectory to improvement. Overall industrial activityhas started to recover to pre‐COVID levels with the output of Large Scale Manufacturing Industries (LSMI) increasing by ~7.41%during July to November’21 as compared to same period last year. Moreover, the target GDP growth given by SBP for FY21 is ~2.1%.

19

POULTRY| BIBLIOGRAPHY

Research Team

Saniya TauseefTeam [email protected]

Noor ZiaAssociate [email protected]

Contact Number: +92 42 35869504

DISCLAIMERPACRA has used due care in preparation of this document. Our information has been obtained from sources we consider to be reliable but its accuracy or completeness is notguaranteed. The information in this document may be copied or otherwise reproduced, in whole or in part, provided the source is duly acknowledged. The presentation should not berelied upon as professional advice.

20

Pakistan Poultry Association DEFRA Sciencedirect PACRA Database The Big Book Project RaboBank 2020 AGBRO Group Indexmandi The Poultry World State Bank of Pakistan Federal Internal Board of Revenue Punjab Board Investment and Trade Ministry of National Food Security & Research The Economic Survey of Pakistan Food and Agriculture Organization of United Nations US Department of Agriculture