edb business partner asa - evry · edb business partner asa fourth quarter 2004 . interim report...

TRANSCRIPT

EDB Business Partner ASAFourth quarter 2004

31.01.05Interim Report Q404 2

Q4 and 2004 highlights

• 2004 – a year with profitable growth – Q4 – double-digit margin, first ever – Full Year – all time high EBITA– Revenue growth - gaining share

• Acquiring IT-operations from Capgemini – Sweden and Norway

• New dividend policy – Annual dividend 20-50% of normalized

result– Suggested 2004 dividend;

NOK 0.50 / share

• Well positioned for profitable growth

31.01.05Interim Report Q404 3

Entering 2005 with new strategic moves

• Skanska FM (Coor) outsourcing IT operations to EDB in Sweden

– TCV NOK 100 mill / 5 years

• EDB outsourcing Internal Services to Skanska FM (Coor)

– 5 years contract - Norway

• Software consolidation agreement with Computer Associate (CA)

– TCV NOK 330 mill / 5 years / Nordic

31.01.05Interim Report Q404 4

Key figures Q4 2004 – Group

NOK million Q4 2004 Q4 2003*

Operating revenue 1 138 1 113 Operating costs 1 025 1 008 Operating profit before goodwill depr. (EBITA) 114 106

EBITA % 10,0 % 9,5 %

Profit from divestments -6 EBIT 67 68

Profit before tax 60 63

Cash flow from operations 283 343 Operational investments (CAPEX) 119 65

Earnings per share (NOK) ** 0,50 0,61

No. of employees 2 484 2 504 * Operating revenues include NOK 105 mill from sold and discontinued activities** EPS before tax costs related to tax reform, NOK 490 mill

31.01.05Interim Report Q404 5

Key figures 2004 – Group

NOK million 2004 2003*

Operating revenue 4 236 4 289 Operating costs 3 848 4 125 Operating profit before goodwill depr. (EBITA) 388 165

EBITA % 9,2 % 3,8 %

Profit from divestments 295 - EBIT 524 -4

Profit before tax 480 -88

Cash flow from operations 610 302 Operational investments (CAPEX) 233 210

Earnings per share (NOK) ** 3,72 -0,59

No. of employees 2 484 2 504 * Operating revenues include NOK 409 mill from sold and discontinued activities** EPS before tax costs related to tax reform, NOK 490 mill

31.01.05Interim Report Q404 6

Operating revenue – Group

0

200

400

600

800

1 000

1 200

Q1 Q2 Q3 Q4

NO

K m

illion

2003 2004 Sold/discontinuedbusiness

31.01.05Interim Report Q404 7

Revenue split by Industry – Group

Distr, Industry,

Public sector; 20 %

Bank / finance;

56 %

Telecom; 24 %

Distr, Industry,

Public sector; 32 %

Bank / finance;

48 %

Telecom; 20 %

Including IBM and Capgemini4. quarter 2004

31.01.05Interim Report Q404 8

EBITA margin – Group

-6 %

-4 %

-2 %

0 %

2 %

4 %

6 %

8 %

10 %

12 %

Q1 Q2 Q3 Q4

2003 2004 Adjusted for non-recurring items

31.01.05Interim Report Q404 9

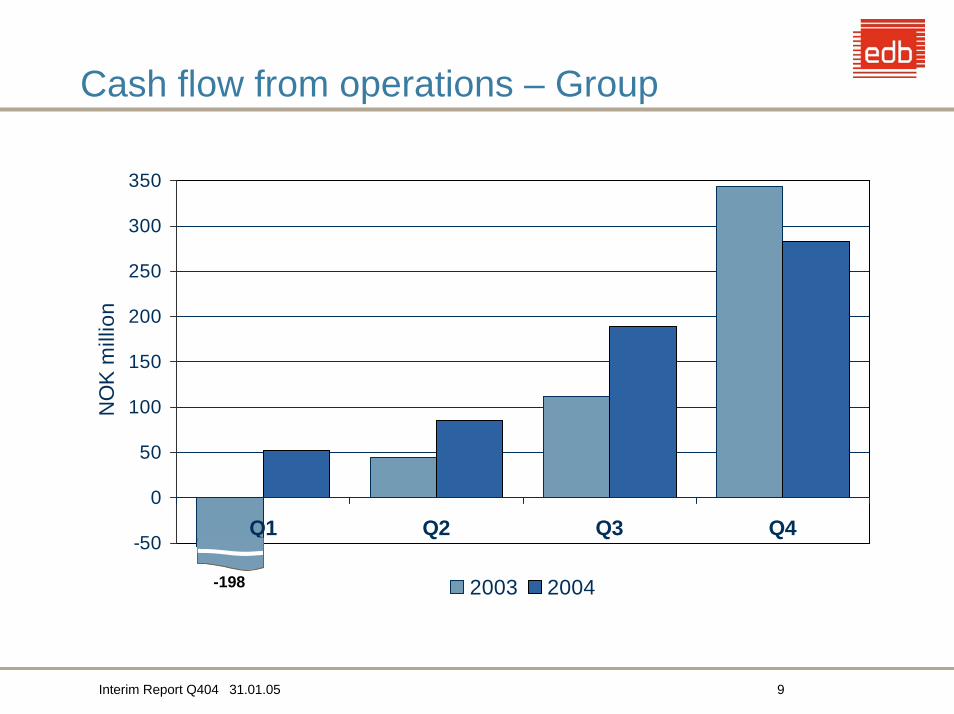

Cash flow from operations – Group

-50

0

50

100

150

200

250

300

350

Q1 Q2 Q3 Q4

NO

K m

illio

n

2003 2004-198

31.01.05Interim Report Q404 10

Net interest-bearing liabilities – Group

0

100

200

300

400

500

600

700

800

Q1 Q2 Q3 Q4*

NO

K m

illio

n

2003 2004

* Increase from Q3 to Q4 is entirely related to IBM and Capgemini transactions

31.01.05Interim Report Q404 11

ROIC – Return On Invested Capital

0,0 %

2,0 %

4,0 %

6,0 %

8,0 %

10,0 %

12,0 %

14,0 %

16,0 %

18,0 %

2003 1Q 2004 2Q 2004 3Q 2004 4Q 2004

• Invested Capital related to acquisitions completed 31.12.2004 not included

31.01.05Interim Report Q404 12

Order backlog – NOK 12.9 billion

TotalNOK mill order backlog

Order backlog 31.12.2004 2005 2006 2007 2008 LaterIT Operations 11 157 2 726 2 142 2 011 1 690 2 588

Bank & Finance 796 333 215 145 60 43

Telecom 95 90 5

Business from IBM/ Capgemini 861 574 191 96

Total order backlog EDB 12 909 3 724 2 552 2 253 1 750 2 631

% of total 29 % 20 % 17 % 14 % 20 %

31.01.05Interim Report Q404 13

Operating revenue by Business Area

0

100

200

300

400

500

600

700

800

900

1 000

Q1 Q2 Q3 Q4

NO

K m

illio

n

2003 2004

IT Operations

0

50

100

150

200

250

Q1 Q2 Q3 Q4

NO

K m

illio

n

2003 2004

Bank & Finance

0

20

40

60

80

100

120

140

160

180

200

Q1 Q2 Q3 Q4

NO

K m

illio

n

2003 2004

Telecom

• Q404/Q403: + 17 % • Q404/Q403: + 4 % • Q404/Q403: - 11 %

Note: Growth in percent is adjusted for sold and discontinued businesses

31.01.05Interim Report Q404 14

EBITA-margin by Business Area

-4 %

-2 %

0 %

2 %

4 %

6 %

8 %

10 %

12 %

14 %

Q1 Q2 Q3 Q4

2003 2004

TelecomBank & Finance

-15 %

-10 %

-5 %

0 %

5 %

10 %

15 %

20 %

Q1 Q2 Q3 Q4

2003 2004

-40,4%0 %

2 %

4 %

6 %

8 %

10 %

12 %

Q1 Q2 Q3 Q42003 2004

IT Operations

• Q404: 16 % • Q404: 5 %• Q404: 10 %

31.01.05Interim Report Q404 15

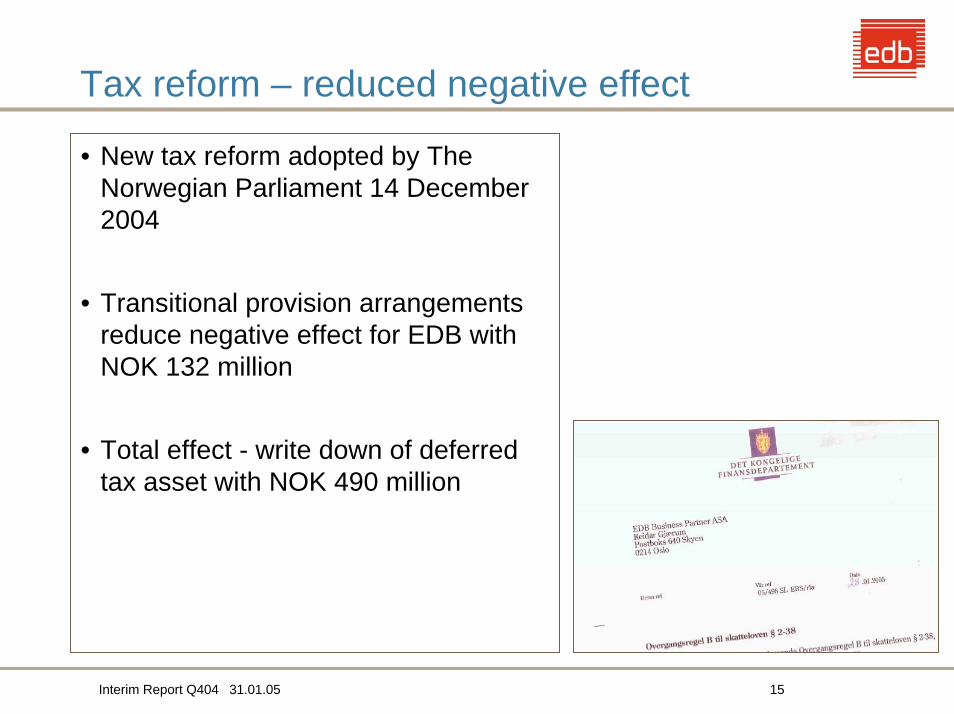

Tax reform – reduced negative effect

• New tax reform adopted by The Norwegian Parliament 14 December 2004

• Transitional provision arrangements reduce negative effect for EDB with NOK 132 million

• Total effect - write down of deferred tax asset with NOK 490 million

31.01.05Interim Report Q404 16

IFRS – no major implementation effects

• Main effects 2004 – Revenues and EBITA increase with app.

NOK 55 mill from changed revenue recognition principles

– Employee option expenses reduces EBITA with NOK 5 mill

– EBIT increases with app NOK 160 mill from reversal of goodwill depreciation

– Net effect direct equity adjustments NOK –160 mill

• Main effects 2005 – Amortization of intangible assets from IBM

and Capgemini transactions; app. NOK 90 mill in 2005 and NOK 40 mill in 2006

– No goodwill amortization– Changed revenue recognition on certain

license sales - may reduce revenues with app NOK 10 mill compared to NGAAP(Q1)

IT Operations

31.01.05Interim Report Q404 18

Q4 Highlights – IT Operations

• Profitable growth and gaining share– Revenue; + 17% – EBITA; + 22%

• Strategic acquisition from Capgemini –Sweden and Norway

• Increased 2005 backlog from growth initiatives

– Deals; NOK 200 million– M&A; NOK 600 million

• Cost cutting efforts on track– Technology consolidation process according

to plan– Software consolidation program with

substantial 2005-effects

31.01.05Interim Report Q404 19

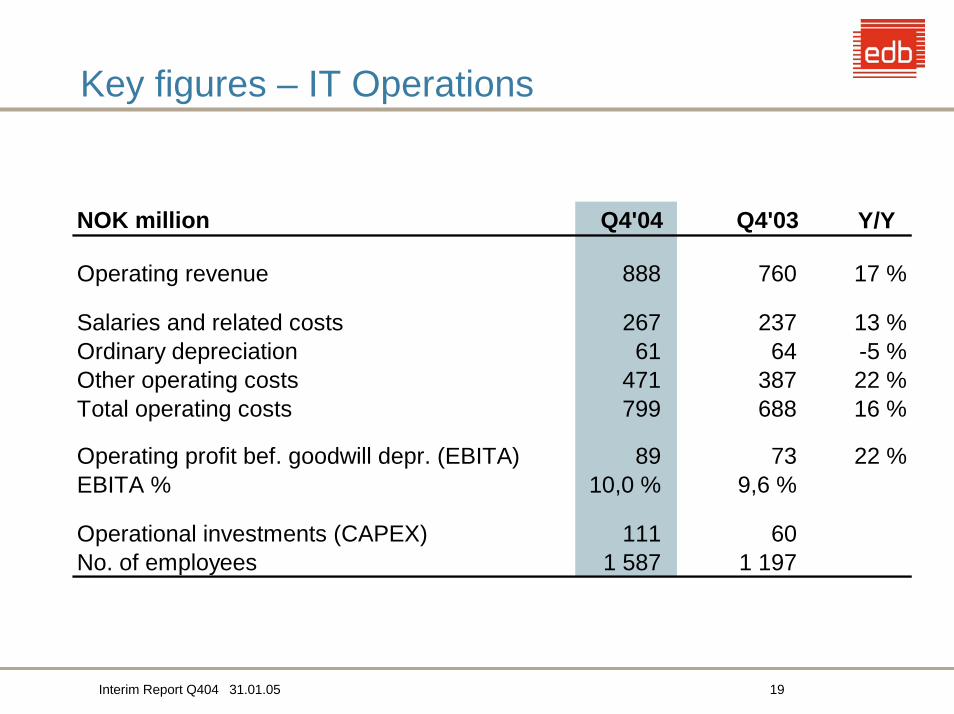

Key figures – IT Operations

NOK million Q4'04 Q4'03 Y/Y

Operating revenue 888 760 17 %

Salaries and related costs 267 237 13 %Ordinary depreciation 61 64 -5 %Other operating costs 471 387 22 %Total operating costs 799 688 16 %

Operating profit bef. goodwill depr. (EBITA) 89 73 22 %EBITA % 10,0 % 9,6 %

Operational investments (CAPEX) 111 60No. of employees 1 587 1 197

Bank & Finance

31.01.05Interim Report Q404 21

Q4 Highlights – Bank & Finance

• Continuous improvement of productivity and profitability

– Best Q4 EBITA-margin ever– Best full year result ever

• New long term contracts confirming competitive position

– Backlog improved

• Growth in electronic bank and card transactions

– High potential for new products and services (Internet bank/Exception-based Banking/Mobile banking)

31.01.05Interim Report Q404 22

Key figures – Bank & Finance

NOK million Q4'04 Q4'03 Y/Y

Operating revenue 219 212 4 %

Salaries and related costs 118 113 4 %Ordinary depreciation 2 3 -33 %Other operating costs 64 66 -3 %Total operating costs 184 182 1 %

Operating profit bef. goodwill depr. (EBITA) 35 30EBITA % 16,0 % 14,1 %

Operational investments (CAPEX) 2 2No. of employees 639 675

Telecom

31.01.05Interim Report Q404 24

Q4 Highlights – Telecom

• Two OEM-agreements with global vendors (incl. Nortel)

• New contracts signed in core areas– Vimpelcom: Mediation upgrade– Belgacom: NIMS (NOK 36 mill)– "European": NIMS (NOK 15 mill)

• Restructuring and cost cutting efforts – New management– Integration of staff functions– Sterling Best Routing – discontinued– HC reductions

31.01.05Interim Report Q404 25

Key figures – Telecom

NOK million Q4'04 Q4'03* Y/Y

Operating revenue 61 173 -49 %

Salaries and related costs 56 90 -36 %Ordinary depreciation 0 3 -56 %Other operating costs 2 61 -63 %Total operating costs 58 154 -45 %

Operating profit bef. goodwill depr. (EBITA) 3 19 -76 %EBITA % 4,8 % 11,1 %

Operational investments (CAPEX) 1 1No. of employees 207 621* Includes System Integration, sold with effect from 1. April 2004

2005 Market Outlook – IT Services

31.01.05Interim Report Q404 27

2004 – strategic moves and important deals

• EDB quantum leaping from acquisitions;

– Telenor, IBM and Capgemini

• EDB outperforming key competitors in size and number of deals

– 13 deals > NOK 100 million – Restructuring of Nordic IT-services

market to accelerate

• Several large out-sourcing deals expected in 2005 and 2006

• Global and regional players positioning to capture new growth

31.01.05Interim Report Q404 28

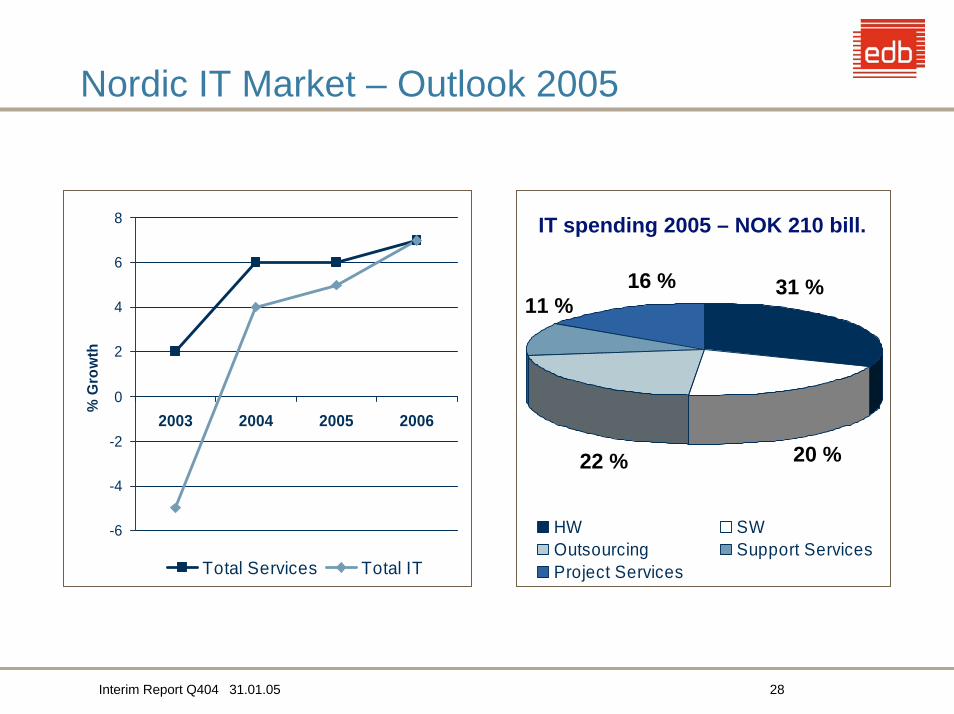

Nordic IT Market – Outlook 2005

-6

-4

-2

0

2

4

6

8

2003 2004 2005 2006

% G

row

th

Total Services Total IT

HW SWOutsourcing Support ServicesProject Services

IT spending 2005 – NOK 210 bill.

31 %16 %

20 %22 %

11 %

31.01.05Interim Report Q404 29

Nordic IT Outsourcing – Top 10 players

IBM GlobalCSC GlobalEDB RegionalTietoEnator RegionalHP GlobalWM Data RegionalErgo Group LocalEDS GlobalKMD LocalCapgemini Global

Company name Player

Source ; IDC (2004 estimates)

31.01.05Interim Report Q404 30

Nordic IT Services – Top 10 players

IBM GlobalTietoEnator RegionalWM Data RegionalHP GlobalCSC GlobalEDB RegionalAccenture GlobalKMD LocalAtos RegionalEmentor Regional

Company name Player

Source ; IDC (2004 estimates)

31.01.05Interim Report Q404 31

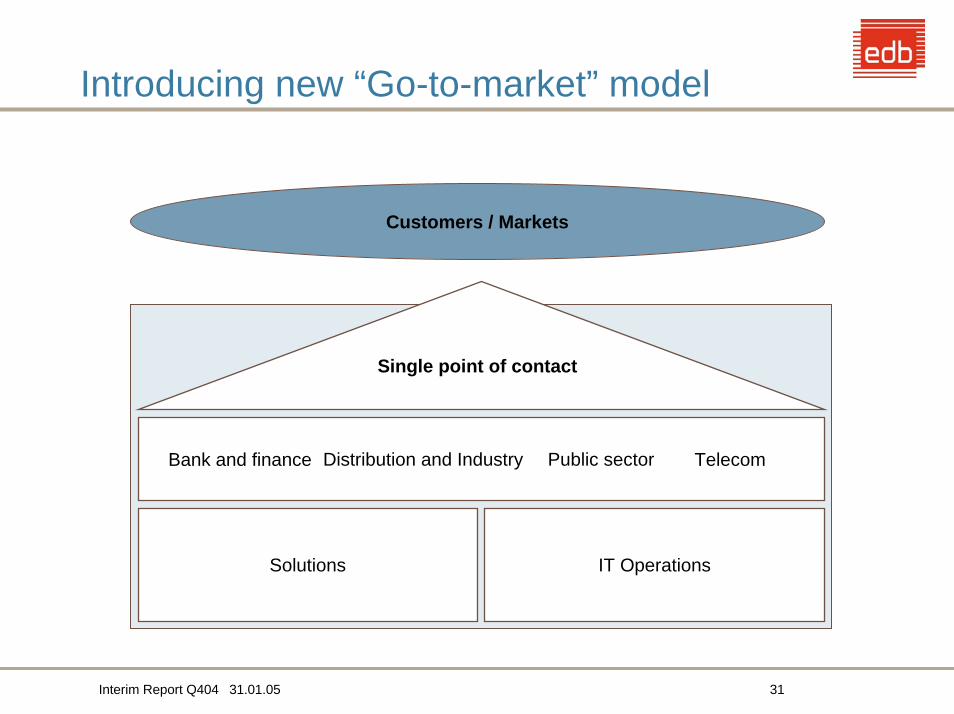

Introducing new “Go-to-market” model

Customers / Markets

Single point of contact

Solutions IT Operations

Bank and finance Distribution and Industry TelecomPublic sector

31.01.05Interim Report Q404 32

Summary

• Cost reductions programs on track

• Profitable growth in 2004

• Gaining share in new market segments

• Growing more than market in 2005

• Continuous growth in Sweden