economic update - bryan yu - central 1 credit union

TRANSCRIPT

Economic Update and Forecast

Bryan Yu Central 1 Credit UnionApril 15, 2015

| 1

|

About Central 1 Credit Union Central 1 is the primary liquidity manager, payments

processor and trade association for our member credit unions in B.C. and Ontario

Members which are also our owners represent a combined system of more than 130 independent credit unions, that have 3.3 million members and assets of more than $92 billion.

Credit Unions in B.C. employ more than 8,700 residents

|

Agenda

• Oil, Oil, Oil!

• National Outlook – How low can rates go?

• B.C. – Where do we go from here?

• Regional wrap-up

|

Headline news: Oil plunges on supply-side shocks

2007 2007-11-092008-09-122009-07-172010-05-212011-03-252012-01-272012-11-302013-10-042014-08-080.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

WTI USD/barrelSaudi Arabia: Retaining market share, prices reflect supply/demand

Source: U.S. Federal Reserve, Central 1 Credit Union Latest: 3/18//2015

$48

|

Main sources of supply increases last year

Q1-14 Q2-14 Q3-14 Q4-14-0.4

0.0

0.4

0.8

1.2

1.6

Saudi Arabia Libya Iraq U.S.

Million barrels/day

Increase in petroleum production since Dec. 2013

Source: U.S. Dept. of Energy – EIA.

|

Oversupply to last well into 2015

Q1-12

4/1/

...

7/1/

...

10/1

/...

Q1-13

4/1/

...

7/1/

...Q1-

Q1-14

4/1/

...

7/1/

...

10/1

/...

Q1-15

4/1/

...

7/1/

...

10/1

/...

Q1-16 Q1- Q1- Q1-

78

82

86

90

94

98

-2

-1

0

1

2

3

Balance (RHS) Production Consumption

Million barrels/day

World Oil Production and Consumption BalanceMillion barrels/day

Source: U.S. EIA, Short-term Energy Outlook, Feb. 2015.

|

Source: Bank of Canada.

|

Price plunge unexpected; higher prices after 2015

20

40

60

80

100

120

ActualConsensus Aug-14Consensus Dec-14Futures

US$ per barrel

Source: U.S. BEA, Consensus Forecasts, NYMEX. Forecast: 2015 - 2019.

WTI Oil Price: Actual and Forecasts

|

Large downgrade to first half 2015 forecast

0

1

2

3

4

Ac-tual

Oct-14

Per cent change at annual rate in real GDP

Source: Statistics Canada, Bank of Canada. Latest actual: Q3-14. Forecast: Q4-14 to Q4-17.

Bank of Canada Economic Growth Forecast

|

Canada’s outlook lowered, sharp cut to income growth

0

1

2

3

4

5

Source: Statistics Canada, Bank of Canada MPR. Latest: 2014 estimated, forecast 2015 to 2017.

1.5

2.0

2.5

3.0

3.5Actual Oct-14

Jan-15 Apr-15

Per Cent Per Cent

Real Gross Domestic Product Real Gross Domestic Income

|

Headline inflation to approach zero

0.0

0.5

1.0

1.5

2.0

2.5

Ac-tual

14-Oct

15-Jan

Per cent change at annual rate

Source: Statistics Canada, Bank of Canada. Latest actual: Q4-14. Forecast Q1-15 to Q4-17.

Bank of Canada Total CPI Inflation Outlook

|

Will the Bank of Canada cut again?

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

3-Mth BA Futures (Apr 10)

Target Overnight Rate

Per cent

3-Month Banker’s Acceptance, Actual and Futures

Source: Bank of Canada, Montreal Exchange, Central 1 Credit Union Latest Actual: Apr/2015

|

Rate outlook cut, long bonds below 3% through 2017, short yield less than 1%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20170.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

3-mo. T-bill LT GoC Bond

Per cent change

Interest Rate Outlook

Source: Statistics Canada, Bank of Canada Latest : 2014

|

Global economy still in growth mode albeit at mild pace

30

35

40

45

50

55

60

Expansion/Contraction Demarcation

IndexJP Morgan Global Manufacturing PMI

Source: Bloomberg, Central 1 Credit Union

|

China’s manufacturing slowdown

2013 2014 201546

48

50

52

54

56

58

Non-manufactur-ing

Index, 50=no change

Source: Bloomberg. Note: Seasonally adjusted. Latest: Feb. 2015

China PMIs

|

U.S. growth disappoints in Q1, uptick expected

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

GDP Mean Forecast

Per cent change at annual rate

U.S. Economic Growth

Source: U.S. Bureau of Economic Analysis, WSJ Survey of Forecasters, Mar/15 Latest : Q4-14

|

U.S. employment growth remains robust, to drive spending

123000

126000

129000

132000

135000

138000

141000

144000

-1000

-800

-600

-400

-200

0

200

400

600

Change (R) Total (L)

Persons (mil.)

U.S. Payroll Employment

Persons (000s)

Source: FRED Latest: Mar/15

|

U.S. housing starts rebalancing after decade of overbuilding

1991 3372534213 1995 3518635674 1999 3664737135 2003 3810838596 2007 3956940057 2011 4103041518 20150

500

1,000

1,500

2,000

2,500

Avg HH formation Housing Starts

(000s)

Source: Federal Reserve St. Louis, Central 1 Credit Union Latest : Q4-14

|

Divergence in monetary policy implied by futures markets – US to rise earlier and faster

Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17 Dec-170.00

0.50

1.00

1.50

2.00

3m Bas (Canada)30d Fed funds (US)

Per centShort-term Interest Rate Futures: Canada and U.S.

Source: Montreal Exchange, CME Group, Central 1 Credit Union. Date: Mar 16/15

|

Low oil, rate divergence hammers Canadian dollar

1/1/2010 12/3/201011/4/201110/5/2012 9/6/2013 8/8/20140.70

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

CAD at more than five-year low

CDN in USDDaily Exchange Rate

2011 2012 2013 2014 2015 2016 2017 2018 20190.70

0.75

0.80

0.85

0.90

0.95

1.00

1.05

1.10

Exchange Rate OutlookCDN in USD

Source: Statistics Canada, Central 1 Credit Union. Daily Latest actual: Apr/15

|

External Economic Outlook Indicator 2013 2014 2015f 2016f 2017f

U.S. real GDP, % chg. 1.9 2.4 2.9 3.1 3.0

Japan GDP, % chg. 1.5 -0.1 1.1 1.7 1.3

China GDP, % chg. 7.7 7.4 6.9 6.8 6.7

EU GDP, % -0.4 1.3 1.7 1.9 1.8

Canada real GDP, % chg. 2.0 2.5 1.8 2.0 2.5

WTI Crude- $/bbl 98 93 52 58 63

CAD – cents/dollar 97.1 90.6 78.4 75.5 74.9

Canada 3-month T-bill 0.97 0.95 0.65 0.50 0.75

Canada GOC Long Yield 2.72 2.77 2.05 2.25 2.70

Source: U.S. BEA, Statistics Canada, Consensus Forecasts, Central 1 Credit Union Mar/15 outlook.

|

Weaker oil will not derail B.C. economic growth

-6

-4

-2

0

2

4

6

8

10

NominalReal

Per cent change in GDPB.C. Economic Growth, Actual and Forecast

Source: Statistics Canada, C1CU. Latest actual: 2011. Forecast: 2014 - 2017.

|

Impacts on growth

• Income impact of Alberta oil shock• Weaker demand and income for interprovincial workers

• B.C. made up more than 25 per cent of Alberta interprovincial workforce (2008)1

• Could constrain oil-sand demand growth for B.C. natural gas

Source: 1Based on Statistics Canada data from, Laporte, Lu and Schellenberg. Interprovincial Employees in Alberta. 2013

|

Impacts on growth

• Lower oil prices lift domestic demand through consumer spending channels, lower input costs for businesses

• U.S. economic lift and lower Canadian dollar drives demand for B.C. exports

• Housing demand sustained by record-low mortgage rates

|

Mild improvements in B.C. labour market

2,140.00

2,160.00

2,180.00

2,200.00

2,220.00

2,240.00

2,260.00

2,280.00

2,300.00

Seas. Adj. 3-mo ma

Persons - millionsB.C. Employment

AWE

Hours Worked

Part-time

Full-time

Total EMP

0 1 2 3

2014 Performance

Source: Statistics Canada, Central 1 Credit Union. Latest actual: Mar/15

|

Population growth edges higher in 2014

-20000

-10000

0

10000

20000

30000

40000

50000

60000International Interprovincial

SOURCE Statistics Canada Central 1 Credit Union)

0.50

0.75

1.00

1.25

1.50Per Cent Persons (000s)

Population Growth Net Migration Flows

Source: Statistics Canada, Central 1 Credit Union Latest actual: 2014

|

Domestic economy continues to show strength

-15

-10

-5

0

5

10

15

Per CentY/Y Retail Sales Growth

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

MLS® SalesUnits

Source: Statistics Canada, Central 1 Credit Union Latest actual: Ret: Dec/14, MLS® Feb/15

|

Housing starts point to steady levels of construction in B.C.

2000 2001M052002M09 2004 2005M052006M09 2008 2009M052010M09 2012 2013M052014M090

10

20

30

40

50

60

SAAR Trend

Units (000s)

Source: CMHC, Central 1 Credit Union Latest : Mar/2015

|

Economy growth to shift away from domestic drivers

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0Domestic Demand GDP

Per Cent

Source: Statistics Canada, Central 1 Credit Union. Latest: 2014e

|

Exports to exceed import gains through 2017

-8

-6

-4

-2

0

2

4

6

8

10

Exports

Imports

Per cent changeExport / Import growth

Opportunities• Forestry cycle to shift higher on

U.S. housing market demand

• Broad manufacturing, including machinery and equipment

• Demand for agriculture, and food manufacturing to lead gains

• Tourism Demand

Source: Statistics Canada, C1CU. Latest actual: 2013, 2014e. Forecast: 2015 - 2017.

|

Exports range-bound but anticipated to pick up

1,800

2,000

2,200

2,400

2,600

2,800

3,000

3,200

3,400Nominal Real

Per CentInt’l Goods Exports - $(millions)

60

70

80

90

100

110

120

130

140Production Exports

Lumber Activity2012=100

Source: Statistics Canada, Central 1 Credit Union Latest actual: Feb 2015

|

Exchange rate sensitive sectors to experience boost

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

0

50000

100000

150000

200000

250000

Same-day or One Night Return

Two-Nights or More Return

SOURCE Statistics Canada Central 1 Credit Union)

2004 2005M09 2007M05 2009M01 2010M09 2012M05 2014250,000

300,000

350,000

400,000

450,000

500,000

Per Cent Persons (000s)International Tourist Inflows Canada-US Auto Flows

|

B.C. Economic and Housing Forecasts

Indicator 2013 2014 2015f 2016f

Real GDP, % chg. 1.9 2.4 2.7 3.4 3.3

Employment, % chg. 0.1 0.6 1.3 1.6 1.8

Unemployment rate, % 6.6 6.0 5.9 5.9 5.9

Population, % chg. 0.9 1.1 1.1 1.1 1.2

Housing starts, (000s) 27.1 28.3 30.0 31.1 31.6

Source: Statistics Canada, CMHC, Central 1 Credit Union Mar/15 outlook.

|

Metro area employment jumps in 2014 on part-time work

1100.0

1140.0

1180.0

1220.0

1260.0

1300.0

monthly, s.a. Annual average

Persons – thousands

Source: Statistics Canada, latest: Feb/2015

Vancouver CMA

LFS metric

Tot. Emp 2.3%

Full-time Emp 1.1%

Part-time Emp 7.1%

Unemployment Rate 5.8%

Annual Growth 2013/14

|

Abbotsford employment drops, but monthly trend climbs

2006 2007M01 2008 2009M01 2010 2011M01 2012 2013M01 2014 201574

76

78

80

82

84

86

88

90

92

94

monthly, s.a. Annual average

Persons – thousands

Source: Statistics Canada, latest: Feb/2015

Abbotsford CMA

LFS metric

Tot. Emp -3.7%

Full-time Emp -1.1%

Part-time Emp -11.7%

Unemployment Rate 7.4%

Annual Growth 2013/14

|

Unemployment rate in decline, but labour slack persists

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

3

4

5

6

7

8

9

10Abbotsford-Mission Vancouver

Per CentUnemployment Rate

62

63

64

65

66

67

68

69

70

Participation RatePer Cent

Source: Statistics Canada, Central 1 Credit Union Latest actual: 2014

|

Retail spending robust, tourism on the mend

-15

-10

-5

0

5

10

15

20Per Cent

Vancouver CMA, Y/Y Retail Sales Growth

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

U.S. Overseas

International Tourist Visits to B.C.Persons (000s)

Source: Statistics Canada, Central 1 Credit Union Latest actual: Ret: Dec/14, MLS® Feb/15

|

Non-residential building investment dips, but activity trends higher in second half

Source: Statistics Canada Latest: 2014

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Abbotsford CMA (L)

Vancouver CMA ( R)

Non-Res Building Investment ($2007)$ mil.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Non-Res Permit Volume - LMSW$ mil.

|

Population growth led by Metro Vancouver area, Fraser Valley lags

2005 2006 2007 2008 2009 2010 2011 2012 2013 20140.0

0.5

1.0

1.5

2.0

2.5Greater Vancouver Fraser Valley

Per Cent

Source: BC Stats, Latest: 2014

Lower Mainland-Southwest Population Growth

|

Vancouver driven by international immigration, loses to other regions

SOURCE Statistics Canada Central 1 Credit Union , latest 2013/14

-20,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Net NaturalIntra-ProvincialInterprovincialInternational

PersonsComponents of Population Change (StatsCan method)

|

Interprovincial migration negative in Abbotsford, modest lift in international gains

SOURCE Statistics Canada Central 1 Credit Union , latest 2013/14

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Net naturalIntra-ProvincialInterprovincialInternational

PersonsComponents of Population Change (StatsCan method)

|

Spring has sprung - Lower Mainland MLS® sales surge in March

2000M01 2001M05 2002M09 2004M01 2005M05 2006M09 2008M01 2009M05 2010M09 2012M01 2013M05 2014M090

1,000

2,000

3,000

4,000

5,000

6,000

Units

Source: CREA, Central 1 Credit Union Latest Mar/15

|

200520062007200820092010201120122013201420150

5

10

15

20

25

30

35

40

45

Housing conditions heat up in the Lower Mainland, prices on the rise

Sales-to-Active Listings Ratio*

2006 Jan-07 2008 Jan-09 2010 Jan-11 2012 Jan-13 2014 Jan-15300,000

350,000

400,000

450,000

500,000

550,000

600,000

-30

-20

-10

0

10

20

30

Benchmark price (L)Annualized m/m change ( R)

MLS® Housing Price$(000s)

Source: CMHC, Central 1 Credit Union, * CMAs/CAs Latest actual: Feb/15

Per Cent

|

Metro Vancouver sales rise to mid-2000 range, Valley sluggish

SOURCE: Landcor, Latest: 2014, resale properties

2005 2005M12 2006M11 2007M10 2008M09 2009M08 2010M07 2011M06 2012M05 2013M04 2014M03 2015M020

20

40

60

80

100

120

140Fraser Valley Greater Vancouver

Index (2005=100)

Lower Mainland Southwest Resale Transactions2013 Growth (%)

|

Price growth concentrated in Metro Vancouver

80

85

90

95

100

105

110

115

120

125

Fraser Valley

Greater Vancouver

Index (2010=100)

Source: Landcor Data Corp, Central 1 Credit Union note: 6-mth mov. average of s.a. data Latest Feb/15

Lower Mainland-Southwest Median Price by Region

Region Feb/15 (s.a.)

Fraser Valley $325,000

Greater Vancouver $557,000

Median price

|

Fraser Valley detached home value steady, apartments fall

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Detached Apartment Attached

Index (2010=100)

Source: Landcor Data Corp, Central 1 Credit Union note: 6-mth mov. average of s.a. data Latest Feb/15

Fraser Valley Median Price by Type

|

Housing starts steady on demand growth, Abbotsford construction still weak

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

200

400

600

800

1,000

1,200

1,400

0

5,000

10,000

15,000

20,000

25,000

Abbotsford CMA (L) Vancouver CMA ( R)

Units

Source: CMHC, Central 1 Credit Union Latest : 2014

Units

|

Economic Outlook

Indicator 2013 2014 2015f 2016f

Employment, % change

Vancouver CMA 0.0 2.3 1.0 1.8

Abbotsford CMA 2.6 -3.7 1.5 1.5

Unemployment Rate, %

Vancouver CMA 6.6 5.8 5.7 5.5

Abbotsford CMA 7.7 7.4 6.5 6.3

Population, % change

Vancouver CMA 1.4 1.3 1.3 1.5

Abbotsford CMA 0.5 0.3 0.6 0.8

Source: Statistics Canada, C1CU forecast

|

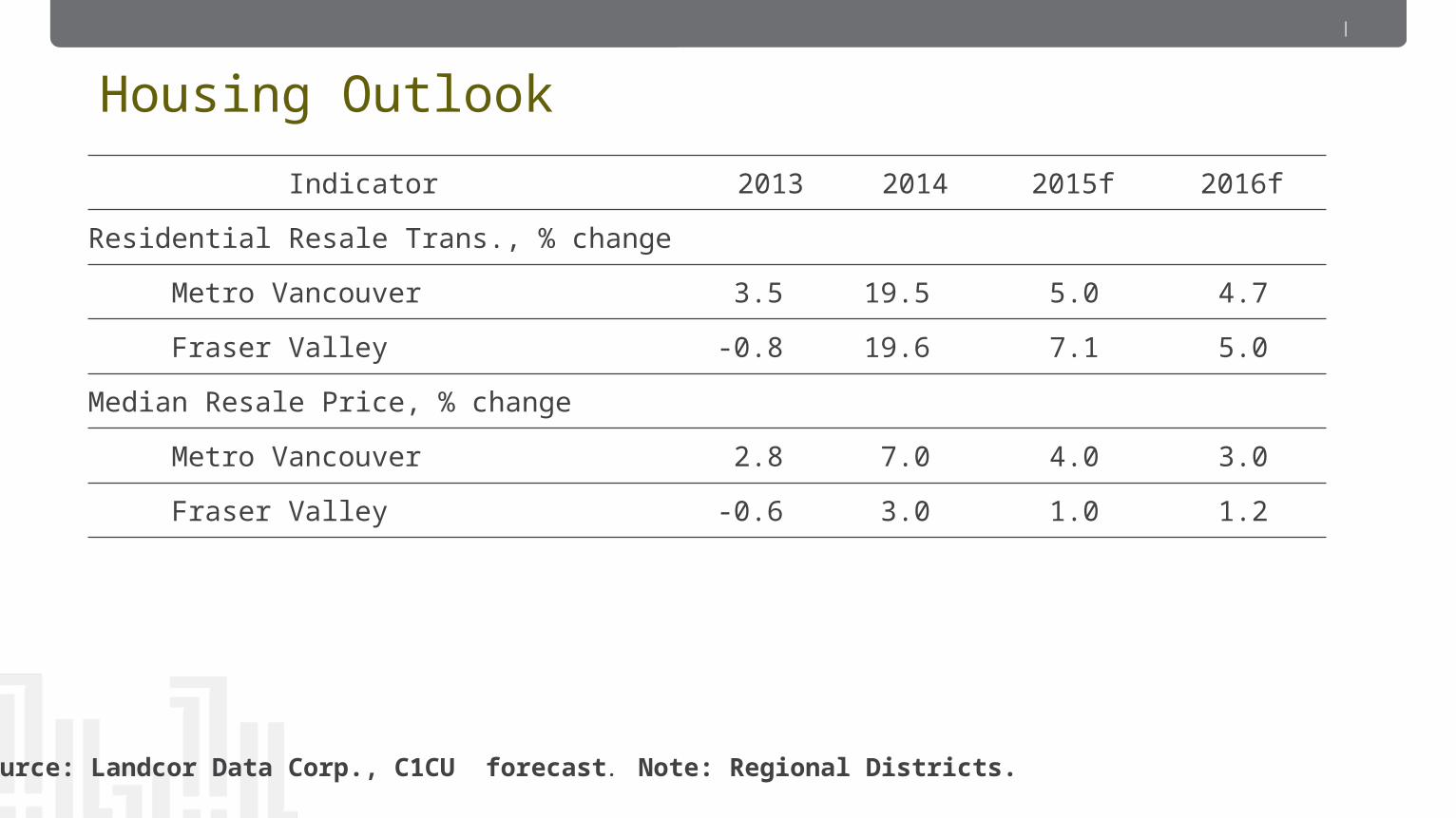

Housing Outlook

Indicator 2013 2014 2015f 2016f

Residential Resale Trans., % change

Metro Vancouver 3.5 19.5 5.0 4.7

Fraser Valley -0.8 19.6 7.1 5.0

Median Resale Price, % change

Metro Vancouver 2.8 7.0 4.0 3.0

Fraser Valley -0.6 3.0 1.0 1.2

Source: Landcor Data Corp., C1CU forecast. Note: Regional Districts.

|

Summary:

Global economy showing sporadic signs of emerging from slowdown

Oil prices to remain low in 2015; post modest gains thereafter

U.S. economy poised to gain momentum; expansion to extend

Global economy on improving trend from low oil prices and policy stimulus

Canada’s economy hit by oil price plunge

Another BoC rate cut likely while U.S. Fed makes first hike

|

Summary:

Lower CAD and improving external economies lifts B.C. economy

Lower Mainland-Southwest economy steady, driven by domestic demand, housing, tourism

Population growth mixed and led by Metro Vancouver due to immigration

Housing sales on the upswing, prices rising in Metro Vancouver, mild uplift in Abbotsford area

Construction a growth sector for economy