economic policy and prospects for reform under a second...

TRANSCRIPT

Economic Policy and Prospects for Reform under a Second Lula Administration

Otaviano CanutoWorld Bank, Executive Director forBrazil, Colombia, Dominican Republic,Ecuador, Haiti, Panama, Philippines, Suriname and Trinidad & Tobago

Woodrow Wilson Center Brazil InstituteWashington, November 1, 2006

1. Succession without a crisis: improved fundamentals2. Growth as the overriding challenge

Succession without a crisis:

improved fundamentals

Public Sector Primary Results and Targets (acc. in 12 months)Public Sector Primary Results and Targets (acc. in 12 months)Net Public Sector Debt / GDPNet Public Sector Debt / GDP

Source:Central Bank

Strong Fiscal Commitment =>expected debt reduction

Historical consolidated Public Sector Primary Surplus

3

Source:Central Bank

Historical consolidated Public Sector Primary Surplus Net Debt/GDP scenarios based on the FOCUS surveyNet Debt/GDP scenarios based on the FOCUS survey

Source:Central Bank and National Treasury* Data of Central Bank – IGP-DI (wholesale price index)‘modified’

35%

37%

39%

41%

43%

45%

47%

49%

51%

53%

2005 2006 2007 2008 2009 2010 2011

Market Scenario GDP 4% GDP 3%

4.33%

2.50%

3.10%

3.70%

4.30%

4.90%

5.50%

Jan-

02

Oct

-02

Jul-0

3

Apr-

04

Jan-

05

Oct

-05

Jul-0

6

% G

DP

Performed Target

% o

f GD

P

Market Expectations on Sep 26, 2006(annual data)

1Q00 through 2Q06 (quarterly data)

43.81Q00

3Q00

1Q01

3Q01

1Q02

3Q02

1Q03

3Q03

1Q04

3Q04

1Q05

3Q05

1Q06

2006 2008 201043

48

53

58

63 61.7

2Q 0650.3

Jan94

Jan95

Jan96

Jan97

Jan98

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Sep06

% o

f GD

P

-1

0

1

2

3

4

5

6

7

4.47

avg. 1994-Jun/954.77%

avg. Jul/95-1998-0.1%

avg. 1999-20023.18%

avg. 2003-20064.54%

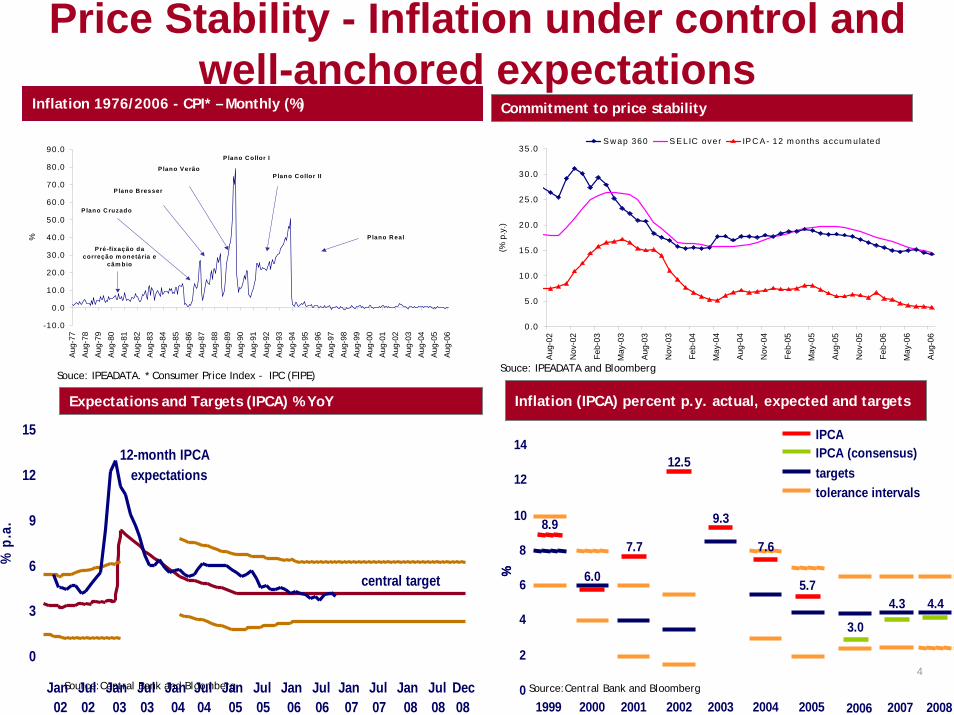

Inflation 1976/2006 - CPI* – Monthly (%)Inflation 1976/2006 - CPI* – Monthly (%)Commitment to price stability

Price Stability - Inflation under control and well-anchored expectations

Commitment to price stability

Expectations and Targets (IPCA) % YoY

Souce: IPEADATA. * Consumer Price Index - IPC (FIPE)

Expectations and Targets (IPCA) % YoY Inflation (IPCA) percent p.y. actual, expected and targetsInflation (IPCA) percent p.y. actual, expected and targets

4Source:Central Bank and Bloomberg

Souce: IPEADATA and Bloomberg

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Aug

-77

Aug

-78

Aug

-79

Aug

-80

Aug

-81

Aug

-82

Aug

-83

Aug

-84

Aug

-85

Aug

-86

Aug

-87

Aug

-88

Aug

-89

Aug

-90

Aug

-91

Aug

-92

Aug

-93

Aug

-94

Aug

-95

Aug

-96

Aug

-97

Aug

-98

Aug

-99

Aug

-00

Aug

-01

Aug

-02

Aug

-03

Aug

-04

Aug

-05

Aug

-06

%

Pré-fixação da correção m onetária e

câm bio

P lano C ruzado

Plano B resser

P lano Verão

P lano C ollor I

P lano C ollor II

P lano R eal

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Aug-

02

Nov

-02

Feb-

03

May

-03

Aug-

03

Nov

-03

Feb-

04

May

-04

Aug-

04

Nov

-04

Feb-

05

May

-05

Aug-

05

Nov

-05

Feb-

06

May

-06

Aug-

06

(% p

.y.)

S w ap 360 S E LIC over IP C A - 12 m onths accum ula ted

% p

.a.

central target

12-month IPCA expectations

0

3

6

9

12

15

Jan02

Jul02

Jan03

Jul03

Jan04

Jul04

Jan05

Jul05

Jan06

Jul06

Jan07

Jul07

Jan08

Jul08

Dec08

%%

targetstolerance intervals

IPCAIPCA (consensus)

0

2

4

6

8

10

12

14

1999 2000 2001 2002 2003 2004 2005 2006

8.9

6.0

7.7

12.5

9.3

7.6

3.0

5.7

2007

4.3

2008

4.4

Source:Central Bank and Bloomberg

Market Expectations – Focus (Oct 30, 2006)

Current account (12 months accumulated - US$ bn)Current account (12 months accumulated - US$ bn)Trade Balance

Reduction in the External VulnerabilityTrade Balance

Net External Debt/Exports accumulated in 12 months*Net External Debt/Exports accumulated in 12 months*

Source: Central Bank. *Public Debt and Private Debt as a share of export accumulated in 12 months

External Trade (Exports + Imports) of GDP (%)External Trade (Exports + Imports) of GDP (%)

6

Source: MDIC - SECEX Source:Central Bank

* Until July, 2006Source: MDIC – SECEX and Central Bank

24.5%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

*

0 .0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Aug

-00

Dec

-00

Apr

-01

Aug

-01

Dec

-01

Apr

-02

Aug

-02

Dec

-02

Apr

-03

Aug

-03

Dec

-03

Apr

-04

Aug

-04

Dec

-04

Apr

-05

Aug

-05

Dec

-05

Apr

-06

Aug

-06

Imp.

and

Exp

. - U

S$

Bn

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

Trad

e B

alan

ce -

US

$ B

n

T rade Balance Im port Export13.8

-30.0

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Aug

-01

Nov

-01

Feb-

02

May

-02

Aug

-02

Nov

-02

Feb-

03

May

-03

Aug

-03

Nov

-03

Feb-

04

May

-04

Aug

-04

Nov

-04

Feb-

05

May

-05

Aug

-05

Nov

-05

Feb-

06

May

-06

Aug

-06

US

$ B

illion

0.5

3.6

1.2

4.7

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1999

2000

2001

2002

2003

2004

2005

Aug

-06

Net External Debt / Exports Gross External Debt / Exports

Brazilian exports by destination (as a % of total exports)Brazilian exports by destination (as a % of total exports)

Brazilian exports by type (as a % of total exports)Brazilian exports by type (as a % of total exports)

7

Broad-based exports: balanced growth across markets and products

2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 41 2 - m o n t h s p e r c e n t a g e

c h a n g e 1

C o n t r ib u t io n ( p . p ) G r o w t h

L a t in A m e r ic a 2 3 . 4 % 2 1 . 0 % 1 6 . 3 % 1 7 . 7 % 2 0 . 4 % 3 1 . 6 % 5 . 2 o f w h ic h M e r c o s u l 1 4 .0 % 1 0 .9 % 5 .5 % 7 .8 % 9 .2 % 3 2 .6 % 2 .4A s ia 1 1 .5 % 1 1 .9 % 1 4 .6 % 1 6 .0 % 1 5 .1 % 2 4 .7 % 3 .7 o f w h ic h C h in a 2 .0 % 3 .3 % 4 .2 % 6 .2 % 5 .6 % 2 1 .4 % 1 .3 o f w h ic h J a p a n 4 .5 % 3 .4 % 3 .5 % 3 .2 % 2 .9 % 2 5 .3 % 0 .7C a n a d a 1 .0 % 1 .0 % 1 .3 % 1 .3 % 1 .2 % 5 1 .1 % 0 .4U S A 2 4 .3 % 2 4 .7 % 2 5 .7 % 2 3 .1 % 2 1 .1 % 1 2 .7 % 4 .7E u r o p e a n U n io n 1 6 .8 % 2 5 .5 % 2 5 .0 % 2 4 .8 % 2 5 .0 % 1 4 .6 % 5 .5O t h e r s 1 3 .0 % 1 5 .9 % 1 7 .0 % 1 7 .1 % 1 7 .1 % 3 9 .8 % 4 .7

T o t a l e x p o r t s ( U S $ b n ) 5 5 . 0 5 8 . 2 6 0 . 4 7 3 . 1 9 6 . 5 1 1 6 . 6 2 -

% g r o w t h 1 4 . 7 % 5 . 7 % 3 . 7 % 2 1 . 1 % 3 2 . 0 % 2 4 , 0 % 3-

S o u r c e : M D IC / S E C E X1 T h i s c o n t r ib u t io n r e f le c t D e c e m b e r 0 4 / N o v e m b e r 0 5 e x p o r t s in t e r m s o f D e c e m b e r 0 3 / N o v e m b e r 0 4 e x p o r t s2 T o t a l in D e c e m b e r 0 4 / N o v e m b e r 0 53 T o t a l g r o w t h in D e c e m b e r 0 4 / N o v e m b e r 0 5

1999 2000 2001 2002 2003 2004 November/041 November/051

Primary products 24.6% 22.8% 26.4% 28.1% 29.0% 29.6% 29.9% 29.0%Intermediary goods 16.6% 15.4% 14.2% 14.9% 15.0% 13.9% 14.1% 13.5%Manufactured products 56.9% 59.0% 56.5% 54.7% 54.3% 54.9% 54.4% 55.4%Special operations 1.8% 2.7% 3.0% 2.4% 1.8% 1.6% 1.6% 2.1%Total (US$ mn) 48.0 55.1 58.2 60.4 73.1 96.5 94.0 116.6 % growth (6.1)% 14.7% 5.7% 3.7% 21.1% 32.0% 31.4% 24.0%Source: MDIC/SECEX1 Total in 12 months

Trade Balances (Varying prices and volumes)

Volumes (as of)

Prices (as of )

2006 2005 2004 2003

2006 44.4 51.6 43.9 34.6

2005 35.8 44.8 37.7 29.7

2004 30.6 38.5 33.7 26.5

2003 26.9 34.0 29.7 24.8Source: Pactual

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Aug

-99

Dec

-99

Apr-

00

Aug

-00

Dec

-00

Apr-

01

Aug

-01

Dec

-01

Apr-

02

Aug

-02

Dec

-02

Apr-

03

Aug

-03

Dec

-03

Apr-

04

Aug

-04

Dec

-04

Apr-

05

Aug

-05

Dec

-05

Apr-

06

Aug

-06

US

$ M

illio

n

Restructured Debt (Bradies) New Bonds Contractual Debt Net Reserves

External Debt – National TreasuryExternal Debt – National Treasury

New

Issuances

International ReservesInternational Reserves

9

Source: National TreasurySource: National Treasury

External Public Debt Profile – New Bonds and Bradies

Management of External Public Debt Lower vulnerability & International Reserves

External Public Debt Profile – New Bonds and Bradies

Source: National Treasury.

Average Maturity – At Issuance of New BondsAverage Maturity – At Issuance of New Bonds

Source: National Treasury*Does not include the A-bond.** As of May/06

4.18

17.92

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2001

2002

2003

2004

2005

*

2006

**

Year

s

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

US

$ M

illion

Principal Interest

Oct 4:74.0

15

25

35

45

55

65

75

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

US$

bill

ion

Nominal Exchange RateNominal Exchange Rate Real Effective Exchange Rate

Exchange and Interest ratesReal Effective Exchange Rate

Souce: IPEADATA. * Consumer Price Index - IPC (FIPE)

Real Interest Rate (360-day Swap)Real Interest Rate (360-day Swap)

Source:Central Bank and Bloomberg

Souce: IPEADATA and Bloomberg

R$/

US$

Sep 292.17

10

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan98

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jun

94=1

00

100.0

100.4

60

80

100

120

140

160

180

Jan88

Jan90

Jan92

Jan94

Jan96

Jan98

Jan00

Jan02

Jan04

Aug06

basket of 15 currencies

%

9.15

10

15

20

25

30

35

40

Jan96

Jan97

Jan98

Jan99

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Sep06

avg. 06:10.0%avg. 96/99:

18.5% avg. 04/05:11.5%

avg. 00/03:15.0%

Federal Domestic Debt IndicatorsFederal Domestic Debt Indicators

Federal Debt Indicators*Federal Debt Indicators*

Management of Domestic Public Debt Lower Vulnerability

11

Minimum Maximum

Stock of DPMFi held by the public (R$ billion) 623.2 731.4 810.3 979.7 1,039.0 1,130.0 1,200.0Average Maturity of DPMFi (months) 33.2 31.3 28.1 27.4 29.8 30.0 35.0Average Life (month)¹ - - - 40.3 44.6 44.0 52.0% Maturing in 12 months 41.1 35.3 46.1 41.6 39.2 31.0 36.0

Share of DPMFi (%)Fixed rate 2.2 12.5 20.1 27.9 31.5 28.0 37.0Price Index 12.5 13.6 14.9 15.5 21.6 18.0 24.0Floating rate 60.8 61.4 57.1 51.8 42.5 39.0 48.0

Exchange rate 22.4 10.8 5.2 2.7 2.2 1.0 3.0Others 2.1 1.8 2.7 2.1 2.2 2.0 4.0

¹ Since these data have been calculated through the use of the commonly used international methodology, the statistics allow for comparisons with the indicators of other countries.

Aug/062002 2003 2005Indicators 20042006

Minimum MaximumStock of DPF* held by the public (R$ billion) 893.3 965.8 1,013.9 1,157.1 1,175.0 1,280.0 1,360.0Average maturity - Federal Outstanding Debt (months) 42.6 39.0 35.3 32.9 35.4 35.0 41.0Average Life (month)** - - - 56.3 57.8 60.0 70.0% Maturing in 12 months 34.6 30.7 39.3 38.2 36.5 28.0 33.0

Share of DPF (%)Fixed rate 1.5 9.5 16.1 23.6 27.8 25.0 33.0Price Index 8.8 10.3 11.9 13.1 19.1 16.0 22.0Floating rate 42.4 46.5 45.7 43.9 37.6 35.0 43.0

Exchange rate 45.8 32.4 24.2 17.6 13.6 11.0 15.0Others 1.4 1.4 2.2 1.8 2.0 1.0 3.0

* It includes the external debt under the responsibility of National Treasury** Since these data have been calculated through the use of the commonly used international methodology, the statistics allow for comparisons with the indicators of other countries.

20042002 20032006

Aug/062005Indicators

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Directed CreditSelic

Interest rate, directed credit (TJLP) and Selic (%)Interest rate, directed credit (TJLP) and Selic (%)Volume and costs of credit

Default rates (above 60 days)

Profitable private sector and dynamic credit & capital markets

Credit to the private sector (Jan 2004=100)Credit to the private sector (Jan 2004=100)

Source:CVM

Risk Perception – Brazil and Emerging MarketsRisk Perception – Brazil and Emerging Markets

Profitability of 500 Top Firms (1981-2004)Profitability of 500 Top Firms (1981-2004)

Source: Conjuntura Econômica - FGV - August 2005

K Markets – Primary Issue (R$ million – current values)K Markets – Primary Issue (R$ million – current values)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

**

Shares Debentures Other*

175.8

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

Feb-

02

May

-02

Aug

-02

Nov

-02

Feb-

03

May

-03

Aug

-03

Nov

-03

Feb-

04

May

-04

Aug

-04

Nov

-04

Feb-

05

May

-05

Aug

-05

Nov

-05

(*) Includes promissory notes, CRIs (real estate receivables certificates), and quotas of credit rightsinvestment funds, among others. (**) Up to July

100

150

200

250

300

350

400

Oct

-05

Nov

-05

Jan-

06

Feb-

06

Mar

-06

Apr-

06

May

-06

Jul-0

6

Aug

-06

Spr

ead

50

150

250

350

450

550S

prea

d D

iffer

ence

Brazil - Emerging Markets EMBI+ Brasil EMBI+ X-Brasil X-Arg

Buy Back

Bradies Call

Some reforms have impacted average GDP growthSome reforms have impacted average GDP growth

Job creation 6 largest metropolitan areasJob creation 6 largest metropolitan areas

14

Job Creation (Net hiring in the formal sector)

Formal job creationJob Creation (Net hiring in the formal sector)

Rise in purchasing power of minimun wageRise in purchasing power of minimun wage

Source: IBGE

Source: Central Bank

1,188.6

-700

-180

340

860

1380

1900

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005*

Net

Adm

ittan

ce -

Thou

sand

6.900

7.400

7.900

8.400

8.900

9.400

Apr-02 Aug-02 Dec-02 Apr-03 Aug-03 Dec-03 Apr-04 Aug-04 Dec-04 Apr-05 Aug-05 Dec-05

Formal jobs

Informal jobs + autonomous

Source: IBGE. Prepared by MF/SPE.

Thousands

70

350

300

260240

200180

151136130

120112100

0

50

100

150

200

250

300

350

400

Jan-95 Oct-95 Jul-96 Apr-97 Jan-98 Oct-98 Jul-99 Apr-00 Jan-01 Oct-01 Jul-02 Apr-03 Jan-04 Oct-04 Jul-05 Apr-060,0

0,5

1,0

1,5

2,0

2,5R$

Minimum wage-to-basic food bundle ratio (right scale)

%

0

1

2

3

4

1981-1990 1991-2003 2004-2006*

1.6

2.3

3.7

Reduction in both poverty and inequality

15

Income Poverty 1992-2004Income Poverty 1992-2004

Comparison of poverty across countriesComparison of poverty across countriesIncome Distribution 1990-2004 Income Distribution 1990-2004

Source: IBGE Source: IBGE

Source: IBGE and The World BankSource: IBGE and The World Bank

< US$ 1/day < US$ 2/day Survey dateBRASIL 8,2 22,4 2001CHINA 16,6 46,7 2001ÍNDIA 35,3 80,6 1999-00

RÚSSIA <2 7,5 2002INDONÉSIA 7,5 52,4 2002MALASIA <2 9,3 1997MÉXICO 9,9 26,3 2000

FILIPINAS 15,5 47,5 2000TAILÂNDIA <2 32,5 2000

% Population living with

Source: IBGE and The World BankSource: IBGE and The World Bank

< US$ 1/day < US$ 2/day Survey dateBRASIL 8,2 22,4 2001CHINA 16,6 46,7 2001ÍNDIA 35,3 80,6 1999-00

RÚSSIA <2 7,5 2002INDONÉSIA 7,5 52,4 2002MALASIA <2 9,3 1997MÉXICO 9,9 26,3 2000

FILIPINAS 15,5 47,5 2000TAILÂNDIA <2 32,5 2000

% Population living with

Income Inequality Measures (1976-2004)Income Inequality Measures (1976-2004)

35,87

36,57

29,82 29,8029,59

28,29

29,30 29,01 28,72

27,26

26,23

25,08

20

22

24

26

28

30

32

34

36

38

40

1992 1993 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

%

0,57

20,

665

0,50

0,55

0,60

0,65

0,70

0,75

0,80

0,85

0,90

0,95

1,00

1976

1977

1978

1979

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1992

1993

1995

1996

1997

1998

1999

2001

2002

2003

2004

0,50

0,55

0,60

0,65

0,70

0,75

0,80

0,85

0,90

0,95

1,00

Theil T

Gini

48,0 48,447,2 46,7 47,3 46,4 45,7

44,7

14,113,513,212,412,611,912,111,5

40,539,5

40,9 40,7 40,4 40,4 41,240,8

1990 1993 1996 1999 2001 2002 2003 2004

50% poorest 40% 10% richest

Reduction in both poverty and inequality

16

Growth and Household IncomeGrowth and Household Income

Inequality Reduction: Labor Income and Bolsa-FamiliaInequality Reduction: Labor Income and Bolsa-FamiliaReturns to education. Average of schooling years of 10 y-old

(or more) people

Returns to education. Average of schooling years of 10 y-old (or more) people

5.0

6.6

4.0

4.5

5.0

5.5

6.0

6.5

7.0

1993 1995 1996 1997 1998 1999 2001 2002 2003 2004

Source: IBGE Source: IBGE

Income Transfer Programs (means-tested + CCTs)Income Transfer Programs (means-tested + CCTs)

2004-2003Gini - Concentration Coefficient Change (p.p.) -1,11 Concentration effect 88% Income effect 12%

Labor Income 1 71%Minimum wage indexed Pensions 2 -10%Other Pensions 3%Interests, dividends and Bolsa-família 3 38%Rentals and donations -2%

1,4%0,6%

1,3%

2,4%

4,7%4,3%

3,1%

2,3% 2,3%2,3%

4,0%

45.000

47.000

49.000

51.000

53.000

55.000

57.000

59.000

61.000

63.000

65.000

Dec

-02

Mar

-03

Jun-

03

Sep

-03

Dec

-03

Mar

-04

Jun-

04

Sep

-04

Dec

-04

Mar

-05

Jun-

05

Sep

-05

Dec

-05

Mar

-06

Jun-

06

Sep

-06

Dec

-06

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%R$ millions

8,2%

5,5%

5,2%

Real GDP yearly change (seasonally adjusted; right scale)

Note: Labor income + pensions, other social insurance and transfers (seguro-desemprego, INSS, FGTS e Bolsa-Família, etc). 2006 = ForecastSources: PME/ IBGE, Caixa Econômica Federal, MF/STN, IPEAdata e SIAFI. Prepared by MF/SPE.

Bolsa-Família

5,69

3,79

0,57

8,3

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

2.001 2002 2003 2004 2005 2006

R$ billionsOther programs

2,64

1,75

1,09

0,25

2,26

0,41

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

2001 2002 2003 2004 2005 2006 *

Cartão-AlimentaçãoAuxílio-GásBolsa-AlimentaçãoBolsa-Escola

R$ billions

Growth as the overriding challenge

Brazilian GDP grew at a lower pace than other emerging economies in the last 25 years

(average, 1980-2005)

0

2

4

6

8

10

China

Singapore

SouthKorea

Malaysia

Thailand

India

Chile

Turkey

Mexico

Brazil

%

The Primary Source of Growth- Productivity

Most Growth Episodes with a Growth Rate of over 7% have a TFG Contribution of 3% or more

GDP Growth Rate TFP GDP Growth Rate TFPCambodia 7.48 3.21China 9.94 6.33 7.13 2.49*Malaysia 8.45 3.4Singapore 7.95 3.69Korea 7.48 3.13Thailand 8.58 4.74Ireland 7.99 3.52Israel 7.03 2.11Chile 7.24 3.55Lebanon 13.51 12.27Syria 7.97 4.87

7.35 3.86

*Could be 0.5% higher because of revision of GDP growth upward during the period, according to Srinivasan, T.N. 2006

Developing Asia

1995-2003 (%)

Source: Jorgenson and Vu 2005. Of the 110 economies or 220 growth episodes studied by Jorgenson and Vu 2005, only these 12 episodes had a growth rate of over 7%.

1989-1995 (%)

Growth Total Factor Productivity

Investm.(risk-adjusted rates of return)

Inflation and Monetary Policy- The last price shock- End of disinflation and search for the natural rate

WPI

Foreign Prices –Commodities (R$)

Fiscal Policy and Quality of Adjustment