economic empowerment conference 2011

TRANSCRIPT

Economic Outlook and current state of the Northern Ireland EconomyAngela McGowan

Chief Economist

Northern Bank

Prepared November 2011

Click icon to add picture

Current state of NI economy

• The Bigger picture:• - Global / European crisis• - UK economy

• SWOT analysis for NI economy• Headline indicators• Economic outlook

• Discussion - making choices

Global recovery 4% per year – long period of slow growth:

Extra hit from the recent financial shock – long-term damage

BUT we expect some rebound in Q4 from: - low inventory levels - lower oil and food prices

West is trapped in low growth and elevated unemployment rates – Emerging mks – 6% growth

The Global Picture .....

• Headwinds from early 2011 (oil and food price shock / Japanese earthquake and Chinese policy tightening) starting to fade. But Aug/ Sept financial shock took its toll.

• There will be long-term damage from the shocks to the global economy this year. The job engine has not started and we now face significant policy tightening in advanced economies.

• As a consequence, central bank rates in the US, Europe and Japan will be kept low for the foreseeable future.

We do not expect a global recession but Europe is a high risk and is expected to contract for at least one quarter. • We don’t believe the Q3 shock was big enough to

trigger a GLOBAL recession (but another hit of 10-15% wuld do it)

• But – it will have an impact upon business and consumer behaviour in Q3 - inventories will be cut

• - investment plans postponed• Consumers will probably spend less

Remember:

- many headwinds are turning into tailwinds and will pull growth upward

- Interest rates will provide some support

But risks remain high around the Eurozone:

• European crisis is the biggest risk at moment.

• This week markets will focus on: - Greece – will it pass the austerity package?- Italy - negotiations over potential pension reform are

expected to continue. Risk of a government reshuffle in Italy remains in focus.

• At the ECOFIN meeting (today), the Ministers of Finance will “discuss the follow-up to the decisions taken” at the EU Summit.

• Markets would like a lot more detail to reduce uncertainty

The Worst case scenario The good alternative

• This scenario centres on a further worsening of sentiment in the interbank markets.

• A tightening of credit standards and drop in asset prices would result in slowing production /rising U and a drop in investments and consumption

• - another global financial crisis would lead to recession in the Western economies and dampen growth in Asia.

• The impact on the real economy would be very severe – particularly in the Euro area – with no room for a fiscal response.

- European leaders would make appropriate moves - to restructure

Greek debt / recapitalise banks etc √√

- Growth and risk sentiment would improve markedly on the back of a strong turnaround in the global manufacturing cycle – with China leading

- China would be willing to support the European Financial Stability Facility.

- US continues to recover.

- The interbank market normalises

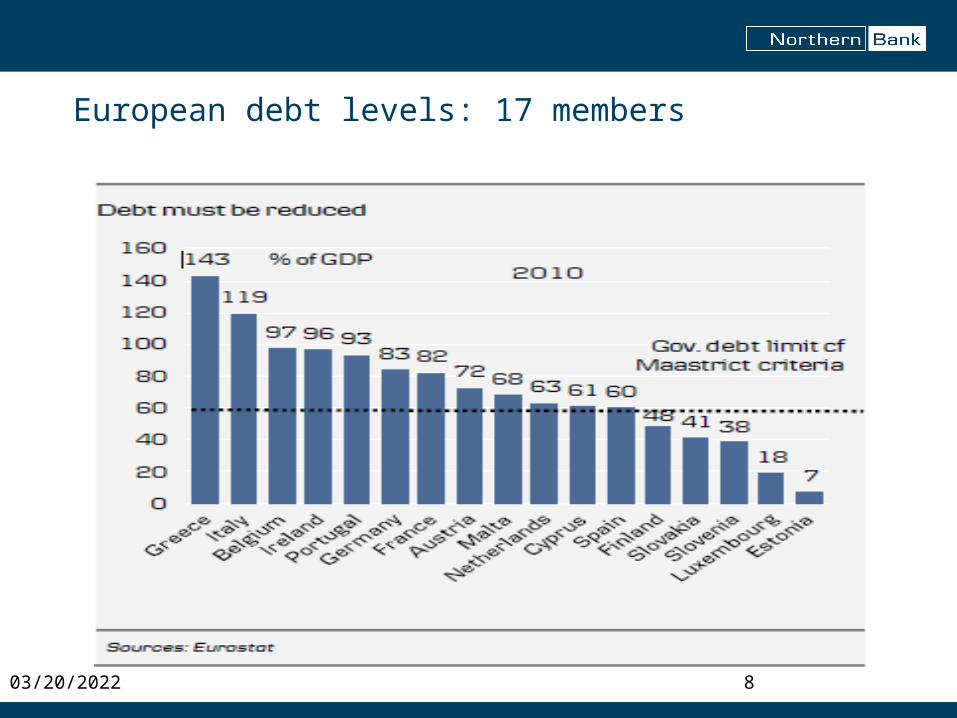

European debt levels: 17 members

04/15/2023 8

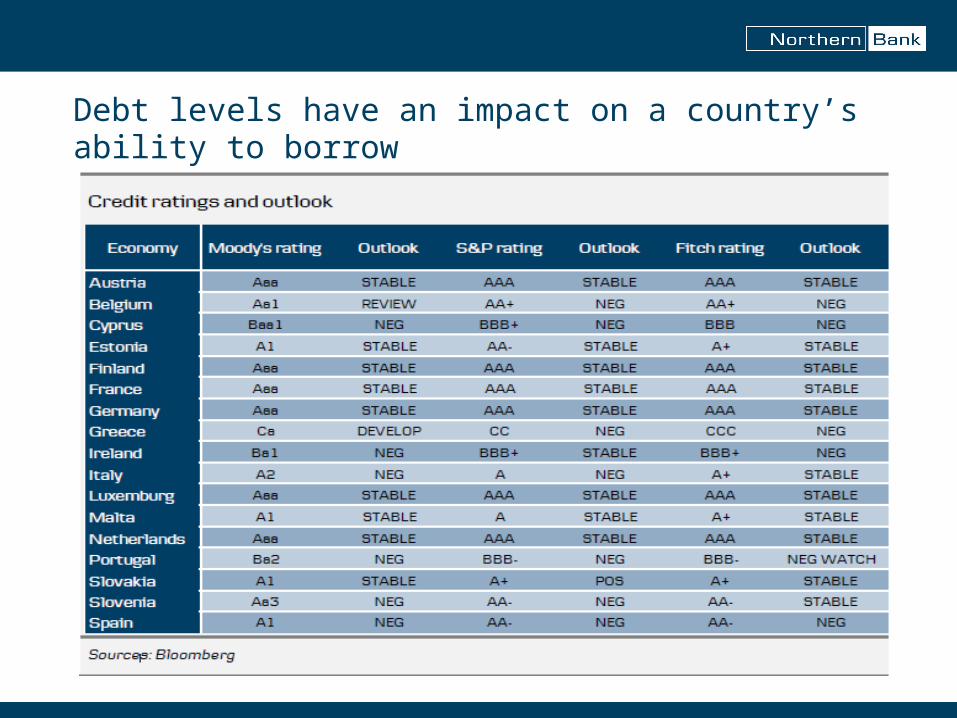

Debt levels have an impact on a country’s ability to borrow

Current state of play

• The ECB cut its key policy rates by 25bp. (downside risks to economic growth -forecast a mild European recession).

• Will probably cut its key rates another 25bp in December.

• The relief that followed after the EU summit last week was short-lived - market is not happy about the lack of detail in the 'comprehensive package'.

• Market sentiment could worsen - but if Italy commits to reforms +G20 delivers a constructive solution + Greek salvage gov’t - all this could be positive for this week.

• Unfortunately, none of these events will be a permanent game changer.

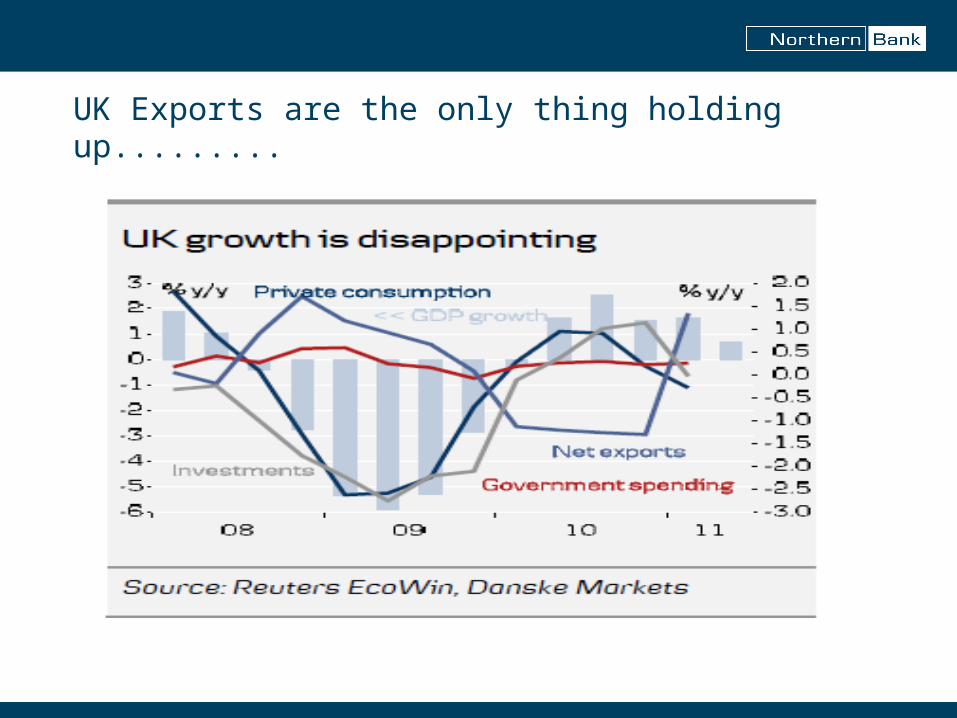

Data suggests UK recovery is still struggling..............UK – Recovery stalling

Unemployment levels risen to 8.1% - labour market flexibility

After 0.1% growth in Q2, ONS estimate Q2 0.5% but -UK in trouble before EU crisis took hold

Problems remain:

Austerity already having an impact on domestic spending

Europe – potential impact for Exports and bank exposures

Inflation still high (5.2% – Sept11)

UK : THE PRESSURE IS ON

UK Exports are the only thing holding up.........

The outside impact on Northern Ireland?

• UK Austerity will have some impact on local public spending – but also huge impact upon confidence.

• European crisis – again an impact upon confidence /investment and potential to hit exports.

• Unemployment risen• Access to finance impact

GVA growth (%)

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Q1 2006

Q3 2006

Q1 2007

Q3 2007

Q1 2008

Q3 2008

Q1 2009

Q3 2009

Q1 2010

Q3 2010

Q1 2011

Q3 2011

Q1 2012

Q3 2012%

NI

UK

Northern Ireland Economic Overview: weak growth ahead and potential for rising unemployment levels is high Since emerging from recession in late 2009, Northern Ireland is also experiencing a very weak recovery

The indicators suggest a sluggish labour in terms of job creation but//unemployment is now at 7.6% (8.1% in UK and 14.4% in RoI)

A fall back into recession cannot be ruled out (probability estimated to be in the region of 25%)

Revisions to sickness benefit could have huge impact

Source: Oxford Economics & Northern Bank August 2010

Consumer confidence and demand collapsed! Sept 11

SWOT analysis for NI economy

strengths

• Infrastructure• Young population• Good education system

(top)

• World–class universities• Smallness /access***• English Speaking• History of Industrial

success / innovation• Political ethos –

democratic and value equality

weaknesses• Low productivity• Small private sector • Smallness***

- economies of scale /- regional restrictions – taxationRecovering from a housing bubble

• Large tail of underachievement• Youth unemployment levels• Economic and social exclusion – LTU• Skills gap• No growth of knowledge

economy • Export / R&D / clusters / start-up

levels• Education system – elitist /

creativity

SWOT analysis for NI economy

Opportunities• University research –

more spin offs• International goodwill /

Diaspora• Growing demand from

Emerging Markets• Connectivity with RoI

and rest of UK• More partnerships PPPs• Taxation autonomy

Threats• Global downturn• Unemployed youth (18%)• Austerity measures• Subvention £9billion• LT Energy supply and cost• Political resistance to

raising local revenue streams:

• - water / rates / health service

Employment in the knowledge economy as % of total employment (NISC CONNECT report 2011)

Business start-ups per 100,000 of the population in the UK

Private sector R&D levels (BERD) extremely low...

Discussion - making economic choices

• Q: What does society actually want?• levels of taxation V levels of public spending ?• intervention V free market ? somewhere in between?

Regulation – how much? Where? – environmental / financial / etc

Regional economic dependence V Independence• Where should our job creation come from?

• – local enterprise and new firm start-ups?• - Foreign investors?• - mixture of both?

- Low or high risk economic strategy? Middle ground?Economics is about optimum use of available resources - but we still need to make

choices according to social consensus. (e.g current school system)• HOWEVER - for that decision making we need better information - we need to know

who will benefit? What is the cost? Who will carry the risk ? What are the alternatives?

• - Who is responsible for getting us there – politicians / private sector – social partnership consensus approach?

For up-to-date info check out the website:www.northernbank.co.uk/economy