dubai, uae 6-9 march 2014 - interniaudit.cz

TRANSCRIPT

globaliia.org

2014 Global Council

Dubai, UAE6-9 March 2014DAY 2

globaliia.org

Opening Remarks

Paul J. Sobel, Chairman of the Board

globaliia.org

Agenda - Tuesday

• Opening Remarks P. Sobel

• Expanding the Umbrella of the IIA D. Beran

• Tuesday Discussion Topics:

• Reassessing IPPF L. Harrington

• Membership Value Proposition H. Silverman

• Feedback Forum and

Closing Session P. Sobel

Open Evening

globaliia.org

Umbrella ProjectExpanded Services

globaliia.org

Agenda

• Expanded Service Project Overview

• Timelines/Actions Taken Since Global

Council

• What We Have Learned from Recent Study

• Discussion Points

globaliia.org

EXPANDED SERVICES

PROJECT OVERVIEW

• Goal B of Global Strategic Plan

The IIA will deliver the value that compels current,

future and former internal auditors to be members

(Membership/Value Proposition)

• Strategy B3

Address the needs of different sectors within the

internal audit or related professional activities.

globaliia.org

Objective

Objective

Identify and recommend potential options on how best to

implement Strategy B.3 – Address the needs of different sectors

within the internal audit or related professional activities, while

ensuring that The IIA also fulfills its core mission of providing

dynamic leadership for the global profession of internal auditing.

Phase 1

Address the disciplines in the 2nd line of defense (LOD) of the

Three Lines of Defense Model, which are most aligned to The

IIA’s current constituents – Risk Management, Compliance,

Internal Control

globaliia.org

Timeline –

Prior to Global Council 2013

Strategy Refresh Mtg. –Addressing the Needs of Diff. Sectors

• Oct. 2012

BOD Mtg. – Proceed with Further Analysis

• Nov. 2012

Global Council –High Priority for Additional Analysis

• Feb. 2013

Do Nothing Was Not An OptionMove Forward with Additional Analysis

8

globaliia.org

Timeline –

Global Council 2013 – July 2013

EC Mtg. – Approved $150k Initial Invest

March 2013

• Oct. 2012

3-Phased Approach –Market Research, Concept Plan, Business Plan

• April 2013

AssessedCompetitive Landscape

• July 2013

Identified and reviewed 160+ organizations serving disciplines in the 2nd LOD. Determined

that additional research was needed to further understand IA ‘S current and future

involvement in 2nd LOD

EC Mtg. –Approved Approach – IA’ s Current & Future Role in 2nd LOD

• July 2013

9

globaliia.org

Timeline – Current State

Assessing Roles of IA in 2nd LOD Study

• Aug 2013-March 2014

Global Council & EC Mtg. Input

• March 2014

Recommendation to BOD

• July 2014

Understand the current and future roles of IA as it relates to risk

management, internal control & compliance

This Week

10

globaliia.org

EXPANDED ROLE OF

INTERNAL AUDIT SURVEY

Preliminary Survey Results

globaliia.org

Purpose Survey

Purpose of the Survey

Understand current and future roles of internal audit as

it relates to risk management, internal control and

compliance.

globaliia.org

Expanded Role Survey

Preliminary Results17 February 2014

January – March 2014• Private and Publicly

Traded Companies• 17 Countries• 6 Languages

500 Responses to 17 FEB• 90% IA

• 74% CAE • 95% Members

globaliia.org

Expanded Role Survey

Preliminary Results17 February 2014

Industry %

Manufacturing 18%

Energy &

Resources

12%

Financial

Services

10%

Retail &

Entertainment

9%

Healthcare 4%

Technology 4%

Logistics 3%

Other 3%

PRIMARY INDUSTRY

globaliia.org

Expanded Services Survey

Preliminary Results17 February 2014

Revenue

Less than US $10M 7%

US $10M - US $ 50M 5%

US $50M – US $100M 5%

US $100M - US $500M 12%

US $500M - US $1B 14%

US $1B – US $10B 38%

US $10B+ 19%

Annual Revenue

globaliia.org

Initial Observations

• IA often has an extended role

globaliia.org

Initial Observations

• IA often has an extended role, but usually not

with primary lead responsibility

• IA faces broadly similar challenges across all

three disciplines (risk management, internal

control, compliance)

globaliia.org

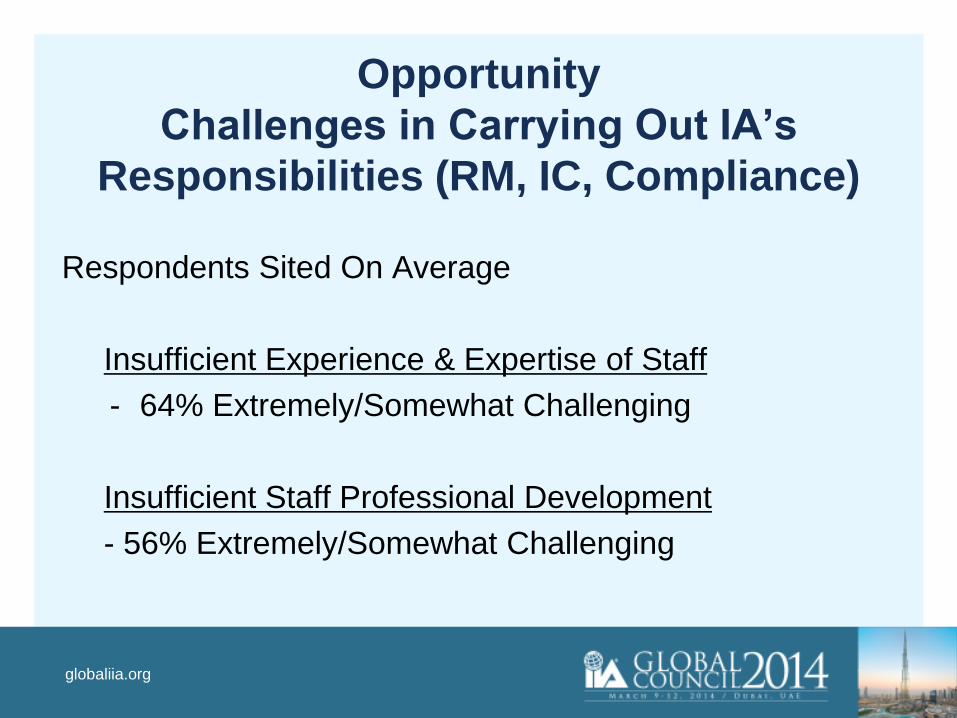

Opportunity

Challenges in Carrying Out IA’s

Responsibilities (RM, IC, Compliance)

Respondents Sited On Average

Insufficient Experience & Expertise of Staff

- 64% Extremely/Somewhat Challenging

Insufficient Staff Professional Development

- 56% Extremely/Somewhat Challenging

globaliia.org

Initial Observations

• IA often has an extended role, but usually not

with primary lead responsibility

• IA faces broadly similar challenges across all

three disciplines (risk management, internal

control, compliance)

• Professionals are interested in subject matter

on each area

globaliia.org

OpportunitiesSubject Matter Information Needed

globaliia.org

High Degree of Confidence in The IIAMuch More Likely to Rely on IIA for Information

IIA

AcctgAssoc

globaliia.org

Initial Observations

• IA often has an extended role, but usually not

with primary lead responsibility

• IA faces broadly similar challenges across all

three disciplines (risk management, internal

control, compliance)

• Professionals are interested in subject matter

on each area

• Increased responsibilities are on the horizon

globaliia.org

Future Changes in

Responsibilities

6.5:1

9:1

20:1

Increase Decrease

globaliia.org

• 13,000+ CRMAs• Demand of CRMA being an indicator for risk management

assurance content

globaliia.org

43% ARE INCREASING THEIR AMOUNT OF EFFORT TO ASSESSING THEIR

ORGANIZATIONS RISK MANAGEMENT EFFECTIVENESS

globaliia.org

44% OF RESPONDENTS INDICATED THAT THEY WERE RECRUITING/BUILDING RISK MANAGEMENT SKILLS FOR THEIR AUDIT

DEPARTMENTS

globaliia.org

10% OF THE AVERAGE AUDIT PLAN IS DEDICATED PROVIDING RISK

MANAGEMENT ASSURANCE

globaliia.org

SUMMARY

• IA’s Role is Expanding in 2nd LoD Disciplines

• Challenge with Insufficient Expertise and

Professional Development

• Demand for Leading Practices,

Benchmarking, Evaluation Tools and

Standards/Guidance.

• Risk Management Potentially Greatest

Opportunity

globaliia.org

Discussion Questions

globaliia.org

Discussion Topic 3:Reassessing the IPPF

Larry Harrington, Vice Chair – Professional Practices

globaliia.org

Drivers

• Regulatory influence

• Local guidance

• Industry specific requirements

• Standards too easy/too hard

• Minimum requirements or aspirational

• Maturity scale

• Forms of guidance, speed to market

globaliia.org

Objectives

• Consider the evolving role of internal audit globally

• Consider the impact of elevating stakeholder

expectations

• Propose updates to the structure of the IPPF that will

encompass existing and developing global and local

guidance to meet the needs of the profession for the

foreseeable future

globaliia.org

Scope

• Definition of Internal Auditing

• Foundational principles

• Direct linkage between standards and guidance

• Need to accommodate

– Industry specific guidance

– Regulations

– Local guidance

• Consideration of maturity models

• Enforcement of Standards

– Conform or explain

• Guidance development responsibilities

globaliia.org

Key Players

• Steering Committee

• Taskforce – global team of IA leaders:• 5 United States

• 4 Europe

• 1 Africa

• 1 Australia

• 1 South America

• 1 Japan

• Project support from Ernst & Young

– Global Internal Audit Leader actively engaged

• IIA Staff Support

globaliia.org

Progress to Date

• November 1-2, 2013 Taskforce meeting in Chicago

– Conceptual framework identified

– Taskforce to develop new Definition recommendations

established

• February 6-7, 2014 Taskforce meeting in Dallas

– New definition drafted, minor work remaining

– Conceptual framework modified, refinement continues

– Principles of Internal Audit Effectiveness developed,

mapping of Standards to Principles in process

globaliia.org

Proposed New Definition

• Current Definition:

– Internal auditing is an independent, objective assurance and

consulting activity designed to add value and improve an

organization's operations. It helps an organization

accomplish its objectives by bringing a systematic,

disciplined approach to evaluate and improve the

effectiveness of risk management, control, and governance

processes. (45 words)

• Proposed Definition:

– Internal auditing is an objective assurance activity that

benefits an organization by providing independent

evaluations, advice, and insight on governance, risk

management and internal control. (25 words)

globaliia.org

Current Framework

globaliia.org

Proposed Framework

Definition of Internal Auditing

Principles and Attributes of Internal Audit Effectiveness

CODE

OF

ETHICS

International Standards for the Professional Practice of Internal Auditing

(The Standards)

Interpretations to Support The Standards

Implementation Guidance

Supplemental Guidance

REQUIRED

RECOMMENDED

globaliia.org

Proposed Framework

Definition of Internal Auditing

Principles and Attributes of Internal Audit Effectiveness

CODE

OF

ETHICS

International Standards for the Professional Practice of Internal Auditing(The Standards)

Interpretations to Support The Standards

Implementation Guidance

Supplemental Guidance

REQUIRED

RECOMMENDED

globaliia.org

Principles of Internal Audit

Effectiveness

• 12 Principles:

– 3 about the individual

– 6 about the function

– 3 about the outputs/outcomes from the function

globaliia.org

Principles of Internal Audit

Effectiveness1. Demonstrates uncompromised integrity.

2. Is objective in mind-set and approach.

3. Demonstrates commitment to ensuring competency of the entire internal audit activity.

4. Is appropriately positioned within the organization with sufficient organizational

authority.

5. Is aligned strategically with the aims and goals of the enterprise.

6. Is sufficiently resourced to evaluate all significant risks.

7. Is committed to quality and continuous improvement within the internal audit activity.

8. Is efficient and effective in execution of all activities.

9. Is effective in communicating.

10.Provides reliable assurance to those charged with governance over the enterprise.

11.Is proactive, anticipatory and future-focused.

12.Enables positive change.

globaliia.org

Timeline

• At its most aggressive …

– Anticipate seeking Board approval for exposure of

proposed framework at International Conference in July

– Receive and address exposure comments in second half

of 2014

– Final Board approval of new framework in December

2014

– Population of new framework in 2015

– New framework released January 2016

globaliia.org

We Would Like Your Input

• Discussion questions in the Background Paper:

1. What is the current adoption rate of the Standards in your

area of the world?

2. What, if anything, is preventing adoption by practitioners of

the Standards, as well as the entire IPPF, in your country?

3. What are the strengths and weaknesses of the current

IPPF structure?

4. Are you aware of any areas where government agencies

have regulated, codified, or adopted any part of the IPPF

into regulation, statute or law?

globaliia.org

We Would Like Your Input

• Discussion questions in the Background Paper:

5. Are you aware of specific guidance that has been

published that goes beyond the Standards or the IPPF that

impact how internal auditing is to be conducted?

6. Based on your experience, are those charged with

governance knowledgeable of the Standards?

7. If the Definition of Internal Audit and/or the structure of the

IPPF were changed, how much of an impact, if any, would

that create in your country?

globaliia.org

We Would Like Your Input

• As well, any reactions you have to the “work-in-

process”:

– Definition

– Framework

– Principles

• Additionally, if your Institute is publishing local

guidance, please share that with your table facilitator

globaliia.org

Break andDiscussion #3

globaliia.org

Discussion Topic 4:Membership Value Proposition

Harold Silverman, Vice-Chair, Global Services

globaliia.org

Background

• Relevant IIA’s Global Strategic Plan – Goal B

The IIA will deliver the value that compels current, future, and

former internal auditors to be members.

• Initiatives so far:

– Alternative Member Servicing Models to support new or struggling

Institutes, launched in 2014

– The “Umbrella Project” to address the needs of related professionals in the

field of risk management, control, and governance, first discussed at Global

Council 2013. A study is underway to better understand the current state of

affairs.

• To date, The IIA has never undertaken a worldwide initiative to

specifically focus on the value proposition of membership.

globaliia.org

2014 Global Council

Discussions Focus

• Whether all Institutes are meeting the needs of internal audit

professionals and what gaps may exist.

• What programs and services should be implemented to support

and strengthen small and newer Institutes.

• Whether service delivery and membership benefits models in place

are maximizing Institutes’ ability to recruit and retain members.

• Whether additional opportunities exist to better serve the needs of:

– Specific sectors within the internal audit activity.

– Internal audit professionals who rotate out of the profession.

– The student population.

globaliia.org

Discussion Questions

1. What strategies does your Institute use to recruit and retain

members? Please explain if these strategies have been

effective or not.

2. What programs and services, if any, should The IIA develop to

support small and newer Institutes? What role, if any, should the

mature Institutes and regional organization play?

globaliia.org

Discussion Questions

3. What is your biggest challenge regarding membership

recruitment and retention?

4. If inability to offer value-added and tangible services is ranked

high, please explain the reasons.

globaliia.org

Discussion Questions

5. What key strategies, if any, should The IIA use to help:

– Increase the membership value proposition on a global

basis?

– Grow membership on a global basis?

– Diversify membership on a global basis?

6. On a global basis, what is the most important strategy The IIA

should focus on?

7. To support a global strategy regarding membership, do you see

the value of all Institutes participating in coordinated

membership recruitment, retention, and/or diversification efforts?

globaliia.org

BREAK

globaliia.org

Feedback Forum

globaliia.org

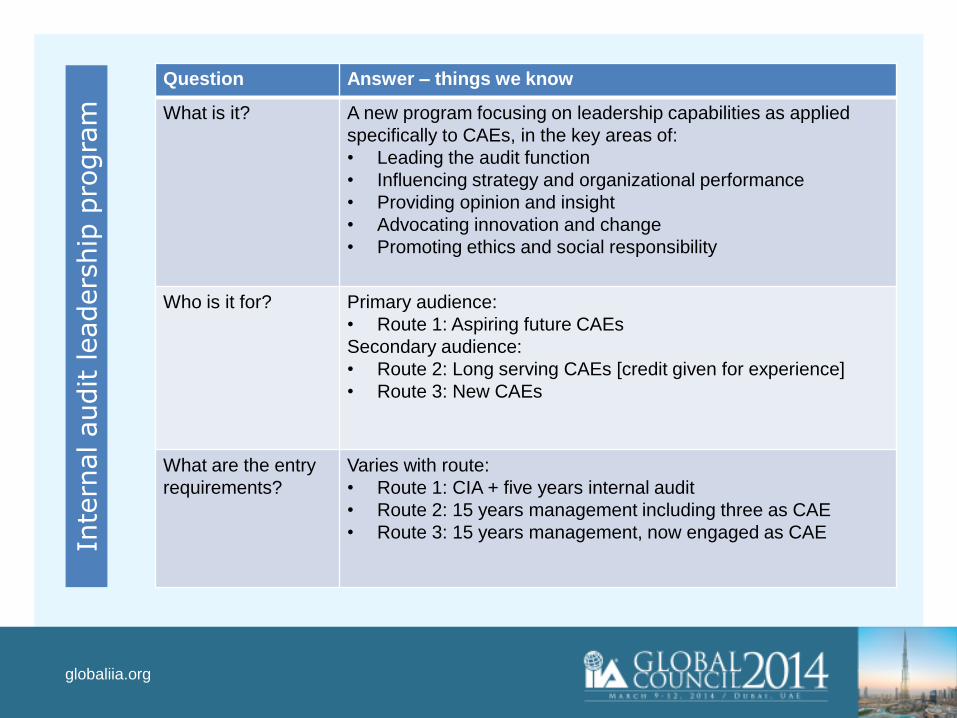

INTERNAL AUDIT

LEADERSHIP PROGRAM

Francis Nicholson, Managing Director of Certifications & Global

Strategic Initiatives

globaliia.org

Question Answer – things we know

What is it? A new program focusing on leadership capabilities as applied

specifically to CAEs, in the key areas of:

• Leading the audit function

• Influencing strategy and organizational performance

• Providing opinion and insight

• Advocating innovation and change

• Promoting ethics and social responsibility

Who is it for? Primary audience:

• Route 1: Aspiring future CAEs

Secondary audience:

• Route 2: Long serving CAEs [credit given for experience]

• Route 3: New CAEs

What are the entry

requirements?

Varies with route:

• Route 1: CIA + five years internal audit

• Route 2: 15 years management including three as CAE

• Route 3: 15 years management, now engaged as CAE

Inte

rnal audit leaders

hip

pro

gra

m

globaliia.org

Question Answer – things we know

How is it assessed? Assessing knowledge, understanding and behavior:

• Three written exams of between 3-4 hours each

• Presentation to a panel followed by questions

• 90-minute panel interview

Who’s on the

panel?

Experienced CAEs who have completed the new program

In what countries? • Exams will be available on-line globally

• Assessment for presentations and interviews will be

available face to face and via WebEx

In what languages? English only at launch with no immediate plans to translate to

other languages (but longer term, subject to demand)

When will it be

available?

Announced July 2014

First exams Autumn 2014

First presentation and interviews December 2014Inte

rnal audit leaders

hip

pro

gra

m

globaliia.org

Question Answer – not yet known

What is it called? • Clear, unambiguous and readily understood globally

• Reflect its uniqueness AND its place within the suite

• Will be abbreviated to a set of initials as a short-form title

and as designatory letters (like CIA, CRMA, CFSA etc)

The name will include:

• ONE of the following:

o “Certification”, OR

o “Certified”, OR

o “Qualification”, OR

o “Qualified”

• EITHER “Audit” OR “Internal Audit”

• EITHER “Leadership” OR “Leader”

What is the fee? • Delivery costs are significantly higher than the CIA

• Costs vary according to volumes and delivery models

• Fee must reflect the value Inte

rnal audit leaders

hip

pro

gra

m

globaliia.org

CBOK 2015

Margie Bastolla, Vice President - IIA Research Foundation

globaliia.org

ALTERNATIVE MEMBER

SERVICING MODEL

Richard Chambers, President and CEO

globaliia.org

Gifts and Closing Session

globaliia.org

Agenda - Wednesday

Tour (for delegates and guests) of Old City Dubai

Lunch

Leave hotel by bus at 8.30

Return to hotel by 16.15

globaliia.org

Thank You