dsa project – planning reform regional competitiveness in the snnpr– the preliminary study...

TRANSCRIPT

DSA

Pro

ject

– P

lannin

g

Refo

rm

Regional Competitiveness in the SNNPR– the preliminary study

Regional Economic Policy Review

Perran PenroseDecember 2004

2D

SA

Pro

ject

– P

lannin

g

Refo

rmDSA Project

• The DSA project has been working with the SNNPRS Bureau of Finance and Economic Development for several years to support the development of a modern budget system‘transaction reforms’ to reform the

budget and accounting system‘planning reforms’ to strengthen the way

budgetary allocations are made

3D

SA

Pro

ject

– P

lannin

g

Refo

rmREPR

• In August 2004 the DSA Project undertook a Regional Economic Policy Review in the Southern Region of Ethiopia

•To put a spotlight on economic growth, and consider how the Region can enhance its competitiveness in order to stimulate growth

• The role of BOFED coordinating economic development and the budget in growth strategy

Objective Focus

4D

SA

Pro

ject

– P

lannin

g

Refo

rm

Background and objectives of this presentation

• SNNPR is in a ‘low-level equilibrium trap’, with stagnating per capita GDP, volatile growth, little evidence of growth impetus in the economy, and little sign that small scale industry is making a material contribution

• Greater realisation that increasing competitiveness should be a core goal of developing countries

Background Key consideration

• Discuss the role of the SNNPR in contributing to Ethiopia’s growth through greater competitiveness

Objective of this presentation …

5D

SA

Pro

ject

– P

lannin

g

Refo

rm

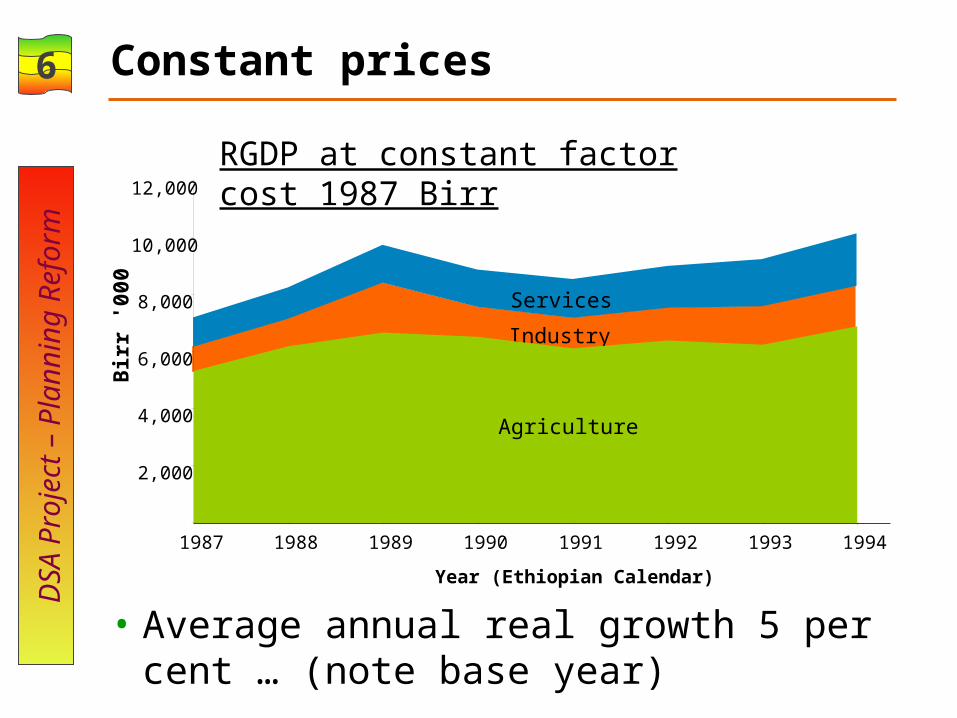

Regional Gross Domestic Product

What do the data tell us?

6D

SA

Pro

ject

– P

lannin

g

Refo

rmConstant prices

RGDP at constant factor cost 1987 Birr

Industry

Services

• Average annual real growth 5 per cent … (note base year)

Agriculture

2,000

4,000

6,000

8,000

10,000

12,000

Bir

r '0

00

1987 1988 1989 1990 1991 1992 1993 1994

Year (Ethiopian Calendar)

7D

SA

Pro

ject

– P

lannin

g

Refo

rmCurrent prices

1988 1989 1990 1991 1992 1993 1994

Year (Ethiopian Calendar)

2,000

4,000

6,000

8,000

10,000

12,000

1987

Bir

r '0

00

Agriculture

Industry

Services

RGDP at current factor cost

• Average annual nominal growth 4 per cent … (note base year)

8D

SA

Pro

ject

– P

lannin

g

Refo

rmPer capita RGDP trends

• But per capita output is stagnant (choice of base year does not make much difference!!)

100

200

300

400

500

600

700

800

900

1987 1988 1989 1990 1991 1992 1993 1994

Per capita RGDP at constant 1987 pricesPer capita RGDP at current prices

9D

SA

Pro

ject

– P

lannin

g

Refo

rmTrend of sectoral shares

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1987 1994 Constant

Agr

icu

ltu

re

Industry

Services

Agr

icu

ltu

re

Industry

Services

• Apparent shift of shares away from agriculture – but main factor has been the movement in relative prices

1994 Current

Agr

icu

ltu

re

Industry

Services

10D

SA

Pro

ject

– P

lannin

g

Refo

rmSub-sector shares in RGDP

• Urbanisation & growth in service sectors not underpinned by primary & secondary sectors

0.6 0.4 Health

2.9 2.2 Education

2.2 1.8 Public Administration

4.9 3.5 Real estates & dwellings

6.5 1.1 Transport & communications

23.514.2Services, of which selected sub-components:

9.5 7.7 Construction

2.7 2.1 Cottage & handicraft

0.8 0.7 Small

0.3 0.3 Large and medium

3.8 3.1 Manufacturing, of which

15.212.4Industry, of which selected sub-components:

19941987

5.7

4.4

?

11D

SA

Pro

ject

– P

lannin

g

Refo

rmSummary of RGDP analysis

• Stagnant trend (output barely exceeds population growth)

• Poor performance in agriculture, considerable volatility in agriculture outputimpact of climate and coffee price dominant

• Pattern of growth (expansion of service sectors not underpinned by manufacturing sector growth) not sustainable in the longer run

• It follows that there has been a very limited impact of government development programmes

12D

SA

Pro

ject

– P

lannin

g

Refo

rm

Current targets & policy conclusions• Current growth targets are not realistic

Target = double RGDP in 5 years

• Agriculture accounts for over 60 per cent of RGDP,but a realistic projection would be that agriculture

will not grow much faster than the population (little possibility of increasing teff productivity) – say average 3% pa. 4 – 5 per cent agriculture growth per year would be a significant achievement (ie higher than population growth)

• To achieve 15 - 20 per cent RGDP growth per year would require dynamic sectors to grow at 30 – 40 per cent. This is not realistic.

13D

SA

Pro

ject

– P

lannin

g

Refo

rmWhere will growth come from?

• Agriculture growthincrease yields of existing cropsintroduce new cropsinnovations in on and off-farm post

harvest processing

• Small scale and cottage industry, services related to agriculture

• Industrial production for extra-regional markets; tourism

• We will discuss some of these later.

14D

SA

Pro

ject

– P

lannin

g

Refo

rm

Regional Competitiveness

some general principles & approaches

15D

SA

Pro

ject

– P

lannin

g

Refo

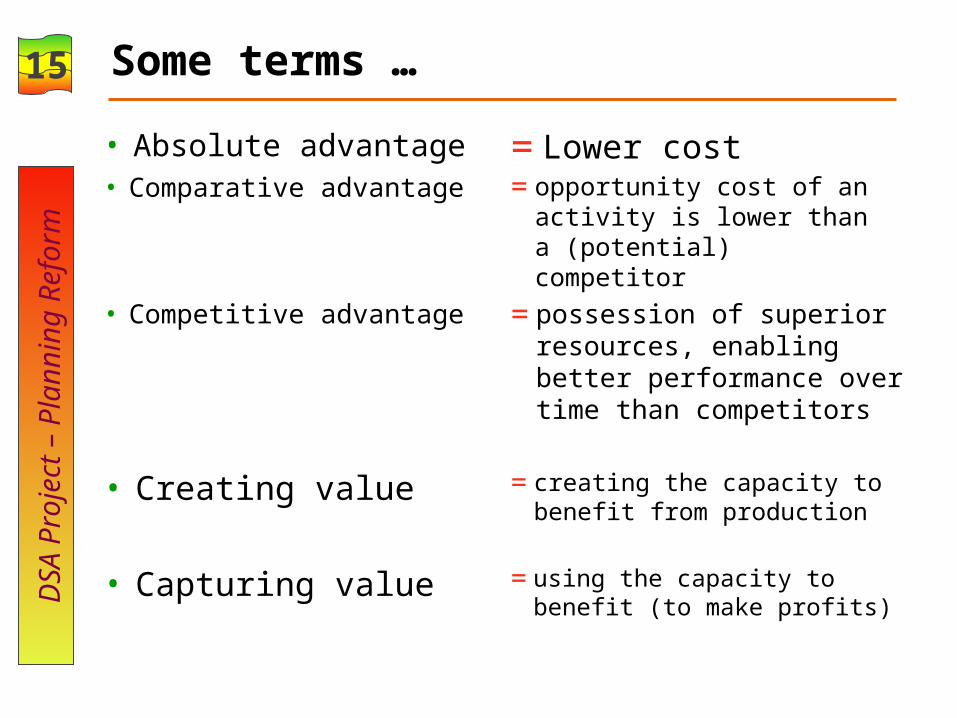

rmSome terms …

• Absolute advantage =Lower cost=opportunity cost of an

activity is lower than a (potential) competitor

• Comparative advantage

• Competitive advantage =possession of superior resources, enabling better performance over time than competitors

• Creating value =creating the capacity to benefit from production

• Capturing value =using the capacity to benefit (to make profits)

16D

SA

Pro

ject

– P

lannin

g

Refo

rm

ASSESSMENT

Country

Competitiveness

Drivers

Industry/Sectoral Competitiveness

Company/Product Competitiveness

•What are the country’s natural comparative advantages?

•What are the prioritized industries and their objectives?

•What are the companies’ strategies and their unique value propositions in relation to domestic and international competitors?

Overview of competitiveness framework & key questions

Regional Competitiveness•What are the priorities of a region

Source: Adapted from A.T.Kearney

•What roles can the public sector play to improve and sustain industry competitiveness?

•What discretion does the region have over its competitiveness drivers?

•What are some of the country’s relative disadvantages when assessed for investment opportunities?

•What are the critical factors to support the nation’s strategy to international competitiveness and how can these be improved?

17D

SA

Pro

ject

– P

lannin

g

Refo

rm

What is required for SNNPR competitiveness & growth?

• Innovation to improve the value of output

• Roads• Water

Innovation Physical Infrastructure

• Small scale industry & agriculture services

• Industrial production for extra-regional markets

• Tourism

Industry

• increase yields of existing crops

• introduce new crops• post harvest processing

(on & off farm)

Agriculture

• Credit• Skills

Human & financial infrastructure

+

18D

SA

Pro

ject

– P

lannin

g

Refo

rm

Infrastructure

Unit cost economics

Human resources

Technology & innovation

Productivity – Value

Wealth

The productivity – competitiveness wheel

Source: Christos Pitelis, Judge Management Institute, Cambridge

19D

SA

Pro

ject

– P

lannin

g

Refo

rm

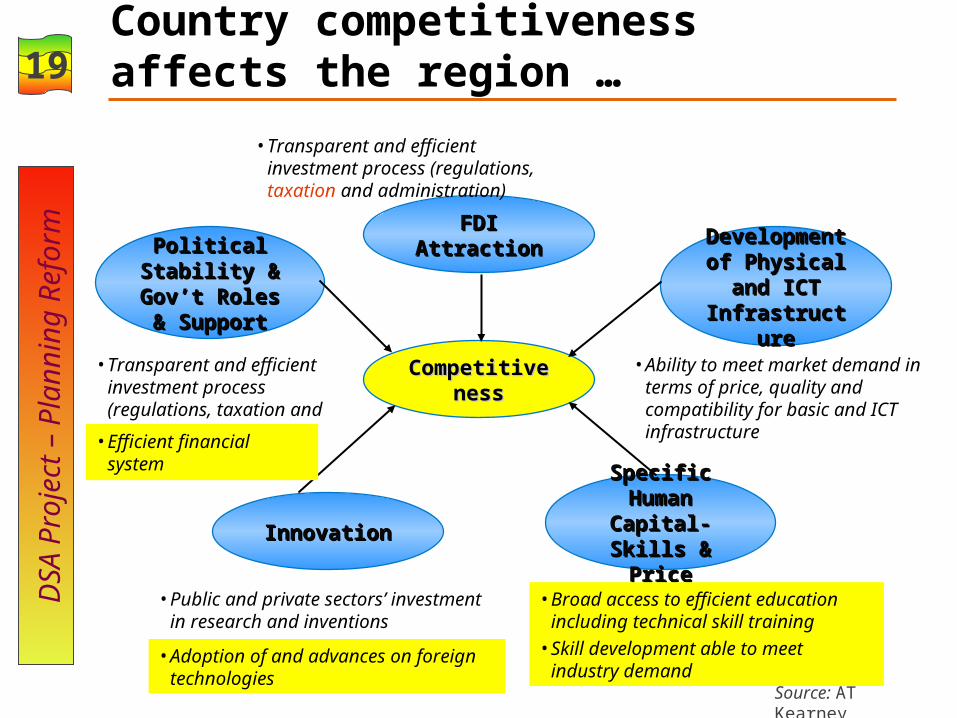

CompetitivenessCompetitiveness

FDI AttractionFDI AttractionDevelopment of Development of

Physical and Physical and ICT ICT

InfrastructureInfrastructure

Political Political Stability & Stability &

Gov’t Roles & Gov’t Roles & SupportSupport

InnovationInnovation

Specific Human Specific Human Capital- Skills Capital- Skills

& Price& Price

• Ability to meet market demand in terms of price, quality and compatibility for basic and ICT infrastructure

• Transparent and efficient investment process (regulations, taxation and administration)

• Broad access to efficient education including technical skill training

• Skill development able to meet industry demand

• Public and private sectors’ investment in research and inventions

• Transparent and efficient investment process (regulations, taxation and administration)

Country competitiveness affects the region …

Source: AT Kearney

• Efficient financial system

• Adoption of and advances on foreign technologies

20D

SA

Pro

ject

– P

lannin

g

Refo

rm

SNNPR & Competitiveness

21D

SA

Pro

ject

– P

lannin

g

Refo

rm

• AnalysisComparative advantage

competitive advantageDifferentiation & focusLinkages, clusters, innovationOwnership structure

• Action plans linked to resource allocation & selected strategic targets

SNNPR & competitiveness / growth

22D

SA

Pro

ject

– P

lannin

g

Refo

rm

Comparative advantage, differentiation, focus

• Comparative advantage in (‘commercial’) agriculturecoffeespiceshides & skinsdairy

• Action plan – how to turn these advantages to competitive advantage?Development of a regional policyRoads, irrigation, local processing capacityFocus on innovation rather than ‘across the

board’ extensionFarmer support institutions

23D

SA

Pro

ject

– P

lannin

g

Refo

rm

Comparative advantage, differentiation, focus

• Comparative advantages in tourismEco tourismWild life (birds, game reserves)Sport (fishing, rafting)Ethnic groups

• How to create ‘destination competitiveness’?Infrastructure (roads, accommodation)Price competition (high costs of travel)Ancillary services (tour operators, car rental)Tax incentives (import duties for tour

operators)Public private partnerships

24D

SA

Pro

ject

– P

lannin

g

Refo

rm

Comparative advantage, differentiation, focus

•Comparative advantage in manufacturing …Large scale manufacturing not regionally

based, loss making / low quality SOEs run from Addis Ababa, skilled but disempowered local management

•Creation of local linkages textiles and local cotton, coffee production and processingdairy(chat?)

25D

SA

Pro

ject

– P

lannin

g

Refo

rmClusters

• Raise productivity by allowing access to specialised inputs and employees, information, institutions and public goods (education, security)

• Increase capacity for innovation by more rapid diffusion of technology and innovation

• Stimulate higher rates of business formation• Cooperatives are a form of cluster

• Next step – to undertake an ‘audit’ of stakeholders along selected value chains together with strengthening existing coordinating body or creating a new one

26D

SA

Pro

ject

– P

lannin

g

Refo

rm

Growth & Agriculture

27D

SA

Pro

ject

– P

lannin

g

Refo

rmImportance of agriculture

• The ideas of competitive advantage may be most applicable to commercialised agriculture and agriculture processing

• The region also needs to address the constraints on small-scale peasant agriculture

• Some recent government policy changes are positiveEncouragement to expand exportsCooperatives seen as essential for marketing

commodities‘Non-peasant’ commercial farms encouraged

through land allocation and infrastructure development

28D

SA

Pro

ject

– P

lannin

g

Refo

rmRegional policy

• The Region does not have its own distinctive policy for agriculture although it has its own characteristics and wide diversity

29D

SA

Pro

ject

– P

lannin

g

Refo

rm

Why a regional agriculture policy?• Decisions on effective measures to

increase value added are best made as locally as possible

• Current extension methods (assisting individual farmers and groups of farmers) may not be the best use of public money, and more detailed area analysis is needed leading to more targeted resources. This involves classification of the full set of potential instruments available at each level.

30D

SA

Pro

ject

– P

lannin

g

Refo

rm

Development of a regional policy

•federal policies and legislation (eg land holding, marketing systems, financial institutions, grades & standards, cooperatives)

•federal institutions (eg DPPC)•federal development programmes across

regions•marketing chains extending beyond regional

boundaries

• Dialogue required with various stakeholders in order to deal with constraints …

Constraints on development of a distinct regional policy

31D

SA

Pro

ject

– P

lannin

g

Refo

rm

Increasing the value of farm output• Agriculture growth normally measured at

constant prices to assess physical output• Price increases bring greater benefits to

producer households, but may have adverse effects on food security

• Increase the weight or volume of existing crops

• Raise unit values of existing crops• Substitution of one crop for another

Three ways of increasing value of farm output

32D

SA

Pro

ject

– P

lannin

g

Refo

rm

1. Increase output of existing crops

• Increased use of inputspresent extremely low

use of purchased inputs – 4.4% of gross value of production in 1992; only 14,000 tons in region (12 tons on coffee in Gedeo!); little use of improved seed.

Low availability of inputs, low rural savings, inflexible publicly planned

marketing systems …

• improved storage (at present about 30% wastage)

• irrigation – in SNNPR 21,000 ha irrigated out of 1.4 million ha cultivated (1.4 per cent)

• adding a crop cycle

• inter-planting

Increased yield per area Increased planted area

33D

SA

Pro

ject

– P

lannin

g

Refo

rm2. Raising producer prices

• improves storage• improved

efficiency in marketing & processing (lowering net margins and shifting benefit to producer)

Increase in price for a particular

quality • improved pest & disease control

• post-harvest technology improvement (threshing of teff, drying of coffee)

• Investment (solid threshing floors, unwashed coffee drying tables)

Produce and sell higher qualities

34D

SA

Pro

ject

– P

lannin

g

Refo

rm3. Switching between crops

• Over the long term introduction of new crops has been the main source of agriculture output growth in sub-Saharan Africa

• Only evidence (apart from chat) of switching in SNNPR is to coffee (not through innovation but through government policy)Only innovations have been washed

processing & organisation in cooperatives

35D

SA

Pro

ject

– P

lannin

g

Refo

rm

Agriculture: Some policy activities …

36D

SA

Pro

ject

– P

lannin

g

Refo

rmInnovation & infrastructure

• Need for innovation to improve the value of output should be the focus for extensionSome reorientation of regional budget policies

(in particular a better focus on expenditures that stimulate agriculture growth

• Strong government support for infrastructure (particularly roads and water)

• Sequential development of lowlands and a better balance between high / mid altitude zones and lowlands

37D

SA

Pro

ject

– P

lannin

g

Refo

rmPost-harvest technology

• large scale destruction of value through physical losses deterioration in quality

• fear of losses increases intensity of market gluts leading to low prices

Improved post-harvest technologies

and storage • communal storage facilities and grain banks

• micro-finance institutions lending for investment in post-harvest technologies

• household subsidies for materials for improved on-farm post harvest infrastructure

Financial support could be provided for:

-

38D

SA

Pro

ject

– P

lannin

g

Refo

rm

What is required? Milk production & marketing

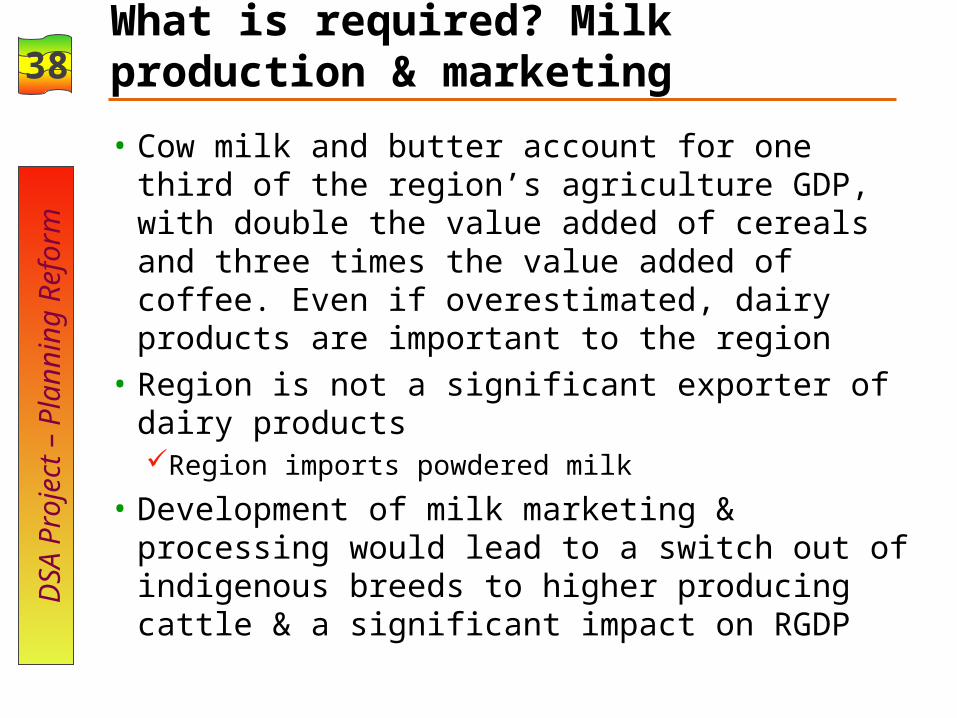

• Cow milk and butter account for one third of the region’s agriculture GDP, with double the value added of cereals and three times the value added of coffee. Even if overestimated, dairy products are important to the region

• Region is not a significant exporter of dairy productsRegion imports powdered milk

• Development of milk marketing & processing would lead to a switch out of indigenous breeds to higher producing cattle & a significant impact on RGDP

39D

SA

Pro

ject

– P

lannin

g

Refo

rmCoffee

• 10 year Coffee Development & Marketing Plan could have an adverse affect on the SNNPR because of the switch from unwashed to washed processing – SNNPR the only region in which most coffee is washedReduced premia on washed coffee Increase in over-capacity in primary processing in

the region, raising unit costs and reducing producer prices

Increased processing in cooperatives could raise costs vs maintaining the trend towards private sector processing

Large scale washed processing methods may not be in the region’s interest – small scale semi-washed processing reduces pollution & would increase value in some areas

40D

SA

Pro

ject

– P

lannin

g

Refo

rmCoffee

• Regional Inspection and Quality Certification Centres (RIQCCs) will create greater market efficiencyincreased incentives to improve qualityprocessors will gain confidence in the quality of

the cherry they have bought and enter into forward contracts

regional coffee would be sold by sample at the Addis Ababa auctions, obviating the long delays and trucking journeys

• Regional government must be fully involved in the planning and siting of the RIQCCs

41D

SA

Pro

ject

– P

lannin

g

Refo

rm

Public Finance Management for Competitiveness

and Growth

42D

SA

Pro

ject

– P

lannin

g

Refo

rmDecentralised?

• Can regions change federal policies?• Can regions adapt federal policies?• What public finance management

discretion does a region have?• Need for strong federal – regional

dialogue• Therefore need to clarify which growth

policy instruments …are under federal government discretionare under regional government discretioncan be transferred from federal to regional

government

43D

SA

Pro

ject

– P

lannin

g

Refo

rmTargets

• Little point in presenting detailed year on year growth targetsMuch projected growth autonomous &

unpredictable, andit is unclear who is responsible

• Set indicative medium term targets for broad aggregates, but be clear where accountability / discretion lies

• BOFED needs to play a more creative role on top of routine allocation activities

44D

SA

Pro

ject

– P

lannin

g

Refo

rmCapital budget

• Most significant & direct impact on growth within government discretion is the capital budget

• Main issue is the composition of the capital budget, which may be influenced more by ‘capacity building’ than growth considerationshave public sector interventions leading to

economic growth been neglected? region arguably has little real discretion on

major investments from its ‘own’ budget, hence creating a potentially serious constraint on using the public sector for growth

offset system still requires reform

45D

SA

Pro

ject

– P

lannin

g

Refo

rm

Investment planning – what needs to be done?

• Identify strategic interventions with the objective of raising growth and competitiveness, coupled with selective indicators

• More technical analysis of the relative returns to different types of investment – this is a serious deficiency in Ethiopian public investment planning

• Is infrastructure spending sufficient?

46D

SA

Pro

ject

– P

lannin

g

Refo

rmInvestment planning …

• What types of analysis do we need? An example if analysis underpinning priorities in Viet Nam … Similar analysis lacking in Ethiopia?

47D

SA

Pro

ject

– P

lannin

g

Refo

rm

Recurrent budget and strategic intervention

• Subsidies (distribution of economic rent)selection of potential incentives

• Identify performance criteria for key regional ‘growth’ bureausneed to identify innovation opportunities

• Better scrutiny of sectoral allocations to increase allocative efficiency

48D

SA

Pro

ject

– P

lannin

g

Refo

rm

Next steps

49D

SA

Pro

ject

– P

lannin

g

Refo

rm

Operationalise the REPR – ‘commercial’ sectors• What can be included in the 1998 - 2000 PEP?

First step

policy commitment from BOFED / regional cabinet

Second step

identification of key production and marketing opportunities, leading to active clustering policies

• identification of key production and marketing opportunities, leading to active clustering policies

• agriculture – milk, high value crops, coffee innovation, …

• tourism & manufacturing

• infrastructure• …. ?