dr. chhiv s. thet: "macroeconomic & financial development-cambodia"

DESCRIPTION

Macroeconomic Development-CambodiaFinancial Development-CambodiaFinancial and Economic System Development-CambodiaTRANSCRIPT

1

Macroeconomic and Financial

Development in Cambodia

Dr. Chhiv S. Thet

Phnom Penh, November 2013

1

Macroeconomic and Financial Development

in Cambodia

By

Dr. Chhiv S. Thet,

Phnom Penh, November, 2013

2

Table of Contents

Part I: Economic and Financial System

1. Economic and financial system of Cambodia

2. Dollarization and Macroeconomic Policy of Cambodia

3. Cambodia Macroeconomic and Economic Growth

3.1 Cambodia Economy Framework

3.2 Agriculture Sector

3.3 Industrial Sector

3.4 Capital Investment

3.5 External Trade

3.6 Inflation and Exchange Rate

3.7 Budget Implementation

Part II: Development of Cambodia Financial Markets

1. Securities Exchange Commission of Cambodia

2. Securities Market of Cambodia

3. Challenges of the Financial Markets Development

3.1 Banking System

3.2 Capital Markets Development of Cambodia

3.3 Governance and Legal Framework and Regulations

3.4 Risk and Other Challenges

2

Macroeconomic and Financial Development

in Cambodia

By

Dr. Chhiv S. Thet,

Phnom Penh, November, 2013

3

PART I

1. Economic and Financial System of Cambodia

The kingdom of Cambodia is currently carrying out the free market economic

system as mentioned in the national institution1. The organizations of economy and taxation

are put into operation within relevant laws and regulations. Cambodia's two largest industries

are textiles and tourism, and agriculture remains the main source of income for country. The

service sector is heavily concentrated on trading activities and catering-related services.

Recently, Cambodia has reported that oil and natural gas reserves have been found off-shore.

In 1995, the government transformed the country's economic system from a planned

economy to its present market-driven system. Currently, Cambodia's foreign policy was

integrated into the regional (ASEAN) and global trading systems (WTO). Some of the

obstacles faced by this emerging economy are the need for a better education system and the

lack of a skilled workforce; particularly in the poverty-ridden countryside, which struggles

with inadequate infrastructure. Nonetheless, Cambodia continues to attract investors because

of its low wages, plentiful labor, proximity to Asian raw materials, and favorable tax

treatment.

The component of current financial system of Cambodia consists of: (1) banking

system: the national bank of Cambodia “center bank” with their 19 branches and commercial

banks, specialized banks and microfinance institutions and (2) insurance companies. Both

organizations support the financial system of Cambodia. However, Cambodian financial

system is still fragile; it cannot provide financing to people for cultivation, commerce and

rural business enterprises. Therefore, in order to strengthen the financial system, Government

has set out the financial development strategies which focused on the financial market

development, especially, the capital market development to sustain the financial system of

1 Constitution of the Kingdom of Cambodia, chapter 5, article 56

3

4

Cambodia. This is new mechanism and alternative for private and public institutions aiming

to raise funds from the capital markets, besides the banking system.

2. Dollarization and Macroeconomic Policy of Cambodia

In 1991-1992, the United Nations Transitional Authority in Cambodia (UNTAC)

was one of the largest and most expensive operations in the UN history, at a cost of USD 1.7

billion. US dollars flooded the economy, creating a new shock against the national currency,

which the National Bank of Cambodia was not prepared to cope with. Subsequently, the

central bank and the unique commercial bank handled all the UNTAC operations and

received growing foreign currency deposits. Dollarization did not result from a policy

decision. It emerged because confidence of the public in the national currency and in the

government policy was eroded.

Figure 1: Bank deposits in USD and Riel

4

5

In the early 1990s, while tax revenues were very limited due to inactive economy,

low profile of the fiscal policy and lack of international support, the budget was mainly

financing by the central bank. The money supply (M2) swelled by 241% in 1990, 29% in

1991, and above 200% in 1992. This resulted in a sharp devaluation of the riel (Cambodian

Currency) and in a three-digit hyperinflation which created an additional shock for potential

users of the riel.

The dollar has been widely used since 1993, until now, dollarization persists despite

the economic and political stability since 1999, indicating an influence of market

expectations on the choice of currency used in Cambodian economy. Due to the lack of

public confidence in the riel, dollarization has helped in maintaining payment capabilities in

Cambodia. First, introduction of large quantities of banknotes in dollars and allowed the

people to switch from using gold to banknotes for transactions and to store wealth. Until then,

using unproductive physical assets such as gold was common practice in Cambodia.

Subsequently, the progress of monetization has encouraged savings within the middle class.

Second, dollarization has prevented capital/fund flight from Cambodia and encouraged to

deepen the financial system. The elimination of incentives to place savings abroad

encouraged the domestic financial intermediation, which resulted in the growth of the

financial system. Third, dollarization lowered the risk of currency devaluation. The demand

for riel remained low and the market very small. Hence there was little incentive for

speculators to try to gain from short term changes in the price of riel. Dollarization has

protected Cambodia against contagion in the face of the Asian crisis (1997-2000). It sustained

confidence of investors in their operations. Fourth, dollarization promoted awareness by

policymakers of the need to avoid bank financing of public deficits. Eventually, the use of

dollar facilitated to integrate Cambodian trade in the international economy. The currency

5

6

stability promoted macroeconomic stability and a predictable business environment. It

reduced the transaction costs and allowed the boom in the garment industry in Cambodia.

However, there are disadvantages in dollarization. First, it undermines the effective

conduct of monetary policy. The National Bank of Cambodia cannot develop instruments of

monetary policy and its role of lender for banks facing liquidity problems is greatly

constrained. Second, the national currency may appear as a symbol of sovereignty and

nationhood. Third, the income from seignorage is minimized. US government gains

seignorage benefits from Cambodia, since the dollar denominated in Cambodia and does not

earn interest.

3. Cambodia Macroeconomic and Economic Growth

The major principal was used in the economic performance in 2011-2013 is based on

production function in real economic sector, effective tax rate in the fiscal policy and money

velocity in the monetary policy. According to primary estimation of National Institute of

Statistics of the Ministry of Planning, it illustrates that real economic growth rate will be

0.1% at constant price and its deflation index will be 2.6% in 2009. The growth supported by

good performance in agriculture and service sectors at 5.4% and 2.3% respectively, offsetting

the decline in other sectors such as industry, especially the garment sector which dropped by

9%. In the year 2010, the Economic and Public Finance Policy Department of the Ministry of

Economy and Finance estimated that the real economic growth rate will approximately

flourish by 5% at constant price and its deflation index will be 4.8%. The real economic

growth rate will, in the period of 2011-2013, increasingly average by 6.3% per annum.

3.1 Cambodia Economy Framework

The economic growth will probably be at 6% at constant price and its deflation

estimated to be 2.9%. This is, in fact, based on global economic recovery from worldwide

financial crisis as well as recovery of Cambodian economy, especially, tourism and

6

7

agriculture sector. Overall the forecasted growth needs more investment capital about 3,023

million USD or around 24.2% of GDP in which public investment is approximately 841

million USD, domestic private investment is 1,505 million USD and foreign direct

investment is 676 million USD. The real economic growth rate, thus, will be responding to

the objectives designed in the National Sustainable Development Plan.

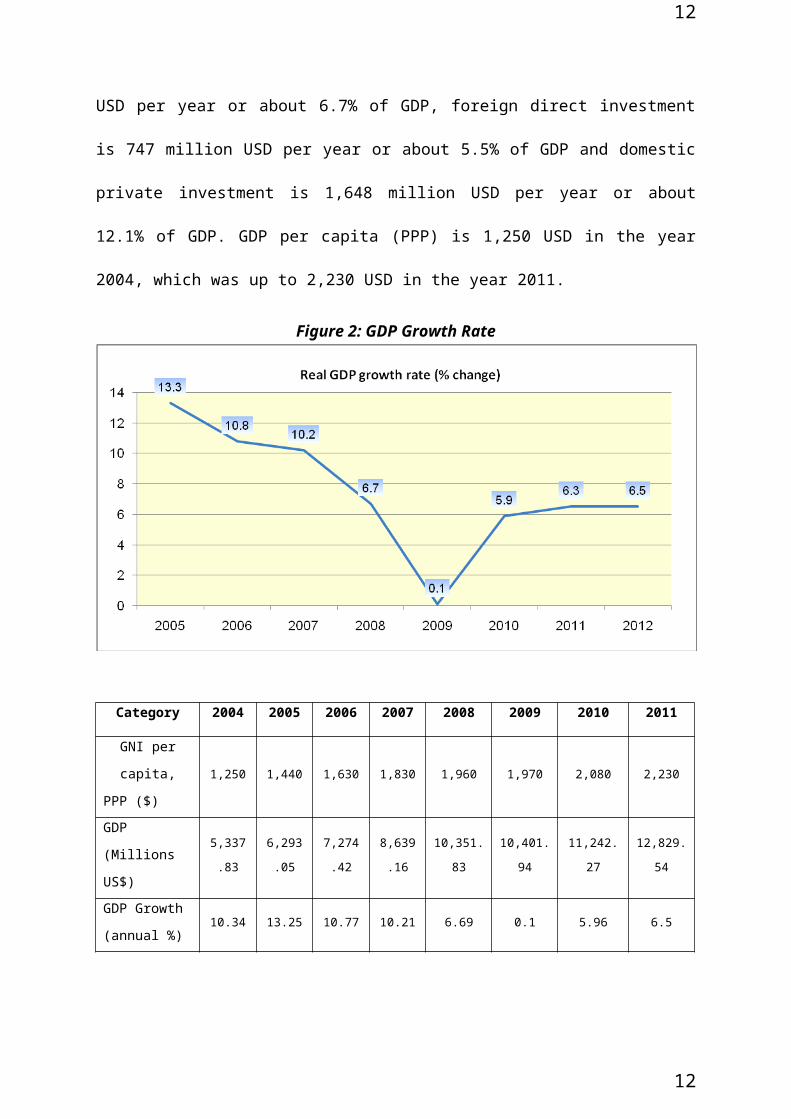

For the period of 2011-2013, economic growth will average by 6.3% in each year.

The increase in 6% is in the year 2011 and in 6.5% in 2012-2013 (figure 2). This growth

needs investment capital approximately 3,316 million USD per year or about 24.3% of GDP

in which public investment is 921 million USD per year or about 6.7% of GDP, foreign direct

investment is 747 million USD per year or about 5.5% of GDP and domestic private

investment is 1,648 million USD per year or about 12.1% of GDP. GDP per capita (PPP) is

1,250 USD in the year 2004, which was up to 2,230 USD in the year 2011.

Figure 2: GDP Growth Rate

Category 2004 2005 2006 2007 2008 2009 2010 2011

GNI per capita,

PPP ($)1,250 1,440 1,630 1,830 1,960 1,970 2,080 2,230

7

8

GDP

(Millions US$)5,337.83 6,293.05 7,274.42 8,639.16 10,351.83 10,401.94 11,242.27 12,829.54

GDP Growth

(annual %)10.34 13.25 10.77 10.21 6.69 0.1 5.96 6.5

8

9

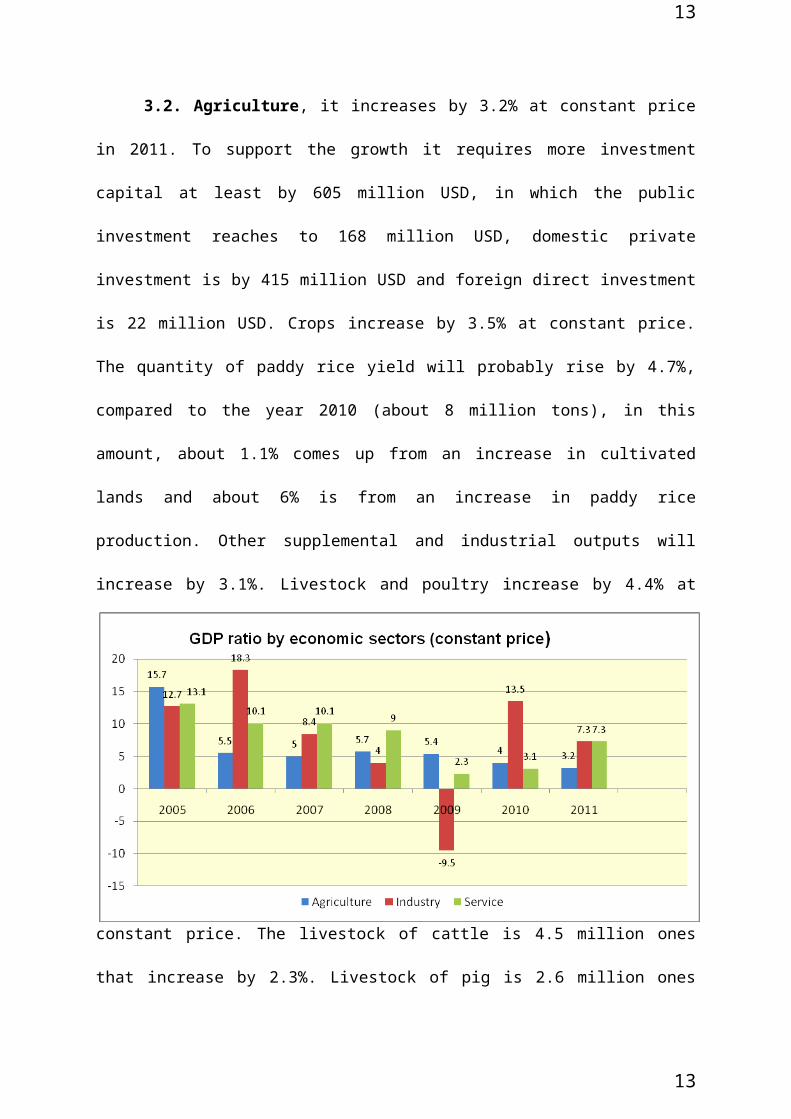

3.2. Agriculture, it increases by 3.2% at constant price in 2011. To support the

growth it requires more investment capital at least by 605 million USD, in which the public

investment reaches to 168 million USD, domestic private investment is by 415 million USD

and foreign direct investment is 22 million USD. Crops increase by 3.5% at constant price.

The quantity of paddy rice yield will probably rise by 4.7%, compared to the year 2010

(about 8 million tons), in this amount, about 1.1% comes up from an increase in cultivated

lands and about 6% is from an increase in paddy rice production. Other supplemental and

industrial outputs will increase by 3.1%. Livestock and poultry increase by 4.4% at constant

price. The livestock of cattle is 4.5 million ones that increase by 2.3%. Livestock of pig is 2.6

million ones that increase by 5% and livestock of poultry is 19.8 million ones that increase of

6.3%, compared to the amount of the previous year 2010. Fisheries increase by 2.5% at

constant price. The total of fisheries output will be 51l million tons in which the industrial

fisheries output will be 239 million tons and the fisheries output by family is 227 million

tons.

Figure 3: GDP ratio by economic sectors

9

10

3.3 Industry, it increases by 7.3% at constant price in 2011. The proportion of this

sector increase by 21.3% of GDP, compared to 21% of GDP in 2010. Overall the increase

need investment capital at least by 1,394 million USD in which the public investment will be

by 459 million USD focusing on electricity and sanitation water supply, irrigation and public

transport system and private investment be equivalent to 935 million USD the domestic

private investment will be by 353 million USD and foreign direct investment will be about

582 million USD. Textile and wearing apparel, it goes up by 10% at constant price in 2011,

compared to the worth of 1.5% in the year 2010, the value of exported garment increase to

more than 3 million USD. Other industrial components food and beverage, plastic products,

machinery spare parts, electronic appliances and construction materials and so on will be in

high increase in order to stabilize growth rate in this sector between 8% and 9% per annum.

Service, it increases by 7.3% at constant price in 2011. Its proportion is up to 38.9% of GDP,

compared to the worth of 38.3% of GDP in the year 2010. Hence, the growth rate will

demand investment capital by 1,022 million USD in which public investment capital is by

212 million USD, domestic private investment capital is by 738 million USD and foreign

direct investment is by 72 million USD. Hotels and restaurants, it increases by 9.4% at

constant price, the foreign visitors about 2.6 million in 2011 that increases in 12% compared

to 2010 and local tourists will come up to 7%. Other services - commerce, telecommunication

and transportation, finance and real estate and business, and so on, will also go up in order to

become constant to the growth in this section with 8% per annum.

3.4 Capital Investment

In year 2011, overall capital investment is about 3,023 million USD or about 24.2%

of GDP that increases in 9.6% compared to 2010 in which public investment is 841 million

USD; foreign direct investment (FDI) is 676 million USD; domestic private investment is

1,505 million USD. The public investment capital sources compose of domestic capital of

10

11

194 million USD, of external grant of 646 million USD - untied aid from development

partner of 340 million USD and foreign loans of 266 million USD.

Figure 4: Growth rate of FDI

3.6 External Trade

In year 2011, overall-exported goods is worth of 4,846 million USD or approximately

38.8% of GDP that increases in 13.2%, compared to the year 2010. Totally-imported goods

are worth of 6,711 million USD or about 53.7% of GDP that increases in 11.8%, compared to

the year 2010. Current account deficit of external payment balance is 1,212 million USD or

around 9.7% of GDP. The deficit is financed through official transfers of 617 million USD

and through capital and finance account of 614 million USD. Total foreign balance of

payment is in surplus of 19 million USD as capital source for increase in nation reserve

capital.

3.7 Inflation and Exchange Rate

In the year 2011, inflation is adjusted to 5.5%. The adjusted inflation is basically due

to determining growth of expending in basket of consumption goods of the last expense of

households. In the year 2011, the last consumption expense of households will increase

11

12

around 12.5% at current price in which increase in real expense is determined about 5.6%, the

population growth is about 1.9 % and its inflation is about 4.5 %. The value of riel exchange

rate against USD that its average price is by 4.135, increasing by 0.2%, compared to the year

2010. Official exchange rate decrease in 0.1% in each year against USD, at the same time,

operational cash flow will increase in average of 22% per year and money velocity will

decrease from 2.49 in the year 2010 to 1.82 in the year 2013. Therefore, overall foreign

capital reserve will be extended in 3.5 month for importing goods and services for local

consumption.

Figure 4: Growth rate of FDI

3.8 Budget Implementation

Budget implementation in the period of 2011-2013, domestic revenue will averagely

increase by 13.5% or around 0.5% of GDP, in a year from 12.6% of GDP in 2010 to 14.2%

of GDP in 2013. At the same time, tax buoyancy in average in 1.45 per year. Totally budget

expenditure will increasingly average 17.8% of GDP - increasing in average of 8.7% per

annum. An average of current budget expenditure is 10.9% of GDP in which salary expense

12

2007 2008 2009 2010 2011-5

0

5

10

15

20

25

3.5

19.7

-0.60000000000

0001

45.5

Inflation rate

Inflation rate

13

accounted for 4.4% of GDP and operational expense is 6.5% of GDP. Expenses of priority

ministries increase by 13.6% and others also increase about 5.8% of GDP. The capital

expenditure average about 6.8% of GDP per year and current budget surplus is 2.2% of GDP

as overall budget deficit is 4% of GDP per year.

In the period of 2011-2013, the worth of exported goods will increase by 15.2% and

import will be up at 11.8% per year. At that time, the current account deficit of external

balance of payment is in average of 8.8% of GDP that will be financed by official transfers of

4.8% of GDP, also capital account and finance of 5.5% of GDP and the rest of 1.5% of GDP

will add into the national capital reserve. As to foreign debt, excluded pervious debt of Russia

and America, will go up to 25.5% of GDP in 2013 and expense on debt service remains of

0.6% of GDP per year.

13

14

PART II

Development of Cambodia Financial Market

The financial Sector has played an important role in developing the private sector and

maintaining sustainable economic growth. In 2001, the Royal Government of Cambodia

(RGC) adopted the Vision and Financial Sector Development Plan for 2001-2010 (FSDP)

which is a long-term strategy for financial sector development in Cambodia. Since that time it

has served to guide the efforts of the RGC, stakeholders and development partners in defining

policy and programs to support the development of the financial sector in Cambodia to

achieve sound and market-based financial system. The second stage, the FSDP was to revise

and update as to address priorities for the period of 2006-2015, building upon the lessons

learned during the initial five years of implementation of the FSDP 2001-2010 and the

objectives of the RGC, the National Strategic Development Plan 2006-2010 and Cambodia’s

Millennium Development Goals.

During 2006, the National Bank of Cambodia (NBC), the Ministry of Economy and

Finance, the Ministry of Commerce, and other stakeholders in Cambodia’s financial sector

worked closely with ADB technical team and development partners through a consultative

process to develop this Financial Sector Development Strategy 2006-2015 (FSDS). The

FSDS intended to provide the strategy, guidance, and framework to support the financial

sector development in Cambodia, particularly; it is a roadmap to establish the financial

markets in the country, in the first priority, is to build the capital market of Cambodia.

The RGC is supporting the development of financial markets in Cambodia for three

reasons:

a) In the short term, addressing the risks arising in the financial system

b) In the intermediate term, removing obstacles to the financial development in

other sectors

c) In the longer term, developing an alternative mechanism for financing and

14

15

investment

The objective is to develop financial markets which appropriately address risks,

remove obstacles to the financial development and support risk management and financial

resource accumulation and allocation. The financial markets may provide a mechanism to

support the finance and investment. At the same time, it is important to develop a progressive

framework for company development which can incentivize company and human capital

development. The international experience has shown it is very difficult to develop effective

financial markets. This has been highlighted by work over the past forty years in the

European Union, especially continental civil law countries, and over the past twenty years by

experiences in Russia, central and Eastern Europe, Asia, and China. At the same time, a

number of significant, positive lessons have emerged for countries seeking to develop the

financial markets. An effective legal framework is essential for markets to develop. The legal

framework has designed to support the protection of investors; ensuring markets are fair,

efficient and transparent; and reduction of systemic risk.

1. Securities Exchange Commission of Cambodia (SECC)

The Securities Exchange Commission of Cambodia (SECC) is established under the

law on the Issuance and Trading of Non-Government Securities. The SECC regulates the

securities industry in Cambodia to contribute to the socio-economic development through

capital mobilization from public securities investors to meet the demand of financing for

business investors. The SECC’s mission is to develop and maintain the confidence of public

investors in Cambodia by protecting their lawful rights and ensuring that issuance and trade

of securities are carried out in a fair and orderly manner; and promote the effective

regulation, efficiency and orderly development of the securities markets; as well as encourage

the varieties of saving tools through buying of securities and other financial instruments

including support the foreign investment and participation in the securities markets in

15

16

Cambodia; and assist the privatization of state-owned enterprises in Cambodia. The SECC is

responsible for regulating, controlling, and developing the securities sector.

2. Securities Market of Cambodia (CSX)

To take one step further in the implementation of the Financial Sector Development

Strategy 2006-2015, the Government of Cambodia decided to establish the Cambodia

Securities Exchange (CSX) as a public enterprise with government shareholding of 55% and

the remaining stake held by the Korea Exchange, a well-known securities exchange operator

of the Republic of Korea. The CSX’s main mandate is to establish and operate a securities

market, a clearing and settlement facility, and a depository, in accordance with the Law on

Issuance and Trading of Non-Government Securities and its subsequent regulations.

With the strong support from the Government of Cambodia, the Ministry of Economy

and Finance, and the Securities and Exchange Commission of Cambodia, we intend to offer

investor-friendly environment for all market participants, and become the main channel of

financing for Cambodia. Besides, the CSX is a place and platform of the securities trading

and facilitates to raise capitals for business and investment, which done by companies and

government institutions and establishes the friendly environment for securities trading for all

investors both local and international investors including offering the products and services to

all market participants and support the state enterprises under the guidance of the

Government of Cambodia.

3. Challenges of the Financial Markets Development

The current economy of Cambodia run off the world economic crisis and started

growing in the form of “V” since 2010 and 2012, after seriously fallen in 2009 and affected

on main sectors such as garment, construction and tourism. Furthermore, although the

banking system of Cambodia now is progressive, but financial sector of Cambodia was in the

first phase, its infrastructure could not sustain the financial markets. Therefore, the challenges

16

17

is that Cambodia strongly relied on banking system for capital collection and allocation

including the financial asset gathering of big banks might lead to the systematic risk and

highest spending for intermediaries.

Moreover, the absence of long-term financing, human resources and management

skills as well as competence might, and lacking of convincing credit, rural financing, and

payment system, information exchange and coordination are main sources of challenges in

the country.

3.1 Banking System

Although, Cambodia financial system has progress, but quantity of saving allocation

is still limited if compared to the neighboring countries in ASEAN. The gap between the

saving and investment sharply increased from -0, 7% in 2006 to -0, 7% in 2010, accordingly,

Cambodia could not relied only on the foreign savings from abroad, it is necessary to

encourage domestic resource collection through the capital markets and moreover, the

capability of center bank is still unable fully to support the financial system in the country.

For financial products is still focus on small sectors of credit and savings. The money market

and inter-banking is still not operating. So, financing has relied on the banking that an

original source of financial crisis in Asian 1997.

Insurance sector is too small in Cambodia, it is not yet fully support the financial

system after the launch of the Cambodian Securities Exchange in July 2011, some foreign

insurance companies has operated the life insurance services, although, the capital source

from the insurance sector is unable to support the capital markets of Cambodia.

17

18

3.2 Capital Markets of Cambodia

The Cambodian securities exchange was established in July 2011, but there is only

one company listing for trading and transactions are allowed to be settled in U.S. dollars for a

transition period of three years, the stock market will eventually boost foreign exchange

transactions and therefore also requires upgrading Cambodia’s shallow foreign exchange

market. Furthermore, the bond market is not yet developed due to lacking some components

for support the market and the principal ratio to determine the value of issuance and other

involving mechanisms.

3.3 Governance and Legal Framework and Regulations

Because of Cambodia financial system is rapidly changing and reinforcing and also

created the new challenges to safeguarding the financial stability in the country. So, the

reinforcement of legal and regulation framework have become more critical after the launch

of the FSDF 2006-2015, particularly, after capital market development. Simultaneously, the

laws and regulations involving in developing the domestic financial markets were

established, but they are not enough to support the operation of efficient market and

transparent transaction, they need to be improved and further new developed in order to

support the strongly financial system, especially, the financial market system in the country.

Additionally, we are lacking the specific research center for studying the laws and other

regulations involving the financial sector development.

In order to strengthen the market infrastructure, the government has carrying out the

law and regulations of international standard of accounting and auditing and international

finance report standard, however, they are still challenging in these sectors because of

incapability of specialized accountants and finance in the country.

18

19

3.4 Risk and Other Challenges

Although, the stock market development is good for both short-term and long-term

economic growth, but there are many challenges for recent situation of Cambodia’s financial

globalization. The systematic risk and speculative bubble should take into account in terms

of the imperfection and fraud in the financial market causing failure of financial stability in

the country. Actually, Cambodia is still a work in progress, but simultaneously, there are

many challenges for the stock exchange development. Just one company trading, the

exchange generated a lot of interest among local and foreign investors. In the first three days

of trading, the share price for Phnom Penh Water Supply Authority (PPWSA) rose 60%

above its IPO price, but by the following week, short term-investors started selling to take in

profits. The stock price came down substantially.

In addition, in order to list on the CSX, it must have at least three years of proper

audits prepared by an accredited international accounting firm approved by the Cambodian

government. This is a hard challenge for many local companies. The institutional investors

from Japan, Korea and China have also taken a bite of the recent IPO but whether that

interest can be sustained for long term or not. The corruption is also a big concern even

though the government passed an anti-corruption law in 2010, but the fear is still in mind of

investors, especially, after general election on July 2013, based on an observation, showed

that the price of PPWSA’s stock is still going down from 6,300 Riel per share in July 2013

to 5,600 Riel per share in November 2013. Furthermore, the lack of capital market

infrastructure and capacity building can be challenges for investors who are not familiar with

the Cambodia securities market.

19

20

References:

National Bank of Cambodia (2010), Economic and Monetary Statistic, Phnom Penh, #196

National Bank of Cambodia (2009), Balance of Payments Statistic Bulletin, issue #29

National Bank of Cambodia (2011), Cambodia Inflation, issued in April 2011, Phnom Penh

Hang Chuon Naron (2009), Macroeconomic, 1st edition, Phnom Penh

Government of Cambodia (2001), Vision and Financial Sector Development Plan 2001-2010

Government of Cambodia (2006), Financial Sector Development Strategy 2006-2015

Ministry of Economy and Finance, http://www.mef.gov.kh/

Securities Exchange Commission of Cambodia, http://secc.org.kh

Economic Institute of Cambodia (2011), Cambodia Economic Watch, Today Economic

Magazine, Phnom Penh

Tal Nay Im, Michel Dabadie (2007), Dollarization in Cambodia, retrieved from http://www.nbc.org.kh/

CDRI (2010), Cambodia Economic Perspective, Phnom Penh

Shik, Eom Kyong (2007), Initial Design for the Cambodian Securities Market, Projection of the Cambodian GDP and Stock Market, Korea Securities Research Institute.

ASEAN Exchanges (2011), Asean Exchange Collaboration, ASEAN Exchange Network. Retrieved from http://www.aseanexchanges.org

20