FAiluRE to ACtThe economic impacTOf current Investment trends InWater and WasteWater treatmentInfrastructure

This report was prepared for the American Society of Civil Engineers by Economic Development Research Group, Inc. in association with Downstream Strategies.

The report was funded by a generous grant from the ASCE Foundation.

American Society of Civil Engineers1801 Alexander Bell DriveReston, Virginia, 20191-4400World Headquarters

101 Constitution Avenue, NWSuite 375 EastWashington, DC 20001Washington Office

[email protected]/failuretoact

Economic Development Research Group, Inc.2 Oliver Street, 9th Floor Boston, MA 02109

www.edrgroup.com

Downstream Strategies295 High Street, Suite 3Morgantown, WV 26505

www.downstreamstrategies.com

Copyright © 2011 by the American Society of Civil Engineers. All Rights Reserved.

★|Contents

2 | List of Figures and Tables

3 | Preface

4 | Executive Summary

10 | Section 1 IntroductIon

13 | Section 2 overvIew of water Infrastructure

17 | Section 3 the overall water and wastewater Infrastructure Gap

24 | Section 4 reGIonal overvIew

28 | Section 5 analytIcal framework

33 | Section 6 economIc Impacts

41 | Section 7 conclusIons

43 | About the Study

45 | Endnotes

47 | References

48 | Acknowledgments

49 | About EDR Group and Downstream Strategies

Atechnicalappendixisseparatelyavailableat www.asce.org/failuretoact

Failure to act The economic impacT of current Investment trends InWaterandWasteWatertreatmentInfrastructure

2 American Society of Civil Engineers

★|Figuresandtables Figures1 WaterUseandPopulationintheUnitedStates,

1950–2005

2 U.S.PopulationServedbyPublicDrinking-WaterandbySelf-Supply,1950–2005

3 U.S.PopulationServedbyPubliclyOwnedWaterTreatmentWorks,1940–2008

4 OverallCapitalInvestmentGapforU.S.WaterInfrastructure,1956–2040

5 ExpectedWastewaterTreatmentandDrinking-WaterInfrastructureNeedsandInvestmentsintheU.S.,2011,2020and2040

6 SpendingbyFederal,State,andLocalGovernments,1956–2040

7 AnnualCapitalNeeds,1995–2040

8 U.S.PopulationGrowthbyRegion,2000–2010

9 GrossRegionalProductGrowth,2000–2010

10 PerCapita20-YearNeedsbyRegion

Tables1 AnnualCapitalGapforWaterInfrastructure

in2010,2020,and2040

2 EstimatedCostsforU.S.HouseholdsandBusinessesduetoUnreliableWaterandWastewaterInfrastructure

3 EffectsonTotalU.S.BusinessSalesandGDPduetoDecliningWaterDeliveryandWastewaterTreatmentInfrastructureSystems,2011–40

4 TheUsefulLivesofDrinking-WaterSystemComponents

5 TheUsefulLivesofWastewaterSystemComponents

6 OverallAnnualCapitalGapforWaterInfrastructurein2010,2020,and2040

7 ChangesinU.S.CapitalSpendingbyFederal,State,andLocalGovernmentsforWaterDeliveryandWastewaterTreatment,1995–2040

8 ComparativeChangesoftheWaterandWastewaterTreatmentCapitalSpendingGapandtheU.S.Economyin2010,2020,and2040

9 RegionalConcernsRegardingBuildingNeworMaintainingtheExistingWaterInfrastructure

10 TopWater-IntensiveIndustriesintheU.S.

11 EffectsonTotalU.S.JobsandPersonalIncomeDuetoDecliningWaterDeliveryandWastewaterTreatmentInfrastructureSystems,2011–40

12 PotentialEmploymentImpactsasaConsequenceofFailingWaterandWastewaterInfrastructure,2020and2040

13 CumulativeLossesofU.S.Exports

14 PotentialU.S.ExportReductionsby2040

15 ComparisonofPotentialScenarios

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 3

ThepurposeoftheFailure to ActreportseriesistoprovideanobjectiveanalysisoftheeconomicimplicationsfortheUnitedStatesofitscontinuedunderinvestmentininfrastructure.Thefourreportsintheserieswillassesstheimplicationsofthepresenttrendsininfrastructureinvest-mentfortheproductivityofindustries,nationalcompetitiveness,andthecostsforhouseholds.

Everyfouryears,theAmericanSocietyofCivilEngineers(ASCE)publishesThe Report Card for America’s Infrastructure,whichgradesthecurrentstateof15nationalinfrastructurecategoriesonascaleofAthroughF.ASCE’s2009Report Cardgavethenation’swastewateranddrinking-waterinfrastructureaD–.ThepresentreportanswersthequestionofhowtheconditionoftheU.S.infrastructuresystemaffectseco-nomicperformance.Inotherwords,howdoesaD–affectAmerica’seconomicfuture?

Thefocusofthisreportisonthepipes,treatmentplants,pumpingstations,andotherinfrastructurethatmakeupthenation’spublicdrinking-waterandwastewatersystems.Mostpublicwaterandwastewatersystemsareownedandoperatedbylocalorregionalgovernmentagencies.Drinking-watersystemsmayalsobe

★|PreFaCe

privatelyownedandoperatedundercontractwithpublicagencies.InaccordancewiththedefinitionsusedbytheU.S.EnvironmentalProtectionAgency(EPA),inthepagesthatfollowweconsiderbothtypesofsystemstobe“public.”Moreover,thisreportanalyzestwotypesofinfrastructureneeds:

1. buildingnewinfrastructuretoserviceincreasingpopulationsandexpandedeconomicactivity;and

2. maintainingorrebuildingexistinginfrastruc-turethatneedsrepairorreplacement.

ThisisthesecondreportinASCE’sFailure to Actseries.Thefirstreport,Failure to Act: The Economic Impact of Current Investment Trends in Surface Transportation Infrastructure,encompasseshighways,bridges,rail,andtransit.Subsequentreportswilladdressenergytrans-mission,aswellasairportsandmarineports.

4 American Society of Civil Engineers

eXeCutiVesummarY

Ofalltheinfrastructuretypes,wateristhemostfundamentaltolife,andisirreplaceablefordrinking,cooking,andbathing.Farmsinmanyregionscannotgrowcropswithoutirriga-tion.Governmentoffices,hospitals,restaurants,hotels,andothercommercialestablishmentscannotoperatewithoutcleanwater.Moreover,manyindustries—foodandchemicalmanufac-turingandpowerplants,forexample—couldnotoperatewithoutthecleanwaterthatisacom-ponentoffinishedproductsorthatisusedforindustrialprocessesorcooling.Drinking-watersystemscollectsourcewaterfromriversandlakes,removepollutants,anddistributesafewater.Wastewatersystemscollectusedwaterandsewage,removecontaminants,anddis-chargecleanwaterbackintothenation’sriversandlakesforfutureuse.Wetweatherinvest-ments,suchassanitaryseweroverflows,preventvarioustypesofpollutantslikesewage,heavymetals,orfertilizerfromlawnsfromeverreach-ingthewaterways.

However,thedeliveryofwaterintheUnitedStatesisdecentralizedandstrained.Nearly170,000publicdrinking-watersystemsarelocatedacrosstheU.S.Ofthesesystems,54,000arecommunitywatersystemsthatcollectivelyservemorethan264millionpeople.Theremain-ing114,000arenon-communitywatersystems,suchasthoseforcampgroundsandschools.Significantly,morethanhalfofpublicdrinking-watersystemsservefewerthan500people.

AstheU.S.populationhasincreased,thepercentageservedbypublicwatersystemshasalsoincreased.Eachyearnewwaterlinesareconstructedtoconnectmoredistantdwellerstocentralizedsystems,continuingtoadduserstoagingsystems.Althoughnewpipesarebeingaddedtoexpandserviceareas,drinking-water

systemsdegradeovertime,withtheusefullifeofcomponentpartsrangingfrom15to95years.

Particularlyinthecountry’soldercities,muchofthedrinking-waterinfrastructureisoldandinneedofreplacement.Failuresindrinking-waterinfrastructurecanresultinwaterdisruptions,impedimentstoemergencyresponse,anddam-agetoothertypesofessentialinfrastructure.Inextremesituationscausedbyfailinginfrastruc-tureordrought,watershortagesmayresultinunsanitaryconditions,increasingthelikelihoodofpublichealthissues.

TheUnitedStateshasfarfewerpublicwaste-watersystemsthandrinking-watersystems—approximately14,780wastewatertreatmentfacilitiesand19,739wastewaterpipesystemsasof2008.1In2002,98percentofpubliclyownedtreatmentsystemsweremunicipallyowned.2Althoughaccesstocentralizedtreat-mentsystemsiswidespread,theconditionofmanyofthesesystemsisalsopoor,withagingpipesandinadequatecapacityleadingtothedischargeofanestimated900billiongallonsofuntreatedsewageeachyear.3

TheEPAestimatedthecostofthecapitalinvestmentthatisrequiredtomaintainandupgradedrinking-waterandwastewatertreatmentsystemsacrosstheU.S.in2010as$91billion.However,only$36billionofthis$91billionneededwasfunded,leavingacapitalfundinggapofnearly$55billion.

WaterinfrastructureintheUnitedStatesisclearlyaging,andinvestmentisnotabletokeepupwiththeneed.Thisstudy’sfindingsindicatethatinvestmentneedswillcontinuetoescalate.AsshowninTable1,ifcurrenttrendspersist,theinvestmentrequiredwillamountto$126billionby2020,andtheanticipatedcapitalfundinggapwillbe$84billion.Moreover,by2040,theneeds

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 5

forcapitalinvestmentwillamountto$195billionandthefundinggapwillhaveescalatedto$144billion,unlessstrategiestoaddressthegapareimplementedintheinterveningyearstoalterthesetrends.

effects on expensesEvenwithincreasedconservationandcost-effectivedevelopmentofotherefficiencymethods,thegrowinggapbetweencapitalneedstomain-taindrinking-waterandwastewatertreatmentinfrastructureandinvestmentstomeetthoseneedswilllikelyresultinunreliablewaterserviceandinadequatewastewatertreatment.

Becausecapitalspendinghasnotbeenkeepingpacewithneeds,theresultinggapwillonlywidenthrough2040.Asaresult,pipeswillleak,theconstructionofthenewfacilitiesrequiredtomeetstringentenvironmentalstandardswillbedelayed,addressingthegapwillbecomeincreas-inglymoreexpensive,andwaterswillbepolluted.

Thisanalysisassumesthatthemountingcoststobusinessesandhouseholdswilltaketheformof:

★ Doingnothingandlivingwithwatershortages,andhigherrates(rationingthroughpriceincreases);ormajoroutlaysbybusinessesandhouseholds,includingexpendituresincurredbymovingtowhereinfrastructureisstillreliable,purchasingand

installingequipmenttoconservewaterorrecyclewater,andincreasingrelianceonself-suppliedwaterand/orwastewatertreatment(i.e.,installingindividualwellsandsepticwastesystemswhenmunicipalfacilitiesandservicesarenotavailableoptions),and

★ Incurringincreasedmedicalcoststoaddressincreasesinwater-borneillnessesduetounreliabledeliveryandwastewatertreatmentservices.

Theseresponsestofailingpublicinfrastructurewillvarybylocation,householdcharacteristics,andsizeandtypeofbusiness.Expendituresduetomoving,orfrominstallingandoperatingnewcapitalequipmentfor“self-supply,”areestimatedforhouseholds,commercialestablishments,andmanufacturers.Thesecostsareestimatedat$35,000perhouseholdand$500,000to$1mil-lionforbusinesses,dependingonsizeandwaterrequirement,andareamortizedover20years.Althoughtheseexpendituresarebasedonthecostsassociatedwithself-supply,thecostsareusedtorepresentoutlaysbysomehouseholdsandbusinessesinresponsetounreliablewaterdeliveryandwastewatertreatmentservices.Thisstudydoesnotassumethatcompaniesorhouseholdsmoveoutsideofthemultistateregionwheretheyarenowlocated.However,movement

Year Spending need gap

2010 36.4 91.2 54.8

2020 41.5 125.9 84.4

2040 51.7 195.4 143.7

sourCesNeedscalculatedfromEPA(1997a,1997b,2001,2003,2005,2008,2009,2010).SpendingcalculatedfromCBO(2010)andUSCB(2011a,2011b).

Table 1★ annual capital Gap for Water infrastructure in 2010, 2020, and 2040 (billions of 2010 dollars)

6 American Society of Civil Engineers

acrossregionalboundariesandrelocationofbusinessesoutsideoftheU.S.iscertainlyaresponsethatmaybetriggeredbydecreasingreliabilityofpublicwaterandsewersystems.Householdsandbusinessesthatdonotself-supplyareassumedtoabsorbthehighercoststhatareaconsequenceofdisruptionsinwaterdeliveryandwastewatertreatmentduetoworseninginfrastructure.Theassumptionforthiscategoryisthatthesehouseholdsandbusinesseswillpaythe$84billionassociatedwiththe2020capitalgap($144billionby2040)intermsofhigherratecostsoverandabovethebaselineprojectedratesforwaterandwastewatertreatment.

Water-borneillnesseswillexactapriceinadditionalhouseholdmedicalexpendituresandlaborproductivityduetosicktimeused.TheEPAandtheCentersforDiseaseControlandPreventionhavetrackedthe30-yearincidenceofwater-borneillnessesacrosstheU.S.,categorizedthetypeofillnesses,anddevelopedamonetaryburdenforthosecases.Thatburdenisdistrib-utedpartiallytohouseholds(29percent),asout-of-pocketfeesfordoctororemergencyroomvisits,andotherillness-relatedexpensesleavinglessforahouseholdtospendonotherpurchases,andmainlytoemployers(71percent),duetolostlaborproductivityresultingfromabsentee-ism.Themonetaryburdenfromcontaminationaffectingthepublic-provisionsystemsoverthehistoricalintervalwas$255million.

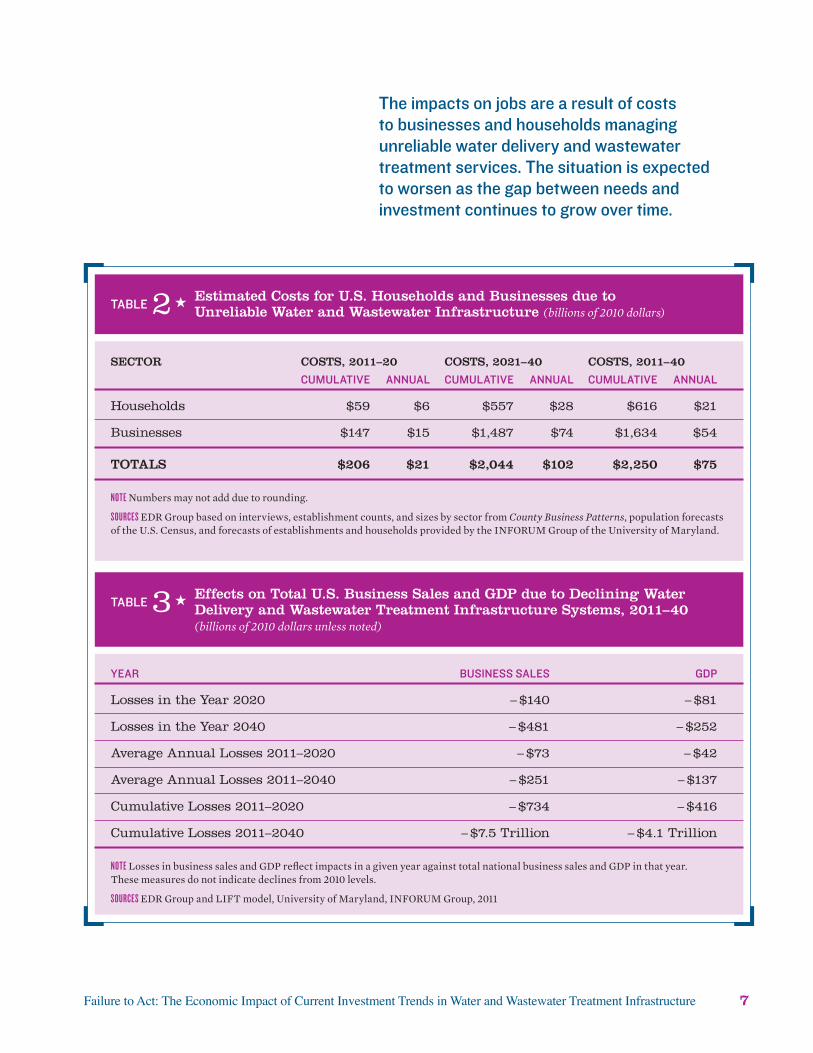

overall Summary of costsThesumofestimatedexpensestohouseholdsandbusinessesduetounreliablewaterdeliv-eryandwastewatertreatmentisshowninTable2.By2020,thetotalcoststobusinessesduetounreliableinfrastructurewillbe$147billionwhilethatnumberwillbe$59billionforhouse-holds.Thetotalimpactofincreasedcostsanddropinincomewillreducethestandardoflivingforfamiliesbyalmost$900peryearby2020.

effects on the national economyBy2020,thepredicteddeficitforsustainingwaterdeliveryandwastewatertreatment

infrastructurewillbe$84billion.Thismayleadto$206billioninincreasedcostsforbusinessesandhouseholdsbetweennowand2020.Inaworstcasescenario,theU.S.willlosenearly700,000jobsby2020.Unlesstheinfrastructuredeficitisaddressedby2040,1.4millionjobswillbeatriskinadditiontowhatisotherwiseanticipatedforthatyear.

Theimpactsoftheseinfrastructure-relatedjoblosseswillbespreadthroughouttheeconomyinlow-wage,middle-wageandhigh-wagejobs.In2020,almost500,000jobswillbethreatenedinsectorsthathavebeentraditionalemployersofpeoplewithoutextensiveformaleducationsorofentry-levelworkers.4Conversely,ingener-allyacceptedhigh-endsectorsoftheeconomy,184,000jobswillbeatrisk.5

Theimpactsonjobsarearesultofcoststobusinessesandhouseholdsmanagingunreliablewaterdeliveryandwastewatertreatmentservices.AsshowninTable3,betweennowand2020,thecumulativelossinbusinesssaleswillbe$734billionandthecumulativelosstothenation’seconomywillbe$416billioninGDP.Impactsareexpectedtocontinuetoworsen.Intheyear2040alone,theimpactwillbe$481billioninlostbusinesssalesand$252billioninlostGDP.6Moreover,thesituationisexpectedtoworsenasthegapbetweenneedsandinvest-mentcontinuestogrowovertime.AverageannuallossesinGDPareestimatedtobe$42billionfrom2011to2020and$185millionfrom2021to2040.7

The role of Sustainable practicesInalllikelihood,businessesandhouseholdswillbeforcedtoadjusttounreliablewaterdeliveryandwastewatertreatmentservicebystrengtheningsustainablepracticesemployedinproductionanddailywateruse.ThesolutionsalreadybeingputforwardandimplementedintheUnitedStatesandabroadincludevoluntarylimitationsorimposedregulationsgoverningthedemandforwater,aswellastechnologies

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 7

Year buSineSS SaleS gdp

Losses in the Year 2020 – $140 – $81

Losses in the Year 2040 – $481 – $252

Average Annual Losses 2011–2020 – $73 – $42

Average Annual Losses 2011–2040 – $251 – $137

Cumulative Losses 2011–2020 – $734 – $416

Cumulative Losses 2011–2040 – $7.5 Trillion – $4.1 Trillion

noteLossesinbusinesssalesandGDPreflectimpactsinagivenyearagainsttotalnationalbusinesssalesandGDPinthatyear.Thesemeasuresdonotindicatedeclinesfrom2010levels.

sourCesEDRGroupandLIFTmodel,UniversityofMaryland,INFORUMGroup,2011

Table 3★ effects on total u.S. Business Sales and GDP due to Declining Water Delivery and Wastewater treatment infrastructure Systems, 2011–40 (billions of 2010 dollars unless noted)

Sector coStS, 2011–20 coStS, 2021–40 coStS, 2011–40

cumulaTive annual cumulaTive annual cumulaTive annual

Households $59 $6 $557 $28 $616 $21

Businesses $147 $15 $1,487 $74 $1,634 $54

totalS $206 $21 $2,044 $102 $2,250 $75

noteNumbersmaynotaddduetorounding.

sourCesEDRGroupbasedoninterviews,establishmentcounts,andsizesbysectorfromCounty Business Patterns,populationforecastsoftheU.S.Census,andforecastsofestablishmentsandhouseholdsprovidedbytheINFORUMGroupoftheUniversityofMaryland.

Table 2★ estimated costs for u.S. Households and Businesses due to unreliable Water and Wastewater infrastructure (billions of 2010 dollars)

The impacts on jobs are a result of costs to businesses and households managing unreliable water delivery and wastewater treatment services. The situation is expected to worsen as the gap between needs and investment continues to grow over time.

8 American Society of Civil Engineers

thatrecyclewaterforindustrialandresidentialpurposes(e.g.,usingrecycledshowerwaterforwateringlawns).Thesetypesofpolicieshavereducedthedemandforwaterandwastewater,and,thereforehavelessenedtheimpactsonexistinginfrastructure.ThemostrecentCleanWatershedsNeedsSurvey(EPA2010)incor-poratesnewtechnologiesandapproacheshighlightedforwastewaterandstormwater:advancedtreatment,reclaimedwastewater,andgreeninfrastructure.Incontrast,themostrecentDrinkingWaterNeedsSurvey(EPA2009)doesnotincludenewtechnologiesandapproaches,suchasseparatepotableandnonpotablewaterandincreasingefficiencies.

Americanbusinessesandhouseholdshavebeenusingwatermoreefficiently,andtheycancontinuetoimprovetheirefficiencyduringthecomingdecades.AsshowninFigure1,thoughtheU.S.populationhascontinuedtogrowsteadilysincethemid-1970s,totalwater

usehasbeenlevel.Overall,U.S.percapitawaterusepeakedinthemid-1970s,withcurrentlevelsbeingthelowestsincethe1950s.Thistrendisduetoincreasesintheefficiencyofindustrialandagriculturalwateruseandisreflectedinanincreaseintheeconomicproductivityofwater.Thesetrendsinindustrialwaterusecanbeexplainedbyanumberoffactors.Forexample,severalwater-intensiveindustries,suchasprimarymetalmanufacturingandpaperman-ufacturing,havedeclinedintheU.S.,therebyreducingwaterwithdrawals.Otherindustrieshavefacedmorestringentwaterqualitystan-dardsundertheCleanWaterAct,whichmayhaveledtotheimplementationoftechnologiesorpracticesthatsavewater.8

Nationally,wateruseinthehomehasremainedstablesincethe1980s.Efficiencyandconservationeffortshavereducedpercapitahouseholdconsumptioninsomestatesandregions.Domesticwaterusehasbecomemore

Figure 1★ Water use and Population in the united States, 1950–2005

nTotalWithdrawals(billionsofgallonsperday)nPopulation(millions)

0

50

100

150

200

250

300

350

400

450

2005200019951990198519801975197019651960195519500

50

100

150

200

250

300

350

sourCeU.S.GeologicalSurvey.

Wit

HD

ra

Wa

lS

Po

Pu

la

tio

n

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 9

efficientthroughtheuseofnewtechnologiessuchaswater-efficienttoiletsthatuseone-thirdofthewaterofoldertoilets.Inaddition,newtechnologiesandapproachesmayreducefuturewaterinfrastructureneeds.Forexample,manycitieshaverecentlyadoptedgreeninfrastructureapproachestowetweatheroverflowmanage-ment.Greenroofs,grassyswales,andraingardens,forexample,areusedtocaptureandreuseraintomimicnaturalwatersystems.Suchtechniquesoftenprovidefinancialsavingstocommunities.

Nevertheless,demandmanagementandsustainablepracticescannotsolvetheproblemalone.Theseeffortsarecounteredbyincreasingpopulationsinhotandaridregionsofthecountry—includingtheSouthwest,RockyMountains,andFarWest—wherethereisgreaterdomesticdemandforoutdoorwateruse.9

Inthisstudy,asecondscenariowasrun,whichassumedthattherewouldbeageneraladjustmentbybusinessesandhouseholdsasthecapitalgapworsened.Inthisscenario,negativeeconomicimpactsmountforabout25years—roughly2011–35,thoughataslowerpacethantheearlierscenario—andthenabateasincreasingnumbersofhouseholdsandbusinessesadjusttotherealityofdeficientinfra-structure,includingnetlossesof538,000jobsby2020and615,000jobsby2040.Inthisscenario,joblossespeakat800,000to830,000intheyears2030–32.

Inaddition,GDPwouldbeexpectedtofallby$65billionin2020and$115billionin2040.ThelowestpointsinthedeclineinGDPwouldbein2029–38,whenlosseswouldexceed$120bil-lionannually.After-taxpersonalincomelossesunderthisscenarioare$87billionin2020and$141billionin2040,whichrepresentsareboundfrom$156billionto$160billioninannuallossesintheyears2030–34.

The objectives and limits of This StudyThepurposeofthisstudyislimitedtopresentingtheeconomicconsequencesofthecontinuingunderinvestmentinAmerica’swater,wastewater,

andwetweathermanagementsystems.Itdoesnotaddresstheavailabilityorshortagesofwaterasanaturalresourceorthecostofdevelopingandharnessingnewwatersupplies.Joiningwaterdeliveryandwastewatertreatmentinfra-structurewiththecostsofdevelopingnewwatersuppliesisanappropriateandimportantsubjectforamoreextensivefollow-upstudy.Thisreportassumesthatthecurrentregulatoryenviron-mentwillremaininplaceandnochangestocurrentregulationswilloccur.Finally,thisworkisnotintendedtoproposeorimplyprescriptivepolicychanges.However,manyorganizationsandinterestgroups,includingASCE,continuetoengagewithpolicymakersatalllevelsofgovernmenttoseeksolutionstothenation’sinfrastructureproblems.

conclusionWell-maintainedpublicdrinkingwaterandwastewaterinfrastructureiscriticalforpublichealth,strongbusinesses,andcleanriversandaquifers.UptothismomentAmericanhouseholdsandbusinesseshaveneverhadtocontemplatehowmuchtheyarewillingtopayforwaterifitbecomeshardtoobtain.

Thisreportdocumentsthatcapitalspendinghasnotbeenkeepingpacewithneedsforwaterinfrastructure,andifthesetrendscontinue,theresultinggapwillonlywidenthrough2040.Asaresult,pipeswillleak,newfacilitiesrequiredtomeetstringentenvironmentalgoalswillbedelayed,O&Mwillbecomemoreexpen-sive,andwaterswillbepolluted.

Therearemultiplewaystopartiallyoffsetthesenegativeconsequences.Possiblepreventivemeasuresincludespendingmoreonexistingtechnologies,investingtodevelopnewtechnolo-giesandthenimplementingthem,andchangingpatternsinwhereandhowwelive.Allthesesolutionsinvolvecosts.Separatelyorincombi-nation,thesesolutionswillrequireactionsonnational,regional,orprivatelevels,andwillnotoccurautomatically.

10 American Society of Civil Engineers

introduCtion

the analysis presented in this report illustrates how

deficiencies in water delivery, wastewater treatment, and wet

weather management infrastructure affect the u.S. economy

and will continue to do so in the future. the report seeks

to highlight not only how deficient water systems impose

costs on households and businesses but also how these costs

affect the productivity and competitiveness of industries,

along with the well-being of households.

1

Thereportincludesthefollowingtopics:

★ anoverviewofwaterdeliveryandwaste-watertreatmentinfrastructure,

★ waterdemandbyregionandthesegmen-tationofconsumers,

★ theshortfallininfrastructureinvestment,★ theregionalimplicationsofthisshortfall,★ anoverviewofthemethodologyemployedtoassesseconomicperformance,and

★ theimplicationsoftheshortfallininfrastructureinvestmentfornationaleconomicperformance.

Thefinalsectionsincludeconclusions,adis-cussionofopportunitiesforfutureresearch,thesourcesandmethodologyused,andacknowledgments.

Thebasisfortheeconomicanalysisisdoc-umentationprovidedbytheEPAinstudiesanddatabasesdevelopedfrom1995through2010;researchbyindustrygroups,suchastheAmericanWaterWorksAssociationandtheNationalAssociationofWaterCompanies;andscholarshipbyandinterviewswithengi-neersandotherexpertsonwaterandsewers.Theneedtomaintaintheexistingwater

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 11

delivery,wastewatertreatment,andrelatedsystemshavesignificantimplicationsforindus-trycompetitivenessandperformance,andalsothestandardsoflivingofhouseholds.

1.1 The objectives and limits of this StudyThepurposeofthisstudyislimitedtopresentingtheeconomicconsequencesofacontinuingtrendofunderinvestmentinAmerica’swaterandwastewatersystems.Itdoesnotaddresstheavailabilityorshortagesofwaterasanaturalresource,orthecostofdevelopingandharnessingnewwatersupplies,anditisnotintendedtopro-poseorimplyprescriptivepolicychanges.

Waterandwastewatercapitalspendingbyfederal,state,andlocalgovernmentshasincreasedconsistentlysince1956.Itisdifficulttopredictfuturelevelsofcapitalspendingbecauseawiderangeoffactorswillexertaninfluenceoverthecomingdecades.Spendingwillbeimpactedbythedegreetowhichinfra-structureactuallyfails,orispredictedtofail,inthenearfuture.Inaddition,capitalspendingwillrisetomeetrequirementsfromnewlawsandregulations.Regionalgrowthdifferencesinfuturepopulationandeconomicactivitywillalsoimpacttheallocationoffuturecapitalspending.Additionally,fundingtrendsarestronglyinflu-encedbypoliticalwill.Withoutattemptingtomodelthenumerouscomplicatedfactorslistedabove,alinearprojectionbasedonhistoricaldataprovidesareasonablelong-termtrendthatisconsistentwithpastpatterns.

Themostimportantchallengeinassessingtheeconomicconsequencesofunreliablewaterandwastewaterserviceisthateconomicdataandtoolstomanipulatethosedataarenotread-ilyavailable.Giventhislimitedinformation,assumptionsarerequiredtoweightheresponsesofbusinessesandhouseholdswhenfacedwith

deterioratingwaterandsewerserviceduetofailinginfrastructure.

Alternativesfacedbyconsuminghouseholdsandbusinessesarenotfeasibleonanationallevel.Oneormoreofthesealternativesmaybeviableforindividualcompaniesorhouseholds,dependingonthelocationandscaleofservicesneeded.Thesealternativesare,however,unre-alisticasleverstoaltersystemcapacityandreliabilityissuesnationwide.Today,alternativesaresummarizedby:

★ Adoptingfurthersustainablepracticesthroughchangesinactivityprocesses,orinstallationofnewequipment;10

★ Doingnothing—andlivingwithwaterdeliv-erydisruptionsandincreasedincidenceofcontaminationduetounreliabledeliveryandwastewatertreatmentservicesandhigherrates(rationingthroughpriceincreases);

★ Significantlyincreasingrelianceon“self-supply”forwatersupplyand/orwastewatertreatment(i.e.,buildingindividualwellsandsepticwastesystemswhenmunicipalfacilitiesandservicesarenotavailableoptions);and

★ Movingtowherewaterandwastewaterservicesarenothinderedbyfailinginfra-structure,ormovetoanareawhereself-supplyispermittedandpracticable;

Theeffectivenessoftheseresponsestofailingpublicinfrastructurewillvarybylocation,size,andtypeofbusiness.Forexample,privatewellandsepticinstallationsarenotverylikelytooccurincities,duetoenvironmentalandregula-toryfactors.Moreover,watersupplyconditionsvarywidelybylocation.Forexample,inmostofCaliforniaitisvirtuallyimpossibletoself-supply

12 American Society of Civil Engineers

water,butitispossibletoself-supplywastewatertreatment.Inadditiontotoday’stechnology,conservationcanaddressaportionofthesupplyproblem,butbyitselfitisnotasocietalsolutiontothebroaderproblemofagingandthedecliningperformanceofmunicipalinfrastructure.

Alltheseoptions,however,generateaddedcostsforhouseholdsandbusinessestablish-ments.Forthepurposesofthisstudy,thecostofself-supplyisestimatedforhouseholds,commercialestablishments,andmanufacturers,andisusedasabasistoestimatetherangeofaddedcoststhatmightbeincurredbyanyoftheseotheralternatives.

Householdsandbusinessesthatwouldorcouldnotself-supply(ormove,orobtainwater-conservingequipment)areassumedtoabsorbthehighercoststhatareaconsequenceofdisruptionsinwaterdeliveryandwastewatertreatmentduetoworseninginfrastructure.Thesecostsareassumedtobethesizeofthecapitalfundinggap,whichunderpresentinvest-menttrendsisexpectedtoreach$144billionby2040,unlessitisaddressedearlier.Theunderlyingassumptionforthiscostisthatthepricesofwaterandwastewatertreatmentwillincreaseasservicesneedtoberationedtostretchtheeffectivenessoftheinfrastructureinovercomingthecapitalgap.Usingthegaptoreflecthighercostsreflectstheconceptofrationingbyprice.

Summarydataandexpertinterviewswereusedtoconstructnationalandmultistateregionalestimatesofcosts.KeysourcesincludeanalysesconductedbytheEPAandotherresearchtoestimatethecapitalfundinggapanddemandbysectorandregion;theAmericanWaterWorksAssociation’s2010WaterandWastewaterRateSurvey,whichisasamplingofutilitydatabysizeanduserclass;andinterviewstobroadlyapproximatethecapitalandoperationsandmaintenancecostsofprivatesystems.

Asthisstudyislimitedtotheeconomiccon-sequencesofcurrentinvestmenttrends,itdoesnotincludethepotentialeconomicimpactsandbenefitsofconstructiontoclosethegapbetweentrendsandidentifiedneeds.Ananalysisthatincludestheeconomicimpactsofconstructionandhownewinvestmentwillaffecteconomicperformancewillvarydependingonthemixofsolutionsthatareimplemented.

in addition to today’s technology, conservation can address a portion of the supply problem, but by itself it is not a societal solution to the broader problem of aging and the declining performance of municipal infrastructure.

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 13

oVerVieWoFWaterinFrastruCture

2.1 drinking-Water

nearly 170,000 public drinking-water systems are found

across the united States. of these, 54,000 are community water

systems that collectively serve more than 264 million people.

community water systems are those that serve more than 25

people a day, all year round. the remaining 114,000 systems

are non-community water systems, such as those for camp-

grounds and schools. only 43 percent of community water

systems are publicly owned; 33 percent are private, and the

balance are maintained by entities whose primary purpose

is something other than water provision.11

2

AsshowninFigure2,thenumberofpeoplewhosupplytheirownwaterusingdomesticwellsandspringshasremainedsteadysince1965.However,asthepopulationhasincreased,thepercentageofthepopulationservedbypublicsystemshasincreased.Thisincreasewasabout3percentperfiveyearsfrom1950to1965,butsincethepubliclysuppliedpopu-lationreached80percent,theincreasehasslowedtoabout1percentperfiveyears.

Thistrendislargelyexplainedbyamigra-tiontocities—theruralpopulationwas36percentofthetotalin1950butdroppedto16percentby2010.Additionally,eachyearnew

waterlinesareconstructed,connectingmoredistantdwellerstocentralizedsystems.

Althoughnewpipesarebeingaddedtoexpandserviceareas,drinking-watersystemsdegradeovertime,withtheusefullifeofcomponentpartsrangingfrom15to95years(Table4).Especiallyinthecountry’soldercit-ies,muchofthedrinking-waterinfrastructureisoldandinneedofreplacement.Failuresindrinking-waterinfrastructurecanresultinwaterdisruptions,impedimentstoemergencyresponse,anddamagetoothertypesofinfrastructure.12Inextremesituations,watershortages,whethercausedbyfailing

14 American Society of Civil Engineers

infrastructureorbydrought,mayresultinunsanitaryconditions,leadingtopublichealthconcerns.Brokenwatermainscandamageroad-waysandstructuresandhinderfire-controlefforts.Unscheduledrepairworktoaddressemergencypipefailuresmaycauseadditionaldisruptionstotransportationandcommerce.

2.2 WastewaterTherearefewerpublicwastewatersystemsthandrinking-watersystems.In2008,14,780waste-watertreatmentfacilitiesand19,739wastewaterpipesystemswereoperationalacrosstheU.S.13

In2002,98percentofpubliclyownedtreatmentworksweremunicipallyowned.14

Althoughaccesstocentralizedtreatmentiswidespread(Figure3),theconditionofmanyofthesesystemsispoor,withagingpipesandinadequatecapacityleadingtothedischargeofanestimated900billiongallonsofuntreatedsewageeachyear.15

Beforeabout1950,itwasacommonpracticetoconstructsystemsthatdirectedwetweatherrunoffintocombinedsewersystems,mixingdischargesknownaswetweatheroverflows(WWOs)withsanitarysewage.Manyofthesecombinedsystemsarestillinusetoday.When

Figure 2★ u.S. Population Served by Public Drinking-Water and by Self-Supply, 1950–2005 (millions)

0

50

100

150

200

250

300Domestic self-supply

Public supply

200520001995199019851980197519701965196019551950

sourCesMacKichan(1951,1957);MacKichanandKammerer(1961);Murray(1968);MurrayandReeves(1972,1977);Solley,Chase,andMann(1983);Solley,Merk,andPierce(1988);Solley,Pierce,andPerlman(1993,1998);Hutsonetal.(2004);Kennyetal.(2009).

nPublicSupplynDomesticSelf-Supply

38%29%

26%22%

20%19%

19%18%

17%

16%

15%

14%

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 15

componenT uSeFul liFe (YearS)

Reservoirs and dams 50–80

Treatment plants—concrete structures 60–70

Treatment plants—mechanical and electrical 15–25

Trunk mains 65–95

Pumping stations—concrete structures 60–70

Pumping stations—mechanical and electrical 25

Distribution 60–95

sourCeEPA(2002,table2-1).

Table 4★ the useful lives of Drinking-Water System components

componenT uSeFul liFe (YearS)

Collections 80–100

Treatment plants—concrete structures 50

Treatment plants—mechanical and electrical 15–25

Force mains 25

Pumping stations—concrete structures 50

Pumping stations-mechanical and electrical 15

Interceptors 90–100

sourCeEPA(2002,table2-1).

Table 5★ the useful lives of Wastewater System components

especially in the country’s older cities, much of the drinking-water infrastructure is old and in need of replacement. Failures in drinking-water infrastructure can result in water disruptions, impediments to emergency response, and damage to other types of infrastructure.

16 American Society of Civil Engineers

aggravatedbyheavyrainandsnowmelt,increasedrunoffoverwhelmsthesewersystem,resultinginthereleaseofthecombinedsewageandstormwaterdirectlyintostreamsthroughWWOs.Inaddition,WWOsalsoresultinthedischargeofuntreatedsewage,butduetoaging

infrastructureratherthanbydesign.Duringwetweather,WWOsallowgroundwatertoseepintopipes,potentiallycausingasystemover-load.Asmoresystemsapproachandsurpasstheireffectivelifespans(Table5),WWOeventsbecomemorecommon.

Figure 3★ u.S. Population Served by Publicly owned Water treatment Works, 1940–2008 (millions)

0

50

100

150

200

250

No discharge

Advanced

Secondary

Less than secondary

Raw2

00

82

00

62

00

42

00

22

00

01

99

81

99

61

99

41

99

21

99

01

98

81

98

61

98

41

98

21

98

01

97

81

97

61

97

41

97

21

97

01

96

81

96

61

96

41

96

21

96

01

95

81

95

61

95

41

95

21

95

01

94

81

94

61

94

41

94

21

94

0

noteInadditiontothepopulationservedbypubliclyownedtreatmentworks,thisfigurealsoshowspopulationwithrawsewagedischarges.Thisfiguredoesnotshowpopulationservedbyonsitewastewatertreatmentsystems.

sourCesEPA2010,figureES-2,whichreferencesU.S.PublicHealthServiceandEPACleanWatershedsNeedsSurveys.

nNoDischargenAdvancednSecondarynLessthanSecondarynRaw

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 17

tHeoVerallWaterandWasteWaterinFrastruCturegaP

the 30-year capital needs for maintaining and expanding the

united States’ water delivery systems, wastewater treatment

plants, and sanitary and storm sewer systems range from approx-

imately $91 billion in 2010, to $126 billion in 2020, to $195 billion

by 2040. these estimates are considerably higher than previous

ones—because they account for escalated costs, a previous

underreporting of local needs by communities, an extension

of analysis from 20 to 30 years of needs, and a more detailed

study of the needs to address raw sewage being discharged

from combined sewage overflows.

3

TheseestimatesareprimarilydrawnfromthefollowingcalculationsoftheEPA:

★ Nationaldrinking-waterneeds(DWNs)over20years,whichtheagencyhasupdatedevery4yearsfrom1995through2007.TheDWNsarebasedonwaterqual-ityproblems,orwater-quality-relatedpublichealthproblemsthatexistedwhenthereportswerereleased,orthatwereexpectedtooccurwithinthenext20years.Forexample,theneedsidentifiedinthe2007DWNsarethoseexpectedfrom2007through2026.16

★ Nationalcleanwatershedneedsover20years,whichtheagencyhasupdatedevery

4yearsfrom1996through2008.Figure6showstheseprogressing20-yearneedestimates.The20-yearneedforagivenyearreferstotheamountrequiredforinvestmentoverthenext20years.Forexample,the2004valueindicatesthatthecapitalneedintheyears2004–23wouldtotal$200billion.17

AsdocumentedbyEPA,20-yearcapitalneedsforwaterdistributionhaveincreaseddra-maticallysince1995.Capitalstockneedsfordrinking-waterarelargelytoaddresspipes(transmissionanddistributionlines),treat-mentsystems,storage,andsource.18Thepipesthatconstitutethetransmissionanddistribu-tionnetworkcovermorethanhalftheneeds

18 American Society of Civil Engineers

fordrinking-waterinfrastructure.EPA(2002)appliesasimpleagingmodeltopipes(normaldistribution)inthe20citiesstudiedbytheAmericanWaterWorksAssociation.Accordingtothismodel,thepeakreplacementneedper-centagewilloccurbetween2030and2040.

Cleanwatershedneeds(CWNs)arebasedonwaterqualityproblems,water-quality-relatedpublichealthproblemsthatexistedonJanuary1oftheCWNs’date,orthatwereexpectedtooccurwithinthenext20years.Forexample,theneedsidentifiedinthe2008CWNsarethoseexpectedfrom2008through2027.Oftheothersectors,WWOsconstitutethelargestportionofthewastewaterandwetweatherneeds;theneedforWWOshasremainedrelativelyconstantsince1996.Incontrast,severaltypesofneedshaveincreasedconsiderably.Bothcategoriesrelatedtothetreatmentplantsthemselves—secondarytreat-mentandadvancedwastewatertreatment—haverisingneeds.Theneedsrelatedtotheconstruc-tionofnewpipesarealsorising.Theneedsforwetweatherhandlingincreaseddramaticallybetween2004and2008,likelyreflectingthenewPhase2MS4requirementsthatbegantotakeeffectacrossthecountryintheearly2000s.

3.1 capital needs, 2010–40Fordrinking-water,wastewater,andwetweathermanagement,Figure4presentspastandprojectedspendingandthecapitalgapthat

islikelytooccurshouldfuturespendingfollowthispath.AsshowninTable6,theoverallcapitalgapforwaterinfrastructure—whichincludesdrinking-water,wastewater,andwetweather—isalreadysignificant:$54.8billionin2010.IfspendingincreasesatthemodestbuthistoricallyconsistentrateshowninFigure4,thegapwillincreaseto$84.4billionby2020and$143.7bil-lionby2040(inconstant2010dollars).19

Additionalfactorsmayresultinadditionalcostsinthefuture,whicharenotconsideredinthisgapanalysis.Thesemayincludethecon-sequencesofclimatechange—watershortages,flooddamagetoinfrastructure,andinfluxesofsaltwaterinnear-coastaquifers,andalsotheneedtoconstructandoperatemoretechnologi-callyadvancedandenergy-intensivetreatmentfacilities—wastewaterrecycling,theremovalofnewlyregulatedcontaminants,anddesalination.20

Thegapanalysisforroutineoperationsandmaintenance(O&M)needsindicatesthatifO&Mspendingcontinuestoincreaseataratesimilartothepast,spendingshouldkeeppacewithneeds,andnogapshoulddevelop.Thisisanunsurprisingoutcome,giventhatO&MneedsaregenerallyfundedthroughuserfeesandrateincreasesthatareintroducedtocoverrisingO&Mcosts.ThisresultisalsoconsistentwiththeEPA’sgapanalysis,whichfoundthatconsis-tentsmallincreasesinrateswouldbegenerallysufficienttopayforincreasingO&Mneeds.21

Year Spending need gap

2010 36.4 91.2 54.8

2020 41.5 125.9 84.4

2040 51.7 195.4 143.7

sourCesNeedscalculatedfromEPA(1997a,1997b,2001,2003,2005,2008,2009,2010).SpendingcalculatedfromCBO(2010)andUSCB(2011a,2011b).ConsumerpriceindexadjustmentfromBLS(2011).

Table 6★ overall annual capital Gap for Water infrastructure in 2010, 2020, and 2040 (2010 dollars in billions)

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 19

However,aspecialburdenwillbeplacedonhouseholdsandbusinessesincitiesthathaveexperiencedpopulationdeclinesduringthelasthalf-century.

O&Mexpendituresforbothdrinking-waterandwastewatertreatmentinfrastructurehaveincreasedsteadilyoverthelastseveraldecades,

withspendingincreasingmorerapidlyintherecentpast.TheAmericanWaterWorksAsso-ciation(AWWA)hasnamedthistheDawnoftheReplacementEra,withthewaveofincreasedspendingpredictedtolast30yearsormore.22Theearliestpipesinstalledinthelate19thcen-turyhaveanaveragelifespanofabout120years,

Figure 4★ overall capital investment Gap for u.S. Water infrastructure, 1956–2040 (billions of 2010 dollars)

0

50

100

150

200

Capital gap

Capital spending

20

40

20

37

20

34

20

31

20

28

20

25

20

22

20

19

20

16

20

13

20

10

20

07

20

04

20

01

19

98

19

95

19

92

19

89

19

86

19

83

19

80

19

77

19

74

19

71

19

68

19

65

19

62

19

59

19

56

sourCesNeedscalculatedfromEPA(1997a,1997b,2001,2003,2005,2008,2009,2010).SpendingcalculatedfromCBO(2010)andUSCB(2011a,2011b).ConsumerpriceindexadjustmentfromBLS(2011).ProjectionsbyDownstreamStrategiesandEDRGroup.

nTotalCapitalGapnTotalCapitalSpending

20 American Society of Civil Engineers

butpipesinstalledafterWorldWarIIhaveashorterlifespan—about75years.Forthisreason,severalgenerationsofpipewillreachtheendoftheirusablelifewithinacoupleofdecades.Watermainsmustbereplacedregardlessofthenumberofcurrentusers,andbecauseO&Mneedsarefulfilledbytaxpayers,asmallerpopu-lationtranslatestohigherpercapitareplacementcosts.Also,smallandruralwaterutilitieswillexperiencehigher-than-averagepercapitareplacementcostsduetotheimpactofalackofeconomiesofscale.23

Figure5showsthedifferenceinneeds,expectedinvestments,andexpectedgapsfordrinking-waterandwastewatertreatmentfor2010,2020,and2040.Totalneedsfordrinking-waterdeliveryinfrastructureareestimatedtohavebeen$35billionin2010,andescalateto$48billionby2020and$74billionby2040(allvalues

arein2010dollars).Althoughmorethanhalfofdrinking-waterneedswerefundedin2010(58percentofthetotalneed),thedollarsexpectedtobeinvestedfalltounder50percentofthetotalneedby2020andto40percentby2040.Inlook-ingatthewastewatertreatmentinfrastructure,theestimateoftotalneedin2010is$40billion,escalatingto$78billionin2020andtonearly$122billionby2040.However,in2010,lessthan30percentofwastewaterinfrastructureneedsweremet,andthisratioofinvestmenttototalneedisexpectedtofallto23percentby2020andto18percentby2040.

Overall,underpresentconsumptiontrendsandtechnologies,theU.S.willneed$126billionininvestmentforwaterandwastewatertreat-mentinfrastructureby2020,and$196billionby2040.However,basedoncurrentinvestment

Figure 5★ expected Wastewater treatment and Drinking-Water infrastructure needs and investments in the u.S., 2011, 2020 and 2040 (billions of 2010 dollars)

sourCesNeedscalculatedfromEPA(1997a,1997b,2001,2003,2005,2008,2009,2010).SpendingcalculatedfromCBO(2010)andUSCB(2011a,2011b).ConsumerpriceindexadjustmentfromBLS(2011).ProjectionsbyDownstreamStrategiesandEDRGroup.

nFundednUnfunded

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

% Unfunded

a

2040

2020

2011

2040

2020

2011

WaSteWater

treatment

DrinkinG Water

$16.1 billion $42.2 billion

$20.8 billion $15.5 billion

$18.0 billion $60.0 billion

$23.5 billion $24.5 billion

$22.2 billion $99.5 billion

$29.5 billion $44.3 billion

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 21

patterns,only33centsonthedollarwillbefundedin2020,fallingto26centsby2040.

EPAdocumentshistoricalcapitalspendingandtrendsinfour-yeartimespansforwaterdeliveryinvestments(1995–2007)andwaste-watertreatmentinfrastructure(1996–2008).Inconstant2010dollars,historicaltrendsshowfed-eral,state,andlocalgovernmentinvestmentsinwaterdeliveryrisingby64percentfrom1995to2007andinwastewatertreatmentsystemsby43percentfrom1996to2008.However,giventheagingofcurrentinfrastructurecoupledwithnationalpopulationgrowth,totalcapitalneedsincreasedby94percentfordrinking-waterand115percentforwastewatertreatmentduringthesameperiods.AsshowninTable7,thisgapisexpectedtobefurtherexacerbatedby2040.

Onatrends-extendedbasis,capitalspendingforwaterdeliveryandwastewatertreatmentinfrastructureisexpectedtocontinuallyincreasefromnowto2040.Inconstant2010value,thedataavailablefromthemid-1950sshowthatcapitalspendingforwaterdeliveryhasgrownfrom$6billionin1956,to$21billionin2007.16Similarly,capitalspendingforwaste-watertreatmentinfrastructurewas$4billionin1956and$18billionin2007.Thesetrendsimplyaninvestmentof$30billionfordrinking-waterand$22billionforwastewaterby2040.Figures6and7illustratethehistoricalandtrendsextendedextrapolationsofwaterandwastewatertreatmentinfrastructure.

Althoughcapitalinvestmentinupgradedwaterandwastewatertreatmentinfrastructureisexpectedtoincreasethrough2040,needs,

Table 7★ changes in u.S. capital Spending by Federal, State, and local Governments for Water Delivery and Wastewater treatment, 1995–2040

Year or change Spending needS

Water delivery 1995 a $13 $17

2007 a $21 $33

% change, 1995–2007 64 94

2040 b $29 $74

% change, 2007–40 40 121

Wastewater treatment 1996 a $11 $24

2008 a $15 $52

% change, 1996–2008 43 115

2040 b $22 $122

% change, 2008–40 43 136

notePercentagesmaynotcalculateduetorounding.aHistorical.bTrends-extendedprojection.

sourCesEPA1995to2008andtrendsexpendedprojectionsfrom2007(water)and2008(wastewater)through2040,calculatedbyDownstreamStrategies.

22 American Society of Civil Engineers

Figure 7★ annual capital needs, 1995–2040 (billions of 2010 dollars)

nDrinking-waternWastewaterandWetWeatherOverflows

0

20

40

60

80

100

120

140

2040203520302025202020152010200520001995

sourCesEPAto2008(water)and2009(wastewaterandwetweather),Trend-lineprojectionfrom2008(water)and2009(wastewaterandwetweather)through2040calculatedbyDownstreamStrategies.

Figure 6★ Spending by Federal, State, and local Governments, 1956–2040(billions of 2010 dollars)

nWaterDeliveryCapitalnWastewaterTreatmentCapital

0

5

10

15

20

25

30

35

204020352030202520202015201020052000199519901985198019751970196519601956

sourCesEPAto2007(water)and2008(wastewater),trend-lineprojectionfrom2007(water)and2008(wastewater)through2040calculatedbyDownstreamStrategies.

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 23

andthereforethecapitalspendinggapisexpectedtogrowatafasterratethanspendingoverthecoming30years.

3.2 comparison of the gap to the national economyThegapbetweenexpectedcapitalneedsandexpendituresforwaterdeliveryandwastewatertreatmentinfrastructureisexpectedtogrowfasterthangrowthinemployment,income,andGDP.Thisistrue,evenbeforeaccountingformacroeconomicimpactsfromashortfallin

waterandwastewaterinfrastructureinvest-ment,nottomentiontheneedstoaddressfailinginfrastructureinsurfacetransportation,energytransmissionservices,marineports,andairports.AsshowninTable8,thewaterandwastewatertreatmentinfrastructureinvest-mentgapgrowsatfasterratesthanincomeorGDP,whetherintotalvaluesorweightedbypopulation.Thegrowthofthegapwillplaceincreasinglygreaterstrainsonhouseholdsandindustriesbetweentodayand2040.

meaSure annual value (2010 dollarS) percenT change

2010 2020 2040 2010–20 2020–40 2010–40

aGGreGate

Water infrastructure gap (billions) $54.8 $84.4 $143.7 54 70 162

U.S. GDP (billions) $14,613 $19,066 $28,453 30 49 95

Personal income (billions) $6,446 $9,236 $14,581 43 58 126

WeiGHteD

Gap per capita $177 $248 $354 40 43 100

Gap per household $464 $645 $916 39 42 97

Per capita income $20,795 $27,085 $35,913 30 33 73

Per worker income $49,655 $61,853 $84,749 25 37 71

GDP per capita $47,139 $55,911 $70,080 19 25 49

GDP per worker $112,561 $127,680 $165,380 13 30 47

note“Aggregatemeasures”aredisplayedinbillionsof2010dollars.However,“weightedmeasures”areshowninsingle2010dollarsandarenotrounded.

sourCesMoodys.comforprojectionsforemployment,GDP,andpersonalincome.PopulationandhouseholdhadareguidedbytheprojectionsoftheSocialSecurityAdministrationandwereaggregatedbytheINFORUMresearchunitoftheUniversityofMaryland.

Table 8★ comparative changes of the Water and Wastewater treatment capital Spending Gap and the u.S. economy in 2010, 2020, and 2040

24 American Society of Civil Engineers

regionaloVerVieW

4.1 building new infrastructure

the need for new water infrastructure in the united States will

generally parallel increases in population and economic activity,

unless new needs are addressed by increasing the efficiency of

existing systems. as shown in Figures 8 and 9, population and

economic activity (measured as gross regional product) are grow-

ing fastest in the nation’s Far West, rocky mountains, Southeast,

and Southwest regions. a fifth region, the mid-atlantic, has also

experienced rapid economic growth. therefore, these regions are

expected to be significantly impacted due to the expansion needs

for existing water, sewer, and wet weather management systems.

4.2 maintaining the existing infrastructure

every four years, the ePa compiles needs assessments for

drinking-water and wastewater infrastructure. these assess-

ments are instructive in helping to identify which regions

are most in need of investments to repair or replace existing

infrastructure.

4

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 25

Figure10summarizesthemostrecentdrinking-waterneedssurvey,whichcompilesneedsoverthenext20years.Needsaregreaterthan$1,000perpersoninfiveregions:FarWest,GreatLakes,Mid-Atlantic,Plains,andSouthwest.

AsshowninFigure10,theMid-Atlanticregionhasparticularlyhighpercapitaneedstoaddresswastewaterandwetweatherneeds.Otherregionswithneedsgreaterthan$800perpersonincludetheFarWest,GreatLakes,NewEngland,andPlains.

TheGreatLakesandMid-Atlanticregionshaveparticularlylargeneedstoaddresswet

weathermanagementtopreventrawsewagefromdischargingintostreams,lakes,andtheAtlanticOcean.Morethan80percentofthetotalprojectedWWOneedsduringthenext20yearswilloccurwithinthesetworegions.

AssummarizedinTable9,theFarWest,Mid-Atlantic,andSouthwestregionshavesig-nificantconcernsforbothbuildingnewwaterinfrastructuretosupportpopulationandeco-nomicgrowth,andalsoformaintainingexistinginfrastructure.Allotherregionshaveconcernsregardingoneortheothercategory—buildingnewormaintainingexistinginfrastructure.

Figure 8★ u.S. Population Growth by region, 2000–2010

0

10

20

30

40

50

60

70

80

90

SouthwestSoutheastRockyMountain

PlainsNewEngland

Mid-AtlanticGreatLakes

FarWest0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

sourCeUSCB(2000,2010).

n2000(million)n2010(million)nAverageAnnualGrowth,2000–2010(%)

Po

Pu

la

tio

n

av

er

aG

e a

nn

ua

l G

ro

Wt

H

26 American Society of Civil Engineers

Figure 9★ Gross regional Product Growth, 2000–2010

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

SouthwestSoutheastRockyMountain

PlainsNewEngland

Mid-AtlanticGreatLakes

Far West0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

sourCesGDPfromBEA(2011).ConsumerpriceindexadjustmentfromBLS(2011).

n2000(trillion)n2010(trillion)nAverageAnnualGrowth,2000–2010(%)

GD

P

av

er

aG

e a

nn

ua

l G

ro

Wt

H

population and economic activity are growing fastest in the nation’s Far West, rocky mountains, Southeast, and Southwest regions. a fifth region, the mid-atlantic, has also experienced rapid economic growth.

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 27

Figure 10★ Per capita 20-Year needs by region

$0$200$400$600$800

$1,000$1,200$1,400$1,600$1,800

$2,000

SouthwestSoutheastRocky Mountain

PlainsNew England

Mid-AtlanticGreat Lakes

Far West

sourCesEPA(2009,2010).PopulationfromUSCB(2010).

nDrinkingWaternWastewaterandStormwaternWetWeatherOverflows

mainTaining exiSTing mainTaining exiSTing

building neW drinking-WaTer WaSTeWaTer and WeT

region inFraSTrucTure inFraSTrucTure WeaTher inFraSTrucTure

Far West X X X

Great Lakes X X

Mid-Atlantic X X X

New England X

Plains X X

Rocky Mountains X

Southeast X

Southwest X X

noteRegionsareagglomerationsofstatesandthereforeissuedfacedbyindividualstates,citiesorsubstateareasaresubsumedintheoverallregionaltotals.Forexample,buildingnewinfrastructureisidentifiedasaneedintheRockyMountainRegion.YetinmetroareaslikeDenverthegreatestexpenditurewillbeinreplacingandupdatingexistinginfrastructure.

sourCesSynthesisbyDownstreamStrategiesandEDRGroupbasedonfigures8–10andassociateddiscussion.

Table 9★ regional concerns regarding Building new or maintaining the existing Water infrastructure

28 American Society of Civil Engineers

analYtiCalFrameWorK5

5.1 The Funding gap

the first step is comparing the two alternative scenarios, to

calculate the funding gap between what would be needed to

maintain the u.S. water and sewer infrastructure and operating

systems to meet anticipated future needs, and what is expected to

be spent given current investment trends. this chapter describes

the analytical process for calculating the 2010–40 funding gap.

in summary, the gap between needs and investment in water

and sewer infrastructure is $55 billion in 2010 and is expected

to grow to $144 billion (in 2010 dollars) by 2040 if present trends

in investment and demand by households and businesses continue.

5.2 costs incurred by households and businessesThesecondstepistoidentifythecostsincurredbyhouseholdsandbusinessesdur-ingthe2010–40periodifcurrentinvestmenttrendsprevailandthenation’swaterandsewerfacilitiesdegradeinperformanceandcapacity.Ouranalysisoftheseconsequencesisbasedoncombiningthefollowingfactors:

★ Averageratesforwaterandsewerserviceandpasttrendsofratechanges;

★ Estimatesofoperationandmaintenancechargesforself-supplysystems;

★ Numberofhouseholdsdependentonpublicwatersystems;

★ Adjustmentsformultiplehouseholdsandbusinessestablishmentsonasingleparcel;

★ Numberofestablishmentsbysizeandtype(commercial, industrial)thatdonotself-supply;and

★ Estimatesforcapitalcostsforconsuminghouseholdsandbusinessestoself-supplywaterandsewerservices.

Usingthesefactorsandtherelatedassump-tions,by2020theapproximate$84billionforecastannualdeficitforsustainingwater

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 29

deliveryandwastewatertreatmentinfra-structuremayleadto$38billionincostsforbusinessesandhouseholdsinthatyearandmorethan$200billionincumulativecostsfrom2011(Table2).Withthecontinuedgrowthofthegapto$144billionby2040,costsaccruingtobusi-nessesandhouseholdsmaybeanadditional$200billionthatyearandby2040amounttoacumulativetotalexceeding$2trillion.Keyanalysisandassumptionsarenotedbelow.

private Water and Sewer alternativesDiggingawellandinstallingasepticsystemisoneoptionforahouseholdandbusinesstorespondtoinadequateinfrastructure,althoughitisnotareasonableresponseforeverylocation(e.g.,acityoralocationwithoutwater,orplaceswherelegalregulationsprohibitsomeorallprivateoptions)orachoicethateverybusinessorhouseholdthatcoulddosowouldpick.Otherpossibleresponsesincludemovingahouseholdorbusinesstoaplacewithadequatewaterandwastewatertreatmentservices,andpurchasingandinstallingequipmentthatwillconservewater.Forthepurposeofthisstudy,weusethecustomer’sresponseofprivatizingasastand-inforallpossibleresponsesunderthepremisethatallpossibleresponsesincurcosts,

andthecostofprivatizationisareasonableproxyforotheradjustments.

Therateofannualself-supplyresponseisassumedtotracktheannualgrowthinthewaterandwastewaterinvestmentgap.Thus,asthegapworsensourscenarioshowsanincreasingnumberofbusinessesandhouseholdshedgingagainstthecostsassociatedwithdeterioratingwaterdeliveryandwastewatertreatmentandreliabilityofservices.

Self-supplycostsdifferbycountlessfactors.Somedependonlocation—includingtheprox-imityofthewatersourceandthescaleofconstructionrequiredtotapthesource—andonlocalregulations.Otherfactorsarerelatedtotheamountofwaterandthesizeofthesepticsystemsdesired.Relatedtothisisthesizeofahousingunit,includingdifferentscalesofsingle-familyhomesandmultifamilydevelopments.Forcommercialandindustrialuse,thetypeandsizeofthebusinessmustbetakenintoaccount,aswellaswhetherthebusinessphysicallystandsaloneorisinanofficebuildingorretailmall.

Wedevelopedoverarchingassumptionsaboutthecostofself-supplythroughaseriesofconsultationswithdesign-buildfirmsandcivilengineersindependentofASCE.Forcommercialandindustrialsectors,onetimecapitalcosts

Sector coStS, 2011–20 coStS, 2021–40 coStS, 2011–40

cumulaTive annual cumulaTive annual cumulaTive annual

Households $59 $6 $557 $28 $616 $21

Businesses $147 $15 $1,487 $74 $1,634 $54

totalS $206 $21 $2,044 $102 $2,250 $75

noteNumbersmaynotaddduetorounding.

sourCesEDRGroupbasedoninterviews,establishmentcounts,andsizesbysectorfromCounty Business Patterns,populationforecastsoftheU.S.Census,andforecastsofestablishmentsandhouseholdsprovidedbytheINFORUMGroupoftheUniversityofMaryland.

Table 2★ estimated costs for u.S. Households and Businesses due to unreliable Water and Wastewater infrastructure (billions of 2010 dollars)

30 American Society of Civil Engineers

rangefrom$500,000tomorethan$1.5million,thoughforthisstudysuchcostswerecappedat$1millionandwereassumedtobeatthelowerendofthescaleforallexceptthelargestbusi-nessestablishmentsintheU.S.Forhouseholds,diggingawellwasestimatedatatypicalrangeof$8,000to$10,000,andinstallingasepticsystemwasestimatedbetween$25,000and$50,000.24Privatecostsforannualoperationandmainte-nancewereestimatedbyintervieweesatrunningatabout$45,000forcommercialandindustrialuse,and$1,000forhouseholds.25

Itshouldbementionedthatnewtechnolo-giesandapproachesmayreducefuturewaterinfrastructureneeds.Forexample,manycit-ieshaverecentlyadoptedgreeninfrastructureapproachestowetweatheroverflowmanage-ment.Greenroofs,grassyswales,andraingardens,forexample,areusedtoinfiltrate,evapotranspire,andcaptureandreuseraintomimicnaturalwatersystems.Suchtechniquesoftenprovidefinancialsavingstocommunities.

average Water ratesThe2010 Water and Wastewater SurveybytheAmericanWaterWorksAssociationreportedwaterandwastewaterratesfor308waterutili-tiesand228wastewaterutilitiesbysizeofutilityandmillionsofgallonsperdayconsumedbyusers.Fiveclassesofresidentialrangesandfourclassesofcommercialandindustrialrangeswereidentified.Weaveragedtheratesandchargesforresidential,commercial,andindustrialcustom-ersnationallyandbymultistateregionaccordingtothelocationandsizeofeachutility.

number of businesses and householdsOurdataonthenumberofbusinessestablish-mentsbysizeandregionweretakenfromU.S. County Business Patternsandaggregatedbycommercialandindustrialclassifications.Themostrecentdataavailablearefor2009,andthesedatawereprojectedto2040basedonemploy-mentprojectsbysectorobtainedfromMoodys.com.HouseholdprojectionswereprovidedbytheINFORUMResearchUnitoftheUniversity

ofMarylandandwereguidedbyprojectionsfromtheSocialSecurityAdministration.

costs among industries and householdsThemostrecentnationalanalysisbysectorbasedonU.S.GeologicalSurveydatawasconductedin1995andshowsthathouseholdsaccountfor56percentofpublicwaterdemand,commercialsectorsaccountfor17percent,industrialsec-torsaccountfor12percent,andpublicusesandlossesmakeuptheremaining15percent.Tenyearslater,theanalysiswascompletedwithoutthisdegreeofdetail,butitshowsthathouseholdsdraw58percentofwaternationally,whichwassimilartothe1995findings.Ifthecostofwaterrisesduetodeficientinfrastructure,thequestionishowcostswillbespreadacrosstheeconomy.Westartedwiththebaseofdemandacrossbroadlydefinedsectors:56percenthouseholds,17percentcommercialestablishments,and12percentindustrialestablishments.Wethenmadeanassumptionthathouseholds,whicharemadeupofvoters,willinsistthatcostsbeassignedtobusinesses,followingthepatternofmanycom-munitiesthathavedualpropertytaxratesanddualutilityrates—oneforhouseholds,andoneforbusinesses.Forthisanalysis,futurecostsareallo-catedtohouseholdsat33percent,thecommercialsectorat24percent,andtheindustrialsectorat28percent.Thesignificantincreaseintheindus-trialsector’sshareisbasedonthelistofkeywaterdependentindustries,whichareallindus-trial,and28ofthetop30water-intensivesectors,includingthetop20,areindustrial.26

The incidence of Waterborne illnessesDeficienciesinthesystemsusedforthepublic-provisionofdrinkingwaterandthehandlingofwastewaterandstormwatercantriggerbacterialandviraloutbreaks.TheEPAandtheCentersforDiseaseControlandPreventionhavetrackedthe30-year27incidenceofwater-borneillnessesacrosstheU.S.,categorizedthetypeofillness,andhavedevelopedamonetaryburdenforthosecases.Basedontheannualpercentageincreaseinthecapitalspendinggapprojectedthrough

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 31

2040,themonetaryburdenforwater-borneill-nessisestimatedtobe$413millionfor2011–20and$1.3billionfor2021–40.28Toputthesecostsinperspective,by2040theU.S.percapitacumu-lativeimpactsofwater-borneillnessesinthefaceofanincreasinginfrastructuregapareestimatedtobe$4.89andtofluctuatebetween$.11and$.21peryearfrom2011to2040.AWorldHealthOrganizationreportestimatesthatthepercapitaworldwideeffectsofwater-borneillnesseswillbe$98in2015.29

adjustments for multiple households and business establishments on Single parcelsThefindingsdiscussedabovewereadjustedtoreflectmultiplehousingunitsandbusinessestab-lishmentsonsingleparcelsbasedonnationaldata.AccordingtothedatareportedbytheU.S.CensusBureau’s“2005–2009AmericanCommunitySur-vey,”roughly128millionhousingunitsareplacedon100millionparcels.Therefore,thehouseholdimpactswerediscountedby21.5percent.

Inaddition,theU.S.EnergyInformationAdministration(EIA)calculatedthat705,000officebuildingsintheU.S.containatotalof1.6millionestablishments,anaverageof2.3perbuilding.Thisisslightlymorethantheaveragenumberofestablishmentsinothertypesofcommercialbuildings(1.7perbuilding)andretail(1.8perbuilding).Nevertheless,alargemajority(70percent)ofofficebuildingshaveonlyoneestablishment.Tobecautious,theofficeratioof2.3wasusedforthisanalysis,andcommercialestablishmentswerediscountedby56.5percent.30UsingtheEIAaverageof1.7wouldproducealowerreductionofestablish-ments(e.g.,usingthe1.7averagewouldresultinareductionrateof41percent).

The broader effects on the nation’s economyThefinalstepistocalculatehowthesecostsultimatelyaffectthenation’seconomy.First,theaddedcostsoffailingtoadequatelyinvestinwaterandsewerinfrastructurewereallocatedtoindustriesandsectorsoftheeconomybasedon

waterrelianceandusagerates.ThentheLIFT(Long-termInter-industryForecastingTool)economicmodelwasusedtocalculatehowtheseaddedhouseholdandbusinesscostswill,overtime,ultimatelyaffectexpenditurepatternsandbusinessproductivityamongindustries,leadingtochangesinthenation’scompetitivenessandeconomicgrowth.Theresultsareprovidedaslong-termchangesinjobsandincomeintheU.S.TheLIFTmodelisanationalpolicyandimpactforecastingsystemdevelopedbyINFORUM,aresearchcenterwithintheDepartmentofEconomicsattheUniversityofMaryland,CollegePark.

5.3 Water-intensive industriesThissectionexaminessectorsoftheU.S.econ-omythataremostdependentonpublicwater/wastewaterinfrastructure.Morikawaetal.(2007)lists11industrysectorsthatarehighlydependentonwaterresourcesorvulnerabletowaterrisks.Thesearenotnecessarilytheelevenmostwater-intensiveindustriesacrosstheU.S.butareindustriesthatmostrelyondependablecleanwatersupply.Thereisoverlapinthewater-intensiveandwater-dependentanalysespresented(chemicals,beverages,foodprocess-ing,butnotablycoreindustriesofautomobilemanufacturing,biotechnology/pharmaceuticalsandelectronicsareclassifiedasamongthemostwaterdependentsectorsintheU.S.economy.Thesearekeyindustrialsectorsofthenationaleconomy,andinclude:

★ Apparel★ Automobile.★ Beverage.★ Biotech/Pharmaceutical★ Chemical,★ ForestProducts,★ FoodManufacturing,★ High-technology/Electronics,★ Metal/Mining,★ Refining,and★ Utilities.

32 American Society of Civil Engineers

Ontheotherhand,Blackhurstetal.(2010)esti-matewaterwithdrawalsfor426sectorsintheU.S.economy.TheystartwithUSGSdatafrom2000,andfirstdisaggregatethepublicsupplysector.Householddeliveriesfrompublicsupplyaresubtractedfromtotalpublicsupply,andtheremainingwaterisallocatedto379economicsectorsbasedontheirshareofpurchasesfromthe“water,sewageandothersystems”sector.31Forsectorswithunreporteddata,theauthorsusecomparableratesforsimilarservicesectors.Theauthorsthenaddinself-suppliedindustrialwithdrawalsfor30sectorsinthefollowingindustries:food,textile,wood,paper,petroleum,chemical,plastic,andprimarymetals.Black-hurst’sfindingsconcludethat15ofthe20mostwater-intensivesectors,measuredbydirect

wateruseperdollarofoutput,arecomprisedofagricultural,miningorpowergenerationindus-triesand,therefore,likelyrelyonself-suppliedwaterandwastewaterservices.

Table10 illustratesthe10mostwater-intensivesectorsotherthanagricultural,mining,andelectricpowergenerationsectors,whichtogetheraccountforpreponderancelargeproportionofself-suppliedwater.Awiderangeofindustriesarewater-dependent.Thetoptwosectors,aswellasseveralothers,arewithinthechemicalindustry.Itisimportanttonotethatthisincludesestimatesofbothpubliclysuppliedandself-suppliedwater,andtherefore,doesnotprovideadirectestimateofthesectorsthatmostrelyonpublicwaterinfrastructure.

induSTrY gallonS/$ ouTpuT

Paint & coating manufacturing 123

Alkalies & chlorine manufacturing 38

Paperboard mills 36

Wineries 34

Pesticide & other agricultural chemical manufacturing 30

Synthetic dye & pigment manufacturing 27

Adhesive manufacturing 21

Industrial gas manufacturing 21

Distilleries 14

Poultry processing 14

Next 20 most intensive sectors 128

sourCeBlackhurstetal.(2010)SupplementalMaterials.Note:Theseestimatesincludeself-suppliedwaterandwaterpurchasedfromprivatewaterandsewersystems,butdonotincludewaterpurchasedfromgovernment-ownedsystems.Estimatesexcludeagricultural,mining,andelectricalpowergenerationsectors,whichareprimarilyself-supplied.

Table 10★ top Water-intensive industries in the u.S. (direct water use per dollar output)

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 33

eConomiCimPaCts

negative impacts on the u.S. economy are a result of businesses and

households managing unreliable water delivery and wastewater

treatment services, which in turn result from a lack of investment

in the national water network. Strategies such as relocation, invest-

ing in conservation technologies, and self-supplying services can

create costs that reduce business income (and, as a consequence,

productivity and wages). costs associated with water-borne

illnesses and higher utility rates divert income from other uses.

6

Thereporthasexaminedtheseeffectsintwoways.First,thereportassumesthathouseholdsandbusinessesdonotadjustbehaviororimplementtechnologiesbeyondwhatisbeingdonetoday,andthatnewconservationmethodsandtechnologiesarenotimplemented.However,inasecondapproach,businessesandhouseholdsareassumedtoadjusttounreliablewaterdeliv-eryandwastewatertreatmentservicebystrengtheningtheirconservationeffortsinproductionanddailywateruse.

6.1 current circumstances

overviewUnlessinvestmentincreasesinwaterinfra-structureortechnology/conservationsolutionschange,thefollowingeconomicoutcomesareexpected:

★ About$734billioninbusinesssaleswillbelostcumulativelyinthenext10years,from2011to2020.

★ By2040,thetotalwillamountto$7.5trillionover30years.

★ Thelossofbusinesssaleswillinclude$416billioninGDPfrom2011to2020,repre-sentingtheactualproductivityintheU.S.

★ By2040,thecumulativelostGDPwillexceed$4trillion(Table3).

34 American Society of Civil Engineers

diSpoSable diSpoSable diSpoSable

perSonal perSonal perSonal

JobS income income income per

(rounded (billionS oF per capiTa houSehold

Year To 100,000) 2010 dollarS) (2010 dollarS) (2010 dollarS)

Average annual losses, 2011–20 – 400,000 – $54 – $200 – $400

Average annual losses, 2021–40 – 1,200,000 – $222 – $600 – $1,500

Average annual losses, 2011–40 – 900,000 – $166 – $500 – $1,200

Cumulative losses, 2011–20 N.A. – $541 – $1,700 – $4,300

Cumulative losses, 2021–40 N.A. – $4,440 – $11,800 – $30,700

Cumulative losses, 2011-40 N.A. – $4,981 – $13,900 – $36,000

noteLossesinjobsandincomereflectimpactsinagivenyearagainsttotalnationaljobsandincomeinthatyear.Thesemeasuresdonotindicatedeclinesfrom2010levels.Totaldisposablepersonalincomeisinbillionsof2010dollars.Percapitalandperhouseholdaveragesarein2010dollarsroundedtothenearest$100.N.A.=notapplicable.

sourCesEDRGroupandLIFTmodel,UniversityofMaryland,INFORUMGroup,2011.

Table 11★ effects on total u.S. Jobs and Personal income Due to Declining Water Delivery and Wastewater treatment infrastructure Systems, 2011–40 (billions of 2010 dollars, unless noted)

Year buSineSS SaleS gdp

Losses in the Year 2020 – $140 – $81

Losses in the Year 2040 – $481 – $252

Average Annual Losses 2011–2020 – $73 – $42

Average Annual Losses 2011–2040 – $251 – $137

Cumulative Losses 2011–2020 – $734 – $416

Cumulative Losses 2011–2040 – $7.5 Trillion – $4.1 Trillion

noteLossesinbusinesssalesandGDPreflectimpactsinagivenyearagainsttotalnationalbusinesssalesandGDPinthatyear.Thesemeasuresdonotindicatedeclinesfrom2010levels.

sourCesEDRGroupandLIFTmodel,UniversityofMaryland,INFORUMGroup,2011

Table 3★ effects on total u.S. Business Sales and GDP due to Declining Water Delivery and Wastewater treatment infrastructure Systems, 2011–40 (billions of 2010 dollars unless noted)

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 35

AsshowninTable11,theselossesinbusinesssalesandGDPwillleadtojobandpersonalincomedeclines.Onaverage,annualjobslosseswillbe367,000eachyearfromduring2011to2020,andmorethan900,000jobsannuallywouldbelostduringthe30-yearspanfrom2011to2040.Joblossesareexpectedtobe669,000by2020andreach1.4millionby2040.Overall,disposablepersonalincomewilldecreasebyatotalof$541billionfrom2011to2020,atanaver-ageof$54billionperyear,andtotalnearly$5trillionfrom2011to2040,whichisanannual

SecTor 2020 2040

Agricultural services and food products – 10,000 – 28,000

Construction – 71,000 – 151,000

Knowledge sector services (excluding medical services)a – 159,000 – 381,000

Medical services – 15,000 223,000

Mining and refining – 1,000 – 3,000

Retail trade – 199,000 – 425,000

Restaurants, bars, and hotels – 63,000 – 175,000

Technology/electronics manufacturing – 4,000 – 11,000

Transportation equipment – 6,000 – 23,000

Transportation services – 16,000 – 51,000

Utilities – 9,000 – 29,000

Wholesale trade – 32,000 – 83,000

Other services and entertainment – 36,000 – 123,000

Other manufacturing – 48,000 – 117,000

total – 669,000 – 1,377,000

aKnowledgesectorservicesgenerallyincludesthemedicalsector.However,duetothepotentialofanincreaseinwater-borneillnessesboughtonbydecayinginfrastructure,thedemandformedicalservicesmayincrease,andthereforetheimpactsaredisplayedseparately.

sourCesEDRGroupandLIFTmodel,UniversityofMaryland,INFORUMGroup,2011.

Table 12★ Potential employment impacts as a consequence of Failing Water and Wastewater infrastructure, 2020 and 2040

on average, annual jobs losses will be 367,000 each year from during 2011 to 2020, and more than 900,000 jobs annually would be lost during the 30-year span from 2011 to 2040.

36 American Society of Civil Engineers

averageof$166billionperyearinlostincomefor30years.By2020,theimpactisexpectedtobealmost$900perhouseholdintermsoflostincomeandoutofpocketexpensesforcostsassociatedwithdeficientinfrastructure.

Givencurrentlevelsofinvestment,capitalinvestmentneeds,anddemandtrends,alongwiththedeteriorationofthewaterdeliveryandwastewatertreatmentinfrastructure,thissce-nariocouldcosttheU.S.nearly700,000jobsin2020and1.4millionjobsoverwhatisotherwiseforecastfor2040.

Thethreesectorsthatwilllosethegreatestnumberofjobsareretail,restaurantsandbars,andconstruction,resultingfromacombinationoflessdisposableincome,increasedwatercosts,andtheincreasingcostsofwater-basedgoods.Inaddition,retailimpactsarelikelyduetohigherintermediate-inputprices,andlessdiscretionaryspendingbyhouseholdsbecausetheyhavehealthcostsduetocontaminatedsystems.Constructionimpactscanbetracedtoageneralincomedeclineamonghouseholdsandcorporations,andtheaddedcostsofconstructionmaterialsthatrequirewatereitherinfactoriesoronconstructionsites.Thisisinthecontextoftheoveralleconomyshowingalmost$481millionlessindustrialout-putand$300millionlessdisposablepersonalincomein2040(in2010dollars).

Theimpactsoftheseinfrastructure-relatedjoblosseswillbespreadthroughouttheeconomyinlow-wage,middle-wageandhigh-wagejobs.In2020,almost500,000jobswillbethreatenedinsectorsthathavebeentraditionalemployersofpeoplewithoutextensiveformaleducationsorentry-levelworkers.32Conversely,ingenerallyacceptedhigh-endsectorsoftheeconomy,184,000jobswillbeatrisk.33Unlesstheinfra-structuregapisaddressed,by2040itsimpactswillputatriskalmost1.2millionjobswithinbasicsectors,whilearelativelystablenetamountof192,000jobsinknowledge-basedindustriesmaybejeopardized.Inthislattergrouping,approximately415,000jobswillbethreatened;however,medicalservicesareexpectedto

growbetween2020and2040duetoincreasingoutlaystofightwater-borneillnesses.34

Althoughassigningindustriestohigheduca-tioncategoriesisageneralization,theimpactwillclearlybefeltacrosssectors.

Theimpactsonjobsarearesultofcoststobusinessesandhouseholdsmanagingunreliablewaterdeliveryandwastewatertreatmentser-vices.Betweennowand2020,thecumulativelossinbusinesssaleswillbe$734billionandthecumulativelosstothenation’seconomywillbe$416billioninGDP(Table3).Impactsareexpectedtocontinuetoworsen.Intheyear2040alone,theimpactwillbe$481billioninlostbusinesssalesand$252billioninlostGDP.35Moreover,thesituationisexpectedtoworsenasthegapbetweenneedsandinvestmentcontin-uestogrowovertime.AverageannuallossesinGDPareestimatedtobe$42billionfrom2011to2020and$185millionfrom2021to2040.

exportsBy2020,exportsarelikelytoshowalossofapproximately$6billioncomparedwithexpectedexportlevels,whichrepresentsanalmost4per-centdecreaseinbusinesssalescomparedwithestimates(seeTable13).By2040,thelossofexports,whichrepresentinternationalbusinesssales,willbeasignificantportionoftheeconomicimpactsthatstemfromthefundinggapinwaterdeliveryandwastewatertreatmentinfrastruc-ture.Exportlossesareexpectedtoincreasesteadilyfrom2011to2040.However,by2040,theleveloflostexportdollarsisexpectedtorisetoalmost$77billion,whichrepresentsapprox-imately16percentofthelosttotalnationalbusinesssales.By2040,exportswillbelostin65ofthe91tradedsectors.Incontrasttodomesticeconomicimpacts,exportlosseswillbeheavilyfeltinthetechnologyandmanufacturingsectors—includingaerospace,instruments,anddrugs—andalsointheassociatedfinanceandprofessionalservicessectors.Thisrippleeffectillustratestheincreasingrateofexportchemicalproductlossesfrom2011through2040.Table14profileslossesbysectorin2040.

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 37

SecTor exporT dollarS loST (predicTed For 2040)

Aerospace – $10.7

Finance and insurance – $8.3

Equipment and machinery – $6.1

Wholesale trade – $5.9

Instruments – $4.7

Agricultural and food products – $4.2

Plastics and rubber products – $3.6

Chemical and drug products – $3.0

Air transportation – $2.6

Professional services – $2.2

SuBtotal – $51.5

Other sectors – $25.2

total – $76.7

noteLossesreflectimpactsinagivenyearagainsttotalnationalexportprojectionsfor2040.Thesemeasuresdonotindicatedeclinesfrom2010levels.

sourCesEDRGroupandLIFTmodel,UniversityofMaryland,INFORUMGroup,2011.

Table 14★ Potential u.S. export reductions by 2040 (billions of 2010 dollars)

cumulaTive annual average

period oF loSSeS exporT loSSeS exporT loSSeS

2011–20 – $20 – $2

2021–40 – $807 – $40

2011–40 – $828 – $28

noteLossesreflectimpactsinagivenyearagainsttotalnationalexportprojections.Thesemeasuresdonotindicatedeclinesfrom2010levels.

sourCesEDRGroupandLIFTmodel,UniversityofMaryland,INFORUMGroup,2011.

Table 13★ cumulative losses of u.S. exports (billions of 2010 dollars)

38 American Society of Civil Engineers

loSSeS adJuSTed STricT TrendS

Jobs, 2020 538,000 669,000

Jobs, 2040 615,000 1,377,000

GDP, 2020 $65 $81

GDP, 2040 $115 $252

Business sales, 2020 $115 $140

Business sales, 2040 $229 $481

Disposable personal income, 2020 $87 $106

Disposable personal income, 2040 $141 $292

annual averaGeS, 2011–20

Jobs 319,000 367,000

GDP $36 $42

Business sales $64 $73

Disposable personal income $48 $54

annual averaGeS, 2021–40

Jobs 720,000 1,195,000

GDP $111 $185

Business sales $208 $340

Disposable personal income $138 $222

sourCesEDRGroupandLIFTmodel,UniversityofMaryland,INFORUMGroup,2011.

Table 15★ comparison of Potential Scenarios (billions of 2010 dollars)

a strict “trends-extended” hypothesis shows declines that proceed much faster after 2020, as infrastructure worsens and the general approaches of households and businesses are to cut back on spending and investing due to the increasingly high cost of reliable delivery and sewer services.

Failure to Act: The Economic Impact of Current Investment Trends in Water and Wastewater Treatment Infrastructure 39