© 2011 Melbourne’s Northern Economic Wedge Inc

POST GFC SWOT: MELBOURNE’S NORTH

2

Post GFC SWOT: Melbourne’s NorthA study commissioned by NORTH Link with support from the Northern Melbourne Regional Development Australia Committee. This report was prepared by National Institute of Economic and Industry Research and provides a detailed analysis of the impact of the GFC and each of the seven LGA’s. The report includes recommendations and benchmarks that will support growth and quality employment outcomes for the region into the future as it undergoes the transition into a knowledge economy.

ConsultantsNational Institute of Economic and Industry Research (NIEIR)

Carmine Consulting

Cover and LayoutI.D.Yours

Copyright © 2011Melbourne’s Northern Economic Wedge Inc, trading as NORTH Link.

This work may not be reproduced in whole or in part or sold without written permission of NORTH Link.

Requests should be forwarded to NORTH Link, PO Box 103, Coburg 3058 [email protected]

DisclaimerEvery effort has been made to ensure that this report is free from error or omission. The information contained in this report has been derived in good faith from sources believed to be reliable and accurate. However, neither NORTH Link nor NIEIR nor any persons involved in the preparation of this report accept any liability whatsoever for any actions taken based on its contents or information.

EnquiriesMr Mick ButeraExecutive Director, NORTH Linkc/- Institute for Advanced StudyLa Trobe UniversityMain Drive, BUNDOORA 3086Telephone: 03 9479 3337Facsimile: 03 9467 8310Email: [email protected]

3

Post GFC SWOT: Melbourne’s North

EXECUTIVE SUMMARY 5

1. MELBOURNE’S NORTH ECONOMIC UPDATE POST GFC 6 1.1 Introduction 6 1.2 Victoria after the GFC 6 1.3 Initial impact of the GFC on the Victorian labour market 6 1.4 About Melbourne’s North 6

2. STRATEGIC ISSUES 8 2.1 Manufacturing and employment 8 2.2 Automotive manufacturing industry – opportunities example 10 2.3 Automotive and associated manufacturing industry 10 2.4 Jobs and skills where future opportunities exist 10 2.5 Significance of Melbourne Airport 10 2.6 Relocation of the Wholesale Market 10 2.7 Cost of carbon and redefining Melbourne’s North 11 2.8 High speed internet 11 2.9 Housing affordability, greenfield developments and the importance of public transport 11 2.10 Education and knowledge economy 12 2.11 Percentage of households with bachelor or higher qualification, 2012 (as highest qualification) 13 2.12 Benefiting from internationalisation 13 2.13 Amenity and environment 14 2.14 Energy use considerations 14 2.15 Transport system considerations 14 2.16 Industry considerations 14

3. MELBOURNE’S NORTH: REGIONAL SWOT 15 3.1 Strengths 15 3.2 Weaknesses 15 3.3 Opportunities 15 3.4 Export opportunities 16 3.5 Threats 16

CONTENTS

PAGE NO.

4

4. THE REGION DESCRIBED 17 4.1 The region compared 17 4.2 Overall employment growth 22 4.3 Resident employment 24 4.4 Unemployment 25 4.5 NIEIR unemployment rate 25

5. COMMENTARY BY LGA 26 5.1 LGA growth areas post GFC 26 5.2 Banyule since the GFC 26 5.3 Darebin since the GFC 27 5.4 Hume since the GFC 27 5.5 Moreland since the GFC 28 5.6 Nillumbik since the GFC 28 5.7 Whittlesea since the GFC 29 5.8 Yarra since the GFC 29 5.9 Employment growth 30 5.10 Pre GFC place of work and resident employment growth 37 5.11 Post GFC place of work and resident employment growth 37

APPENDIX A: GROSS PRODUCT DEFINITION AND DATA SOURCES 39

APPENDIX B:REGIONAL SUMMARY TABLES MELBOURNE’S NORTH 40

APPENDIX C: MELBOURNE’S NORTH LGA TABLES 47

PAGE NO.

CONTENTS CONTINUED

5

Post GFC SWOT: Melbourne’s North

Future policies that build on the opportunities for regional growth in the post GFC environment include:

redefining Melbourne’s North as a carbon efficient economy and society through improved energy efficiency of buildings, communities and distance and transport to employment

ongoing development of the knowledge economy, including maximising the benefit of the NBN to the region

planning for the future skills of residents – a region of education and skills development with policies to assist lower skilled workers in employment towards a carbon efficient economy

positioning Melbourne’s North as a gateway to Melbourne with major assets including tertiary institutions, health developments, businesses, the rapidly developing Melbourne Airport, transport infrastructure and the newly locating Wholesale Markets and taking advantage of the opportunities in which these things can be better connected to create significant future growth

policies to continually improve amenity while maintaining some degree of housing affordability.

Summaries on trends in each of the LGAs since the GFC are included in section 5 of this document.

The global financial crisis (GFC) had a profound effect on economies at local, state, federal and global levels. As a result, economies are permanently altered and new attitudes are required to ensure that growth in the future occurs and is sustainable.

The GFC had specific implications for Melbourne’s North, which comprises the local government areas (LGAs) of Banyule, Darebin, Hume, Moreland, Nillumbik, Whittlesea and Yarra. Employment, particularly in manufacturing (notably the automotive sector) has been adversely affected.

However, the region is experiencing increasing dynamism through residential growth, improving skills of residents, business development, diversity and amenity. There has been employment growth at Melbourne Airport and the relocation of the Melbourne Wholesale Fruit and Vegetable Market and other major developments will provide additional opportunities.

Threats to the economic development of the region in the current environment have been identified as:

offshoring employment, particularly in manufacturing

continued hollowing out of manufacturing supply chains

low skill levels of some residents and increasing skill demands of local industry

carbon pricing adversely affecting regional competitiveness, particularly exports

impact of economic development of India and China, particularly on manufacturing

strength of the Australian dollar.

EXECUTIVE SUMMARY

6

1.1 IntroductionThis report describes the current economic circumstances of each of northern Melbourne’s LGAs and their economic progress since the GFC.

The GFC has permanently altered the economic dynamics of the world and Victorian economies and it is highly unlikely once the stimulus effects have faded that things will go back to the way they were. Unless the crisis is understood, it will not be possible to plan for a more sustainable (if more subdued) future prosperity.

Countries that have unsustainably relied on increased credit over the last two decades to drive growth will have to return to the fundamentals to drive growth, namely industry development, knowledge creation and the accumulation of physical and human capital. This is a slower, longer-term process with paybacks extending over decades rather than months. In addition economies like the US and Australia, which have combined high growth with high current account deficits and high foreign borrowings, will find that they will have to curtail growth to levels consistent with the reduced availability of global finance.

Overall world growth will be slower, generally in the range of 3 to 4 per cent, rather than in excess of 5 per cent as was the case from 2003 to 2008.

1.2 Victoria after the GFCFactors limiting Victoria’s economic growth are likely to be:

household debt deleveraging

high interest rates (relative to the rest of the world)

decline in local content of major resource projects and high Victorian excess capacity

future carbon price shock.

1.3 Initial impact of the GFC on the Victorian labour marketBetween June quarter 2008 and June quarter 2009, the following occurred in Victoria:

Victorian full time employment fell by 32,400, or 1.7 per cent

Victorian part time employment increased by 17,100, or 2.1 per cent

total weekly hours worked fell by 2.3 million, or 2.5 per cent

most of the loss of full time positions was in the 15 to 24 age segment

households become disadvantaged by increased numbers of dependents and reduced total real incomes

the NIEIR unemployment level increased by 40,000 (see 4.1 for an explanation of the NIEIR unemployment rate).

1.4 About Melbourne’s North Melbourne’s North is a highly diverse and dynamic region that covers the LGAs of Banyule, Darebin, Hume, Moreland, Nillumbik, Whittlesea and Yarra. Its inner areas are rapidly transitioning to knowledge economy and creative industry type development as manufacturing, logistics and warehousing activities grow in the outer areas.

Melbourne’s North is evolving from a manufacturing region towards a knowledge economy region in which high tech manufacturing has been retained and significant research hubs are being developed. The region’s diverse and increasingly skilled residents provide an opportunity for the growth and relocation of businesses.

Inner areas such as Yarra, Northcote and Brunswick are strongholds of arts and entertainment and there are a number of quality residential precincts, with significant developments planned. With increasing infrastructure and major assets such as Melbourne Airport, freight hubs, transport networks and the relocating wholesale markets, the growth potential for Melbourne’s North is high. Yet the region still retains large areas of its natural environment combined with strong lifestyle attributes.

MELBOURNE’S NORTH ECONOMIC UPDATE POST GFC1

Post GFC SWOT: Melbourne’s North

7

The continuing development of Activity Centres and Central Activities Districts (such as Broadmeadows in Hume) are reshaping the way in which Melbourne conducts its business and social activities. These initiatives are broadening the emphasis of future development, from growth driven by core city-centric activities to a locally integrated model of commercial, industrial and residential development, strengthening existing centres in the region as well as developing new centres for growth.

The economic development task will be to build on current resources, infrastructure, businesses and skills to create new regional opportunities.

Different areas, different images – the following map describes the diversity and strengths of Melbourne’s North.

8

2.1 Manufacturing and employmentThe GFC created challenges for regions around the globe. For Melbourne’s North and particularly the rapidly developing LGA of Hume, there has been a decline in manufacturing employment in industries such as automotive. Many job losses have occurred as part of a realignment of global strategies forced on large international companies by the GFC. It has been difficult for local policy makers to influence this trend, which is driven by the cheaper prices available in China and elsewhere in Asia. Car sales improved after the GFC but high petrol costs and changing lifestyles are having an impact on large car sales, the traditional manufacturing niche for Australian-based automotive manufacturers. Ford has announced more job cuts that will further affect manufacturing employment numbers in Melbourne’s North.

Retraining is now a regional issue, along with networks for retrenched workers to find equivalently skilled and paid work. The capacity to compete for new employment may also be an issue for some Hume residents because of the low level of skills in at least part of the population.

If there are major automotive manufacturing closures or downsizing of operations in the region while new jobs are being created in other parts of the manufacturing sector (food processing for example), stranding of the lowest skilled workers in casual work or long term structural unemployment remains an issue for both Hume and Whittlesea.

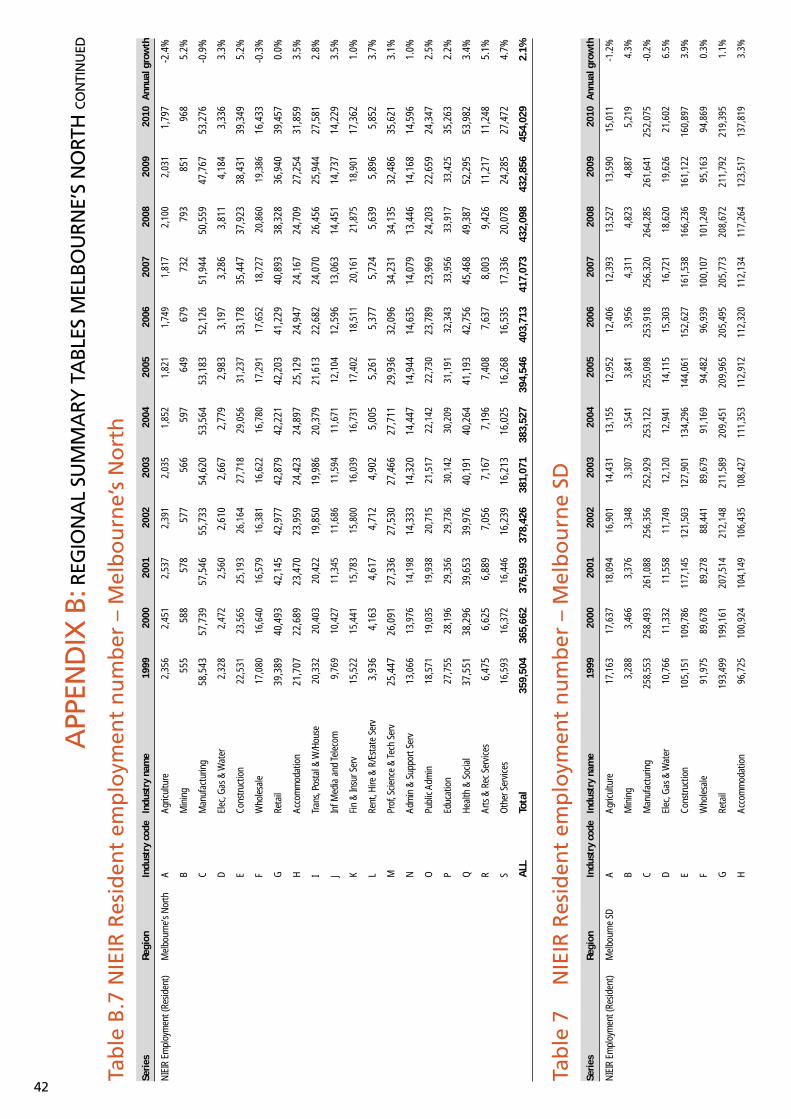

Table 2.1 gives the performance of the manufacturing sector in Melbourne’s North, Melbourne Statistical Division (SD) and Victoria between 1999 and 2010. For Melbourne’s North, the figures show a slight bounce-back in 2010 with the sector adding 1749 jobs in the year. This was not the case for the Melbourne SD, where job numbers declined overall.

Manufacturing sales, value add and exports also increased in Melbourne’s North in 2010. The reasons for this need further investigation but some of the improvement could be due to an increase in automotive manufacturing in the period after the GFC. Investment in the sector in Melbourne’s North has also held up reasonably well during and after the GFC period.

This section includes commentary on strategic issues that are likely to shape the future development of Melbourne’s North.

Table 2.1 Manufacturing

Region Sub Region Item Industry 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Melbourne MN Value added at factor cost ($m cmv) C 5810 5980 5771 5703 5585 5702 5554 5392 5160 5115 4866 5073

Melbourne MN Sales ($m cmv) C 18090 18743 18224 18153 17915 18425 18095 17718 17120 17078 16318 17033

Melbourne MN Investment ($m cmv) C 47 74 101 98 99 115 135 149 141 199 203 185

Melbourne MN Export ($m cmv) C 10391 11596 11811 11869 11794 11467 10917 10641 10557 10964 10503 10914

Melbourne MN Employment C 67219 67316 67260 65636 63636 60707 59164 58193 57963 58089 56477 58226

Melbourne All Value added at factor cost ($m cmv) C 22730 23449 22626 22730 22661 23961 24057 24013 23695 24082 23015 22521

Melbourne All Sales ($m cmv) C 72655 75394 73257 74091 74070 78625 79244 79409 78823 80657 77461 75872

Melbourne All Investment ($m cmv) C 240 381 524 516 523 614 728 815 776 1098 1123 1014

Melbourne All Export ($m cmv) C 43765 47564 48468 49969 49778 50036 48966 48220 48230 51883 51285 49635

Melbourne All Employment C 261709 262557 262162 259979 256485 253285 254306 256912 262248 269294 266409 258512

VIC All Value added at factor cost ($m cmv) C 28072 28806 27847 28049 28403 30211 30421 30405 29985 29591 28077 28508

VIC All Sales ($m cmv) C 91788 94670 92094 93295 94719 101006 101980 102200 101235 100367 95620 97466

VIC All Investment ($m cmv) C 310 490 672 666 680 802 951 1062 1009 1422 1451 1311

VIC All Export ($m cmv) C 59716 62630 63081 65032 66033 66292 64645 63072 62432 64392 63210 65043

VIC All Employment C 324553 323916 324080 322340 323109 320653 322873 326899 331870 331950 326123 329099

STRATEGIC ISSUES

2

9

Post GFC SWOT: Melbourne’s North

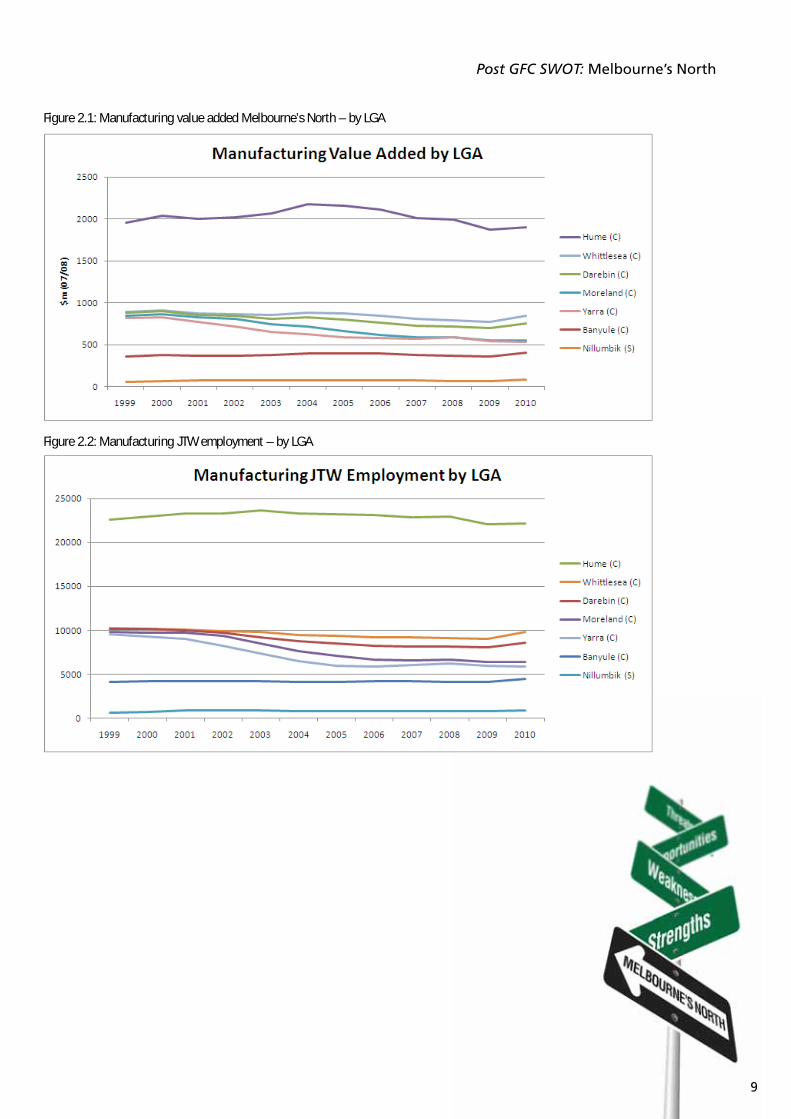

Figure 2.1: Manufacturing value added Melbourne’s North – by LGA

Figure 2.2: Manufacturing JTW employment – by LGA

10

2.2 Automotive manufacturing industry – opportunities example

Export of cars.

Export of components.

Growth of after-market firms (but not in manufacturing, growth would come from providing other kinds of services and sales of imported products).

Find niches in which Victorian industry can compete and create international markets.

Develop more intellectual property that is currently subject to international ownership; this is also an issue in terms of where the benefits flow.

Produce components and engines as part of a global supply chain. Ford focus is to develop what we have, making it more efficient and of a higher quality.

Value adding Australia’s primary production; aluminium is a good example of this.

Information technology development for transport and warehouse management.

Tier one suppliers as well as highly specialised lower tier suppliers to become global suppliers.

Government to increase the standards required in terms of the environment; use legislation to keep out components with poor environmental outcomes, such as the import of cheap exhaust systems for the after-market.

After-market firms have the capacity to innovate with new products for the local and export markets but not a lot of innovation, research and development is going on.

The development of alternative fuels technologies. Italy and South Korea are the leaders in LPG technology, ironic given that they do not have their own supplies of LPG. Engineering for different kinds of fuels is an opportunity in Australia.

2.3 Automotive and associated manufacturing industryGroups at risk of long term unemployment were identified as:

process workers

older workers

workers with poor literacy and numeracy, particularly English language skills.

2.4 Jobs and skills where future opportunities exist

Highly technical skills with problem solving capabilities.

Robotics skills – more technology and automation so more can go wrong.

Engineers across a range of automotive industry disciplines.

Designers.

CAD staff.

Product management and marketing.

Supervisors with a broad set of specialised skills.

Team leaders.

Hand welders.

Higher level production workers.

2.5 Signifi cance of Melbourne Airport Melbourne Airport employment continues to grow and provides major opportunity for further development in the region, particularly surrounding the airport. Many of the jobs created will be knowledge intensive and there are opportunities for innovation, research and education within the greater complex.

More than $1 billion in investment planned in next two years.

Employment for 12,500 people.

This equates to 11,000 full time equivalent positions.

Main employment areas are:

retail

aviation

air traffic control

air and road transport

airport management

security

hospitality.

Melbourne Airport experienced 22 per cent employment growth in the five years to 2008.

2.6 Relocation of the Wholesale MarketThe relocation of the Melbourne Wholesale Fruit and Vegetable Market, which should be considered as a major infrastructure project in its own right with more than $1 billion of planned investment in the redevelopment cycle over the next ten years, will provide a major benefit and ongoing opportunities for Melbourne’s North. The Wholesale Market currently has an annual turnover of more than $1.6 billion.

2 STRATEGIC ISSUES CONTINUED

11

Post GFC SWOT: Melbourne’s North

The rationale for the relocation of the Wholesale Market is to create a modern facility with improved access and a contemporary and integrated trading environment, greater opportunity for future development, and growth in a related cluster of developments within the new food precinct. These developments could include businesses that are concerned with logistics and distribution of fresh produce, associated processing and packaging, various trading and export related activities, and education and training.

2.7 Cost of carbon and redefi ning Melbourne’s NorthA long term issue for Melbourne’s North has been one of perception. Old and outmoded perceptions are hard to shift.

Is the image of the Melbourne’s North one that will attract high tech, globally connected and high value adding firms? How can the North’s image be redefined within a contemporary and forward looking economic context? Policies that help to redefine the region as a carbon efficient economy will enhance its future competitiveness and will be attractive to both new business and skilled residents.

Redefining the region’s image means:

efficient buildings (housing, commercial and industrial developments) that require less energy in daily use

efficient local communities where residents are close to employment or close to efficient modes of transport

appropriately skilled residents who can build and work in this environment

companies that can develop intellectual property to meet the needs of contemporary low carbon economies

industry that uses new technologies to reduce energy consumptions and carbon emissions

continually improving amenity and cultural and recreational opportunities for residents

solid links between the region’s businesses and tertiary and research centres

water efficient communities and internet enabled communities.

2.8 High speed internetOver the coming decades, high speed internet will result in significant structural change in the demand for occupations. More importantly, it will mean more flexibility in the location of jobs that service the requirements of the region. These changes will create an opportunity to strengthen the regional skills base in terms of a growing online economy.

Given the region’s educational and research infrastructure, the change will offer first mover advantage and an opportunity to define Melbourne’s North as a growing information economy.

2.9 Housing affordability, greenfi eld developments and the importance of public transportThe consequences of low dwelling construction rates are that the housing shortage is likely to increase, with consequences for all regions including Melbourne’s North.

High dwelling prices and rents in regions with good employment access (chiefly the inner and middle suburbs of the metropolitan cities) will reserve these regions for high-income earners and those with the luck to have inherited a house in the region.

These high-employment regions will also be characterised by increasing average household size, particularly when measured in numbers of adults per household. The increase will be due to adult children who have not left their parents’ home and the formation of group households of varying degrees of functionality. The only way in which low-income tenants not provided with social housing will be able to afford the rents will be by overcrowding and, given the economic incentives, this will be difficult to prevent.

At the other extreme, the population of regions with poor employment access will continue to increase as people are attracted to low-cost housing, particularly social security recipients who have given up hope of working.

The population living in marginal housing such as backyard caravans will also increase.

Higher levels of investment in transport, social and industry infrastructure and on community services will play a critical role in improving the level of accessible and affordable housing in Melbourne’s North.

In Melbourne there has been an overall reduction in the rate of dwelling construction, though not to the depressed Sydney levels. Strong growth in Melbourne’s outer south east had characterised the boom but faltered, and growth switched to Melbourne’s west. Further growth demand is forecast for Melbourne’s North.

There has been a premise that Melbourne’s North has pockets of housing affordability. As the region develops further, the likelihood of a continued decline in housing affordability is high, so it is important to consider housing affordability as a long term strategic issue.

12

The 2010 State of the Regions Report (NIEIR and ALGA) investigated housing affordability issues in Australia, and some aspects of this report are worth summarising. When greenfield sites are developed, a certain amount of local service employment can be guaranteed. But if residential value is to be created by local job generation, these service jobs must be complemented by employment that exports out of the local area.

In the post-war period that employment was most frequently provided by manufacturing. This was because manufacturing does not require the range of interpersonal contact that is the essence of the knowledge economy, and strongly appreciates the virtues of large, low-cost greenfield sites. Provided a labour supply was available within driving distance, manufacturers were attracted to these sites and decentralised to the urban fringes and provincial centres. An unintended consequence of the Australian Government decision (circa 1985) to cease supporting manufacturing industry was an increase in the difficulty of attracting new employment to metropolitan fringe and country locations. It is not that the knowledge economy necessarily favours city centres, but successful decentralisation of the knowledge economy requires investment in advanced telecommunications, transport and lifestyle support.

If the jobs will not come to the greenfields, the alternative is to link the fields to the jobs. Suitable greenfields are necessarily on the fringes of already-developed urban areas. Fields that are nowhere near existing employment nodes are too far from job locations for better transport to make a difference, while fields that already have high accessibility to jobs will be built up.

The strategy of creating residential value by transport investments is an old one. A century ago, the growth of commuter suburbs for Australia’s metropolitan areas was supported by state government investment in railways and tramways. In the second half of the twentieth century the states, though hampered by limited finance, attempted to do the same with radial roads. It took some time to realise the deficiencies of the radial-road policy – it takes large amounts of road space to carry significant flows of commuters and similarly large amounts of car-park space to house their vehicles once they get to the workplace. If the necessary road and parking space is not provided the result is congestion, which can only be relieved by widening the road at generally prohibitive cost in land purchases. (The recent Henry tax review says that congestion can be managed by appropriate tolls, but this is chiefly a means of rationing road space, not amplifying it to increase the flow of commuters. Large commuter flows can only efficiently be handled by rail.)

From the 1980s on, as the knowledge economy developed and the finance sector expanded, employment growth accelerated in the inner cities and decelerated on the metropolitan fringes. The insistence on roads as the preferred transport investment combined with high land costs and restricted budgets to seriously limit the expansion of transport capacity between fringe metropolitan greenfields and the regions where employment was growing.

It is only recently that attention has returned to rail investments, which have the capacity to handle large commuter flows without the multi-lane land requirements of roads. Perth was the first Australian metropolitan area to modernise operating practices on its suburban railways and add new lines, and now Melbourne shows signs of following suit. This is essential for the successful development of Melbourne’s North.

2.10 Education and knowledge economyThe Melbourne’s North: the new knowledge economy report discussed the importance of the knowledge economy and industry and research links to the region’s future development prospects. Issues and opportunities include:

equity in school education funding

accommodating students in the region

patents

incubators

building on the NBN – new media, digital economy, social media, film, audio, publishing

design and engineering exports

business services

medicine and social services

arts and culture.

2 STRATEGIC ISSUES CONTINUED

13

Post GFC SWOT: Melbourne’s North

2.11 Percentage of households with bachelor or higher qualifi cation, 2012 (as highest qualifi cation)The level of resident skills and qualifications are a strategic issue for some parts of the region.

2.12 Benefi ting from internationalisationThe 2006 census showed that the number of residents in Melbourne’s North who consider they are not proficient in spoken English had declined from 58,700 in 1996 to 55,000 in 2006.

However the proportion that speaks a language other than English increased, indicating that either individual migrants had improved their English skills between 1996 and 2006 or the newer arrivals have better English skills. It is likely to be a combination of both trends.

14

2.13 Amenity and environmentContinual improvement of amenities and environmental standards will assist Melbourne’s North in making the region the place to be for families and businesses, including:

design and architectural standards

housing for the future – building in regional competitiveness

high quality office accommodation

places to stay

industrial and commercial buildings – design, efficiency and co-generation

water supply and systems.

2.14 Energy use considerations Gas/electricity/oil.

Creating communities with local jobs.

Effective transport systems.

Alternative sources of energy.

Construction of energy efficient housing, commercial and industrial buildings

2.15 Transport system considerations

Rail.

Light rail.

Congestion in the inner parts of Melbourne’s North.

Airport and connectivity.

2.16 Industry considerations Wholesale markets.

Manufacturing – what is happening in Melbourne’s North?

Airport precinct.

Knowledge based exports, particularly education.

2 STRATEGIC ISSUES CONTINUED

Post GFC SWOT: Melbourne’s North

15

3.1 Strengths The region’s existing asset base can be leveraged to further

improve economic performance. Assets include Melbourne Airport, medical precincts, and colleges and universities. New assets such as the wholesale markets, freight hubs and master plan developments will add to existing opportunities.

A diverse economic base, development of which has managed to offset the decline of the manufacturing industry in the region.

A growing tertiary sector with developing research capacity.

The knowledge economy strengths of the inner areas combined with the industrial strengths of parts of the outer areas of the region.

The opportunity, because of redevelopment options in the inner areas and the available greenfield sites in the outer areas, to develop well planned and sustainable communities.

Melbourne’s North is a gateway to Melbourne with major transport links to the north and with Melbourne Airport providing access to interstate and international markets.

3.2 Weaknesses Inefficient and ineffective transport links reducing household

capacity for mobility in some parts of the region, including sparse road, rail, tram and bus links within a given employment catchment and especially to major employment nodes.

Historical perception – it is important to remind policy makers that the region has changed in terms of its amenity and capacity to provide local employment in a developing and diverse set of industries.

Level of household skills and the imbalance between skills demand of local industry when compared to resident skills. This is a critical policy issue and will drive the local economic outcomes and resident wellbeing for the former manufacturing zones within the region. Issues of skills imbalance also go beyond local industry. The region’s household skills mix will need to include residents with the capacity to access CBD

knowledge type employment, as this will assist the rapidly expanding cities of Hume and Whittlesea to provide improved business services to local industries as highly qualified individuals switch from CBD type employment to local employment when improved opportunities arise.

Relatively poor linkages between local enterprises and catchment enterprises and catchment industries making relatively poor use of catchment skills. This is a knowledge and information based issue requiring improved business and employment networks with improved communications and links.

Strategic drivers of regional productivity form supply chains oriented outside the catchment or are highly capital intensive with low value added ratios accruing to catchment residents. This requires more activity at a local level that generates local investment in research and innovation to create greater value adding opportunities and the capacity to retain profits in the region, rather than exporting them.

3.3 Opportunities In greenfield sites in outer parts of the region and

redevelopment areas in the inner parts of the region, to build in competitive advantage by creating sustainable housing and sustainable communities. That is, to create energy and water efficient buildings and local skilled employment opportunities.

Leverage regional assets to reduce regional inefficiencies.

To improve transport systems and in doing so lift regional productivity and amenity.

To improve supply chain efficiency and industry links, both internal and external to the region, by attracting export oriented enterprises to establish in the region and increasing knowledge intensity of local production to improve value adding ratios.

To build on the opportunities to diversify some of the region’s employment opportunities into emerging knowledge economy sectors.

MELBOURNE’S NORTH: REGIONAL SWOT3

16

Focus employment growth strategies and training efforts on growth sectors including some aspects of the manufacturing industry and regional assets including Melbourne Airport (aviation, transport and logistics), medical precincts and universities (research and commercialisation of intellectual property), wholesale markets (food processing and manufacturing, food logistics and exports) and niche education developments such as the aviation college.

3.4 Export opportunities Export of skills, such as design and engineering skills, business

services skills.

Export of intellectual property rights in bioscience, manufacturing, media, aerospace systems and technology, green technologies.

Export of specialist food items and manufactures.

Export of education and skills development.

Licensing of locally developed intellectual property such as inventions relating to climate change adaptation technologies or renewable energy.

3.5 Threats Offshoring of employment, particularly in the manufacturing

industry and particularly in the automotive manufacturing industry.

Continued hollowing out of manufacturing industry supply chains, creating future declines in this sector.

The low skill levels of residents in some parts of Melbourne’s North and increasing skills demands of local industry leading to long term structural unemployment and stranding of residents away from suitable employment nodes.

A carbon price shock damaging competitiveness of the region, particularly exports.

Lack of opportunity for local enterprises to access new business generated by the mining/energy export boom, particularly steel fabrication and engineering.

The impact of the economic development of India and China on the region and particularly manufacturing.

The strength of the Australian dollar and its impact on the region’s economic structure longer term.

3 MELBOURNE’S NORTH: REGIONAL SWOT CONTINUED

Post GFC SWOT: Melbourne’s North

17

4.1 The region comparedPopulationThe figure compares the annual population increase of Melbourne’s North, the Melbourne SD and Victoria. The figures show that, increasingly, Melbourne’s North is taking a greater share of Melbourne’s population growth.

Figure 4.1: Population growth

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Melbourne's North

Melbourne SD

Victoria

Figure 4.2: Population share of growth increase

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Melbourne's North

Melbourne SD

Victoria

THE REGION DESCRIBED

4

18

Growth in the number of householdsThe changing social composition of Melbourne’s North is reflected in the share of growth in the number of households.

Figure 4.3: Number of households – growth

0

500,000

1,000,000

1,500,000

2,000,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Melbourne's North

Melbourne SD

Victoria

Figure 4.4: Number of households – share of growth increase

0.0%

0.5%

1.0%

1.5%

2.0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Melbourne's North

Melbourne SD

Victoria

Growth in resident employmentMelbourne’s North grew employment relatively strongly in 2010 when compared to Victoria and the Melbourne SD. The North’s employment bounced back more rapidly than in other Melbourne regions. In 2010, 22 per cent of Melbourne’s employed workforce lived in Melbourne’s North.

Figure 4.5: Growth in employment

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Melbourne's North

Melbourne SD

Victoria

4 THE REGION DESCRIBED CONTINUED

Post GFC SWOT: Melbourne’s North

19

NIEIR unemployment rateFigure 4.6 shows the decline in resident unemployment in Melbourne’s North when compared to the Melbourne SD and Victoria. This is despite the region’s exposure to manufacturing employment and the corresponding manufacturing skills base of its traditional residents. The NIEIR unemployment rate includes a proportion of residents shifted to benefits other than the unemployment benefit.

Figure 4.6: Decline in NIEIR unemployment

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Melbourne's North

Melbourne SD

Victoria

For Melbourne’s North residents the figures show a significant decline in resident unemployment just prior to the GFC, and a slightly lower level of growth in unemployment post GFC when compared to the Melbourne SD and Victoria, restating the region’s relative resilience so far.

NIEIR structural resident unemployment rateStructural unemployment is the NIEIR estimate of unemployment including all those that could be and may wish to be workforce participants but are excluded because of barriers to employment such as low skills, language barriers and other forms of disadvantage that create long term disengagement from the workforce. Although the level of structural unemployment in Melbourne’s North has reduced, the level is still higher than the Melbourne SD and Victoria. This highlights the need for continuing education and reskilling of the most disadvantaged in the community.

Figure 4.7: Structural unemployment rate

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Melbourne's North

Melbourne SD

Victoria

20

Headline unemployment rateThe headline unemployment rate confirms the decline in overall unemployment in Melbourne’s North.

Figure 4.8: Headline unemployment rate

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Melbourne's North

Melbourne SD

Victoria

Resident employment growth by sector Figure 4.9 shows the growth in employment by sector for residents from Melbourne’s North, including the period after the GFC. Longer term growth occurred in construction, electricity gas and water, accommodation, information media and telecoms, rent hire and real estate services, professional scientific and technical services, education and training, manufacturing, health and social services, and art and recreation services. There is a decline in manufacturing employment for people living in Melbourne’s North. Post GFC there were noticeable declines in the financial services sector and wholesale. Accommodation and other services performed particularly well post GFC.

A Agriculture

B Mining

C Manufacturing

D Electricity, gas and water

E Construction

F Wholesale

G Retail

H Accommodation

I Transport, postal and warehousing

J Information media and telecommunications

K Financial and insurance services

L Rent, hire and real estate services

M Professional, scientific and technical services

N Administration and support services

O Public administration

P Education and training

Q Health and social

R Arts and recreation services

S Other services

Figure 4.9: Melbourne’s North annual growth – residential employment

4 THE REGION DESCRIBED CONTINUED

Post GFC SWOT: Melbourne’s North

21

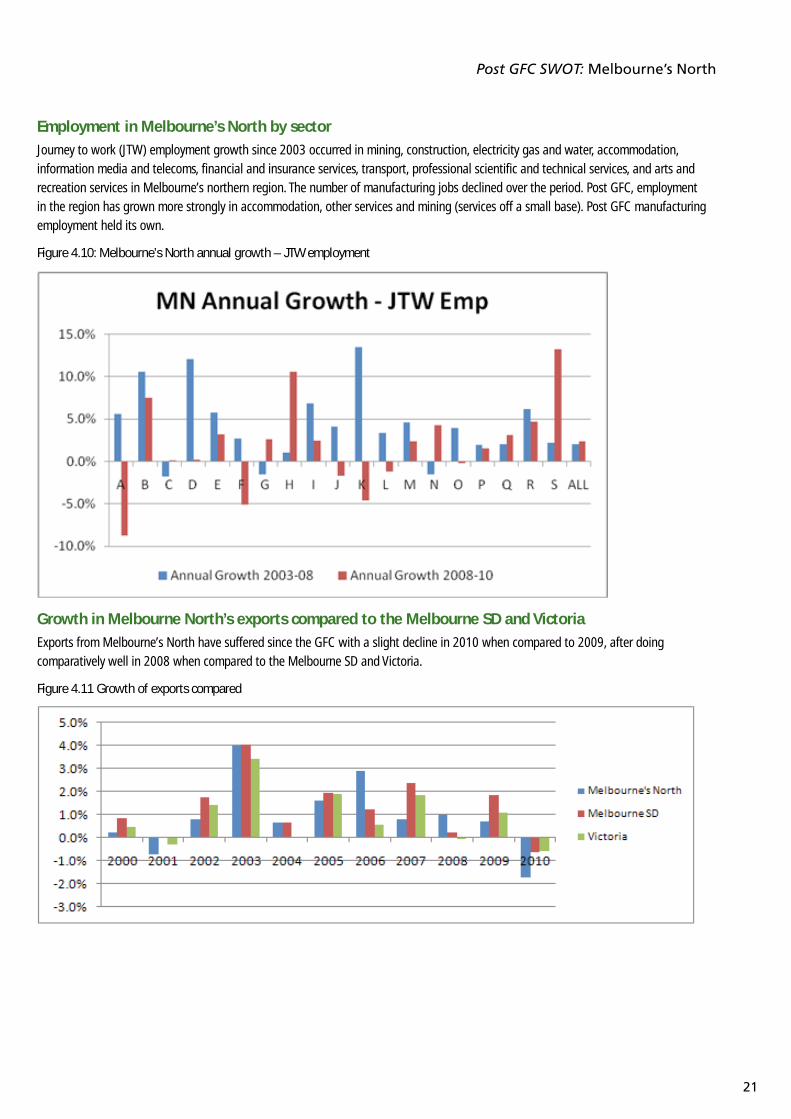

Employment in Melbourne’s North by sector Journey to work (JTW) employment growth since 2003 occurred in mining, construction, electricity gas and water, accommodation, information media and telecoms, financial and insurance services, transport, professional scientific and technical services, and arts and recreation services in Melbourne’s northern region. The number of manufacturing jobs declined over the period. Post GFC, employment in the region has grown more strongly in accommodation, other services and mining (services off a small base). Post GFC manufacturing employment held its own.

Figure 4.10: Melbourne’s North annual growth – JTW employment

Growth in Melbourne North’s exports compared to the Melbourne SD and VictoriaExports from Melbourne’s North have suffered since the GFC with a slight decline in 2010 when compared to 2009, after doing comparatively well in 2008 when compared to the Melbourne SD and Victoria.

Figure 4.11 Growth of exports compared

22

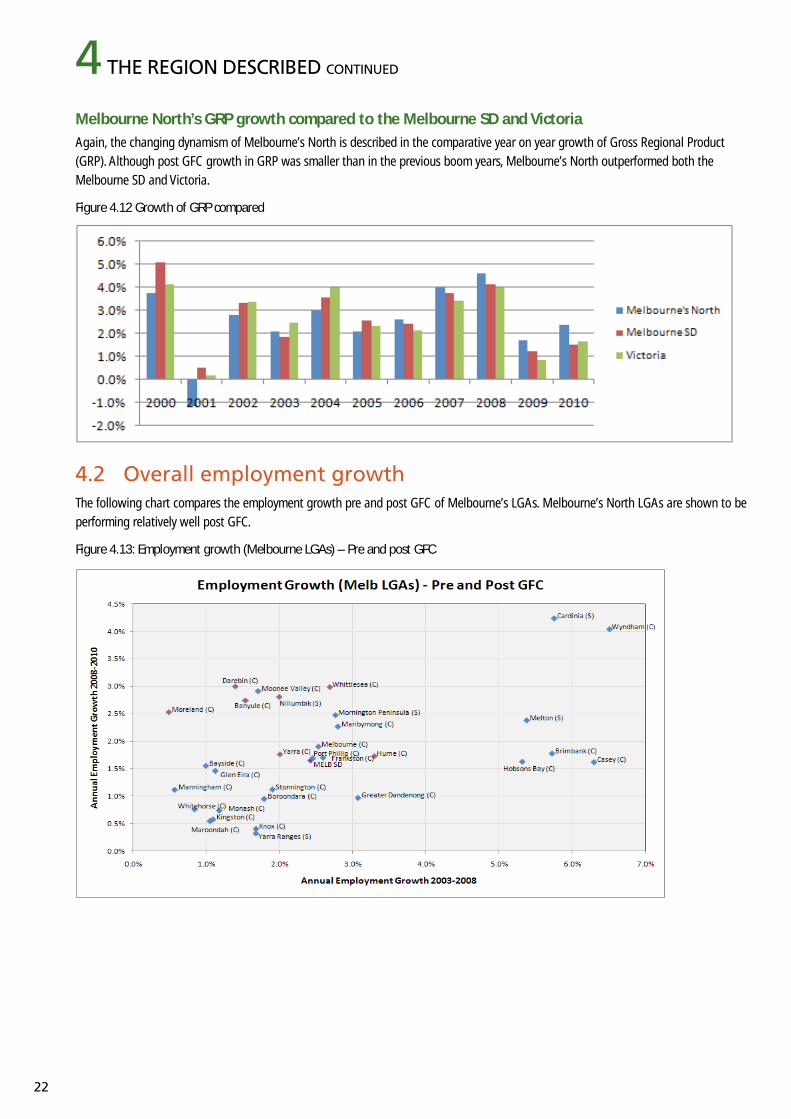

Melbourne North’s GRP growth compared to the Melbourne SD and VictoriaAgain, the changing dynamism of Melbourne’s North is described in the comparative year on year growth of Gross Regional Product (GRP). Although post GFC growth in GRP was smaller than in the previous boom years, Melbourne’s North outperformed both the Melbourne SD and Victoria.

Figure 4.12 Growth of GRP compared

4.2 Overall employment growthThe following chart compares the employment growth pre and post GFC of Melbourne’s LGAs. Melbourne’s North LGAs are shown to be performing relatively well post GFC.

Figure 4.13: Employment growth (Melbourne LGAs) – Pre and post GFC

4 THE REGION DESCRIBED CONTINUED

23

Post GFC SWOT: Melbourne’s North

A recent comparison of Melbourne’s RDA regions showed the following information.

Population Western Melbourne is the fastest growing region, averaging

3.6 per cent per annum.

Southern Melbourne has 33 per cent of Melbourne’s population.

Melbourne East has 25 per cent of Melbourne’s population.

Northern Melbourne has 22 per cent of Melbourne’s population.

Western Melbourne has 20 per cent of Melbourne’s population.

Age profi le The proportion of the population aged 0 to 19 years is

declining in all regions.

There has been a rise in the actual numbers in the 0 to 19 years group in all regions except Melbourne East.

Similarly, the growth in the 20 to 29 year age group has not been as fast as population growth in Northern Melbourne, Southern Melbourne and Melbourne East.

The 20 to 54 year age group grew as a proportion of total population in all regions except Melbourne East.

All regions have an increasing proportion and increasing actual numbers of people in the 55 years and over age group.

Workforce Western Melbourne has the fastest growing workforce,

averaging 3.6 per cent per annum over the last 5 years.

Southern Melbourne has the largest workforce, currently 735,000 or 33 per cent of Melbourne Metro.

The smallest workforce is in Western Melbourne, with 439,000 or 20 per cent of Melbourne Metro.

Employment Western Melbourne has the fastest growing employment and

Melbourne East the slowest growing.

33 per cent of Melbourne’s employed live in Southern Melbourne, 26 per cent in Melbourne East, 22 per cent in Northern Melbourne and 19 per cent in Western Melbourne.

670,000 residents of Southern Melbourne are employed and 398,000 residents of Western Melbourne are employed.

Wages and salaries Wages are highest in Melbourne East and Southern

Melbourne, with average wage and salary incomes per capita of $25,618 and $24,249 per annum.

Average wages and salaries have declined since the GFC, due in part to less paid hours being worked.

Benefi ts The regions with the highest proportion of income coming

from Government Benefits are Western Melbourne at 14.3 per cent and Northern Melbourne at 13.8 per cent.

The regions with the lowest proportion are Melbourne East at 10.4 per cent and Southern Melbourne at 11.6 per cent.

Northern Melbourne has a higher than average proportion of people on Disability Support Pensions (age 25+), and Long Term Unemployed, but lower than average on Parenting Payment Single and Non-Student Youth Allowance.

Melbourne East and Southern Melbourne have lower than average proportions of the population on all Allowances with the exception of the Student Youth Allowance.

Western Melbourne has a higher than average proportion of the population receiving Disability Support (15-20year olds), Parenting Payment Single (age 21+), Long Term and Short Term Unemployed and Youth Allowance Student.

Disposable income The regions with the highest disposable income per capita are

Melbourne East $33,300 per annum and Southern Melbourne $32,900 per annum.

The regions with the lowest disposable income per capita are Western Melbourne $29,800 per annum and Northern Melbourne $30,900 per annum.

Patent applications Patent applications per 100,000 capita are a measure of the

relative levels of innovation in a community.

Melbourne East, Southern Melbourne and Western Melbourne all have average patents per capita higher than the Australian average.

NIEIR unemployment This measure of unemployment includes an adjustment for

any excess recipients of disability payments, i.e. where the number of people on disability payments increases at a rate faster than expected by population growth.

Before 2008, all regions except Southern Melbourne were experiencing a decline in NIEIR unemployment.

After 2008, all regions except Melbourne’s North are experiencing an increase in NIEIR unemployment reflecting the slowdown due to the GFC.

24

Unemployment rates Trends in the NIEIR unemployment rate indicate that unemployment is the highest in Western Melbourne and lowest in Melbourne’s

North and Melbourne East.

Headline unemployment is highest in Western Melbourne and lowest in Northern Melbourne.

Structural unemployment (which is an indicator of those least able to find work, such as the long term unemployed and those on disability allowance) is highest in Western and Northern Melbourne and lowest in Melbourne East.

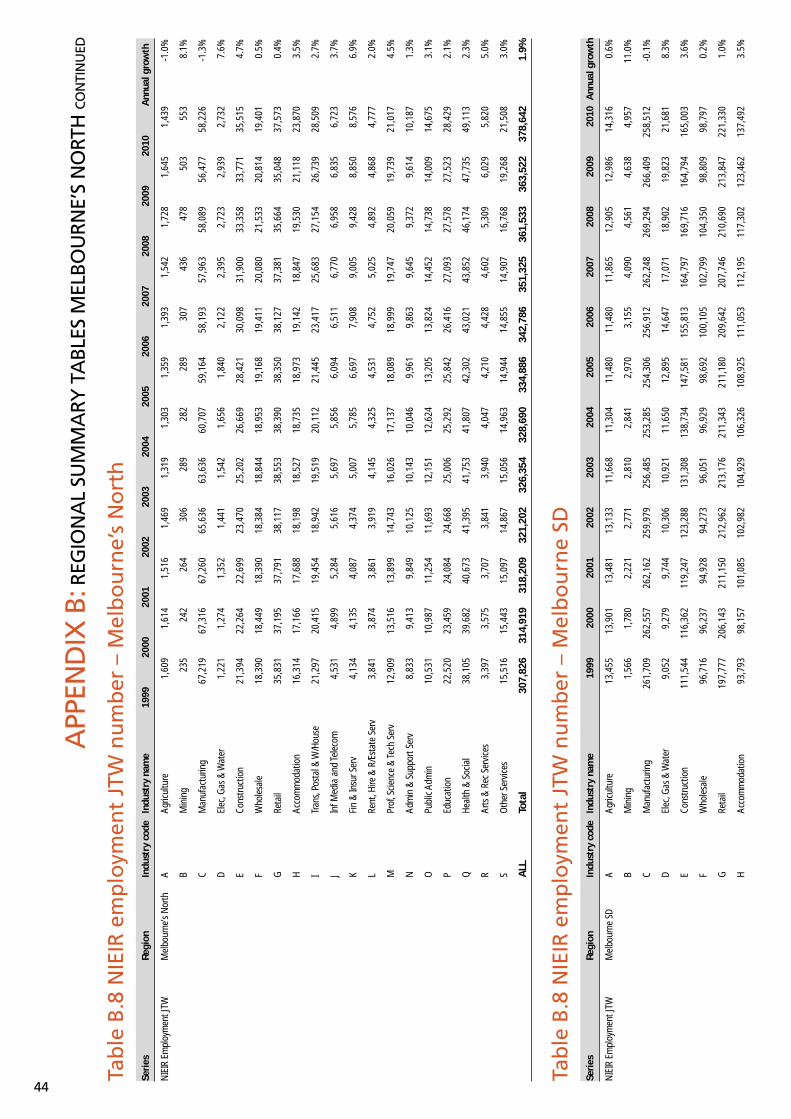

JTW employment by LGAEmployment provided in each LGA in Melbourne’s North has increased over the period 1996 to 2010. Hume and Yarra have grown employment the most at around 3 per cent per annum, while Moreland has grown employment the least at .34 per cent per annum.

Figure 4.14: Total JTW employment by LGA

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

Total JTW Employment by LGA

le (C)

in (C)

(C)

and (C)

bik (S)

( )

4.3 Resident employmentResident employment (employment of those living in an LGA) has risen in all of the region’s LGAs, the highest growth occurring in Yarra at 3 per cent per annum and Hume at 2.8 per cent per annum.

Figure 4.15: Total resident employment by LGA

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

Total Resident Employment by LGA

le (C)

in (C)

(C)

and (C)

bik (S)

( )

4 THE REGION DESCRIBED CONTINUED

25

Post GFC SWOT: Melbourne’s North

4.4 UnemploymentHume has the highest number of unemployed. This number continues to grow and indicates some degree of stranding of low skilled workers. Darebin has reduced its unemployed residents the most.

Figure 4.16: NIEIR unemployment rate by LGA

0

2000

4000

6000

8000

10000

12000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

NIEIR Unemployment by LGA

Banyule (C)

Darebin (C)

Hume (C)

Moreland (C)

Nillumbik (S)

Whittlesea (C)

Yarra (C)

4.5 NIEIR unemployment rateFigure 4.17: NIEIR unemployment rate by LGA

0%

2%

4%

6%

8%

10%

12%

14%

16%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

NIEIR Unemployment Rate by LGA

Banyule (C)

Darebin (C)

Hume (C)

Moreland (C)

Nillumbik (S)

Whittlesea (C)

Yarra (C)

26

5.1 LGA growth areas post GFCBanyule

Other services

Accommodation and food services

Retail

Construction

Manufacturing

Administrative and support services

Darebin Other services

Accommodation and food services

Administrative and support services

Retail

Construction

Manufacturing

Hume Accommodation and food services

Other services

Professional, scientific and technical services

Yarra Transport, postal and warehousing

Health care and social assistance

Moreland Accommodation and food services

Other services

Transport, postal and warehousing

Professional, scientific and technical services

Information media and telecoms

Nillumbik Other services

Accommodation and food services

Retail

Manufacturing

Administrative and support services

Whittlesea Other services

Accommodation and food services

Retail

Construction

Manufacturing

Administrative and support services

5.2 Banyule since the GFC Unemployment rate has increased slightly from a low of 3.1

per cent (NIEIR 5 per cent) in 2007 to 3.4 per cent (NIEIR 5.3 in 2010). Banyule residents have been successful in maintaining employment.

The workforce has continued to grow.

Wages and salaries are actually slightly up on the 2007 number, so local spending power has been sustained. Disposable income is slightly higher in 2010 than it was in 2007.

Benefits paid in 2010 were lower than in 2007.

Business income is higher in 2010 than it was in 2007.

All categories of social security income were below the Australian average in 2010.

Banyule’s population is growing fastest in terms of overall numbers in the 30-54 age group; the 0-19 year old population is declining the fastest and the rate of decline appears to be increasing.

Banyule’s households have continued to grow richer and household debt to gross income has continued to increase between 2007 and 2010.

Residential building construction value was lower in 2010 than it was in 2007. This may relate to housing affordability issues.

Non-residential construction value was higher in 2010 than it was in 2007.

The following section provides LGA level data and a commentary on the economic circumstances of each of the region’s LGAs.

COMMENTARY BY LGA

5

27

Post GFC SWOT: Melbourne’s North

Resident consumption continues to grow overall.

Resident hours worked has continued to grow and was higher in 2010 than it was in 2007; total resident income was also higher.

The numbers of hours worked in Banyule also increased.

Between 2006 and 2010, resident employment rose from 64,000 to 68,000.

Jobs in the region rose from 37,000 to 48,000.

Comparing 2006 to 2010, there was an increase in both place of residence and place of work jobs in the following sectors: manufacturing, construction, retail, accommodation and food services, professional scientific and technical services, admin and support services, public admin and safety, education and training, and other services.

Sectors that performed poorly in terms of jobs, again both place of residence and place of work were: financial and insurance services, information media and telecoms, transport postal and warehousing, wholesale, and electricity gas and water.

Arts jobs declined.

5.3 Darebin since the GFC Unemployment rate has decreased from 6.6 per cent (NIEIR

7.7 per cent) in 2007 to 6.1 per cent (NIEIR 6.5 in 2010).

The workforce has continued to grow, as employment has increased.

Wages and salaries are up on the 2007 number, so local spending power has increased. Disposable income is higher in 2010 than it was in 2007.

Benefits paid in 2010 were higher than in 2007.

Business income is higher in 2010 than it was in 2007.

Darebin has higher than average recipients of Social Security Benefits for Disability Support 25+, Unemployment and Student Allowance.

Darebin’s population has declined in the under 20 and over 55 age groups; the middle ranges have increased.

Darebin’s households have continued to grow richer and household debt to gross income has continued to increase between 2007 and 2010.

Residential building construction value was higher in 2010 than it was in 2007.

Non-residential construction value was higher in 2010 than it was in 2007.

Resident consumption continues to grow overall.

Resident hours worked has continued to grow and was higher in 2010 than it was in 2007; total resident income was also higher.

The numbers of hours worked in Darebin also increased.

Between 2006 and 2010, resident employment rose from 64,000 to 72,000.

Jobs in the region rose from 51,000 to 56,000.

Comparing 2006 to 2010, there was an increase in both place of residence and place of work jobs in the following sectors: other services, manufacturing, construction, accommodation and food services, education and training, retail, professional scientific and technical services, public administration and safety, health care and social assistance, and administration and support services.

Sectors that performed poorly in terms of jobs, again both place of residence and place of work were: transport postal and warehousing, wholesale, information media and telecoms, and financial and insurance services.

5.4 Hume since the GFC Unemployment rate has increased from a low of 6.8 per cent

(NIEIR 9.6 per cent) in 2007 to 8.6 per cent (NIEIR 11.3 in 2010).

The workforce has continued to grow, as both employment and unemployment have increased.

Wages and salaries are only slightly up on the 2007 number, so local spending power has remained steady. Disposable income is slightly higher in 2010 than it was in 2007.

Benefits paid in 2010 were higher than in 2007.

Business income is higher in 2010 than it was in 2007.

Hume has higher than average recipients of Social Security Benefits for Disability Support, Parenting Payment Single 25+, Unemployment and Youth Allowance.

Hume’s population is growing across all age groups, although the proportion under 20 has declined and the older age group proportions have increased.

Hume’s households have continued to grow richer and household debt to gross income has continued to increase between 2007 and 2010.

Residential building construction value was higher in 2010 than it was in 2007.

Non-residential construction value was higher in 2010 than it was in 2007.

Resident consumption continues to grow overall.

Resident hours worked has continued to grow and was higher in 2010 than it was in 2007; total resident income was also higher.

The numbers of hours worked in Hume also increased.

28

Between 2006 and 2010, resident employment rose from 72,000 to 77,000.

Jobs in the region rose from 31,000 to 32,000.

Comparing 2006 to 2010, there was an increase in both place of residence and place of work jobs in the following sectors: transport postal and warehousing, accommodation and food services, other services, health care and social assistance, wholesale, information media and telecoms, arts and recreation, and professional scientific and technical services.

Sectors that performed poorly in terms of jobs, again both place of residence and place of work, were: retail, manufacturing, public administration and safety, education and training, financial and insurance services, administration and support services, electricity gas and water, and rental, hiring and real estate services.

5.5 Moreland since the GFC Unemployment rate has increased from 5.2 per cent (NIEIR 6

per cent) in 2007 to 5.3 per cent (NIEIR 5.4 per cent in 2010).

The workforce has continued to grow, as employment has increased.

Wages and salaries are up on the 2007 number, so local spending power has increased. Disposable income is higher in 2010 than it was in 2007.

Benefits paid in 2010 were the same as in 2007.

Business income is higher in 2010 than it was in 2007.

Moreland has higher than average recipients of Social Security Benefits for Disability Support 25+, Unemployment and Student Allowance.

Moreland’s population has declined in the under 20 and over 55 age groups; the middle ranges have increased.

Moreland’s households have continued to grow richer and household debt to gross income has continued to increase between 2007 and 2010.

Residential building construction value was higher in 2010 than it was in 2007.

Non-residential construction value was lower in 2010 than it was in 2007.

Resident consumption continues to grow overall.

Resident hours worked has continued to grow and was higher in 2010 than it was in 2007; total resident income was also higher.

The numbers of hours worked in Moreland also increased.

Between 2006 and 2010, resident employment rose from 68,000 to 77,000.

Jobs in the region rose from 38,000 to 52,000.

Comparing 2006 to 2010, there was an increase in both place of residence and place of work jobs in the following sectors: accommodation and food services, transport postal

and warehousing, health care and social assistance, other services, information media and telecoms, arts and recreation, wholesale, and professional scientific and technical services.

Sectors that performed poorly in terms of jobs, again both place of residence and place of work were: retail, public administration and safety, financial and insurance services, education and training, administration and support, manufacturing, and electricity gas and water.

5.6 Nillumbik since the GFC Unemployment rate has increased from 1.6 per cent (NIEIR 2.9

per cent) in 2007 to 1.9 per cent (NIEIR 3.2 per cent in 2010).

The workforce has continued to grow, as employment and unemployment have increased.

Wages and salaries are up on the 2007 number, so local spending power has increased. Disposable income is slightly higher in 2010 than it was in 2007.

Benefits paid in 2010 were higher than in 2007.

Business income is higher in 2010 than it was in 2007.

Nillumbik has lower than average recipients in all categories of Social Security benefits.

Nillumbik’s population has declined in the under 20 age group; the older ranges have all increased.

Nillumbik’s households have continued to grow richer and household debt to gross income has decreased between 2007 and 2010.

Residential building construction value was higher in 2010 than it was in 2007.

Non-residential construction value was higher in 2010 than it was in 2007.

Resident hours worked declined slightly between 2007 and 2010; total resident income increased over the same period.

The numbers of hours worked in Nillumbik has increased.

Between 2006 and 2010, resident employment rose from 37,000 to 39,000.

Jobs in the region rose from 15,000 to 16,000.

Comparing 2006 to 2010, there was an increase in both place of residence and place of work jobs in the following sectors: other services, construction, manufacturing, professional scientific and technical services, education and training, accommodation and food services, retail, and public administration and safety.

Sectors that performed poorly in terms of jobs, again both place of residence and place of work were: wholesale, transport postal and warehousing, information media and telecoms, financial and insurance services, health care and social assistance, electricity gas and water, arts and recreation, and administrative and support services.

5 COMMENTARY BY LGA CONTINUED

29

Post GFC SWOT: Melbourne’s North

5.7 Whittlesea since the GFC Unemployment rate has increased slightly from 5 per cent

(NIEIR 8.5 per cent) in 2007 to 5.7 per cent (NIEIR 8.8 in 2010).

The workforce has continued to grow. Both employment and unemployment have grown.

Wages and salaries are actually slightly up on the 2007 number, so local spending power has been sustained. Disposable income is slightly higher in 2010 than it was in 2007.

Benefits paid in 2010 were slightly lower than in 2007.

Business income is higher in 2010 than it was in 2007.

Disability Support 25+, Parenting Payment Single 25+ and the Student Allowance were the Social Security categories higher than the Australian average.

Whittlesea’s population is growing across all age groups, leaving the age structure similar to that in 2006.

Whittlesea’s households have continued to grow richer and household debt to gross income has continued to increase between 2007 and 2010.

Residential building construction value in 2010 was more than twice the 2007 value, indicating that the northern fringe is still one of Melbourne’s growth areas.

Non-residential construction value was lower in 2010 than it was in 2007, although 2008 and 2009 were both higher than 2007.

Resident consumption continues to grow overall.

Resident hours worked has continued to grow and was higher in 2010 than it was in 2007; total resident income was also higher.

The numbers of hours worked in Whittlesea also increased.

Between 2006 and 2010, resident employment rose from 64,000 to 72,000.

Jobs in the region rose from 42,000 to 46,000.

Comparing 2006 to 2010, there was significant increase in both place of residence and place of work jobs in the following sectors: manufacturing, construction, other services, retail, and accommodation and food services. Business services, government administration, education and training, and health care and social assistance also had employment increases.

Sectors that performed poorly in terms of jobs, again both place of residence and place of work were: transport postal and warehousing, wholesale, information media and telecoms, electricity gas and water, and financial and insurance services.

5.8 Yarra since the GFC Unemployment rate has increased slightly from 5.4 per cent

(NIEIR 5.8 per cent) in 2007 to 6.6 per cent (NIEIR 6.8 in 2010).

The workforce has continued to grow.

Wages and salaries are actually slightly up on the 2007 number, so local spending power has been sustained. Disposable income is slightly higher in 2010 than it was in 2007.

Benefits paid in 2010 were higher than in 2007.

Business income is higher in 2010 than it was in 2007.

Most categories of social security income were below the Australian average in 2010; the exceptions were the Student Allowance, Unemployment and Disability Allowance 25+, reflecting the proximity to tertiary institutions and amenities.

Yarra’s population is growing fastest in terms of overall numbers in the 30-54 age group; the 0-19 year old population is declining.

Yarra’s households have continued to grow richer and household debt to gross income has decreased since 2007.

Residential building construction value was higher in 2010 than it was in 2007.

Non-residential construction value was higher in 2010 than it was in 2007.

Resident consumption continues to grow overall.

Resident hours worked has continued to grow and was higher in 2010 than it was in 2007; total resident income was also higher.

The numbers of hours worked in Yarra also increased.

Between 2007 and 2010, resident employment rose from 44,500 to 51,000.

Jobs in the region rose from 72,000 to 78,500.

Comparing 2006 to 2010, there was an increase in both place of residence and place of work jobs in most sectors. The following sectors had notable increases: transport postal and warehousing, education and training, and arts and recreation. There was a significant rise in health care and social assistance.

Sectors that performed poorly in terms of jobs, again both place of residence and place of work were: manufacturing and retail.

There was a decline in residents employed in construction, accommodation and food services and in professional services, although jobs in these industries rose in Yarra.

30

Manufacturing employment growth

Figure 5.1: Manufacturing employment growth (Melbourne LGAs) – pre and post GFC

Construction employment growth

Figure 5.2: Construction employment growth (Melbourne LGAs) – pre and post GFC

5.9 Employment growthThe following tables provide a comparison of employment growth pre and post GFC by industry sector.

5 COMMENTARY BY LGA CONTINUED

Post GFC SWOT: Melbourne’s North

31

Wholesale employment growth

Figure 5.3: Wholesale employment growth (Melbourne LGAs) – pre and post GFC

Retail employment growth

Figure 5.4: Retail employment growth (Melbourne LGAs) – pre and post GFC

32

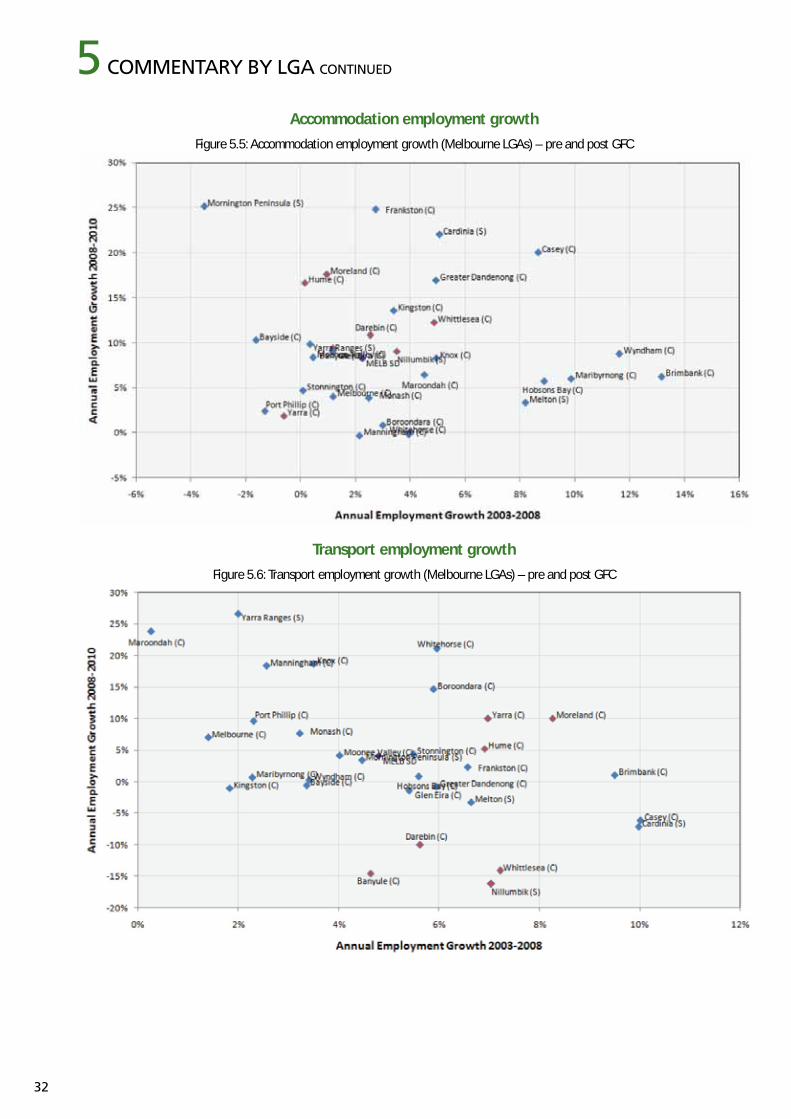

Accommodation employment growth

Figure 5.5: Accommodation employment growth (Melbourne LGAs) – pre and post GFC

Transport employment growth

Figure 5.6: Transport employment growth (Melbourne LGAs) – pre and post GFC

5 COMMENTARY BY LGA CONTINUED

Post GFC SWOT: Melbourne’s North

33

IT employment growth

Figure 5.7: IT employment growth (Melbourne LGAs) – pre and post GFC

Financial employment growth

Figure 5.8: Financial employment growth (Melbourne LGAs) – pre and post GFC

34

Professional employment growth

Resident consumption remained at similar levels from Figure 5.9: Professional employment growth (Melbourne LGAs) – pre and post GFC

Administration employment growth

Figure 5.10: Administration employment growth (Melbourne LGAs) – pre and post GFC

5 COMMENTARY BY LGA CONTINUED

Post GFC SWOT: Melbourne’s North

35

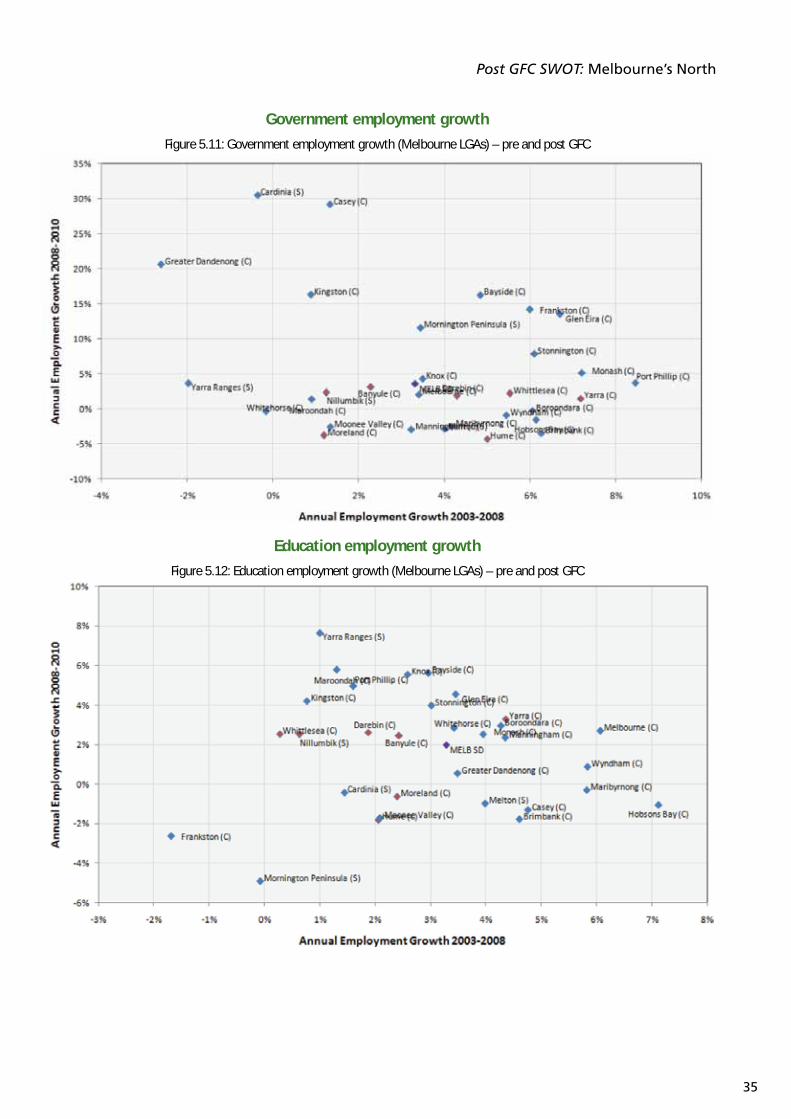

Government employment growth

Figure 5.11: Government employment growth (Melbourne LGAs) – pre and post GFC

Education employment growth

Figure 5.12: Education employment growth (Melbourne LGAs) – pre and post GFC

36

Health employment growth

Figure 5.13: Health employment growth (Melbourne LGAs) – pre and post GFC

Other services employment growth

Figure 5.14: Other services employment growth (Melbourne LGAs) – pre and post GFC

5 COMMENTARY BY LGA CONTINUED

Post GFC SWOT: Melbourne’s North

37

5.10 Pre GFC place of work and resident employment growthLGAs that appear above the line have resident employment growth that is faster than place of work employment growth.

Figure 5.15: Place of work and resident employment growth(Melbourne LGAs) – pre GFC

5.11 Post GFC place of work and resident employment growthLGAs that appear above the line have resident employment growth that is faster than place of work employment growth.

Figure 5.16: Place of work and resident employment growth(Melbourne LGAs) – post GFC

38

APPENDICES

Post GFC SWOT: Melbourne’s North

39

Gross Product is identical with Gross Value Added for any geographic area. It comprises the sale value of goods and services produced in the region in a time period, less the costs of raw materials and other inputs purchased from other businesses, less taxes. The basic concept is very similar to the tax base for GST. Ideally, Gross Local Product would have the same definition as Gross National Product or Gross State Product. However, it is not possible to allocate the Gross Operating Surplus of corporate businesses (including any surplus of government enterprises) to LGAs. (The Gross Operating Surplus comprises corporate Gross Value Added less wages and related payments.) Gross Local Product therefore comprises:

employee compensation paid in respect of production in the LGA; plus

gross value added by unincorporated enterprises in the LGA less employee compensation paid by those enterprises (equivalent to Gross Mixed Income generated in the LGA); plus

imputed Gross Value Added of owner-occupied houses in the LGA.

Corporate businesses are those incorporated with shareholders, who ultimately control the company and are entitled to dividends when paid. Various other forms of legal incorporation, which lack the shareholder-dividend component, are not treated as incorporated, save that the definition includes branches of overseas companies and is extended by the ABS on an ad-hoc basis to include businesses organised as co-operatives, credit unions and mutual societies where these businesses maintain full accounts and operate in a manner similar to shareholder companies. The extension includes trusts whose chief activity is the holding of financial assets. All other businesses and non-profit-making organisations are excluded from the definition – these exclusions include partnerships, trusts which operate businesses (especially in the agricultural sector), community and philanthropic non-profit institutions and any other non-shareholder organisations not specifically transferred to the corporate sector. In all cases Gross Mixed Income generated by the organisation is calculated after employee compensation is paid. It will be noted

that non-profit organisations are exempt from personal and corporation taxes so that the Gross Mixed Income they generate has to be estimated directly.

As regards organisations which generate taxable Mixed Income, the ABS definition is influenced by the definition used by the Tax Commissioner. This allows taxpayers to declare as business income any income in which compensation for the taxpayer’s labour is mixed with a capital return which is not legally separable from the labour return (as it is when incorporation requires the separation of employee compensation from dividends to shareholders). The Tax Commissioner allows the declaration of mixed income in respect of trusts operating in primary industry, but not otherwise. The ABS adjusts the net taxable income so declared back to Gross Mixed Income, adding back deductions declared by taxpayers, estimates for various non-taxable components and finally an estimate for understatement on tax returns. This is published by industry and postcode of taxpayer residence.

Control totals for Gross Local Product are available from the ABS State Accounts. NIEIR distributes the components as follows.

Employee compensation by local employment by industry (Census JTW adjusted and updated) and earnings (Census JTW, also tax statistics imputed by industry from area of residence back to area of work by JTW).

Gross taxable mixed income (including losses) generated by a similar process to employee compensation.

Gross non-taxable mixed income by local employment in such industries, from Census JTW.

Data sources Labour Force

Census

Journey to Work Matrix

Tax data

NIEIR modelling

APPENDIX A:GROSS PRODUCT DEFINITION

AND DATA SOURCESA

40

Tab

le B

.1 P

op

ula

tio

nSe

ries

Regi

on19

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

10A

nnua

l gro

wth

Popu

latio

nM

elbo

urne

’s N

orth

751,

332

757,

416

766,

801

774,

845

783,

239

790,

982

802,

124

814,

947

830,

619

847,

856

867,

791

883,

069

1.5%

Popu

latio

nM

elbo

urne

SD

3,38

0,41

73,

423,

359

3,47

2,20

73,

524,

533

3,57

8,00

23,

626,

603

3,68

1,22

63,

743,

635

3,81

8,41

53,

902,

673

3,99

6,16

04,

060,

991

1.7%

Popu

latio

nVi

ctor

ia4,

685,

965

4,74

0,88

64,

804,

269

4,86

2,56

34,

922,

902

4,98

0,82

35,

047,

896

5,12

5,77

05,

220,

540

5,32

6,20

85,

442,

458

5,52

0,13

31.

5%

MN

% o

f SD

– po

pula

tion

Mel

bour

ne’s

Nor

th22

.2%

22.1

%22

.1%

22.0

%21

.9%

21.8

%21

.8%

21.8

%21

.8%

21.7

%21

.7%

21.7

%-0

.2%

MN

% o

f VIC

– p

opul

atio

nM

elbo

urne

SD

16.0

%16

.0%

16.0

%15

.9%

15.9

%15

.9%

15.9

%15

.9%

15.9

%15

.9%

15.9

%16

.0%

0.0%

SD %

of V

IC –

pop

ulat

ion

Vict

oria

72.1

%72

.2%

72.3

%72

.5%

72.7

%72

.8%

72.9

%73

.0%

73.1

%73

.3%

73.4

%73

.6%

0.2%

MN

– p

opul

atio

n in

crea

seM

elbo

urne

’s N

orth

–0.

8%1.

2%1.

0%1.

1%1.

0%1.

4%1.

6%1.

9%2.

1%2.

4%1.

8%

SD –

pop

ulat

ion

incr

ease

Mel

bour

ne S

D–

1.3%

1.4%

1.5%

1.5%

1.4%

1.5%

1.7%

2.0%

2.2%

2.4%

1.6%

VIC

– po

pula

tion

incr

ease

Vict

oria

–1.

2%1.

3%1.

2%1.

2%1.

2%1.

3%1.

5%1.

8%2.

0%2.

2%1.

4%

Tab

le B

.2 N

um

ber

of

ho

use

ho

lds

Seri

esRe

gion

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Ann

ual g

row

th

Hous

ehol

dsM

elbo

urne

’s N

orth

251,

986

255,

250

258,

576

261,

196

264,

396

267,

691

270,

702

273,

401

275,

965

279,

194

282,

899

287,

255

1.2%

Hous

ehol

dsM

elbo

urne

SD

1,14

8,12

41,

165,

610

1,18

3,56

21,

199,

960

1,22

0,20

21,

240,

095

1,25

6,44

71,

271,

093

1,28

4,22

41,

299,

180

1,31

5,56

61,

332,

631

1.4%

Hous

ehol

dsVi

ctor

ia1,

591,

969

1,61

5,04

21,

638,

687

1,65

9,39

21,

685,

559

1,71

1,73

51,

734,

281

1,75

4,99

61,

773,

487

1,79

3,63

31,

814,

859

1,83

7,42

31.

3%

MN

% o

f SD

– ho

useh

olds

Mel

bour

ne’s

Nor

th21

.9%

21.9

%21

.8%

21.8

%21

.7%

21.6

%21

.5%

21.5

%21

.5%

21.5

%21

.5%

21.6

%-0

.2%

MN

% o

f VIC

– h

ouse

hold

sM

elbo

urne

SD

15.8

%15

.8%

15.8

%15

.7%

15.7

%15

.6%

15.6

%15

.6%

15.6

%15

.6%

15.6

%15

.6%

-0.1

%

SD %

of V

IC –

hou

seho

lds

Vict

oria

72.1

%72

.2%

72.2

%72

.3%

72.4

%72

.4%

72.4

%72

.4%

72.4

%72

.4%

72.5

%72

.5%

0.1%

MN

– h

ouse

hold

s in

crea

seM

elbo

urne

’s N

orth

–1.

3%1.

3%1.

0%1.

2%1.

2%1.

1%1.

0%0.

9%1.

2%1.

3%1.

5%

SD –

hou

seho

lds

incr

ease

Mel

bour

ne S

D–

1.5%

1.5%

1.4%

1.7%

1.6%

1.3%

1.2%

1.0%

1.2%

1.3%

1.3%

VIC

– ho

useh

olds

incr

ease

Vict

oria

–1.

4%1.

5%1.

3%1.

6%1.

6%1.

3%1.

2%1.

1%1.

1%1.

2%1.

2%

APP

END

IX B

:R

EGIO

NA

L SU

MM

ARY

TA

BLE

S M

ELB

OU

RN

E’S

NO

RTH

B

Post GFC SWOT: Melbourne’s North

41

Tab

le B

.3 N

IEIR

res

iden

t em

plo

ymen

tSe

ries

Regi

on19

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

10A

nnua

l gro

wth

NIE

IR e

mpl

oym

ent

Mel

bour

ne’s

Nor

th35

9,50

436

5,66

237

6,59

337

8,42

638

1,07

138

3,52

739