LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 1

LBMA Precious Metals Conference 2013, Rome Monday 30th September.

Is Europe waisting its crisis?Intervention of Francesco Papadia*

With the assistance of Mădălina Norocea1

2

I. Monnet and Padoa-Schioppa: on the brink theory. II. A complex crisis

a. Economic, b. Financial/monetary, c. Institutional, limitations in

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

III.The progress so fara. In the economic field, b. In the financial/monetary field, c. In the institutional field as regards

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

IV.An overall assessment.

PLAN OF THE PRESENTATION

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 2

3

I. Monnet and Padoa-Schioppa: on the brink theory. II. A complex crisis

a. Economic, b. Financial/monetary, c. Institutional, limitations in

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

III.The progress so fara. In the economic field, b. In the financial/monetary field, c. In the institutional field as regards

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

IV.An overall assessment.

Progressing through crises

4

Pro-active vs. Re-active

“the euro will survive and emerge stronger from the crisis”

“ J’ai toujours pensé que l’Europe se feraitdans les crises, et qu’elle serait la somme dessolutions qu’on apporterait à ces crises ”Jean Monnet

Adequate speed of speed of reaction?

“Delors fu capo, con un gesto che pochi ricordano.Il gesto fu di anticipare al 1988 la liberalizzazionedei movimenti di capitale, la liberalizzazionefinanziaria, innescando così quello stringersi dicontraddizioni che portò a riconoscere come solavia d´uscita la moneta unica”

Tommaso Padoa-Schioppa

If it’s not broken don’t fix it

...“Because deep national sovereignty is relinquished only

during an extraordinary crisis, the euro area policy response can only

be reactive” Bergsten, Kirkegaard

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 3

5

I. Monnet and Padoa-Schioppa: on the brink theory. II. A complex crisis

a. Economic, b. Financial/monetary, c. Institutional, limitations in

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

III.The progress so fara. In the economic field, b. In the financial/monetary field, c. In the institutional field as regards

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

IV.An overall assessment.

Crisis

GDP developments

0.9

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Ind

ex (

1999

bas

e ye

ar)

Germany Greece Ireland Italy Portugal Spain Euro area

Source: IMF

6

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 4

Budget deficit (% of GDP)

-35

-30

-25

-20

-15

-10

-5

0

519

91

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

%

Germany Greece Ireland Italy Portugal Spain

Crisis

Source: IMF

7

Public gross debt (%of GDP)

0

20

40

60

80

100

120

140

160

180

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

%

Germany Greece Ireland Italy Portugal Spain

Crisis

Source: IMF

8

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 5

9

Nominal unit labour costs

Source: EU Commission, AMECO

1.0

1.1

1.2

1.3

1.420

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Reb

ased

ind

ex (

200

5=10

0)

Germany Ireland Greece Spain Italy Portugal

Crisis

Current account balances (% of GDP)

-20

-15

-10

-5

0

5

10

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

%

Germany Greece Ireland Italy Portugal Spain

Crisis

Source: IMF

10

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 6

11

I. Monnet and Padoa-Schioppa: on the brink theory. II. A complex crisis

a. Economic, b. Financial/monetary, c. Institutional, limitations in

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

III.The progress so fara. In the economic field, b. In the financial/monetary field, c. In the institutional field as regards

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

IV.An overall assessment.

EONIA-MRO spread

Source: ECB

12

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

Jan-

03

Aug

-03

Mar

-04

Sep

-04

Apr

-05

Oct

-05

May

-06

Nov

-06

Jun-

07

Jan-

08

Jul-

08

Feb

-09

Aug

-09

Mar

-10

Sep

-10

Apr

-11

Nov

-11

May

-12

Dec

-12

bp

s

21 7653 4

Notes:(1) Lehman Brothers Collapse; Injection of liquidity via fine tuning operations(2) Narrowing of the corridor & Full allotment at fixed rate(3) 1st 1 year LTRO(4) Start of SMP(5) & (6)The 3 year LTROs(7) Deposit rate cut to 0

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 7

0.00

0.50

1.00

1.50

2.00

2.50

%

Euribor 3mth-OIS

Euribor 6mth-OIS

Euribor 12 mth-OIS

0

5

10

%

Spain IrelandPortugal Italy

10 yr govies spread to DE:

0

4

8

An

nu

al y

ield

%

DE and ES covered bond spread

Unprecedented spreads

13

Source: ECB, Markit

14

I. Monnet and Padoa-Schioppa: on the brink theory. II. A complex crisis

a. Economic, b. Financial/monetary, c. Institutional, limitations in

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

III.The progress so fara. In the economic field, b. In the financial/monetary field, c. In the institutional field as regards

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

IV.An overall assessment.

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 8

15

Economic and Fiscal Union

Idiosyncratic shocks

mutualizing tool

Banking union

Maastricht Treaty

Growth and Stability Pact

Single currency

Single payment system

National supervisi

on“doom loop”

Single currency

Shock absorbance alternative tool

Monetarists vs. Economists

Monetary Union

Mild version

Missing institutional components :

Crisis

16

I. Monnet and Padoa-Schioppa: on the brink theory. II. A complex crisis

a. Economic, b. Financial/monetary, c. Institutional, limitations in

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

III.The progress so fara. In the economic field, b. In the financial/monetary field, c. In the institutional field as regards

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

IV.An overall assessment.

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 9

Current account balances (% of GDP)

-20

-15

-10

-5

0

5

1019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

1420

1520

1620

1720

18

%

Germany Greece Ireland Italy Portugal Spain

Estimates

Source: IMF

17

Budget deficit (% of GDP)

-35

-30

-25

-20

-15

-10

-5

0

5

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

%

Germany Greece Ireland Italy Portugal Spain

Estimates

Source: IMF

18

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 10

19

Nominal unit labour costs

Source: EU Commission, AMECO

0.9

1.0

1.1

1.2

1.3

1.4

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Reb

ased

ind

ex (

200

5=10

0)

Germany Ireland Greece Spain Italy Portugal

Public gross debt (%of GDP)

020406080

100120140160180200

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

%

Germany Greece Ireland Italy Portugal Spain

Estimates

Source: IMF

20

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 11

Estimates

GDP developments

0.9

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Ind

ex (

199

9 b

ase

year

)

Germany Greece Ireland Italy Portugal Spain Euro area

Source: IMF

21

22

I. Monnet and Padoa-Schioppa: on the brink theory. II. A complex crisis

a. Economic, b. Financial/monetary, c. Institutional, limitations in

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

III.The progress so fara. In the economic field, b. In the financial/monetary field, c. In the institutional field as regards

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

IV.An overall assessment.

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 12

EONIA-MRO spread

Source: ECB

23

Notes:(1) Lehman Brothers Collapse; Injection of liquidity via fine tunning operations(2) Narrowing of the corridor & Full allotment at fixed rate(3) 1st 1 year LTRO(4) Start of SMP(5) & (6)The 3 year LTROs(8) Start of 3 yr LTROs early repayment (9) MRO rate cut

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4Ja

n-03

Aug

-03

Mar

-04

Sep

-04

Apr

-05

Oct

-05

May

-06

Nov

-06

Jun-

07

Jan-

08

Jul-

08

Feb

-09

Aug

-09

Mar

-10

Sep

-10

Apr

-11

Nov

-11

May

-12

Dec

-12

Jun-

13

bp

s

21 7653 4 8 9

Unprecedented spreads

Source: ECB, Markit

0

1

2

3

%

Euribor 3mth-OISEuribor 6mth-OISEuribor 12 mth-OIS

0

5

10

%

Spain Ireland

Portugal Italy

10 yr govies spread to DE:

0

2

4

6

8

Oct

-07

Jan-

08

Apr

-08

Jul-

08

Oct

-08

Jan-

09

Apr

-09

Jul-

09

Oct

-09

Jan-

10

Apr

-10

Jul-

10

Oct

-10

Jan-

11

Apr

-11

Jul-

11

Oct

-11

Jan-

12

Apr

-12

Jul-

12

Oct

-12

Jan-

13

Apr

-13

Jul-

13An

nu

al y

ield

%

24

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 13

25

I. Monnet and Padoa-Schioppa: on the brink theory. II. A complex crisis

a. Economic, b. Financial/monetary, c. Institutional, limitations in

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

III.The progress so fara. In the economic field, b. In the financial/monetary field, c. In the institutional field as regards

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

IV.An overall assessment.

26

Single currency

Single payment system

National supervisi

on

Economic and Fiscal Union

Idiosyncratic shocks mutualizing tool

Banking union

Maastricht Treaty

Growth and Stability Pact

“doom loop”

Single currency

Shock absorbance alternative tool

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 14

27

EU Economic Governance Regime1998/1999 Stability and Growth PactPreventive / Corrective Arm: Surveillance of budgetary and economic policies; Excessive deficit procedure implementation.2010 European SemesterSynchronizing the economic and fiscal reporting calendars; Changing the ex-post coordination to ex-ante; Dealing with the prevention part of the MIPMarch 2011 Euro Plus PactCoordination of fiscal policies through structural dialogDecember 2011 "Six Pack" (5 Regulations and 1 Directive)Applies to all 27 MS, with specific sanctioning rules to € area MSStrengthening the SGPs fiscal surveillance procedures: Reinforcing the Preventive and Corrective Arm (i.e. the EDP applied to the MS that breached the deficit/ debt criteria); Operationalizing the debt criteria (launching the EDP on the basis of a debt ratio of above 60% of GDP); Quantitative definition of "significant deviation" from MTO; Financial sanctions for €-area MS imposed gradually from preventive arm to later stages of EDP; Enforcing RQMV;Macroeconomic Scoreboard (MIP): New mechanism to identify and correct macroeconomic imbalances.

(*) “ Two pack” (2 Regulations )€-area MS onlyIntroduce stronger surveillance and assessment mechanism: Setting a common budgetary timeline; budget drafts to be presented to the EC before 15th of October; Common budgetary rules to be monitored by independent institutions

January 2013 Fiscal compactThe fiscal section of the TSCG (Treaty on Stability, Coordination and Governance) Compliance with budgetary and debt rules; Structural balance of general government should be at MTO or automatic adjustments will be triggered.

Note: (*) Proposed by the EC in November 2011 and agreed upon on February 2013

28

Single currency

Single payment system

National supervision

Economic and Fiscal Union

Idiosyncratic shocks mutualizing tool

Banking union

Maastricht Treaty

Growth and Stability Pact

“doom loop”

Single currency

Shock absorbance alternative tool

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 15

29

Banking union

A single Rule Book

A single supervision:

A single resolution mechanism

A common deposit guarantee scheme

ECBPolitical difficulties

Technical difficulties

Idiosyncratic shocks

mutualizing tool

EFSF

ESM

Liquidity provisions

30

I. Monnet and Padoa-Schioppa: on the brink theory. II. A complex crisis

a. Economic, b. Financial/monetary, c. Institutional, limitations in

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

III.The progress so fara. In the economic field, b. In the financial/monetary field, c. In the institutional field as regards

i. banking union, ii. fiscal and economic union,iii. mutualisation of shocks,

IV.An overall assessment.

LBMA/LPPM Precious Metals Conference 9/30/2013

Session 1 ‐ Papadia 16

31

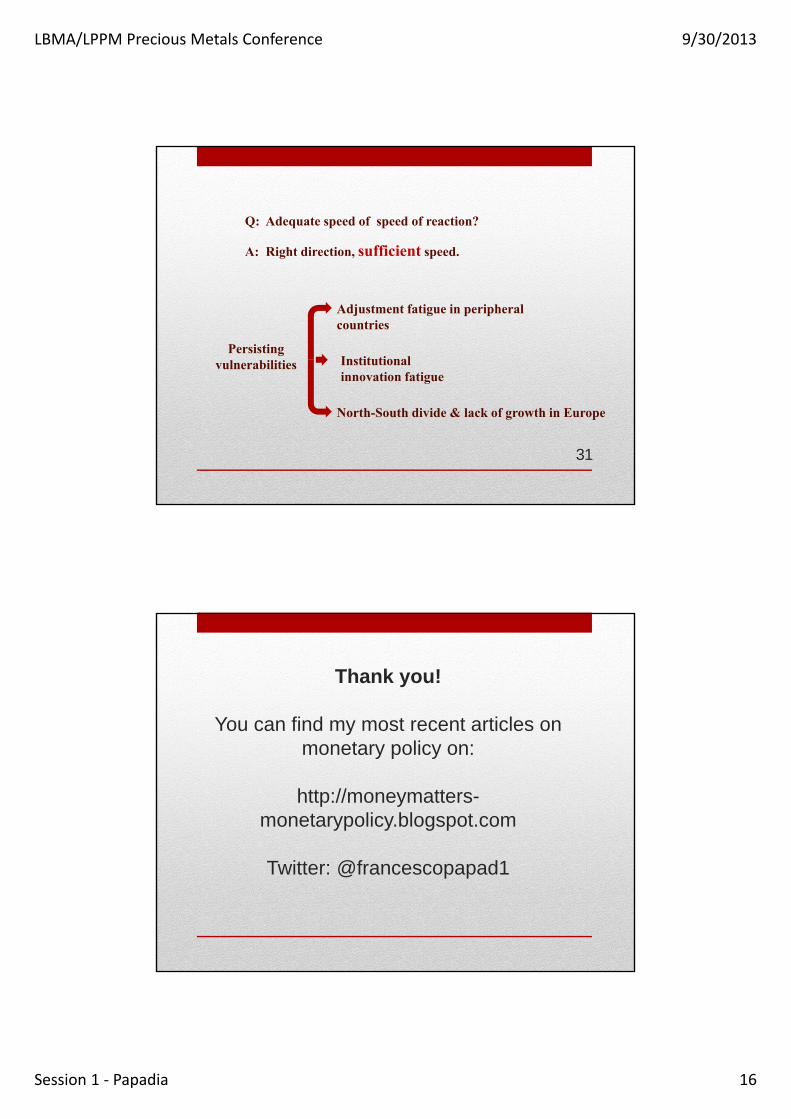

Q: Adequate speed of speed of reaction?

A: Right direction, sufficient speed.

Persisting vulnerabilities

Adjustment fatigue in peripheral countries

Institutional innovation fatigue

North-South divide & lack of growth in Europe

Thank you!

You can find my most recent articles on monetary policy on:

http://moneymatters-monetarypolicy.blogspot.com

Twitter: @francescopapad1