Maintaining U.S. Beef Industry Competitiveness with High-Priced Grain

Derrell S. Peel

Breedlove Professor of Agribusiness

And Livestock Marketing Specialist

Oklahoma State University

Major Beef Industry Issues

• Changes in U.S. Agriculture• Increased Global Demands on Agriculture• Current U.S. Beef Market Situation• Long Run Structural Change in the U.S. Beef

Industry• Other Issues

– Environmental, animal welfare, local foods, etc

U.S. Beef Industry Opportunities and Challenges

• Ability to use forage implies an important role in meeting global food demand

• High grain prices means that the beef industry must adjust production systems

• Beef industry must take advantage of flexibility in production to maintain competitiveness

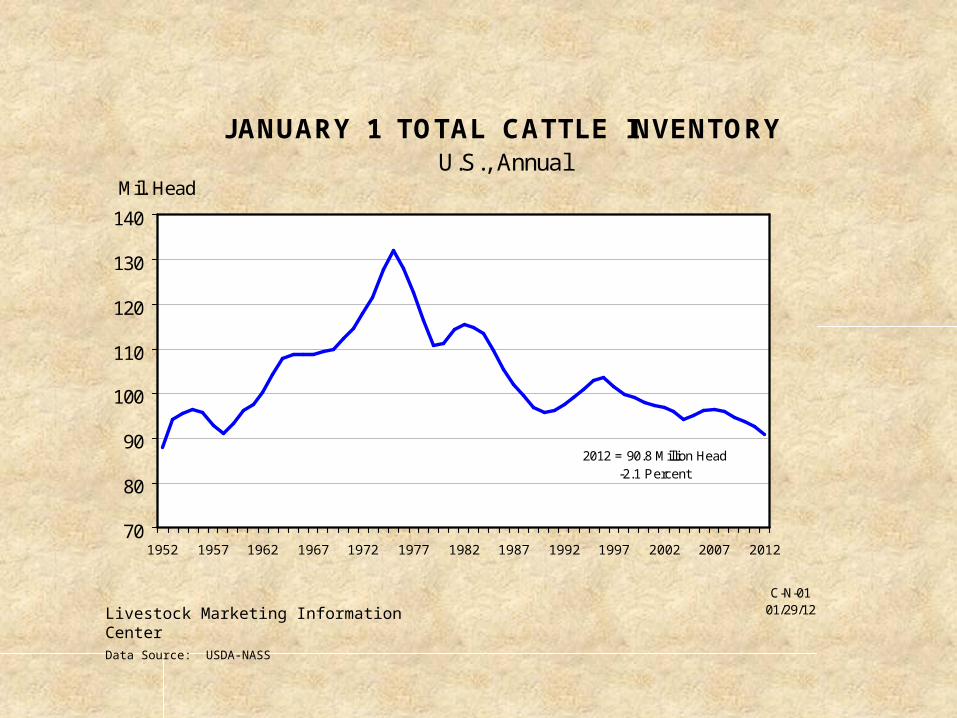

JANUARY 1 TOTAL CATTLE INVENTORYU.S., Annual

70

80

90

100

110

120

130

140

1952 1957 1962 1967 1972 1977 1982 1987 1992 1997 2002 2007 2012

Mil. Head

C-N-0101/29/12

-2.1 Percent2012 = 90.8 Million Head

Livestock Marketing Information CenterData Source: USDA-NASS

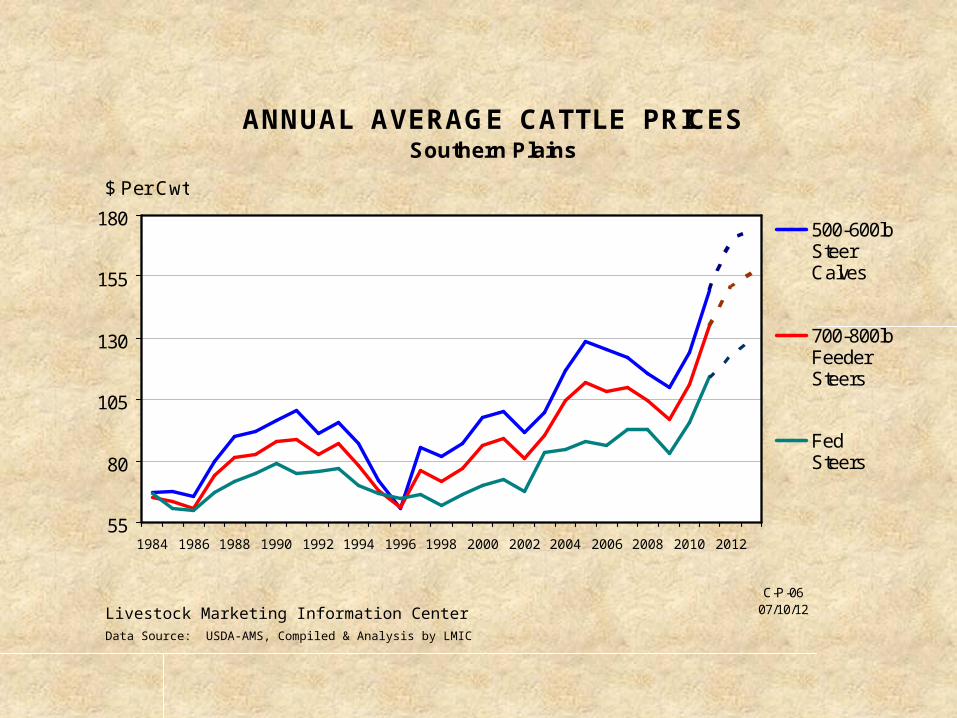

ANNUAL AVERAGE CATTLE PRICESSouthern Plains

55

80

105

130

155

180

1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

$ Per Cwt

500-600lbSteerCalves

700-800lbFeederSteers

FedSteers

C-P-0607/10/12Livestock Marketing Information Center

Data Source: USDA-AMS, Compiled & Analysis by LMIC

BEEF PRODUCTIONU.S., Annual

10

12

14

16

18

20

22

24

26

28

30

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Bil. Pounds

Livestock Marketing Information CenterData Source: USDA-NASS

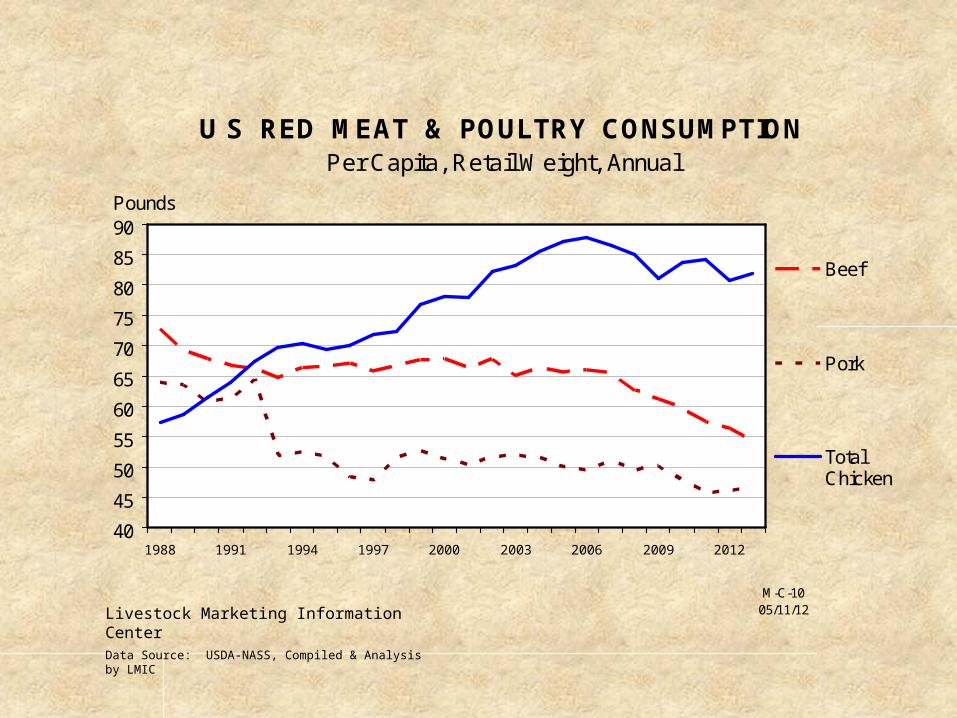

U S RED MEAT & POULTRY CONSUMPTIONPer Capita, Retail Weight, Annual

40

45

50

55

60

65

70

75

80

85

90

1988 1991 1994 1997 2000 2003 2006 2009 2012

Pounds

Beef

Pork

TotalChicken

M-C-1005/11/12Livestock Marketing Information Center

Data Source: USDA-NASS, Compiled & Analysis by LMIC

United States: Beef Trade

0200400600800

10001200140016001800

1,00

0 M

ET

RIC

TO

NS

Exports Imports

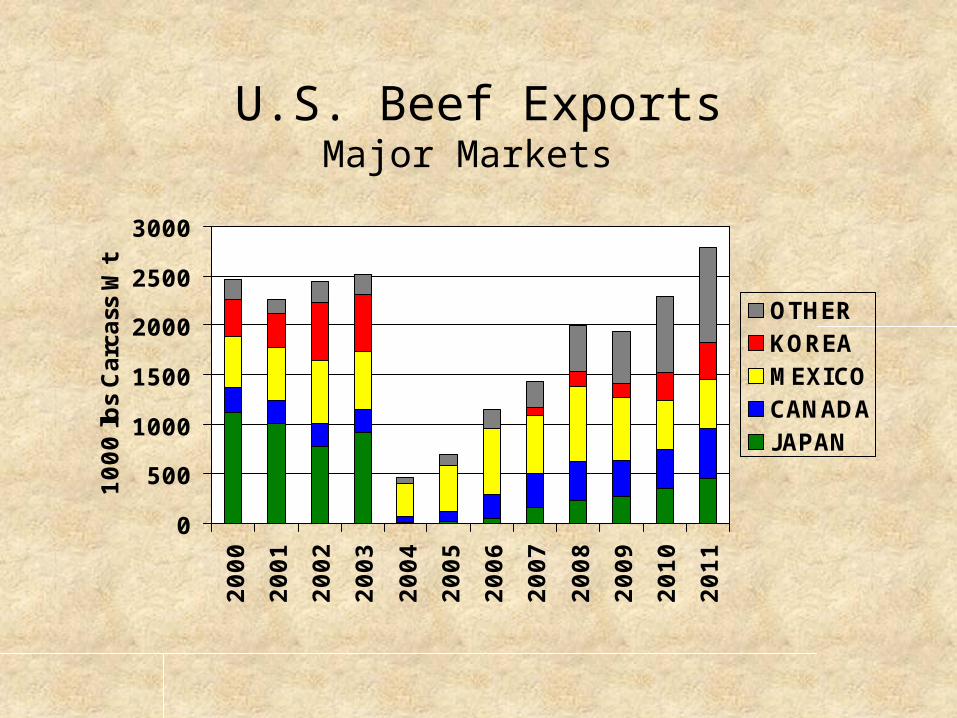

U.S. Beef ExportsMajor Markets

0

500

1000

1500

2000

2500

30002000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1000 lbs

Carc

ass

Wt

OTHERKOREAMEXICOCANADAJAPAN

MAJOR U S BEEF IMPORT SOURCESCarcass Weight, Annual

0

200

400

600

800

1000

1200

Australia NewZealand

Canada Mexico Nicaragua Uruguay Brazil Argentina

Mil. Pounds

Avg.2005/09

2010

2011

I-N-3605/11/12Livestock Marketing Information Center

Data Source: USDA-ERS & USDA-FAS, Compiled & Analysis by LMIC

CATTLE IMPORTS FROM CANADA AND MEXICO

Annual

0

500

1000

1500

2000

1986 1989 1992 1995 1998 2001 2004 2007 2010

Thou. Head

Mexico

Canada

I-N-1305/11/12Livestock Marketing Information Center

Data Source: USDA-ERS & USDA-FAS, Compiled & Analysis by LMIC

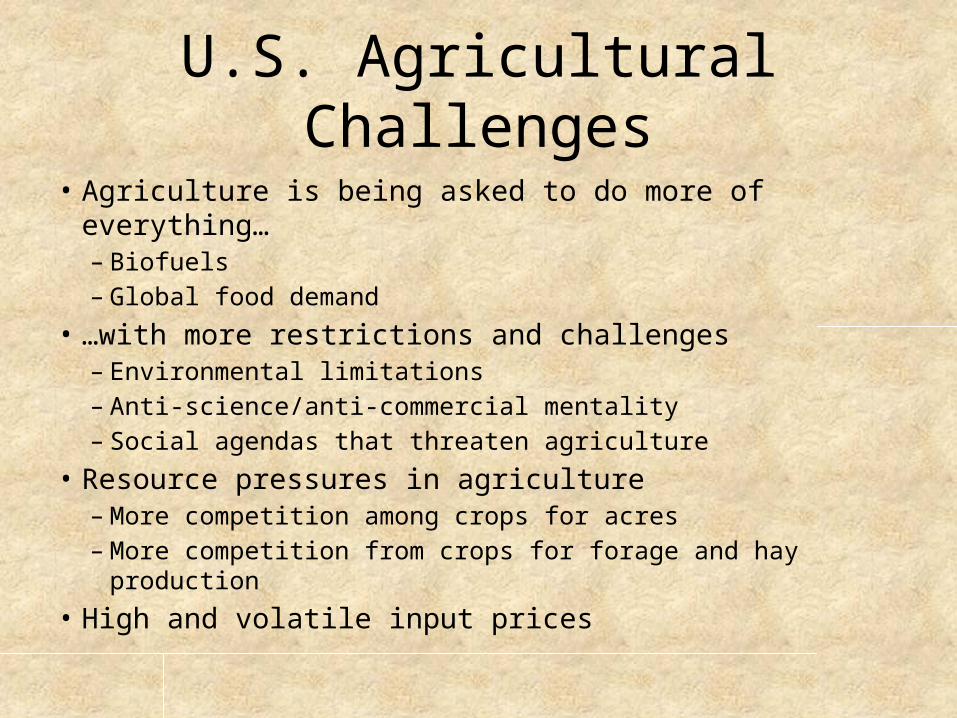

U.S. Agricultural Challenges

• Agriculture is being asked to do more of everything…– Biofuels – Global food demand

• …with more restrictions and challenges– Environmental limitations– Anti-science/anti-commercial mentality– Social agendas that threaten agriculture

• Resource pressures in agriculture– More competition among crops for acres– More competition from crops for forage and hay production

• High and volatile input prices

Corn for Food, Seed and Industrial Use

0

1000

2000

3000

4000

5000

6000

7000

Mil

lio

n B

ush

els

Ethanol

Other

U.S. CORN DISAPPEARANCE AND STOCKSCrop Year

0

2

4

6

8

10

12

14

16

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Bil. Bushels

Stocks

Exports

Food, Seed& Industrial

Feed &Residual

G-NP-1206/29/12Livestock Marketing Information Center

Data Source: USDA-NASS, Compiled & Forecasts by LMIC

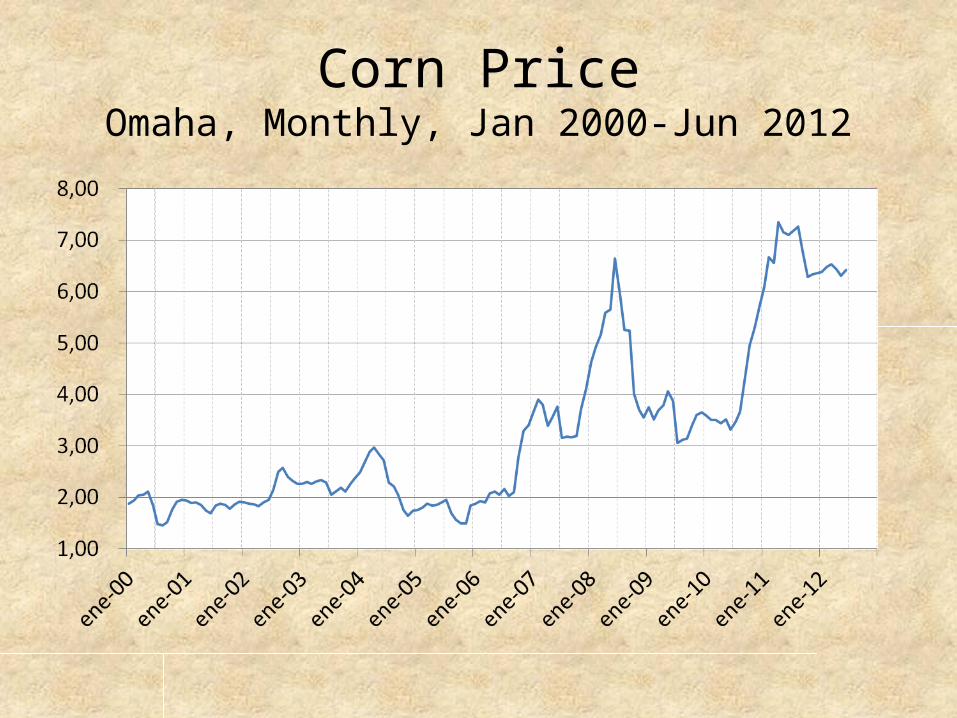

Corn PriceOmaha, Monthly, Jan 2000-Jun 2012

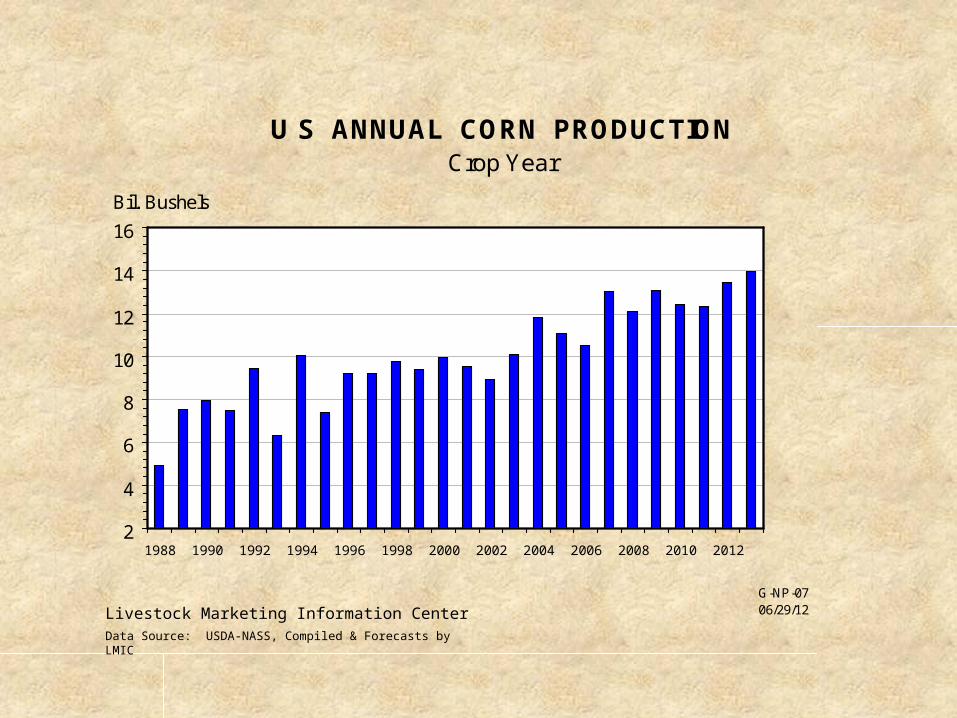

U S ANNUAL CORN PRODUCTIONCrop Year

2

4

6

8

10

12

14

16

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Bil. Bushels

G-NP-0706/29/12Livestock Marketing Information Center

Data Source: USDA-NASS, Compiled & Forecasts by LMIC

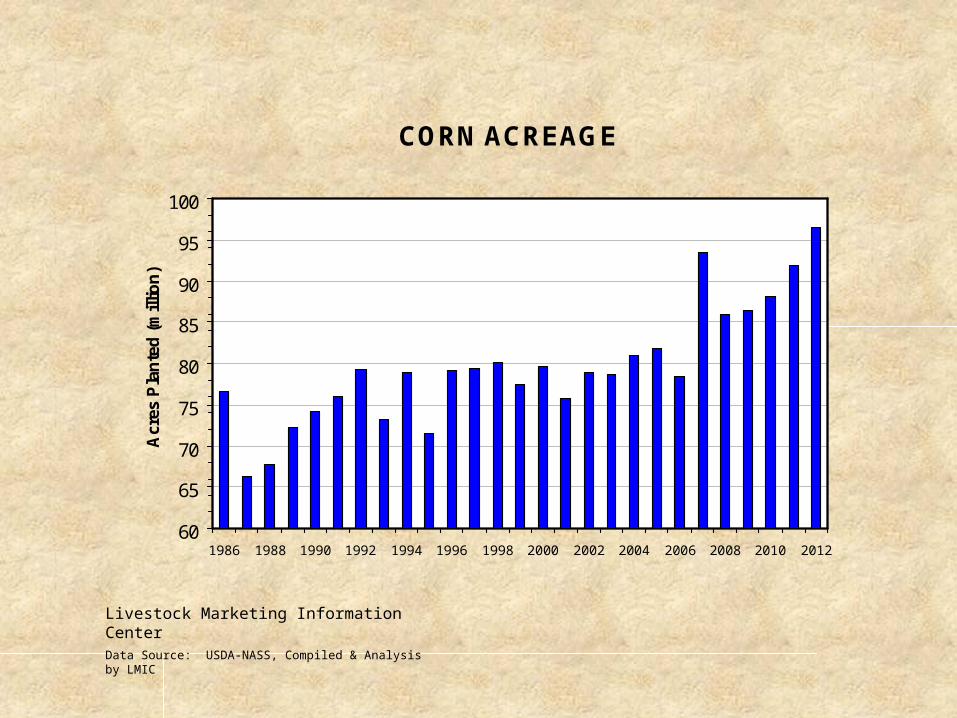

CORN ACREAGE

60

65

70

75

80

85

90

95

100

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Acr

es P

lan

ted

(m

illio

n)

Livestock Marketing Information CenterData Source: USDA-NASS, Compiled & Analysis by LMIC

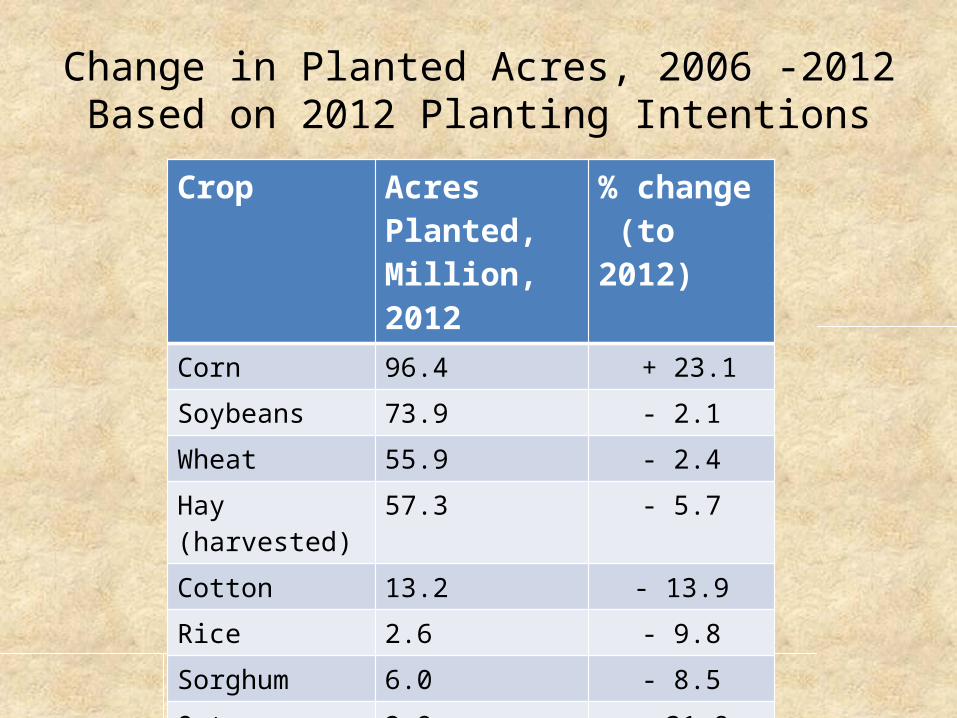

Change in Planted Acres, 2006 -2012Based on 2012 Planting Intentions

Crop Acres Planted, Million, 2012

% change (to 2012)

Corn 96.4 + 23.1Soybeans 73.9 - 2.1Wheat 55.9 - 2.4Hay (harvested) 57.3 - 5.7Cotton 13.2 - 13.9Rice 2.6 - 9.8Sorghum 6.0 - 8.5Oats 2.9 - 31.8Barley 3.3 - 4.9

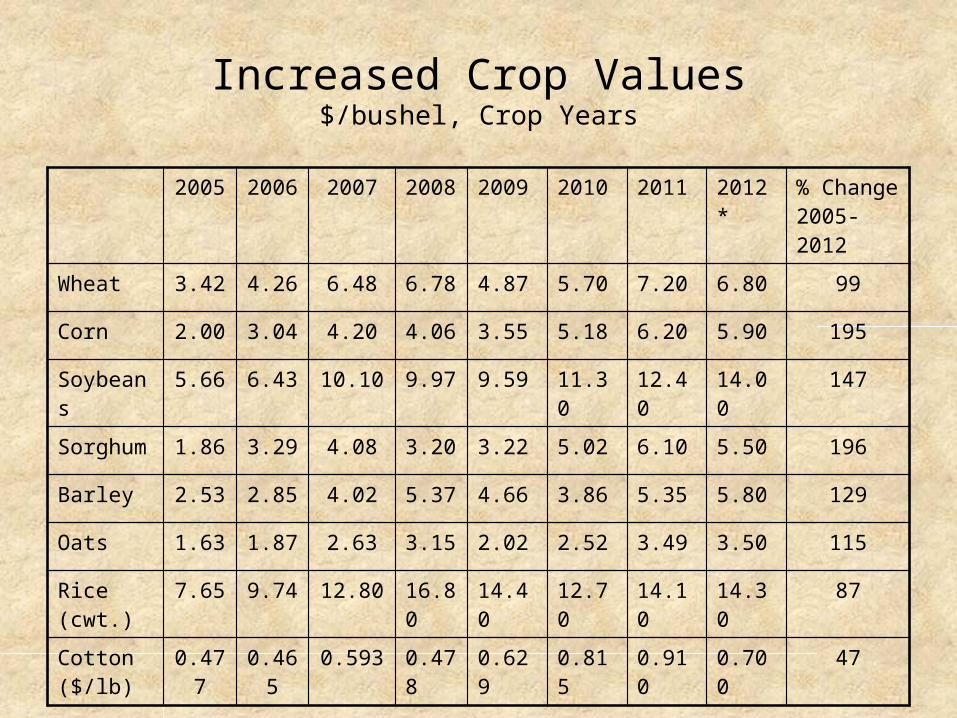

Increased Crop Values$/bushel, Crop Years

2005 2006 2007 2008 2009 2010 2011 2012* % Change 2005-2012

Wheat 3.42 4.26 6.48 6.78 4.87 5.70 7.20 6.80 99

Corn 2.00 3.04 4.20 4.06 3.55 5.18 6.20 5.90 195

Soybeans 5.66 6.43 10.10 9.97 9.59 11.30 12.40 14.00 147

Sorghum 1.86 3.29 4.08 3.20 3.22 5.02 6.10 5.50 196

Barley 2.53 2.85 4.02 5.37 4.66 3.86 5.35 5.80 129

Oats 1.63 1.87 2.63 3.15 2.02 2.52 3.49 3.50 115

Rice (cwt.)

7.65 9.74 12.80 16.80 14.40 12.70 14.10 14.30 87

Cotton ($/lb)

0.477 0.465 0.593 0.478 0.629 0.815 0.910 0.700 47

Short and Long Run Impacts of High Grain Prices on Beef Cattle

• Short Run– Adjustments within current production systems

• Tweaking the current system

– Other factors dominating • Current market situation

• Long Run– Adjustments to new production systems

• Different fundamental market incentives

– Within the context of dynamic short market conditions

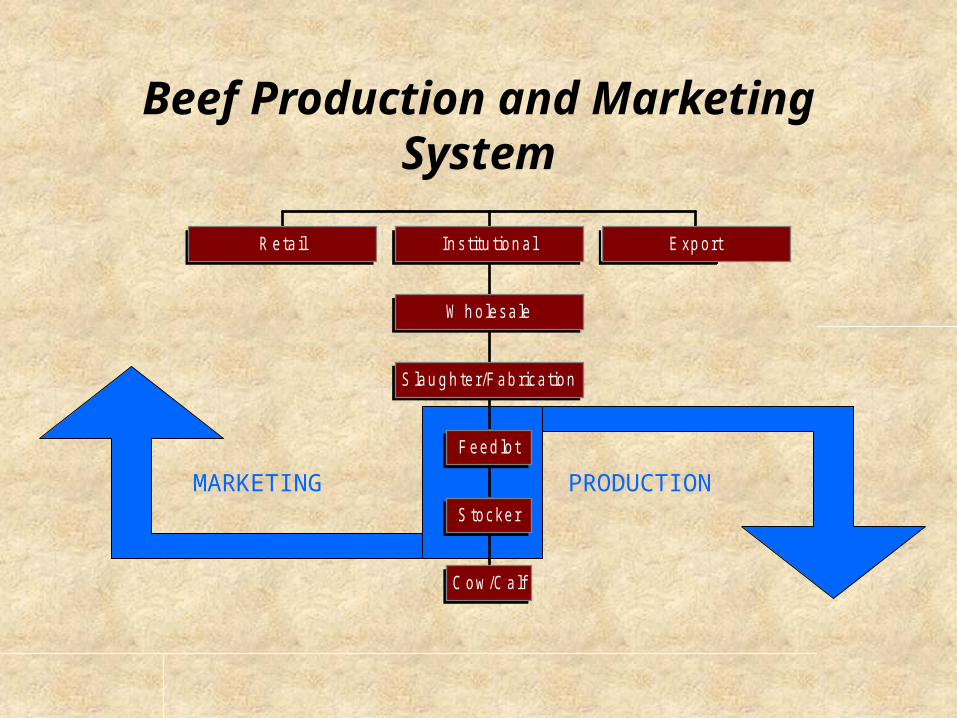

Beef Production and Marketing System

R eta il

C ow /C a lf

S tocker

F eed lo t

S lau g h te r/F ab rica tion

W h o lesa le

In s titu tion a l E xp ort

MARKETING PRODUCTION

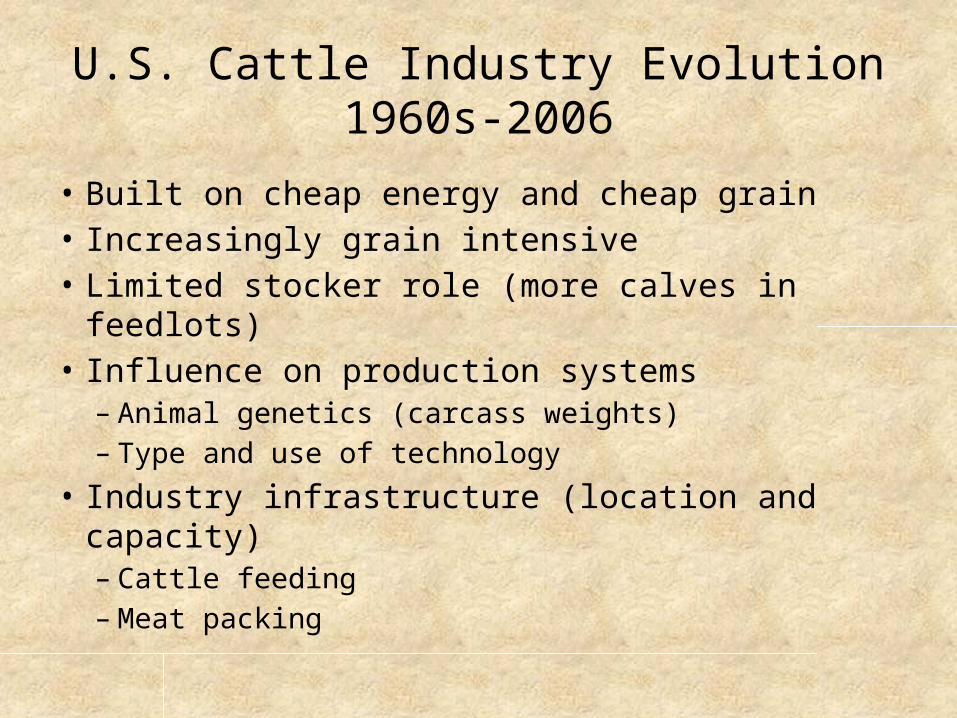

U.S. Cattle Industry Evolution1960s-2006

• Built on cheap energy and cheap grain• Increasingly grain intensive• Limited stocker role (more calves in feedlots)• Influence on production systems

– Animal genetics (carcass weights)– Type and use of technology

• Industry infrastructure (location and capacity)– Cattle feeding – Meat packing

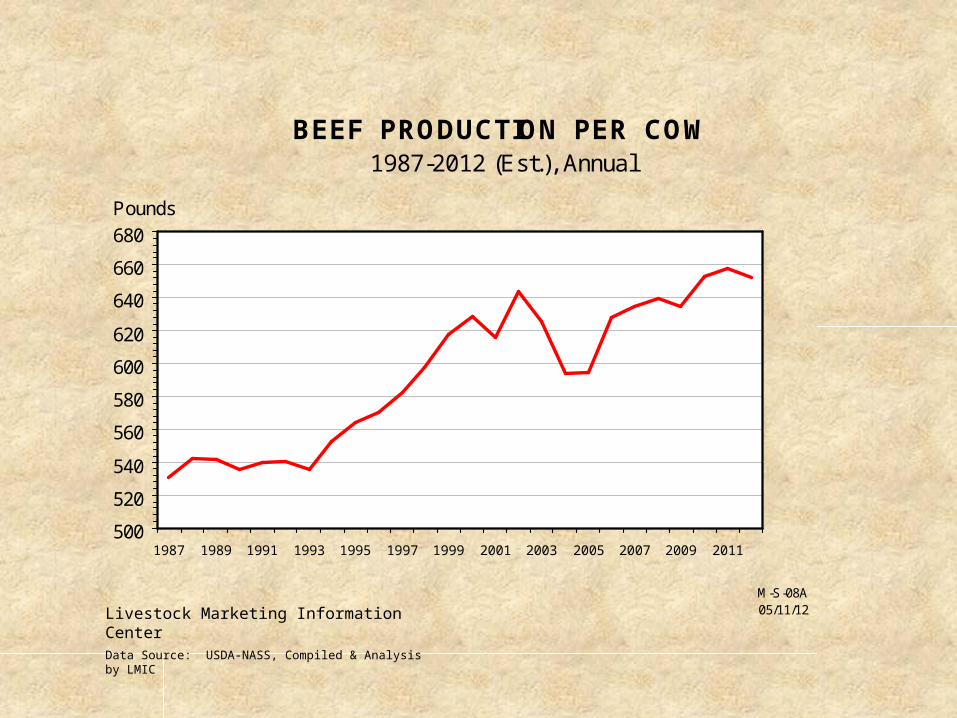

BEEF PRODUCTION PER COW1987-2012 (Est.), Annual

500

520

540

560

580

600

620

640

660

680

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

Pounds

M-S-08A05/11/12Livestock Marketing Information Center

Data Source: USDA-NASS, Compiled & Analysis by LMIC

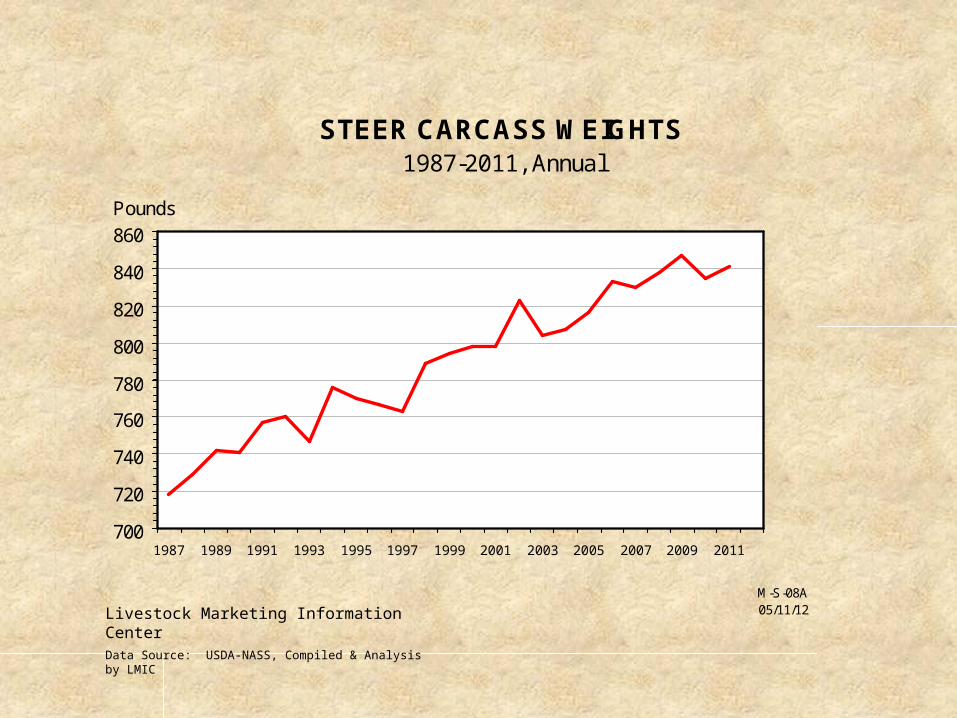

STEER CARCASS WEIGHTS1987-2011, Annual

700

720

740

760

780

800

820

840

860

1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

Pounds

M-S-08A05/11/12Livestock Marketing Information Center

Data Source: USDA-NASS, Compiled & Analysis by LMIC

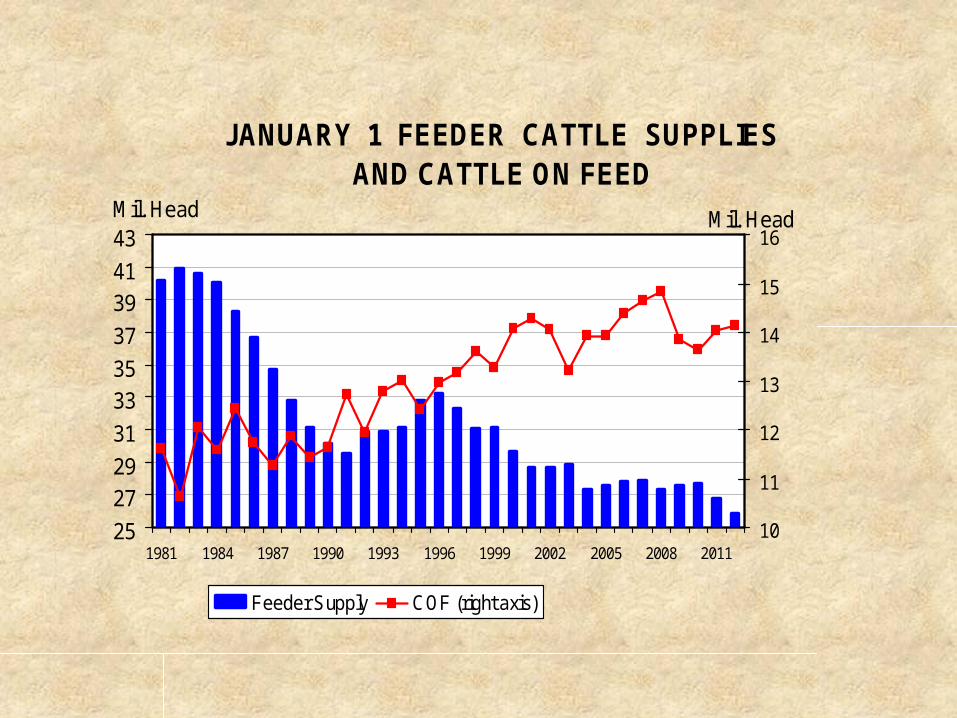

JANUARY 1 FEEDER CATTLE SUPPLIES AND CATTLE ON FEED

25

2729

31

3335

37

3941

43

1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

Mil. Head

10

11

12

13

14

15

16Mil. Head

Feeder Supply COF (right axis)

Cattle on Feed as a % of Feeder Supply, January 1

24%

28%

32%

36%

40%

44%

48%

52%

56%

“The Beef Industry Can Survive High Corn Prices Better Than the

Pork and Poultry Industries”

• True statement?• What are the implications for the beef industry?

It is often said:

KANSAS FEEDLOT CLOSEOUTSPounds of Feed (Dry Basis)Per Pound of Gain, Steers

5.6

5.7

5.8

5.9

6.0

6.1

6.2

6.3

6.4

6.5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Pounds

Avg.2006/10

2011

2012

06/29/12Data Source: KSU Focus on Feedlots, Compiled by LMIC

Estimated Concentrate Feed per Pound of Meat Produced

• Broilers 1.80• Hogs 2.90• Beef (by feedlot placement weight)

– 550 lb. 3.50– 750 lb. 3.02– 1000 lb. 2.39

Beef Industry Market Coordination

• Price Signals to Coordinate Production Sectors– Level of Production– Change Production System

• Allocate Forage Resources• Grain versus Forage Use

– Timing

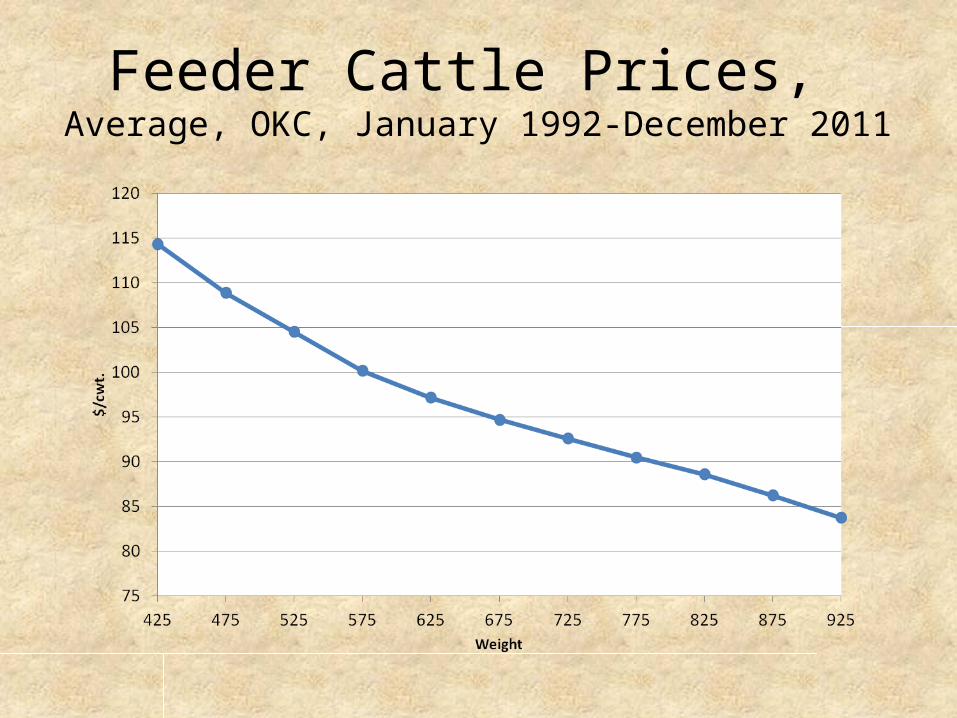

Feeder Cattle Prices, Average, OKC, January 1992-December 2011

Price Signals in the Beef Industry

• Cow-calf Production– Increase or decrease cattle production based on calf

prices• Stocker Production

– Increase or decrease forage use based on price relationship between light and heavy feeder cattle

• Feedlot Production– Increase or decrease grain use based on grain price

and relationship between light and heavy feeder cattle

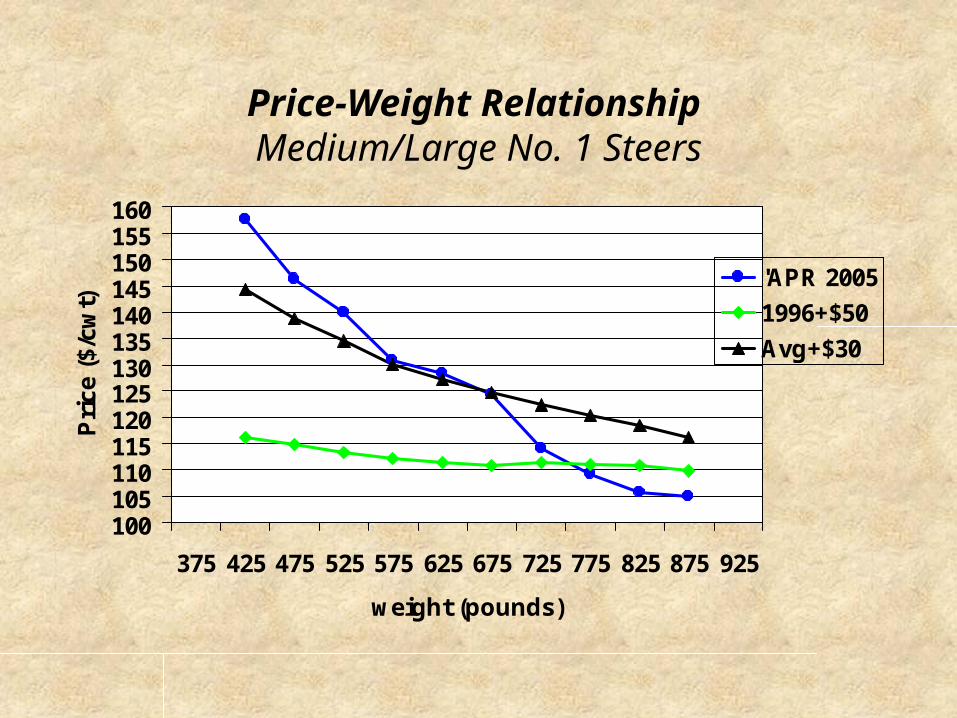

Price-Weight Relationship Medium/Large No. 1 Steers

100105110115120125130135140145150155160

375 425 475 525 575 625 675 725 775 825 875 925

weight (pounds)

Pri

ce (

$/cw

t)

'APR 2005

1996+$50

Avg+$30

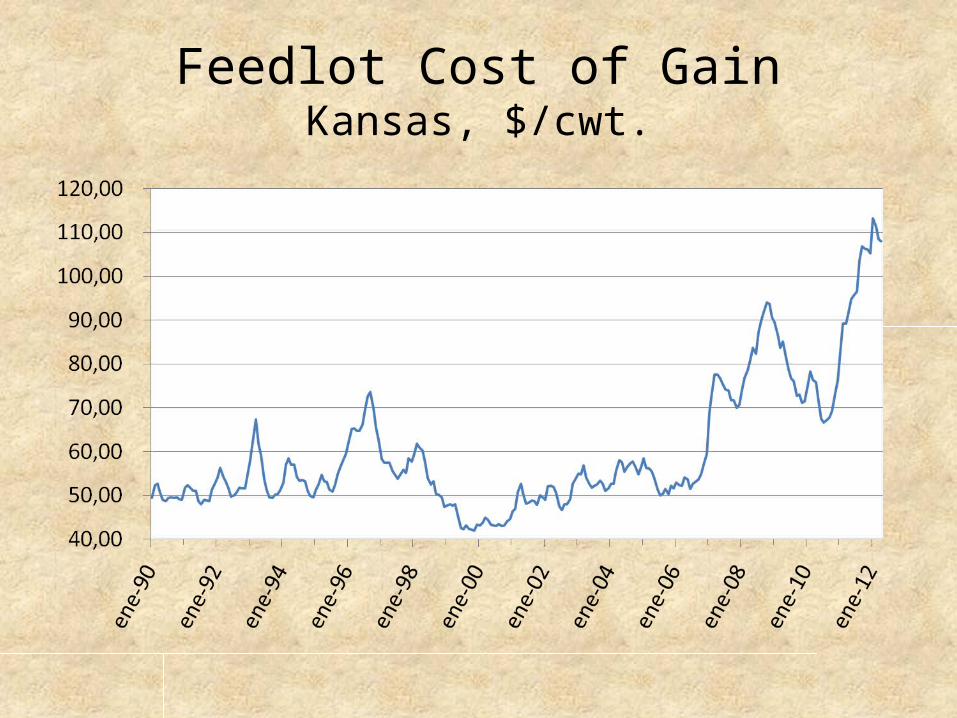

Feedlot Cost of GainKansas, $/cwt.

Cattle Markets are Providing Twin Signals to U.S. Producers at the Current Time

• Increase Calf Production– Herd Expansion– May change in 3-6 years

• More Stocker Production– Keep feeder cattle on forage longer– More flexibility– Likely to be permanent

• Both Signals Imply Increased Demand for Forage

Permanently Higher Grain Prices is a Game Changer for the U.S. Beef Industry

• Change from grain intensive to forage intensive to maintain competitiveness– Must emphasize ruminant advantages– Will continue to use grain finishing but in a less intensive way– Enhanced role for stocker production

• Influence on production systems– Animal genetics (change animal size?)– Type and use of technology?– Better forage management– New forages and new forage systems?

• Industry infrastructure (location and capacity)– Different feeding industry?– Regional shifts in cattle feeding, cow-calf and stocker production

Potential Structural Change in the U.S. Beef Industry

Current System New System?

Cow Size (pounds) 1100-1500 950-1350

Stocker (Forage based) Gain (pounds) 0-400 150-500

Feedlot Placement Weight (pounds) 550-850 750-1050

Slaughter Weight (pounds) 1250-1500 1050-1300

Days on Feed (Feedlot) 130-200 90-120

Feedlot (Grain based) Gain (pounds) 450-700 300-500

Age at Slaughter 15-20 18-22

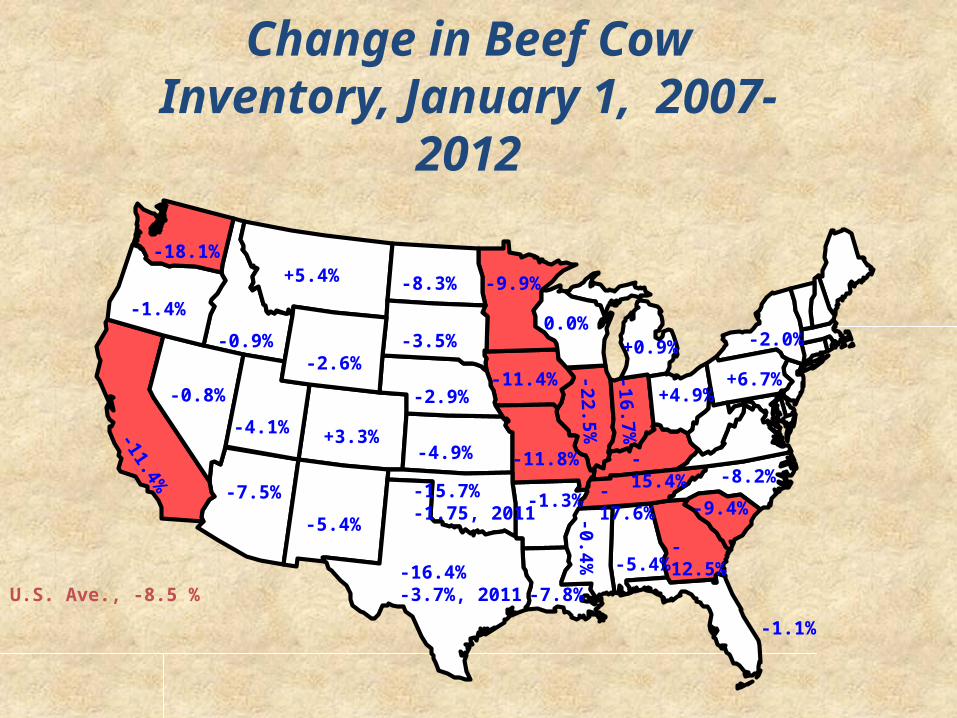

U.S. Ave., -8.5 %

Change in Beef Cow Inventory, January 1, 2007-2012

-11.4%

-18.1%

-1.4%

+5.4%

-0.9%-2.6%

+3.3%-4.9%

-15.7%-1.75, 2011-5.4%

-4.1%

-16.4%-3.7%, 2011

-11.8%

-1.1%

-15.4%

-8.3%

-3.5%

-2.9%

-17.6%

-5.4%-12.5%

-1.3%

-11.4%-0.8%

-7.5%

-9.9%

-7.8%

0.0%

-22.5%

-16.7%

-0.4%

-9.4%

-8.2%

+4.9%

+0.9%

+6.7%

-2.0%

“The Beef Industry Can Survive High Corn Prices Better Than the

Pork and Poultry Industries”• True, but with implications

– Ruminant flexibility is an advantage only if the industry changes to capitalize on those capabilities

– Failure to change is a disadvantage• Ruminants will always be the least efficient user of

grain

The U.S. Beef Industry Faces New Questions

• For the last 4-5 decades:– “How can we get cattle to use more grain?”

• For the coming decades:– “How can we produce high quality beef using the

least amount of grain?”

The Weekly Email NewsletterFrom OSU Animal Science and Agricultural Economics

Send Email to [email protected]

THANK YOU!