Download - Knowing Early and Enough Prevents Bank Runs

© Copyright 2005 All Rights Reserved

Knowing Early and Enough Prevents Bank Runs

Presented by: Jean Pierre Sabourin, CEO

International Financial Planning Advisors Conference 23 February 2008

Discussion

Importance of public awareness on deposit insurance

Lessons learnt from the Northern Rock bank run

Deposit insurance – a form of consumer protection and its importance in financial planning

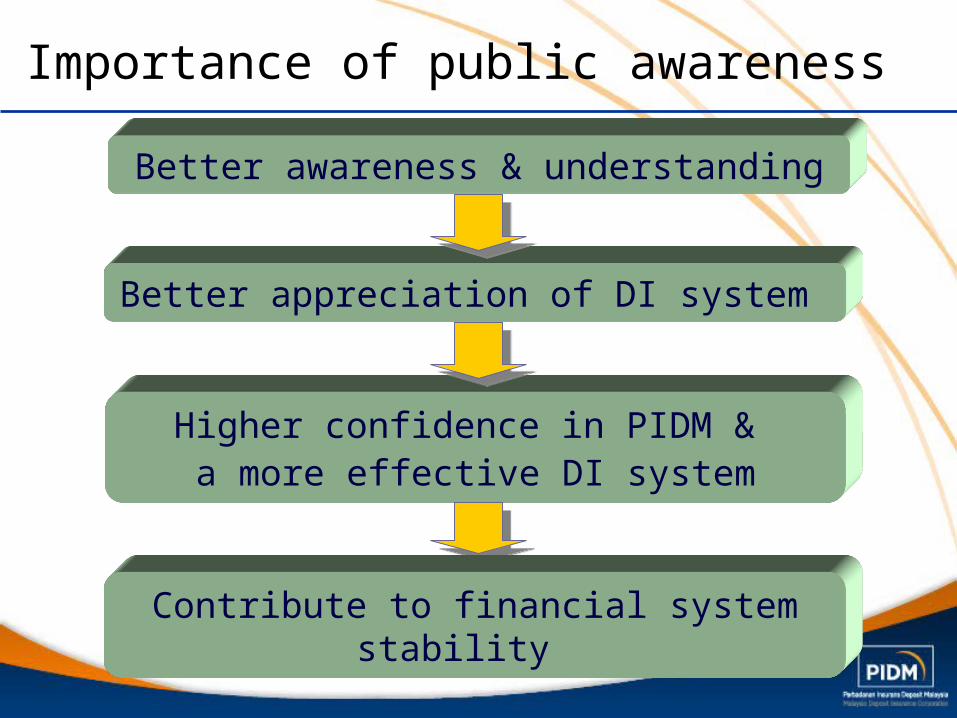

Importance of public awareness

Better awareness & understanding

Better appreciation of DI system

Higher confidence in PIDM & a more effective DI system

Contribute to financial system stability

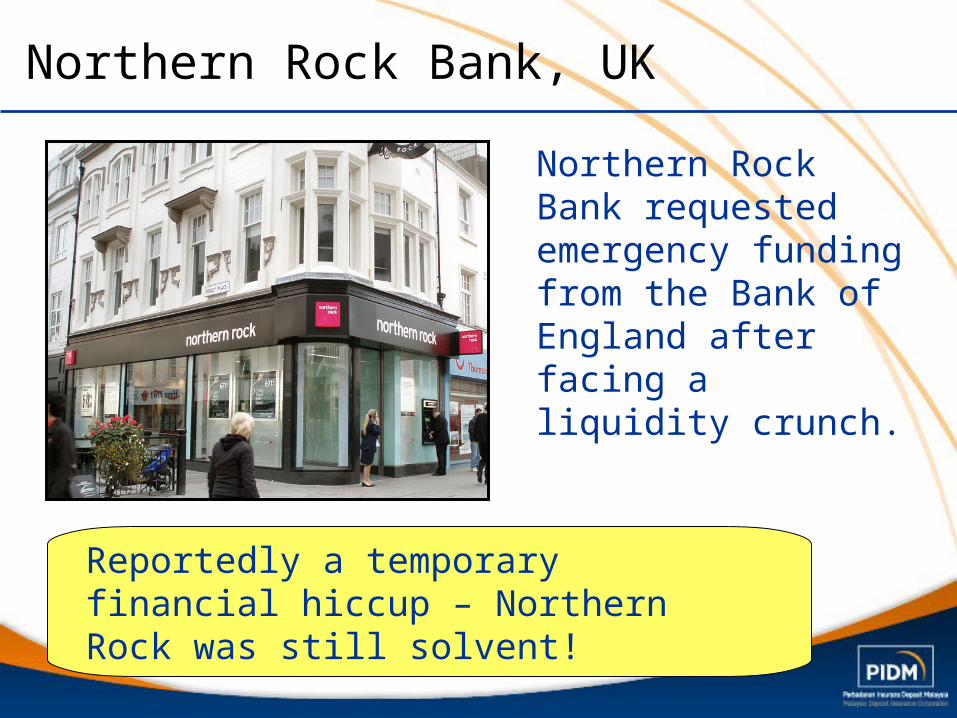

Northern Rock Bank, UK

Northern Rock Bank requested emergency funding from the Bank of England after facing a liquidity crunch.

Reportedly a temporary financial hiccup – Northern Rock was still solvent!

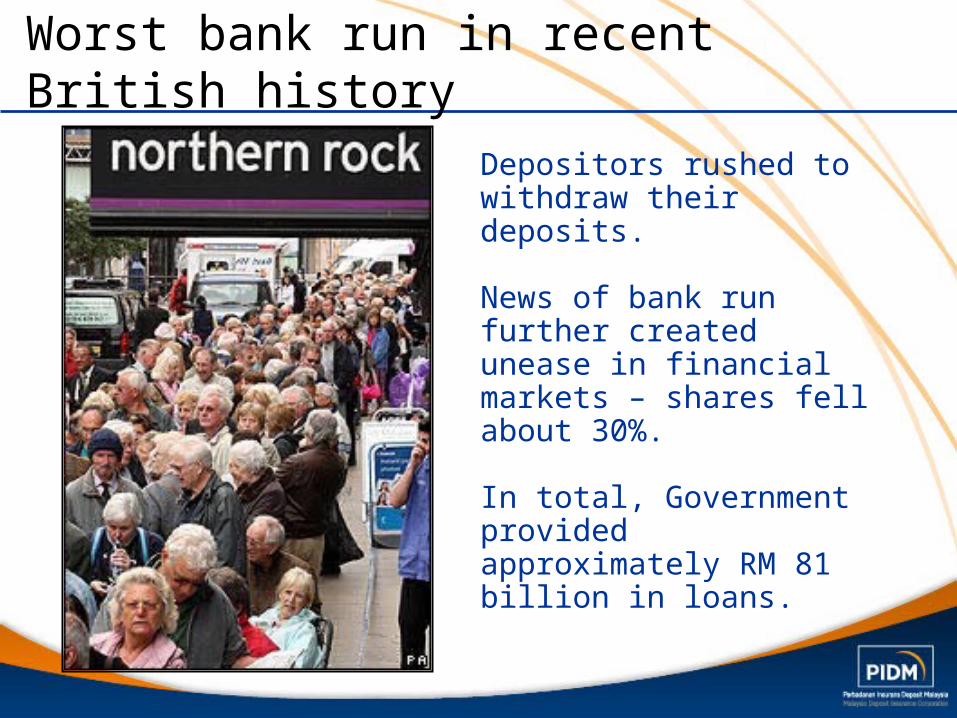

Worst bank run in recent British history

Depositors rushed to withdraw their deposits.

News of bank run further created unease in financial markets – shares fell about 30%.

In total, Government provided approximately RM 81 billion in loans.

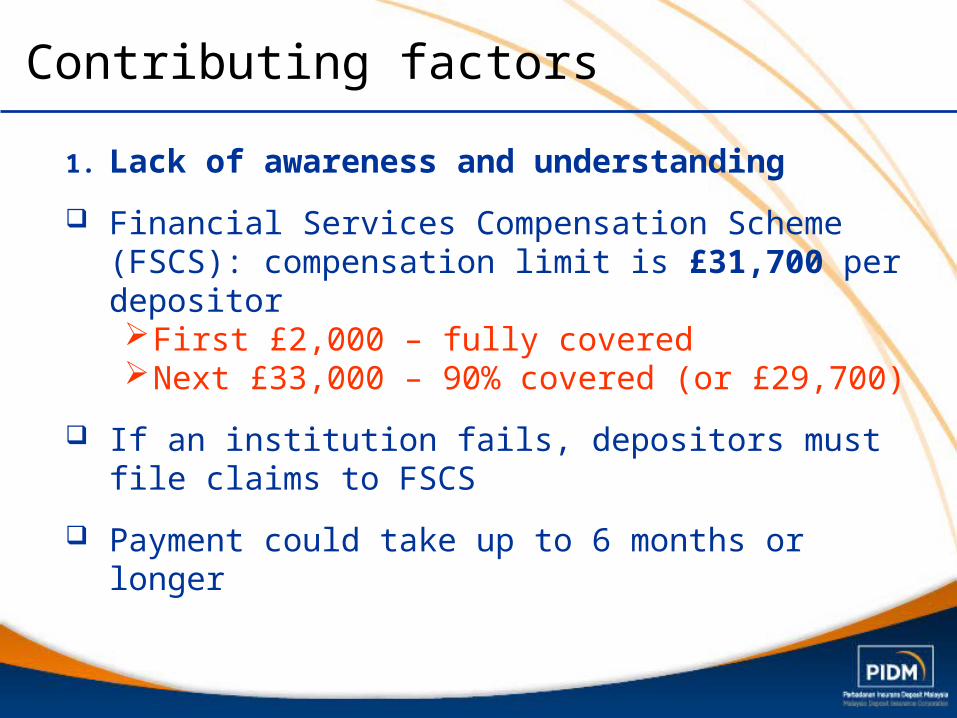

Contributing factors

1. Lack of awareness and understanding

Financial Services Compensation Scheme (FSCS): compensation limit is £31,700 per depositorFirst £2,000 – fully coveredNext £33,000 – 90% covered (or £29,700)

If an institution fails, depositors must file claims to FSCS

Payment could take up to 6 months or longer

Contributing factors (cont’d)

2. Lack of confidence

Depositors do not fully understand how the scheme

worked felt that they had to wait too long for

their deposits to be reimbursed also felt that the coverage limit was

inadequate

Subsequently, guarantee increased to 100% (up to £35,000).

What can we learn from Northern Rock?

LESSON NO. 1LESSON NO. 1

Peace of mind only works if you know you are adequately protected.

LESSON NO. 2LESSON NO. 2

Never say "don't panic”.

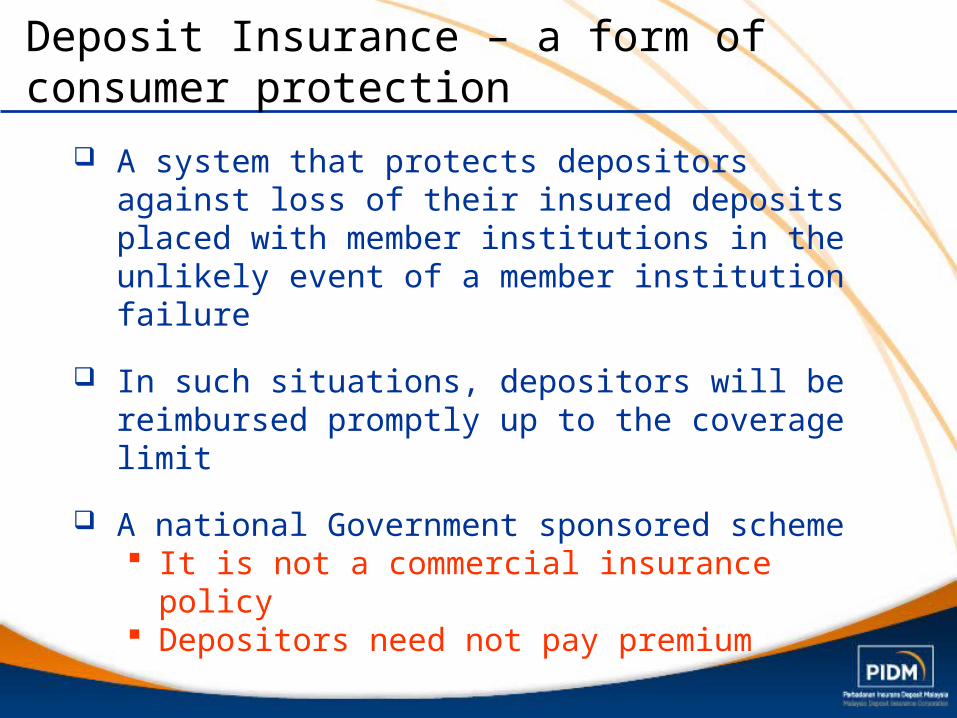

Deposit Insurance – a form of consumer protection

A system that protects depositors against loss of their insured deposits placed with member institutions in the unlikely event of a member institution failure

In such situations, depositors will be reimbursed promptly up to the coverage limit

A national Government sponsored scheme It is not a commercial insurance policy Depositors need not pay premium

Importance of deposit insurance

Deposit insurance contributes to the overall economic growth by building public confidence in the banking system

PIDM is committed in building public awareness

It is crucial for depositors to know how deposit insurance works for them

In bad times, such knowledge gives certainty and comfort to depositors in the face of rumours of bank failure

Deposit insurer’s fundamental role

One of a deposit insurer’s fundamental role –wealth protection

Our role complements the major role of the financial planning profession – wealth creation and management

Most clients’ investment portfolio would also include deposit products offered by banks

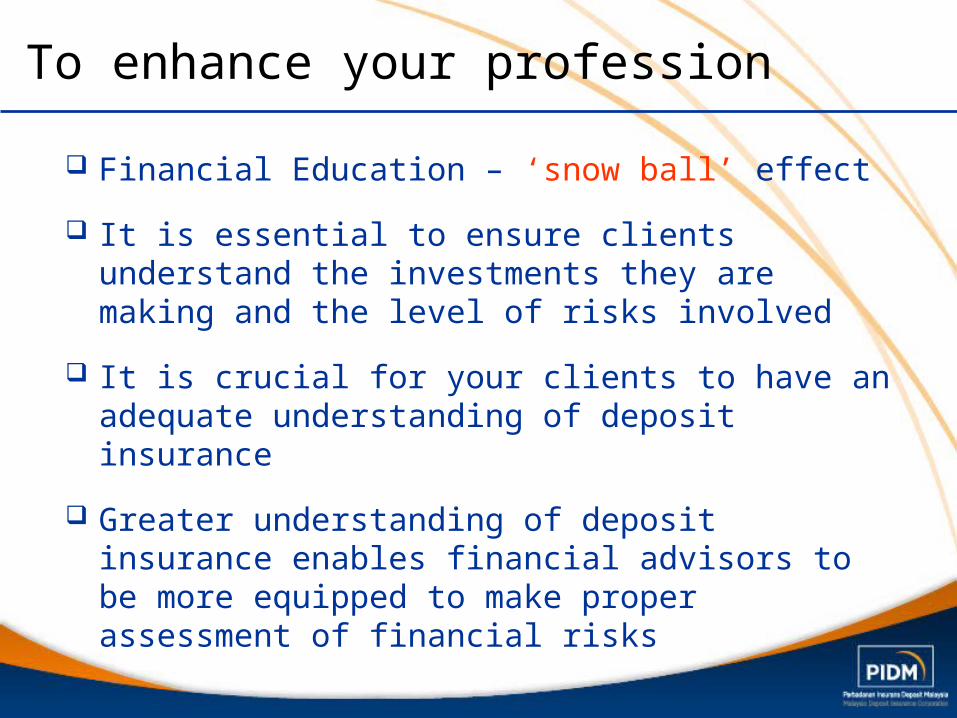

To enhance your profession

Financial Education – ‘snow ball’ effect

It is essential to ensure clients understand the investments they are making and the level of risks involved

It is crucial for your clients to have an adequate understanding of deposit insurance

Greater understanding of deposit insurance enables financial advisors to be more equipped to make proper assessment of financial risks

Financial literacy promotes market discipline

A well-informed public less susceptible to unsubstantiated rumours, hence preventing such rumours from creating consumer panic

Financial literacy aims to educate consumers

ability to make informed decisions on financial products

access to information and ability to compare information

capability to scrutinise conduct of banking institutions

Value of the deposit insurance system

A well-designed deposit insurance system forms a stable financial system

The establishment of an effective deposit insurance system can also mitigate the problem of moral hazard, the existence of which often undermines the value of deposit insurance system

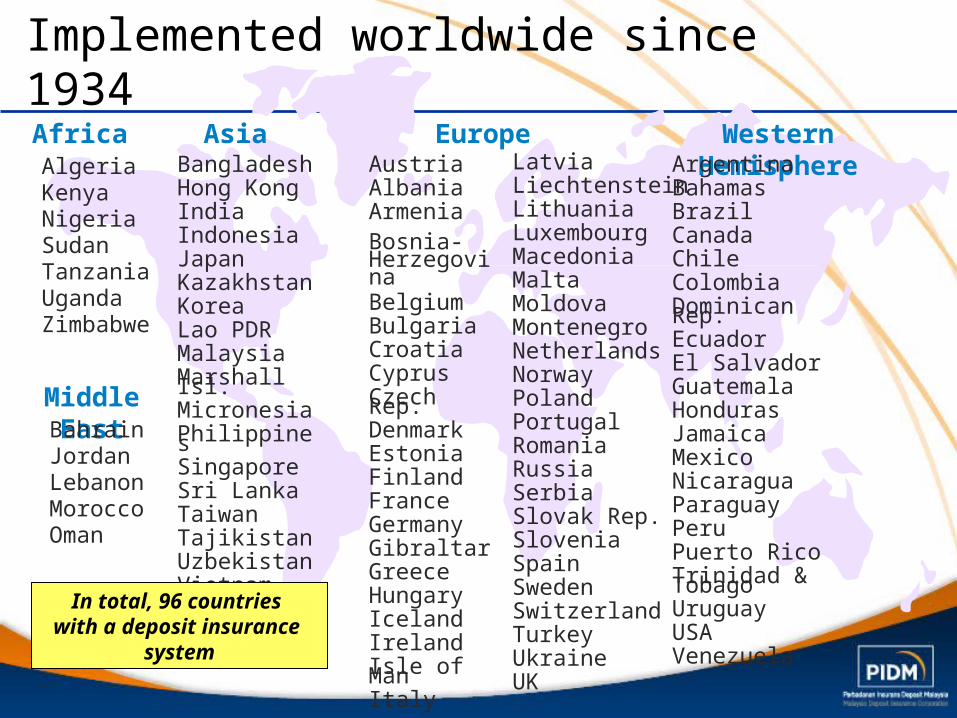

Africa Asia Europe

Middle East

Western HemisphereAlgeriaKenyaNigeriaSudanTanzaniaUgandaZimbabwe

BangladeshHong KongIndiaIndonesiaJapanKazakhstanKoreaLao PDRMalaysia Marshall Isl.MicronesiaPhilippinesSingaporeSri LankaTaiwanTajikistanUzbekistanVietnam

AustriaAlbaniaArmeniaBosnia- HerzegovinaBelgiumBulgariaCroatiaCyprusCzech Rep.DenmarkEstoniaFinlandFranceGermanyGibraltarGreeceHungaryIcelandIrelandIsle of ManItaly

LatviaLiechtensteinLithuaniaLuxembourgMacedoniaMaltaMoldovaMontenegroNetherlandsNorwayPolandPortugalRomaniaRussiaSerbiaSlovak Rep.SloveniaSpainSwedenSwitzerlandTurkeyUkraineUK

BahrainJordanLebanonMoroccoOman

ArgentinaBahamasBrazilCanadaChileColombiaDominican Rep.EcuadorEl SalvadorGuatemalaHondurasJamaicaMexicoNicaraguaParaguayPeruPuerto RicoTrinidad & TobagoUruguayUSAVenezuela

Implemented worldwide since 1934

In total, 96 countries with a deposit

insurance system

In Malaysia

In Malaysia, deposit insurance was proposed in 2001 as part of the Financial Sector Master Plan

Akta Perbadanan Insurans Deposit Malaysia 2005 (PIDM Act) enacted by Parliament in July 2005

Perbadanan Insurans Deposit Malaysia (PIDM) established to administer a deposit insurance system in Malaysia

PIDM is an operationally independent statutory body, accountable to the Parliament through the Minister of Finance

PIDM’s responsibilities

Statutory Mandate(a) Administer a deposit insurance system

under the PIDM Act;(b) Provide insurance against the loss of part

or all deposits of a member institution; (c) Provide incentives for sound risk

management in the financial system; and(d) Promote or contribute to the stability of

the financial system

In achieving objects under (b) and (d), PIDM will act in such manner as to minimise costs

tothe financial system.

PIDM’s responsibilities [cont’d]

Functions

(a) Assess and collect premiums from member institutions

(b) Manage Deposit Insurance Funds(c) Undertake resolution of non-viable

banks(d) Reimburse depositors should a member

institution fail(e) Comply with Shariah principles in

respect of Islamic deposits and funds(f) Create and enhance public awareness

on the deposit insurance system

BNM remains the primary supervisor and regulator of the financial system

PIDM complements BNM’s role in promoting financial stability

Strategic Alliance Agreement between PIDM and BNM with respect to exchange of information and collaboration

PIDM may undertake resolution on member institutions upon notification of non-viability by BNM

Role of PIDM in the financial system

Features of deposit insurance system

Dual System

PIDM administers both Islamic and conventional deposit insurance systems under a single organisation

Membership

All licensed commercial banks (22) and all licensed Islamic banks (12)

Membership is mandatory under the PIDM Act

Who are our members?

ABN Amro Bank Affin Bank Alliance Bank Malaysia * AmBank Bangkok Bank Bank of America

Malaysia Bank of China (Malaysia) Bank of Tokyo-

Mitsubishi UFJ (Malaysia)

CIMB Bank Citibank * Deutsche Bank

(Malaysia)* With Islamic

windows

EON Bank Hong Leong Bank HSBC Bank Malaysia * J. P. Morgan Chase

Bank Malayan Banking

Berhad OCBC Bank (Malaysia)

* Public Bank * RHB Bank Standard Chartered

Bank Malaysia * The Bank of Nova

Scotia United Overseas Bank

(Malaysia)

Commercial Banks

Who are our members? (cont’d)

Affin Islamic Bank Al Rajhi Bank AmIslamic Bank Asian Finance Bank Bank Islam Malaysia Bank Muamalat Malaysia CIMB Islamic Bank EONCAP Islamic Bank Hong Leong Islamic Bank Kuwait Finance House Maybank Islamic Berhad RHB Islamic Bank

Islamic Banks

Membership decal

Coverage

Automatic coverage for all depositors with RM deposits Depositors need not apply or pay

premiums Eligible deposits include Ringgit-

denominated savings and current accounts and fixed deposits

Coverage limit RM60,000 per depositor per member

institution

Separate coverage Based on legal ownership of deposit

Funding

Annual insurance premiums are paid by member institutions

PIDM administers two separate funds Islamic Deposit Insurance Fund Conventional Deposit Insurance Fund

Flat rate premium assessment – 2005 to 2007

Differential premium systems from 2008 onwards

Payment to depositors

Depositors will be promptly reimbursed on their insured deposits Based on records of member

institution

According to PIDM Act, PIDM shall reimburse depositors within 3 months from date of winding-up order

Depositors can file a claim with the bank’s liquidator for uninsured amount

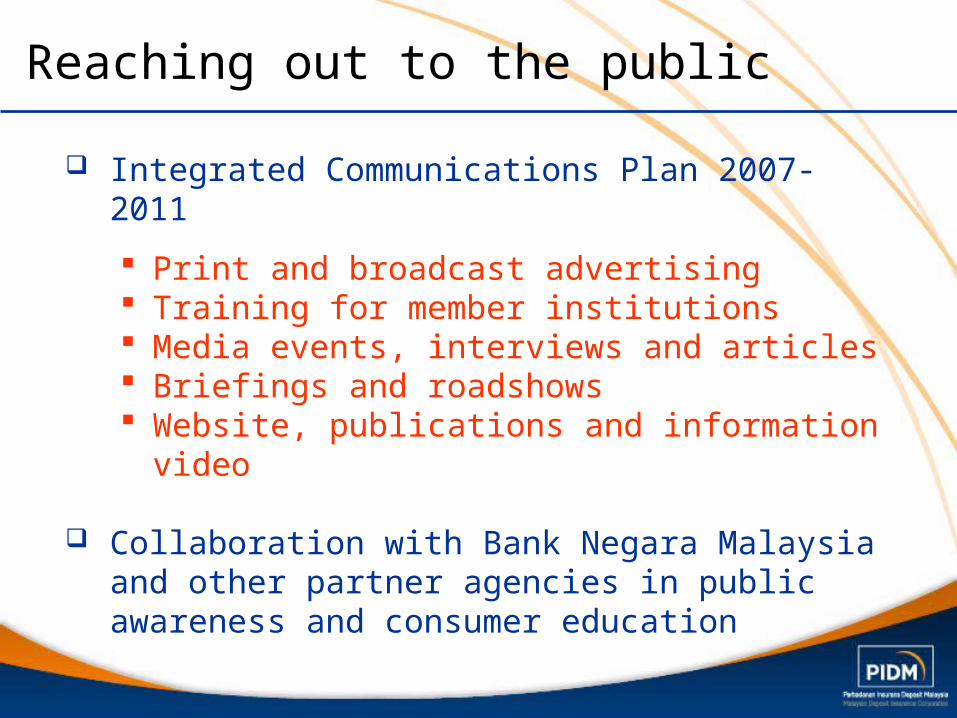

Reaching out to the public

Integrated Communications Plan 2007-2011

Print and broadcast advertising Training for member institutions Media events, interviews and articles Briefings and roadshows Website, publications and information

video

Collaboration with Bank Negara Malaysia and other partner agencies in public awareness and consumer education

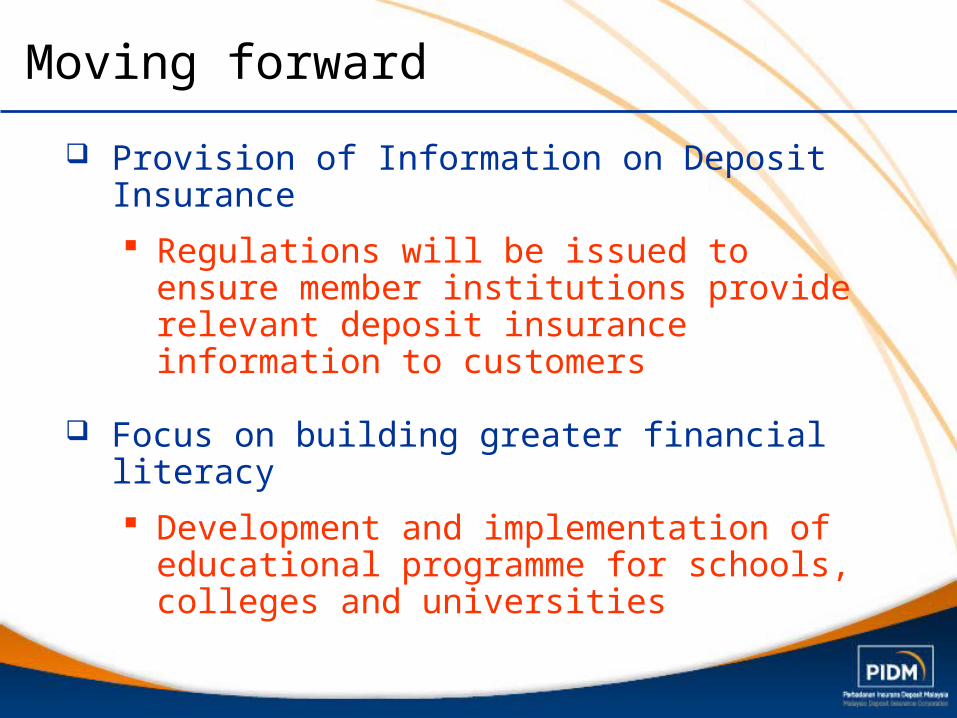

Moving forward

Provision of Information on Deposit Insurance

Regulations will be issued to ensure member institutions provide relevant deposit insurance information to customers

Focus on building greater financial literacy

Development and implementation of educational programme for schools, colleges and universities

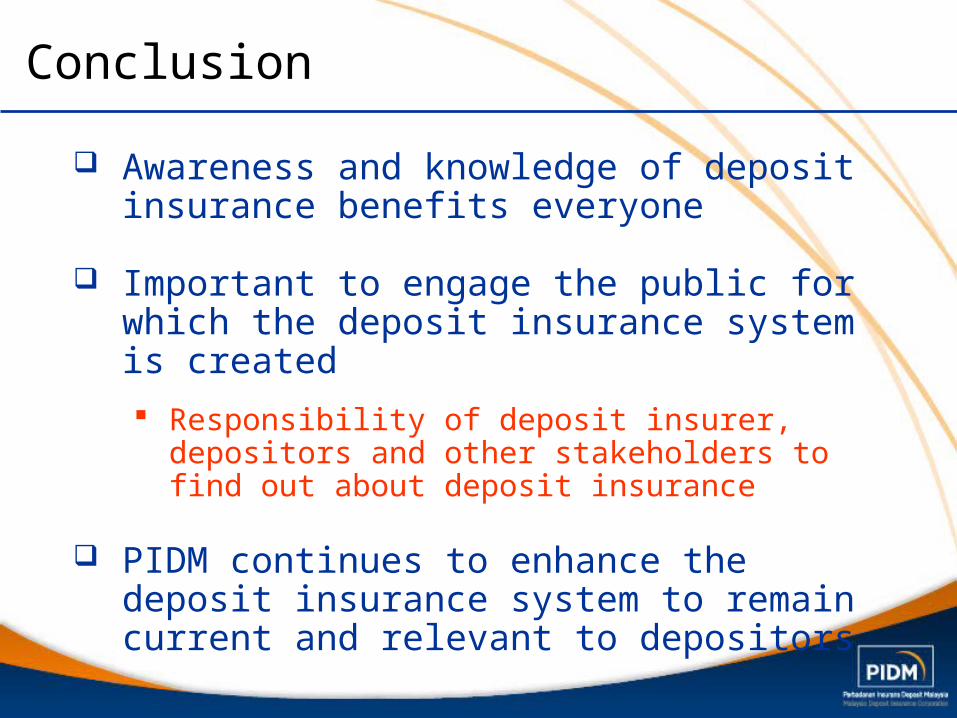

Conclusion

Awareness and knowledge of deposit insurance benefits everyone

Important to engage the public for which the deposit insurance system is created

Responsibility of deposit insurer, depositors and other stakeholders to find out about deposit insurance

PIDM continues to enhance the deposit insurance system to remain current and relevant to depositors

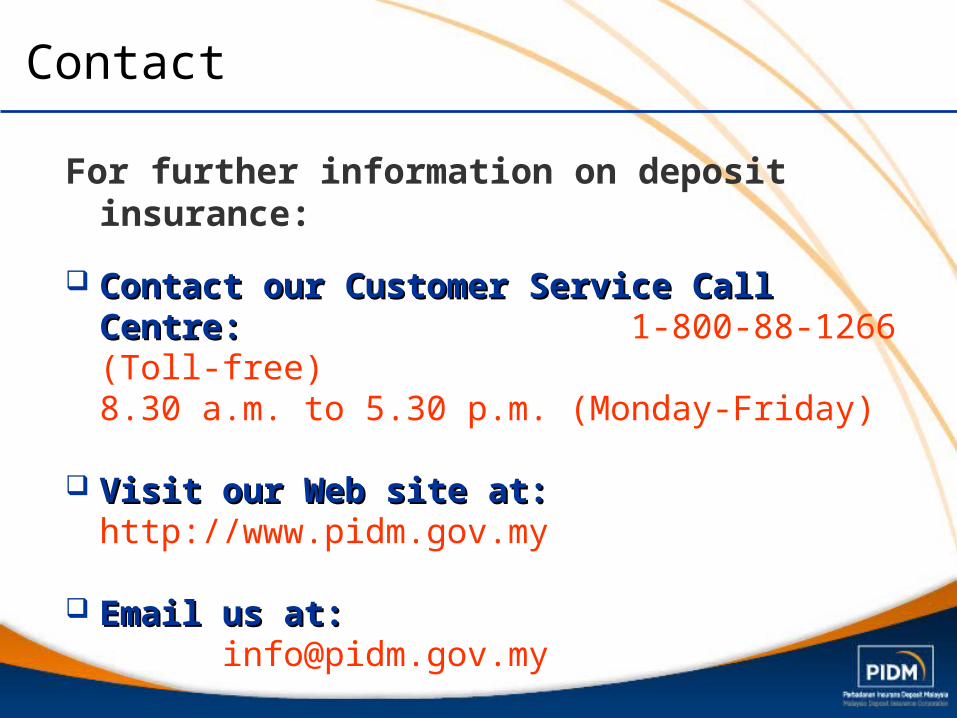

Contact

For further information on deposit insurance:

Contact our Customer Service Call Contact our Customer Service Call Centre:Centre: 1-800-88-1266 (Toll-free) 8.30 a.m. to 5.30 p.m. (Monday-Friday)

Visit our Web site at:Visit our Web site at: http://www.pidm.gov.my

Email us at:Email us at: [email protected]

© Copyright 2005 All Rights Reserved

Thank You