Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

January 11, 2016

Freight Pulse 40 Shipper Survey: Shippers' Macro Outlook Remains Relatively Unchanged

M O R G A N S T A N L E Y R E S E A R C H Morgan Stanley & Co. LLC

N O R T H A M E R I C A

Alexander Vecchio, CFA [email protected] (212) 761-6233 Ravi Shanker [email protected] (212) 761-6350 Tracy Huang [email protected] (212) 761-3373 Diane Huang [email protected] (212) 761-8290

North America Freight Transportation

In our latest shipper surveys, respondents' economic outlook remained relatively unchanged from our previous survey with sentiment continuing to trend similar to 2013 levels. Shippers continue to report high inventory levels and the % of shippers expecting to reduce inventories remains high relative to history. Volume growth expectations remain flattish for Rail and +1-2% for TL/LTL while rate growth expectations continued to decelerate across all modes. Despite ongoing improvement in Rail service reliability, shippers expect Intermodal volume growth to decelerate over the next 6 months as falling fuel prices and looser TL capacity make TL more competitive.

Freight/Macro Highlights: (1) Shippers’ Economic Outlook Remains Relatively Unchanged; (2) Automotive Shippers Most Constructive on Macro; Chemical Shippers Least Constructive; (3) Inventories Still Elevated, with % of Shippers Expecting to Reduce Inventories Still Relatively High; (4) Expectations for Capacity Tightness Continue to Decline Across All Modes ex. Barge; (5) Barge and Rail Service Levels Show the Most Sequential Improvement.

Rail Highlights: (1) Rail Volume Growth Expectations Remain at 0.5%; (2) Shippers Expect Rail Rate Growth to Decelerate in Next 6 Months; (3) More Shippers Expect Rail Spend to Remain Unchanged Though Rate Negotiations Have Become More Difficult; (4) Avg. Intermodal Discount to Truckload (Ex. Fuel) Returns to Historical Average of ~15%; (5) Rail Service Reliability Continued to Improve Sequentially in 4Q15.

Truck Highlights: (1) Intermodal Volume Growth Expectations Decelerate to the Lowest Level Since Sept 2009; (2) Rate Growth Expectations Decelerate to ~1% across All Truck Modes; (3) Shippers Expect Capacity to Loosen Across All Truck Modes; (4) Improving Rail Service a Larger Factor Driving Intermodal Growth, but Fuel Efficiency Remains Most Important; (5) More Shippers Reporting that TL Price Discounts Have Offset Some of the Rail Cost Differential.

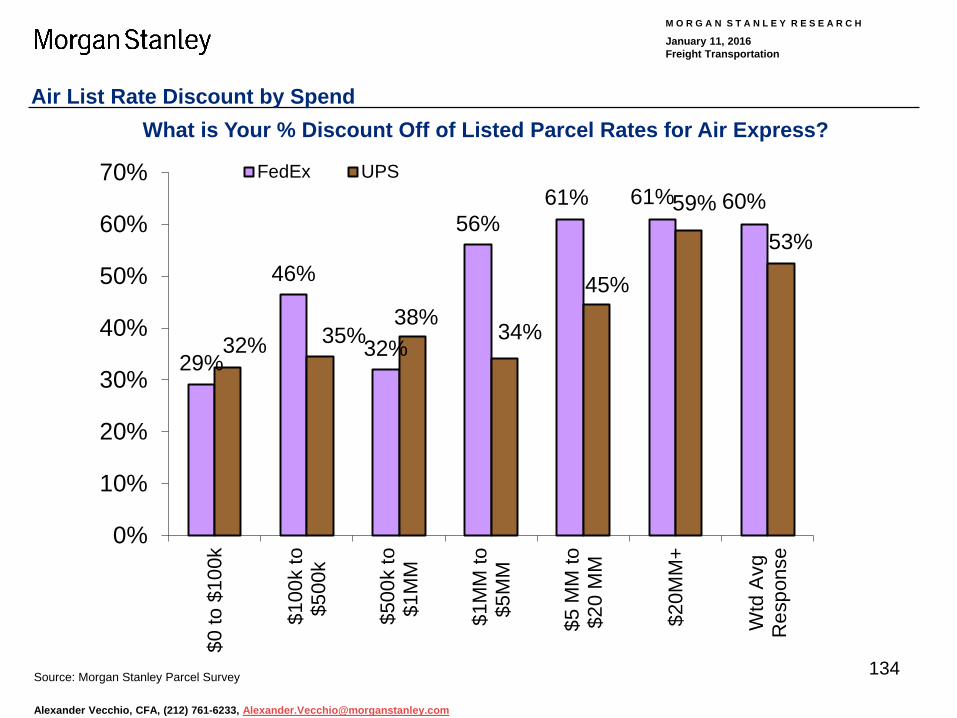

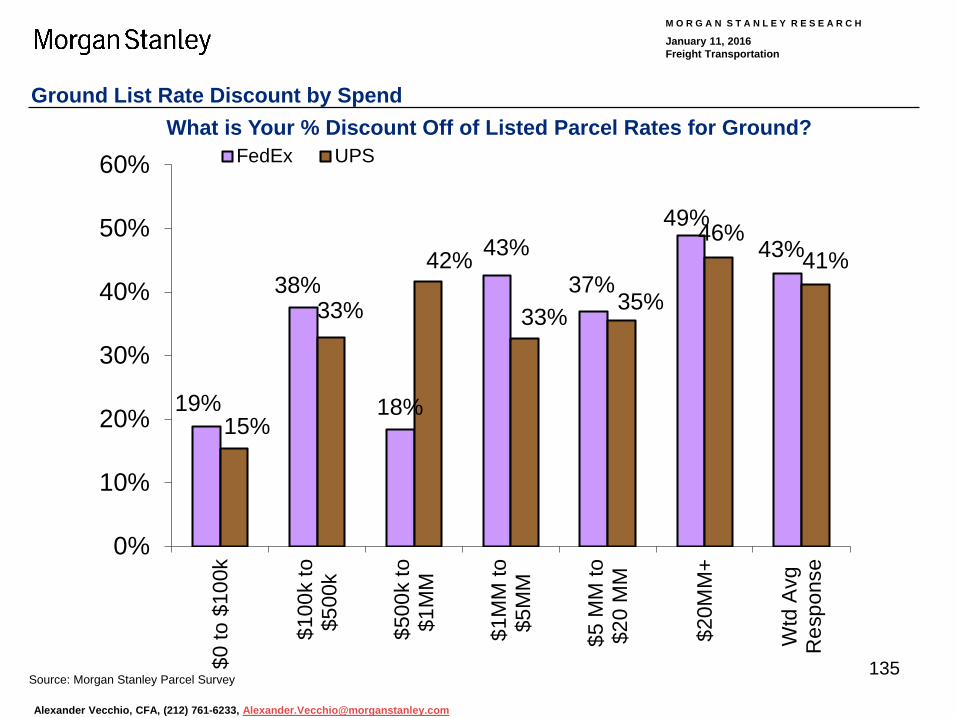

Parcel Highlights: (1) Air, International, and Ground Parcel Volume Growth Expectations Edge Lower; (2) Parcel Pricing Growth Expectations Remain in the 1-2% Range over the Next 6 Months; (3) Shippers Expect B2C as % of Total Parcel Shipment Stay Roughly Unchanged from Prior Survey Results; (4) Shippers See Parcel Carriers Becoming More Aggressive in Trying to Win Business; (5) According to Shippers, Discounts Off List Rates Increased Seq. for FDX Air & Ground.

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

2

Freight Pulse: General Freight and Macro Highlights

General Freight and Macro Highlights

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

3

Freight Pulse: General Freight and Macro Key Takeaways

1. Economic Outlook

2. Economic Outlook by Industry

Automotive Shippers Most Constructive on Macro; Chemical Shippers Least Constructive

3. Inventory & Restocking

Inventories Still Elevated, with % of Shippers Expecting to Reduce Inventories Still Relatively High

4. Capacity Expectations

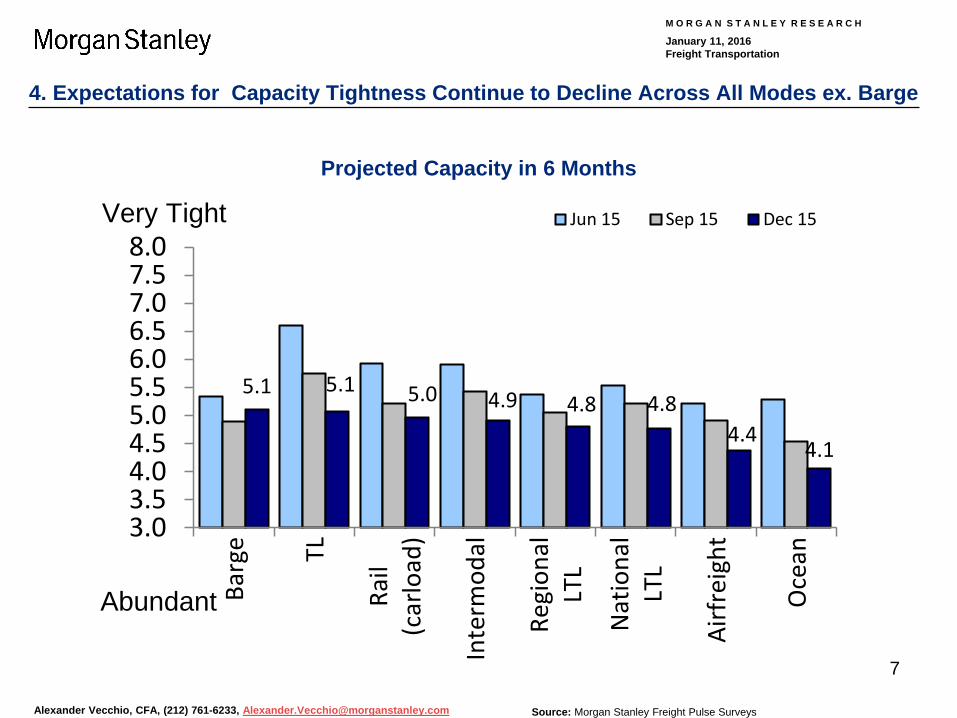

Expectations for Capacity Tightness Continue to Decline Across All Modes ex. Barge

5. Service Trends Barge and Rail Service Levels Show the Most Sequential Improvement

Shippers’ Economic Outlook Remains Relatively Unchanged

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

4

5.6

7.1

4.2

5.6

4.4

5.4

6.25.9

5.2 5.1

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0StrongEconomy

No Change

Recession

1. Shippers’ Economic Outlook Remains Relatively Unchanged

Source: Morgan Stanley Freight Pulse Surveys

State of the Economy from Shippers’ Perspective

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

5

1

2

3

4

5

6

7

8

9

10 Food and Beverage Retailing Chemical

Manufacturing Metals and Mining Automotive

StrongEconomy

No Change

Recession

Source: Morgan Stanley Freight Pulse Surveys

Shippers’ View of the Economy by Industry

2. Automotive Shippers Most Constructive on Macro; Chemical Shippers Least Constructive

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

6

Source: Morgan Stanley Freight Pulse Surveys

-70%

-50%

-30%

-10%

10%

30%

50%

70%

-50%-40%-30%-20%-10%

0%10%20%30%40%50%

Apr 0

9

Apr 1

0

Jan

11

Jun

11

Dec

11

Jun

12

Dec

12

Jun

13

Dec

13

Jun

14

Dec

14

Jun

15

Dec

15

Net O

rder

ing

/ Inv

ento

ry(%

Hig

her Y

/Y -

% L

ower

)

Net C

hg in

Ord

erin

g Le

ss N

et C

hg

in In

vent

ory

(Ordering - Inventory) (LHS)

Net Ordering (RHS)

Net Inventory (RHS)

45%44%43%43%46%43%41%41%46%46%45%36%40%41%45%49%

42%42%51%

37%35%

35%33%44%39%37%

34%45%44%37%34%39%

45%37%32%33%30%

31%39%

38%

45%43%

20%23%

13%17%17%23%

14%15%17%20%17%19%23%26%

23%21%26%

20%11%

18%22%

0%10%20%30%40%50%60%70%80%90%

100%

Jan

11A

pr 1

1Ju

n 11

Sep

11D

ec 1

1M

ar 1

2Ju

n 12

Sep

12D

ec 1

2M

ar 1

3Ju

n 13

Sep

13D

ec 1

3M

ar 1

4Ju

n 14

Sep

14D

ec 1

4M

ar 1

5Ju

n 15

Sep

15D

ec 1

5

% o

f Res

pond

ents

Increaseinventory levels

Reduce inventorylevels

Maintain currentinventory levels

Shippers' Net Y/Y Orders vs. Net Y/Y Inventory Shippers' Inventory Plans

3. Inventories Still Elevated, with % of Shippers Expecting to Reduce Inventories Still Relatively High

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

7

4. Expectations for Capacity Tightness Continue to Decline Across All Modes ex. Barge

Source: Morgan Stanley Freight Pulse Surveys

5.1 5.1 5.0 4.9 4.8 4.84.4

4.1

3.03.54.04.55.05.56.06.57.07.58.0

Barg

e TL

Rail

(car

load

)

Inte

rmod

al

Regi

onal

LTL

Nat

iona

lLT

L

Airf

reig

ht

Oce

an

Jun 15 Sep 15 Dec 15

Abundant

Very Tight

Projected Capacity in 6 Months

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

8

5. Barge and Rail Service Levels Show the Most Sequential Improvement

How would you rate service levels among different modes of transportation for the past 6 months?

Source: Morgan Stanley Freight Pulse Surveys

-0.1

0.3

0.20.0

0.4

-0.1

0.30.2

0.6

0.40.3 0.3

0.30.2

0.0 0.0

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Barge Rail(carload)

Truckload Intermodal Ocean Airfreight NationalLTL

RegionalLTL

Sequ

entia

l Poi

nt C

hang

e

Sep 15 Dec 15

Poor

Excellent

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

9

Freight Pulse: Railroad Highlights

Railroad Highlights

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

10

Freight Pulse: Rail Key Takeaways

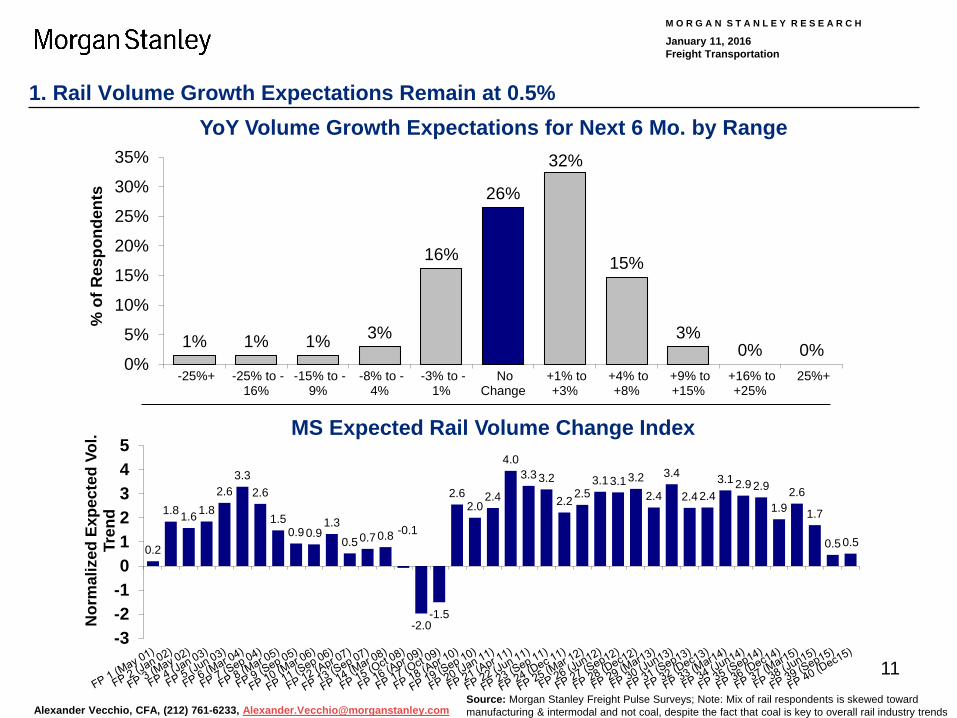

1. Rail Volume Rail Volume Growth Expectations Remain at 0.5%

2. Pricing Shippers Expect Rail Rate Growth to Decelerate in Next 6 Months

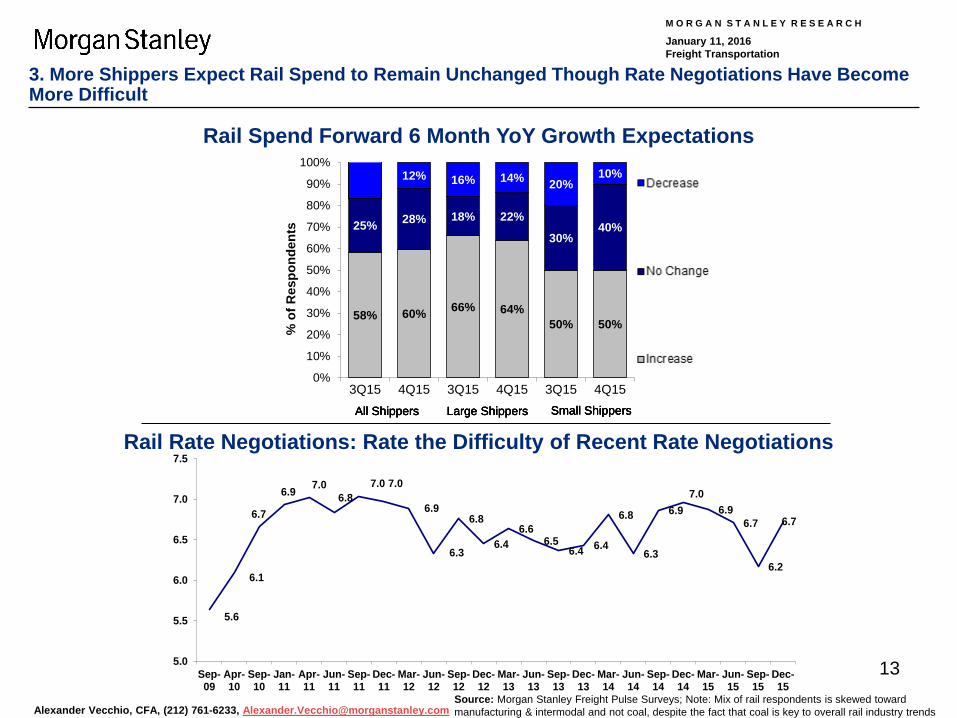

3. Spending More Shippers Expect Rail Spend to Remain Unchanged Though Rate Negotiations Have Become More Difficult

4. Intermodal Avg. Intermodal Discount to Truckload (Ex. Fuel) Returns to Historical Average of ~15%

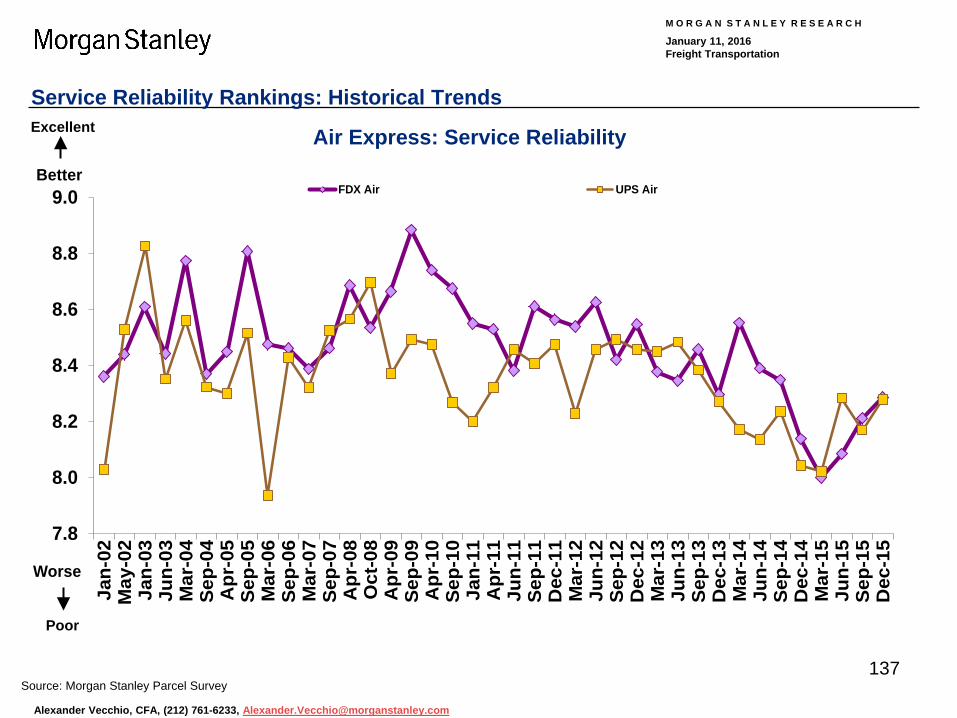

5. Service Trends Rail Service Reliability Continued to Improve Sequentially in 4Q15

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

11

1% 1% 1% 3%

16%

26%

32%

15%

3%0% 0%

0%

5%

10%

15%

20%

25%

30%

35%

-25%+ -25% to -16%

-15% to -9%

-8% to -4%

-3% to -1%

NoChange

+1% to+3%

+4% to+8%

+9% to+15%

+16% to+25%

25%+

% o

f Res

pond

ents

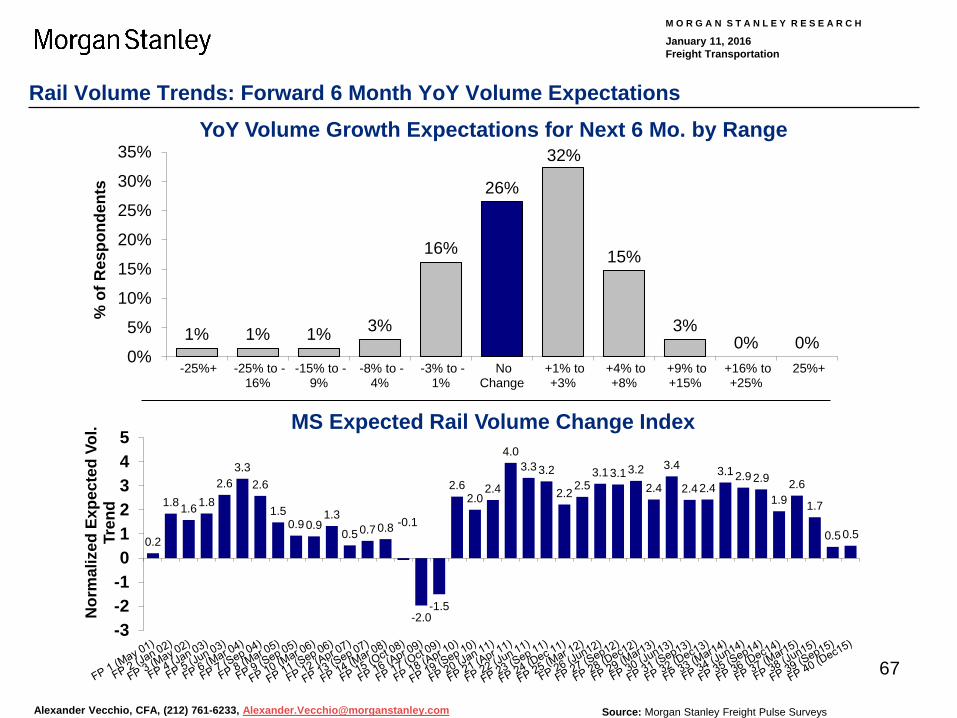

1. Rail Volume Growth Expectations Remain at 0.5%

Source: Morgan Stanley Freight Pulse Surveys; Note: Mix of rail respondents is skewed toward manufacturing & intermodal and not coal, despite the fact that coal is key to overall rail industry trends

0.2

1.8 1.6 1.82.6

3.32.6

1.50.9 0.9

1.3

0.5 0.7 0.8 -0.1

-2.0-1.5

2.62.0

2.4

4.03.3 3.2

2.2 2.53.1 3.1 3.2

2.4

3.4

2.4 2.43.1 2.9 2.9

1.92.6

1.7

0.5 0.5

-3-2-1012345

Nor

mal

ized

Exp

ecte

d Vo

l. Tr

endYoY Volume Growth Expectations for Next 6 Mo. by Range

MS Expected Rail Volume Change Index

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

12

2.9%0.0% 1.5% 0.0%

4.4%

29.4%26.5%

32.4%

1.5% 1.5% 0.0%0%

5%

10%

15%

20%

25%

30%

35%

-15%+ -15% to -11%

-10% to -6%

-5% to -3%

-2% to -1%

NoChange

+1% to+2%

+3% to+5%

+6% to+10%

+11% to+15%

15%+

% o

f Res

pond

ents

2. Shippers Expect Rail Rate Growth to Decelerate in Next 6 Months

2.7

1.9

1.0

2.21.92.6

4.4 4.4

5.6 5.9

3.53.33.5

2.72.72.6

1.2

2.53.13.1

4.33.6

3.73.5 3.6

2.52.82.62.62.42.62.42.9

2.72.73.2 3.33.4

1.71.4

01234567

Nor

mal

ized

Exp

ecte

d R

ate

Tren

dYoY Rate Growth Expectations for Next 6 Mo. by Range

MS Expected Rail Rate Change Index

Source: Morgan Stanley Freight Pulse Surveys; Note: Mix of rail respondents is skewed toward manufacturing & intermodal and not coal, despite the fact that coal is key to overall rail industry trends

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

13

Rail Spend Forward 6 Month YoY Growth Expectations

Source: Morgan Stanley Freight Pulse Surveys; Note: Mix of rail respondents is skewed toward manufacturing & intermodal and not coal, despite the fact that coal is key to overall rail industry trends

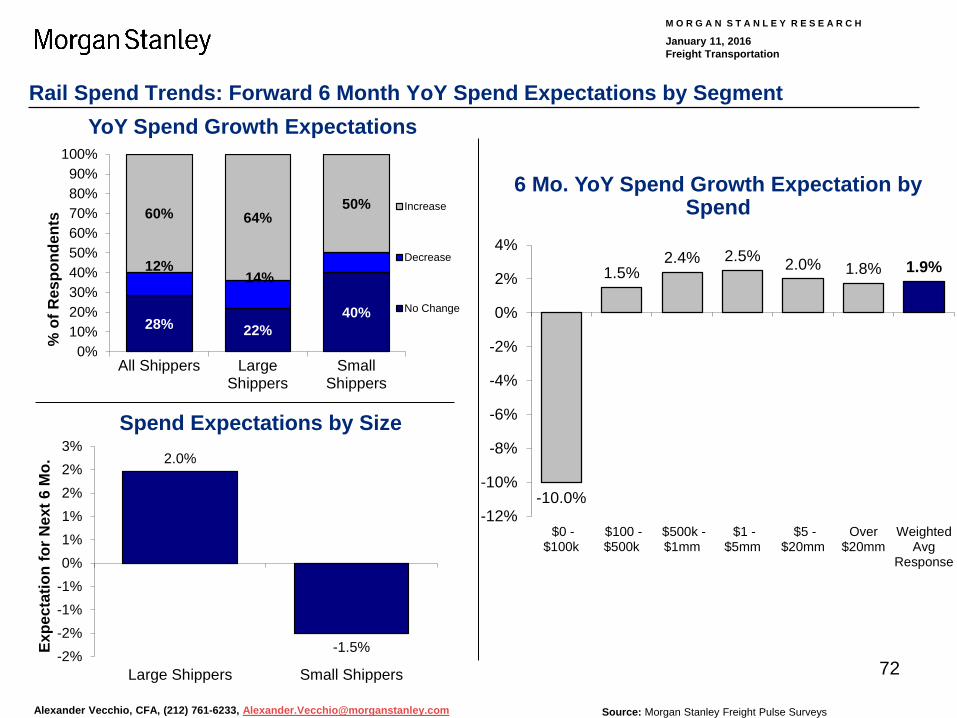

3. More Shippers Expect Rail Spend to Remain Unchanged Though Rate Negotiations Have Become More Difficult

58% 60% 66% 64%50% 50%

25% 28% 18% 22%

30%40%

12% 16% 14% 20%10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

3Q15 4Q15 3Q15 4Q15 3Q15 4Q15

% o

f Res

pond

ents

Decrease

No Change

Increase

All Shippers Large Shippers Small ShippersAll Shippers Large Shippers Small ShippersAll Shippers Large Shippers Small ShippersAll Shippers Large Shippers Small Shippers

Rail Rate Negotiations: Rate the Difficulty of Recent Rate Negotiations

5.6

6.1

6.7

6.9 7.0 6.8

7.0 7.0

6.9

6.3

6.8

6.4 6.6

6.5 6.4 6.4

6.8

6.3

6.9 7.0

6.9 6.7

6.2

6.7

5.0

5.5

6.0

6.5

7.0

7.5

Sep-09

Apr-10

Sep-10

Jan-11

Apr-11

Jun-11

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Dec-13

Mar-14

Jun-14

Sep-14

Dec-14

Mar-15

Jun-15

Sep-15

Dec-15

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

14

Source: Morgan Stanley Freight Pulse Surveys

12%

13%

14%

15%

16%

17%

18%

19%

20%S

ep 0

6

Sep

07

Oct

08

Sep

09

Sep

10

Ap

r 11

Sep

11

Mar

12

Sep

12

Mar

13

Sep

13

Mar

14

Sep

14

Mar

15

Sep

15

Ave

rag

e In

term

od

al %

Dis

cou

nt

vs. T

L

Discount Excluding Fuel Historical Average (ex. Fuel)

What discount is being offered in the marketplace for intermodal services when compared to TL services in a similar lane?

4. Avg. Intermodal Discount to Truckload (Ex. Fuel) Returns to Historical Average of ~15%

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

15

5. Rail Service Reliability Continued to Improve Sequentially in 4Q15

5.76.25.96.05.75.45.45.25.15.55.35.65.56.16.16.16.25.96.06.06.26.26.26.16.36.26.76.66.56.56.15.76.05.85.95.85.76.16.2

02468

10Value for Dollar (Scale 1 = Worst to 10 = Best)

6.16.16.56.46.15.95.45.65.85.96.15.76.36.26.66.96.36.15.85.55.65.85.65.86.05.95.96.26.66.06.35.75.05.25.35.24.95.55.76.1

02468

10Service Reliability (Scale 1 = Worst to 10 = Best)

Source: Morgan Stanley Freight Pulse Surveys; Note: Mix of rail respondents is skewed toward manufacturing & intermodal and not coal, despite the fact that coal is key to overall rail industry trends

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

16

Freight Pulse: Trucking Highlights

Trucking Highlights

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

17

Freight Pulse: Trucking Key Takeaways

1. Truck Volume

2. Pricing Rate Growth Expectations Decelerate to ~1% across All Truck Modes

3. Capacity Shippers Expect Capacity to Loosen Across All Truck Modes

4. Intermodal Use Improving Rail Service a Larger Factor Driving Intermodal Growth, but Fuel Efficiency Remains Most Important

5. Intermodal Cost More Shippers Reporting that TL Price Discounts Have Offset Some of the Rail Cost Differential

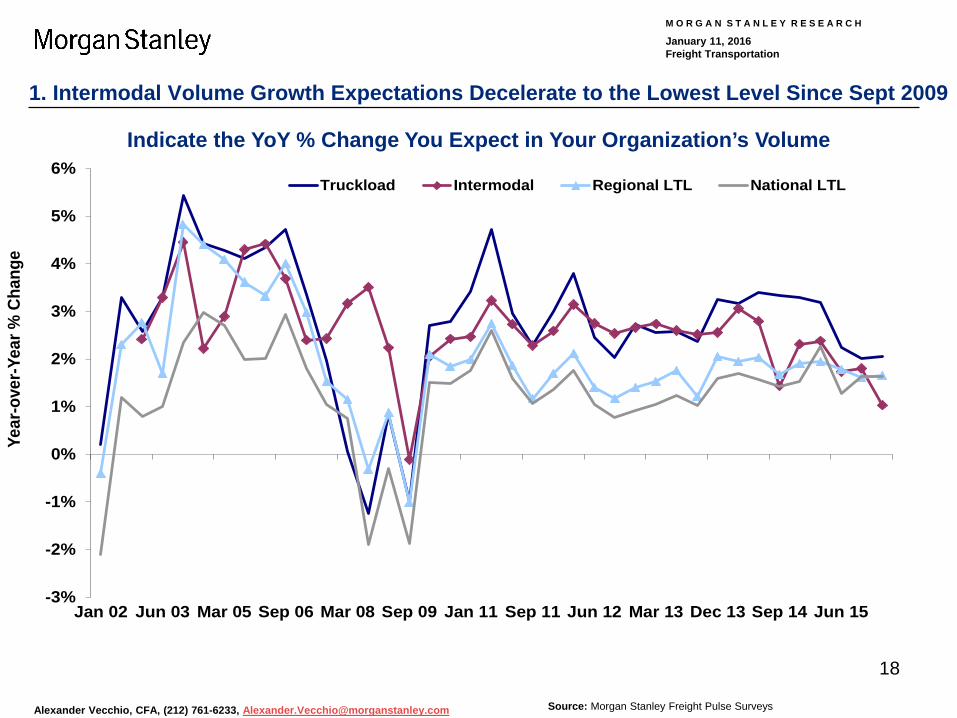

Intermodal Volume Growth Expectations Decelerate to the Lowest Level Since Sept 2009

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

18

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

Jan 02 Jun 03 Mar 05 Sep 06 Mar 08 Sep 09 Jan 11 Sep 11 Jun 12 Mar 13 Dec 13 Sep 14 Jun 15

Year

-ove

r-Yea

r % C

hang

e

Truckload Intermodal Regional LTL National LTL

1. Intermodal Volume Growth Expectations Decelerate to the Lowest Level Since Sept 2009

Source: Morgan Stanley Freight Pulse Surveys

Indicate the YoY % Change You Expect in Your Organization’s Volume

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

19

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

Jan 02 Jun 03 Mar 05 Sep 06 Mar 08 Sep 09 Jan 11 Sep 11 Jun 12 Mar 13 Dec 13 Sep 14 Jun 15

Year

-ove

r-Yea

r % C

hang

e

Truckload Intermodal Regional LTL National LTL

Source: Morgan Stanley Freight Pulse Surveys

2. Rate Growth Expectations Decelerate to ~1% across All Truck Modes

Indicate the YoY % Change You Expect in Your Organization’s Base Rates

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

20

7.5

6.6

5.6 5.6

7.2

6.25.6 5.6

6.6

5.95.5 5.4

5.85.4 5.2 5.15.1

4.9 4.8 4.8

1

2

3

4

5

6

7

8

9

10

Truckload Intermodal National LTL Regional LTL

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Abundant

Balanced

Very Tight

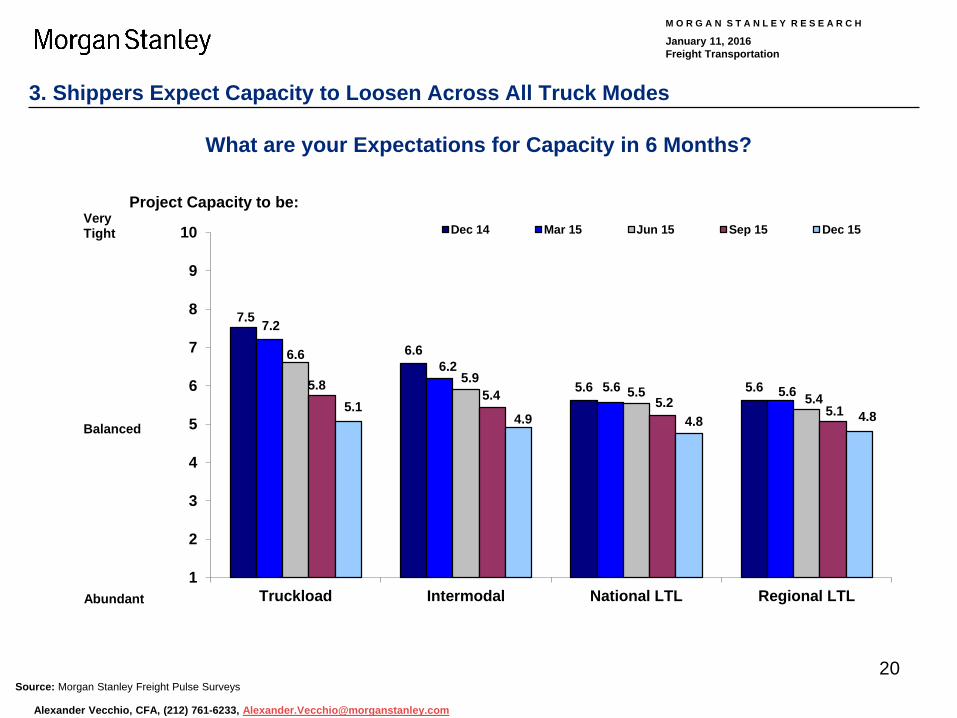

Project Capacity to be:

3. Shippers Expect Capacity to Loosen Across All Truck Modes

Source: Morgan Stanley Freight Pulse Surveys

What are your Expectations for Capacity in 6 Months?

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

21

6.9 6.77.1

6.76.3 6.3

5.7 5.96.6 6.9 7.0 6.7 6.6

6.3 6.1 6.1

7.4 7.3 7.2 7.0 6.96.4 6.2

5.8

1

2

3

4

5

6

7

8

9

10

Barge Truckload RegionalLTL

Intermodal Ocean National LTL Rail(carload)

Airfreight

Jun 15 Sep 15 Dec 15

Poor

Excellent

4. Improving Rail Service a Larger Factor Driving Intermodal Growth, but Fuel Efficiency Remains Most Important

Source: Morgan Stanley Freight Pulse Survey

6.3 6.85.6

5.0 4.6 4.5

6.1 6.6

5.3 5.24.4 4.1

5.56.3

5.4 5.24.4 4.2

5.56.4

5.05.7

4.5 4.1

123456789

10

TL Rates HaveRisen to Point

Where IntermodalIs Competitive

Intermodal is morefuel efficient

Turning to theIntermodal

Alternative MoreOften During

Periods of TightCapacity

RailroadIntermodal Service

Has Improved

Strong ImportGrowth

Strong ExportGrowth

FP 37 (Mar15) FP 38 (Jun15) FP 39 (Sep15) FP 40 (Dec15)

What Factors are Impacting Your Use of Intermodal Most?

“Value for the Dollar” for Each Mode

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

22

5. More Shippers Reporting that TL Price Discounts Have Offset Some of the Rail Cost Differential

Source: Morgan Stanley Freight Pulse Surveys

1 2 3 4 5 6 7 8 9

10

Oct

08

Apr 0

9Se

p 09

Apr 1

0Se

p 10

Jan

11Ap

r 11

Jun

11Se

p 11

Dec

11

Mar

12

Jun

12Se

p 12

Dec

12

Mar

13

Jun

13Se

p 13

Dec

13

Mar

14

Jun

14Se

p 14

Dec

14

Mar

15

Jun

15Se

p 15

Dec

15

Rail doesn't support faster inventory turnoverTL price discounts have offset some of the rail cost differentialOther Factors

StronglyAgree

StronglyDisagree

What Factors are Limiting your Organization from Shipping More Volume on the Railroads?

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

23

Freight Pulse: Parcel Highlights

Parcel Highlights

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

24

Freight Pulse: Parcel Key Takeaways

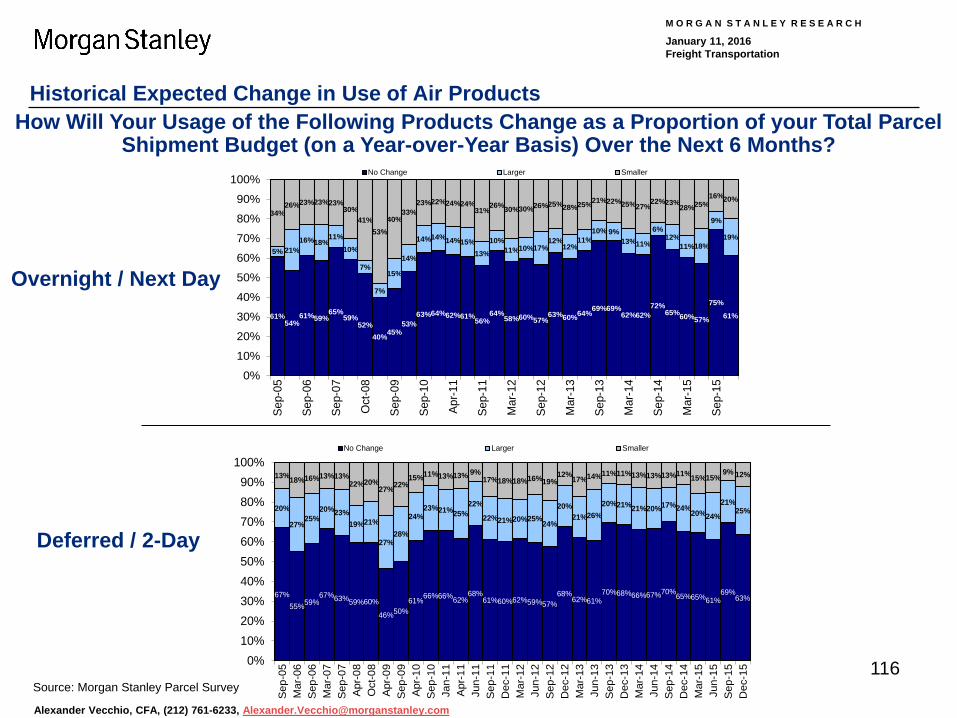

1. Parcel Volumes Air, International, and Ground Parcel Volume Growth Expectations Edge Lower

2. Pricing Parcel Pricing Growth Expectations Remain in the 1-2% Range over the Next 6 Months

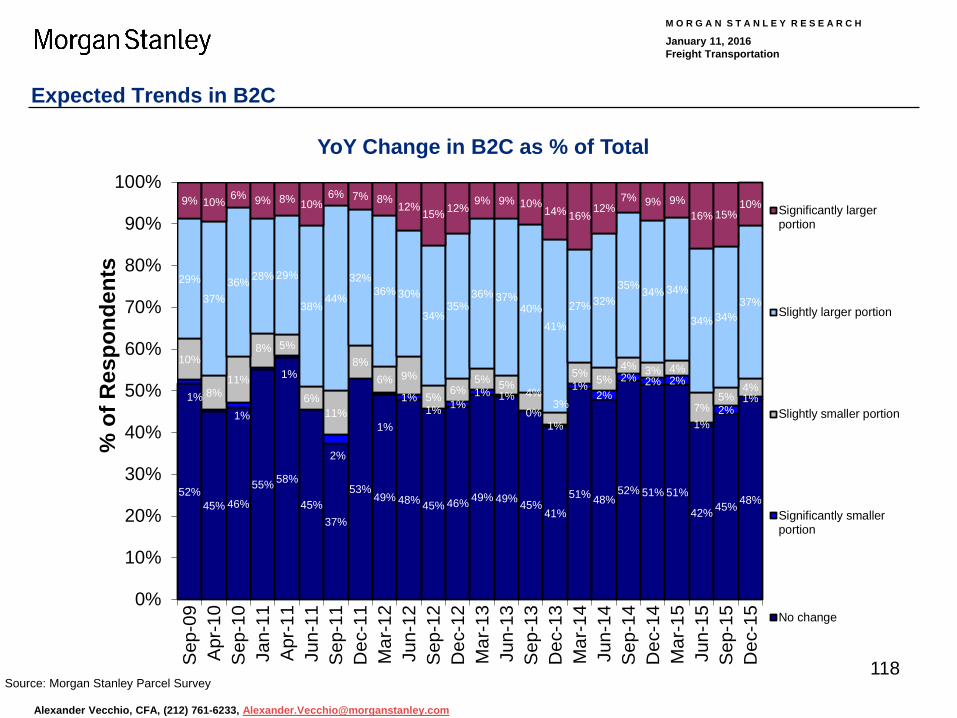

3. B2C Shippers Expect B2C as % of Total Parcel Shipment Stay Roughly Unchanged from Prior Survey Results

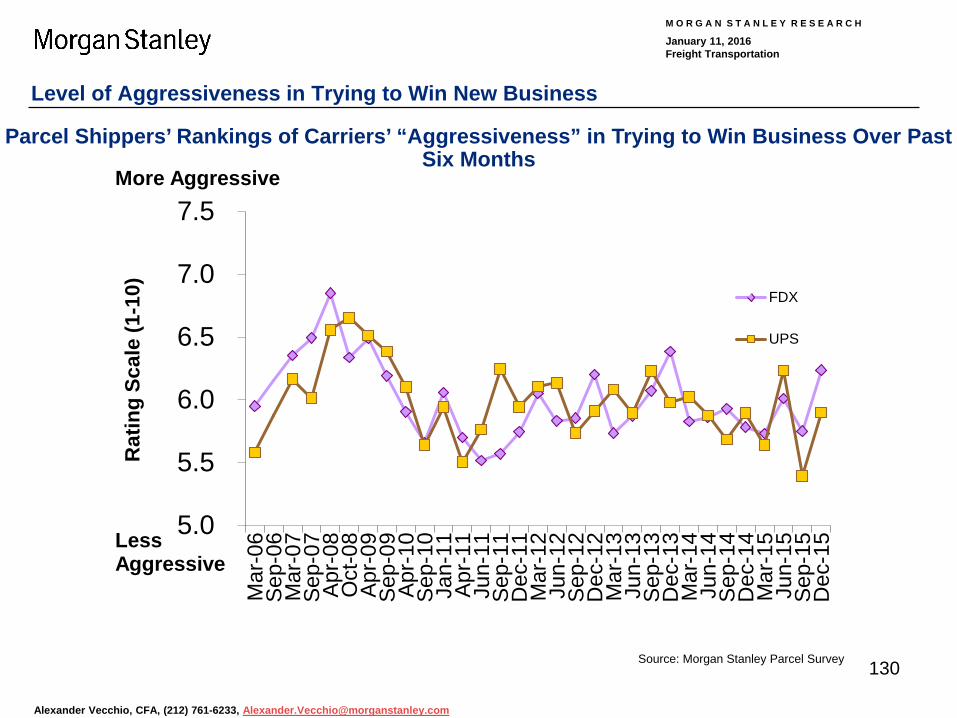

4. Aggressiveness Shippers See Parcel Carriers Becoming More Aggressive in Trying to Win Business

5. Rate Discounts According to Shippers, Discounts Off List Rates Increased Seq. for FDX Air & Ground

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

25

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

Jan-

02M

ay-0

2Ja

n-03

Jun-

03M

ar-0

4S

ep-0

4A

pr-0

5S

ep-0

5M

ar-0

6S

ep-0

6M

ar-0

7S

ep-0

7A

pr-0

8O

ct-0

8A

pr-0

9S

ep-0

9A

pr-1

0S

ep-1

0Ja

n-11

Apr

-11

Jun-

11S

ep-1

1D

ec-1

1M

ar-1

2Ju

n-12

Sep

-12

Dec

-12

Mar

-13

Jun-

13S

ep-1

3D

ec-1

3M

ar-1

4Ju

n-14

Sep

-14

Dec

-14

Mar

-15

Jun-

15S

ep-1

5D

ec-1

5

Air Ground Int'l

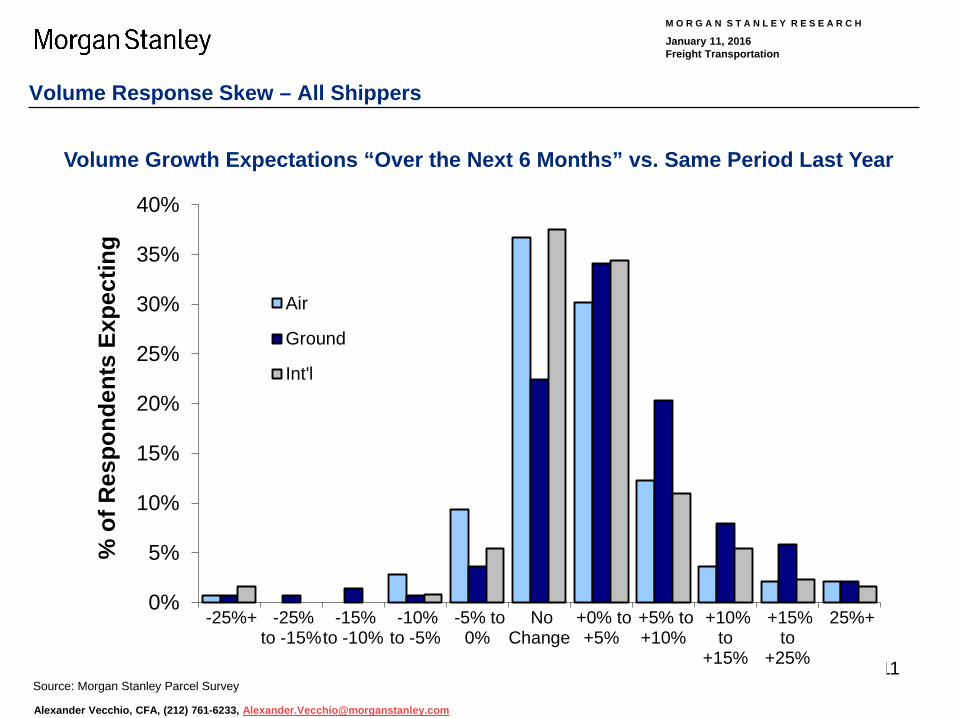

1. Air, International, and Ground Parcel Volume Growth Expectations Edge Lower

Source: Morgan Stanley Parcel Survey

Volume Growth Expectations “Over the Next 6 Months” vs. Last Year

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

26

2. Parcel Pricing Growth Expectations Remain in the 1-2% Range over the Next 6 Months

-0.5%0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%4.5%

Jan-

02M

ay-0

2Ja

n-03

Jun-

03M

ar-0

4S

ep-0

4A

pr-0

5S

ep-0

5M

ar-0

6S

ep-0

6M

ar-0

7S

ep-0

7A

pr-0

8O

ct-0

8A

pr-0

9S

ep-0

9A

pr-1

0S

ep-1

0Ja

n-11

Apr

-11

Jun-

11S

ep-1

1D

ec-1

1M

ar-1

2Ju

n-12

Sep

-12

Dec

-12

Mar

-13

Jun-

13S

ep-1

3D

ec-1

3M

ar-1

4Ju

n-14

Sep

-14

Dec

-14

Mar

-15

Jun-

15S

ep-1

5D

ec-1

5

Air Ground Int'l

Includes All responses, equally-weighted. Source: Morgan Stanley Parcel Survey

Average Base Rate Expectations “Over the Next 6 Months” vs. Last Year

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

27 Source: Morgan Stanley Parcel Survey

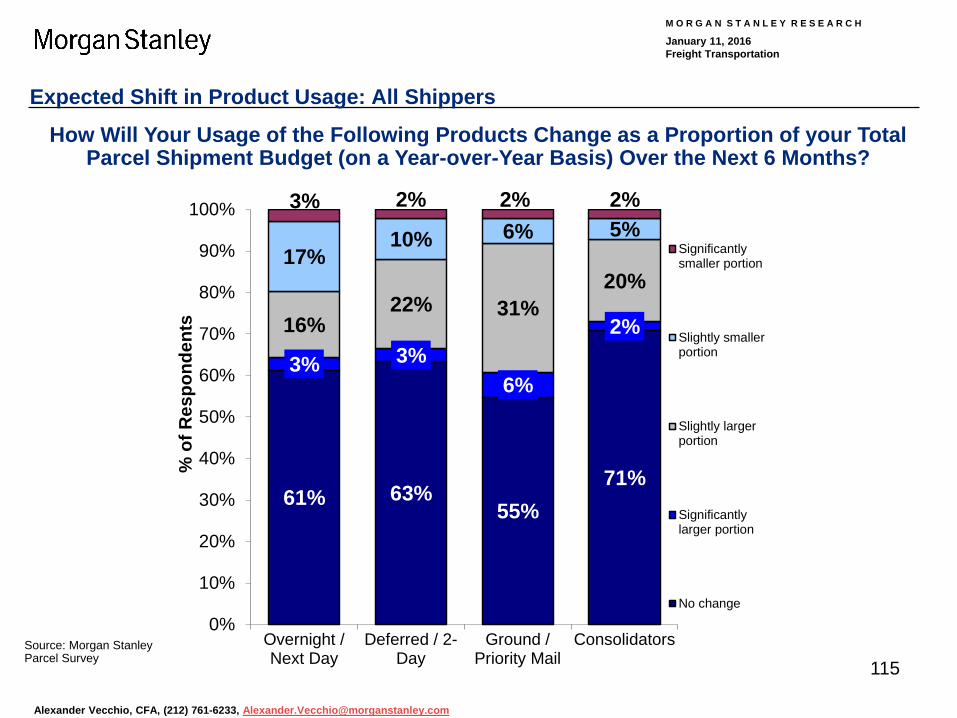

3. Shippers Expect B2C as % of Total Parcel Shipment Stay Roughly Unchanged from Prior Survey Results

YoY Change in B2C as % of Total

52%45% 46%

55% 58%

45%37%

53%49% 48% 45% 46% 49% 49% 45%

41%

51% 48%52% 51% 51%

42% 45% 48%

1%1%

1%

2%

1%

1%1% 1%

1% 1%0%

1%

1%2%

2% 2% 2%

1%2%

1%

10%

8%11%

8% 5%

6%11%

8%6% 9%

5% 6%5% 5%

4%3%

5% 5%4% 3% 4%

7%5%

4%

29%

37%36% 28% 29%

38%44%

32%36% 30%

34%35%

36% 37%40%

41%

27% 32%35% 34% 34%

34% 34%37%

9% 10% 6% 9% 8% 10%6% 7% 8%

12%15% 12%

9% 9% 10%14% 16%

12%7% 9% 9%

16% 15%10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Se

p-09

Apr-1

0Se

p-10

Jan-

11Ap

r-11

Jun-

11Se

p-11

Dec

-11

Mar

-12

Jun-

12Se

p-12

Dec

-12

Mar

-13

Jun-

13Se

p-13

Dec

-13

Mar

-14

Jun-

14Se

p-14

Dec

-14

Mar

-15

Jun-

15Se

p-15

Dec

-15

% o

f Res

pond

ents

Significantly largerportion

Slightly larger portion

Slightly smaller portion

Significantly smallerportion

No change

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

28

5.0

5.5

6.0

6.5

7.0

7.5M

ar-0

6Se

p-06

Mar

-07

Sep-

07Ap

r-08

Oct

-08

Apr-0

9Se

p-09

Apr-1

0Se

p-10

Jan-

11Ap

r-11

Jun-

11Se

p-11

Dec

-11

Mar

-12

Jun-

12Se

p-12

Dec

-12

Mar

-13

Jun-

13Se

p-13

Dec

-13

Mar

-14

Jun-

14Se

p-14

Dec

-14

Mar

-15

Jun-

15Se

p-15

Dec

-15

FDX

UPS

More Aggressive

LessAggressive

Rat

ing

Scal

e (1

-10)

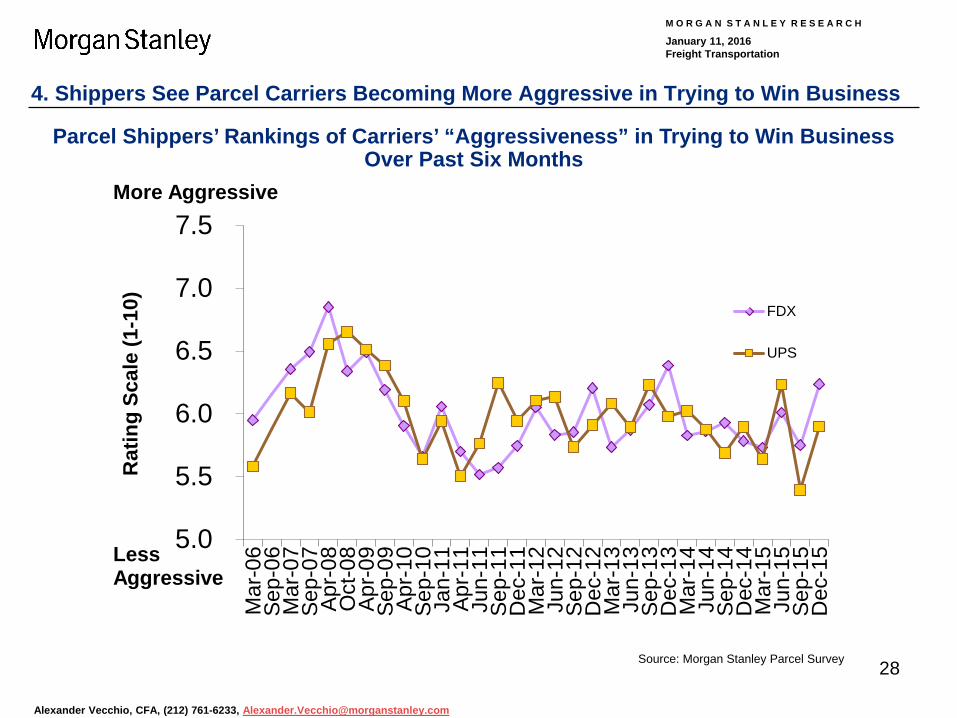

4. Shippers See Parcel Carriers Becoming More Aggressive in Trying to Win Business

Source: Morgan Stanley Parcel Survey

Parcel Shippers’ Rankings of Carriers’ “Aggressiveness” in Trying to Win Business Over Past Six Months

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

29 Source: Morgan Stanley Parcel Survey

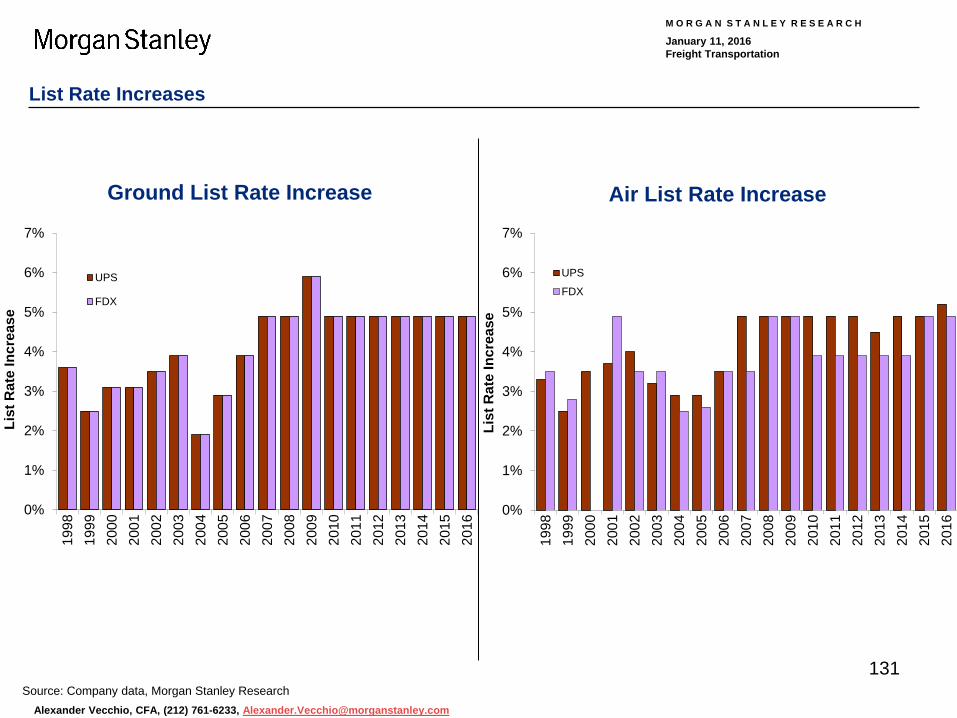

5. According to Shippers, Discounts Off List Rates Increased Seq. for FDX Air & Ground

Average List Rate Discount

15%

20%

25%

30%

35%

40%

45%

50%

55%

Apr

-05

Mar

-06

Mar

-07

Apr

-08

Apr

-09

Apr

-10

Jan-

11

Jun-

11

Dec

-11

Jun-

12

Dec

-12

Jun-

13

Dec

-13

Jun-

14

Dec

-14

Jun-

15

Dec

-15

Dis

coun

t Off

List

Rat

esFDX Ground UPS Ground FDX Air UPS Air

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

30

Appendix

Appendix

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

31

About the Surveys Part 1: About the Surveys

1. General Freight 2. Rail Industry 3. Truck Industry 4. Parcel Industry

Summary of Contents

General Freight Trends

Rail Trends

Truck Trends

Parcel Trends

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

32

General Freight: About the Freight Pulse Survey

Note: just those shippers providing an industry classification and spend. Source: MS Freight Pulse Surveys

20% 19%18%

15%

7%5%

3% 2% 2% 2% 2% 2% 2% 1% 1% 0%0%

10%

20%

30%3P

L

Oth

er In

dust

ry

Man

ufac

turin

g

Food

and

Bev

erag

e

Ret

ailin

g

Che

mic

al

Pape

r & P

acka

ging

Com

pute

r / T

ech

Auto

mot

ive

Fore

st /

Build

ing

Prod

ucts Min

ing

Fina

ncia

l / L

egal

Serv

ices

Phar

mac

eutic

al

Indu

s Eq

uip

/ Cap

Goo

ds

Agric

ultu

re

Elec

trica

l Gen

erat

ion

Respondents by Industry

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

33

General Freight: Segmented by Shipper Profile

Note: just those shippers providing an industry classification and spend. Source: MS Freight Pulse Surveys

Trucking, 63%

Railroads (including

Intermodal), 3%

Both Trucking

and Railroads (including

Intermodal), 34%

< $100k, 14.8%

$100k to $500k, 4.6%

$500k to $1MM, 1.5% $1MM to

$5MM, 12.8%

$5 MM to $40 MM, 56.6%

$40MM+, 9.7%

Modes Used Respondents’ Total Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

34

Rails: Segmented by Industry and Shipper Profile

$0 -$100k, 7%

$100 -$500k, 3%

$500k -$1mm, 8%

$1 -$5mm, 13%

$5 -$20mm,

30%

Over $20mm,

39%

Source: Morgan Stanley Freight Pulse Surveys

Rail Respondents by Industry Respondents’ Rail Spend

20% 19%

14%13%

6% 6%4% 3% 3% 3%

2% 2% 2% 1% 1% 1%0%

5%

10%

15%

20%

25%

Oth

er In

dust

ry

3PL

Man

ufac

turin

g

Food

and

Bev

erag

e

Che

mic

al

Ret

ailin

g

Pap

er &

Pac

kagi

ng

Min

ing

Aut

omot

ive

Com

pute

r/Tec

hnol

ogy

Indu

stria

lE

quip

men

t/Cap

ital…

Fina

ncia

l/Leg

alS

ervi

ces

Fore

st/B

uild

ing

Pro

duct

s

Agr

icul

ture

Pha

rmac

eutic

al

Ele

ctric

al G

ener

atio

n

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

35

Trucks: Segmented by Industry and Shipper Profile

Source: Morgan Stanley Freight Pulse Surveys

21%19%19%

15%

7%4% 3% 2% 2% 2% 2% 1% 1% 1% 1% 0%

0%

10%

20%

30%

3PL

Oth

er In

dust

ry

Man

ufac

turin

g

Food

and

Bev

erag

e

Ret

ailin

g

Che

mic

al

Pap

er &

Pac

kagi

ng

Com

pute

r / T

ech

Aut

omot

ive

Fore

st /

Build

ing…

Pha

rmac

eutic

al

Min

ing

Indu

s E

quip

/ C

ap…

Fina

ncia

l / L

egal

…

Agr

icul

ture

Ele

ctric

al G

ener

atio

n

< $100k, 11%

$100k to $500k, 5%

$500k to $1MM, 3%

$1MM to $5MM, 14%

$5 MM to $20 MM,

18%

$20MM+, 50%

Truck Respondents by Industry Respondents’ Truck Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

36

Parcel: About Our Parcel Survey

$0 to $100k, 23%

$100k to $500k, 11%

$500k to $1MM, 8%$1MM to

$5MM, 21%

$5 MM to $20 MM,

17%

$20MM+, 19%

31%

20%

13% 13% 12% 12%

0%

10%

20%

30%

40%

Man

ufac

turin

g

Who

lesa

le /

Dis

tribu

tion

Oth

er

Ret

ail

3PL

Prov

ider

Con

sulta

nt

Source: Morgan Stanley Parcel Survey

Respondents' Parcel Spend Respondents' Primary Business

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

37

Parcel: Respondent Profile

$0 to $10, 19%

$11 - $25, 10%

$26 -$50, 5%

$51 -$100, 16%

$100 -$1,000,

14%

$1,000+, 35%

0 - 100k, 43%

100k -500k, 23%

500k -1MM, 7%

1MM -5MM, 13% 5MM+,

15%

Source: Morgan Stanley Parcel Survey

Company Sales ($MM) Parcels Shipped

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

38

UPS, 49%UPS, 58%

UPS, 33%

FDX, 47% FDX, 33%

FDX, 32%

USPS, 5%

USPS, 1%

DHL, 0%

DHL, 31%

Other, 1% Other, 3% Other, 4%

0%

20%

40%

60%

80%

100%

Air Ground Int'l

Dol

lar-

wei

ghte

d %

of r

espo

nden

ts

Parcel: Market Share of Respondents Roughly Consistent with Market

Source: Morgan Stanley Parcel Survey

UPS, 41% UPS, 48%

UPS, 29%

50% 40%

36%

USPS, 4% USPS, 9%

USPS, 8%

DHL, 1%

DHL, 15%

Other, 3% Other, 3%

Other, 8%

0%

20%

40%

60%

80%

100%

Air Ground Int'l

% o

f res

pond

ents

Primary Parcel Carrier – Weighted by Spend Parcel Carrier – Average of All Responses

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

39

Summary of Contents

Part 1: General Freight Industry Trends 1. Service Trends 2. Capacity Trends 3. Modal Shift 4. Intermodal vs. Truck

Part 2: Macro Trends 1. Inventories and Orders 2. Economic Outlook

About the Surveys

General Freight Trends

Rail Trends

Truck Trends

Parcel Trends

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

40

7.6 7.4 7.06.6

6.3 6.3 5.9 5.5

7.5 7.67.2 6.9

6.3 6.3 6.3 5.7

7.8 7.6 7.56.9 6.9 6.7 6.5

6.1

0

1

2

3

4

5

6

7

8

9

10

Airfreight Regional LTL Truckload National LTL Barge Intermodal Ocean Rail (carload)

Jun 15 Sep 15 Dec 15

Poor

Excellent

Service Reliability & Value by Mode: Average Across All Shippers

Source: Morgan Stanley Freight Pulse Surveys

“Service Reliability” for Each Mode

6.9 6.77.1

6.76.3 6.3

5.7 5.96.6 6.9 7.0 6.7 6.6

6.3 6.1 6.1

7.4 7.3 7.2 7.0 6.96.4 6.2

5.8

1

2

3

4

5

6

7

8

9

10

Barge Truckload RegionalLTL

Intermodal Ocean NationalLTL

Rail(carload)

Airfreight

Jun 15 Sep 15 Dec 15

Poor

Excellent “Value for the Dollar” for Each Mode

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

41

Capacity by Mode

Source: Morgan Stanley Freight Pulse Surveys

Current Capacity Projected Capacity in 6 Months

5.1 5.1 5.0 4.9 4.8 4.8 4.4 4.1

123456789

10

Barg

e TL

Rail

(car

load

)

Inte

rmod

al

Regi

onal

LTL

Nat

iona

lLT

L

Airf

reig

ht

Oce

an

Abundant

Very Tight

4.9 4.8 4.7 4.6 4.5 4.5 4.3 3.9

123456789

10

Barg

e

Rail

(car

load

)

Inte

rmod

al

Regi

onal

LTL

Nat

iona

lLT

L TL

Airf

reig

ht

Oce

an

Abundant

Very Tight

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

42

12%

5%

15%13%

41%

4%6%

2% 2% 1%0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1 2 3 4 5 6 7 8 9 10

Airfreight - % of Shippers Providing Rankings

Abundant Very Tight

Capacity Ranking Skew: Airfreight

Source: Morgan Stanley Freight Pulse Surveys

11%

4%

13% 11%

46%

4% 4% 2% 1% 2%0%

10%

20%

30%

40%

50%

60%

1 2 3 4 5 6 7 8 9 10

Airfreight - % of Shippers Providing Rankings

Abundant Very Tight

Current Capacity Projected Capacity in 6 Months

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

43

Capacity Ranking Skew: Ocean

15%

9%

20%

16%

25%

6%

2%

6%

1% 0%0%

5%

10%

15%

20%

25%

30%

1 2 3 4 5 6 7 8 9 10

Ocean - % of Shippers Providing Rankings

Abundant Very Tight

Source: Morgan Stanley Freight Pulse Surveys

10% 10%

22%

14%

28%

2%6% 7%

0% 1%0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1 2 3 4 5 6 7 8 9 10

Ocean - % of Shippers Providing Rankings

Abundant Very Tight

Current Capacity Projected Capacity in 6 Months

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

44

2%5%

15% 15%

43%

6% 5%7%

1% 1%0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1 2 3 4 5 6 7 8 9 10

Rail (carload) - % of Shippers Providing Rankings

Abundant Very Tight

Capacity Ranking Skew: Rail (Carload)

Source: Morgan Stanley Freight Pulse Surveys

1%4%

13%15%

41%

10%8%

4% 3% 1%0%

10%

20%

30%

40%

50%

60%

1 2 3 4 5 6 7 8 9 10

Rail (carload) - % of Shippers Providing Rankings

Abundant Very Tight

Current Capacity Projected Capacity in 6 Months

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

45

Capacity Ranking Skew: Barge

7%3%

10%7%

55%

3% 3% 3% 3% 3%

0%

10%

20%

30%

40%

50%

60%

70%

1 2 3 4 5 6 7 8 9 10

Barge - % of Shippers Providing Rankings

Abundant Very Tight

Source: Morgan Stanley Freight Pulse Surveys

0%3%

14%10%

48%

3%

14%

3%0%

3%

0%

10%

20%

30%

40%

50%

60%

70%

1 2 3 4 5 6 7 8 9 10

Barge - % of Shippers Providing Rankings

Abundant Very Tight

Current Capacity Projected Capacity in 6 Months

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

46

Shipper Modal Shift Statistics – Truckload to Rail

54%

42%

4%

58%

39%

3%

61%

36%

3%

61%

37%

3%

69%

30%

1%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

Truckload to Rail

92% 89%100%

75%66%

44%60%

8% 11%0%

25%33%

56%39%

1% 1%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to$4

0 M

M

$40

MM

+

Wei

ghte

dAv

gR

espo

nse

% o

f Res

pond

ents

Yes, shiftinga significantamount ofvolume

Yes, shiftingsome volume

No

Truckload to Rail - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

47

Shipper Modal Shift Statistics – Rail to Truckload

82%

15%

2%

83%

16%

1%

77%

22%

1%

78%

21%

1%

80%

18%

2%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

Rail to Truckload

96% 89%100%

83% 80%

44%

71%

4% 0%19%

50%

26%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to$4

0 M

M

$40

MM

+

Wei

ghte

dAv

gR

espo

nse

% o

f Res

pond

ents

Yes, shiftinga significantamount ofvolume

Yes, shiftingsome volume

No

Rail to Truckload - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

48

Shipper Modal Shift Statistics – Airfreight to LTL

85%

13%

1%

90%

9%1%

86%

13%

1%

86%

13%

1%

84%

14%

1%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

Airfreight to LTL

88%

56%67%

92% 86% 88% 87%

44%

8% 12% 13% 12%

0% 2% 1%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to$4

0 M

M

$40

MM

+

Wei

ghte

dAv

gR

espo

nse

% o

f Res

pond

ents

Yes, shifting asignificantamount ofvolume

Yes, shiftingsome volume

No

Airfreight to LTL - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

49

Shipper Modal Shift Statistics – LTL to Airfreight

97%

3% 0%

96%

3% 1%

97%

3% 0%

97%

3% 0%

96%

4%0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

LTL to Airfreight

92%78%

100% 96% 99% 94% 98%

22%

1% 2%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to$4

0 M

M

$40

MM

+

Wei

ghte

dAv

gR

espo

nse

% o

f Res

pond

ents

Yes, shifting asignificantamount ofvolume

Yes, shiftingsome volume

No

LTL to Airfreight - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

50

Shipper Modal Shift Statistics – Truckload to LTL

80%

20%

0%

78%

20%

1%

83%

17%

0%

84%

15%

0%

85%

14%

2%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

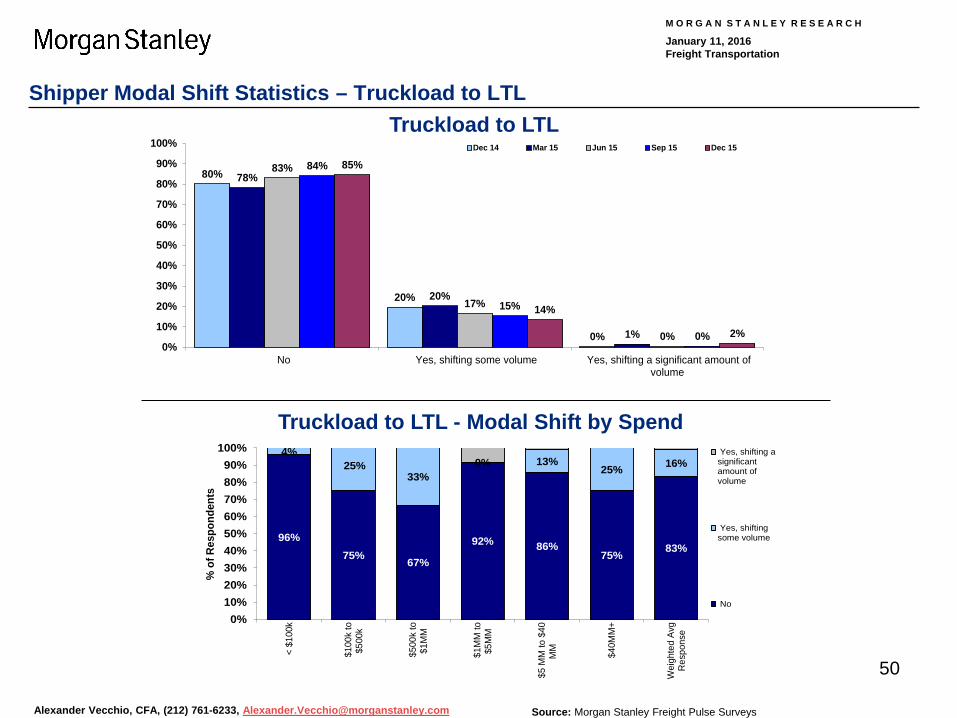

Truckload to LTL

96%75% 67%

92% 86%75% 83%

4%25%

33%0% 13%

25% 16%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to $

40M

M

$40

MM

+

Wei

ghte

d Av

gR

espo

nse

% o

f Res

pond

ents

Yes, shifting asignificantamount ofvolume

Yes, shiftingsome volume

No

Truckload to LTL - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

51

Shipper Modal Shift Statistics – LTL to Truckload

61%

35%

4%

65%

33%

2%

63%

35%

2%

63%

34%

2%

64%

33%

4%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

LTL to Truckload

88%75%

67% 71%61%

44%58%

12%25% 29%

36%

44%37%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to$4

0 M

M

$40

MM

+

Wei

ghte

dAv

gR

espo

nse

% o

f Res

pond

ents

Yes, shifting asignificantamount ofvolume

Yes, shiftingsome volume

No

LTL to Truckload - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

52

Shipper Modal Shift Statistics – Ocean to Rail

99%

1% 0%

98%

1% 0%

96%

4% 0%

97%

3% 0%

96%

4%0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

Ocean to Rail

96% 100% 100%88%

99%88%

96%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to$4

0 M

M

$40

MM

+

Wei

ghte

dAv

gR

espo

nse

% o

f Res

pond

ents

Yes, shifting asignificantamount ofvolume

Yes, shiftingsome volume

No

Ocean to Rail - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

53

Shipper Modal Shift Statistics – Rail to Ocean

97%

2% 1%

97%

3% 0%

97%

3% 0%

97%

3% 0%

97%

3% 0%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

Rail to Ocean

96% 100% 100%91%

100%88%

97%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to$4

0 M

M

$40

MM

+

Wei

ghte

dAv

gR

espo

nse

% o

f Res

pond

ents

Yes, shifting asignificantamount ofvolume

Yes, shiftingsome volume

No

Rail to Ocean - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

54

Shipper Modal Shift Statistics – Airfreight to Ocean

88%

11%

1%

91%

8%1%

86%

13%

1%

90%

9%1%

86%

11%3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

Airfreight to Ocean

88%

63% 67%88% 87% 94% 88%

8% 11% 10%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to$4

0 M

M

$40

MM

+

Wei

ghte

dAv

gR

espo

nse

% o

f Res

pond

ents

Yes, shifting asignificantamount ofvolume

Yes, shiftingsome volume

No

Airfreight to Ocean - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

55

Shipper Modal Shift Statistics – Ocean to Airfreight

92%

7%1%

90%

9%2%

94%

5%1%

94%

6%0%

94%

6%0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

Ocean to Airfreight

96% 100%

33%

88%97% 94% 96%

0% 3% 4%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to$4

0 M

M

$40

MM

+

Wei

ghte

dAv

gR

espo

nse

% o

f Res

pond

ents

Yes, shifting asignificantamount ofvolume

Yes, shiftingsome volume

No

Ocean to Airfreight - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

56

Shipper Modal Shift Statistics – Barge to Rail

99%

1% 0%

98%

2% 0%

97%

3% 0%

98%

2% 0%

98%

2% 0%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

Barge to Rail

100%89%

100% 100% 97% 100% 98%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to$4

0 M

M

$40

MM

+

Wei

ghte

dAv

gR

espo

nse

% o

f Res

pond

ents

Yes, shifting asignificantamount ofvolume

Yes, shiftingsome volume

No

Barge to Rail - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

57

Shipper Modal Shift Statistics – Rail to Barge

93%

7%0%

95%

5%0%

94%

6%0%

98%

2% 0%

96%

3% 1%0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No Yes, shifting some volume Yes, shifting a significant amount ofvolume

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Source: Morgan Stanley Freight Pulse Surveys

Rail to Barge

96% 100% 100% 96% 98% 94% 97%

6% 3%

0%10%20%30%40%50%60%70%80%90%

100%

< $

100k

$10

0k to

$500

k

$50

0k to

$1M

M

$1M

M to

$5M

M

$5

MM

to $

40M

M

$40

MM

+

Wei

ghte

d Av

gR

espo

nse

% o

f Res

pond

ents

Yes, shifting asignificantamount ofvolume

Yes, shiftingsome volume

No

Rail to Barge - Modal Shift by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

58

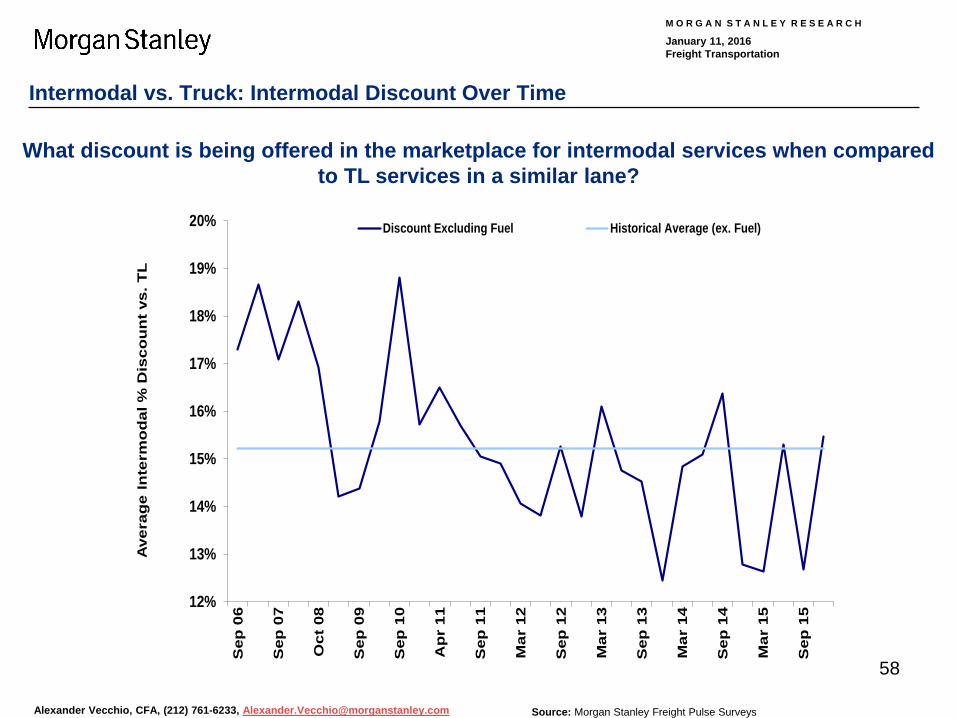

Intermodal vs. Truck: Intermodal Discount Over Time

Source: Morgan Stanley Freight Pulse Surveys

12%

13%

14%

15%

16%

17%

18%

19%

20%S

ep 0

6

Sep

07

Oct

08

Sep

09

Sep

10

Ap

r 11

Sep

11

Mar

12

Sep

12

Mar

13

Sep

13

Mar

14

Sep

14

Mar

15

Sep

15

Ave

rag

e In

term

od

al %

Dis

cou

nt

vs. T

L

Discount Excluding Fuel Historical Average (ex. Fuel)

What discount is being offered in the marketplace for intermodal services when compared to TL services in a similar lane?

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

59

Summary of Contents

Part 1: General Freight Industry Trends 1. Service Trends 2. Capacity Trends 3. Modal Shift 4. Intermodal vs. Truck

Part 2: Macro Trends 1. Inventories and Orders 2. Economic Outlook

About the Surveys

General Freight Trends

Rail Trends

Truck Trends

Parcel Trends

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

60

Shipper Inventory and Stocking Trends

Source: Morgan Stanley Freight Pulse Surveys

38%33%

30%28%

44%

28%

0%5%

10%15%20%25%30%35%40%45%50%

Higher Same Lower

% o

f Res

pond

ents

Inventory Ordering

Shipper Inventories and Orders Relative to Last Year

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

61

17%10%

41%46%42%47%36%

22%31%

45%

28%33%28%31%34%36%33%39%42%45%40%36%28%25%28%

36%

22%

31%34%43%37%

39%

43%

45%

39%

43%36%47%45%44%38%51%43%41%39%46%

45%48%

47%44%

47%

68%

28%20%15%16%

25%35%

24%16%

29%31%25%24%22%26%

16%18%17%16%15%19%25%28%28%

0%10%20%30%40%50%60%70%80%90%

100%

% o

f Res

pond

ents

Higher Same Lower

43% 41% 41% 46% 46% 45%36% 40% 41% 45% 49% 42% 42%

51%37% 35%

34%45% 44% 37% 34% 39%

45% 37% 32% 33% 30%31% 39%

38%

45% 43%

23%14% 15% 17% 20% 17% 19% 23% 26% 23% 21% 26% 20%

11% 18% 22%

0%10%20%30%40%50%60%70%80%90%

100%

% o

f Res

pond

ents

Maintain current inventory levels Reduce inventory levels Increase inventory levels

Shipper Inventory and Stocking Trends

Source: Morgan Stanley Freight Pulse Surveys

Y/Y Change in Shippers' Inventory Y/Y Change in Shippers' Orders

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

62

Assessing Restocking Potential: Net Inventory Trends and Inventory Plans

Source: Morgan Stanley Freight Pulse Surveys

-70%

-50%

-30%

-10%

10%

30%

50%

70%

-50%-40%-30%-20%-10%

0%10%20%30%40%50%

Apr 0

9

Apr 1

0

Jan

11

Jun

11

Dec

11

Jun

12

Dec

12

Jun

13

Dec

13

Jun

14

Dec

14

Jun

15

Dec

15

Net O

rder

ing

/ Inv

ento

ry(%

Hig

her Y

/Y -

% L

ower

)

Net C

hg in

Ord

erin

g Le

ss N

et C

hg

in In

vent

ory

(Ordering - Inventory) (LHS)

Net Ordering (RHS)

Net Inventory (RHS)

45%44%43%43%46%43%41%41%46%46%45%36%40%41%45%49%

42%42%51%

37%35%

35%33%44%39%37%

34%45%44%37%34%39%

45%37%32%33%30%

31%39%

38%

45%43%

20%23%

13%17%17%23%

14%15%17%20%17%19%23%26%

23%21%26%

20%11%

18%22%

0%10%20%30%40%50%60%70%80%90%

100%

Jan

11A

pr 1

1Ju

n 11

Sep

11D

ec 1

1M

ar 1

2Ju

n 12

Sep

12D

ec 1

2M

ar 1

3Ju

n 13

Sep

13D

ec 1

3M

ar 1

4Ju

n 14

Sep

14D

ec 1

4M

ar 1

5Ju

n 15

Sep

15D

ec 1

5

% o

f Res

pond

ents

Increaseinventory levels

Reduce inventorylevels

Maintain currentinventory levels

Shippers' Net Y/Y Orders vs. Net Y/Y Inventory Shippers' Inventory Plans

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

63

5.6

7.1

4.2

5.6

4.4

5.4

6.25.9

5.2 5.1

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0StrongEconomy

No Change

Recession

Economic Outlook: Average Across All Shippers

State of the Economy from Shippers’ Perspective

Source: Morgan Stanley Freight Pulse Surveys

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

64

10.0

7.7

6.0 5.7 5.7 5.4 5.3 5.2 5.1 5.0 4.7 4.5 4.5 4.3

123456789

1011

Agric

ultu

re

Fina

ncia

l / L

egal

Serv

ices

Fore

st /

Build

ing…

Auto

mot

ive

Phar

mac

eutic

al

Reta

iling 3P

L

Oth

er In

dust

ry

Man

ufac

turin

g

Food

and

Beve

rage

Min

ing

Indu

s Eq

uip

/Ca

p G

oods

Pape

r &Pa

ckag

ing

Com

pute

r /Te

ch

Strong Economy

No Change

Recession

Economic Outlook: Granular View by Spend and Shipper Industry

Source: Morgan Stanley Freight Pulse Surveys

State of Economy - All Shippers

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

65

1

2

3

4

5

6

7

8

9

10 Food and Beverage Retailing Chemical

Manufacturing Metals and Mining Automotive

StrongEconomy

No Change

Recession

Economic Outlook: View by Industry Over Time

Shippers’ Historical View of the Economy by Industry Segment

Source: Morgan Stanley Freight Pulse Surveys

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

66

Summary of Contents

Part 1: Key Rail Trends 1. Volume Trends 2. Rate Trends 3. Spend Trends 4. Pricing Trends 5. Service Trends

Part 2: Special Topics 1. Intermodal 2. Rate Mitigation Efforts 3. Rail Competition 4. Rate Negotiations 5. Rate Cases 6. Support for Legislation

About the Surveys

General Freight Trends

Rail Trends

Truck Trends

Parcel Trends

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

67

Rail Volume Trends: Forward 6 Month YoY Volume Expectations

1% 1% 1% 3%

16%

26%

32%

15%

3%0% 0%

0%

5%

10%

15%

20%

25%

30%

35%

-25%+ -25% to -16%

-15% to -9%

-8% to -4%

-3% to -1%

NoChange

+1% to+3%

+4% to+8%

+9% to+15%

+16% to+25%

25%+

% o

f Res

pond

ents

0.2

1.8 1.6 1.82.6

3.32.6

1.50.9 0.9

1.3

0.5 0.7 0.8 -0.1

-2.0-1.5

2.62.0

2.4

4.03.3 3.2

2.2 2.53.1 3.1 3.2

2.4

3.4

2.4 2.43.1 2.9 2.9

1.92.6

1.7

0.5 0.5

-3-2-1012345

Nor

mal

ized

Exp

ecte

d Vo

l. Tr

end

Source: Morgan Stanley Freight Pulse Surveys

YoY Volume Growth Expectations for Next 6 Mo. by Range

MS Expected Rail Volume Change Index

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

68

YoY Volume Growth Expectations

Rail Volume Trends: Forward 6 Month YoY Volume Expectations by Segment

26% 22% 30%

24% 26%30%

50% 52%40%

0%10%20%30%40%50%60%70%80%90%

100%

All Shippers LargeShippers

SmallShippers

% o

f Res

pond

ents

Increase

Decrease

No Change

0.8%

-2.8%-3.5%-3.0%-2.5%-2.0%-1.5%-1.0%-0.5%0.0%0.5%1.0%1.5%

Large Shippers Small Shippers

Expe

ctat

ions

for N

ext 6

Mo.

-6.3%

1.0%

-1.6%

2.0%

0.8% 0.5% 0.6%

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

$0 -$100k

$100 -$500k

$500k -$1mm

$1 -$5mm

$5 -$20mm

Over$20mm

WeightedAvg

Response

Source: Morgan Stanley Freight Pulse Surveys

YoY Volume Growth Expectations 6 Mo. YoY Volume Growth Expectation by

Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

69

Rail Rate Trends: Forward 6 Month YoY Rate Expectations

2.9%0.0% 1.5% 0.0%

4.4%

29.4%26.5%

32.4%

1.5% 1.5% 0.0%0%

5%

10%

15%

20%

25%

30%

35%

-15%+ -15% to -11%

-10% to -6%

-5% to -3%

-2% to -1%

NoChange

+1% to+2%

+3% to+5%

+6% to+10%

+11% to+15%

15%+

% o

f Res

pond

ents

2.7

1.9

1.0

2.21.92.6

4.4 4.4

5.6 5.9

3.53.33.5

2.72.72.6

1.2

2.53.13.1

4.33.6

3.73.5 3.6

2.52.82.62.62.42.62.42.9

2.72.73.2 3.33.4

1.71.4

01234567

Nor

mal

ized

Exp

ecte

d R

ate

Tren

d

Source: Morgan Stanley Freight Pulse Surveys

YoY Rate Growth Expectations for Next 6 Mo. by Range

MS Expected Rate Change Index

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

70

Rail Rate Trends: Forward 6 Month YoY Rate Expectations by Segment

29% 22%40%

9%8%

10%

62% 70%50%

0%10%20%30%40%50%60%70%80%90%

100%

All Shippers LargeShippers

SmallShippers

% o

f Res

pond

ents

Increase

Decrease

No Change

2.0%

-0.5%-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Large Shippers Small Shippers

Expe

ctat

ions

for N

ext 6

Mo.

-4.5%

0.0%

1.7%2.4%

2.0% 1.8% 1.9%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

$0 -$100k

$100 -$500k

$500k -$1mm

$1 -$5mm

$5 -$20mm

Over$20mm

WeightedAvg

Response

Source: Morgan Stanley Freight Pulse Surveys

6 Mo. YoY Rate Growth Expectation by Spend

YoY Rate Growth Expectations

YoY Rate Growth Expectations

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

71

Rail Spend Trends: Forward 6 Month YoY Spend Expectations

3%0% 0% 1%

7%

28%

40%

18%

1% 0% 0%

-5%

5%

15%

25%

35%

45%

55%

(30%)+ (30) to(21%)

(20) to(11%)

(10) to(6%)

(5) to(1%)

NoChange

1 to 5% 6 to 10% 11 to 20% 21 to 30% 30%+

% o

f Res

pond

ents

Source: Morgan Stanley Freight Pulse Surveys

YoY Rail Spend Growth Expectations for Next 6 Mo. by Range

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

72

Rail Spend Trends: Forward 6 Month YoY Spend Expectations by Segment

28% 22%40%

12%14%

60% 64%50%

0%10%20%30%40%50%60%70%80%90%

100%

All Shippers LargeShippers

SmallShippers

% o

f Res

pond

ents

Increase

Decrease

No Change

2.0%

-1.5%-2%-2%-1%-1%0%1%1%2%2%3%

Large Shippers Small Shippers

Expe

ctat

ion

for N

ext 6

Mo.

-10.0%

1.5%2.4% 2.5% 2.0% 1.8% 1.9%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

$0 -$100k

$100 -$500k

$500k -$1mm

$1 -$5mm

$5 -$20mm

Over$20mm

WeightedAvg

Response

Source: Morgan Stanley Freight Pulse Surveys

6 Mo. YoY Spend Growth Expectation by Spend

Spend Expectations by Size

YoY Spend Growth Expectations

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

73

Rail Pricing Trends: Renewal Rates

0%

10%

5% 4% 4%

6%6%

15%

7%

4%

12%

3% 3% 3%

1%

0%

3%

8%

3% 3% 3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

$0 - $100k $100 -$500k

$500k -$1mm

$1 - $5mm $5 -$20mm

Over$20mm

WeightedAvg

Response

YoY

Incr

ease

in R

ates

Ex-

Fuel

FP 38 (Jun15) FP 39 (Sep15) FP 40 (Dec15)

Source: Morgan Stanley Freight Pulse Surveys

Expectations for Current Year YoY Pricing Ex-Fuel by Spend

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

74

Rail Service Trends: Average Service Levels

5.96.4 6.2 6.1 5.8

5.4 5.5 5.5 5.55.8 5.5

5.9 5.86.3 6.5 6.2 6.2

5.8 5.8 5.8 6.0 5.9 6.0 6.0 6.1 6.06.5 6.6

6.2 6.45.9

5.3 5.6 5.5 5.5 5.3 5.6 5.9 6.2

123456789

10

Source: Morgan Stanley Freight Pulse Surveys

Average Service Levels (Scale 1 = Worst to 10 = Best)

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

75

Rail Service Trends: Detail

6.16.16.56.46.15.95.45.65.85.96.15.76.36.26.66.96.36.15.85.55.65.85.65.86.05.95.96.26.66.06.35.75.05.25.35.24.95.55.76.1

02468

10

5.76.25.96.05.75.45.45.25.15.55.35.65.56.16.16.16.25.96.06.06.26.26.26.16.36.26.76.66.56.56.15.76.05.85.95.85.76.16.2

02468

10

Source: Morgan Stanley Freight Pulse Surveys

Service Reliability (Scale 1 = Worst to 10 = Best)

Value for Dollar (Scale 1 = Worst to 10 = Best)

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

76

Summary of Contents

Part 1: Key Rail Trends 1. Volume Trends 2. Rate Trends 3. Spend Trends 4. Pricing Trends 5. Service Trends

Part 2: Special Topics 1. Intermodal 2. Rate Mitigation Efforts 3. Rail Competition 4. Rate Negotiations 5. Rate Cases 6. Support for Legislation

About the Surveys

General Freight Trends

Rail Trends

Truck Trends

Parcel Trends

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

77

Intermodal: What Factors Are Impacting Your Use of Intermodal Most?

Source: Morgan Stanley Freight Pulse Surveys

Avg. Response on Scale of 1 (Least Impact) to 10 (Most Impact)

6.3 6.85.6

5.0 4.6 4.5

6.1 6.6

5.3 5.24.4 4.1

5.56.3

5.4 5.24.4 4.2

5.56.4

5.05.7

4.5 4.1

123456789

10

TL Rates HaveRisen to Point

Where IntermodalIs Competitive

Intermodal is morefuel efficient

Turning to theIntermodal

Alternative MoreOften During

Periods of TightCapacity

RailroadIntermodal Service

Has Improved

Strong ImportGrowth

Strong ExportGrowth

FP 37 (Mar15) FP 38 (Jun15) FP 39 (Sep15) FP 40 (Dec15)

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

78

Intermodal: Average % Discount to Truckload Carriers?

11121314151617181920

Avg.

Rai

l % D

isco

unt t

o Tr

uckl

oad

Avg. Excl. Fuel = 15.5%

Source: Morgan Stanley Freight Pulse Surveys

Avg. Discount Excl. Fuel

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

79

Rate Mitigation: What Have You Done in an Effort to Reduce Railroad Spend ?

5.9 5.65.1

4.65.4 5.5

5.9

4.55.4

5.95.5

4.65.0

5.75.1

4.4

1

2

3

4

5

6

7

8

9

10

Have Not Made AnyChanges; are Paying Higher

Rail Rates

Moved Freight to AnotherMode (i.e. Truck or Barge)

Moved Freight to AnotherRailroad

Changed Sourcing Facility toIncrease Competitive Options

FP 37 (Mar15) FP 38 (Jun15) FP 39 (Sep15) FP 40 (Dec15)StronglyAgree

StronglyDisagree

Source: Morgan Stanley Freight Pulse Surveys

All Shippers

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

80

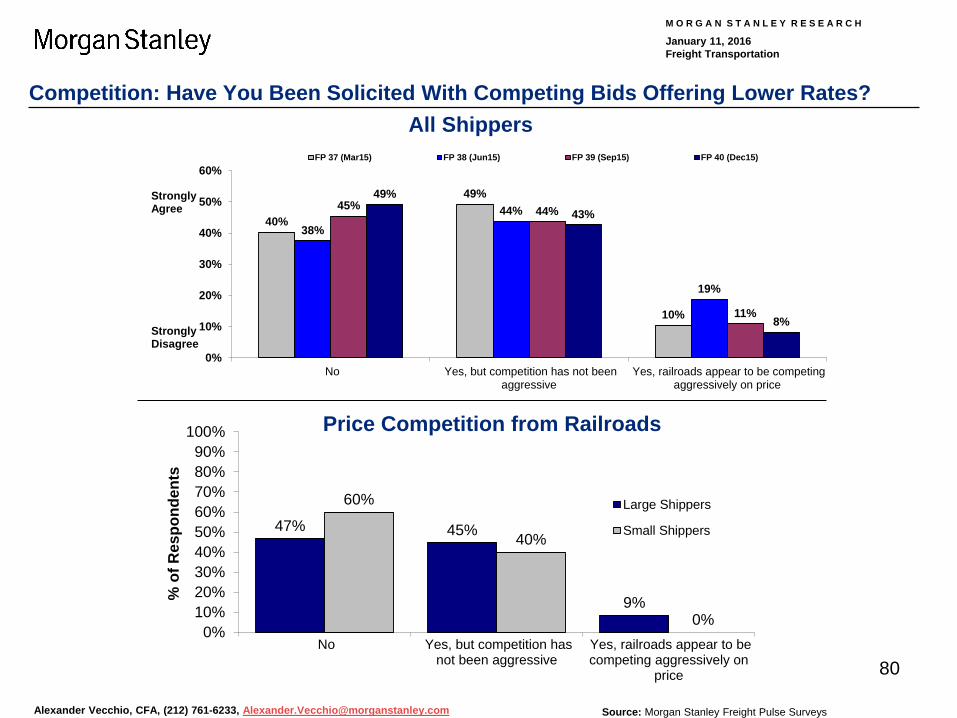

Competition: Have You Been Solicited With Competing Bids Offering Lower Rates?

47% 45%

9%

60%

40%

0%0%

10%20%30%40%50%60%70%80%90%

100%

No Yes, but competition hasnot been aggressive

Yes, railroads appear to becompeting aggressively on

price

% o

f Res

pond

ents

Large Shippers

Small Shippers

Source: Morgan Stanley Freight Pulse Surveys

Price Competition from Railroads

All Shippers

40%

49%

10%

38%44%

19%

45% 44%

11%

49%

43%

8%

0%

10%

20%

30%

40%

50%

60%

No Yes, but competition has not beenaggressive

Yes, railroads appear to be competingaggressively on price

FP 37 (Mar15) FP 38 (Jun15) FP 39 (Sep15) FP 40 (Dec15)

StronglyAgree

StronglyDisagree

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

81

Rail Rate Negotiations: Rate the Difficulty of Recent Rate Negotiations

5.6

6.1

6.7

6.9 7.0 6.8

7.0 7.0

6.9

6.3

6.8

6.4 6.6

6.5 6.4 6.4

6.8

6.3

6.9 7.0

6.9 6.7

6.2

6.7

5.0

5.5

6.0

6.5

7.0

7.5

Sep-09

Apr-10

Sep-10

Jan-11

Apr-11

Jun-11

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Dec-13

Mar-14

Jun-14

Sep-14

Dec-14

Mar-15

Jun-15

Sep-15

Dec-15

Source: Morgan Stanley Freight Pulse Surveys

Scale of 1 (Least Difficult) to 10 (Most Difficult)

M O R G A N S T A N L E Y R E S E A R C H

January 11, 2016 Freight Transportation

Alexander Vecchio, CFA, (212) 761-6233, [email protected]

82

Legislation: Do You Expect to Take a More Active Role in Legislative Rail Reform?

19% 26%

50%50%

60%

31% 24%40%