ENINCON Energy & Infra Consulting

October 2013

Business Report Series

Domestic and International Coal Market in India 2013

Understanding Demand Segmentation and Evolving Dynamics of Coal in India

October 2013

Copyright© 2013 ENINCON, All Rights Reserved

ENINCON Energy & Infra Consulting

Investment Opportunity Factor Business Report Series - EREP

Rise in Coal

imports in India

from FY-06 to

FY-13

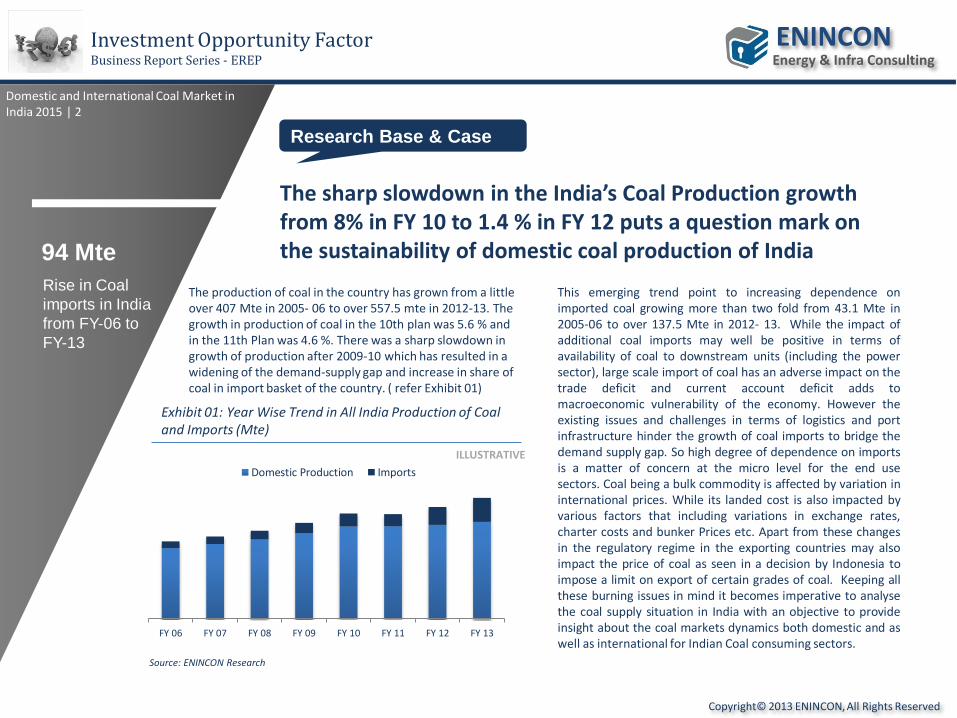

94 Mte

The sharp slowdown in the India’s Coal Production growth from 8% in FY 10 to 1.4 % in FY 12 puts a question mark on the sustainability of domestic coal production of India

Research Base & Case

This emerging trend point to increasing dependence on imported coal growing more than two fold from 43.1 Mte in 2005-06 to over 137.5 Mte in 2012- 13. While the impact of additional coal imports may well be positive in terms of availability of coal to downstream units (including the power sector), large scale import of coal has an adverse impact on the trade deficit and current account deficit adds to macroeconomic vulnerability of the economy. However the existing issues and challenges in terms of logistics and port infrastructure hinder the growth of coal imports to bridge the demand supply gap. So high degree of dependence on imports is a matter of concern at the micro level for the end use sectors. Coal being a bulk commodity is affected by variation in international prices. While its landed cost is also impacted by various factors that including variations in exchange rates, charter costs and bunker Prices etc. Apart from these changes in the regulatory regime in the exporting countries may also impact the price of coal as seen in a decision by Indonesia to impose a limit on export of certain grades of coal. Keeping all these burning issues in mind it becomes imperative to analyse the coal supply situation in India with an objective to provide insight about the coal markets dynamics both domestic and as well as international for Indian Coal consuming sectors.

Exhibit 01: Year Wise Trend in All India Production of Coal and Imports (Mte)

ILLUSTRATIVE

Source: ENINCON Research

Domestic and International Coal Market in India 2015 | 2

FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13

Domestic Production Imports

The production of coal in the country has grown from a little over 407 Mte in 2005- 06 to over 557.5 mte in 2012-13. The growth in production of coal in the 10th plan was 5.6 % and in the 11th Plan was 4.6 %. There was a sharp slowdown in growth of production after 2009-10 which has resulted in a widening of the demand-supply gap and increase in share of coal in import basket of the country. ( refer Exhibit 01)

Copyright© 2013 ENINCON, All Rights Reserved

ENINCON Energy & Infra Consulting

~ 60 GW

Of planned

capacities of 12th

FYP to be coal

based

Research Case

Power Sector is likely to witness a three fold increase in coal imports with import volumes to cross 125 MT by 2020

The power generation sector relies on domestic source as far as meeting coal demand is concerned. Almost, 80 per cent of the coal required by the power industry is sources locally. The share of coal imports is on high since last five years due to lack of domestic production and low quality coal availability in India. The impending demand supply gap is likely to witness a 125 MT of coal coming from imports by 2020 ( refer Exhibit 02). The major challenge will be the unfazed monopoly of CIL making it unable to service the emerging demand. Considering the current levels production at 450 MT, and a 6% CAGR for the increase in production rate, the coal production will reach at 680 MT which depicts a shortage of over 200 MT. The attempt of privatization failed miserably as coal blocks allocated remained unexplored, which led to much hyped Coalgate Scam. As importing coal is the best option to narrow down the demand - supply gap, infrastructure inadequacy will not make it easy. Coal supply chain is a major problem and CIL now moving towards hiving off the same to power plants.

Exhibit 02: Coal Supply Projection to Power Sector by 2020

Key Issues concerning coal supplies to power sector Mining inefficiency of CIL Low quality of coal Higher coal logistics cost Large unmet demand Unexplored captive coal blocks Coal Supply chain

ILLUSTRATIVE

Investment Opportunity Factor Business Report Series - EREP

Domestic and International Coal Market in India 2015 | 3

FY 12 FY 13 FY 14 FY 15 FY 16 FY 17 FY 18 FY 19 FY 20

Imported

Domestic

Copyright© 2013 ENINCON, All Rights Reserved

ENINCON Energy & Infra Consulting

Investment Opportunity Factor Business Report Series - EREP

ENINCON

ENINCON Research &

Services Framework

Research Reports

ENINCON Research

Desk

Business Stakeholders/Parti

cipants

Experts Insights/ Market view

Validated data & analysis

Opportunity mapping

& Market sizing

First hand sector

knowledge & inputs

Gist of the report in .pdf

format for ready use

Free Author

support on report & Competitive

cost

Customized Research Solution

Primary research

inputs from F2F

interviews

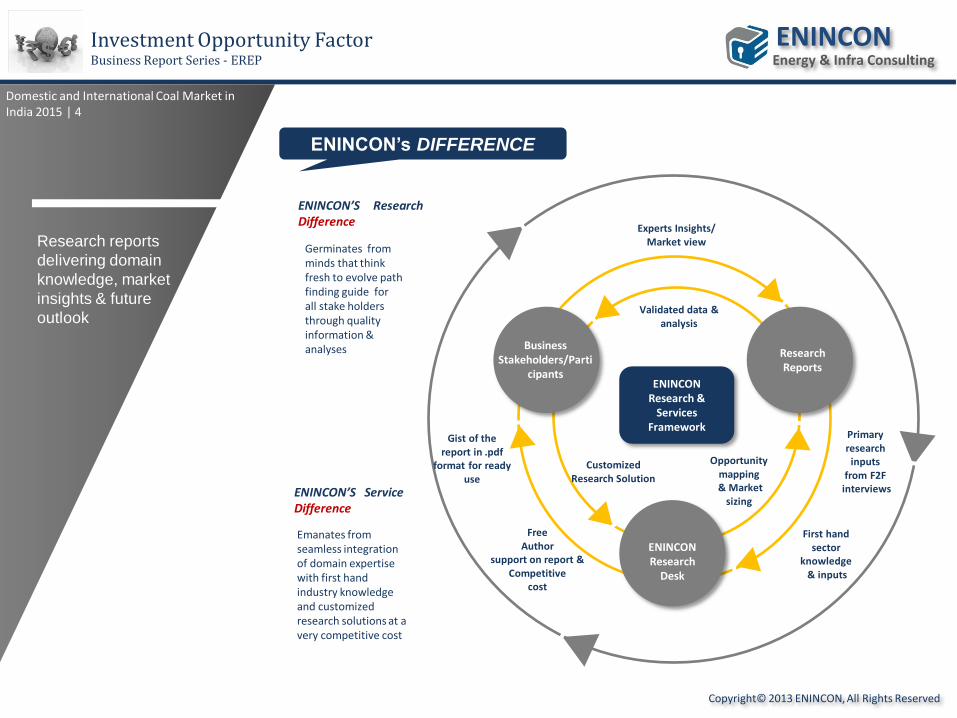

ENINCON’S Research Difference

Germinates from minds that think fresh to evolve path finding guide for all stake holders through quality information & analyses

Emanates from seamless integration of domain expertise with first hand industry knowledge and customized research solutions at a very competitive cost

ENINCON’S Service Difference

ENINCON’s DIFFERENCE

Domestic and International Coal Market in India 2015 | 4

Research reports

delivering domain

knowledge, market

insights & future

outlook

Copyright© 2013 ENINCON, All Rights Reserved

ENINCON Energy & Infra Consulting

Copyright© 2013 ENINCON, All rights reserved

Investment Opportunity Factor Business Report Series - EREP

Research Objective & Results

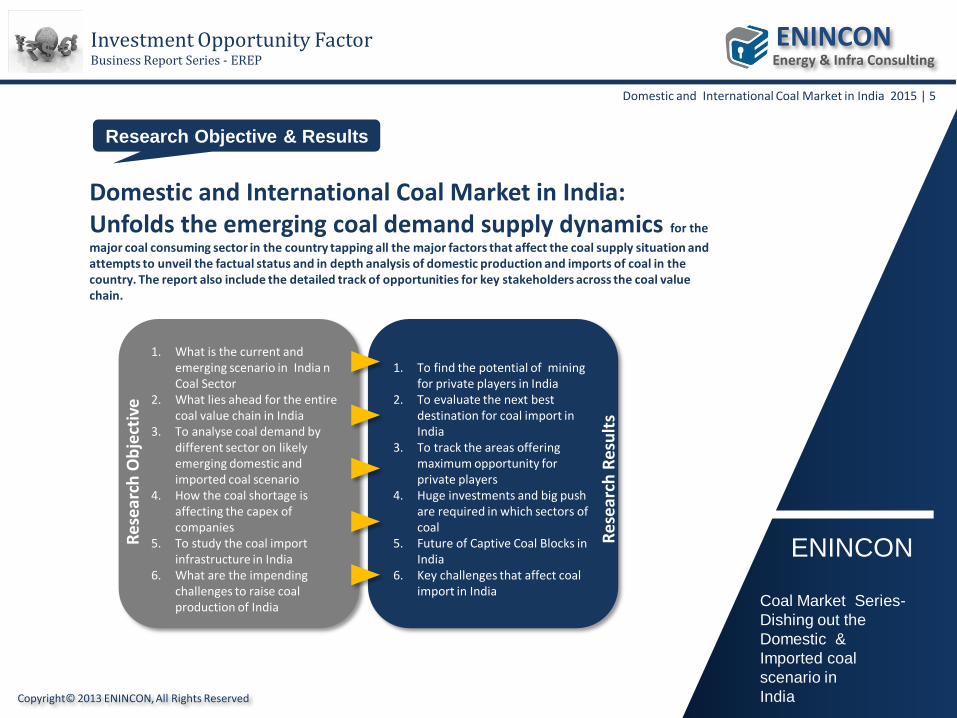

Domestic and International Coal Market in India: Unfolds the emerging coal demand supply dynamics for the

major coal consuming sector in the country tapping all the major factors that affect the coal supply situation and attempts to unveil the factual status and in depth analysis of domestic production and imports of coal in the country. The report also include the detailed track of opportunities for key stakeholders across the coal value chain.

Res

earc

h O

bje

ctiv

e

Res

earc

h R

esu

lts

1. What is the current and emerging scenario in India n Coal Sector

2. What lies ahead for the entire coal value chain in India

3. To analyse coal demand by different sector on likely emerging domestic and imported coal scenario

4. How the coal shortage is affecting the capex of companies

5. To study the coal import infrastructure in India

6. What are the impending challenges to raise coal production of India

1. To find the potential of mining for private players in India

2. To evaluate the next best destination for coal import in India

3. To track the areas offering maximum opportunity for private players

4. Huge investments and big push are required in which sectors of coal

5. Future of Captive Coal Blocks in India

6. Key challenges that affect coal import in India

Domestic and International Coal Market in India 2015 | 6

ENINCON

Coal Market Series-

Dishing out the

Domestic &

Imported coal

scenario in

India

Domestic and International Coal Market in India 2015 | 5

Copyright© 2013 ENINCON, All Rights Reserved

ENINCON Energy & Infra Consulting

Investment Opportunity Factor Business Report Series - EREP

Identifying eccentric

opportunities

Opportunities for PSUs and

the savings for DISCOMs

Opportunities for equipment manufacturers

Opportunities for equipment manufacturers

Domestic and International Coal Market in India 2015 | 6

ENINCON Research reports

delivering domain

knowledge, market

insights & future

outlook

Key Queries Resolved

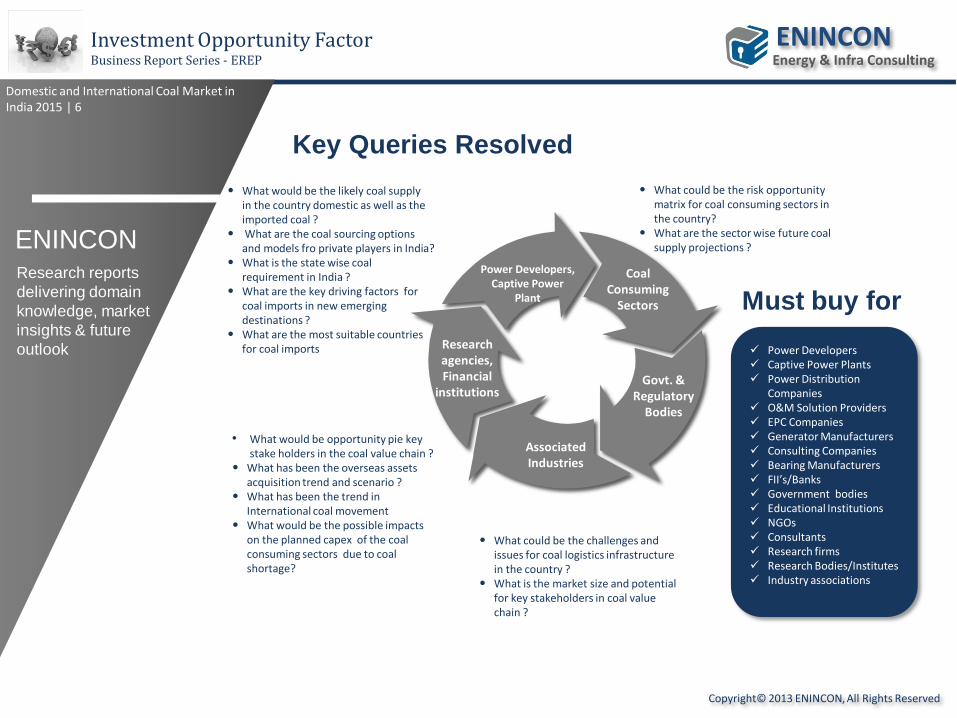

• What would be the likely coal supply in the country domestic as well as the imported coal ?

• What are the coal sourcing options and models fro private players in India?

• What is the state wise coal requirement in India ?

• What are the key driving factors for coal imports in new emerging destinations ?

• What are the most suitable countries for coal imports

Must buy for

Power Developers Captive Power Plants Power Distribution

Companies O&M Solution Providers EPC Companies Generator Manufacturers Consulting Companies Bearing Manufacturers FII’s/Banks Government bodies Educational Institutions NGOs Consultants Research firms Research Bodies/Institutes Industry associations

• What would be opportunity pie key stake holders in the coal value chain ?

• What has been the overseas assets acquisition trend and scenario ?

• What has been the trend in International coal movement

• What would be the possible impacts on the planned capex of the coal consuming sectors due to coal shortage?

• What could be the challenges and

issues for coal logistics infrastructure in the country ?

• What is the market size and potential for key stakeholders in coal value chain ?

• What could be the risk opportunity

matrix for coal consuming sectors in the country?

• What are the sector wise future coal supply projections ?

Power Developers, Captive Power

Plant

Research agencies, Financial

institutions

Associated Industries

Govt. & Regulatory

Bodies

Coal Consuming

Sectors

Copyright© 2013 ENINCON, All Rights Reserved

ENINCON Energy & Infra Consulting

1. Executive Summary

2. Coal in India- A Brief Know How 2.1 Coal in Primary Energy Mix 2.2 Coal Consumption Trend in India 2.3 Coal Import Trend in India 2.4 Coal Mining Growth Trend in India 2.5 Regulatory Policy & Framework 2.6 Private Sector Participation 2.7 Coal India’s Accountability 2.8 Impending Issues & Challenges

3. Existing Demand-Supply Dynamics of Coal in India 3.1 Demand Supply Position for Coal Consuming Sectors 3.2 Risk Opportunity Matrix for Coal Consuming Sectors 3.3 Current & Future Consumption Analysis for Coal Consuming Sector 3.4 Factors Dampening Growth of Coal Consuming Industries in India 4. Coal for Power Generation in India 4.1 Region Wise Coal Fired Power Plants in India & their Coal Requirement 4.2 Supply Dynamics for Power Generation- Fuel Linkage, E-auction & Imports 4.3 Coal Sourcing Options & Model for Power Sector 4.4 Key Coal Consuming Companies in Power Sector - Profile Analysis 4.4.1 Existing Operation 4.4.2 Planned Capex/ Expansion 4.5.3 Coal Demand 4.5.4 Coal Sourcing 4.5.5 Imports Volume 4.5.6 Fuel Linkages 4.6 Future Outlook- Coal for Power Generation in India 2020

5. Coal for Cement Production in India 5.1 Region Wise Cement Plants in India & their Coal Requirement 5.2 Coal Demand and Supply Source 5.3 Coal Sourcing Options and Model for Cement Industry 5.4 Case Study- Impact of Coal Shortage 5.5 Key Coal Consuming Companies in Cement Industry- Profile Analysis 5.5.1 Existing Operations 5.5.2 Planned Capex/ Expansion 5.5.3 Coal Demand 5.5.4 Import Volume 5.5.5 Coal Source- Fuel Linkages 5.6 Future Outlook- Coal Demand for Cement Industry- 2020

6. Coal for Sponge Iron Industry in India 6.1 Region Wise Sponge Iron Plants in India & their Coal Requirement 6.2 Coal Demand and Supply Source 6.3 Coal Sourcing Options and Model for Sponge Iron Industry 6.5 Case Study- Impact of Coal Shortage 6.6 Key Coal Consuming Companies in Sponge Iron Industry- Profile Analysis 6.6.1 Existing Operations 6.6.2 Planned Capex/ Expansion 6.6.3 Coal Demand 6.6.4 Import Volume 6.6.5 Coal Source- Fuel Linkages 6.6 Future Outlook- Coal Demand for Sponge Iron Industry- 2020

7. Coal Requirement in Steel and Process Industry in India -2020 7.1 Region Wise Steel and Process in India & their Coal Requirement 7.2 Coal Demand and Supply Source 7.3 Coal Sourcing Options and Model for Steel and Process Industry

Contents & Coverage Domestic and International Coal Market in India 2015 | 7

Copyright© 2013 ENINCON, All Rights Reserved

ENINCON Energy & Infra Consulting

Contents & Coverage Domestic and International Coal Market in India 2015 | 8

7.4 Case Study- Impact of Coal Shortage 7.5 Key Coal Consuming Companies in Steel and Process Industry- Profile Analysis 7.5.1 Existing Operations 7.5.2 Planned Capex/ Expansion 7.5.3 Coal Demand 7.5.4 Import Volume 7.5.5 Coal Source- Fuel Linkages 7.6 Future Outlook- Coal Demand for Cement Industry- 2020

8. Domestic Coal Supply in India 8.1 Coal Supply Structure 8.2 Region Wise Mine Update 8.2.2 Open Cast Mines 8.2.3 Under Ground Mines 8.3 Coal Production Trends 8.3.1 Coal India’s Production Trend 8.3.2 Coal Block Production Trends 8.4 Coal Production Outlook – 2020

9. Imported Coal Supply in India 9.1 Global Coal Supply Dynamics 9.2 Country Wise Analysis of Coal Supply to India 9.3 Seaborne Coal Supply to India-2012 9.4 Seaborne Coal Supply to India Outlook-2020 9.5 Impact of Logistics and Port Infrastructure

10. Coal Import Destinations for India 10.1 Country Specific Analysis 10.2 Country Wise Comparative Analysis

10.2.1 Logistics

10.2.2 Pricing 10.2.3 Coal Resource 10.2.4 Other Parameters 10.3 Risk/ Opportunity Matrix 10.4 Impact Assessment

11. Coal Import Infrastructure in India 11.1 Port Wise Analysis 11.1.1 Coal Handling Capacities 11.1.2 Coal Handling Infrastructure at Major Ports 11.2 Coal Transportation and Disposition Issues 11.3 Shortfall in Coal Import Infrastructure 11.3.1 Key Challenges 11.3.2 Way Forward 11.4 Relevance Matrix for Major Consumers 11.5 Imported Coal Deficit- Future Dynamics 11.6 Opportunities for Major Stakeholders vis-à-vis deficit

12. International Coal Market-Trade and Movement 12.1 Trend Analysis 12.2 Coal Movement across the Globe 12.3 Factors affecting Coal Trade 12.4 International Coal Pricing 12.4.1 Spot 12.4.2 Medium term 12.4.3 Long Term 12.5 Global Coal trade Models 12.6 Global Benchmarks and Best Practices for Coal Trade- Leaning’s for India 12.7 Profile of Key Players

Copyright© 2013 ENINCON, All Rights Reserved

ENINCON Energy & Infra Consulting

Contents & Coverage

13. Opportunity Assessment for Key Stakeholders in Indian Coal Sector 13.1 Value Chain Analysis for Stakeholders 13.2 Assessment of Market Size and Potential 13.3 Opportunities in Store- Short, Medium and Long Term Analysis 13.4 Overseas Asset Acquisition- Trend and Scenario

14. ENINCON’s Findings

15. Recommendations

Domestic and International Coal Market in India 2015 | 9

Copyright© 2013 ENINCON, All Rights Reserved