Commercial insurance underwriting Best practice case underwriting and portfolio management

© 2013 Towers Watson. All rights reserved. towerswatson.com

1

A presentation to the Turkish CUOs

by David Ovenden

Nov 2013

Agenda

© 2013 Towers Watson. All rights reserved. towerswatson.com

2

Introduction

The Turkish

market in an

international

context

TW best practice

framework

Thoughts and

priorities

Introductions

© 2013 Towers Watson. All rights reserved. towerswatson.com

3

David Ovenden

Director, RCS

London

Chris Halliday

Consultant, RCS

Istanbul

Phone. +44 207 8865106

Mobile. +44 7908 1188855

Phone. +90 212 337 2104

Mobile. +90 530 303 3822

© 2013 Towers Watson. All rights reserved. towerswatson.com

4

Introduction

The Turkish

market in an

international

context

TW best practice

framework

Thoughts and

priorities

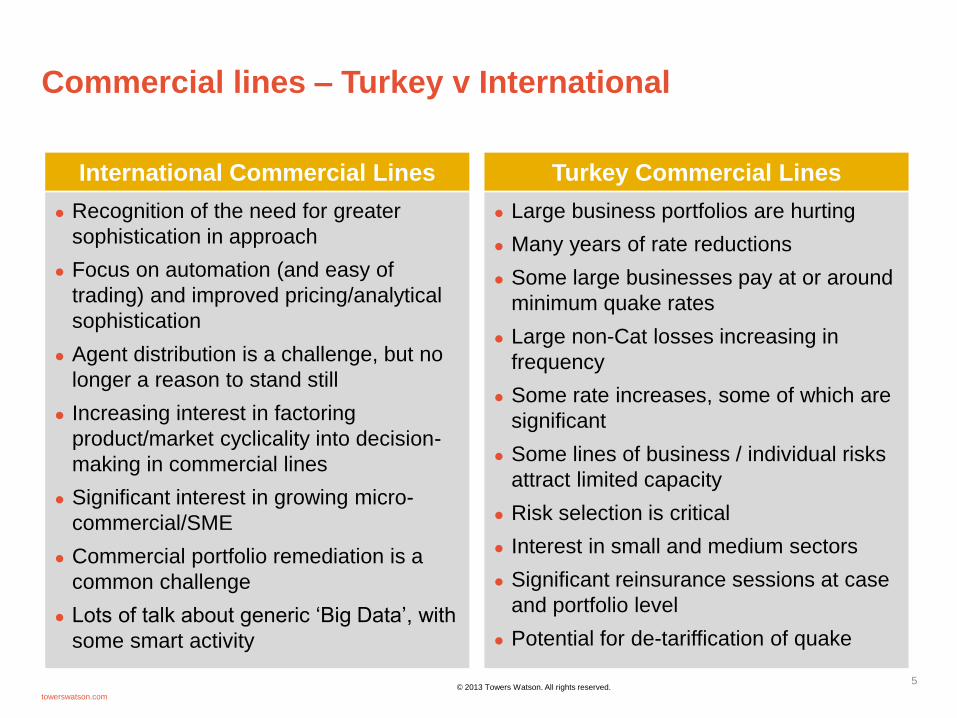

Commercial lines – Turkey v International

© 2013 Towers Watson. All rights reserved.

towerswatson.com

5

Recognition of the need for greater

sophistication in approach

Focus on automation (and easy of

trading) and improved pricing/analytical

sophistication

Agent distribution is a challenge, but no

longer a reason to stand still

Increasing interest in factoring

product/market cyclicality into decision-

making in commercial lines

Significant interest in growing micro-

commercial/SME

Commercial portfolio remediation is a

common challenge

Lots of talk about generic ‘Big Data’, with

some smart activity

Large business portfolios are hurting

Many years of rate reductions

Some large businesses pay at or around

minimum quake rates

Large non-Cat losses increasing in

frequency

Some rate increases, some of which are

significant

Some lines of business / individual risks

attract limited capacity

Risk selection is critical

Interest in small and medium sectors

Significant reinsurance sessions at case

and portfolio level

Potential for de-tariffication of quake

International Commercial Lines Turkey Commercial Lines

© 2013 Towers Watson. All rights reserved. towerswatson.com

6

Introduction

The Turkish

market in an

international

context

TW best practice

framework

Thoughts

questions and

priorities

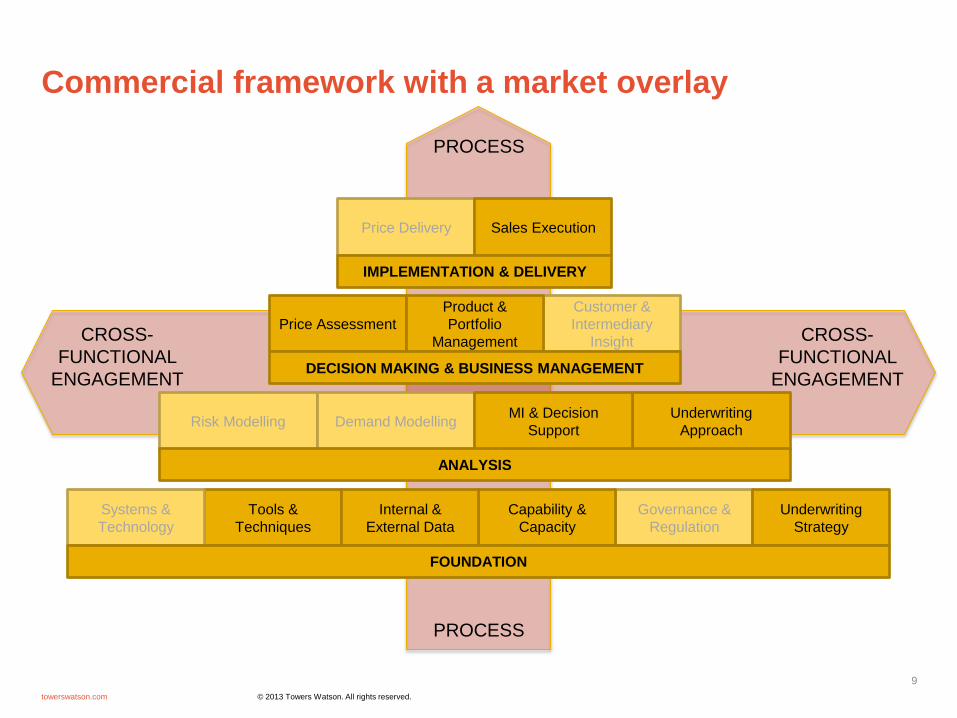

PROCESS

PROCESS

CROSS-

FUNCTIONAL

ENGAGEMENT

CROSS-

FUNCTIONAL

ENGAGEMENT

Best practice underwriting

© 2013 Towers Watson. All rights reserved. towerswatson.com

7

Price Delivery

Governance &

Regulation

Tools &

Techniques

Capability &

Capacity

Internal &

External Data

Systems &

Technology

Underwriting

Strategy

Customer &

Intermediary

Insight

Price Assessment

FOUNDATION

Underwriting

Approach Risk Modelling Demand Modelling

MI & Decision

Support

ANALYSIS

Product &

Portfolio

Management

DECISION MAKING & BUSINESS MANAGEMENT

Sales Execution

IMPLEMENTATION & DELIVERY

Case Underwriting Best Practice Components

• Client

• Exposure

• Context

Background

• Appetite

• Acceptance Criteria

Initial Acceptance

• Condition

• Extensions

• Exclusions

Case UW

• Client Solutions

• Cover & Price options

Deal Options • Conclusion

• Documentation

• Policy Execution

Negotiate

© 2013 Towers Watson. All rights reserved. towerswatson.com

8

Active Portfolio Management

Governance Environment

Decision Support, Data, MI & Communication

• Tech Price

• Actual Price

Pricing

PROCESS

PROCESS

CROSS-

FUNCTIONAL

ENGAGEMENT

CROSS-

FUNCTIONAL

ENGAGEMENT

Commercial framework with a market overlay

© 2013 Towers Watson. All rights reserved. towerswatson.com

9

Price Delivery

Governance &

Regulation

Tools &

Techniques

Capability &

Capacity

Internal &

External Data

Systems &

Technology

Underwriting

Strategy

Customer &

Intermediary

Insight

Price Assessment

FOUNDATION

Underwriting

Approach Risk Modelling Demand Modelling

MI & Decision

Support

ANALYSIS

Product &

Portfolio

Management

DECISION MAKING & BUSINESS MANAGEMENT

Sales Execution

IMPLEMENTATION & DELIVERY

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

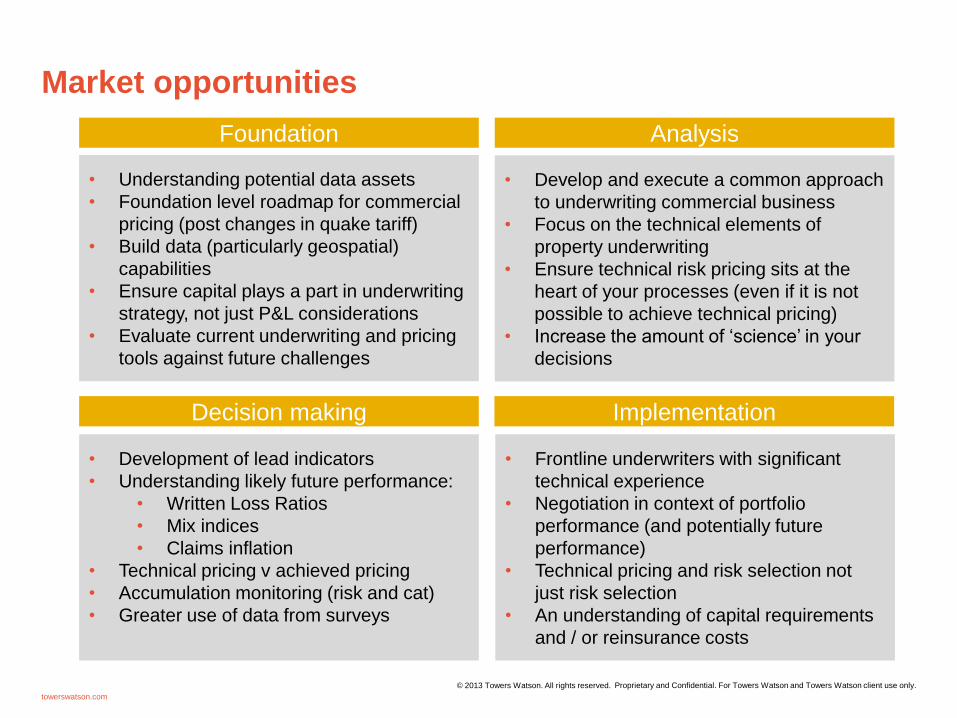

Market opportunities

towerswatson.com

© 2013 Towers Watson. All rights reserved.

• Understanding potential data assets

• Foundation level roadmap for commercial

pricing (post changes in quake tariff)

• Build data (particularly geospatial)

capabilities

• Ensure capital plays a part in underwriting

strategy, not just P&L considerations

• Evaluate current underwriting and pricing

tools against future challenges

• Develop and execute a common approach

to underwriting commercial business

• Focus on the technical elements of

property underwriting

• Ensure technical risk pricing sits at the

heart of your processes (even if it is not

possible to achieve technical pricing)

• Increase the amount of ‘science’ in your

decisions

• Development of lead indicators

• Understanding likely future performance:

• Written Loss Ratios

• Mix indices

• Claims inflation

• Technical pricing v achieved pricing

• Accumulation monitoring (risk and cat)

• Greater use of data from surveys

• Frontline underwriters with significant

technical experience

• Negotiation in context of portfolio

performance (and potentially future

performance)

• Technical pricing and risk selection not

just risk selection

• An understanding of capital requirements

and / or reinsurance costs

Foundation Analysis

Decision making Implementation

Agenda

© 2013 Towers Watson. All rights reserved. towerswatson.com

11

Introduction

The Turkish

market in an

international

context

TW best practice

framework

Thoughts

questions and

priorities

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

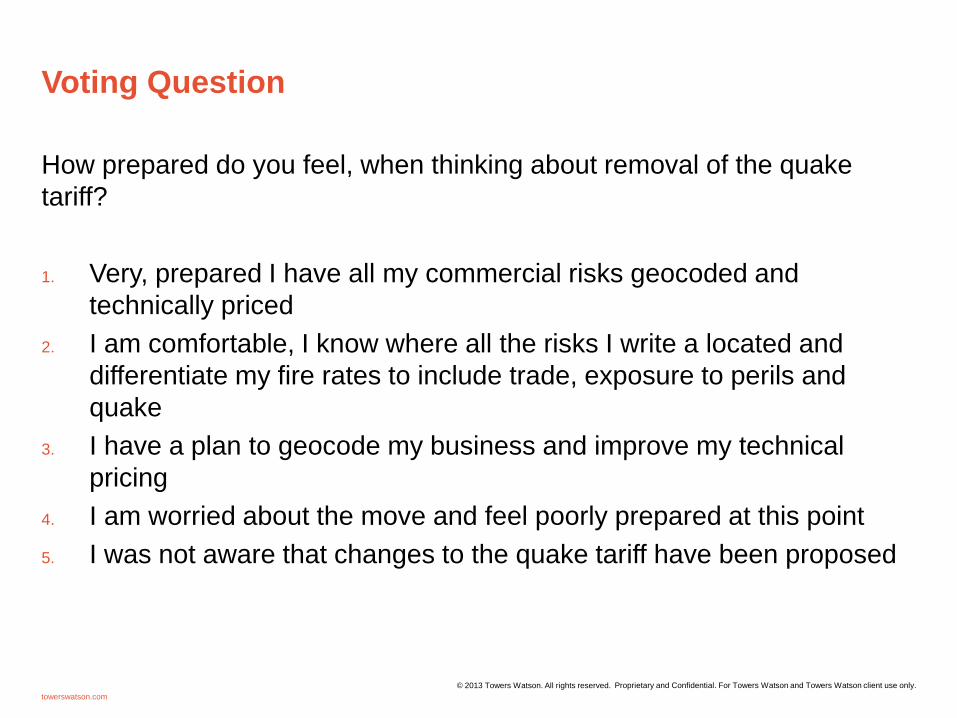

Voting Question

How prepared do you feel, when thinking about removal of the quake

tariff?

1. Very, prepared I have all my commercial risks geocoded and

technically priced

2. I am comfortable, I know where all the risks I write a located and

differentiate my fire rates to include trade, exposure to perils and

quake

3. I have a plan to geocode my business and improve my technical

pricing

4. I am worried about the move and feel poorly prepared at this point

5. I was not aware that changes to the quake tariff have been proposed

towerswatson.com

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

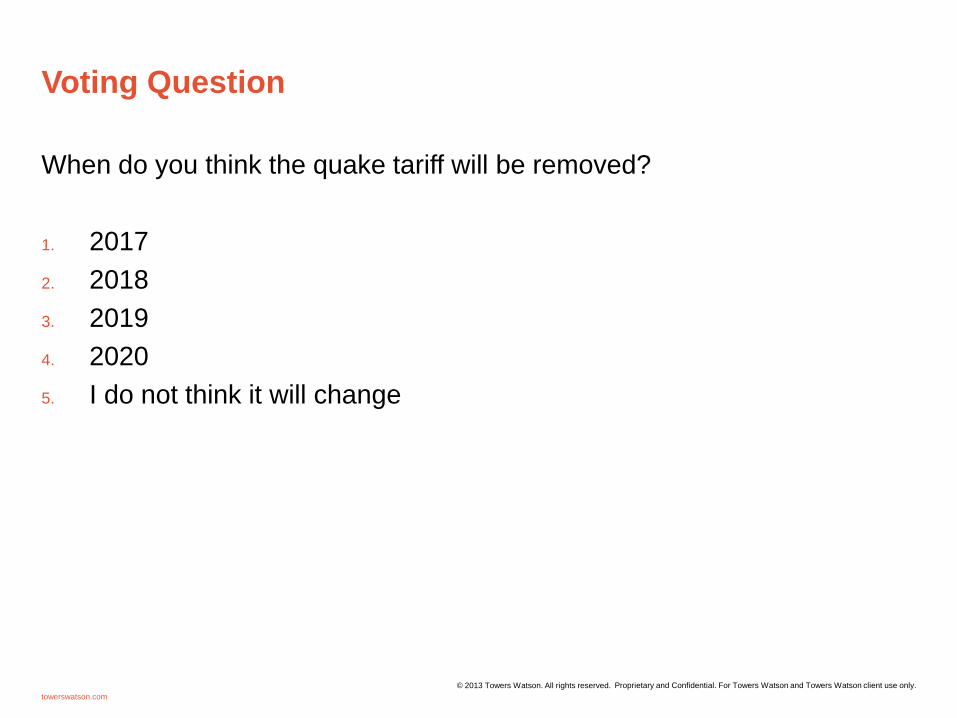

Voting Question

When do you think the quake tariff will be removed?

1. 2017

2. 2018

3. 2019

4. 2020

5. I do not think it will change

towerswatson.com

© 2013 Towers Watson. All rights reserved.

Building a strong analytical foundation

© 2013 Towers Watson. All rights reserved. towerswatson.com

14

An

aly

tic

al

Wo

rks

tre

am

s

Having a detailed understanding of performance at a product level is vital.

Understanding the relationship between exposure and rate achieved is a

minimum requirement. Industry leading retention management requires a

view of technical price

Rate and

exposure data

Are you capturing the pricing and underwriting information

you need when the claims are reported? A lot is spoken about ‘big data’

but the best sources of underlying claims data, on which to layer external

data, are you own claimants.

Claims cause

codes

Where are you winning, what trades, sectors, geographies are you

competitive? Are you getting a ‘fair’ share of an agents business? Do my

commission and additional remuneration payments represent value for

money? All simple issues, but is the data granular enough?

New and

retention

performance

It will take some time to geocode your commercial exposures, however the

benefits in terms of underwriting decision support and RI purchasing will

deliver a significant return on investment – especially if the quake tariff is

removed.

Geospatial Data

Building a strong foundation will allow you to out-compete and remain agile

Building a strong analytical foundation

© 2013 Towers Watson. All rights reserved. towerswatson.com

15

An

aly

tic

al

Wo

rks

tre

am

s

Having a detailed understanding of performance at a product level is vital.

Understanding the relationship between exposure and rate achieved is a

minimum requirement. Industry leading retention management requires a

view of technical price

Rate and

exposure data

Are you capturing the pricing and underwriting information

you need when the claims are reported? A lot is spoken about ‘big data’

but the best sources of underlying claims data, on which to layer external

data, are you own claimants.

Claims cause

codes

Where are you winning, what trades, sectors, geographies are you

competitive? Are you getting a ‘fair’ share of an agents business? Do my

commission and additional remuneration payments represent value for

money? All simple issues, but is the data granular enough?

New and

retention

performance

It will take some time to geocode your commercial exposures, however the

benefits in terms of underwriting decision support and RI purchasing will

deliver a significant return on investment – especially if the quake tariff is

removed.

Geospatial Data

Building a strong foundation will allow you to out-compete and remain agile

A Canadian insurer

has out performed the

market by some 3

percentage points over

the last 5 years. Much

of this outperformance

has been built on their

ability to capture,

manage and analyse

internal and external

data.

In Ireland a

commercial insurer

was able to

substantially

reduced reinsurance

cost and capital

loadings by

providing they were

less flood exposed

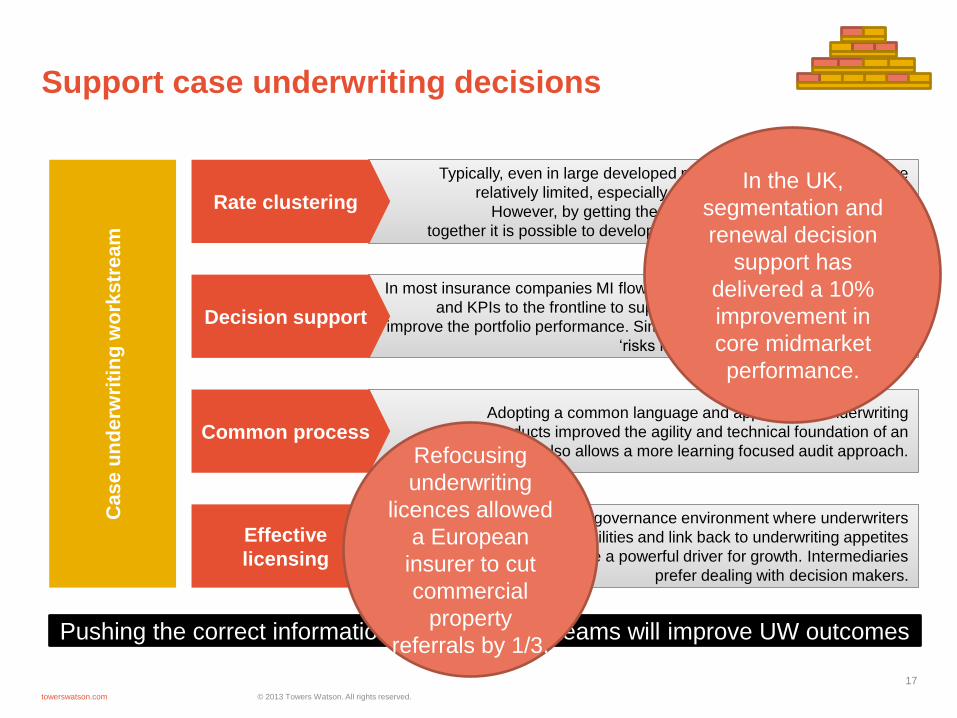

Support case underwriting decisions

© 2013 Towers Watson. All rights reserved. towerswatson.com

16

Cas

e u

nd

erw

riti

ng

wo

rkstr

ea

m

In most insurance companies MI flows up the organisation. By directing MI

and KPIs to the frontline to support decision making it is possible to

improve the portfolio performance. Simple decision support points include;

‘risks like these’ and intermediary scores

Decision support

Adopting a common language and approach to underwriting

specific products improved the agility and technical foundation of an

organisation. It also allows a more learning focused audit approach. Common process

An effective governance environment where underwriters

authorities reflect their capabilities and link back to underwriting appetites

and the business plan can be a powerful driver for growth. Intermediaries

prefer dealing with decision makers.

Effective

licensing

Typically, even in large developed markets the volumes of data are

relatively limited, especially when you get down to trade level.

However, by getting the underwriters and actuaries working

together it is possible to develop board averages from which to start.

Rate clustering

Pushing the correct information to the frontline teams will improve UW outcomes

Support case underwriting decisions

© 2013 Towers Watson. All rights reserved. towerswatson.com

17

Cas

e u

nd

erw

riti

ng

wo

rkstr

ea

m

In most insurance companies MI flows up the organisation. By directing MI

and KPIs to the frontline to support decision making it is possible to

improve the portfolio performance. Simple decision support points include;

‘risks like these’ and intermediary scores

Decision support

Adopting a common language and approach to underwriting

specific products improved the agility and technical foundation of an

organisation. It also allows a more learning focused audit approach. Common process

An effective governance environment where underwriters

authorities reflect their capabilities and link back to underwriting appetites

and the business plan can be a powerful driver for growth. Intermediaries

prefer dealing with decision makers.

Effective

licensing

Typically, even in large developed markets the volumes of data are

relatively limited, especially when you get down to trade level.

However, by getting the underwriters and actuaries working

together it is possible to develop board averages from which to start.

Rate clustering

Pushing the correct information to the frontline teams will improve UW outcomes

In the UK,

segmentation and

renewal decision

support has

delivered a 10%

improvement in

core midmarket

performance.

Refocusing

underwriting

licences allowed

a European

insurer to cut

commercial

property

referrals by 1/3.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

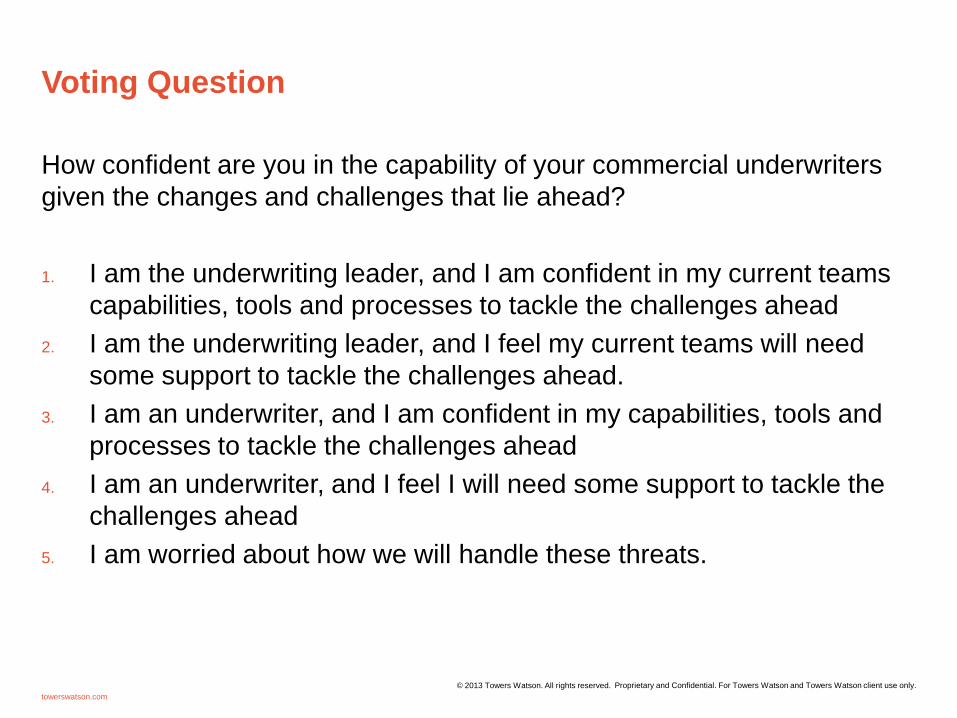

Voting Question

How confident are you in the capability of your commercial underwriters

given the changes and challenges that lie ahead?

1. I am the underwriting leader, and I am confident in my current teams

capabilities, tools and processes to tackle the challenges ahead

2. I am the underwriting leader, and I feel my current teams will need

some support to tackle the challenges ahead.

3. I am an underwriter, and I am confident in my capabilities, tools and

processes to tackle the challenges ahead

4. I am an underwriter, and I feel I will need some support to tackle the

challenges ahead

5. I am worried about how we will handle these threats.

towerswatson.com

© 2013 Towers Watson. All rights reserved.

Deploy appropriate automation

© 2013 Towers Watson. All rights reserved. towerswatson.com

19

Au

tom

ate

d u

nd

ew

riti

ng

wo

rks

tre

am

It is possible to ‘fastrack’ or have a low touch renewal approach for some

small and medium business. Segmentation and a better understanding of

‘technical’ price will allow sophisticated approaches to automatic renewal,

freeing the underwriters to write new business

Fastrack

renewals

An important part of the automation process is the product development.

Simple products that are well suited to the target audience with features,

deductibles , assumptions and conditions that reflect the automated basis

of acceptance.

SME products

When automating new business or renewals it is important to identify

outliers, risks that look weird, that perhaps an underwriter would spot.

These outliers can be pushed out of the process. Identify outliers

Understanding what trades and products represent suitable targets for

automation is key to balance the needs of efficiency and effectiveness. Segmentation

Balancing efficiency and effectiveness will deliver competitive advantage

Deploy appropriate automation

© 2013 Towers Watson. All rights reserved. towerswatson.com

20

Au

tom

ate

d u

nd

ew

riti

ng

wo

rks

tre

am

It is possible to ‘fastrack’ or have a low touch renewal approach for some

small and medium business. Segmentation and a better understanding of

‘technical’ price will allow sophisticated approaches to automatic renewal,

freeing the underwriters to write new business

Fastrack

renewals

An important part of the automation process is the product development.

Simple products that are well suited to the target audience with features,

deductibles , assumptions and conditions that reflect the automated basis

of acceptance.

SME products

When automating new business or renewals it is important to identify

outliers, risks that look weird, that perhaps an underwriter would spot.

These outliers can be pushed out of the process. Identify outliers

Understanding what trades and products represent suitable targets for

automation is key to balance the needs of efficiency and effectiveness. Segmentation

Balancing efficiency and effectiveness will deliver competitive advantage

A market leading

European insurer was

able to drive profitable

growth in a competitive

European market by

repositioning its Small

Business products,

simplifying the

quotation process and

improving speed to

market.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

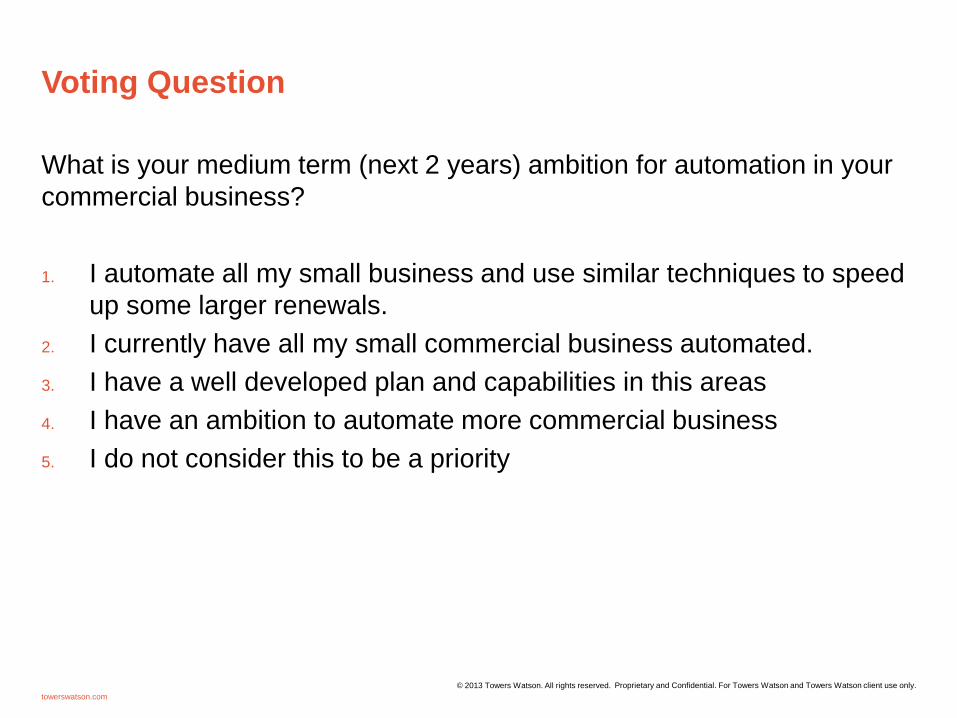

Voting Question

What is your medium term (next 2 years) ambition for automation in your

commercial business?

1. I automate all my small business and use similar techniques to speed

up some larger renewals.

2. I currently have all my small commercial business automated.

3. I have a well developed plan and capabilities in this areas

4. I have an ambition to automate more commercial business

5. I do not consider this to be a priority

towerswatson.com

© 2013 Towers Watson. All rights reserved.

Proprietary and Confidential. For Towers Watson and Towers Watson client use only.

Questions

towerswatson.com

© 2013 Towers Watson. All rights reserved.