Download - China RMB Devaluation 2016

1

ChinaRMBDevaluationLikelyin2016

China is in the acute phase of a deleveraging process that is causingremarkable volatility across financial markets. China must make harddecisionstoavoidcrisisandmoveontothesecond,morebenign,phase.China’s debt binge has been well documented and now the inevitabledeleveragingoccurring.MuchliketheUSin2008,Chinanowfacestoughchoices. The political leaders in Beijing must engineer a deleveragingeitherthroughrecapitalization,currencydevaluation,economicgrowth,oroutrightdefault.The probability of outright default is quite low. China has enoughresources to absorbmuchof thebaddebt,while adefault riskspoliticalandsocialunrest.ItisdoubtfulthattheChineseleadershipwouldchoosethis path. Choosing default, as the solution to its debt problem is a lastresort,it’spossiblebutnotprobable.The next least likely solution is engineering economic growth. The debtbuildup since 2008 created tremendous excess capacity in virtually alleconomic sectors. Ghost cities and zombie factories are a few of theobservable outcomes of this excess capacity. The economic impact ofexcesscapacityisstagnationatbestandrecessionatworst.Therefore,theprobabilityofanotherChinagrowthmiracleisalsoquitelow.Over the last year, the Chinese government attempted and failed tojumpstart its public equitymarkets. The plan was to fashion a vibrantequitymarketthatdebt-ladenfirmscouldusetorecapitalizeviaIPO’s.Thedebtburdenwouldhavebeenshiftedfromcorporationstoequityholders.Alas,theonlythingthatChineseleaderswereabletogeneratewasastockmarketbubbleandsubsequentcrash. Inordertohaltthecrash,officialswereforcedtosuspendIPO’s. Ineffect,thishasshutthestockmarketto

February7,2016

BKCMLLC340MadisonAveNewYork,NY10173212-220-9249 • Chinahasatmost5monthsbeforeacurrencycrisis.

• China’sFXreservesareinadequaterelativetothesizeofitseconomy.

• Chinareacheda“MinskyMoment”in2014thatcouldkeeptheassetpricesdepresseduntil2019.

• WeexpectadevaluationoftheRMBontheorderof25%+in2016.

2

anyfirmlookingtorecapitalize.CurrencydevaluationisChina’slastandonlyrealisticchoice,inourview.Acurrencydevaluationof25%wouldstimulateexportgrowthandfosterinflationthatcouldeasethedeleveragingprocess.Ofcourseadevaluationofthismagnitudewouldsendshockwavesthroughfinancialmarkets,butinthemediumtolongrunitappearstobethemostprobablepath.Ontheotherhand,thereisalong-termargumentforastrongercurrency,especially as China shifts toward consumption. A stronger Chinesecurrencywould giveChinese citizensmorepurchasingpower that couldincreaseconsumptionof foreigngoods. Inourview, it is thiscompetingargumentthathascausedChinatocommitamonetarypolicyerror.The competing arguments on the proper direction of the Yuan, coupledwithcapitalflighthaveforcedChinatodefenditscurrency.BydefendingitscurrencyChinaisactuallyconductingquantitativetightening(QT)andthiscontractionarypolicyhascreatedanuglydeflationarydeleveraging.Theterm“uglydeleveraging”wascoinedbyRayDalioofBridgewaterandin our view accurately describes the current situation. In an uglydeflationary deleveraging very few asset classes do well, typicallycommoditiesandequitiesfallwhilebondsrise.Youmay be asking yourself why Chinamatters to the US stockmarket.AfteralltheUSisarelativelyclosedeconomythatgenerallybenefitsfromthedeflationaryforcescurrentlyswirlingaroundtheworld.Chinamattersto investorsbecausemostof thecompanies in theS&P500havegrowthmodelsthatcenteronChina.Inarecentreport,OlegMelentyevofDeutscheBank, laidouta fewstatsabouttheimportanceofChinatotheglobaleconomy:

Smartphones:70%ofallsalesarecomingoutsideofNorthAmericaandEurope,45%aresoldinBRICscountries;Bigpharma:43%ofsalesareoutsideofUS/EU/Japan;Education–alongwithtravelandthusretail–contributes1/4toallUSservices exports, the single-largest line-item; 62% of all internationalstudentsintheUSarecomingfromChina;Social media – Facebook, Google and Twitter receive about 1/3rd oftheiradrevenuefromEMcountries;Media – themovie industry only breaks out international sales,which

3

are65%oftotal–butit’sreasonabletoassumethatthisbeingasmall-ticketitem,theproportionofEMsalesherecouldbeclosetoEMshareofworldpopulation,whichis85%.Mostofthesegoodsandservicessoldinternationallydonotregisterasexports from the US as they are assembled/provided, delivered, andbooked by non-US subsidiaries of multinational corporations. As anobvious example, if all such revenueswere booked as exports, Apple’ssales in China alone would account for 1/2 of all US exports to thatcountry,servicesincluded!

ThefeedbackloopbetweenChinaandUScorporationsisstrongerthananaïve analysis of direct exportswould suggest. In the first fewweeks ofJanuary,USinvestorsdirectlyexperiencedthepowerofthisfeedbackloop.Chinaisonthevergeofitsown“2008”moment.Chinahasachoice;intheshort termitmustabandon itsdesire forreservecurrencystatusand itsplan to boost consumption through increased purchasing power. Theseareadmirablegoals,butbettersuitedforafterthedeleveragingprocess.IfChinadoesnotmake thedevaluationchoice it risksa crisis that couldtakeyearstoresolve.DuringsimilarexperiencesittooktheUS2yearsin2007-2009 and 1930-1932 before it moved to the second stage of thedeleveraging. Japanalsooffersacautionaryexampleofaneconomythatprolongeditsdeleveragingandsufferedlostdecades.UntilChinaaddresses itsdebtproblemtheglobaleconomywillcontinuetoslowandfinancialmarketswillcontinuetoremainvolatile. Thereisapath forward, but recent policy mistakes make it unclear if China willchoosewisely.Asthisprocessunfolds,investorsneedtoexerciseextremecaution.

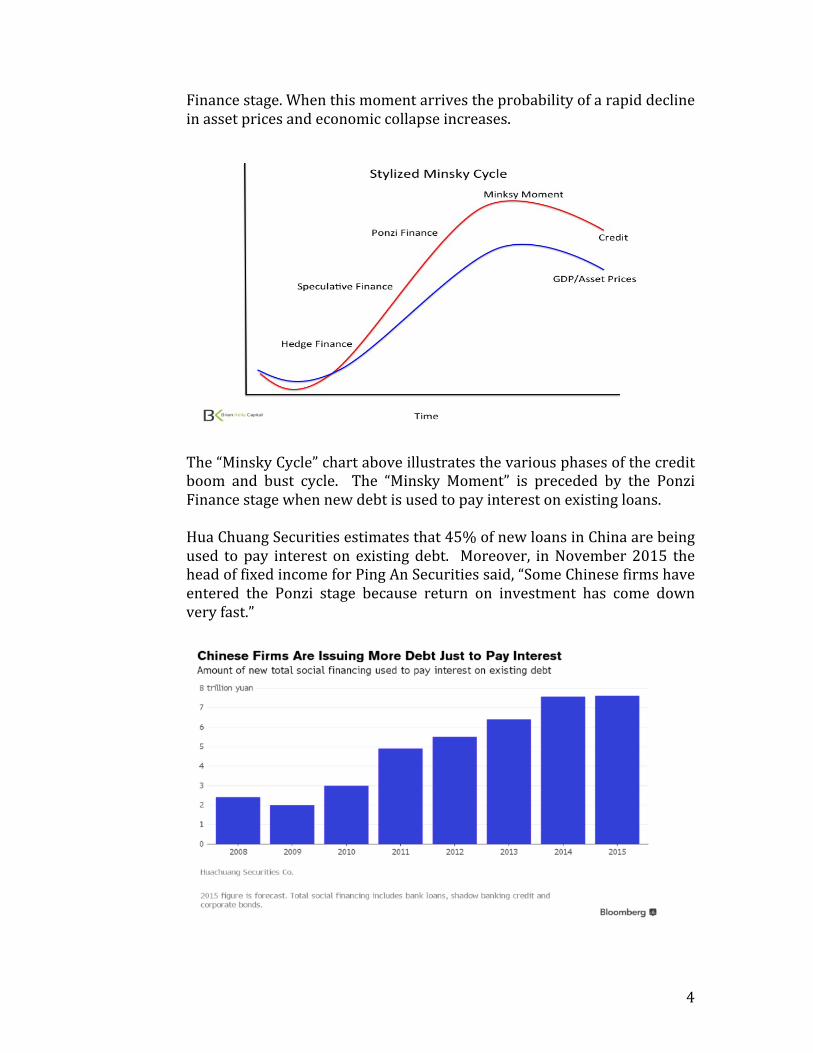

China’sMinskyMoment“…Itcanbeshownthatifhedgefinancingdominates,thentheeconomymaywell be an equilibrium-seeking and containing system. In contrast, thegreater the weight of speculative and Ponzi finance, the greater thelikelihoodthattheeconomyisadeviationamplifyingsystem.” -HymanMinskyMinsky’s analysis of credit cycles accurately describes the boom-bustperiods experienced by virtually all economies over time. A “MinskyCycle” reaches its climax when corporations or governments begin toborrowmoneytopayinterestonexistingloans,thisistheso-calledPonzi

4

Financestage.Whenthismomentarrivestheprobabilityofarapiddeclineinassetpricesandeconomiccollapseincreases.

The“MinskyCycle”chartaboveillustratesthevariousphasesofthecreditboom and bust cycle. The “Minsky Moment” is preceded by the PonziFinancestagewhennewdebtisusedtopayinterestonexistingloans.HuaChuangSecuritiesestimatesthat45%ofnewloansinChinaarebeingused topay interest on existingdebt. Moreover, inNovember2015 theheadoffixedincomeforPingAnSecuritiessaid,“SomeChinesefirmshaveentered the Ponzi stage because return on investment has come downveryfast.”

5

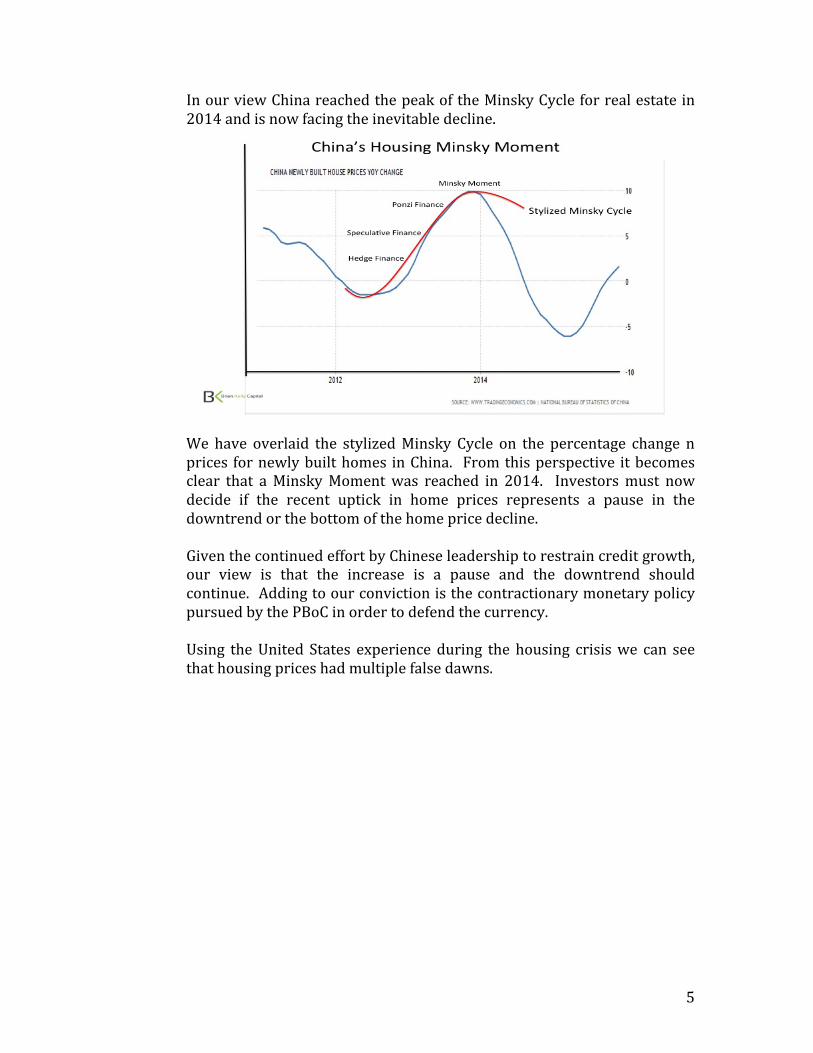

InourviewChinareachedthepeakoftheMinskyCycleforrealestatein2014andisnowfacingtheinevitabledecline.

We have overlaid the stylizedMinsky Cycle on the percentage change nprices fornewlybuilthomes inChina. Fromthisperspective itbecomesclear that aMinskyMomentwas reached in 2014. Investorsmust nowdecide if the recent uptick in home prices represents a pause in thedowntrendorthebottomofthehomepricedecline.GiventhecontinuedeffortbyChineseleadershiptorestraincreditgrowth,our view is that the increase is a pause and the downtrend shouldcontinue.AddingtoourconvictionisthecontractionarymonetarypolicypursuedbythePBoCinordertodefendthecurrency.Using theUnited States experience during the housing crisiswe can seethathousingpriceshadmultiplefalsedawns.

6

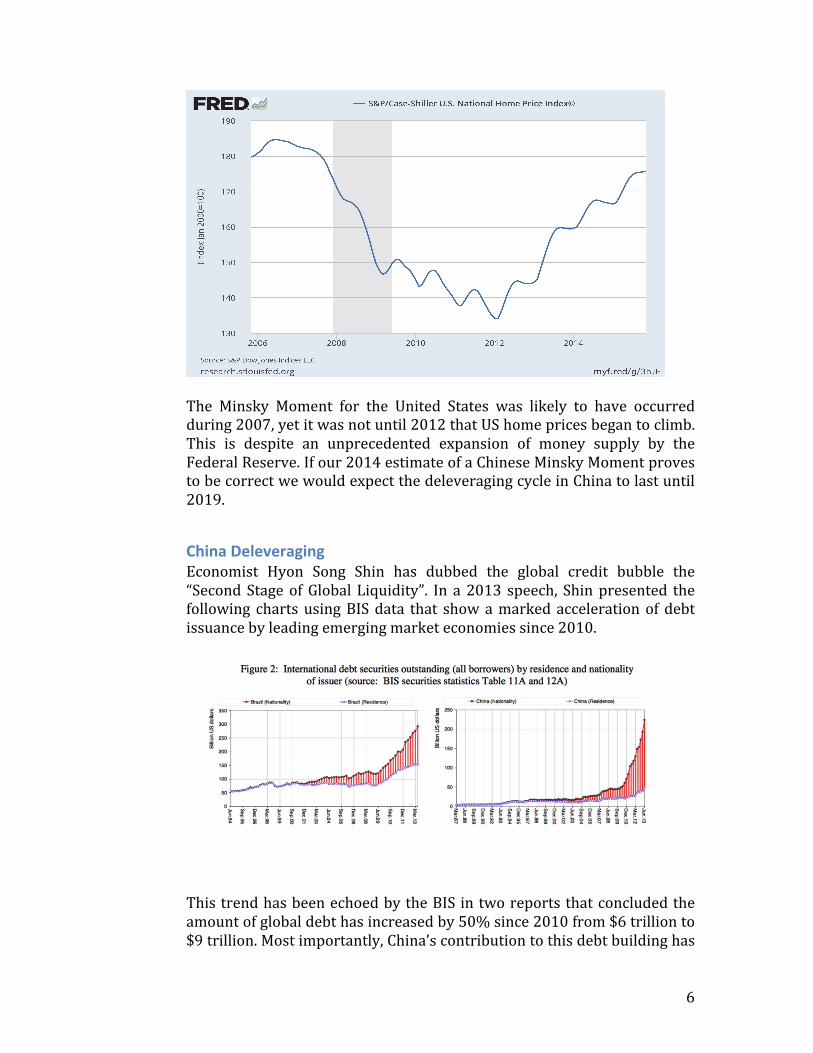

The Minsky Moment for the United States was likely to have occurredduring2007,yetitwasnotuntil2012thatUShomepricesbegantoclimb.This is despite an unprecedented expansion of money supply by theFederalReserve.Ifour2014estimateofaChineseMinskyMomentprovestobecorrectwewouldexpectthedeleveragingcycleinChinatolastuntil2019.

ChinaDeleveragingEconomist Hyon Song Shin has dubbed the global credit bubble the“SecondStageofGlobal Liquidity”. In a2013 speech, Shinpresented thefollowing chartsusingBISdata that showamarkedaccelerationofdebtissuancebyleadingemergingmarketeconomiessince2010.

ThistrendhasbeenechoedbytheBIS intworeportsthatconcludedtheamountofglobaldebthasincreasedby50%since2010from$6trillionto$9trillion.Mostimportantly,China’scontributiontothisdebtbuildinghas

7

increasedalmostfive-foldsince2009.

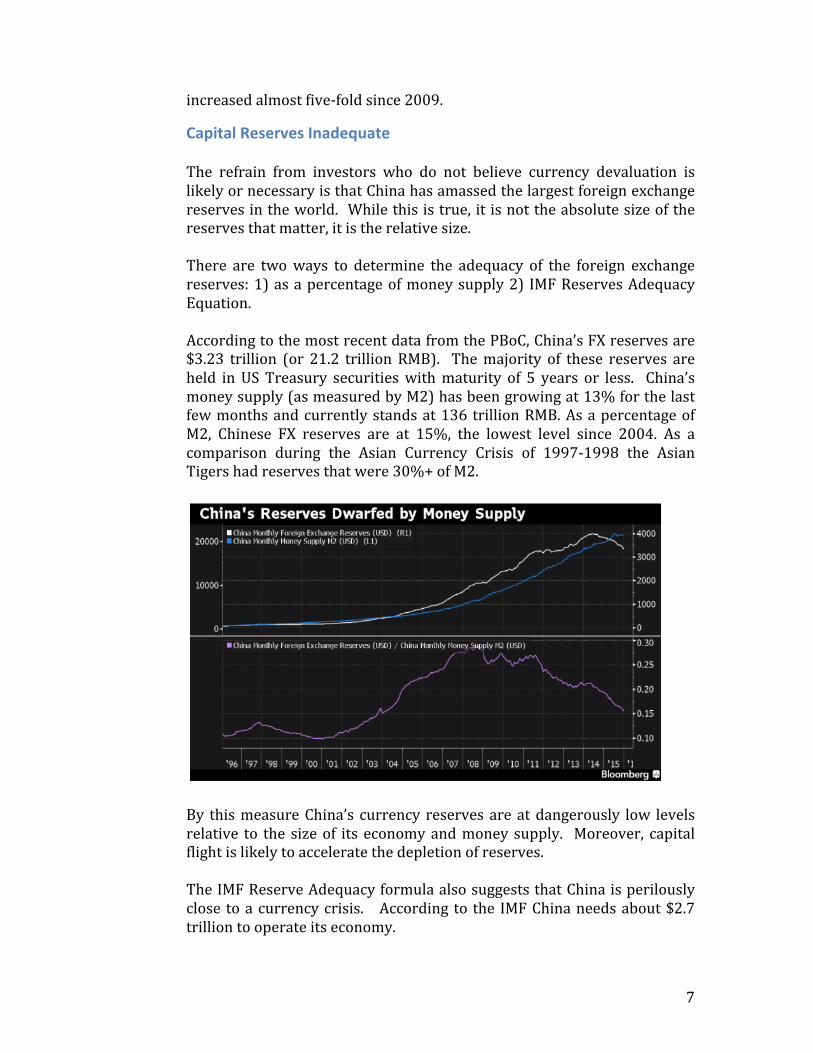

CapitalReservesInadequateThe refrain from investors who do not believe currency devaluation islikelyornecessaryisthatChinahasamassedthelargestforeignexchangereservesintheworld. Whilethisistrue,itisnottheabsolutesizeofthereservesthatmatter,itistherelativesize.There are twoways to determine the adequacy of the foreign exchangereserves:1)asapercentageofmoneysupply2) IMFReservesAdequacyEquation.AccordingtothemostrecentdatafromthePBoC,China’sFXreservesare$3.23 trillion (or 21.2 trillionRMB). Themajority of these reserves areheld inUS Treasury securitieswithmaturity of 5 years or less. China’smoneysupply(asmeasuredbyM2)hasbeengrowingat13%forthelastfewmonthsandcurrentlystandsat136trillionRMB.AsapercentageofM2, Chinese FX reserves are at 15%, the lowest level since 2004. As acomparison during the Asian Currency Crisis of 1997-1998 the AsianTigershadreservesthatwere30%+ofM2.

By thismeasureChina’s currency reservesareatdangerously low levelsrelative to the sizeof its economyandmoney supply. Moreover, capitalflightislikelytoacceleratethedepletionofreserves.TheIMFReserveAdequacyformulaalsosuggeststhatChinaisperilouslyclose toacurrencycrisis. According to the IMFChinaneedsabout$2.7trilliontooperateitseconomy.

8

ThismeansthatChinahasabout$500billionbeforeithitstheminimumlevel of reserves suggested by the IMF. This level of reserve adequacyplacesChinaamongtheworstinemergingmarketswithonlySouthAfrica,CzechRepublic,andTurkeywithlowerscores

The following chart compares the weakness in the South African Rand,CzechKoruna,TurkishLiraandtheRMB.

9

Since January 2014, the Rand has depreciated by 56%; the Koruna by20%; and the Lira by 35%, while the RMB has only fallen 8%. TheimplicationisthatonarelativebasisthereisroomfortheRMBtofallbyanother10-50%.

In2015,itisestimatedthatChineseFXreservesdeclinedby$1trillion,orabout $83b per month. The most recent official data from the PBoCpeggedJanuary2016outflowat$99.5b.Inanefforttobeprudentandconservativeweusetheaverageof$83bpermonth of outflows. Based on this level of outflows, China has about 7months before it effectively runs out of reserves. As the level of excessreserve approaches $3 trillionwewould expect the outflows to becomenon-linear.Therefore,theamountoftimebeforeChinaeffectivelydepletesitsreservesisprobablycloserto5months.It is not unreasonable to expect further capital flight even if Chinamanagestoengineerasoftlanding.Chinesecitizensareallowedtomoveamaximumof$50,000peryearfromChina.If5%ofChina’s1.3bpopulationdecidedtomovethisamountitwouldcompletelydepletethe$3.2trillionin reserves. Even more striking is that it would only take 1% of thepopulationoptingtosendthemaximumof$50,000outofChinatodepleteits$600bcushionbeforeitshitstheIMF’slowerbound.

DevaluationistheOnlyOptionTherearetwooptionsbesidesdevaluationthatChinamayuseorthatthemarketmaybecountingon:capitalcontrolsandSDRreservereallocation.In our view, neither of these will be enough for China to avoid adevaluation.

10

Chinacurrentlyhascapitalcontrolsthatarefamouslyporous. WewouldexpectChinatousecapitalcontrolsasafirstlineofdefenseasFXreservescontinue to be depleted. However,we do not expect capital controls tostemtheoutflow.AsanexporteconomytherearemanyopportunitiesforChinese companies and citizens to continue to use techniques like over-invoicingtosendcapitaloutofChina.Thesecond“hope”forChinaisforeignbuyingoftheRMBwhenitformallyenters the SDR in October 2016. Many have suggested that reservemanagerswillbuyRMBinordertobetteralignFXreserveswiththeratiosoftheSDRbasket.Itiscriticaltonote,thatSDRinclusiondoesnotrequirereserve managers to reallocate into RMB. Given the widespreadexpectation for continued RMB devaluation, it is unlikely that reservemanagerswillopttobuyRMBbeforedevaluation.Fromourperch, theonlyoptionChinahas isdevaluationandwewouldrecommendChinadevaluesoonerthanlater. Thelongertheywaittoactthe more disruption will occur. As well, with $3.23 trillion in reservesChinawouldexperienceawindfallprofitfromaone-off25%+devaluation.Previousepisodesofdeleveragingsuggestthat25%+devaluationislikelyandneededtoreducethedebtburden.Thefollowingtableshowspreviousdeleveragingperiodsand thecurrencydevaluationduring thatperiodoftime.WeexpectthatalargeRMBdevaluationcouldoccurin2016andwehavepositionedourselvesaccordingly.

DeleveragingPeriod CurrencyDevaluation

UnitedStates1930-1937 40% devaluation after peg togoldbroken

UnitedKingdom1949 Bank of England devalued by30%inSeptember1949

Thailand1997-1997 40%devaluationSouthKorea1997-1998 34%devaluationIndonesia1997-1998 83%devaluationUnitedStates2008 40%devaluationafterQE