rmb internalization and trade from china: opportunity for greater growth

TRANSCRIPT

RMB Internationalization and Trade

from China: Opportunity for greater

Growth

2 September 2015

Pat Antonacci, Managing Director – Pre-Sales & Services, SWIFT Americas

Jason Li, Director, Head of China Desk, Standard Chartered Bank

Session overview

Introductions

Market trends

Perspectives from Standard Chartered Industry developments impacting RMB

Financial institution and corporate use cases

SWIFT’s portfolio to support RMB

Questions?

LARC_RMB worksession 2

RMB is definitively growing…

3

RMB

Since

Jan

2013

+ 205% in payments

value

+ 268% in payments

volume

+ 14% Countries with

in/out payments (106)

+ 40% Financial

Institutions (1611)

+ 8 positions as world payments

currency

Payments value (MT103 and MT202 excl. COV) weight

Source: SWIFT Watch LARC_RMB worksession

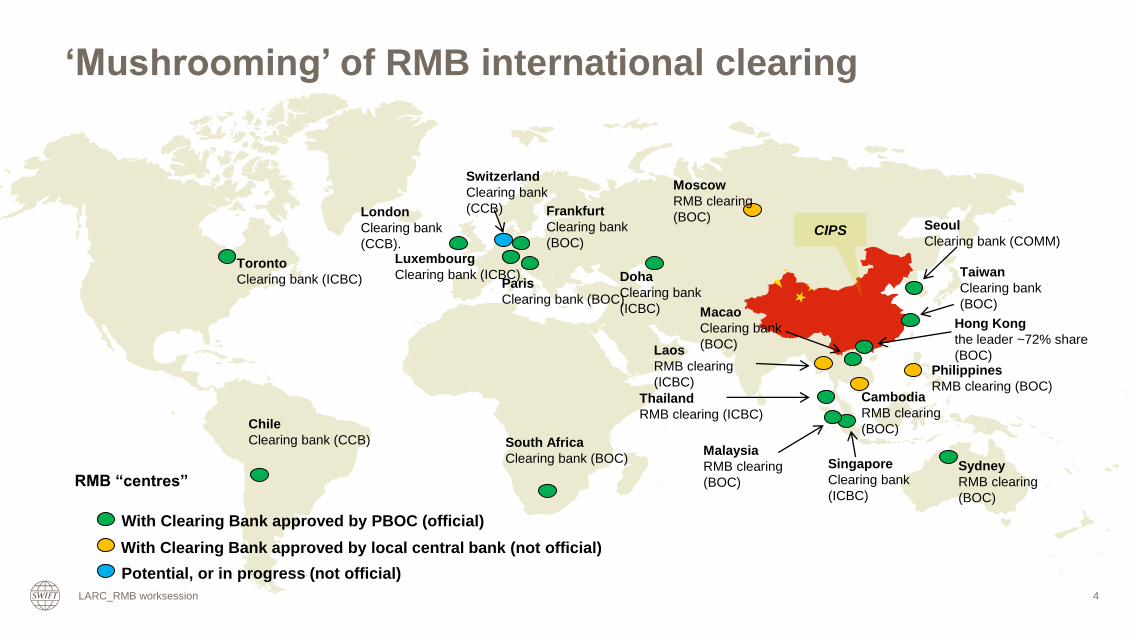

Hong Kong

the leader ~72% share

(BOC)

Thailand

RMB clearing (ICBC)

London

Clearing bank

(CCB).

Singapore

Clearing bank

(ICBC)

Luxembourg

Clearing bank (ICBC)

With Clearing Bank approved by PBOC (official)

Potential, or in progress (not official)

RMB “centres”

Taiwan

Clearing bank

(BOC) Macao

Clearing bank

(BOC)

Frankfurt

Clearing bank

(BOC)

With Clearing Bank approved by local central bank (not official)

Laos

RMB clearing

(ICBC)

Malaysia

RMB clearing

(BOC)

Cambodia

RMB clearing

(BOC)

Philippines

RMB clearing (BOC)

Moscow

RMB clearing

(BOC)

Paris

Clearing bank (BOC)

Seoul

Clearing bank (COMM)

Sydney

RMB clearing

(BOC)

Toronto

Clearing bank (ICBC) Doha

Clearing bank

(ICBC)

Switzerland

Clearing bank

(CCB)

‘Mushrooming’ of RMB international clearing

CIPS

4

Chile

Clearing bank (CCB)

LARC_RMB worksession

South Africa

Clearing bank (BOC)

RMB Payments RMB Securities

RMB Trade Finance RMB Treasury

YTD 2014

97,26%

2,74%

YTD 2013

98,48%

1,52%

YTD 2012

98,08% 1,92%

YTD 2014

71,73%

28,27%

YTD 2013

72,06%

27,94%

YTD 2012

84,00%

16,00%

YTD 2013

49,51%

50,49%

YTD 2012

52,68%

43,20%

56,80%

47,32%

YTD 2014 YTD 2014

99,91%

0,09%

YTD 2013

99,98%

0,02%

YTD 2012

99,98%

0,02%

% of

international

RMB excl. CN/HK

% of international RMB

incl. CN/HK

RMB evolution per business area Growth and Proportion of Truly Offshore RMB*

LARC_RMB worksession * International RMB flows sent and received in value – October 2014

RMB Tracker

5

RMB Index

RGI fell 0.8% in April 2015

LARC_RMB worksession 6

SWIFT Monthly RMB Tracker Monthly reporting and statistics on renminbi

(RMB) progress towards becoming an

international currency

Launched November, 2011

LARC_RMB worksession 7

Perspectives from Standard Chartered

Jason Li, Director, Head of China Desk, Standard Chartered Bank

LARC – China update

September 2015

Standard Chartered

71 Footprint Markets markets in

Americas

markets in

Europe

markets in

Africa

markets in

MENAP

markets in

South Asia

10 14 15 10 4

markets in

Greater

China

markets in

North East Asia

markets in

ASEAN

3 4 11

Standard Chartered Presence

Reported results

Profit before tax

$5,193m FY 2013: $6,958m

Loans and advances to customers

$289bn FY 2013: $296bn

Customer deposits

$470bn FY 2013: $435bn

Capital and liquidity metrics

Common Equity Tier 1 (transitional) ratio

10.5% FY 2013: 10.9%

Common Equity Tier 1 (end point basis) ratio

10.7%

FY 2013: 11.2%

Liquid asset ratio

32% FY 2013: 29.8%

Over 150 years in the world’s most dynamic markets

Financial highlights For the full year 2014

Strong credentials

Primary listings in London,

Hong Kong and Mumbai

top 20 in FTSE 100 Index

We bank the people and

companies driving investment,

trade and the creation of wealth

across Asia, Africa and the

Middle East.

Credit ratings

A+/Aa2/AA-

S&P/Moody’s/Fitch

China – Is the glass half full or half empty?

Where are we today?

2011 2012 2013 2014 2015F 2016F

GDP growth, % 9.2 7.7 7.7 7.3 6.9 6.8

CPI, % 5.4 2.6 2.6 2.0 1.6 2.1

1-yr base saving rate, % 3.50 3.00 3.00 2.75 2.25 2.25

Current account, % of GDP 1.9 2.3 2.1 2.3 2.8 2.9

USD-CNY (year end) 6.301 6.28 6.05 6.21 6.50 6.35

Source: Standard Chartered Research

Our macroeconomic views

CNY – Recent devaluation does not really support exports

Standard Chartered Research

Substantial progress in Internationalizing the RMB

• China is the world’s largest trade

country ($4.3 trn)

• About 27% of China’s own trade now

settled in RMB

• Fully liberalized RMB cross-border

current account movement

• Become world’s 5th most used

payment currency since Jan 2015

(SWIFT data)

• RQFII granted to 13 countries/ regions

with quota amounted to RMB970Bn

• China Interbank Bond Market

• CNH Bond Market: Outstanding: RMB

742bn

• Shanghai – HK Stock Connect launched

on 17 Nov 2014

• Mutual Recognition of Funds to be

launched on 1 July 2015

• IMF will discuss and vote if RMB

should be included in the Special

Drawing Right (“SDR”)

• >60 central banks has hold RMB as

part of their foreign reserve

• 32 Central Banks have signed

Bilateral Swap Agreement with

PBOC

Longer Term

Direction

Gradual Currency /

Financial Reform

Interest rate

liberalization

FX Convertibility

Continued opening of

Capital Account

Investment

Currency

Trade

Currency Reserve Currency

Driven by RMB Trade Settlement

The use of RMB for trade settlement has increased more than 7 times since 2011.

RMB as a % of World Payment Currencies

October 2011 through December 2014

2.17%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-14

16 Source: SWIFT RMB Tracker January 2015

Growing Liquidity in Offshore RMB Hubs

17

Accumulation of RMB in the offshore market remains strong, with close to CNH 1.7 trillion of deposits in the six main RMB hubs.

Source: HKMA Monetary Statistics (December 2014 Issue); Central Bank of the Republic of China (Taiwan) (15-Jan-15); Monetary Authority of Singapore; Bank of Korea; Paris Europlace; City of

London

1,004

302 257

120

20 19

0

200

400

600

800

1,000

1,200

HK… Taiwan… SG… S. Korea… France… London…

CN

H D

ep

os

it V

olu

me

s (

Bn

)

Offshore RMB

Convert to FCY Keep in RMB

FX Hedge:

FX Swap

Cross Currency Swap

FCY Inter-

Company

Loan

FCY Deposit

Current

Account

(FCY)

Time

Deposits

(FCY)

Invest in

Mainland

Capital

Markets

Current

Account

(CNH)

CNH Deposit

Invest in

CNH

Securities

Trade

Settlement

CNH to

Working

Capital /

Liquidity

Manage

Liquidity

MCY

Notional Pool

Regional

RMB Cash

Pool

Time

Deposits

(CNH)

Structured

Investment

(CNH)

CNH Bonds

Interest

Optimize

Government

Bonds

CNH CDs

CNH

Discount

Notes Corporate

and

FI Bonds

RQFII

SH-HK Stock

Connect

Shanghai

Gold

Exchange

Offshore uses of RMB expanding rapidly

Where are we going? Key drivers for Renminbi

■ New Free-Trade Zones and offshore RMB centers

Three new FTZs and expansion of Shanghai

Up to 10 more offshore RMB centers this year, including Toronto and possibly LatAm

■ Trade settlement volumes continue to increase

Over 25% of China trade and growing

Already the dominant currency for trade between China and KR, PH, SG, TW

■ Investments boosting settlement volumes

Shanghai-Hong Kong Stock Connect already live

Shenzhen-Hong Kong targeted by end of year

■ Push to add RMB to IMF Special Drawing Rights status

Will lead to a surge of interest for RMB assets, especially Bonds

Key drivers for Renminbi

Offshore RMB Clearing Centers

21

• Current RMB clearing centers

• Potential RMB clearing centers

RMB clearing centers are emerging across the globe, providing direct access to RMB settlement outside China.

China continues to announce new RMB clearing banks as it expands the use of RMB outside its borders.

The recently announced RMB clearing banks in Europe, Asia, and Middle East will expedite the adoption of the RMB as a trade settlement currency in these

regions.

RMB Clearing Centers across the Globe PBOC-designated Clearing Banks by Location

Americas Europe Asia

Toronto Frankfurt

London

Luxembourg

Paris

Zurich

Bangkok

Doha

Dubai (in discussions)

Hong Kong

Kuala Lumpur

Macau

Taiwan

Seoul

Singapore

Sydney

As of 6-Feb-15

Clearing Center Clearing Bank Remarks

Hong Kong Bank of China RMB clearing services launched on Feb-04

Macau Bank of China Appointed by the PBOC on 4-Aug-04

Taiwan Bank of China RMB clearing services launched on 6-Feb-13

Singapore ICBC RMB clearing services launched on 27-May-13

London China Construction Bank RMB clearing services launched on 29-Jul-14

Seoul Bank of Communications RMB clearing services launched on 6-Nov-14

Frankfurt Bank of China RMB clearing services launched on 17-Nov-14

Paris Bank of China RMB clearing services launched on 3-Dec-14

Luxembourg ICBC RMB clearing services launched on 4-Dec-14

Doha ICBC Appointed by the PBOC on 2-Nov-14

Toronto ICBC Appointed by the PBOC on 3-Nov-14

Sydney Bank of China Appointed by the PBOC on 14-Nov-14

Kuala Lumpur Bank of China Appointed by the PBOC on 5-Jan-15

Bangkok ICBC Appointed by the PBOC on 5-Jan-15

Zurich TBD MOU signed on 21-Jan-15

Benefits of an RMB Clearing Bank

Direct access to onshore RMB liquidity

Access to RMB clearing services in the same time zone

Greater operational efficiency for companies and banks seeking to use RMB

denominated services

Capture regional RMB flows by leveraging trade linkages with China

Sustainable and increasing use of RMB for China’s trade

Over 25% of China’s trade redenominated into RMB – already the

dominant currency for trade with Korea, Philippines, Singapore, Taiwan

IMF reviewing CNY for inclusion in the SDR

The IMF SDR review is an important near-term

consideration for the CNY

The Cross Border Interbank Payment System (CIPS) is a new clearing

platform for cross-border RMB settlement

Phase 1 rollout expected in Q4 2015 – 20 banks part of the first batch

including Standard Chartered

CIPS will become the only channel for international RMB clearing while

CNAPS will be the national RMB clearing

Banks will need to process cross-border RMB transactions through a CIPS

member bank

Extended settlement windows (09:00–20:00)

Real-time gross settlement

Will support both Chinese and English characters

Overview

Cross-Border Interbank Payment System (CIPS)

What to

expect

CIPS will become a CHIPS for Renminbi

Increase of China’s world GDP % will result in growing exposure

USA

CHINA

GDP IN

2010

USA

CHINA

PROJECTED GDP BY

2030

Percentage of World GDP

24%

10% 17%

24%

Source: Standard Chartered Research

What are we seeing?

■ 35% of China trade to be denominated in RMB by 2020

■ 83% of respondents already use at least one offshore RMB product

■ Three in ten clients intend to leverage China FTZs

■ Of these, one third plan to do cross-border RMB liquidity management

■ CNH usage – Primarily for deposits, trade, and FX

■ About 30% prefer to settle trade in RMB (exports & imports) vs 15% for USD

■ Trade continues to be driven by FX risk management, cost savings, requests from offshore

buyers

Our latest corporate survey

Offshore

Parent or

Affiliate

China

Pool Header

PP PP PP

Offshore

Borrower or

Cash Pool

Corporates – Incorporating China into Asia liquidity management

Two-way Lending (Shanghai Free Trade Zone)

Eligibility

Corporates with an entity in the FTZ

FTZ entity as China pool header links with offshore entities

Benefits

No quotas for outflows or inflows

Fund inflows can exceed outflows

Inflows do not consume Borrowing Gap or Foreign Debt Quota

FTZ

Entrust

Loan Loan

China (non-FTZ)

Two-way Lending (pan-China)

Eligibility

Annual cross-border FCY volumes > USD 100 Mn

Lend up to 50% of equity of onshore entities or borrow up to their aggregate

Foreign Debt Quota

Benefits

Consolidates FCY from various China accounts

No FTZ entity required

Unlocks trapped China cash / Bring funds into China

Loan

Two-way Lending (pan-China)

Eligibility

China entities throughout China

Bring in up to 10% of total equity of onshore entities

Benefits

Does not consume FDQ

No FTZ entity required

Unlocks trapped China cash / Bring funds into China

Offshore

Borrower or

Cash Pool

Loan

RMB Pool Header Pool Participants

China

Single entity or

Cash Pool

Corporates – Re-denominating settlements with China

Clients are leveraging Renminb invoicing to:

2

• Reduce administrative burden 3

• Improve margins 1

• Grow market share

-----------

-----------

-----------

-----------

-----------

-----------

-----------

-----------

-----------

-----------

-----------

-----------

No access to Offshore Renminbi investment market and lack of hedging options

Onshore CNY

Cannot access onshore FX and deposit options

Offshore CNH

“Best of Both Worlds”

CNY nostro in China & CNH nostro in Hong Kong

Onshore investments

Onshore FX market

Direct access to CNAPS

No restrictions on usage

Abundant RMB investment options

Full array of FX hedging options

Banks – Opening both CNY and CNH nostros

■ Incorporating China into regional/global liquidity management

Regulatory liberalization from both RMB and FCY fronts

Excess cash is no longer a problem

How do I bring funds into China?

■ FX management increasingly necessary

Increased RMB volatility likely to continue

Explosion of hedging options

Local vs centralized FX risk management?

■ Should my company re-denominate into RMB?

Cost-benefits are worth exploring

What is the impact - ERPs, accounting, etc.

Extending to third party settlements

Key takeaways – Corporates

■ Large international banks are at the head of the pack

Challenge is to keep up with regulatory changes

Client RMB cross-border volumes picking up

CIPS launching by end of 2015

■ Smaller international banks have basic linkages in place

Initial CNY/CNH nostro accounts opened in China and Hong Kong

Training sales staff and corporate clients

Individual settlements not coming soon

■ Investors & Intermediaries – Leaped ahead of the game

Shanghai-HK StockConnect already live, Shenzhen-HK is next

Numerous reforms in Free Trade Zones (e.g. Gold Exchange in Shanghai FTZ)

UK issues first RMB bond

Key takeaways – Financial institutions

LARC_RMB worksession 33

Questions?

LARC_RMB worksession 34

SWIFT’s Portfolio supporting your RMB

strategy

SWIFT Economics Economic Indicators

Support Decision-Making

RMB Tracker The SWIFT Index RMB Market

Insights

LARC_RMB worksession 35

Watch analytics Dynamic search and analysis of business data only

SWIFT can provide

Watch

Traffic Analytics

Watch Message

Cost Analytics

Watch

Value Analytics Watch Billing

Analytics

LARC_RMB worksession 36

Watch analytics Dynamic search and analysis of business data only

SWIFT can provide

LARC_RMB worksession 37

Watch Insights Visual and business-oriented dashboards

Pre-defined, yet dynamic

Payments &

Cash Management Payments &Trade

Finance

Manage

correspondent

network

Trade Finance

Develop

footprint and

portfolio

Develop

footprint and

portfolio

Your top cash management

messages sent and received YTD

The evolution of the number of

counterparties and countries you

have activities with

Your activity share in MT700 YTD

and its variations compared to last

year

LARC_RMB worksession 38

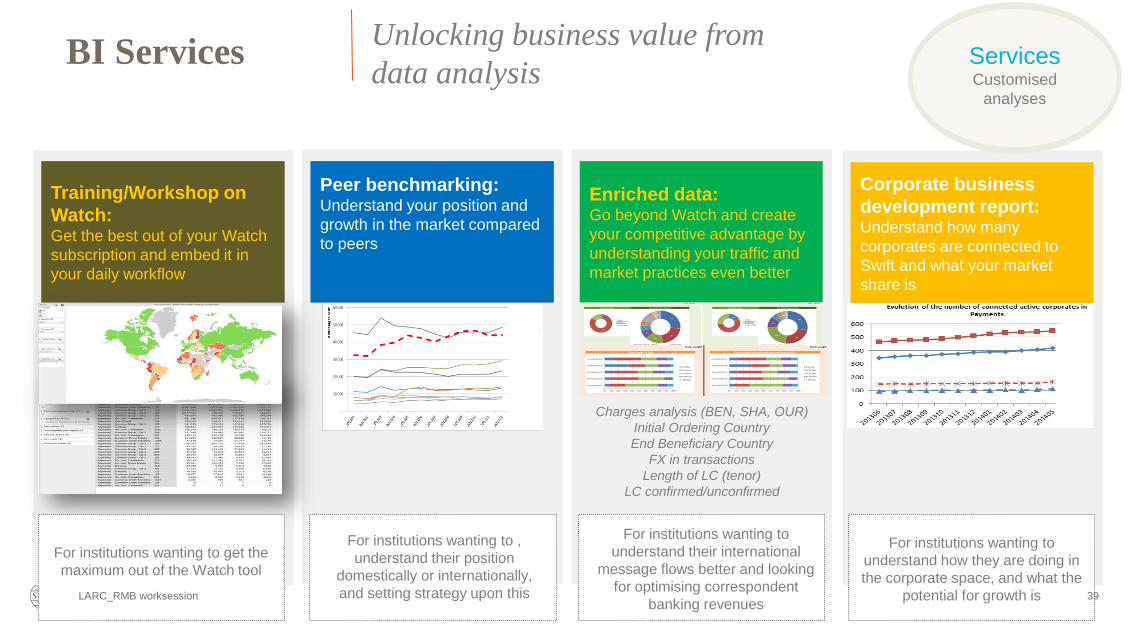

Charges analysis (BEN, SHA, OUR)

Initial Ordering Country

End Beneficiary Country

FX in transactions

Length of LC (tenor)

LC confirmed/unconfirmed

Peer benchmarking: Understand your position and

growth in the market compared

to peers

Enriched data: Go beyond Watch and create

your competitive advantage by

understanding your traffic and

market practices even better

Training/Workshop on

Watch: Get the best out of your Watch

subscription and embed it in

your daily workflow

Ordering option Top 10 Ordering Country Ordering option Top 10 Ordering Country

Initial ordering Initial ordering

4%

81%

15%

Blank

Option A

Other options

27%

22%

15%

8%

6%

5%

5%

5%4% 3%

United Arab Emirates Russia United States

Ukraine Turkey Kazakhstan

United Kingdom Poland Tajikistan

Uzbekistan

18%

55%

27%Blank

Option A

Other options

28%

24%23%

11%

5%

3%3%1%1%1%

United Arab Emirates Uzbekistan Russia

Cyprus Azerbaijan Armenia

Switzerland Kyrgyzstan Czech Republic

TajikistanTenor Length in 2013 Tenor Length with preferred correspondents in 2013

Tenor Length Tenor Length

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Correspondent E

Correspondent D

Correspondent C

Correspondent B

Correspondent A

0-30 days

31-60 days

61-90 days

91-180 days

> 180 days

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Correspondent E

Correspondent D

Correspondent C

Correspondent B

Correspondent A

0-30 days

31-60 days

61-90 days

91-180 days

> 180 days

Corporate business

development report: Understand how many

corporates are connected to

Swift and what your market

share is

For institutions wanting to get the

maximum out of the Watch tool

For institutions wanting to ,

understand their position

domestically or internationally,

and setting strategy upon this

For institutions wanting to

understand their international

message flows better and looking

for optimising correspondent

banking revenues

For institutions wanting to

understand how they are doing in

the corporate space, and what the

potential for growth is

Services Customised

analyses

BI Services Unlocking business value from

data analysis

LARC_RMB worksession 39

SWIFT Business Intelligence offering for RMB

40 LARC_RMB worksession

Thought Leadership Learn how SWIFT can support or engage with the Industry on several aspects relative to the

RMB internationalisation through White papers, conferences, articles, and much more.

Public

(for free)

Monthly RMB Tracker Monthly reporting and statistics on renminbi

(RMB) progress towards becoming an

international currency

Public

(for free)

RMB Market Insights .

BI Engagements - Customised RMB Analyses The Quarterly RMB Tracker, providing market data, can be extended to provide business insights

on RMB activity to build TRUST and INTIMACY with the specific business lines

SWIFT customers

(payable offers)

Strategic decisions within RMB Market Insight reports

Develop your business

Identifying cross border payments opportunities with China

Designate investments accordingly

Risk Management

Support Expansion of business activities:

o Transaction Banking

o Treasury

o F/X

o Implementation

o Customer Service

Drive workforce

Measure results

LARC_RMB worksession 41

Want to know more?

SWIFT enables YOU to gain unique insights at any time on the RMB progresses

in becoming an international currency:

- Market intelligence

- Your financial institution activity

- Your activity share and/or peer benchmark

42

Business Intelligence Transaction Banking

#SWIFTBI

Key resources for more information:

- Business Intelligence solutions

LARC_RMB worksession

SWIFT Latin American Regional Conference 1-2 September 2015 43

Questions.

SWIFT Latin American Regional Conference 1-2 September 2015 44

Digi-voting

SWIFT Latin American Regional Conference 1-2 September 2015

On a scale of 1 to 5 please rate your level of satisfaction with

this session.

Lowest Highest

45

SWIFT Latin American Regional Conference 1-2 September 2015

On a scale of 1 to 5 please rate your level of satisfaction with

the session speakers.

Lowest Highest

46

SWIFT Latin American Regional Conference 1-2 September 2015 47

Agenda what’s next

• Plenary: 12:30

www.swift.com

LARC_RMB worksession 49

LARC_RMB worksession

Sample graphs and tables from RMB Market Insights

50

51

61 76

May-13 May-15

+25%

526

450

May-15 May-13

+17%

May-15 May-13

114

87

+31%

+26%

290

365

May-13 May-15

+22%

May-15 May-13

1,081

888

Share of RMB

users

22% 28% 33% 37% 27% 37% 26% 33% 29% 35%

RMB growth over the years in Payments Number of Financial Institutions, International flow sent and

received directly with China and Hong Kong

LARC_RMB worksession

Ready for RMB?

More than 1,400 Financial Institutions in over 100 countries are already

doing business in the Chinese currency: the Renminbi (RMB).

Is yours one of them?

Are you looking to understand more about RMB internationalisation, or

further expand your RMB business?

Or, are you still trying to figure out what the internationalisation of the RMB

means for your bank?

LARC_RMB worksession 52

LARC_RMB worksession 53

Market trends

Increased globalization

Currency devaluation

Growth in Trade and Supply Chain

Remittances