11 Portfolio Committee; 10 September 2013

SAPA Presentation

to the

Portfolio Committee

on Agriculture, Forestry and Fisheries

10 September 2013

12 Portfolio Committee; 10 September 2013

1. The local poultry industry is vital to South Africa

2. It is devastated by dumped imports, which are the portions the developed world doesn’t want

3. The media battle has been won by Amie, but the real war is for food security and jobs

4. Countries worldwide protect their industries in many ways

5. South Africa is an efficient producer of chicken

6. And imports contain significant risks

7. Brining has been on many peoples lips

8. Tariffs will not cause exploding local prices

9. And SAPA is stepping up transformation

SAPA’s story

13 Portfolio Committee; 10 September 2013

Poultry is more than 65% of South African consumed animal protein and is the

biggest grocery category in South Africa

It is the single largest part of agriculture in South Africa – almost ¼ of

agricultural GDP

It is the second biggest user of local maize and the major user of soy beans

It is core to South Africa’s food security

Animal products in general represent the major growth area for local agriculture

It employs 50 000 people directly and 60 000 indirectly plus 18 000 in the grain

industry

Poultry meat generates R30 billion in local farm gate revenue, and about R1

billion in corporate taxes in a normal year (excluding all the VAT generated in the

value chain). If it collapsed R30bn in foreign exchange would be lost to SA to

imports

1. The local poultry industry is vital to South Africa

14 Portfolio Committee; 10 September 2013

The industry is in crisis. Latest published company audited results show…

Astral SA chicken business -180% loss (results to March)

Country Bird Holdings SA chicken business -150% loss(results to June)

Rainbow Chicken SA chicken business -103% loss (results to June)

Afgri SA Poultry -R229m loss (results to June)

Jobs are being lost and businesses are downscaling or closing (eg Darling, Argyle, Berwin, Sangiro are gone or in business rescue)

Why is this happening?Traditional exporters like Brazil/Argentina/Thailand continue to grow while a global

recession is underway

Traditional importers like Russia and China are becoming self sufficient due to food security concerns

….and therefore Africa has become a greater target for the developed world’s unwanted surpluses

2. It is devastated by dumped imports, which are the portions the developed world doesn’t want

15 Portfolio Committee; 10 September 2013

And this is what is happening

2. It is devastated by dumped imports, which are the portions the developed world doesn’t want

Breast meat and wings are desired by the developed world and exporters (eg Brazil, Argentina and EU countries in surplus) make their money out of these portions

Leg quarters are not desired and they are sold for whatever price they can get (From R6/kg to R16/kg over the last year (Sars): almost always lower than what they sell the same thing for in Brazil and EU ie: dumped)

16 Portfolio Committee; 10 September 2013

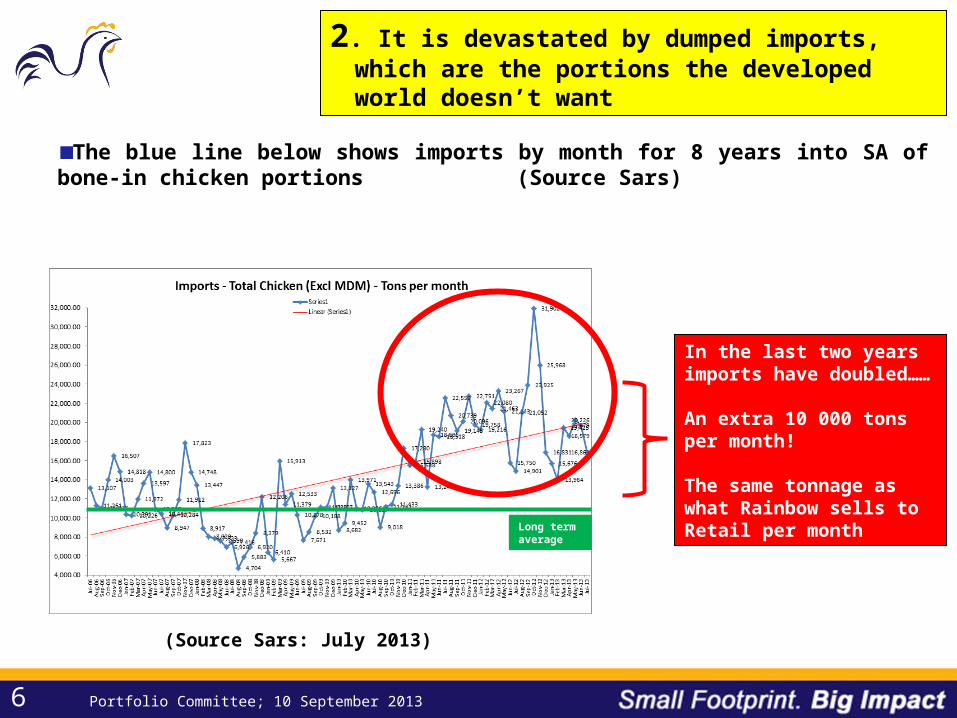

The blue line below shows imports by month for 8 years into SA of bone-in chicken portions (Source Sars)

2. It is devastated by dumped imports, which are the portions the developed world doesn’t want

(Source Sars: July 2013)

In the last two years imports have doubled……

An extra 10 000 tons per month!

The same tonnage as what Rainbow sells to Retail per monthLong term

average

17 Portfolio Committee; 10 September 2013

The EU is the major problem with respect to dumped bone in chicken pieces (Source Sars)

2. It is devastated by dumped imports, which are the portions the developed world doesn’t want

(Source Sars: July 2013)

EU 45%

2011 Bone in chicken imports2013

EU 74%

18 Portfolio Committee; 10 September 2013

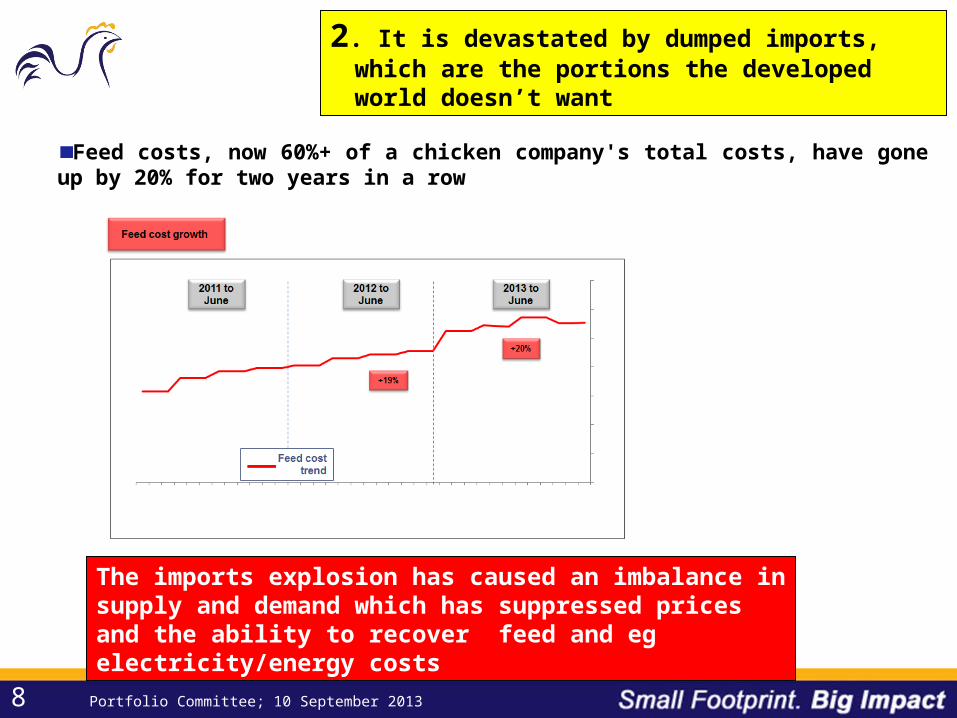

Feed costs, now 60%+ of a chicken company's total costs, have gone up by 20% for two years in a row

2. It is devastated by dumped imports, which are the portions the developed world doesn’t want

The imports explosion has caused an imbalance in supply and demand which has suppressed prices and the ability to recover feed and eg electricity/energy costs

19 Portfolio Committee; 10 September 2013

The meat importing industry employs only a few thousand people

All other jobs referred to by them are in logistics and selling that would be retained if the imported volume is replaced by local production

Food security has become one of the Worlds primary agricultural drives. Chicken imported today at very low prices may well become unavailable or very expensive tomorrow if exporters find countries prepared to pay more!

There are 110 000 jobs at risk directly and indirectly, and this excludes the grain farming industry in South Africa.

After people, chicken farming consumes the most maize and soya in SA. This industry would likely collapse if poultry does, as there is not enough

infrastructure to export South Africa’s grain production

SA manufacturers profits go into three things:-- payment of taxes- dividends to institutional shareholders ie PIC (if there is any profit)- and the rest is fully reinvested in the SA poultry industry (no-one sits on cash)

Importers contribution to the above is minimal

3. The media battle has been won by Amie, but the real war is for food security and jobs

110 Portfolio Committee; 10 September 2013

4. Countries worldwide protect their industries in many ways for food security and jobs reasons

The world trade in agriculture is highly distorted

Countries rely on 1. trade measures and 2. SPS (Sanitary and Phyto-sanitary barriers)

1. Trade MeasuresOur tariffs are low by world standards

For example tariffs/kg for bone in cuts:-

South Africa R2.20

EU R5.06

Canada 238% (+-R38)

Switzerland 63% (+-R10)

Developing countriesIndonesia 20% (+-R3)

Egypt 30% (+-R5)

India 100% (+-R16)

Russia 32% (+-R5)

111 Portfolio Committee; 10 September 2013

4. Countries worldwide protect their industries in many ways for food security and jobs reasons

2. SPS (Sanitary and Phyto-sanitary barriers)

A few examples of SPS currently

Brazil – does not approve any of our abattoirs for export to them

China – all abattoir approval worldwide was withdrawn and countries had to reapply

Russia – restricted imports by 50% last year (WTO report)

EU – no SA abattoirs are approved for export to them. They have also banned all poultry because of Ostrich flu here

Australia and New Zealand – bans all poultry imports

Our neighbours: Namibia – recently introduced a small quota: Botswana – permit required but none made available: Zimbabwe – no imports from SA due to Ostrich flu : Mozambique – permit required but none made available

Nigeria and Kenya – borders closed to all poultry imports due to local industry prioritised

Clearly, the world uses these barriers as a less emotive way of restricting trade

112 Portfolio Committee; 10 September 2013

5. South Africa is an efficient producer of chicken

South Africa is an efficient producer of poultry, slightly behind Brazil but ahead of USA

But we are disadvantaged on cost of grain due to logistics, subsidies and tariff realities which grain exporters levy. This is out of our industry control

SA manufacturers have had a more than doubling cost of electricity in 4 years, not experienced by exporters

SA producers are the lowest cost sellers into the KFC system worldwide! - a strong signal of efficiency Source: KFC

Maize and soya make up 80% of feed cost

113 Portfolio Committee; 10 September 2013

6. And imports contain significant risks

In South Africa1200 abattoirs are approved for export to South Africa. None of these have been

personally visited by South African officials

South African abattoirs are constantly overseen by state vets

There is thus a huge food safety and health disparity between local and imported chicken

Sapa has sampled and independently tested 80 samples of imported chicken pieces in the last 8 months for unacceptable contamination

The results reported relate only to the samples tested.

(Total sample sets to date = 80)Test methods are all SANAS Accredited with the exception of PCR tests.

Results

114 Portfolio Committee; 10 September 2013

7. Brining has been on many peoples lips

Why brine?

• Brining is an international practise for many meat products (bacon, ham, chicken)• When frozen chicken defrosts it loses moisture which needs replacing• Quick Service Restaurants (KFC, Chicken Licken etc) request their global standard for

moisture addition of 15-20% for succulence and flavour reasons (despite it costing them more)

• In blind independent taste tests, all local consumers prefer brined product• It is safe, technically supported and consumers prefer it

Sapa acknowledges governments desire to cap brining and has already submitted a Code of Practise proposal to Daff proposing a moisture cap and a monitoring proposal

Sapa is keen to work with Daff on a brine/moisture level cap that all stakeholders find acceptable

Contrary to their media blitz, some of the biggest importers have been importing, defrosting and injecting at very high levels

115 Portfolio Committee; 10 September 2013

7. Brining has been on many peoples lips

If we exclude brine from South African Individually Quick Frozen, compared to all other forms of imported and local chicken, brined IQF is actually the cheapest chickenCURRENT ADVERTISED

FrozenBrined

IQF

Imported Leg

Quarters

FreshBraaiPack

FreshSkinlessFillets

VALUE PROPOSITION

70/30Meat / Fat & Skin Grams 489.7 703.7 703.7 1 000.0 Bones Grams 214.3 296.3 296.3 - Brine Grams 296.0 - - - Total content Grams 1 000.0 1 000.0 1 000.0 1 000.0 On shelf price RSP kg 17.00 29.99 29.99 46.99 Excluding brine & bones RSP kg 34.70 42.62 42.62 46.99 Protein Content Grams 91.08 130.89 130.89 213.90 % 13.94% 18.60% 18.60% 21.39%

R/kg index 81% 100% 100% 96%

Composition values can vary depending on product mix and bird size

116 Portfolio Committee; 10 September 2013

8. Effects of Tariffs: Tariffs do not cause exploding local prices

Only five categories of poultry imports are applied for. (MDM or mechanically deboned meat, which is one third of all poultry imports is not applied for)

The tariff on each varies according to the price suppression level

The SA poultry industry has been selling frozen chicken in 2013 for prices below two years ago, despite massive cost increases in feed

Sapa has commissioned three price effect analyses (Genesis Analytics). The most likely effect is less than 10% price increase. This will only go part way to covering feed cost inflation

Unfortunately, these tariffs won’t affect the bulk of bone in imports which come from the EU

117 Portfolio Committee; 10 September 2013

9. Sapa is stepping up transformation

Developing farmers are struggling as much, or more than large companies

Governments investment plan in agri land reform will be unsustainable due to poultry imports and dumping

Sapa has a Developing Farmers Poultry Organisation (DPFO), with 270 members (60% have had to close) and a national executive committee whose members sit on all Sapa bodies.

Sapa and the industry are progressing a Transformation workstream with Government departments and individuals like Dr Zweli Mkhize

This involves transformation at industry level (Sapa), as well as company level

Sapa is keen to step up the pace of this with key government decision makers, and we need momentum from government as well to assist us

118 Portfolio Committee; 10 September 2013

Survive the current crisis

Grow

Transform

Improve skill levels

Try to open export markets with Government assistance

Support the rural economy

Industry future plans

119 Portfolio Committee; 10 September 2013

We ask that the Portfolio Committee help us by persuading all relevant Ministries and sector departments to:

Help enforce SPS phytosanitary measures;Act more aggressively against illegal imports and exports; Ensure compliance at all ports of entry, especially Durban Treat SAPA as partners with regular communications and meetings – and not as enemies;Open the doors of engagement with governmentBe candid, open minded and transparent when dealing with SAPA for the betterment of long-term good relationships;Help us deal with high input costsImprove the regulatory framework; andImprove food security.

120 Portfolio Committee; 10 September 2013

Thank You

eNkosi

Dankie

Re a Leboga