dof asa q3 2010 asa/ir/archive/2010_q3_dof_asa_pres.pdfdof asa presentation q3 2010 - 8 the new...

TRANSCRIPT

DOF ASA PRESENTATION

Q4 2009

The New Horizon

DOF ASAQ3 2010

CEO – Mons S. Aase CFO – Hilde Drønen

DOF ASA PRESENTATION

Q3 2010 - 2

The New Horizon

Agenda

Highlights Q3

Overview Group

Status DOF Subsea

Status Supply

Q3 Financials

Outlook

DOF ASA PRESENTATION

Q3 2010 - 3

The New Horizon

Highlights Q3

Contracts:

15 years contract with Total Argentina for Skandi Patagonia

4 AHTS newbuilds, 4 x 8 years with Petrobras

3 x RSV‟s, 3 x 5 years with Petrobras

Skandi Admiral onhire to Petrobras end September

Several contracts for DOF Subsea resulting in good asset utilisation

in Q4

Fleet:

Sale of hull 81 under construction at Cochin yard

Norskan ordered 3 AHTS at STX Promar, Brazil

Skandi Skolten delivered in July

Skandi Vitoria delivered and onhire to Petrobras early October

Skandi Peregrino delivered mid November, enroute to Brazil to

commence a long term contract with Statoil

Skandi Stord extended 2 more years with Statoil

Skandi Aker ”Ship of the Year 2010”

DOF ASA PRESENTATION

Q3 2010 - 4

The New Horizon

Highlights Q3

Financial:

Refinancing bonds in DOF ASA and DOF Subsea AS

Share issue DOF Installer ASA

Listing of Norskan postponed

DOF ASA PRESENTATION

Q3 2010 - 5

The New Horizon

Modern fleet

3 AHTS’s

13 PSV’s

2 CSV

3 state of the art

installation AHTS

vessels

Company overview

DOF Installer

Modern fleet & Equipment

21 CSV/ROV vessels

40 ROV’s + 1 AUV

Leading Subsea Contractor

DOF Subsea

Modern fleet

17 AHTS’s

7 PSV’s

2 CSV’s

NorskanDOF Subsea

Holding

Ship owning

Company

DOF ASA

DOF ASA PRESENTATION

Q3 2010 - 6

The New Horizon

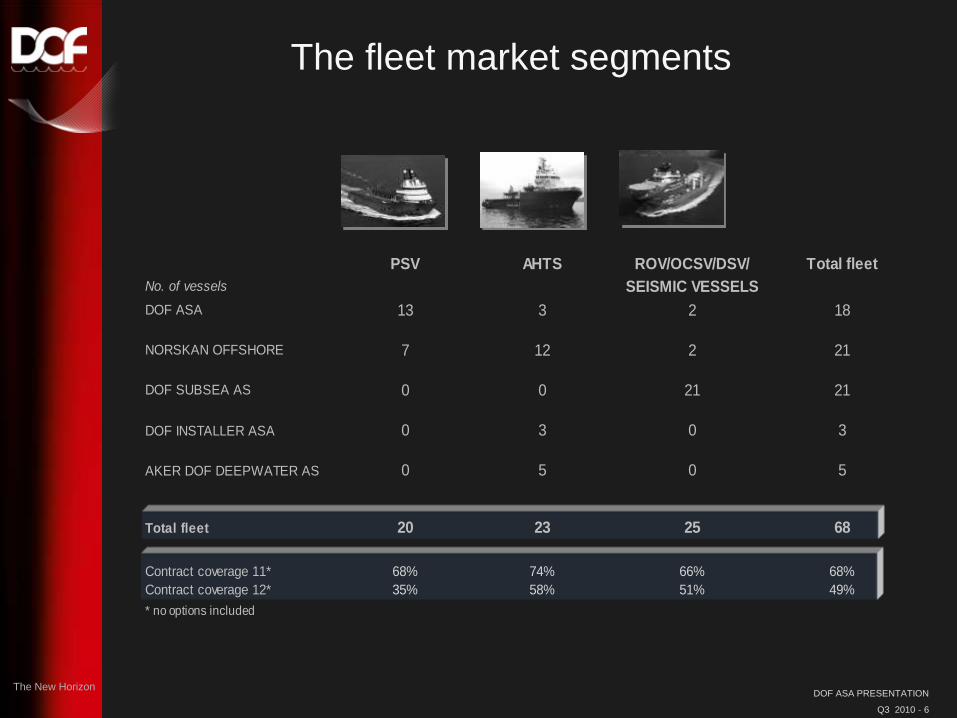

The fleet market segments

PSV AHTS ROV/OCSV/DSV/ Total fleet

No. of vessels SEISMIC VESSELS

DOF ASA 13 3 2 18

NORSKAN OFFSHORE 7 12 2 21

DOF SUBSEA AS 0 0 21 21

DOF INSTALLER ASA 0 3 0 3

AKER DOF DEEPWATER AS 0 5 0 5

Total fleet 20 23 25 68

Contract coverage 11* 68% 74% 66% 68%

Contract coverage 12* 35% 58% 51% 49%

* no options included

DOF ASA PRESENTATION

Q3 2010 - 7

The New Horizon

GLOBAL PLAYER

GEOGRAPHICAL FOCUS AREAS

PerthRio de Janeiro

Buenos Aires

Singapore

Houston

St. Johns

Aberdeen

Austevoll

Cairo

Brunei

Macae

Jakarta

Manila

Angola

St. Petersburg

Bergen

23

2

21

4

1

1

DOF ASA PRESENTATION

Q3 2010 - 8

The New Horizon

8

Long Term Contracted Cash Flows…

DOF group has solid cash flow visibility over the next 3-5 years

By Nov 2010 the total back-log (incl. options) was approx NOK 34 bn

Firm contract counts for NOK 19 bn

Options count for NOK 15 bn

The vessel Backlog amount to approximately 4 times the current

yearly revenue

Backlog Development (Year-End)

Note: Includes extension options on long-term contracts.

-

5

10

15

20

25

30

35

2010 2011 2012 2013 2014 2015 2016 2017

The New Horizon DOF ASA PRESENTATION

Q3 2010 - 9

DOF SUBSEA

Photographer: Harald M. Valderhaug

DOF ASA PRESENTATION

Q3 2010 - 10

The New Horizon

DOF Subsea Contract Coverage (Vessels)

FIRM CONTRACTS UNDER CONSTRUCTIONOPTIONAL PERIOD

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

Geobay

Geograph Petrobras - Jun 2016

Ocean Protector (Bergen) Seaforce - Sept 2014 + 2y opt

Geosund

Geosea

Geoholm

Skandi Seven Subsea 7 -Mar 2013 +4y opt

Skandi Salvadore Chevron -Sept 2011 +2y opt

Skandi Singapore (H621)

Skandi Vitoria Petrobras - July 2014 + 4y opt

Skandi Niteroi (H24)

Skandi Skolten

Skandi Hercules (H722)

Skandi Bergen (H723)

Skandi Aker (H705) AKOFS 2 - Jan 2015 + 5y opt

Skandi Santos (H716) AKOFS 1 - Jan 2015 + 5y opt

Skandi Patagonia Total - Dec 2025

Skandi Inspector Fugro - Q4 2010

Skandi Carla Fugro - July 2012 + 14y opt

Skandi Neptune Subsea 7 - Dec 2013 + 3y opt

Skandi Achiever Technip - Aug 2015 + 4y opt

Skandi Acergy Acergy - Aug 2016 + 6y opt

Skandi Arctic Technip - mar 2017 + 8y opt

Q4Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

201220112010 2013 2014 2015

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

DOF ASA PRESENTATION

Q3 2010 - 11

The New Horizon

FIRM CONTRACTS OPTIONAL PERIOD

DOF Subsea Contract Coverage (ROV & Others)

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Norskan Botafogo Petrobas

Skandi Fluminence Petrobras

Skandi Chieftain Petrobras

DOF ASA Skandi Vega Statoil (May)

Skandi Seven Subsea 7

Skandi Aker AKOFS (May)

Subsea IRM contract Shell Philipines

TGT White Rhino TGT VSP Vietnam

Devils Creek Development SapuraAcergy

Victorian Desalination Plant Thiess Pty

Survey and Positioning Heerema

Field Development Technip

Pazflor SURF Oproject Technip

Well positioning BP Angola

Survey, FPSO Instal. Ghana Technip

Survey, Seismic Node Inst. Nigeria Seabird

Survey support BP

Survey support BP Angola

Urugua Saipem

Asia

Reg

ion

Atl

an

tic r

eg

ion

DOFCON

No

rskan

2010 2011 2012

DOF ASA PRESENTATION

Q3 2010 - 12

The New Horizon

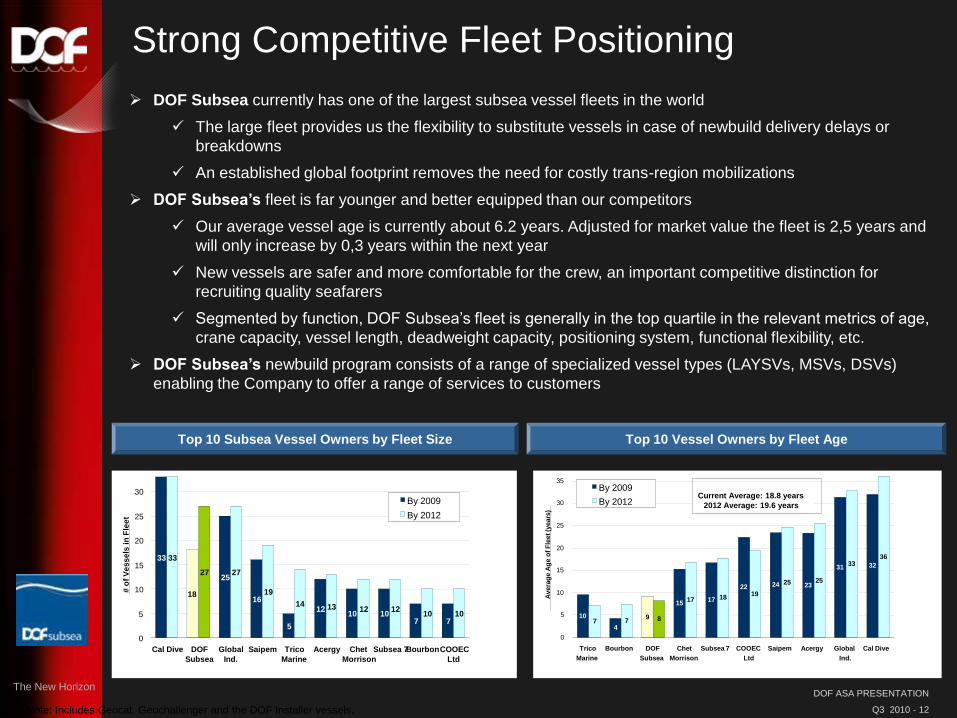

Strong Competitive Fleet Positioning

DOF Subsea currently has one of the largest subsea vessel fleets in the world

The large fleet provides us the flexibility to substitute vessels in case of newbuild delivery delays or

breakdowns

An established global footprint removes the need for costly trans-region mobilizations

DOF Subsea’s fleet is far younger and better equipped than our competitors

Our average vessel age is currently about 6.2 years. Adjusted for market value the fleet is 2,5 years and

will only increase by 0,3 years within the next year

New vessels are safer and more comfortable for the crew, an important competitive distinction for

recruiting quality seafarers

Segmented by function, DOF Subsea‟s fleet is generally in the top quartile in the relevant metrics of age,

crane capacity, vessel length, deadweight capacity, positioning system, functional flexibility, etc.

DOF Subsea’s newbuild program consists of a range of specialized vessel types (LAYSVs, MSVs, DSVs)

enabling the Company to offer a range of services to customers

Top 10 Vessel Owners by Fleet AgeTop 10 Subsea Vessel Owners by Fleet Size

33

16

5

1210 10

7 7

33

19

14 13 12 1210 10

18

2527 27

0

5

10

15

20

25

30

Cal Dive DOF

Subsea

Global

Ind.

Saipem Trico

Marine

Acergy Chet

Morrison

Subsea 7BourbonCOOEC

Ltd

# o

f V

es

se

ls i

n F

lee

t

By 2009

By 2012

10

4

1517

22 24 23

31 32

7 7 8

17 1819

25 25

3336

9

0

5

10

15

20

25

30

35

Trico

Marine

Bourbon DOF

Subsea

Chet

Morrison

Subsea 7 COOEC

Ltd

Saipem Acergy Global

Ind.

Cal Dive

Avera

ge A

ge o

f F

leet (y

ears

)

By 2009

By 2012Current Average: 18.8 years

2012 Average: 19.6 years

Note: Includes Geocat, Geochallenger and the DOF Installer vessels.

DOF ASA PRESENTATION

Q3 2010 - 13

The New Horizon

Skandi Singapore - DSV

Delivery Q2 2011

DP II Dive Support Vessel

2 x Triton XLX W ROV

18 man saturation diving

system

140 t Crane

900 m2 Cargo deck area

100 men accommodation

DOF ASA PRESENTATION

Q3 2010 - 14

The New Horizon

Skandi Skolten – The new generation vessels

Construction & AHTS

vessel

Hybrid propulsion

361 t Bollard Pull

36 000 BHP

250 t Crane

2 x W ROV

1 070 m2 Cargo deck

area

90 men accommodation

Design STX AH-04 | Built: 2010

DOF ASA PRESENTATION

Q3 2010 - 15

The New Horizon

Status Supply

Photographer: Harald M. Valderhaug

DOF ASA PRESENTATION

Q3 2010 - 16

The New Horizon

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

PSV

1 Skandi Falcon Reliance spot

2 Skandi Marstein SHELL UK Opt Nov 2016

3 Skandi Foula SHELL UK

4 Skandi Rona SHELL UK

5 Skandi Buchan TOTAL

6 Skandi Sotra STATOIL

7 Skandi Caledonia M OG

8 Skandi Barra TOTAL

9 Skandi Texel Peterson Supplylink Opt Jan 2016

10 Skandi Commander SHELL

11 Skandi Mongstad STATOIL Firm Aug 2016 / Opt Aug 2021

12 Skandi Flora STATOIL Opt Feb 2017

13 Skandi Gamma (PSV 06 LNG) STATOIL Firm Mar 2016/ Opt Mar 2019

AHTS

14 Skandi Stord STATOIL

15 Skandi Admiral* PETROBRAS

16 Skandi Vega STATOIL Opt May 2018

*Backlog under Brazil contract overview

CSV

17 Skandi Fjord Halliburton Opt Oct 2017

18 Skandi Olympia FUGRO

2010 2011 2012 2013 2014 2015

DOF Contract Coverage

FIRM CONTRACTS UNDER CONSTRUCTIONOPTIONAL PERIOD

DOF ASA PRESENTATION

Q3 2010 - 17

The New Horizon

Aker DOF Deepwater AS - 50% DOF

Vessel Name

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

1 Skandi Peregrino (VN) STATOIL

2 Skandi TBN Vietnam

3 Skandi TBN Vietnam

4 Skandi TBN Vietnam

5 Skandi TBN Vietnam

201520142010 2011 2012 2013

Aker DOF Deepwater - Contract Coverage

FIRM CONTRACTS UNDER CONSTRUCTIONOPTIONAL PERIOD

DOF ASA PRESENTATION

Q3 2010 - 18

The New Horizon

Brazilian Fleet9

Brazilian Fleet (Under

Construction)7

International Fleet

10

International Fleet (Under Construction)

10

Norskan‟s Market Position in BrazilNorskan is well positioned to serve the high-end offshore support vessel

market in Brazil

Leading owner of a diversified Brazilian

offshore support vessel fleet

Largest AHTS and CSVs owner in Brazil with a

versatile fleet

Leading owner of large PSVs and AHTSs in

Brazil (including current newbuilds)

One of the youngest fleets in the industry

Unique, “best-in-class” Brazilian-flagged

vessels

One of the largest tonnage capacities in the

Brazilian offshore industry to benefit from REB

regime

Capacity to import 6 to 8 additional high-end

vessels (through REB)

Chasing the Day Rate Business

Source: ODS Petrodata; includes vessels currently owned in Brazil and announced Brazilian newbuild programs1 Calculated at IPO

Norskan Vessel Breakdown 1

Companies operating in Brazil owning PSVs ≥ 3,000 dwt,

AHTS ≥ 10,000 bhp

Companies operating in Brazil owning CSVs

DOF ASA PRESENTATION

Q3 2010 - 19

Vessel J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

1 Skandi Leblon SHELL

2 Skandi Flamengo PETROBRAS

3 Skandi Waveney STATOIL

4 Skandi Stolmen PETROBRAS

5 Skandi Captain PETROBRAS

6 Skandi Yare PETROBRAS Opt Jan 2016

7 Skandi Hav PETROBRAS Opt Sep 2019

8 Skandi Copacabana PETROBRAS

9 Skandi Botafogo PETROBRAS

10 Skandi Rio PETROBRAS

11 Skandi Fluminense PETROBRAS

12 Skandi Giant PETROBRAS

13 Skandi Admiral PETROBRAS

14 Skandi Møgster OGX

15 Sanko Bay OGX18

16 Skandi Ipanema OGX

17 Skandi Peregrino STATOIL

18 Skandi Amazonas PETROBRAS 8 yrs f irm cont ract Fir m Jul 2019 / Opt Jul 2027

19 Skandi Iguaçu PETROBRAS 8 yrs f irm cont ract Fir m Dec 2019 / Opt Dec 2027

20 Hull 30 STX AH 11 PETROBRAS 8 yrs f irm cont ract Fir m Nov 2020 / Opt Nov 2028

21 Hull 31 STX AH 11 PETROBRAS 8 yrs f irm cont ract Fir m May 2021 / Opt May 202919

22 Hull 33 STX AH 1119

23 Skandi Chieftain PETROBRAS

24 Skandi Emerald/Odin Viking OGX

25 Skandi Salvador CHEVRON# #

26 Skandi Santos PETROBRAS Opt Nov 2020# #

27 Skandi Vitória PETROBRAS Opt Dec 2017

28 Skandi Niterói

29 Geograph PETROBRAS 5 yrs f r im cont ract

30 Skandi TBN 1 PETROBRAS 5 yrs f r im cont ract

31 Skandi TBN 2 PETROBRAS 5 yrs f r im cont ract

2015Q1 Q2 Q3 Q4

2014Q1 Q2 Q3 Q4

2013Q1 Q2 Q3 Q4

2011Q1 Q2 Q3 Q4

2012Q1 Q2 Q3 Q4

2010Q1 Q2 Q3 Q4

DOF / Norskan /DOF Subsea Contracts in Brazil

FIRM CONTRACTS UNDER CONSTRUCTIONOPTIONAL PERIOD

DOF ASA PRESENTATION

Q3 2010 - 20

The New Horizon

Norskan continued growth in Brazil

Since 2000, Norskan has assembled a strong portfolio of Brazilian-flagged vessels,

allowing for superior crew training and professional development

Successful track record during its 10-year history

in Brazil

In-depth knowledge of the Brazilian market

Leading position in OSV markets and strong

presence in subsea market and construction

support

Fleet and crew better suited to the Brazilian

offshore support market relative to competitors

17 Brazilian-flagged vessels that enjoy significant

competitive advantages under Brazilian foreign

fleet substitution rules

Norskan has in 2010 secured 7 long term

contracts in Brazil to be started in the period fm

2011-2013 and is uniquely positionned to win

more contracts

Norskan is expected to have substantial

growth in earnings and has therefore

postponed a potential IPO to get focus on

2012 estimates

DOF ASA PRESENTATION

Q3 2010 - 21

The New Horizon

Financials

DOF ASA PRESENTATION

Q3 2010 - 22

The New Horizon

Financial/Operational Highlights Q3 2010

• Utilization Subsea fleet (85%)

Good activity in the North Sea and Brazil

Lower activity in Australia

• Utilization Supply fleet (91%)

Two vessels in transit to new operational areas

Class docking

• Two vessels delivered in 3rd quarter

Skandi Skolten, in operation since July/August

Skandi Vitoria, in operation from October

• Unrealised currency gain on long term debt

DOF ASA PRESENTATION

Q3 2010 - 23

The New Horizon

ALL FIGURES IN NOK MILLION

Result Q3 2010

2010 2009 2010 2009 2009

Q3 Q3 YTD YTD

Operating income 1 237 1 120 3 888 3 166 4 327

Total operating income 1 237 1 120 3 888 3 166 4 327

operating expenses vessels 805 745 2 632 2 228 3 094

Total operating expenses 805 745 2 632 2 228 3 094

Operating profit before depreciation EBITDA 433 375 1 256 939 1 234

Depreciation 301 215 825 566 837

Write-down 179

Operating profit - EBIT 132 160 431 373 218

Net profit from associated companies -9 3 -7 176 192

other financial Items -262 -40 -484 -287 -163

Unralized profit/ loss on currencies 339 496 -1 900 758

Net financial costs 68 459 -492 789 787

Pre-tax profit 200 619 -61 1 162 1 005

Taxes 26 122 46 272 201

Result 174 497 -107 890 803

DOF ASA PRESENTATION

Q3 2010 - 24

The New Horizon

P&L Supply and Subsea

ALL FIGURES IN NOK MILLIONDOF ASA

DOF SUB.

HOLDINGTotal DOF ASA

DOF SUB.

HOLDINGTotal

Q3 2010 Q3 2010 Q3 2010 YTD 2010 YTD 2010 YTD 2010

Operating income 408 829 1 237 1 400 2 488 3 888

Other income - -

Total operating income 408 829 1 237 1 400 2 488 3 888

Operating expenses 256 549 805 892 1 740 2 632

Total operating expenses 256 549 805 892 1 740 2 632

Operating profit before

depreciation 163 270 433 508 748 1 256

Ebitda margin 40 % 33 % 35 % 36 % 30 % 32 %

DOF ASA PRESENTATION

Q3 2010 - 25

The New Horizon

Results - Business SegmentsALL FIGURES IN NOK MILLION

68

86

279

EBITDA Q3 2010

68

83 223

EBITDA Q3 2009

EBITDA

Q3 2010 Q3 2009

PSV 68 68

AHTS 86 83

CSV 279 223

Total 433 374

DOF ASA PRESENTATION

Q3 2010 - 26

The New Horizon

Results – Geographical SegmentsALL FIGURES IN NOK MILLION

110

6

159

158

EBITDA Q3 2010

185

25

81

83

EBITDA Q3 2009

EBITDA

Q3 2010 Q3 2009

Europe/ West Africa 110 185

Australasia 6 25

Brazil 159 81

America/Worldwide 158 83

Total 433 374

DOF ASA PRESENTATION

Q3 2010 - 27

The New Horizon

Currency effects on Q3 2010 results

ALL FIGURES IN NOK MILLION

Financial items Q3 2010 Acc Q3 2010 Q3 2009 Acc Q3 2009

Share of loss profit from associated -8 -7 4 176

Interest reveneue 21 57 15 64

Interest costs -232 -554 -148 -474

Realized currency gain/loss long debt -3 40 60 109

Realized currency gain/loss on forex instruments -9 -8 -113 -98

Realized operational currency gain/loss (-) 66 63 -27

Other financial expenses -106 -83 81 75

Total financial items -271 -491 -101 -175

Unrealized profit/loss on currencies

Unrealized currency gain/loss on long debt 223 -39 477 788

Unrealized currency gain/loss on forex instruments 116 38 18 112

Unrealized operational currency gain

Total unrealized profit/loss on currencies 339 -1 495 900

Total financial items 68 -492 394 725

DOF ASA PRESENTATION

Q3 2010 - 28

The New Horizon

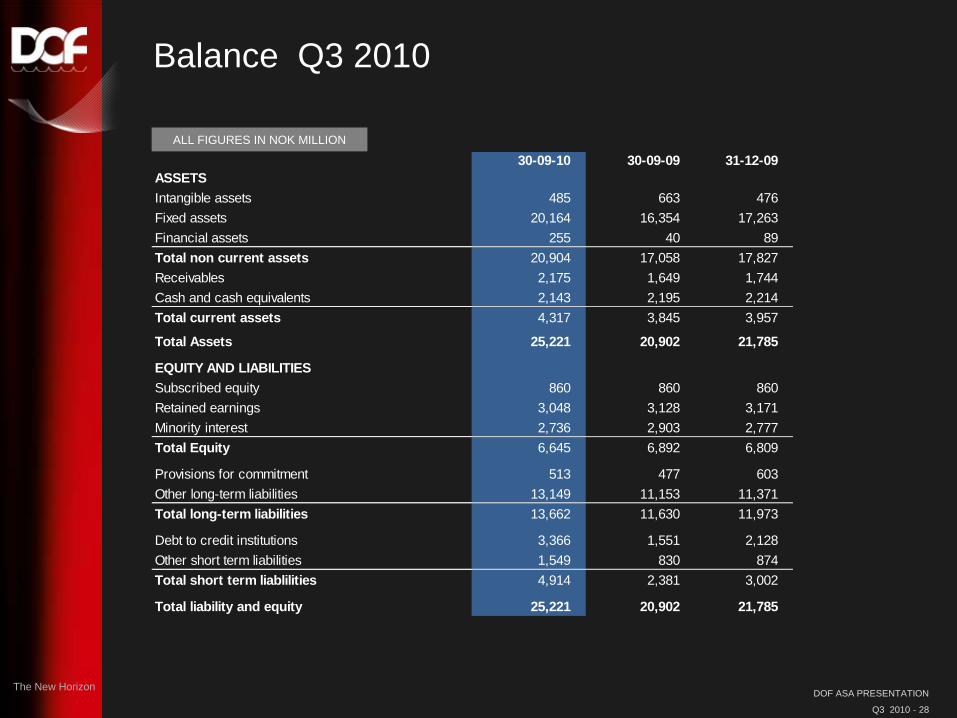

Balance Q3 2010

ALL FIGURES IN NOK MILLION

30-09-10 30-09-09 31-12-09

ASSETS

Intangible assets 485 663 476

Fixed assets 20,164 16,354 17,263

Financial assets 255 40 89

Total non current assets 20,904 17,058 17,827

Receivables 2,175 1,649 1,744

Cash and cash equivalents 2,143 2,195 2,214

Total current assets 4,317 3,845 3,957

Total Assets 25,221 20,902 21,785

EQUITY AND LIABILITIES

Subscribed equity 860 860 860

Retained earnings 3,048 3,128 3,171

Minority interest 2,736 2,903 2,777

Total Equity 6,645 6,892 6,809

Provisions for commitment 513 477 603

Other long-term liabilities 13,149 11,153 11,371

Total long-term liabilities 13,662 11,630 11,973

Debt to credit institutions 3,366 1,551 2,128

Other short term liabilities 1,549 830 874

Total short term liablilities 4,914 2,381 3,002

Total liability and equity 25,221 20,902 21,785

DOF ASA PRESENTATION

Q3 2010 - 29

The New Horizon

Key figures Q3 2010

2010 2009 2010 2009 2009

Q3 Q3 YTD YTD

Profit per share ex. minority interest 1.85 6.24 -0.08 10.84 9.16

Profit per share ex. unrealized loss/gain -1.81 0.01 -1.16 -0.12 0.52

Cashflow per share 1.50 2.61 7.90 6.72 12.10

Ebitda margin 35% 34% 32% 30% 29%

Ebit margin 11% 14% 11% 12% 5%

Return on net capital 3% 7% -2% 13% 12%

Equity ratio 26% 33% 26% 33% 31%

Net interest bearing debt 14,154 10,379 14,154 10,379 11,073

Net interest bearing debt ex. unemployed capital 10,726 6,091 10,726 6,091 6,478

No of shares 91,037,975 82,767,975 91,037,975 82,767,975 87,730,811

Face value per share 2 2 2 2 2

DOF ASA PRESENTATION

Q3 2010 - 30

The New Horizon

-

100,000

200,000

300,000

400,000

500,000

600,000

Q4 -2006

Q1 -2007

Q2 -2007

Q3 -2007

Q4 -2007

Q1 -2008

Q2 -2008

Q3 -2008

Q4 -2008

Q1 -2009

Q2 -2009

Q3 -2009

Q4 -2009

Q1 -2010

Q2 -2010

Th

ou

san

d N

OK

PSV

AHTS

CSV

DOF High asset values

Fair market values DOF fleet have been stable through 2008 and 2009

Fair market values Brazilian built vessels have increased with approx. 25%

since 2006

All vessels (built 1983-2010) are valued higher then original capex

Valuation of PSV (UT 755 and MT 6000), AHTS (UT 722L) and Subsea ROV vessel.

DOF ASA PRESENTATION

Q3 2010 - 31

The New Horizon

Significant Asset Coverage

The combined market value DOF vessels in operation per September is NOK 20bn

Supply FMV NOK 9 bn NIBD NOK 4,5bn

Subsea FMV NOK 11bn NIBD NOK 6,0 bn

Asset-level gearing on the fleet including new-builds is 59%, decreasing to 44% in 2014

Provides a significant equity cushion on top of existing vessel-level

financing

We forecast significant gearing reduction upon completion of the current

newbuild program

Total Fleet Market value

Vessels (a) 20 000

Other Equipment (b) 1 000

Total Fleet 21 000

Note: Vessel values as of 30 June, 2010.(a) Does not include market value of the remaining vessels to be delivered in 2010-

2013DOF Subsea are included 100% in the calculation and JV‟s with 50%.

(b) Includes ROVs, AUV, diving systems, other equipment.

Gearing forecast summary

0 %

20 %

40 %

60 %

80 %

100 %

120 %

2010E 2011E 2012E 2013E 2014E

59 % 60 % 57 % 52 % 44 %

41 % 40 % 43 % 48 % 56 %

debt Equity

DOF ASA PRESENTATION

Q3 2010 - 32

The New Horizon

DOF BOND 500 maturity in July 2011

Fleet loan 5 vessels DOF 600 A new facility in progress, planned completion Q4 2010

Fleet loan 4 vessels DOF Subsea 900 A new facility in progress, planned completion Q4 2010

Debt to be refinanced next 12 months

ALL FIGURES IN NOK MILLION

DOF ASA PRESENTATION

Q3 2010 - 33

The New Horizon

The DOF Group New Builds

New Builds DOF ASA Group 31.10.2010 NOK 000

Vessel Name PROJECT

PRICE PAID IN

REMAINING

CAPEX FINANCING ** EQUITY LTV

Sum New Builds DOF ASA Group 11.135.466 1.955.123 9.180.343 8.352.620 827.723 75 %

Relative share New Builds DOF ASA Group 9.988.306 1.755.818 8.232.488 7.537.620 694.868 75 %

DOF ASA /DOF Rederi (100%) 553.870 110.000 443.870 415.000 28.870 75 %

Norskan (100%) 5.474.275 783.513 4.690.762 4.357.620 333.142 80 %

Aker DOF Deepwater (JV 50 %) 866.161 144.805 721.356 590.000 131.356 68 %

DOF SUBSEA (100 %) 913.000 350.000 563.000 650.000 -87.000 71 %

DOF SUBSEA (JV 50%) 281.000 54.500 226.500 225.000 1.500 80 %

DOF INSTALLER (78,5%) 1.900.000 313.000 1.587.000 1.300.000 287.000 68 %

**Total planned financing new-building program: NOK 7,5 bnSecured financing new-building program: NOK 5,7 bn

DOF ASA PRESENTATION

Q3 2010 - 34

The New Horizon Picture of Skandi Mongstad

OUTLOOK

DOF ASA PRESENTATION

Q3 2010 - 35

The New Horizon

SHORT TERM OUTLOOK

High contract coverage for both supply and subsea in

Q4

More vessels contributing compared to previous

quarters

Ebitda in Q4 expected to be better than Q2 Ebitda

DOF ASA PRESENTATION

Q3 2010 - 36

The New Horizon

Q4 2010 H1 2011 H2 2011 2012 2013

Skandi Urca (8 yrs Petrobras)

Skandi Angra

Skandi Iquazu (8 yrs Petrobras)

Skandi Paraty (8 yrs Petrobras)

Skandi Vietnam 5

Skandi Vietnam 6

Skandi Vietnam 4

Skandi Bergen (Project)

Skandi Niterói

Skandi Amazonas (8 yrs Petrobras)

Skandi Gamma (6 yrs Statoil)

Skandi Emerald

Skandi Hawk

Skandi Singapore

Skandi Hercules (Project)

Skandi Vitoria (4 yrs Petrobras)

Skandi Ipanema (1.5 yrs OGX)

Skandi Peregino (2 yrs Statoil)

50 Vessels

54 Vessels

58 Vessels

62 Vessels

66 Vessels

Long Term OutlookEbitda growth new vessels

Brazil DOF Supply

DOF Installer DOF Subsea

Vessels in Operation

DOF ASA PRESENTATION

Q3 2010 - 37

The New Horizon

MARKET SUMMARY DOF FLEET

Supply

Weak North Sea spot market expected near term

Several long term opportunities for PSV‟s in the North Sea

Strong market in Brazil – several new tenders

Subsea

Expected lower activities in the North Sea during winter season

Higher activity in Asia in Q4 2010 and Q1 2011 compared to Q3

High activity in Brazil

DOF ASA PRESENTATION

Q3 2010 - 38

The New Horizon

Thank you

DOF ASA PRESENTATION

Q3 2010 - 39

The New Horizon

DISCLAIMER

This presentation by DOF ASA designed to provide a high level overview of aspects of theoperations of the DOF ASA Group.

The material set out in the presentation is current as at 18 November, 2010.

This presentation contains forward-looking statements relating to operations of the DOF ASAGroup that are based on management‟s own current expectations, estimates and projectionsabout matters relevant to DOF ASA„s future financial performance. Words such as “likely”,“aims”, “looking forward”, “potential”, “anticipates”, “expects”, “predicts”, “plans”, “targets”,“believes” and “estimates” and similar expressions are intended to identify forward-lookingstatements.

References in the presentation to assumptions, estimates and outcomes and forward-lookingstatements about assumptions, estimates and outcomes, which are based on internal businessdata and external sources, are uncertain given the nature of the industry, business risks, andother factors. Also, they may be affected by internal and external factors that may have amaterial effect on future business performance and results.

No assurance or guarantee is, or should be taken to be, given in relation to the future businessperformance or results of the DOF ASA Group or the likelihood that the assumptions, estimatesor outcomes will be achieved.

While management has taken every effort to ensure the accuracy of the material in thepresentation, the presentation is provided for information only. DOF ASA , its officers andmanagement exclude and disclaim any liability in respect of anything done in reliance on thepresentation.

All forward-looking statements made in this presentation are based on information presentlyavailable to management and DOF ASA assumes no obligation to update any forward looking-statements. Nothing in this presentation constitutes investment advice and this presentationshall not constitute an offer to sell or the solicitation of any offer to buy any securities orotherwise engage in any investment activity.

You should make your own enquiries and take your own advice (including financial and legaladvice) before making an investment in the company's shares or in making a decision to hold orsell your shares.