does mandated disclosure induce a structural change in the determinants of nonaudit service...

TRANSCRIPT

Auditing: A Journal of Practice & Theory American Accounting AssociationVol. 30, No. 2 DOI: 10.2308/ajpt-50001May 2011pp. 51–76

Does Mandated Disclosure Induce aStructural Change in the Determinants of

Nonaudit Service Purchases?

Lawrence J. Abbott, Susan Parker, and Gary F. Peters

SUMMARY: We investigate the association between mandated fee disclosures and

structural changes in the determinants of nonaudit services (NAS). The Securities and

Exchange Commission (SEC) underscored the importance of understanding the impact

of disclosures when the Auditor Independence Rules of 2000 explicitly relied on market

responses to discipline NAS purchases. In contrast, the Sarbanes-Oxley Act of 2002

(SOX) relied upon prohibitions of NAS. Our findings suggest that market-based

approaches were functioning prior to SOX prohibitions. We find that after the SEC

mandated fee disclosures, NAS purchases become negatively associated with firms

seeking financing and positively associated with managerial ownership. We also

document a significantly smaller propensity for NAS purchases among larger firms,

compared to a nondisclosure environment. Last, we find that mandated disclosures

significantly increase the negative association between NAS purchases and effective

audit committees. Collectively, our findings are consistent with mandated disclosures

increasing agency cost incentives for limiting NAS purchases.

Keywords: nonaudit services; mandatory disclosures; auditor fees.

Data Availability: The data are available from public sources.

INTRODUCTION

The impact of nonaudit services (NAS) on perceived audit quality has been the subject of a

considerable amount of prior research. This stream of research includes investigations of

stock and bond markets’ reactions to NAS disclosure as a proxy for perceived auditor

Lawrence J. Abbott is an Associate Professor at the University of Wisconsin–Milwaukee, Susan Parker is anAssociate Professor at Santa Clara University, and Gary F. Peters is an Associate Professor at the Universityof Arkansas.

We thank the two anonymous reviewers and Clive Lennox (associate editor) for their useful comments and suggestions.

Editor’s note: Accepted by Clive Lennox.

Submitted: October 2009Accepted: August 2010

Published Online: May 2011

51

independence.1 These studies show that firms with higher levels of NAS purchases are associated

with higher costs of debt and equity capital (Dhaliwal et al. 2008; Brandon et al. 2004; Nam 2005),

as well as with lower earnings response coefficients (Francis and Ke 2006; Krishnan et al. 2005;

Higgs and Skantz 2006). Despite these findings, there is comparatively little research on how

mandated NAS disclosures impact subsequent NAS purchases. In this study, we investigate

whether the introduction of mandated NAS disclosures is associated with structural changes in the

relations between certain company characteristics and NAS purchases in pre- and post-disclosure

settings.2 We accomplish this by comparing NAS purchases made in 2000 (pre-disclosure) with

those made by the same set of firms (employing the same auditor) in 2001 (post-disclosure).

By examining the impact of mandated NAS disclosure on NAS purchasing behavior, our study

seeks to provide evidence on the potential regulatory efficacy of disclosure requirements such as the

Securities and Exchange Commission’s (SEC) Auditor Independence Rules of 2000, which

mandated audit fee and NAS disclosures. During the rule-making deliberations, the SEC adopted a

demand-side approach to regulating NAS purchases. In particular, the SEC sought to ‘‘let the

market decide’’ the optimal level of NAS purchases by imposing a mandatory NAS disclosure

regime. That is, in the event that the market imposed penalties on firms with relatively higher levels

of NAS, the penalties would provide registrants with market-based incentives to lower their NAS

purchases (Unger 2001; Levitt 2000). However, the subsequent Sarbanes-Oxley Act (SOX) took a

supply-side approach to the NAS issue by banning several NAS services (Canada et al. 2008; U.S.

House of Representatives 2002). Consequently, our test setting represents a unique window of

opportunity since it occurs after the Auditor Independence Rules of 2000, but before the SEC

altered the NAS definitions and before SOX.

This specific period setting provides a natural experiment in which to test the agency-based

demand for audit quality signals.3 The market’s initial price protection reaction to NAS disclosures

was economically significant (Dhaliwal et al. 2008; Francis and Ke 2006; Krishnan et al. 2005;

Higgs and Skantz 2006; Nam 2005; Brandon et al. 2004). Moreover, the ‘‘price protection’’

reaction was consistent with central tenets of the agency-based demand for audit quality (Watts and

Zimmerman 1983; Jensen and Meckling 1976). However, for timing reasons, we argue that

companies could not have incorporated the market’s negative reaction to the NAS disclosures into

their 2000 NAS purchase decisions, whereas NAS purchased in 2001 included the anticipated

reactions.4 By examining pre- and post-disclosure NAS purchases for the same set of firms, we

isolate the effect of the mandated NAS disclosures and concomitant market’s price protection

1 Whether NAS impairs actual audit quality is an empirical question on which we do not provide evidence.Examples of this literature stream include: DeFond et al. 2002; Ashbaugh et al. 2003; Dopuch et al. 2001;Ferguson et al. 2004; Frankel et al. 2002; Chung and Kallapur 2003; Ruddock et al. 2006; among others. Incontrast, our study focuses on the management response to perceived audit quality concerns.

2 It is important to note that we explore only shifts in the determinants of NAS purchases. We make no predictionson whether the overall level of NAS purchased may change, though we later present some descriptive data on theshift in NAS purchases.

3 We use the term audit quality signal to refer to publicly available proxies for audit quality. As investors cannotdirectly observe audit quality, they must use proxies for it, with the Big N/non-Big N dichotomy serving as themost pervasive audit quality signal. We posit the NAS/audit fee ratio is another publicly available signal ofperceived audit quality.

4 Hereafter, we refer to NAS purchased in 2000 (disclosed in 2001) as purchases in the ‘‘nondisclosureenvironment.’’ While the year 2000 NAS purchases were eventually disclosed, contracting parties most likelyacted in a manner consistent with a nondisclosure environment. This is because the disclosure requirements of theAuditor Independence Rules were enacted somewhat unexpectedly in November of 2000, with an effective datefor proxy statements filed beginning February 2001 (Abbott et al. 2003b). This suggests the companies purchasedthe majority of NAS prior to the promulgation of the Auditor Independence Rules. In addition, the contractingparties most likely could not have predicted the market’s reaction to the disclosures until the actual disclosuresappeared in 2001.

52 Abbott, Parker, and Peters

Auditing: A Journal of Practice & TheoryMay 2011

reaction on NAS purchasing behavior. Prior agency-based NAS research has either (1) not

explored subsequent year NAS purchases (Abbott et al. 2003a), or (2) documented the effect of

agency costs on auditor fees (Firth 1997; Parkash and Venable 1993), without addressing the role

of market reactions to mandated NAS disclosures in creating subsequent year agency effects. Thus,

we believe our paper advances the understanding of the influence of disclosure on the demand for

audit quality signals in a powerful, quasi-laboratory setting. Figure 1 summarizes our research

setting.

A final purpose of the study is to examine the impact of NAS disclosure on another key NAS

purchase stakeholder, the audit committee. Prior research provides evidence indicating that audit

committees have litigational incentives to reduce NAS purchases, regardless of the disclosure

environment (Abbott et al. 2003a). However, behavioral research by Gaynor et al. (2006) suggests

that NAS disclosures exacerbate an audit committee’s litigational concerns and incentives.

However, prior archival NAS research ignores the impact of disclosure on audit committees’

influence over NAS purchase decisions (e.g., Omer et al. 2006; Asthana and Krishnan 2006; Abbott

et al. 2003a; Firth 1997; Parkash and Venable 1993). Our study directly tests the behavioral results

of Gaynor et al. (2006) in an archival setting.

Our research design requires us to replicate the Abbott et al. (2003a) agency-based NAS

purchasing model using their sample of year 2000 NAS purchases. We then compare the same

model’s estimated coefficients to those produced using 2001 NAS purchases for the same set of

sample firms. We perform Chow tests for inter-year differences in the coefficient estimates to

determine if the mandated NAS disclosure environment structurally changed the relationships

between NAS and agency-based independent variables found in the Abbott et al. (2003a) model. By

keeping the sample firms, auditors, model, and independent variable values as consistent as

possible, we seek to isolate the effects of mandated NAS disclosure on NAS purchasing behavior.

Consistent with Abbott et al. (2003a), we find little support for an agency-based model for

NAS purchases in a nondisclosure environment—i.e., 2000 NAS purchases. In contrast, we

document statistically significant structural differences in the relation between the NAS/audit fee

ratio and three of our four primary agency conflict variables when switching to a disclosure

environment. We also find similar results when we use the same model to predict which firms were

more likely to reduce 2001 NAS purchases relative to 2000 NAS purchases. Specifically, we

document that inside ownership and financing activity become statistically significant determinants

of NAS purchasing behavior in the disclosure environment. In addition, the positive association

between company size and the demand for NAS decreases during the post-disclosure environment,

consistent with the larger agency costs of larger firms.5 We also document a statistically significant

increase in the magnitude of our audit committee effectiveness coefficient for the subsequent year

FIGURE 1Timing of NAS Purchases and Mandatory Disclosure Rules

5 We fail to document any relation—in either the disclosure or nondisclosure environments—between the NAS/audit fee ratio and our fourth agency conflict variable, leverage.

Does Mandated Disclosure Induce a Structural Change? 53

Auditing: A Journal of Practice & TheoryMay 2011

NAS purchases. The agency-based model’s R2 increases over 70 percent from the initial year (i.e.,

nondisclosure environment) to the subsequent year of NAS disclosure (i.e., disclosure

environment). We interpret these results as consistent with disclosures providing a market-based

mechanism for managers to weigh the costs and benefits of purchasing NAS.

We contribute to the literature in three ways. First, our results provide support for the

agency-based demand for publicly available audit quality signals in a powerful test setting. We find

evidence consistent with the SEC’s Auditor Independence Rules of 2000 fulfilling their intended

purpose of creating market-driven, demand-side incentives with respect to the NAS/audit fee ratio.

As such, the SOX supply-side approach of banning certain NAS may have hurt some registrants if

those banned NAS services previously served to increase overall audit quality (Abbott et al. 2007;

Gaynor et al. 2006). Second, the evidence provided herein suggests that registrants learned from the

market’s negative price protection reaction and, in accordance with agency theory, recalibrated their

subsequent year NAS purchases. Our test setting may serve to resolve some of the inconsistent

findings in prior research on the relation between agency costs and auditor choice, a second heavily

researched audit quality signal (Blouin et al. 2007; Barton 2005; DeFond 1992). Our test setting

avoids some of the issues arising in prior agency cost-auditor choice studies such as endogeneity

(Copley and Douthett 2002; Ireland and Lennox 2002), self-selection (Chaney et al. 2004; Ireland

and Lennox 2002), and auditor switching costs (Blouin et al. 2007; DeFond 1992). Finally, our

results provide archival, empirical support for the audit committee incentive arguments of Gaynor et

al. (2006).

We organize the remainder of our paper as follows. The second section reviews prior research

and develops our hypotheses. The third section describes our research design. The fourth section

presents our sample selection and results, as well as sensitivity analyses. The fifth section

concludes.

PRIOR RESEARCH AND HYPOTHESIS DEVELOPMENT

The Agency-Based Demand for Audit Quality Signals

Jensen and Meckling (1976) describe how agency conflict occurs as a result of the separation

of ownership and control of the firm. Critical to the current study, investors recognize the potential

for agency conflict resulting from this separation and rationally discount the representations/

disclosures of management, most notably management-prepared financial statements (Jensen and

Meckling 1976). In the process of discounting (price protection), investors impose agency costs on

management. Management, in turn, can mitigate these costs by voluntarily hiring independent

auditors for monitoring, thus increasing the visibility of their actions (Jensen and Meckling 1976).

Increases in the divergence between manager and investor preferences or decreases in visibility

dictate a greater degree of perceived agency conflict by market participants who, in turn, impose

greater agency costs on these firms. This creates the agency-based demand for audit quality

(DeFond 1992; Watts and Zimmerman 1983).

Since audit quality is generally not directly observable, the market—which imposes agency

costs on registrants—must use publicly available proxies for it, typically auditor size (Barton 2005;

DeFond 1992). Consistent with the auditor size signal, prior studies show that Big N audited

companies enjoy a higher earnings response coefficient (Teoh and Wong 1993) and lower costs of

debt and equity capital (Mansi et al. 2004; Pittman and Fortin 2004; Hogan 1997; Beatty 1989;

Balvers et al. 1988). Thus, Big N auditors can reduce agency costs (in the form of reduced

discounting of financial statement representations by the stock and/or bond market) by providing

financial statement users with a higher level of perceived audit quality. Collectively, prior research

suggests that managers with greater agency conflicts can enhance the efficacy of their financial

statements by providing signals of perceived audit quality.

54 Abbott, Parker, and Peters

Auditing: A Journal of Practice & TheoryMay 2011

NAS Purchase Disclosures as a Perceived Audit Quality Signal

The impact of NAS on auditor independence in fact and in appearance has been an academic

and regulatory concern for some time, particularly under the tenure of SEC Chairman Arthur Levitt

in the late 1990s. Levitt (2000) frequently voiced his concerns that consulting and other services

‘‘shorten the distance between the auditor and management’’ and that ‘‘independence—if not in fact,

then certainly in appearance—becomes a more elusive proposition.’’ Levitt originally proposed

banning all NAS services provided by the financial statement auditor (SEC 2000a). The AICPA and

Big 5 auditors strenuously objected to these proposals. Firms argued that in addition to the added

value of services provided to clients, NAS can increase the quality of financial statement audits.

After a heated debate, the parties reached a compromise in November 2000. FRR No. 56, Revisionof the Commission’s Auditor Independence Requirements, required all proxy statements filed after

February 4, 2001, to contain disclosures about audit and nonaudit fees (SEC 2000b). This

regulation represented a ‘‘market-based’’ approach to the NAS issue. That is, instead of prohibiting

the supply of NAS, the SEC allowed the market to be the ultimate arbiter of NAS’ impact on

auditor independence and allowed managers to weigh the subsequent costs and potential benefits of

NAS purchases.

With NAS disclosures, investors could potentially utilize the NAS/audit fee ratio as a means of

gauging unobservable audit quality. Although high NAS may not impair an auditor’s ability to

detect a material misstatement, investors may perceive that NAS reduces the auditor’s willingness

to demand a correction of a misstatement should one occur (Beck et al. 1988; DeAngelo 1981).

Recent research has examined whether the market perceives NAS as lowering audit quality. These

studies use research designs that largely mirror those investigating the Big N/non-Big N audit

quality signal. These studies find that high-NAS firms have lower earnings response coefficients

(Francis and Ke 2006; Higgs and Skantz 2006; Krishnan et al. 2005), as well as higher costs of debt

(Dhaliwal et al. 2008; Brandon et al. 2004) and equity capital (Nam 2005). In sum, these studies

suggest that market participants: (1) use the NAS ratio as an audit quality signal, (2) price-protect

themselves from perceived reductions in audit quality due to NAS in a manner consistent with

agency theory, (3) impose economically significant costs on high-NAS registrants via this price

protection, and (4) provide an agency-based set of incentives for registrants to adjust the NAS ratio

in an effort to increase perceived audit quality.

Prior Research on the Determinants of NAS Purchases

Prior research examining the explicit relation between agency conflict variables and the NAS

fee ratio is relatively limited. Examples include Parkash and Venable (1993), Firth (1997), and

Abbott et al. (2003a), among others. Parkash and Venable (1993) examine the relation between

recurring NAS fees and proxies for agency costs during the temporary ASR 250 time period of

1979–1981. However, it is important to recognize that the NAS fee environment studied by Parkash

and Venable (1993) was quite different compared to the 2000–2001 period. Specifically, Parkash

and Venable (1993) find a mean (median) NAS/audit fee ratio of 0.24 (0.17) for their sample of

Fortune 500 firms in 1979–1981 (the previous disclosure regime of ASR 250). In contrast, Abbott

et al. (2003b) document a mean (median) NAS/audit fee ratio of 1.60 (0.96) in 2000, which

represents a growth in NAS purchases (relative to audit fees) of at least 500 percent. The SECPS

(Securities and Exchange Commission Practice Section) data for the ASR 250 period suggested that

only 25 percent of firms purchased any NAS from their auditors and that only 5 percent incurred

NAS fees exceeding their audit fees (Abbott et al. 2003b). In contrast, Abbott et al. (2003b) showed

that more than 99 percent of sampled Big 5 auditees reported NAS purchases greater than zero in

the initial months of the current regime. Moreover, 51 percent of these reported an NAS fee greater

than the audit fee.

Does Mandated Disclosure Induce a Structural Change? 55

Auditing: A Journal of Practice & TheoryMay 2011

Parkash and Venable (1993) are able to partition NAS into recurring and nonrecurring

categories because ASR 250 required this distinction. They document a statistically significant,

positive relation between the recurring NAS/audit fee ratio and proxies for agency conflict, such as

managerial ownership and outside investment concentration. The authors also document a negative

relation between this ratio and leverage. Parkash and Venable (1993) do not find any inter-period

differences in slope coefficients between the initial year of study (1979) and the subsequent year

(1980), nor do they test for the relation between securities issuances and the NAS fee ratio. Similar

to Parkash and Venable (1993), Firth (1997) documents significant associations with certain agency

costs variables and NAS, using 1993 data from the U.K. However, neither study examines the

impact of the audit committee in the NAS purchase decision.

Using the initial year of the more recent NAS disclosure regime, Abbott et al. (2003a) extend

Parkash and Venable (1993) by examining the impact of audit committee involvement in the NAS

purchase decision. They posit that an effective audit committee’s demand for audit quality will

result in a reduced NAS/audit fee ratio, and find a negative relation between the presence of an

effective audit committee and the NAS/audit fee ratio.6 However, unlike Parkash and Venable

(1993) and Firth (1997), Abbott et al. (2003a) find little support for an agency cost-based demand

for a lower NAS/audit fee ratio. The authors state, ‘‘Given the time-frame and speed of the

(disclosure) rule’s enactment, the ability of managers to adjust the level of NAS . . . may have been

limited. This may explain why some of agency cost-based variables are not significant . . . in

subsequent periods, we may see a greater adjustment of NAS purchases in response to . . . the

response of the market to high NAS fee ratios.’’ Given the limitations of Parkash and Venable

(1993) and Firth (1997) and the findings of Abbott et al. (2003a), the current study extends and

complements prior literature by investigating whether the regulatory approach of prescribingmandated NAS disclosures can induce market discipline mechanisms consistent with agency cost

theory.

Hypothesis Development

The initial NAS disclosures proved to be enlightening to many interested parties. Much of the

investing public appeared surprised by both the frequency and magnitude of NAS services (Weil

2001). In particular, then SEC Commissioner Laura Unger, stated ‘‘we were all quite surprised to

learn this . . . in fact, the numbers appear to demonstrate the problem may be larger than we

originally thought’’ (Unger 2001). In a response to these disclosures and perhaps to the market’s

initial reaction to them, the (then) Big 5 audit firms intensely lobbied the SEC to change the

definitions of audit and nonaudit services.7 The lobbying efforts were successful, such that

beginning with the 2003 proxy season, the corresponding definitions of audit (nonaudit) services

were widened (narrowed) (SEC 2003).8

These developments have important implications for the current study. First, given the date that

the disclosure rules were enacted (November 15, 2000) and the lack of publicity about the proposed

regulation, it is very unlikely that NAS purchase decisions made by firms with December 31, 2000,

6 Note that the audit committee’s desire to reduce the NAS/audit fee ratio is present in the absence of NASdisclosures. The potential for disclosure in the context of litigation or SEC investigation, should allegations of amisstatement occur, is what motivates an effective audit committee to seek a reduction in the NAS/audit fee ratio.

7 This does not necessarily imply that the Big 4 performed market-reaction studies to the NAS disclosures. Therewere, however, numerous press articles that pointed to NAS as a potential factor in the Enron debacle, as well asto the demise of Arthur Andersen (McNamee 2002; Liesman et al. 2002; Weil 2001).

8 The SEC amended the definitions used in the disclosure regulation with the issuance of FTC release 33–8183,with early adoption for 2002 NAS purchases. The effect essentially reduced the NAS/audit fee ratio withoutcurtailing the supply of NAS provided (Weil and Rappaport 2003).

56 Abbott, Parker, and Peters

Auditing: A Journal of Practice & TheoryMay 2011

year-ends considered the potential for negative market reactions to NAS disclosures. This is

because the vast majority of 2000 NAS purchases would have been contracted by November 15,

2000, and contracting parties (i.e., management, audit committees, and auditors) could not have

anticipated the disclosure requirements and the market’s reaction—if any—to the disclosures at the

time of contracting. By contrast, the decisions to purchase NAS in 2001 most likely did incorporate

the potential impact of the market’s price protection reaction to the NAS disclosure. Collectively,

these events provide an opportunity to investigate whether the prescription of mandated NAS

disclosures induced a market-based response that structurally altered the relationship between NAS

purchases and agency- and governance-based company characteristics.9 Our agency-based

variables include insider ownership, leverage, external financing, and size. From a governance

perspective, we investigate the potential structural changes in the audit committee/NAS purchase

relation.

Inside Ownership

Following prior literature, we expect agency costs to decrease as insider ownership increases

due to the alignment of manager and owner incentives (DeFond 1992; Jensen and Meckling 1976).

Parkash and Venable (1993) argue that in the management-owned firm, managers have incentives

to capture the benefits of NAS from the incumbent external auditor, whereas the managers of

externally owned firms must weigh the potential benefits of NAS against the potential agency costs

induced by the perceived impairment of auditor independence. However, it is not clear that in the

absence of NAS disclosure the above trade-offs exist. This is consistent with the lack of significant

associations documented in Abbott et al. (2003a) between insider ownership and NAS purchased in

a nondisclosure environment.

In the presence of mandated NAS disclosure, market-imposed agency costs are more likely to

outweigh the potential benefits of NAS (Parkash and Venable 1993). Thus, we expect lower

(higher) levels of management ownership to be associated with lower (higher) perceived net

benefits from purchases of NAS when mandated disclosures are present. We anticipate the

disclosure environment and market reaction will increase management’s sensitivity to these

incentives. As such, we expect the coefficient estimate for insider ownership to increase under the

mandatory disclosure regime. To test this assertion, we compare the coefficient estimates in a period

when firms purchased NAS without mandated disclosures to the coefficient estimates in a period

with mandated disclosure. In turn, the test of our null hypothesis is binsider ownership2000 ¼binsider ownership2001. This leads to our first hypothesis (in alternative form):

H1: Mandatory NAS disclosures will create a positive association between insider ownership

and the NAS/audit fee ratio in comparison to the statistically insignificant association

documented in the nondisclosure regime.

Leverage

Chow (1982) and Parkash and Venable (1993) argue that higher levels of debt increase the

incentives for maintaining the perceived independence of the external auditor and thus, by

extension, decrease the level of NAS purchases. These authors posit that increased debt levels

correspond to more financial statement-based debt covenants, which require greater auditor

certification of compliance. However, it is unclear whether these underlying incentives could

9 We focus on the agency-based variables because the relations between these and the NAS purchase decisions arethose most likely to be structurally altered by the market’s perception of NAS as a proxy for audit quality.

Does Mandated Disclosure Induce a Structural Change? 57

Auditing: A Journal of Practice & TheoryMay 2011

impact NAS purchase decisions in a period when mandated disclosures were not anticipated. The

results of prior research suggest that the market’s initial perception of NAS was consistent with

NAS having a detrimental impact on auditor independence (Dhaliwal et al. 2008; Francis and Ke

2006; Higgs and Skantz 2006). As such, we assert that mandated disclosures will mitigate the

demand for NAS purchases in firms with greater levels of debt. Similar to our insider ownership

hypothesis, we test the leverage assertion by comparing the coefficient estimates in a period when

firms purchased NAS without mandated disclosures to the coefficient estimates in purchases in a

period with mandated disclosure. In turn, the test of the null hypothesis in this case is bleverage2000

¼ bleverage2001. This leads to our second hypothesis (in alternative form):

H2: Mandatory NAS disclosures will create a negative association between leverage and the

NAS/audit fee ratio, in comparison to the statistically insignificant association

documented in the nondisclosure regime.

External Financing

The results of Dhaliwal et al. (2008), Brandon et al. (2004), and Nam (2005) suggest that the

market imposed higher costs of debt and equity capital on firms with higher NAS once disclosures

were available. Dhaliwal et al. (2008) argue that the documented positive association between

higher interest rates and higher NAS purchases was a reaction to the perceived independence of the

firm’s auditors. This perception provides firms with an incentive to curtail NAS purchases from

auditors in a mandated disclosure environment. However, Abbott et al. (2003a) do not find a

significant relation between NAS fee ratios and demand for external financing in a nondisclosure

environment. Given the enhanced response of the capital markets, we expect that those firms

anticipating future external financing will curtail their NAS purchases under the mandatory

disclosure regime. Following the previous hypotheses, the test of the null hypothesis in this case is

bexternal financing2000¼ bexternal financing2001. This leads to our third hypothesis (in alternative

form):

H3: Mandatory NAS disclosure will create a negative relation between anticipated external

financing needs and the NAS/audit fee ratio, in comparison to the statistically insignificant

relation documented in the nondisclosure regime.

Size

Prior research generally finds a positive association between size and the purchase of NAS

(e.g., Palmrose 1986; Barkess and Simnett 1994; Firth 1997). The positive association is generally

attributable to the demands for services that come from larger companies exhibiting greater degrees

of complexity in systems design, as well as the demand for ‘‘one-off’’ consultancy associated with

company size. However, size is also associated with greater information asymmetry between

owners and their agents, creating greater market-imposed agency costs and greater demand for audit

quality among larger companies (DeFond 1992). As such, we expect larger companies to be more

sensitive to perceptions of impaired audit quality in the mandated disclosure environment and

reduce their demand for NAS from incumbent auditors accordingly.

Consistent with prior literature, we expect size to be positively associated with the demand for

NAS. However, we expect this association to decrease in the presence of mandated NAS

disclosures, consistent with the benefits of NAS being offset by the larger agency costs facing larger

companies. Following the previous hypothesis, we test this assertion by comparing parameter

estimates of company size in a period when companies made NAS purchase decisions without

mandated disclosure to purchase decisions made in a period with mandated disclosure. In turn, the

58 Abbott, Parker, and Peters

Auditing: A Journal of Practice & TheoryMay 2011

test of the null hypothesis in this case is bsize2000¼bsize2001. This leads to our fourth hypothesis (in

alternative form):

H4: Mandatory NAS disclosures will decrease the positive association between size and NAS/

audit fee ratio as documented in the nondisclosure regime.

Audit Committee Effectiveness

Our final hypothesis concerns the audit committee, a key stakeholder in the NAS purchase

decision. The role of the audit committee includes monitoring the financial reporting environment

of the company, and thus the perceived and real independence of auditors. Accordingly, we expect

effective audit committees to act as a mitigating factor in the purchase of NAS. Abbott et al.

(2003a) posit that litigation concerns arising from misstatements provide an incentive for audit

committees with high reputational investments to lower the NAS/audit fee ratio. Consistent with

their argument, they provide evidence of a significant, negative relation between ACE and the NAS

fee ratio. However, it remains an empirical question whether mandated disclosures will magnify the

negative association.

Gaynor et al. (2006) specifically investigate the impact of disclosure on the propensity of audit

committee members to lower the NAS/audit fee ratio. Gaynor et al. (2006) document a significantly

larger reduction in the NAS/audit fee ratio in a disclosure, rather than nondisclosure, setting. These

results are attributed to increased scrutiny by shareholders (and potential litigants) resulting from

the public dissemination of NAS information. However, Gaynor et al. (2006) utilize a laboratory

setting and thus do not provide archival evidence. We expect a relation between ACE and the NAS

fee ratio that is incrementally greater than that documented in Abbott et al. (2003a). The test of the

null hypothesis in this case is baudit committee2000¼ baudit committee2001. This leads to our final

hypothesis (in alternative form):

H5: Mandatory NAS disclosures will intensify the negative association between the presence

of an effective audit committee and the NAS/audit fee ratio as documented in the

nondisclosure regime.

RESEARCH DESIGN

Sample Selection

For comparative purposes, we utilize the sample previously used in Abbott et al. (2003a). Table

1 (Panel A) reconciles 2000 and 2001 observations. The original sample consisted of the 310

nonfinancial firms filing proxies with the SEC between February 5, 2001, and March 16, 2001, plus

an additional randomly chosen sample of 250 firms filing proxies from March 19, 2001, to June 30,

2001, for a total of 538 firms.10 Forty-seven firms merged, became private, or disappeared prior to

the release of the 2001 proxy statement, leaving 491 firms potentially available for inclusion. We

also deleted the 107 firms that were audited by Arthur Andersen or which switched auditors during

2001. These selection criteria control for distortions in NAS purchase decisions related to early

defections of Andersen clients, as this behavior may not accurately reflect the contracting decisions

made by these companies otherwise. Last, an additional 46 firms did not have sufficient information

10 The March 16, 2001, to June 30, 2001, sample was selected by creating a list of the firms filing during the periodin chronological order, and using systematic random sampling to generate sample of 250 firms from theapproximately 6,000 firms filing proxies within the period.

Does Mandated Disclosure Induce a Structural Change? 59

Auditing: A Journal of Practice & TheoryMay 2011

TABLE 1

Sample Selection Results

Panel A: Sample Reconciliation with Abbott et al. (2003a)

# of Sample Firms % of Original Sample

Original Abbott et al. (2003a) sample 538 100

Deleted firms:

Merged or acquired (8) (1.5)

Ceased reporting prior to issuance of 2001

proxy statement (32) (5.9)

Not included on Compustat in 2001 (7) (1.3)

Arthur Andersen clients or switched auditors (107) (19.9)

Total deleted firms (154) (28.6)

Firms potentially available for the current study 386 71.7

Insufficient data available on Compustat (46) (8.5)

Total used in regressions 338 63.0

Panel B: Industry Composition

Focus IndustryRelated Two-Digit

SIC Codes# of Sample

Firms % of SampleCompustat

Population %

Construction 15–17 5 1.5 1.0

Consumer Product

& Food 20–33 89 26.3 14.5

Energy 10–14, 46, 49 41 12.1 7.0

Financial Services 60–64, 67 3* 0.9 24.9

Information and

Communication 48, 73, 78, 79, 84 54 16.0 18.3

Manufacturing 34–39 104 30.8 18.2

Personal Services

and Healthcare 72, 80, 83 5 1.5 1.7

Professional,

Commercial,

Services, Education 75, 76, 82, 87, 89 4 1.1 2.3

Real Estate 65, 70 3 0.9 1.3

Retail and Wholesale 50–59 19 5.6 7.8

Transportation 40–42, 44, 45, 47 11 3.3 1.8

All Other 1, 2,7, 8, 99 0 0.0 1.2

Totals 338 100 100

* Firms included in this segment are from the insurance industry and nonbank financial services industry (i.e., brokeragehouses, etc.). Sample does not include banks and other financial institutions that face additional regulation unique to theirindustry.

60 Abbott, Parker, and Peters

Auditing: A Journal of Practice & TheoryMay 2011

on Compustat to calculate our additional financing variable. This resulted in a sample of 338 firms

available for both 2000 and 2001.11

Table 1 (Panel B) provides information about the distribution of industries in our sample

compared with the Compustat population. Our sample contains a higher proportion of consumer

products and food, energy, and manufacturing. Our sample also contains very few firms classified

as financial services firms, as Abbott et al. (2003a) excluded banking-related firms due to their

differing regulatory and financial structures. We performed t-tests and Mann-Whitney F-tests (not

reported) for differences in mean (median) total assets. We did not find any significant difference

between the sample and the Compustat population in terms of mean (median) size.

Regression Model

Following Abbott et al. (2003a), we employ the multivariate regressions below for years 2000

and 2001 to test our hypotheses.

NASAFRATIO2000;2001 ¼ b0 þ b1INOWN2000;2001 þ b2LEVERAGE2000;2001

þ b3FINANCE2000;2001 þ b4SIZE2000;2001 þ b5ACE2000;2001

þ b6BLOCK2000;2001 þ b7BIG42000;2001 þ b8ACQ2000;2001

þ b9CHGCEO2000;2001 þ b10RESTR2000;2001 þ b11RETURN2000;2001

þ e

where:

NASAFRATIO ¼ the ratio of total NAS fees (including nonaudit fees and any information

technology implementation fees) to total audit fees;

INOWN ¼ the cumulative percentage of voting control held by managers and directors;

LEVERAGE ¼ the ratio of long-term debt to total assets;

FINANCE ¼ the net cash flows derived from external financing deflated by total assets,

measured in the year subsequent to the NASAFRATIO year;

SIZE ¼ the natural log of total assets;

ACE ¼ an indicator variable equal to 1 if the audit committee is comprised entirely of

independent directors and meets at least four times during the year, and 0 otherwise;

BLOCK¼the cumulative ownership percentage of voting control held by blockholders holding at

least 5 percent of the outstanding common shares and who are unaffiliated with management;

BIG4¼ an indicator variable equal to 1 if the firm employs a Big 4 auditor, and 0 otherwise;

ACQ¼ the number of acquisitions made by the firm during the year or in the prior two years;

CHGCEO¼ an indicator variable equal to 1 if a new external CEO has been appointed during

the year or in the previous two years, and 0 otherwise;

RESTR¼ an indicator variable equal to 1 if a firm restructuring occurred during the year or in

the previous two years, and 0 otherwise; and

RETURN ¼ the total stock return (stock appreciation plus dividends) for the prior year.

Our primary tests compare the regression results from the fiscal year ended 12/31/2000 to

results pertaining to the fiscal year ended 12/31/2001.12 The subscripts on each variable indicate

11 Our overall sample size compares favorably with the per-year sample of Parkash and Venable (1993) and issomewhat smaller than that of Firth (1997), who includes 500 firms.

12 We collect year 2000 (2001) proxy data via the calendar year 2001 (2002) proxy statement as the 2001 (2002)proxy statement relates to the fiscal year ended 12/31/2000 (2001). In instances where the proxy statement forfiscal year 2000 (2001) was issued in the final two months of calendar year 2000 (2001) (less than 3 percent ofour observations), the applicable variables (NASAFRATIO, INOWN, ACE, CHGCEO, and BLOCK) are retrievedfrom proxy statements released in calendar year 2000 (2001) relating to fiscal year 2000 (2001).

Does Mandated Disclosure Induce a Structural Change? 61

Auditing: A Journal of Practice & TheoryMay 2011

that we run the regression model twice, once for the nondisclosure year (2000) and once for the first

year of mandatory disclosure (2001). Since our objective is to compare the results of the model

across the differing disclosure regimes, we then use a Chow test to determine whether the

coefficient estimates from the two models are statistically different. The Chow tests support our

hypotheses if the coefficient estimates significantly differ in the predicted directions between 2000

(nondisclosure period) and 2001 (disclosure period).

Variable Definitions

Table 2 describes the variables in detail.13 Our dependent variable (NASAFRATIO) is the ratio

of total NAS fees (including information technology, or IT, fees) to audit fees. Prior research

TABLE 2

Variable Definitions

Variable Name Description

AUDITFEE ¼ total audit fees (from proxy statements);

ITFEE ¼ total information technology implementation fees (from proxy statements);

NONAUDITFEE ¼ total nonaudit fees (excluding information technology fees) (from proxy statements);

NASAFRATIO ¼ ratio of total nonaudit service fees (including nonaudit fees and any information

technology implementation fees) to total audit fees;

DECRRATIO ¼ indicator variable with a value of 1 if the 2001 NASAFRATIO was less than the 2000

NASAFRATIO, 0 else;

DECRNAS ¼ indicator variable with a value of 1 if the firm’s total 2001 NAS fees (ITFEE þNONAUDITFEE) were less than firm’s total 2000 NAS fees, 0 else;

INOWN ¼ cumulative percentage of voting control held by managers and directors (from proxy

statements);

LEVERAGE ¼ ratio of long-term debt (Compustat item 9) to total assets (Compustat item 6);

FINANCE ¼ net cash flows received from external financing activities. Compustat item formula

(108 � 115 � 127) þ (111 � 114 � 301) following Bradshaw et al. (2006);

SIZE ¼ natural log of total assets (in millions) (Compustat item 6);

ACE ¼ audit committee effectiveness variable coded 1 for an audit committee that is

composed entirely of outside directors and meets at least four times annually, 0 else

(from proxy statements);

BLOCK ¼ cumulative ownership percentage of voting control held by blockholders holding at

least 5 percent of the outstanding common shares and are unaffiliated with

management (from proxy statements);

BIG4 ¼ indicator variable set to 1 if the firm employs a Big 4 auditor during the year, 0 else

(Compustat item 149);

ACQ ¼ indicator variable set to 1 if the firm made at least one acquisition during the year and

two preceding years, 0 else (based on Compustat item 129);

CHGCEO ¼ indicator variable set to 1 if a new external CEO has been appointed during the year

and two preceding years, 0 else (from proxy statements);

RESTR ¼ indicator variable set to 1 if the firm reported restructuring costs (Compustat item 376)

during the year, 0 else; and

RETURN ¼ total stock return (stock appreciation plus dividends) (Compustat items 26 and 199).

13 NASAFRATIO, INOWN, ACE, BLOCK, and CHGCEO are collected by hand from the applicable proxystatement. We collect the remaining variables from Compustat. More specific information is included inTable 2.

62 Abbott, Parker, and Peters

Auditing: A Journal of Practice & TheoryMay 2011

commonly uses this ratio as a proxy for perceived auditor independence (e.g., Davis and Hollie

2008; Dhaliwal et al. 2008; Krishnan et al. 2005; Brandon et al. 2004). In subsequent tests, we also

include alternative proxies for our dependent variable, including NAS fees scaled by total assets,

total sales, and total fees. We also use logistic regressions that utilize binary dependent variables

identifying reductions in NAS purchases.

INOWN captures the degree of voting control held by managers and directors. LEVERAGE is

the ratio of long-term debt to total assets. We measure securities issuance activities (FINANCE)

following the formula found in Bradshaw et al. (2006), recognizing inherent timing differences

between NAS purchases and NAS disclosures. For example, assuming Company A purchased

$300,000 in NAS services during year 2000, this $300,000 would be disclosed to the market during

2001 in the annual proxy statement. In 2001, Company A would (1) disclose $300,000 in year 2000

NAS purchases, (2) observe the general market reaction to the initial NAS disclosures, and (3)

recognize that 2001 NAS purchases would be disclosed in 2002, thus (potentially) impacting the

cost of capital for debt/equity issuances made in 2002. Accordingly, for the 2000 (2001)

regressions, we utilize 2001 (2002) values of the Bradshaw et al. (2006) FINANCE variable.

We measure SIZE as the natural log of total assets. Our hypothesis generally predicts that the

SIZE-induced demand (positive coefficient) for NAS will decrease during the post-disclosure

environment due to the increase in agency costs, which is positively associated with larger firms.

ACE, coded ‘‘1,’’ is the audit committee, is entirely independent, and meets at least four times per

year. We expect the mandatory disclosure regime to increase the sensitivity of audit committees to

the scrutiny of stakeholders concerning the disclosure of NAS purchases.

In addition to our test variables, we control for other factors that prior research has posited to

affect the NAS fee ratio. For these control variables, we do not believe the mandated NAS disclosure

environment will impact the relation between these determinants and the NAS/audit fee ratio. We

define BLOCK as the cumulative percentage of outstanding stock held by unaffiliated shareholders

with 5 percent or greater stakes. Following the results documented in Abbott et al. (2003a), we

expect this variable to be negative in the initial year as blockholders use the financial statements as a

means of monitoring and, thus, discourage high levels of NAS purchases. However, we do not

expect that mandated NAS disclosures will alter this coefficient estimate.14 The Big 4 auditors offer a

wider array of expertise and have more aggressively expanded into consulting services, thus we

control for the presence of a Big 4 auditor via our dichotomous BIG4 variable. As in Firth (1997), we

expect a positive association between BIG4 and our dependent variable. However, there is not an apriori reason for the mandated NAS disclosures to either intensify or mitigate this relation.

Firth (1997) notes that certain situations, such as new acquisitions (ACQ), CEO turnover

(CHGCEO), and restructuring (RESTR), give rise to increased demand for consulting services,

regardless of the NAS disclosure environment. Hence, we predict a positive association between the

NAS ratio and such special situations, but do not expect that changes in the disclosure environment

will impact this association. Firth (1997) also asserts that a poorly performing company may

demand more external consulting services to improve profitability. Firth (1997) finds significantly

higher NAS fee ratios when stock returns are lower, and therefore we expect a negative association

between the NAS fee ratio and prior-period stock returns (RETURN). Similar to ACQ, RESTR, and

14 From the perspective of the Abbott et al. (2003a) study, BLOCK is treated as an agency variable because theseauthors expect the NASAFRATIO to vary with the presence of parties who have an interest in the credibility offinancial reporting. However, BLOCK differs from our other test variables in that it is unclear whether the publicdisclosure of audit and nonaudit fees would have any impact on the relationship documented by Abbott et al.(2003a). We note that it is possible that large blockholders would be able to influence the firm’s NAS purchasedecisions, regardless of whether the audit and nonaudit fee information is public or not. Thus, it is difficult todetermine whether a hypothesis that predicts a change in the relationship between BLOCK and theNASAFRATIO prompted by new public disclosures is warranted. Thus, we treat BLOCK as a control variable.

Does Mandated Disclosure Induce a Structural Change? 63

Auditing: A Journal of Practice & TheoryMay 2011

CHGCEO, we do not expect the disclosure environment to impact the predicted negative relation

between RETURN and our dependent variable.

RESULTS

Descriptive Results

Table 3, Panels A and B, shows a comparison of the descriptive statistics for fiscal years 2000

and 2001. Fees (not adjusted for inflation) were somewhat larger in all categories in 2001,

compared to 2000. The median audit fee increased by approximately 5.9 percent, while the median

NAS fee increased by only 3.5 percent. When we delete the single, largest $79.5 ($35) million NAS

fee (not reported) in 2001 (2000), the mean NAS purchase decreases from $1,588,663 to

$1,478,044, or a fairly large (and statistically significant) 7 percent reduction in NAS from 2000 to

2001 (we report our sensitivity tests for outliers subsequently). This compares to an increase in

mean audit fees from $818,461 to $836,876 for the same period. In addition, we believe that

increases in nonaudit fees across the 25th and 50th percentiles most likely represent

‘‘continuations’’ of existing NAS arrangements, rather than registrants actively purchasing more

NAS. More specifically, NAS purchases at the 25th (50th) percentile increased less than 4 percent

(3.5 percent)—close to the U.S. inflation rate for the period. Moreover, NAS purchases at the 75th

percentile decreased from $1,495,000 to $1,361,164, representing a large (and statistically

significant) decline of nearly 9 percent. In contrast, audit fees increased at the 25th, 50th, and 75th

percentiles (as well as the mean audit fee) from 2000 to 2001. One interpretation consistent with

these results is that while the overall demand for NAS remained positive, purchases of NAS

services from incumbent auditors decelerated considerably in the wake of the market’s generally

unfavorable view of or reaction to the purchase of NAS (e.g., Unger 2001; Dhaliwal et al. 2008;

Brandon et al. 2004; Nam 2005).15

Table 3, Panel C, describes our DECRNAS and DECRRATIO variables. To further dif-

ferentiate those firms with increases versus decreases in NAS fees, we also utilize logistic

regressions in subsequent tests where we define the dependent as DECRNAS (coded ‘‘1’’ if the

total 2001 NAS fees are less than the 2000 NAS fees) and DECRATIO (coded ‘‘1’’ if the NAS

fee ratio decreased from 2000 to 2001). Of our sample, 177 firms (52.4 percent) exhibited

decreases in their NAS fees from 2000 to 2001. In contrast, 155 (6) firms exhibited increases (no

change) in their NAS fees.16 Similarly, 186 firms (55.2 percent) exhibited a decrease in their

NAS fee ratio from 2000 to 2001. In contrast, the remaining 146 (6) firms exhibited increases (no

change) in their NAS ratio.

With respect to our remaining variables, our sample firms experienced a slightly higher level of

restructurings (mean of 0.10 in 2001 versus 0.086 in 2000) and a slightly lower incidence of CEO

change (mean of 0.044 in 2000 and 0.029 in 2001). In 2000, 44 percent of the sample firms had

audit committees that were entirely independent and met at least four times during the year covered

by the proxy statement. In 2001, 48 percent of committees met these criteria. In 2000, the mean

15 The annualized growth rate of NAS in the U.S. for the ten-year period through 2000 was approximately 16.5percent (Jenkins and Krawczyk 2003). This compares to our mean NAS growth rate of less than 4 percent. Thus,it appears that the rapid growth in NAS purchases from incumbent auditors significantly decelerated in post-disclosure regime.

16 Less than 3 percent of our sample reported zero NAS fees, and there was almost complete overlap of these firmsacross 2000 and 2001, resulting in the six firms who exhibited no change in their NAS fees. Seven out of 338firms (or approximately 2.07 percent of our sample) had a NASAFRATIO of 0 in 2000, and six firms (or 1.77percent of our sample) had a NASAFRATIO of 0 in 2001. All six firms with a NASAFRATIO of 0 in 2001 had asimilar ‘‘0’’ value in 2000. Eliminating these firms did not qualitatively affect our results. Consequently, wereported OLS results in preference to the less common Tobit analysis (discussed in the sensitivity tests section).

64 Abbott, Parker, and Peters

Auditing: A Journal of Practice & TheoryMay 2011

TABLE 3

Descriptive Data

Panel A: Descriptive Statistics for 338 Sample Firms for Fiscal Year 2000

Variable Mean Median Min. Max. 25th % 75th % Std. Dev.

AUDITFEE $818,461 $424,524 $18,000 $6.7m $138,700 $844,695 $1,325,671

ITFEE $704,201 $0 $0 $17.9m $0 $0 $3,730,134

NONAUDITFEE $1,687,513 $306,920 $0 $35m $84,500 $1,495,000 $3,681,981

NASAFRATIO 1.984 1.092 0.000 17.95 0.485 2.347 2.499

INOWN 0.179 0.109 0.004 0.887 0.025 0.305 0.202

LEVERAGE 0.204 0.183 0.000 0.776 0.013 0.294 0.199

FINANCE 0.024 �0.006 �0.114 0.278 �0.052 0.046 0.008

ASSETS (in mil) $4,227 $611 $2.008 $47,603 $114 $2,861 $13,123

ACE 0.444 0.000 0.000 1.000 0.000 1.000 0.496

BLOCK 0.148 0.118 0.000 0.878 0.000 0.256 0.146

BIG4 0.940 1.000 0.000 1.000 1.000 1.000 0.236

ACQ 0.236 0.000 0.000 1.000 0.000 0.000 0.599

CHGCEO 0.044 0.000 0.000 1.000 0.000 0.000 0.206

RESTR 0.086 0.000 0.000 1.000 0.000 0.000 0.280

RETURN 0.049 0.025 �0.245 0.548 �0.022 0.233 0.504

Panel B: Descriptive Statistics for 338 Sample Firms for Fiscal Year 2001

Variable Mean Median Min. Max. 25th % 75th % Std. Dev.

AUDITFEE $836,876 $449,750 $26,000 $7.6m $157,025 $880,301 $1,346,228

ITFEE $640,475 $0 $0 $41.3m $0 $0 $4,262,491

NONAUDITFEE $1,708,878 $317,771 $0 $79.5m $87,798 $1,361,164 $4,167,371

NASAFRATIO 1.738 0.986 0.000 20.13 0.493 2.311 2.109

INOWN 0.163 0.101 0.003 0.856 0.024 0.287 0.225

LEVERAGE 0.199 0.185 0.000 0.778 0.012 0.291 0.198

FINANCE 0.021 �0.006 �0.112 0.224 �0.058 0.039 0.101

ASSETS (in mil) $4,540 $621 $2.003 $49,005 $118 $2,902 $13,774

ACE 0.476 0.000 0.000 1.000 0.000 1.000 0.499

BLOCK 0.149 0.112 0.000 0.876 0.000 0.243 0.149

BIG4 0.940 1.000 0.000 1.000 1.000 1.000 0.252

ACQ 0.254 0.000 0.000 1.000 0.000 0.000 0.613

CHGCEO 0.029 0.000 0.000 1.000 0.000 0.000 0.169

RESTR 0.104 0.000 0.000 1.000 0.000 0.000 0.304

RETURN 0.043 0.048 �0.333 0.605 �0.031 0.133 0.778

Panel C: Proportion of 338 Firms with Decreasing NAS from 2000–2001

Variable Mean Median Min. Max. 25th % 75th % Std. Dev.

DECRRATIO 0.524 1.000 0.000 1.000 0.000 1.000 0.4994

DECRNAS 0.552 1.000 0.000 1.000 0.000 1.000 0.4964

All variables are defined in Table 2, with the exception of ASSETS, which are denoted in millions, and are logged forregression purposes.

Does Mandated Disclosure Induce a Structural Change? 65

Auditing: A Journal of Practice & TheoryMay 2011

(median) total assets of our sample firms were $4.2 billion ($611 million), and in 2001, the mean

(median) was $4.5 billion ($621 million). Non-Big 4 auditors account for 9.4 percent (9.3 percent)

of the sample in 2000 (2001). Other variables showed little change between years.

We also conducted tests of the inter-period correlation from 2000 to 2001 for each of the test

and control variables (not reported). We document very high, significant, inter-period Pearson

pairwise correlations for all the independent variables except those measuring external financing,

acquisitions, CEO change, restructurings, and return.17 It seems reasonable that there would be

relatively little year-to-year change in variables such as leverage, managerial ownership, audit

committee characteristics, etc. It also seems reasonable that acquisitions, restructurings, CEO

changes, returns, and capital infusions would be less likely to be repeated in successive years. The

high correlations on some variables should increase our ability to isolate the effects of disclosure on

NAS purchasing behavior. In effect, only the disclosure environment is manipulated, while most of

our independent variables remain relatively constant across the two sample periods.

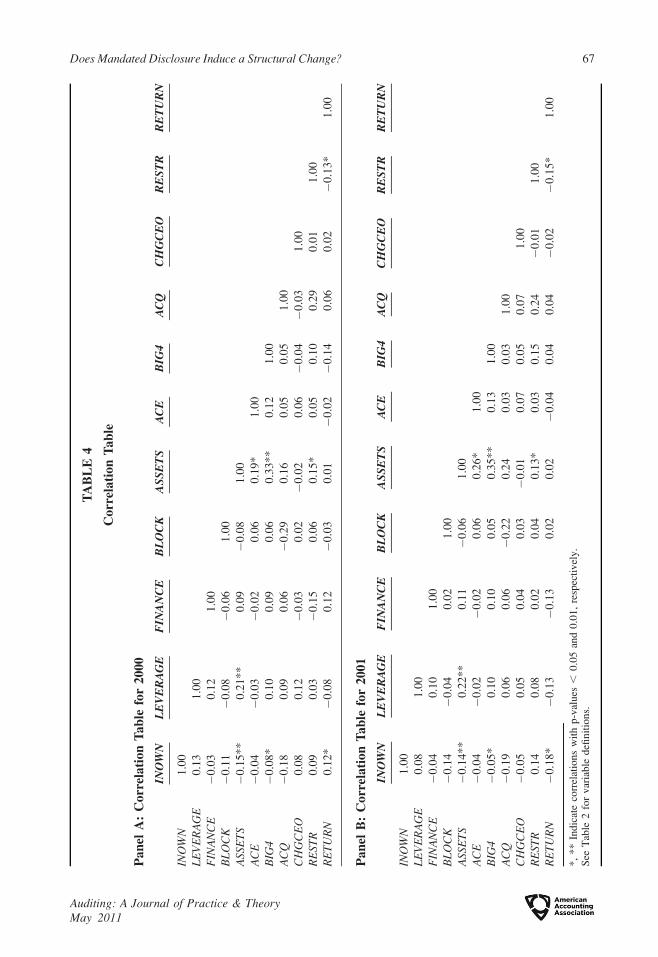

Table 4, Panels A and B, shows the cross-sectional correlations between the independent

variables for 2000 and 2001. Few of the correlations are significant, and many of the significant

correlations relate to size. In both years, ASSETS exhibits a significant positive correlation with

BIG4, LEVERAGE, and RESTR, and a negative correlation with INOWN. Profitability (RETURN) is

negatively correlated with restructuring and Big 4 auditor, and positively correlated with inside

ownership. Correlations between the independent variables are qualitatively similar within each

year, with the exception of the correlation between RETURN and BIG4, which is not significant in

2001. The similar correlations are consistent with our use of the same firms in our 2000 and 2001

sample years. Tests for multicollinearity (Belsley et al. 1980) did not reveal any areas of concern.

Univariate Results

Table 5 partitions the sample by increases or decreases in the NAS fee ratio (Panel A) and

whether NAS fees increased or decreased overall (Panel B). Panel A shows that the 189

observations that exhibited smaller NAS fee ratios in 2001 (relative to 2000) had significantly lower

inside ownership and were less likely to restructure. These firms were larger and more likely to seek

external financing. Panel B shows similar results when considering the 177 observations with lower

NAS fees in 2001 (compared to 2000) in dollar terms. However, high leverage does not appear to

spur reduction in subsequent year NAS fees. The univariate results are consistent with our first,

third, and fourth hypotheses.

The univariate results for our audit committee variable support our final hypothesis. As

expected, firms with effective audit committees were more likely to decrease their NAS purchases

in terms of both dollars and as a percentage of audit fees. This is consistent with effective audit

committees being more responsive to disclosed NAS, as NAS disclosure may serve as a potential

trigger for litigation (Huang et al. 2008; Church and Zhang 2005).

Chow Tests and Multivariate Results

Overall, the multivariate results corroborate the patterns documented in the univariate tests and

support the related hypotheses. For comparative purposes, the first column in Table 6 shows the

regression results for 2000, the year firms purchased NAS without the presence of mandatory

17 As an example, we calculated the pairwise correlation between our ACE variable values of 2000 and ACEvariable values in 2001. The pairwise correlation coefficient equaled 0.8755, suggesting very little change inACE between the two years. The inter-period correlations for INOWN, LEVERAGE, SIZE, and BLOCK are 0.84,0.94, 0.94, and 0.84, respectively. The inter-period correlation for BIG4 is 1.0, as we eliminated any firm that hadchanged auditors during 2001.

66 Abbott, Parker, and Peters

Auditing: A Journal of Practice & TheoryMay 2011

TA

BL

E4

Co

rrel

ati

on

Ta

ble

Pa

nel

A:

Co

rrel

ati

on

Ta

ble

for

20

00

INO

WN

LE

VE

RA

GE

FIN

AN

CE

BL

OC

KA

SS

ET

SA

CE

BIG

4A

CQ

CH

GC

EO

RE

ST

RR

ET

UR

N

INO

WN

1.0

0

LE

VE

RA

GE

0.1

31

.00

FIN

AN

CE

�0

.03

0.1

21

.00

BL

OC

K�

0.1

1�

0.0

8�

0.0

61

.00

ASS

ET

S�

0.1

5*

*0

.21

**

0.0

9�

0.0

81

.00

AC

E�

0.0

4�

0.0

3�

0.0

20

.06

0.1

9*

1.0

0

BIG

4�

0.0

8*

0.1

00

.09

0.0

60

.33

**

0.1

21

.00

AC

Q�

0.1

80

.09

0.0

6�

0.2

90

.16

0.0

50

.05

1.0

0

CH

GC

EO

0.0

80

.12

�0

.03

0.0

2�

0.0

20

.06

�0

.04

�0

.03

1.0

0

RE

STR

0.0

90

.03

�0

.15

0.0

60

.15

*0

.05

0.1

00

.29

0.0

11

.00

RE

TU

RN

0.1

2*

�0

.08

0.1

2�

0.0

30

.01

�0

.02

�0

.14

0.0

60

.02

�0

.13

*1

.00

Pa

nel

B:

Co

rrel

ati

on

Ta

ble

for

20

01

INO

WN

LE

VE

RA

GE

FIN

AN

CE

BL

OC

KA

SS

ET

SA

CE

BIG

4A

CQ

CH

GC

EO

RE

ST

RR

ET

UR

N

INO

WN

1.0

0

LE

VE

RA

GE

0.0

81

.00

FIN

AN

CE

�0

.04

0.1

01

.00

BL

OC

K�

0.1

4�

0.0

40

.02

1.0

0

ASS

ET

S�

0.1

4*

*0

.22

**

0.1

1�

0.0

61

.00

AC

E�

0.0

4�

0.0

2�

0.0

20

.06

0.2

6*

1.0

0

BIG

4�

0.0

5*

0.1

00

.10

0.0

50

.35

**

0.1

31

.00

AC

Q�

0.1

90

.06

0.0

6�

0.2

20

.24

0.0

30

.03

1.0

0

CH

GC

EO

�0

.05

0.0

50

.04

0.0

3�

0.0

10

.07

0.0

50

.07

1.0

0

RE

STR

0.1

40

.08

0.0

20

.04

0.1

3*

0.0

30

.15

0.2

4�

0.0

11

.00

RE

TU

RN

�0

.18

*�

0.1

3�

0.1

30

.02

0.0

2�

0.0

40

.04

0.0

4�

0.0

2�

0.1

5*

1.0

0

*,

**

Indic

ate

corr

elat

ions

wit

hp-v

alues

,0.0

5an

d0.0

1,

resp

ecti

vel

y.

See

Tab

le2

for

var

iable

defi

nit

ions.

Does Mandated Disclosure Induce a Structural Change? 67

Auditing: A Journal of Practice & TheoryMay 2011

disclosure requirements. The results show that in year 2000, none of our test variables are significant

except SIZE and ACE, consistent with the Abbott et al. (2003a) results from the original sample. The

significance of SIZE is also consistent with larger companies having more complex systems and a

wider range of activities in which NAS can add value to the client (Firth 1997). The significance of

ACE is as expected, given the audit committee’s concerns about monitoring auditor independence.

We then turn our attention to the results for 2001, the first year in which firms purchased NAS

conditioned upon mandatory disclosure. In general, we see that each of our test variables (INOWN,

FINANCE, SIZE, ACE) is significant and has the predicted sign, with the exception of LEVERAGE,

TABLE 5

Univariate Analysis

Panel A: Decreases and Increases in NAS/Audit Fee Ratios in 2001

Variable

Mean for Firmswith Decreased

NAS/Audit Fee Ratio

Mean for Firmswith Increased

NAS/Audit Fee Ratio F-statistic

INOWN 0.126 0.169 4.888*

LEVERAGE 0.189 0.227 1.013

FINANCE 0.035 �0.005 5.033*

ASSETS (in mil) $4,888.992 $4,103.115 6.018*

ACE 0.561 0.369 9.224**

BLOCK 0.143 0.158 1.005

BIG4 0.923 0.945 0.112

ACQ 0.238 0.275 0.224

CHGCEO 0.026 0.034 0.777

RESTR 0.079 0.134 6.881*

RETURN 0.045 0.041 0.995

Observations n ¼ 189 n ¼ 149

Panel B: Decreases and Increases in NAS Fees (in dollars) in 2001

Variable

Mean for Firmswith DecreasedNAS Fees ($)

Mean for Firmswith IncreasedNAS Fees ($) F-statistic

INOWN 0.133 0.163 5.012*

LEVERAGE 0.194 0.212 0.998

FINANCE 0.033 �0.005 5.278*

ASSETS (in mil) $4,905.077 $4,082.445 5.998*

ACE 0.559 0.379 9.138**

BLOCK 0.143 0.157 1.322

BIG4 0.924 0.943 0.130

ACQ 0.237 0.273 0.189

CHGCEO 0.028 0.031 0.552

RESTR 0.073 0.137 7.337*

RETURN 0.044 0.043 1.002

Observations n ¼ 177 n ¼ 161

*, ** Significant at p-values less than 0.05 and 0.01, respectively.See Table 2 for all variable definitions.

68 Abbott, Parker, and Peters

Auditing: A Journal of Practice & TheoryMay 2011

which was insignificant in both sample periods. To ascertain whether the disclosure environment

induces a change in the regression coefficients, we next conduct Chow tests. Our Chow tests,

discussed in greater detail in the succeeding paragraphs, support H1, H3, H4, and H5.

INOWN was negative and insignificant in 2000, and positive and significant in 2001. The

results of the Chow test show that the coefficient in 2001 is significantly different from the

coefficient in 2000 (p , 0.01 level). The tests support the prediction that greater managerial

ownership is associated with higher NAS purchases from the auditor when fees are subject to

disclosure, but not when firms purchase NAS in the absence of disclosures. This is consistent with

the need to weigh the benefits of NAS against the associated agency costs in the disclosure

environment. Similarly, the FINANCE variable also displays results consistent with the disclosure-

induced agency costs predicted by the hypotheses. The multivariate results suggest that firms

engaging in future financing exhibit a significantly negative association with the NAS fee ratio in

year 2001, but that such a relation was nonexistent in 2000. The Chow tests confirm that the 2001

and 2000 coefficients are significantly different from each other. Firms facing the need to raise

capital appear to be sensitive to the disclosure-induced agency costs of purchasing NAS. Thus, they

appear to have constrained their purchases of NAS once it became clear that the market imposed

higher costs of capital on firms disclosing higher NAS fee ratios.

We note the change in purchasing patterns based on company size (SIZE) continues to support

our fourth hypothesis. Although larger firms were more likely to purchase greater amounts of NAS

in both years, our Chow test confirms a significant decrease in the magnitude of this association in

the subsequent year. The decrease in magnitude of this coefficient is consistent with larger firms

being more sensitive to political costs (and concomitant market-imposed agency costs). This

TABLE 6

Regression Results

NASAFRATIO ¼ b0 þ b1INOWN þ b2LEVERAGEþ b3FINANCE þ b4SIZEþ b5ACE þ b6BLOCK þ b7BIG4þ b8ACQþ b9CHGCEOþ b10RESTRþ b11RETURN þ e

Variable Year 2000 Parameter Estimate t-stat Year 2001 Parameter Estimate t-stat

Intercept �2.984 �3.998** �2.916 �3.099**,a

INOWN �0.461 �0.776 0.393 3.692**,a

LEVERAGE 0.033 0.858 �0.297 �1.001

FINANCE 0.554 0.444 �0.152 �2.995**,a

SIZE 0.391 5.458** 0.364 4.192**,a

ACE �0.687 �3.449** �1.338 �4.985**,a

BLOCK �1.684 �2.446* �1.548 �2.362*

BIG4 0.543 0.885 0.448 0.885

ACQ �0.395 �0.788 �0.425 �0.598

CHGCEO 0.122 0.208 0.103 0.288

RESTR 1.063 2.003* 0.777 2.113*

RETURN 0.003 0.668 �0.081 �0.344

n ¼ 338 Adj R2 ¼ 0.1702 Adj R2 ¼ 0.2975 n ¼ 338

*, ** Significant at p-levels of less than 0.05 and 0.01, respectively.a Chow tests for differences in coefficients (year 2000 versus year 2001) significant at the 1 percent level. We do notmake a directional prediction for the effect of disclosure on our control variables, and thus the significance level fordifferences in the control variable coefficients reflects a two-tailed test.All variables per Table 2, except SIZE, which is the natural log of total assets (in millions).

Does Mandated Disclosure Induce a Structural Change? 69

Auditing: A Journal of Practice & TheoryMay 2011

suggests that the disclosures provided agency cost incentives for larger firms to curb their NAS

purchases to a greater extent than smaller firms.

Although firms with effective audit committees (ACE) are associated with relatively lower

levels of NAS in both years, the Chow test for differences in coefficient estimates between years

confirms that this negative association increases during the disclosure period (2001). This supports

the hypothesis that effective audit committees are more responsive to the level of NAS purchases

when they know that such purchases are subject to disclosure. This also provides empirical, archival

support for the results of Gaynor et al. (2006).

With respect to the control variables, our Chow test (two-tailed) for the difference in the

coefficients is not significant for blockholder ownership (BLOCK), although the coefficients exhibit

a significantly negative association with the purchase of NAS in both years. We speculate that the

element of public disclosure might be less important to blockholders who might have access to

information about a firm’s NAS purchases, or who may have the ability to influence the NAS

sourcing decision in the absence of public disclosure. Chow tests for differences in the coefficients

for our remaining control variables (BIG4, ACQ, CHGCEO, RESTR, and RETURN) are not

significant, suggesting that the mandated NAS disclosures did not structurally alter the relation

between these independent variables and the NAS/audit fee ratio.

We also observed a dramatic increase in the explanatory power of the agency-based demand

models from the initial disclosure year 2000 (R2¼ 0.1702) to year 2001 (R2¼ 0.2975). An F-test

for differences in the explanatory power of the regression models was significant at p-value , 0.01.

Overall, our results are consistent with firms choosing to adjust their NAS purchasing patterns once

it was clear that the market would impose agency costs on companies disclosing larger amounts of

NAS.

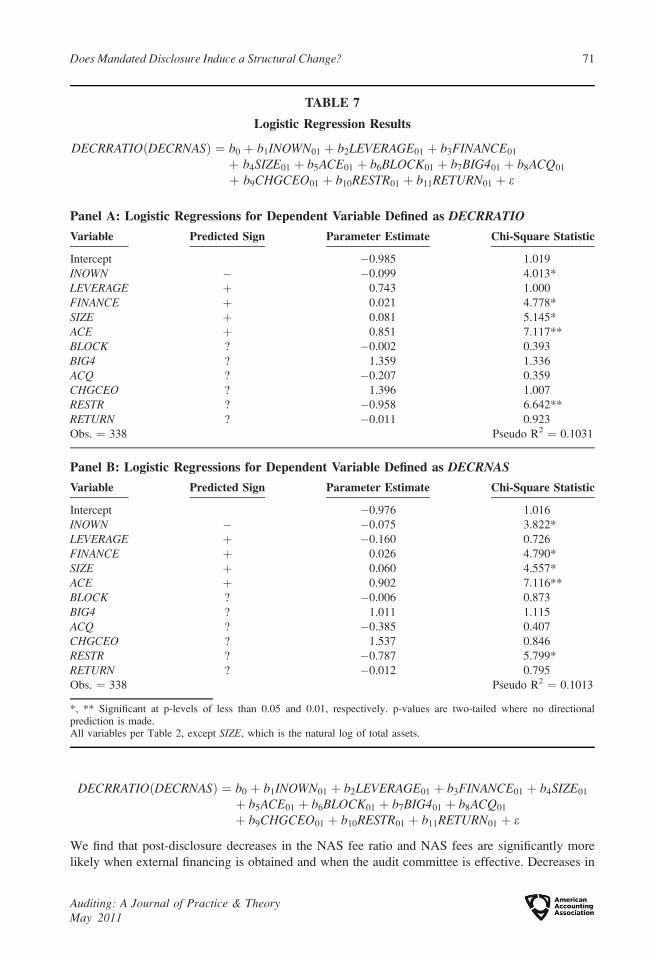

Logistic Regressions

While the market’s unfavorable reaction to the initial NAS disclosures was statistically and

economically significant, the overwhelming majority of firms continued to purchase some amount

of NAS in the mandatory disclosure environment. Given the size of the percentage changes of fees

(see descriptive statistics in Table 3), it appears that, in general, most firms either maintained their

current level of NAS services or decreased their purchases. However, as described in Table 3, some

firms exhibited increases in NAS fees. A continuation (or even increase) of NAS purchases is

consistent with companies continuing to weigh the potential costs and benefits from these types of

services, even in the presence of mandated disclosures. Thus, we extended our tests to discern

whether our NAS ratio results are consistent with certain firms decreasing their total NAS purchases

in response to newly imposed agency-related costs created by the disclosure environment. We

utilize logistic regressions where we define the dependent variables as DECRRATIO (coded 1 if the

sample firm decreased the NAS fee ratio from 2000 to 2001) and DECRNAS (coded 1 if the firm

decreased its purchases of NAS from the auditor in dollar terms from 2000 to 2001).18 Table 7

shows the results of these additional logistic regressions. The regression model is as follows:

18 We measure our independent variables using their 2001 values. However, one might easily argue that the 2000variables might be relevant to 2001 NAS purchases under some conditions. As a sensitivity test, we conductedlogistic regressions by substituting the 2000 values for our disclosure-impacted variables ACE, SIZE, andINOWN (and kept the CEOCHG, RESTR, ACQ, and RETURN variables intact with their 2001 values) and theresults are substantively unchanged. As such, we believe we have effectively isolated the impact of the change inNAS disclosure on purchasing behavior. We do not utilize changes in our independent variables becauseconceptually our hypotheses relate to how the disclosure environment in 2001 alters relations among ourvariables.

70 Abbott, Parker, and Peters

Auditing: A Journal of Practice & TheoryMay 2011

DECRRATIOðDECRNASÞ ¼ b0 þ b1INOWN01 þ b2LEVERAGE01 þ b3FINANCE01 þ b4SIZE01

þ b5ACE01 þ b6BLOCK01 þ b7BIG401 þ b8ACQ01

þ b9CHGCEO01 þ b10RESTR01 þ b11RETURN01 þ e

We find that post-disclosure decreases in the NAS fee ratio and NAS fees are significantly more

likely when external financing is obtained and when the audit committee is effective. Decreases in

TABLE 7

Logistic Regression Results

DECRRATIOðDECRNASÞ ¼ b0 þ b1INOWN01 þ b2LEVERAGE01 þ b3FINANCE01

þ b4SIZE01 þ b5ACE01 þ b6BLOCK01 þ b7BIG401 þ b8ACQ01

þ b9CHGCEO01 þ b10RESTR01 þ b11RETURN01 þ e

Panel A: Logistic Regressions for Dependent Variable Defined as DECRRATIO

Variable Predicted Sign Parameter Estimate Chi-Square Statistic

Intercept �0.985 1.019

INOWN � �0.099 4.013*

LEVERAGE þ 0.743 1.000

FINANCE þ 0.021 4.778*

SIZE þ 0.081 5.145*

ACE þ 0.851 7.117**

BLOCK ? �0.002 0.393

BIG4 ? 1.359 1.336

ACQ ? �0.207 0.359

CHGCEO ? 1.396 1.007

RESTR ? �0.958 6.642**

RETURN ? �0.011 0.923

Obs. ¼ 338 Pseudo R2 ¼ 0.1031

Panel B: Logistic Regressions for Dependent Variable Defined as DECRNAS

Variable Predicted Sign Parameter Estimate Chi-Square Statistic

Intercept �0.976 1.016

INOWN � �0.075 3.822*

LEVERAGE þ �0.160 0.726

FINANCE þ 0.026 4.790*

SIZE þ 0.060 4.557*

ACE þ 0.902 7.116**

BLOCK ? �0.006 0.873

BIG4 ? 1.011 1.115

ACQ ? �0.385 0.407

CHGCEO ? 1.537 0.846

RESTR ? �0.787 5.799*

RETURN ? �0.012 0.795

Obs. ¼ 338 Pseudo R2 ¼ 0.1013

*, ** Significant at p-levels of less than 0.05 and 0.01, respectively. p-values are two-tailed where no directionalprediction is made.All variables per Table 2, except SIZE, which is the natural log of total assets.

Does Mandated Disclosure Induce a Structural Change? 71

Auditing: A Journal of Practice & TheoryMay 2011

the NAS ratio (NAS fees) are also less likely when inside ownership is higher and when the

company is larger. Our logistic regression evidence supplements our Chow test results and yields

qualitatively similar evidence.

Sensitivity Tests

We pooled our two years of data and introduced interaction terms to test whether the test

variables exhibit significant changes in 2001. Our results from the pooled regression are

qualitatively the same as those obtained from the Chow tests and logistic regression. In addition, we

recognize that the ratio of NAS to audit fees is only one of many possible measures identified with

the perception of impaired audit independence. We used three additional measures including the