division of corporation finance … piper llp (us) ... t 415.836.2598 f 415.659.7309 january 30,...

TRANSCRIPT

January 31 2017

Brad Rock DLA Piper LLP (US) bradrockdlapipercom Re Ross Stores Inc Dear Mr Rock This is in regard to your letter dated January 30 2017 concerning the shareholder proposal submitted by The Humane Society of the United States for inclusion in Ross Storesrsquo proxy materials for its upcoming annual meeting of security holders Your letter indicates that the proponent has withdrawn the proposal and that Ross Stores therefore withdraws its December 28 2016 request for a no-action letter from the Division Because the matter is now moot we will have no further comment

Copies of all of the correspondence related to this matter will be made available on our website at httpwwwsecgovdivisionscorpfincf-noaction14a-8shtml For your reference a brief discussion of the Divisionrsquos informal procedures regarding shareholder proposals is also available at the same website address Sincerely Evan S Jacobson Special Counsel cc PJ Smith The Humane Society of the United States pjsmithhumanesocietyorg

DLA Piper LLP (US)

555 Mission Street Suite 2400San Francisco California 94105-2933wwwdlapipercom

Brad RockbradrockdlapipercomT 4158362598F 4156597309

January 30 2017VIA E-MAIL

OFFICE OF CHIEF COUNSELDIVISION OF CORPORATION FINANCESECURITIES AND EXCHANGE COMMISSION100 F STREET NEWASHINGTON DC 20549

Re Ross Stores IncWithdrawal of No-action Request and Notice of Intent to Omit from Proxy Materials theShareholder Proposal of the Humane Society of the United States

Ladies and Gentlemen

In a letter dated December 28 2016 we requested that the Staff of the Division of CorporationFinance concur that our client Ross Stores Inc a Delaware corporation (the ldquoCompanyrdquo) ispermitted to exclude from its proxy statement and form of proxy for its 2017 Annual Meeting ofStockholders (collectively the ldquo2017 Proxy Materialsrdquo) a stockholder proposal (the ldquoProposalrdquo)and statement in support thereof received on October 31 2016 from The Humane Society of theUnited States (ldquoHSUSrdquo)

Attached as Exhibit A is an email notice to the Company dated January 30 2017 fromMr PJ Smith Corporate Engagement Manager of HSUS which withdraws the Proposalsubmitted by HSUS In reliance on this notice from HSUS we hereby withdraw theDecember 28 2016 no-action request relating to the Proposal and the Companys ability toexclude it from the 2017 Proxy Materials pursuant to Rule 14a-8 under the Exchange Act of1934

January 30 2017Page Two

Please call me at (415) 836-2598 with any questions regarding this matter

Very truly yours

DLA Piper LLP (US)

Brad RockPartner

Enclosures

cc Ken Jew Senior Vice President General Counsel amp Assistant Corporate SecretaryRoss Stores Inc

The Humane Society of the United StatesAttn PJ Smith Corporate Engagement Manager1255 23rd Street NW Suite 450Washington DC 20037

EXHIBIT A

Email Notice from The Humane Society of the United States to withdraw Proposal[Edited to remove personally identifiable email and phone information]

From PJ Smith [mailto[xxx]humanesocietyorg]Sent Monday January 30 2017 200 PMTo Ken Jew (Legal)Subject HSUS stockholder proposal withdrawal

Hi Ken

Hope yoursquore well Please allow this e-mail to serve as official notification that HSUS is withdrawing itsshareholder proposal

I look forward to finding ways Ross and HSUS can work together to reduce the risks that go along withselling animal fur Irsquom confident these issues will continue to gain traction socially and in business asmore and more major companies become leaders on animal welfare

Happy to chat anytime Thanks

BestPJ Smith

PJ SmithSenior Manager Fashion Policy[xxx]humanesocietyorg301366xxxx

The Humane Society of the United States1255 23rd Street NW Suite 450Washington DC 20037humanesocietyorg

Join Our Email List Facebook Twitter Blog

WEST2751772421

DLA Piper LLP (US)

555 Mission Street Suite 2400San Francisco California 94105wwwdlapipercom

Brad RockbradrockdlapipercomT 4158362598F 4156597309

December 28 2016

VIA E-MAIL

OFFICE OF CHIEF COUNSELDIVISION OF CORPORATION FINANCESECURITIES AND EXCHANGE COMMISSION100 F STREET NEWASHINGTON DC 20549

Re Ross Stores IncNotice of Intent to Omit from Proxy Materials the ShareholderProposal of the Humane Society of the United States

Ladies and Gentlemen

This letter is to inform you that our client Ross Stores Inc a Delaware corporation (ldquoRossStoresrdquo or the ldquoCompanyrdquo) intends to omit from its proxy statement and form of proxy for its2017 Annual Meeting of Stockholders (collectively the ldquo2017 Proxy Materialsrdquo) a stockholderproposal (the ldquoProposalrdquo) and statement in support thereof received from The Humane Societyof the United States (ldquoHSUSrdquo or the ldquoProponentrdquo)

Pursuant to Rule 14a-8(j) we have

filed this letter with the Securities and Exchange Commission (theldquoCommissionrdquo) no later than eighty (80) calendar days before the Companyintends to file its definitive 2017 Proxy Materials with the Commission and

concurrently sent copies of this correspondence to the Proponent

Rule 14a-8(k) and Staff Legal Bulletin No 14D (Nov 7 2008) (ldquoSLB 14Drdquo) provide thatstockholder proposal proponents are required to send companies a copy of any correspondencethat the proponents elect to submit to the Commission or the staff of the Division of CorporationFinance (the ldquoStaffrdquo) Accordingly we are taking this opportunity to inform the Proponent thatif the Proponent elects to submit additional correspondence to the Commission or the Staff withrespect to this Proposal a copy of that correspondence should be furnished concurrently to theundersigned on behalf of the Company pursuant to Rule 14a-8(k) and SLB 14D

December 28 2016Page Two

THE PROPOSAL

The Proposal states

RESOLVED that shareholders ask that Ross Stores Inc adopt a policy and amend othergoverning documents as necessary to require that the Boardrsquos Chair be an independentdirector as defined by NYSE This independence requirement shall apply prospectively soas not to violate any contractual obligation at the time this resolution is adopted Compliancewith this policy is waived if no independent director is available and willing to serve asChair The policy should also specify how to select a new independent Chair if a currentChair ceases to be independent between annual shareholder meetings

A copy of the Proposal and Supporting Statement as well as related correspondence with theProponent are attached to this letter as Exhibit A

BACKGROUND

While the Proposal submitted by HSUS ostensibly relates to a matter of corporate governancethat is a pretext As plainly indicated in emails sent by an HSUS representative to Ross Storesofficers and directors prior to submitting the Proposal as well as in other prior and subsequentcommunications from HSUS in reality this is just a tactic and a further chapter in an ongoingcampaign by HSUS to pressure the Company to adopt a ldquofur freerdquo policy consistent with thepursuit by HSUS of its mission to promote the broad adoption of such policies by retailers foodcompanies and others In its own words HSUS has ldquoengaged with Ross for many yearsregarding the issue of products containing real furrdquo

In an email dated September 13 2016 addressed to Michael Balmuth (Executive Chairman ofRoss Stores) PJ Smith (Corporate Engagement Manager of HSUS) states

ldquoIrsquom writing from The Humane Society of the United States to let you know that wersquoreconsidering a shareholder proposal at Ross seeking an independent board chair policyand to see if you or senior management would consider coming to the table with usinstead (Emphasis added)

Wersquove engaged with Ross for many years regarding the issue of products containing realfur

Since Ross does not knowingly buy real animal fur we hope yoursquoll agree that it wonrsquottake much to make the policy public on your website Is this something yoursquod supportThanks so much and Irsquom happy to chat any time Have a great dayrdquo

December 28 2016Page Three

A copy of the referenced email as well as other related email correspondence from theProponent is attached to this letter as Exhibit B

Previously HSUS has made numerous other efforts and threats in pursuing its unique agendaover the years including a prior stockholder proposal and other attempts to take advantage ofrules and resources of federal governmental agencies that are intended for other purposes Thesepast efforts have also included campaigns of personal emails to officers or Board members of theCompany offering to stop the governmental action if ldquoappropriate actionrdquo (ie adoption of a ldquofurfreerdquo policy) is taken

For the Companyrsquos 2012 Annual Meeting of Stockholders HSUS submitted an express proposalfor the purpose of requesting a vote by the Companyrsquos shareholders on adoption of a ldquofur freerdquopolicy HSUS withdrew that proposal however before the Staff had responded to a no-actionrequest submitted by Ross Stores presumably because the Staff had issued its response inconnection with an essentially equivalent proposal concurring with the other registrantcompanyrsquos determination to exclude it See Ross Stores Inc (avail March 6 2012) andDilliardrsquos Inc (avail Feb 22 2012) The 2012 no-action request from Ross Stores and relatedcorrespondence with HSUS can be found at httpswwwsecgovdivisionscorpfincf-noaction14a-82012humanesociety030612-14a8pdf

More recently HSUS has sought to use the threat of federal rules intended to provide consumerprotection rights as a tool to pursue its own desire to pressure the Company and other retailers toadopt and publicly announce ldquofur freerdquo policies In August of 2016 HSUS issued a press releaseto draw attention to the petition it filed with the US Federal Trade Commission (the ldquoFTCrdquo) torequest that the FTC bring enforcement action under federal consumer protection laws against 17retailers alleging false advertising in regard to garments containing fur At page 22 of its 33-page long petition HSUS noted that one item of womenrsquos clothing (previously called out in apress release by HSUS in 2012) had allegedly been obtained by an HSUS investigator from aCompany store in October 2012 and that the investigator had examined the black fur trim anddetermined that it was animal fur and not faux fur as indicated on one sewn-in label Inconjunction with making the press release a representative of HSUS sent an email to the CEO ofRoss Stores ending with a post script note ldquops In the past wersquove recommended to the FTCthat the agency remove certain companies from our petitions even after theyrsquore filed and wouldconsider doing so here too if appropriate actions could be taken on this issuerdquo Copies ofrelevant items of email correspondence from representatives of HSUS are included in Exhibit Battached to this letter

As is apparent to anyone who visits the stores Ross Stores does not target apparel or othermerchandise that contains animal fur or consistently carry any particular merchandise thatcontains fur As an off-price retailer Ross Stores sources its products primarily from excess

December 28 2016Page Four

inventory of other retailers and from production overruns by manufacturers Items made fromfur or that include fur are not a meaningful merchandise category for the Company and are notsignificant or recognizable enough to even be separately tracked To the extent the Companyfrom time to time happens to carry isolated items that use any fur they are typically items ofapparel with purely incidental amounts of fur trim such as on winter coats or perhaps on fashionaccessories or in the lining of gloves The Companyrsquos buying staff believes that products thatuse animal fur represent far less than one percent (1) of the Companyrsquos clothing shoes andaccessory purchases

Ross Stores operates two brands of off-price retail apparel and home fashion stores AtOctober 29 2016 Ross Stores operated 1535 stores ndash 1342 Ross Dress for Lessreg locations in36 states the District of Columbia and Guam and 193 ddrsquos DISCOUNTSreg stores in 15 statesRoss offers first-quality in-season name brand and designer apparel accessories footwear andhome fashions for the entire family at savings of 20 to 60 off department and specialty storeregular prices every day Ross Dress for Less targets customers who are primarily from middleincome households while ddrsquos DISCOUNTS features a more moderately-priced assortment offirst-quality in-season name brand apparel accessories footwear and home fashions for theentire family at savings of 20 to 70 off moderate department and discount store regularprices every day Ross Stores sells recognizable brand-name merchandise that is current andfashionable in each category The mix of sales year to date by department in fiscal 2016 has beenapproximately as follows Ladies 29 Home Accents and Bed and Bath 24 Shoes 14Menrsquos 13 Accessories Lingerie Fine Jewelry and Fragrances 12 and Childrenrsquos 8 Themerchandise offerings also include product categories such as small furniture and furnitureaccents educational toys and games luggage gourmet food and cookware watches sportinggoods and in select Ross stores fine jewelry

The Board of Directors of Ross Stores (the ldquoBoardrdquo) currently consists of eleven (11) authorizedmembers The roles of Chairman of the Board (ldquoChairrdquo) and of Chief Executive Officer(ldquoCEOrdquo) are held by two separate individuals A separation of those roles has been in place onthe Board for twenty (20) years Michael Balmuth currently serves as Executive ChairmanMr Balmuth was formerly the Companyrsquos CEO from 1996 to 2014 The current CEO is BarbaraRentler she has been in that position since 2014 Beginning in fiscal 2014 the Board has alsodesignated a Lead Independent Director to act as a liaison between Chair CEO and independentdirectors and to serve as the designated Chair of the Nominating and Corporate GovernanceCommittee The designation of a Lead Independent Director is a widely adopted approach instructuring Board leadership to enhance the involvement and oversight of management by theindependent directors The Lead Independent Director position currently rotates annually amongthe independent directors

December 28 2016Page Five

BASES FOR EXCLUSION

The Company believes that the Proposal is excludable under at least two of the bases forexclusion set forth in Rule 14a-8(i) of the Exchange Act

1 [Rule 14a-8(i)(4)] Personal Grievance Special Interest If the proposal relates tothe redress of a personal claim or grievance against the company or any otherperson or if it is designed to result in a benefit to [the Proponent] or to further apersonal interest which is not shared by the other shareholders at large and

2 [Rule 14a-8(i)(3)] Violation of Proxy Rules If the proposal or supportingstatement is contrary to any of the Commissionrsquos proxy rules includingRule 14a-9 which prohibits materially false or misleading statements in proxysoliciting materials

ANALYSIS

A The Proposal is designed to result in a benefit to HSUS or to further a personalinterest of HSUS which is not shared by the other shareholders at large

Rule 14a-8(i)(4) permits the exclusion of a shareholder proposal that is designed to result in abenefit to the proponent or to further a personal interest of the proponent which is not shared bythe other shareholders at large Such a proposal is an abuse of the security holder proposalprocess

Although on its face appearing to be a proposal seeking a change on a matter of boardgovernance that is merely a pretext and is not the objective of HSUS in submitting the proposalThe Proposal was submitted by HSUS as a tactic to obtain leverage in its ongoing efforts topressure Ross Stores to publicly adopt a ldquofur freerdquo policy The real reason the Proposal wassubmitted is baldly revealed in the earlier (September 13 2016) email from HSUS quoted atlength in the Background Section above ldquo wersquore considering a shareholder proposal at Rossseeking an independent board chair policy and to see if you or senior management wouldconsider coming to the table with us instead rdquo Similar email messages were sent by HSUSto other members of the Board When the Company declined the invitation to ldquocome to thetablerdquo or engage further with HSUS regarding its continued demands for public announcement ofa ldquofur freerdquo policy HSUS subsequently delivered a request to include the Proposal by letterdated October 31 2016 Copies of relevant items of correspondence from representatives ofHSUS are included in Exhibit A and Exhibit B attached to this letter

The Commission has stated that Rule 14a-8(i)(4) is designed to ldquoinsure that the security holderproposal process [is] not abused by proponents attempting to achieve personal ends that are not

December 28 2016Page Six

necessarily in the common interest of the issuerrsquos shareholders generallyrdquo Exchange ActRelease No 20091 (Aug 16 1983) In addition the Commission has stated in discussing thepredecessor of Rule 14a-8(i)(4) (Rule 14a-8(c)(4)) that Rule 14a-8 ldquois not intended to provide ameans for a person to air or remedy some personal claim or grievance or to further somepersonal interest Such use of the security holder proposal procedures is an abuse of the securityholder proposal process and the cost and time involved in dealing with these situations do adisservice to the interests of the issuer and its security holders at largerdquo Exchange Act ReleaseNo 34-19135 (Oct 14 1982) Thus Rule 14a-8(i)(4) provides a means to exclude shareholderproposals the purpose of which is to ldquoair or remedyrdquo a personal grievance or advance somepersonal interest This interpretation is consistent with the Commissionrsquos statement at the timethe rule was adopted that ldquothe Commission does not believe that an issuerrsquos proxy materials are aproper forum for airing personal claims or grievancesrdquo Exchange Act Release No 12999(Nov 22 1976)

The Commission also has confirmed that this basis for exclusion applies even to proposalsphrased in terms that ldquomight relate to matters which may be of general interest to all securityholdersrdquo and thus that Rule 14a-8(i)(4) justifies the omission of neutrally-worded proposals ldquoif itis clear from the facts presented by the issuer that the proponent is using the proposal as a tacticdesigned to redress a personal grievance or further a personal interestrdquo Exchange Act ReleaseNo 19135 (Oct 14 1982) The Staffrsquos interpretation of Rule 14a-8(i)(4) clearly contemplateslooking beyond the four corners of a proposal for the purpose of identifying a personal interest orgrievance to which the submission of the proposal relates

Consistent with this interpretation of Rule 14a-8(i)(4) the Staff on numerous occasions hasconcurred in the exclusion of a proposal that included a facially-neutral resolution but where thefacts demonstrated that the proposalrsquos true intent was to further a personal interest or redress apersonal claim or grievance For example in State Street Corp (avail Jan 5 2007) the Staffagreed that the company could exclude under Rule 14a-8(i)(4) a facially-neutral proposal that thecompany separate the positions of Chair and CEO and provide for an independent Chair whenbrought by a former employee after that former employee was ejected from the companyrsquosprevious annual meeting for disruptive conduct and engaged in a lengthy campaign of publicharassment against the company and its CEO

Similarly in Pfizer Inc (avail Jan 31 1995) the proponent contested the circumstances of hisretirement claiming that he had been forced to retire as a result of illegal age discrimination Healso sent a letter to the companyrsquos CEO asking the CEO to review and remedy his situationAfter failing to receive a satisfactory outcome from Pfizerrsquos internal review and from the CEOthe proponent submitted what Pfizer described in its no-action request to the Staff as a ldquoveryunclearrdquo shareholder proposal that appeared to seek a shareholder vote on the CEOrsquoscompensation Despite the proposal addressing a topic that potentially could have been of

December 28 2016Page Seven

general interest among Pfizerrsquos shareholders Pfizer argued that the evidence of the proponentrsquoscontinued claims against Pfizer including in the letter that the proponent sent to the CEOsupported the conclusion that the shareholder proposal was part of his effort to seek redressagainst Pfizer and the Staff concurred that the proposal was excludable under the predecessor toRule 14a-8(i)(4) See also American Express Co (avail Jan 13 2011) (proposal to amend thecode of conduct to include mandatory penalties for noncompliance was excludable as a personalgrievance when brought by a former employee who previously had sued the company fordiscrimination and defamation)

As was the case in State Street Corp where there was a lengthy campaign of public harassmentagainst the company and its CEO here HSUS has ldquoengaged with Ross for many years regardingthe issue of products containing real furrdquo in a continuous and public campaign of harassmentThe current Proposal is in reality not made for the ostensible and apparently neutral reasonsstated in the Proposal but in ongoing pursuit of a personal agenda unique to the Proponent

It is further evidence of the Proponentrsquos insincerity and lack of good faith in submitting theProposal that the Proposal includes obvious errors and the Supporting Statement is completelyoff topic and misdirected The Proposal seeks a policy ldquothat the Boardrsquos Chair be anindependent director as defined by NYSErdquo (emphasis added) But Ross Stores is listed on theNASDAQ Stock Market not the NYSE And as discussed further under Section C below theSupporting Statement is devoted almost entirely to reasons in favor of separation of the Chairposition from the role of CEO But the Board of Ross Stores has already done that formore than 20 years Almost nothing in the Supporting Statement could be applicable to RossStores An obvious explanation for this thoughtlessness is that the Proponent has no actualinterest in changing or even understanding the governance aspects at this company TheProposal was not really submitted for that reason but purely as a cynical tactic to pressure seniormanagement of Ross Stores to ldquocome to the tablerdquo and to meet the demand by HSUS to adopt aldquofur freerdquo policy This is an abuse by the Proponent of the SECrsquos rules and processes forbringing shareholder proposals and an effort to achieve personal ends that are not in the commoninterest of the issuerrsquos shareholders generally which should not be tolerated

For the reasons discussed above the Company has concluded that it may exclude the Proposalfrom the 2017 Proxy Materials under Rule 14a-8(i)(4) We respectfully ask that the Staff concurthat from the facts presented by the Company it has been shown the Proponent is using theProposal as a tactic designed to further a personal interest and to result in a benefit to theProponent which is not shared by the other shareholders at large

December 28 2016Page Eight

B The Proposal may be excluded under Rule 14a-8(i)(3) because the Proposal reliesupon a reference to the NYSE independence definitions for a central aspect of theProposal rendering the Proposal impermissibly vague and indefinite

We believe that the Proposal may also be properly excluded from the 2017 Proxy Materialspursuant to Rule 14a-8(i)(3) because the Proposal seeks to impose a policy of independence byreference to a particular set of external standards namely the New York Stock Exchange (theldquoNYSErdquo) listing rules to implement the central aspect of the Proposal but fails to sufficientlydescribe or explain the substantive provisions of those standards rendering the Proposalimpermissibly vague and indefinite so as to be inherently misleading

As further discussed below the Proposal is virtually identical to the proposal in Chevron Corp(avail Mar 15 2013) and Wellpoint Inc (avail Feb 24 2012 recon denied Mar 27 2012)and substantially similar to proposals in The Proctor amp Gamble Company (avail Jul 6 2012recon denied Sept 20 2012) Cardinal Health Inc (avail Jul 6 2012) The Clorox Company(avail Aug 13 2012) and Harris Corporation (avail Aug 13 2012) In each case the Staffpermitted the company to exclude a similar proposal pursuant to Rule 14a-8(i)(3)

The Staff consistently has taken the position that a shareholder proposal is excludable underRule 14a-8(i)(3) when it is vague and indefinite so that ldquoneither the stockholders voting on theproposal nor the company in implementing the proposal (if adopted) would be able todetermine with any reasonable certainty exactly what actions or measures the proposal requiresrdquoStaff Legal Bulletin No 14B (Sept 15 2004) (ldquoSLB 14Brdquo) see also Dyer v SEC 287 F2d 773781 (8th Cir 1961) (ldquo[I]t appears to us that the proposal as drafted and submitted to thecompany is so vague and indefinite as to make it impossible for either the board of directors orthe stockholders at large to comprehend precisely what the proposal would entailrdquo)

In Staff Legal Bulletin No 14G (Oct 16 2012) (ldquoSLB 14Grdquo) the Staff explained its approach toassessing whether a proposal that contains a reference to an external standard is vague andmisleading addressing specifically the context where a proposal contains a reference to awebsite

In evaluating whether a proposal may be excluded on this basis we consider only theinformation contained in the proposal and supporting statement and determine whetherbased on that information shareholders and the company can determine what actions theproposal seeks

If a proposal or supporting statement refers to a website that provides informationnecessary for shareholders and the company to understand with reasonable certaintyexactly what actions or measures the proposal requires and such information is not also

December 28 2016Page Nine

contained in the proposal or in the supporting statement then we believe the proposalwould raise concerns under Rule 14a-9 and would be subject to exclusion underRule 14a-8(i)(3) as vague and indefinite

The Staff has applied this standard to a number of proposals that ndash just like the Proposal ndashrequested that companies adopt a policy to appoint an independent director to serve as Chair InChevron Corp (avail Mar 15 2013) the Staff quoted the first paragraph of the language fromSLB 14G set forth above and concurred that a proposal could be excluded under Rule 14a-8(i)(3)because the proposal referred to but did not explain the NYSE listing standards for determiningwhether a director qualified as an independent director Because an understanding of the NYSElisting standardsrsquo definition of ldquoindependent directorrdquo was necessary to determine with anyreasonable certainty exactly what actions or measures the proposal required the Staff explainedldquo[i]n our view this definition is a central aspect of the proposalrdquo Thus the Staff concurred inexclusion of the proposal ldquobecause the proposal does not provide information about what theNew York Stock Exchangersquos definition of lsquoindependent directorrsquo meansrdquo See also McKessonCorp (avail Apr 17 2013 recon denied May 31 2013) in which the Staff repeated theevaluation standard from SLB 14G and then concluded ldquoAccordingly because the proposaldoes not provide information about what the New York Stock Exchangersquos definition oflsquoindependent directorrsquo means we believe shareholders would not be able to determine with anyreasonable certainty exactly what actions or measures the proposal requiresrdquo

Similarly in Wellpoint Inc the Staff concurred that the company could exclude a proposal thatwas virtually identical to the Proposal In its no-action request Wellpoint argued that it couldexclude the proposal pursuant to Rule 14a-8(i)(3) because it relied upon an external standard ofindependence to implement the ldquocentral aspectrdquo of the proposal (as in the Proposal the NYSEstandards) but nevertheless failed to describe the substantive provisions of the standard TheStaff concurred noting ldquoin particular [the companyrsquos] view that in applying this particularproposal to [the company] neither shareholders nor the company would be able to determinewith any reasonable certainty exactly what actions or measures the proposal requiresrdquoFollowing Wellpoint the Staff concurred with the exclusion of similar proposals in The Proctoramp Gamble Company Cardinal Health Inc The Clorox Company and Harris Corporation Ineach of those cases the proposals sought a bylaw or policy requiring a Chair ldquowho isindependentrdquo from the company and for this purpose ldquoindependentrdquo would have ldquothe meaningset forth in the NYSE listing standardsrdquo In each case the company argued that the proposalcould be excluded pursuant to Rule 14a-8(i)(3) because the proposal relied upon an externalstandard of independence to implement the central aspect of the proposal ndash as in the Proposalthe NYSE standards ndash but nevertheless failed to describe or explain the substantive provisions ofthe standard Absent such a description or explanation in the proposal shareholders would beunable to determine the specific independence requirements to be applied under the proposalsIn each case the Staff concurred

December 28 2016Page Ten

The Proposal requests that ldquoRoss Stores Inc adopt a policy and amend other governingdocuments as necessary to require that the Boardrsquos Chair be an independent director as definedby NYSErdquo and in substance is identical to the proposals in Chevron Corp Wellpoint and theother cited no-action request cases As in each of these cited cases the Proposal relies upon anexternal standard of independence (the NYSE standard) in order to implement the requestedpolicy but fails to describe or explain the substantive provisions of the standard Without adescription of the NYSErsquos listing standards in the proposal shareholders will be unable todetermine the specific standard of independence to be applied under the Proposal and thereforewould be unable to make an informed decision on the merits of the proposal As Staff precedentindicates the Companyrsquos shareholders cannot be expected to make an informed decision on themerits of the Proposal without knowing what they are voting on See SLB 14B

The Proposal is distinguishable from other shareholder proposals which the Staff did not concurwere vague and indefinite and thus were not excludable under Rule 14a-8(i)(3) and in whichthe proposal requested that the Chair be an independent director (by the NYSE standard) and besomeone who had not previously served as an executive officer of the company See PepsiCoInc (avail Feb 2 2012) Reliance Steel amp Aluminum Co (avail Feb 2 2012) Sempra Energy(avail Feb 2 2012) General Electric Co (avail Jan 10 2012 recon denied Feb 1 2012) andAllegheny Energy Inc (avail Feb 12 2010) In those instances the proposals contained a two-prong standard of independence which standing alone could reasonably be expected to permitshareholders to make an informed decision on the merits of the proposal In contrast theProposal like those in Chevron Corp Wellpoint and the other examples noted only includes asingle standard of independence (the NYSE standard of independence) that is neither describedor explained in nor understandable from the text of the Proposal or the Supporting Statement Inthis regard again as in Chevron Corp Wellpoint and the other examples the SupportingStatementrsquos references to separation of the roles of Chair and CEO does not provide anyinformation to shareholders as to the NYSE standards of independence In fact many companiesthat have separated the role of Chair and CEO have an executive chairman who would not satisfythe NYSE standard for independence

Consistent with Wellpoint Chevron Corp and the other precedents because the Proposalsimilarly relies on the NYSE standard of independence for implementation of a central elementof the Proposal without describing or explaining that standard the Proposal is impermissiblyvague and indefinite so as to be inherently misleading and therefore excludable under Rule 14a-8(i)(3) The Proposalrsquos failure to describe or explain the substantive provisions of the NYSEstandards of independence which is necessary to implement the central aspect of the Proposalwill render shareholders who are voting on the Proposal unable to determine with any reasonablecertainly what actions or measures the Proposal requires

December 28 2016Page Eleven

C The Proposal may be excluded under Rule 14a-8(i)(3) because the SupportingStatement is contrary to the Commissionrsquos proxy rules including Rule 14a-9 whichprohibits materially false or misleading statements in proxy soliciting materials

Under Rule 14a-8(i)(3) a proposal may also be omitted from a registrantrsquos proxy statement if theproposal or supporting statement is contrary to any of the Commissionrsquos proxy rules includingRule 14a-9 which prohibits materially false or misleading statements in proxy solicitingmaterials

SLB 14B provides that a company may rely on Rule 14a-8(i)(3) to exclude a shareholderproposal if that proposal among other things contains statements that are objectively false ormisleading or if substantial portions of the proposal or the supporting statement are irrelevant toa consideration of the subject matter of the proposal such that there is a strong likelihood that areasonable shareholder would be uncertain as to the matter on which he or she is being asked tovote See eg Bank of America Corp (Mar 12 2013) (allowing exclusion under Rule 14a-8(i)(3) of a proposal requiring a stockholder value committee to explore ldquoextraordinarytransactionsrdquo defined as transactions that would require shareholder approval but providing asexamples transactions that were not extraordinary and would not require shareholder approval)Freeport-McMoRan Copper amp Gold Inc (Feb 22 1999) (permitting exclusion of a proposalunless revised to delete discussion of a news article regarding alleged conduct by the companyrsquoschairman and directors that was irrelevant to the proposalrsquos subject matter the annual election ofdirectors) Pursuant to SLB 14B reliance on Rule 14a-8(i)(3) to exclude a proposal or portionsof a supporting statement may be appropriate in only a few limited instances The Staff hasexplained that a shareholder proposal can be sufficiently misleading and therefore may beexcluded in reliance on Rule 14a-8(i)(3) if the company and its shareholders might interpret theproposal differently such that ldquoany action ultimately taken by the [c]ompany uponimplementation [of the proposal] could be significantly different from the actions envisioned bythe shareholders voting on the proposalrdquo Fuqua Industries Inc (Mar 12 1991)

Another basis for exclusion is where ldquothe company demonstrates objectively that a factualstatement is materially false or misleadingrdquo SLB 14B In this regard the Staff consistently hasallowed the exclusion under Rule 14a-8(i)(3) of shareholder proposals that contain statementsthat are false or misleading See eg Wal-Mart Stores Inc (avail Apr 2 2001) (concurring inthe exclusion of a proposal to remove all ldquogenetically engineered crops organisms or productsrdquobecause the text of the proposal misleadingly implied that it related only to the sale of foodproducts) McDonaldrsquos Corp (avail Mar 13 2001) (granting no-action relief because theproposal to adopt ldquoSA 8000 Social Accountability Standardsrdquo did not accurately describe thestandards)

December 28 2016Page Twelve

The Supporting Statement from the Proponent is entirely an argument for the separation ofthe Chair and CEO positions and is irrelevant to the question of requiring an independentChair This creates a mistaken and misleading impression as to the subject of the Proposal andthe impression that Ross Stores does not already separate those roles when in fact the Board ofRoss Stores has had a separate Chair and CEO for 20 years It reads as if the Proponent copieda 2012 supporting statement for a different proposal ndash namely to institute a separation of theCEO position from the Chair position (whether or not filled by an independent director) andmade minor changes to the first sentence and the conclusion to insert references to independentdirector status None of the rest of the discussion supports the actual Proposal In addition theSupporting Statement is materially misleading when it asserts that the cited sources and theincluded quotes provide support for a requirement that an independent director serve as Chair

At least 75 of the words in the Supporting Statement (246 out of 329) are arguments for nothaving the CEO also hold the Chair position Below is an analysis of each paragraph of theSupporting Statement

The initial statement as to ldquothe logicrdquo for the concept of an independence requirement for theChair position ends ldquo3 there is a potential conflict of interest and lack of checks and balanceswhen a CEO is his or her own overseer while simultaneously managing the businessrdquo This is anargument for having separate individuals hold the two positions but does not addressindependence

The quotequestion in the next paragraph attributed to Andy Grove (famous former chairman ofIntel Corporation) ends ldquoThe Chairman runs the Board How can the CEO be his own bossrdquoThis again is an argument not for an independent director as Chair but for separation

The next paragraph cites a Sullivan amp Cromwell survey stating that approximately 70 ofrespondents believe the head of management should not concurrently chair the Board Again anargument for separation and irrelevant to the issue of adopting a policy to require anindependent Chair

The next paragraph ends ldquoin 2012 44 of all SampP 500 companies had Boards not chaired bytheir CEOrdquo Ross Stores was already one of those companies in 2012 As an update accordingto Spencer Stuart that figure had increased to 48 in 2015 (just over half (52) of companies inthe SampP 500 Index were led by a dual chairmanCEO while 29 had an independent Chair and19 an executive or other outside Chair) Spencer Stuart Board Index (2015) Yet again thisincludes no information relevant to or supportive of the question of independence which is theonly substantive point advocated in the Proposal

The next paragraph bears particular examination In it the Proponent states

December 28 2016Page Thirteen

ldquoAn independent Board Chair has also been found to improve financial performance A2012 GMI Ratings report titled The Costs of a Combined ChairCEO found thatcompanies with a separate CEO and Chair provide investors with five-year shareholderreturns nearly 28 higher than those of companies helmed by a party of onerdquo

The initial sentence of this paragraph asserts that performance has been found to improve wherethere is ldquoan independent Board Chairrdquo However in the cited GMI Ratings report ndash while itclearly notes the distinction between independent and non-independent directors serving as aseparate Chair from the CEO ndash the reported performance results are based collectively on allinstances of separation of the roles and are not based on having an independent director asChair It is completely misleading to suggest that an independent Chair policy had been foundto improve performance rather than a separation of Chair and CEO based on that report

The next paragraph of the Supporting Statement notes that numerous institutions supportseparation including CalPERS (Americarsquos largest public pension fund) and InstitutionalShareholder Services (ISS) Once again this is support for separation of CEO and Chair (whichRoss Stores does already) but provides no support in regard to a required policy ofindependence Furthermore it is misleading to cite ISS as supportive of the Proposal Until2014 ISS had a stated voting recommendation policy that would have likely led ISS torecommend ldquoAGAINSTrdquo this Proposal because Ross Stores has a separate CEO and Chair andalso a Lead Independent Director with a specified role and duties in support of Board oversightof management In 2015 ISS adopted a change in its voting recommendation guidelines on theissue of an independent director as Chair in favor of a ldquoholisticrdquo approach to that questionHowever ISS still includes on a case-by-case basis the same considerations it had in 2014While ISS indicates that in general it favors an independent director as Chair it is misleading tosuggest that ISS categorically recommends a vote FOR such a proposal Finally the paragraphindicates that The Council of Institutional Investors ldquostates that a lsquoboard should be chaired by anindependent directorrsquordquo While that quote is literally correct the paragraph from which it wastaken does not include any discussion of the independentnon-independent status of a directorserving as Chair but is focused entirely on whether the CEO should concurrently serve as theChair This yet again is not an argument for an independent director as Chair but forseparation

This brings up the last paragraph of the Supporting Statement which is simply a conclusion toencourage stockholders to vote for the Proposal

As this detailed analysis of the Supporting Statement shows it is misleading on multiple levelsFundamentally it is misleading because it is completely off topic It is entirely an argument insupport of separating the Chair and CEO positions ndash which would mislead a stockholder eitherinto thinking that subject (separation of the two roles) is what the Proposal addresses andor into

December 28 2016Page Fourteen

believing that Ross Stores does not already do so (when it does) The Supporting Statement isalso misleading in its key elements and its citations which are mischaracterized as being focusedon the independencenon-independence of a separate Chair In fact none of the cited supportactually pertains to the only policy change requested in the Proposal

As in the no-action letters referenced above the Supporting Statement here contains substantialdiscussion of matters that are unrelated to and do not support the actual subject matter of theProposal These statements are misleading because they are irrelevant to the ldquocore topicrdquo of theProposal and are likely to confuse shareholders as to what they are being asked to approve Inview of the foregoing the Company has concluded that the Proposal may be excluded in relianceon Rule 14a-8(i)(3)

CONCLUSION

Ross Stores hereby requests that the Staff concur with the conclusion that it can properly excludethe Proposal and confirm that the Staff will not recommend any enforcement action if RossStores excludes the Proposal from the 2017 Proxy Materials Should you disagree with theconclusions set forth herein we would appreciate the opportunity to confer with you prior to theissuance of the Staffrsquos response Moreover Ross Stores reserves the right to submit to the Staffadditional bases upon which the Proposal may properly be excluded from the 2017 ProxyMaterials

By copy of this letter the Proponent is being notified of Ross Storesrsquo intention to omit theProposal from its 2017 Proxy Materials

December 28 2016Page Fifteen

We would be happy to provide you with any additional information and answer any questionsthat you may have regarding this subject If we can be of any further assistance in this matterplease do not hesitate to call me at (415) 836-2598

Very truly yours

DLA Piper LLP (US)

Brad RockPartner

Enclosures

cc Ken Jew Senior Vice President General Counsel amp Corporate SecretaryRoss Stores Inc

The Humane Society of the United StatesAttn PJ Smith Corporate Engagement Manager2100 L Street NWWashington DC 20037

EXHIBIT A

PROPOSAL

RESOLVED that shareholders ask that Ross Stores Inc adopt a policy and amend other governingdocuments as necessary to require that the Boardrsquos Chair be an independent director as defined byNYSE This independence requirement shall apply prospectively so as not to violate any contractualobligation at the time this resolution is adopted Compliance with this policy is waived if no independentdirector is available and willing to serve as Chair The policy should also specify how to select a newindependent Chair if a current Chair ceases to be independent between annual shareholder meetings

SUPPORTING STATEMENT

As Executive Chair Ross Storesrsquo Board Chair is a company executive rather than an independentdirectormdasha practice thatrsquos come under increasing scrutiny for putting shareholders at risk This concept ofa Board Chair independence requirement is based on the following logic

1 The role of management including the CEO is to run the company and

2 the Boardrsquos role is to provide independent oversight of management including of the CEOtherefore

3 there is a potential conflict of interest and lack of checks and balances when a CEO is his or herown overseer while simultaneously managing the business

As Intelrsquos former chair Andrew Grove asks ldquoIs a company a sandbox for the CEO or is the CEO anemployee If hersquos an employee he needs a boss and that boss is the Board The Chairman runs theBoard How can the CEO be his own bossrdquo

Increasingly board members seem to agree According to a Sullivan amp Cromwell survey of 400 Boardmembers approximately 70 of respondents believe the head of management should not concurrentlyChair the Board

Indeed this is a growing issue in 2012 44 of all SampP 500 companies had Boards not chaired by theirCEO

An independent Board Chair has also been found to improve financial performance A 2012 GMI Ratingsreport titled The Costs of a Combined ChairCEO found that companies with a separate CEO and Chairprovide investors with five-year shareholder returns nearly 28 higher than those of companies helmedby a party of one

It makes sense then that numerous institutions support separation including CalPERS (Americarsquos largestpublic pension fund) and Institutional Shareholder Services (ISS) Additionally The Council ofInstitutional Investors whose members invest over $3 trillion states that a ldquoboard should be chaired by anindependent directorrdquo

Ensuring the Board Chair position is held by an independent directormdashrather than by companymanagementmdashwould benefit Ross Stores and its shareholders and we encourage shareholders to voteFOR this proposal

ri~~I ~~J~Y ~~ THE HUMANE SOCIETY

OF THE UNITED STATES

Erit L 3e11 Lhal E)q Cha of the Board

Jennifer leaning MD S ~ ~ Vice Chalf

Kathleen M linehan Eq Ooard Treasurer

Wayrl Picele PreSJdent amp CW

MichJc MJrkJriln (hie( Program amp Policy Office~

Laura tllalorey Chief Ope1ati7g Olf1Ce1

G Thomas Waite Ill Treasirer amp CFO

A11d1ew N Rtwdn Pl D Ch1el lritema11onal Oifias amp CJ~f Sciemifit Offite1

Robull A K ndler General C ounse Vice P1esdenr amp ClO

Janet D Frake 5eaetary

DIRECTORS

Jeffrey J Arcmiaco Eric l Berrthal Eq Michael J Blarnvell D VM MPH Jeny Cesak James Costcs bnita W Coupe Esq Neil B Fon Esq CA Jane Greerspu1 Gal~ Cathy Kangas Jonathan U Kaufeh Esq Paula A Kilak D VM Jennifer lcJning MD SM H Kathl n M Linehan Es~ John Mackey Mar1 I Max Pa tr ck l McDonnell Judy Nei Sharen teE Patrick Judy Peil Marier G Probst Jonath3 M Ratner Joshua s Reicren PhD Waler J Stewar Esq lndrewWeinstein JaonVe1i David 0 Wiebers MD Lona Willams

October 31 2016

John G Call EVP of Finance and Legal and Corporate Secretary Ross Stores

5130 Hacienda Drive Dublin CA 94568

Via UPS and email johncallroscom

RE Shareholder Proposal for Inclusion in the 2017 Proxy Materials

Dear Mr Call

Enclosed with this letter is a shareholder proposal submitted for inclusion in the proxy statement for the 2017 annual meeting and a letter from The Humane Society of the

United States (HSUS) brokerage firm BNY Mellon confirming ownership of Ross Stores common stock The HSUS has continuously held at least $2000 in market value

of Ross Stores common stock for the one-year period preceding and including the date of this letter and will hold at least this amount through and including the date of the 2017 shareholder meeting

Please contact me if you need any further information or have any questions If Ross Stores will attempt to exclude any portion of this proposal under Rule 14a-8 please advise me within 14 days of your receipt of this proposal I can be reached at 301-366-

6074 or pjsmithhumanesocietyorg Thank you for your assistance

Sincerely

PJ Smith Corporate Engagement Manager

Celebrat ing Animals I Confronting Cruelty

2 100 l Stbulleet NW Washington DC 20037 t 202 4521100 f 2027786132 humanesooetyorg

~middot BNY MELLON

October 31 2016

Frank J Mangone Vice President Sr Relationship Manager

BNY Mellon Wealth Management Family Office 200 Park Avenue Floor 8 New York NY 10016

John G Call EVP of Finance and Legal and Corporate Secretary Ross Stores 5130 Hacienda Drive Dublin CA 94568

Dear Mr Call

T 212 922 7526 F 877 340 3476 frank mangonebnymellon com

BNY Mellon National Association custodian for The Humane Society of the United States verifies that The Humane Society of the United States has continuously held at least $200000 in market value of Ross Stores common stock for the one-year period preceding and including the date of this letter Thank you

Best Regards

J-~~ Frank J Mangone Vice President BNY Mellon Wealth Management 212-922-7526

RESOLVED that shareholders ask that Ross Stores Inc adopt a policy and amend other governing documents as necessary to require that the Boards Chair be an independent director as defined by NYSE This independence requirement shall

apply prospectively so as not to violate any contractual obligation at the time this resolution is adopted Compliance with this policy is waived if no independent director is available and willing to serve as Chair The policy should also specify how to select a new independent Chair if a current Chair ceases to be independent between annual shareholder meetings

SUPPORTING STATEMENT

As Executive Chair Ross Stores Board Chair is a company executive rather than an independent director-a practice thats

come under increasing scrutiny for putting shareholders at risk This concept of a Board Chair independence requirement is based on the following logic

1 The role of management including the CEO is to run the company and 2 the Boards role is to provide independent oversight of management including of the CEO therefore

3 there is a potential conflict of interest and lack of checks and balances when a CEO is his or her own overseer while simultaneously managing the business

As Intels former chair Andrew Grove asks Is a company a sandbox for the CEO or is the CEO an employee If hes an

employee he needs a boss and that boss is the Board The Chairman runs the Board How can the CEO be his own boss

Increasingly board members seem to agree According to a Sullivan amp Cromwell survey of 400 Board members approximately 70 of respondents believe the head of management should not concurrently Chair the Board

Indeed this is a growing issue in 2012 44 of all SampP 500 companies had Boards not chaired by their CEO

An independent Board Chair has also been found to improve financial performance A 2012 GMI Ratings report titled The Costs of a Combined ChairCEO found that companies with a separate CEO and Chair provide investors with five-year

shareholder returns nearly 28 higher than those of companies helmed by a party of one

It makes sense then that numerous institutions support separation including CalPERS (Americas largest public pension fund) and Institutional Shareholder Services (ISS) Additionally The Council of Institutional Investors whose members

invest over $3 trillion states that a board should be chaired by an independent director

Ensuring the Board Chair position is held by an independent director-rather than by company management-would

benefit Ross Stores and its shareholders and we encourage shareholders to vote FOR this proposal

EXHIBIT B

CORRESPONDENCE WITH HSUS

From PJ Smith ltXXXXhumanesocietyorggtDate September 13 2016 at 40536 PM EDTTo michaelbalmuthrdquoSubject RossHSUS

Dear Michael

I hope yoursquore well Irsquom writing from The Humane Society of the United States to let you know that wersquoreconsidering a shareholder proposal at Ross seeking an independent board chair policy and to see if youor senior management would consider coming to the table with us instead

As background Everyone from the company who Irsquove worked with has been terrific including MarkLeHocky who was a great emissary for Ross Wersquove engaged with Ross for many years regarding theissue of products containing real fur Ross has told us privately that it does not knowingly sell itemscontaining real fur though unfortunately will not confirm that point in a public statement

Today animal welfare issues have come to bear such social and business relevance that we now ask allcompanies to make their sourcing policies transparentmdashwhich is indeed what dozens of the largestcompanies with animals in their supply chains (especially those that are publicly-owned) have done Forexamples Armani Hugo Boss HampM Zara Overstockcom SeaWorld and many top food companies

Since Ross does not knowingly buy real animal fur we hope yoursquoll agree that it wonrsquot take much to makethe policy public on your website Is this something yoursquod support Thanks so much and Irsquom happy tochat any time Have a great day

BestPJ Smith

PJ SmithCorporate Engagement ManagerXXXXhumanesocietyorg301366XXXX

[Sample email from HSUS to Ross Stores directors]

From PJ Smith ltXXXXhumanesocietyorggtDate October 5 2016 at 53502 AM GMT+9To stephenmilliganrdquogtSubject Ross board of directors

Hi Steve

I hope yoursquore well Irsquom writing from The Humane Society of the United States to let you know that wersquoreconsidering a shareholder proposal at Ross seeking an independent board chair policy and to see ifyoursquod support senior management coming to the table with us instead

As background Everyone from the company who Irsquove worked with has been terrific including MarkLeHocky whorsquos been a great emissary for Ross Wersquove engaged with Ross for many years regarding theissue of products containing real fur Ross has told us privately that it does not knowingly sell itemscontaining real fur though unfortunately will not institute a public-facing fur-free statement

Today animal welfare issues have come to bear such social and business relevance that we now ask allcompanies to make their sourcing policies transparentmdashwhich is indeed what dozens of the largestcompanies with animals in their supply chains (especially those that are publicly-owned) have done Forexamples Armani Hugo Boss HampM Zara Overstockcom SeaWorld and many top food companies

Since Ross does not knowingly buy real animal fur we hope yoursquoll agree that it wonrsquot take much to makethe policy public on your website Is this something yoursquod support Thanks so much and Irsquom happy tochat any time Have a great day

BestPJ Smith

PJ SmithCorporate Engagement ManagerXXXXhumanesocietyorg301366XXXX

From PJ Smith [mailtoXXXXhumanesocietyorg]Sent Monday December 12 2016 228 PMTo Michael Balmuth (NYBO Exec) Barbara Rentler (Chief Executive Officer)Subject HSUS

Hi Michael and Barbara

Hope yoursquore well Wanted to let you know that Irsquoll be in the San Francisco area for the month of Januaryin case yoursquod like to get together to discuss HSUSrsquos shareholder proposal and possible policy languagefor Ross now that TJ MaxxMarshallrsquos and Burlington Coat Factory are fur free

From my past discussions with Mark LeHocky I donrsquot think it requires much for us to get aligned on thisand hope you agree

Looking forward to hearing from you Have a happy holiday

BestPJ

PJ SmithSenior Manager Fashion PolicyXXXXhumanesocietyorg301366XXXX

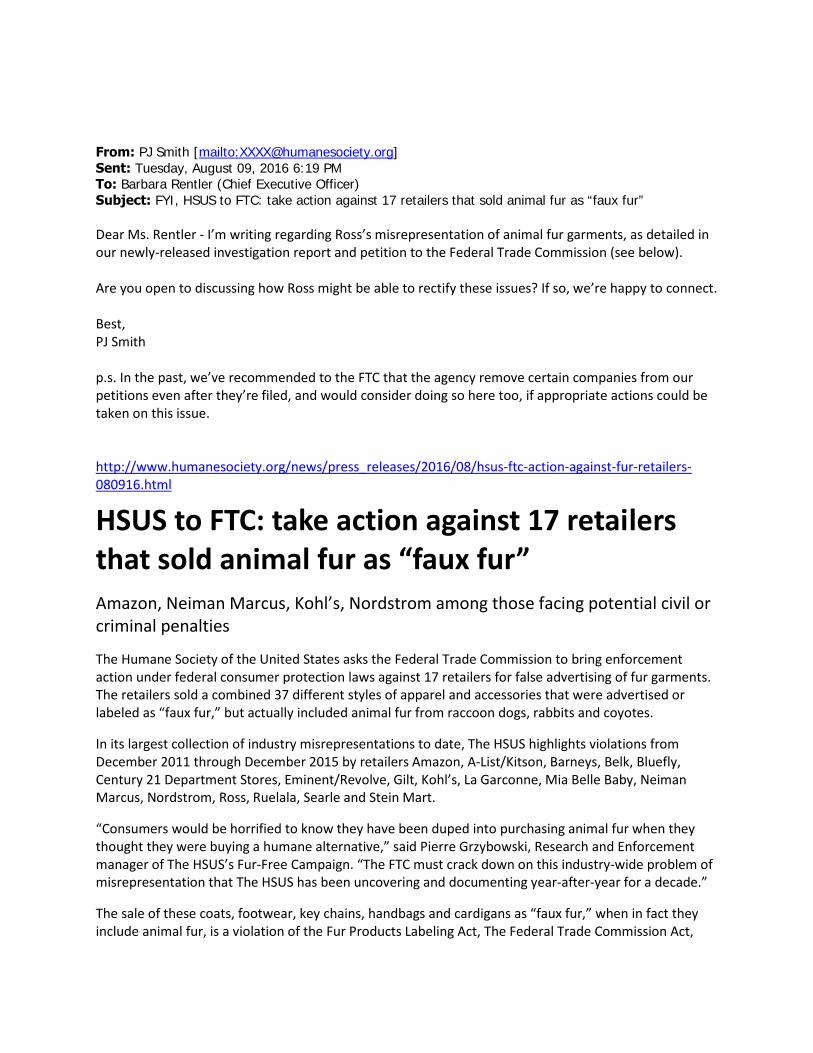

From PJ Smith [mailtoXXXXhumanesocietyorg]Sent Tuesday August 09 2016 619 PMTo Barbara Rentler (Chief Executive Officer)Subject FYI HSUS to FTC take action against 17 retailers that sold animal fur as ldquofaux furrdquo

Dear Ms Rentler - Irsquom writing regarding Rossrsquos misrepresentation of animal fur garments as detailed inour newly-released investigation report and petition to the Federal Trade Commission (see below)

Are you open to discussing how Ross might be able to rectify these issues If so wersquore happy to connect

BestPJ Smith

ps In the past wersquove recommended to the FTC that the agency remove certain companies from ourpetitions even after theyrsquore filed and would consider doing so here too if appropriate actions could betaken on this issue

httpwwwhumanesocietyorgnewspress_releases201608hsus-ftc-action-against-fur-retailers-080916html

HSUS to FTC take action against 17 retailersthat sold animal fur as ldquofaux furrdquoAmazon Neiman Marcus Kohlrsquos Nordstrom among those facing potential civil orcriminal penalties

The Humane Society of the United States asks the Federal Trade Commission to bring enforcementaction under federal consumer protection laws against 17 retailers for false advertising of fur garmentsThe retailers sold a combined 37 different styles of apparel and accessories that were advertised orlabeled as ldquofaux furrdquo but actually included animal fur from raccoon dogs rabbits and coyotes

In its largest collection of industry misrepresentations to date The HSUS highlights violations fromDecember 2011 through December 2015 by retailers Amazon A-ListKitson Barneys Belk BlueflyCentury 21 Department Stores EminentRevolve Gilt Kohlrsquos La Garconne Mia Belle Baby NeimanMarcus Nordstrom Ross Ruelala Searle and Stein Mart

ldquoConsumers would be horrified to know they have been duped into purchasing animal fur when theythought they were buying a humane alternativerdquo said Pierre Grzybowski Research and Enforcementmanager of The HSUSrsquos Fur-Free Campaign ldquoThe FTC must crack down on this industry-wide problem ofmisrepresentation that The HSUS has been uncovering and documenting year-after-year for a decaderdquo

The sale of these coats footwear key chains handbags and cardigans as ldquofaux furrdquo when in fact theyinclude animal fur is a violation of the Fur Products Labeling Act The Federal Trade Commission Act

and in some cases a violation of outstanding cease-and-desist orders already issued by the agencyViolations can carry penalties of up to one year in prison andor fines of up to $40000

MICHAEL Michael Kors Marc by Marc Jacobs Burberry Brit Canada Goose Rebecca Minkoff Elie Tahariand Rag amp Bone are among the 32 different brands of apparel and accessories sold by the retailersnamed in the petition

The submission represents the latest in a series of HSUS investigations and actions regarding rampantfalse advertising and labeling in the animal fur apparel industry The HSUS previously sought FTC actionon the problem in March 2007 April 2008 November 2011 July 2014 and April 2015 But lack ofvigorous industry-wide enforcement has allowed widespread violations to go unchecked

Neiman Marcus and EminentRevolve are already under 20-year cease-and-desist orders from the FTCfollowing an HSUS petition that identified similar violations in 2011

More details can be found in the links below

Enforcement petition

Graphical summary

PJ SmithCorporate Engagement ManagerXXXXhumanesocietyorg301366XXXX

The Humane Society of the United States1255 23rd Street NW Suite 450Washington DC 20037humanesocietyorg

- Ross Stores Inc (The Humane Society of the United States)

- Ross Stores-HSUS-NAL-withdrawal

-

DLA Piper LLP (US)

555 Mission Street Suite 2400San Francisco California 94105-2933wwwdlapipercom

Brad RockbradrockdlapipercomT 4158362598F 4156597309

January 30 2017VIA E-MAIL

OFFICE OF CHIEF COUNSELDIVISION OF CORPORATION FINANCESECURITIES AND EXCHANGE COMMISSION100 F STREET NEWASHINGTON DC 20549

Re Ross Stores IncWithdrawal of No-action Request and Notice of Intent to Omit from Proxy Materials theShareholder Proposal of the Humane Society of the United States

Ladies and Gentlemen

In a letter dated December 28 2016 we requested that the Staff of the Division of CorporationFinance concur that our client Ross Stores Inc a Delaware corporation (the ldquoCompanyrdquo) ispermitted to exclude from its proxy statement and form of proxy for its 2017 Annual Meeting ofStockholders (collectively the ldquo2017 Proxy Materialsrdquo) a stockholder proposal (the ldquoProposalrdquo)and statement in support thereof received on October 31 2016 from The Humane Society of theUnited States (ldquoHSUSrdquo)

Attached as Exhibit A is an email notice to the Company dated January 30 2017 fromMr PJ Smith Corporate Engagement Manager of HSUS which withdraws the Proposalsubmitted by HSUS In reliance on this notice from HSUS we hereby withdraw theDecember 28 2016 no-action request relating to the Proposal and the Companys ability toexclude it from the 2017 Proxy Materials pursuant to Rule 14a-8 under the Exchange Act of1934

January 30 2017Page Two

Please call me at (415) 836-2598 with any questions regarding this matter

Very truly yours

DLA Piper LLP (US)

Brad RockPartner

Enclosures

cc Ken Jew Senior Vice President General Counsel amp Assistant Corporate SecretaryRoss Stores Inc

The Humane Society of the United StatesAttn PJ Smith Corporate Engagement Manager1255 23rd Street NW Suite 450Washington DC 20037

EXHIBIT A

Email Notice from The Humane Society of the United States to withdraw Proposal[Edited to remove personally identifiable email and phone information]

From PJ Smith [mailto[xxx]humanesocietyorg]Sent Monday January 30 2017 200 PMTo Ken Jew (Legal)Subject HSUS stockholder proposal withdrawal

Hi Ken

Hope yoursquore well Please allow this e-mail to serve as official notification that HSUS is withdrawing itsshareholder proposal

I look forward to finding ways Ross and HSUS can work together to reduce the risks that go along withselling animal fur Irsquom confident these issues will continue to gain traction socially and in business asmore and more major companies become leaders on animal welfare

Happy to chat anytime Thanks

BestPJ Smith

PJ SmithSenior Manager Fashion Policy[xxx]humanesocietyorg301366xxxx

The Humane Society of the United States1255 23rd Street NW Suite 450Washington DC 20037humanesocietyorg

Join Our Email List Facebook Twitter Blog

WEST2751772421

DLA Piper LLP (US)

555 Mission Street Suite 2400San Francisco California 94105wwwdlapipercom

Brad RockbradrockdlapipercomT 4158362598F 4156597309

December 28 2016

VIA E-MAIL

OFFICE OF CHIEF COUNSELDIVISION OF CORPORATION FINANCESECURITIES AND EXCHANGE COMMISSION100 F STREET NEWASHINGTON DC 20549

Re Ross Stores IncNotice of Intent to Omit from Proxy Materials the ShareholderProposal of the Humane Society of the United States

Ladies and Gentlemen

This letter is to inform you that our client Ross Stores Inc a Delaware corporation (ldquoRossStoresrdquo or the ldquoCompanyrdquo) intends to omit from its proxy statement and form of proxy for its2017 Annual Meeting of Stockholders (collectively the ldquo2017 Proxy Materialsrdquo) a stockholderproposal (the ldquoProposalrdquo) and statement in support thereof received from The Humane Societyof the United States (ldquoHSUSrdquo or the ldquoProponentrdquo)

Pursuant to Rule 14a-8(j) we have

filed this letter with the Securities and Exchange Commission (theldquoCommissionrdquo) no later than eighty (80) calendar days before the Companyintends to file its definitive 2017 Proxy Materials with the Commission and

concurrently sent copies of this correspondence to the Proponent

Rule 14a-8(k) and Staff Legal Bulletin No 14D (Nov 7 2008) (ldquoSLB 14Drdquo) provide thatstockholder proposal proponents are required to send companies a copy of any correspondencethat the proponents elect to submit to the Commission or the staff of the Division of CorporationFinance (the ldquoStaffrdquo) Accordingly we are taking this opportunity to inform the Proponent thatif the Proponent elects to submit additional correspondence to the Commission or the Staff withrespect to this Proposal a copy of that correspondence should be furnished concurrently to theundersigned on behalf of the Company pursuant to Rule 14a-8(k) and SLB 14D

December 28 2016Page Two

THE PROPOSAL

The Proposal states

RESOLVED that shareholders ask that Ross Stores Inc adopt a policy and amend othergoverning documents as necessary to require that the Boardrsquos Chair be an independentdirector as defined by NYSE This independence requirement shall apply prospectively soas not to violate any contractual obligation at the time this resolution is adopted Compliancewith this policy is waived if no independent director is available and willing to serve asChair The policy should also specify how to select a new independent Chair if a currentChair ceases to be independent between annual shareholder meetings

A copy of the Proposal and Supporting Statement as well as related correspondence with theProponent are attached to this letter as Exhibit A

BACKGROUND

While the Proposal submitted by HSUS ostensibly relates to a matter of corporate governancethat is a pretext As plainly indicated in emails sent by an HSUS representative to Ross Storesofficers and directors prior to submitting the Proposal as well as in other prior and subsequentcommunications from HSUS in reality this is just a tactic and a further chapter in an ongoingcampaign by HSUS to pressure the Company to adopt a ldquofur freerdquo policy consistent with thepursuit by HSUS of its mission to promote the broad adoption of such policies by retailers foodcompanies and others In its own words HSUS has ldquoengaged with Ross for many yearsregarding the issue of products containing real furrdquo

In an email dated September 13 2016 addressed to Michael Balmuth (Executive Chairman ofRoss Stores) PJ Smith (Corporate Engagement Manager of HSUS) states

ldquoIrsquom writing from The Humane Society of the United States to let you know that wersquoreconsidering a shareholder proposal at Ross seeking an independent board chair policyand to see if you or senior management would consider coming to the table with usinstead (Emphasis added)

Wersquove engaged with Ross for many years regarding the issue of products containing realfur

Since Ross does not knowingly buy real animal fur we hope yoursquoll agree that it wonrsquottake much to make the policy public on your website Is this something yoursquod supportThanks so much and Irsquom happy to chat any time Have a great dayrdquo

December 28 2016Page Three

A copy of the referenced email as well as other related email correspondence from theProponent is attached to this letter as Exhibit B

Previously HSUS has made numerous other efforts and threats in pursuing its unique agendaover the years including a prior stockholder proposal and other attempts to take advantage ofrules and resources of federal governmental agencies that are intended for other purposes Thesepast efforts have also included campaigns of personal emails to officers or Board members of theCompany offering to stop the governmental action if ldquoappropriate actionrdquo (ie adoption of a ldquofurfreerdquo policy) is taken

For the Companyrsquos 2012 Annual Meeting of Stockholders HSUS submitted an express proposalfor the purpose of requesting a vote by the Companyrsquos shareholders on adoption of a ldquofur freerdquopolicy HSUS withdrew that proposal however before the Staff had responded to a no-actionrequest submitted by Ross Stores presumably because the Staff had issued its response inconnection with an essentially equivalent proposal concurring with the other registrantcompanyrsquos determination to exclude it See Ross Stores Inc (avail March 6 2012) andDilliardrsquos Inc (avail Feb 22 2012) The 2012 no-action request from Ross Stores and relatedcorrespondence with HSUS can be found at httpswwwsecgovdivisionscorpfincf-noaction14a-82012humanesociety030612-14a8pdf

More recently HSUS has sought to use the threat of federal rules intended to provide consumerprotection rights as a tool to pursue its own desire to pressure the Company and other retailers toadopt and publicly announce ldquofur freerdquo policies In August of 2016 HSUS issued a press releaseto draw attention to the petition it filed with the US Federal Trade Commission (the ldquoFTCrdquo) torequest that the FTC bring enforcement action under federal consumer protection laws against 17retailers alleging false advertising in regard to garments containing fur At page 22 of its 33-page long petition HSUS noted that one item of womenrsquos clothing (previously called out in apress release by HSUS in 2012) had allegedly been obtained by an HSUS investigator from aCompany store in October 2012 and that the investigator had examined the black fur trim anddetermined that it was animal fur and not faux fur as indicated on one sewn-in label Inconjunction with making the press release a representative of HSUS sent an email to the CEO ofRoss Stores ending with a post script note ldquops In the past wersquove recommended to the FTCthat the agency remove certain companies from our petitions even after theyrsquore filed and wouldconsider doing so here too if appropriate actions could be taken on this issuerdquo Copies ofrelevant items of email correspondence from representatives of HSUS are included in Exhibit Battached to this letter

As is apparent to anyone who visits the stores Ross Stores does not target apparel or othermerchandise that contains animal fur or consistently carry any particular merchandise thatcontains fur As an off-price retailer Ross Stores sources its products primarily from excess

December 28 2016Page Four

inventory of other retailers and from production overruns by manufacturers Items made fromfur or that include fur are not a meaningful merchandise category for the Company and are notsignificant or recognizable enough to even be separately tracked To the extent the Companyfrom time to time happens to carry isolated items that use any fur they are typically items ofapparel with purely incidental amounts of fur trim such as on winter coats or perhaps on fashionaccessories or in the lining of gloves The Companyrsquos buying staff believes that products thatuse animal fur represent far less than one percent (1) of the Companyrsquos clothing shoes andaccessory purchases

Ross Stores operates two brands of off-price retail apparel and home fashion stores AtOctober 29 2016 Ross Stores operated 1535 stores ndash 1342 Ross Dress for Lessreg locations in36 states the District of Columbia and Guam and 193 ddrsquos DISCOUNTSreg stores in 15 statesRoss offers first-quality in-season name brand and designer apparel accessories footwear andhome fashions for the entire family at savings of 20 to 60 off department and specialty storeregular prices every day Ross Dress for Less targets customers who are primarily from middleincome households while ddrsquos DISCOUNTS features a more moderately-priced assortment offirst-quality in-season name brand apparel accessories footwear and home fashions for theentire family at savings of 20 to 70 off moderate department and discount store regularprices every day Ross Stores sells recognizable brand-name merchandise that is current andfashionable in each category The mix of sales year to date by department in fiscal 2016 has beenapproximately as follows Ladies 29 Home Accents and Bed and Bath 24 Shoes 14Menrsquos 13 Accessories Lingerie Fine Jewelry and Fragrances 12 and Childrenrsquos 8 Themerchandise offerings also include product categories such as small furniture and furnitureaccents educational toys and games luggage gourmet food and cookware watches sportinggoods and in select Ross stores fine jewelry

The Board of Directors of Ross Stores (the ldquoBoardrdquo) currently consists of eleven (11) authorizedmembers The roles of Chairman of the Board (ldquoChairrdquo) and of Chief Executive Officer(ldquoCEOrdquo) are held by two separate individuals A separation of those roles has been in place onthe Board for twenty (20) years Michael Balmuth currently serves as Executive ChairmanMr Balmuth was formerly the Companyrsquos CEO from 1996 to 2014 The current CEO is BarbaraRentler she has been in that position since 2014 Beginning in fiscal 2014 the Board has alsodesignated a Lead Independent Director to act as a liaison between Chair CEO and independentdirectors and to serve as the designated Chair of the Nominating and Corporate GovernanceCommittee The designation of a Lead Independent Director is a widely adopted approach instructuring Board leadership to enhance the involvement and oversight of management by theindependent directors The Lead Independent Director position currently rotates annually amongthe independent directors

December 28 2016Page Five

BASES FOR EXCLUSION

The Company believes that the Proposal is excludable under at least two of the bases forexclusion set forth in Rule 14a-8(i) of the Exchange Act

1 [Rule 14a-8(i)(4)] Personal Grievance Special Interest If the proposal relates tothe redress of a personal claim or grievance against the company or any otherperson or if it is designed to result in a benefit to [the Proponent] or to further apersonal interest which is not shared by the other shareholders at large and

2 [Rule 14a-8(i)(3)] Violation of Proxy Rules If the proposal or supportingstatement is contrary to any of the Commissionrsquos proxy rules includingRule 14a-9 which prohibits materially false or misleading statements in proxysoliciting materials

ANALYSIS

A The Proposal is designed to result in a benefit to HSUS or to further a personalinterest of HSUS which is not shared by the other shareholders at large

Rule 14a-8(i)(4) permits the exclusion of a shareholder proposal that is designed to result in abenefit to the proponent or to further a personal interest of the proponent which is not shared bythe other shareholders at large Such a proposal is an abuse of the security holder proposalprocess

Although on its face appearing to be a proposal seeking a change on a matter of boardgovernance that is merely a pretext and is not the objective of HSUS in submitting the proposalThe Proposal was submitted by HSUS as a tactic to obtain leverage in its ongoing efforts topressure Ross Stores to publicly adopt a ldquofur freerdquo policy The real reason the Proposal wassubmitted is baldly revealed in the earlier (September 13 2016) email from HSUS quoted atlength in the Background Section above ldquo wersquore considering a shareholder proposal at Rossseeking an independent board chair policy and to see if you or senior management wouldconsider coming to the table with us instead rdquo Similar email messages were sent by HSUSto other members of the Board When the Company declined the invitation to ldquocome to thetablerdquo or engage further with HSUS regarding its continued demands for public announcement ofa ldquofur freerdquo policy HSUS subsequently delivered a request to include the Proposal by letterdated October 31 2016 Copies of relevant items of correspondence from representatives ofHSUS are included in Exhibit A and Exhibit B attached to this letter

The Commission has stated that Rule 14a-8(i)(4) is designed to ldquoinsure that the security holderproposal process [is] not abused by proponents attempting to achieve personal ends that are not

December 28 2016Page Six

necessarily in the common interest of the issuerrsquos shareholders generallyrdquo Exchange ActRelease No 20091 (Aug 16 1983) In addition the Commission has stated in discussing thepredecessor of Rule 14a-8(i)(4) (Rule 14a-8(c)(4)) that Rule 14a-8 ldquois not intended to provide ameans for a person to air or remedy some personal claim or grievance or to further somepersonal interest Such use of the security holder proposal procedures is an abuse of the securityholder proposal process and the cost and time involved in dealing with these situations do adisservice to the interests of the issuer and its security holders at largerdquo Exchange Act ReleaseNo 34-19135 (Oct 14 1982) Thus Rule 14a-8(i)(4) provides a means to exclude shareholderproposals the purpose of which is to ldquoair or remedyrdquo a personal grievance or advance somepersonal interest This interpretation is consistent with the Commissionrsquos statement at the timethe rule was adopted that ldquothe Commission does not believe that an issuerrsquos proxy materials are aproper forum for airing personal claims or grievancesrdquo Exchange Act Release No 12999(Nov 22 1976)

The Commission also has confirmed that this basis for exclusion applies even to proposalsphrased in terms that ldquomight relate to matters which may be of general interest to all securityholdersrdquo and thus that Rule 14a-8(i)(4) justifies the omission of neutrally-worded proposals ldquoif itis clear from the facts presented by the issuer that the proponent is using the proposal as a tacticdesigned to redress a personal grievance or further a personal interestrdquo Exchange Act ReleaseNo 19135 (Oct 14 1982) The Staffrsquos interpretation of Rule 14a-8(i)(4) clearly contemplateslooking beyond the four corners of a proposal for the purpose of identifying a personal interest orgrievance to which the submission of the proposal relates