disruptive innovation in christian higher education for access ed 2015 by andrew sears

TRANSCRIPT

Dr. Andrew Sears

President, City Vision College

Disruptive Innovation in

Christian Higher Education

PCs

Mobile

Disruptive Innovation Theory

Mainframes

Traditional

Higher

Education

Community

College

For Profit

Higher Education

Disruptive Innovation Theory

High Price Online Ed

Radically Affordable & Accessible

Online Education

Disruptive Innovation Theory

Image Source: Wikimedia

Online education is here

Cell Phones in 1983

Smart Phones: Disruptive Technology

Diamandis, P. H., & Kotler, S. (2012). Abundance: The future is better than you think. New York: Free

Press. p. 289

“People with a smart phone today can access tools that would have cost thousands a few decades ago.”

2. Christian Mega-

Universities

3. For Profit Universities

4. Shifts inDemographics

5. Increasing Costs

1. Economics of Online Education

5 Reasons for Limited Growth

for Most Christian Colleges

Christian

Colleges

1. Economics of Online Education

1. Online marginal cost per student at scale

(10,000+ students) is likely between $500-

3,000

2. Online education opens up competition

independent of geography

3. Online education is a platform business

where you pay “rent” to be visible (20-30% of

revenue)

4. Dominant characteristic of online education is

consolidation

13% of students are online only

Sources: Disruptive Innovation in Christian Higher Education, Andrew Sears, Doctoral Dissertation, 2014, Bakke University

Ambient Insight

• Top 20 largest online schools account for one-third online market.

• Higher education overall, about 222 schools make up one-third of enrollment.

Source: Online Higher Education Market Update - Eduventures. (n.d.). Retrieved March 16, 2015, from

http://www.eduventures.com/insights/online-higher-education-market-update/

Online Education = Consolidation

Go Big or Go Home

2. Christian Mega-universities & Growth

Liberty U43%

Grand Canyon U39%

All of CCCU18%

Estimated Growth Since 2005

Total Growth:

175,808 students

3. Growth of For Profits

Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and

Regulation. Center for College Affordability and Productivity (NJ1).

4. Demographic Shifts:

The End of the Good Times

Source: Hussar, W. J., & Bailey, T. M. (2014). Projections of Education Statistics to 2022. NCES

2014-051. National Center for Education Statistics.

5. Cost: Increasing Cost of Higher Education

The Pell Institute for the Study of Opportunity in Higher Education. (2015, January). Indicators of Higher Education

Equity in the United States 45 Year Trend Report. http://www.pellinstitute.org/

Bachelor’s Attainment by Income Quartile

37 pt. growth

3 pt. growth

6 pt. growth

19 pt. growth

Increasing focus on

Top quartile

Increases Cost

Future of Higher Education 2035

Tier 1: The Elite ◦ Serve top 5-10% students, tuition >$100k

◦ Analogy: New York Times, Economist

Tier 2: High Quality, Moderate Cost◦ 50% in bankruptcy, tuition $50-100k, high touch

◦ Analogy: Physical Retail, Cable TV

Tier 3: Good Enough Quality, Low Cost◦ 100k+ students or niche, tuition $100-$5,000/year

◦ Analogy: Huffington Post, niche ecommerce, Netflix

Tier 4: Courseware Ecosystem Small Businesses◦ Sell apps, courses, educational content, books, certificates, student services, videos, etc.

◦ Analogy: eBay/Amazon merchants, bloggers, self-publishers, app developers

Tier 5: Courseware platforms◦ 100’s of millions or billions of students

Source: Disruptive Innovation in Christian Higher Education, Andrew Sears, Doctoral Dissertation, 2014, Bakke University

Possible Futures1. Government

◦ Universal Community College, Nationalized Higher Education:

Obamacare for Higher Education

◦ Government mega universities: 1 million+ students

◦ Problem: increases secularizing influence of government education

2. Global Educational Conglomerate◦ 50% of “degrees” globally by 2050 may come from 3-4 tech

companies offering free education with a small payment for the

credential

◦ Problem: Likely to follow same secularizing tendency as media

conglomerates

3. Disruptive Innovation in Christian Higher Education◦ Innovators learn to build modularly on 1 & 2 to expand Christian

market share in post-secondary educationSource: Disruptive Innovation in Christian Higher Education, Andrew Sears, Doctoral Dissertation, 2014, Bakke University

University of Phoenix (2010)

Enrollment = 600,000

University of Phoenix (2015)

Enrollment = 215,000

Advice for Christian Colleges

1. Invest in marketing◦ Facilities expense is replaced by marketing expense (rent paid to

tech ecosystems)

2. Create an independent skunkworks division◦ “New wine in new wineskins”

◦ Conduct “lean startup” experiments to determine where to focus

◦ Fund an independent division to provide low-cost online

education. i.e. YourSchoolNameX

3. Develop plan to cut cost by 50%◦ Quit building buildings. Sell or lease buildings. Repurpose

buildings as earned income through co-working spaces and

incubation.

◦ Online education should have independent finances, so it can

reinvest revenue in online programs.

Current Stage

of Online Education

LMS Stage Courseware Stage

Image Source: Wikimedia

Innovation Cycle of Online Education

Process for Modular Christian Education

Theology & Christian Worldview

Audience, Pedagogy

& Goals

Christian Community

ChristianCourses

Theology Courses

Secular Courseware

Secular MOOCs & Open

Education ResourcesS

ub

ject

s

Comparing Business Models

For Profit◦ Revenue: $11,130 per student

◦ Instruction: 26%

Private Nonprofit◦ Revenue: $37,869 per student

◦ Instruction: 33%

◦ Research: 12.5%

Public◦ Revenue: $18,922 per student

◦ Instruction: 28%

◦ Research: 14%

Source: Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and Regulation. Center for

College Affordability and Productivity (NJ1). Retrieved from http://heartland.org/sites/all/modules/custom/heartland_migration/files/pdfs/29010.pdf

Understanding the for Profit Business Model

Sources: Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and Regulation. Center for

College Affordability and Productivity (NJ1). Retrieved from http://heartland.org/sites/all/modules/custom/heartland_migration/files/pdfs/29010.pdf

http://www.help.senate.gov/imo/media/for_profit_report/PartII/GrandCanyon.pdf

Marketing$3,389 35%

Profit $1,848 19%

Instruction$2,177 22%

Other $2,295 24%

For Profit Expenses (Grand Canyon)

Private Nonprofit: 32%

Modular Transformation of Computer Industry

Source: Only the Paranoid Survive, Andy Grove

U of A U of B

Virtually Integrated University

Univ.

Unbundled University

MOOCsOpen Ed

Resources

Study

Groups

Contracted

Courses

Adjunct

Faculty

Faculty

NetworksChurches

Internship

Univ.

Univ.

Univ.Research

LabCorporations Individuals

Open

ContentPublishers

Self-

Publish

Univ.Student

Community

Faculty

Community

Course

Materials

Written

Knowledge

Knowledge

Discovery

The Unbundled University

Churches

U of C U of D

Student

Community

Faculty

Community

Course

Materials

Written

Knowledge

Knowledge

Discovery

City Vision’s Re-bundled Online Ed Model

City Vision

Independent Educational Providers

(Straighterline)

Courseware

(Pearson & Mcgraw-Hill)

MOOCsOpen

Education Resources

Internship Sites (70+ sites)

Competency Credit for

Unaccredited Ministry &

Church Training

Church & Ministry

Discipleship Study Groups

Families & Home Schools

Content

Partners

Community

Partners

Traditional Higher Education

Traditional Monastery

Higher Education Model

Local Christian

Community

Practical Work

ExperienceStudents “Close” to Instructor

Distant From

Students

Re-bundling Online Education with

Church Study Groups & Internships

Local Discipleship &

Study Groups

Practical Work

Experience

Distant From

Students

Instructor

City Vision Educational Philosophy

Online Education

Local Discipleship

& Study Groups

Internships: Practical

Work Experience

What organization has the most locations in the USA?

14,146

25,900

Sources: http://hirr.hartsem.edu/research/fastfacts/fast_facts.html

http://www.usatoday.com/story/money/business/2014/05/04/24-7-wall-st-most-popular-stores/8614949/

314,000

Case Study Lessons for Christian Colleges

Retail & ecommerce◦ Operational effectiveness & scale

Theater, Movies, Cable TV, Blockbuster, Netflix◦ Offer high value both/and product

◦ Invest in digital growth not physical growth

VoIP/Skype◦ Domestic vs. Global Dominance

Journalism & News◦ Be more like innovators while retaining your strengths

Farming◦ Innovate & consolidate

Christian response to radio & Hollywood◦ Build culture/systems to outcompete rather than withdraw &

judgeSource: Disruptive Innovation in Christian Higher Education, Andrew Sears, Doctoral Dissertation, 2014, Bakke University

Possible Christian Models of Disruptive Innovation

Christian Megauniversities

◦ Liberty, Grand Canyon

Competency Based Education

◦ Lipscomb University, DePaul University, Antioch School of Church Planting

Radically New Education Models

◦ Logos Mobile Ed, Right Now Media, City Vision

Christian Open Education

◦ Open Biola, Covenant, Regent Luxvera, ChristianCourses.com, Christian Leaders

Institute, BiblicalTraining.org

◦ Aggregators of Christian Course Content: iTunes, Udacity, YouTube, Vimeo

Investment and Outsourcing Companies◦ Significant Systems, Capital Education Group, Bisk Education

Global Innovators

◦ Global University

Course Vendors & Clearinghouses◦ Knowledge Elements, Bible Mesh, Learning House

For More Information

Dissertation: “Disruptive Innovation in Christian Higher

Education and the Poor.” http://goo.gl/bKBt0x◦ YouTube Playlist: http://goo.gl/6Wptak (will soon include this talk)

◦ Bibliography: https://www.zotero.org/andrewsears/items

Slideshare for this talk: http://goo.gl/UOjpLK

Website: www.cityvision.edu

LinkedIn: www.linkedin.com/in/andrewsears

Contact: [email protected] 617-282-9798 x101

Would be glad to present to your school and am open to

consulting opportunities

Coming Soon in 2015 Disruptive Innovation in Christian

Higher Education book and website

Suggested Reading Christensen, C., Johnson, C. W., & Horn, M. B. (2010). Disrupting Class, Expanded Edition: How

Disruptive Innovation Will Change the Way the World Learns (2nd ed.). McGraw-Hill.

DeMillo, R. A. (2011). Abelard to Apple: the fate of American colleges and universities.

Cambridge, Mass.: MIT Press.

Horn, M. B., Staker, H., & Christensen, C. M. (2014). Blended: Using Disruptive Innovation to

Improve Schools (1 edition). San Francisco: Jossey-Bass.

Ries, E. (2011). The Lean Startup: How Today’s Entrepreneurs Use Continuous Innovation to

Create Radically Successful Businesses (First Edition). Crown Business.

Carey, K. (2015). The End of College: Creating the Future of Learning and the University of

Everywhere. New York: Riverhead Books.

Christensen, C. M., & Raynor, M. E. (2003). The Innovator’s Solution: Creating and Sustaining

Successful Growth (1 edition). Boston, Mass: Harvard Business School Press.

Craig, R. (2015). College Disrupted: The Great Unbundling of Higher Education. New York:

Palgrave Macmillan Trade.

McCluskey, F. B., & Winter, M. L. (2012). The Idea of the Digital University: Ancient Traditions,

Disruptive Technologies and the Battle for the Soul of Higher Education. Policy Studies

Organization.

Selingo, J. J. (2013). College (un)bound: the future of higher education and what it means for

students. Boston: Houghton Mifflin Harcourt.

Appendix

Essential Elements of Christian Education

1. Christian worldview

2. Christian community

3. Christian content

4. Christian care for stakeholders

Advice for Faculty

Case Studies: ◦ Music industry, journalism, TED

Find Research Funding or Find your “TED Talk”◦ Start with your “Idea Worth Spreading”

Read Platform, The Startup of You and The

Alliance

Establish your platform across multi-format and

multi-channel revenue sources

◦ Spread ideas horizontally across different media and

markets

◦ Teaching, consulting, writing, blogging, etc.

What is Driving Increasing Cost in Higher

Education? Part 1

Increased Productivity in Other

Sectors

Increased Cost of High Skilled Labor =

Increase Costs of Faculty & Senior Administration

Increased• standardized tests• large lectures• teaching assistants• administrative staff• adjuncts

Symptoms to CopeUnderlying Cause 1

Baumol’s Cost Disease

Economics of Superstars

Sources: Archibald, R. B., & Feldman, D. H. (2010). Why Does College Cost So Much? (First Edition edition). Oxford, U.K. ;

New York: Oxford University Press, USA.

Disruptive Innovation in Christian Higher Education, Andrew Sears, Doctoral Dissertation, 2014, Bakke University

Increasing Cost of High Skilled Labor

Source: Archibald, R. B., & Feldman, D. H. (2010). Why Does College Cost So Much? (First Edition edition). Oxford, U.K. ;

New York: Oxford University Press, USA.

What is Driving Increasing Cost in Higher

Education? Part 2

Decreasing Gov’t

Funding of Higher

Education

Sources: Archibald, R. B., & Feldman, D. H. (2010). Why Does College Cost So Much? (First Edition edition). Oxford, U.K. ;

New York: Oxford University Press, USA.

Disruptive Innovation in Christian Higher Education, Andrew Sears, Doctoral Dissertation, 2014, Bakke University

About City Vision College History: Started Rescue College in 1998 as a Program of AGRM,

DETC Accreditation in 2005, Transferred to TechMission in 2008

Degrees

◦ Bachelor’s in Nonprofit Management, Addictions Studies, Missions

◦ Master’s in Technology and Ministry

Statistics

◦ 79% of receive Pell grants

◦ 67% graduation rate in 2013

◦ Cumulative 91% job placement rate

◦ Tripled enrollment since 2008

Goal is to be Radically Affordable

◦ Tuition $6,000/year undergrad and $10,800 grad, $3,500 for interns,

$3,000 in developing countries

◦ Cost is less than 95% of private nonprofit institutions (16th lowest Christian)

◦ CCCU Average Tuition: $24,355, Liberty University’s online tuition $12,882,

National average tuition $30,994

Image Source: Wikimedia

Stage in Adoption Cycle for

Post-Secondary Degrees

US

AverageGlobal

Average

Top

Quartile

3rd

Quartile

1st & 2nd

Quartile

How to Cross the Chasm for the Bottom Half

1. Radically Affordable◦ Radically low cost and debt

◦ Options: Gov’t subsidy or disruptive innovation

2. Ease of Access◦ Location, Time, Working Students, Mobile

3. Remedial education available if needed◦ Adaptive for students at any level

4. Cultural fit◦ Adult Friendly, No Assimilation

Why City Vision is Uniquely Positioned

for This Opportunity?

Jesus(Christian)

Technology(radically

affordable)

Justice (Serves bottom

half)

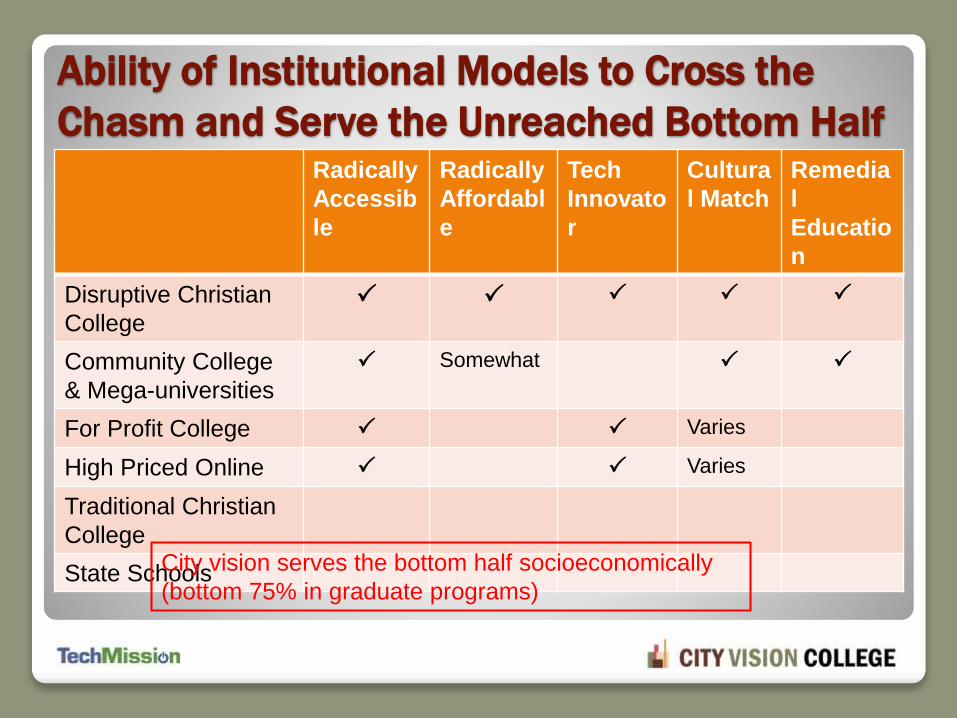

Ability of Institutional Models to Cross the

Chasm and Serve the Unreached Bottom HalfRadically

Accessib

le

Radically

Affordabl

e

Tech

Innovato

r

Cultura

l Match

Remedia

l

Educatio

n

Disruptive Christian

College

Community College

& Mega-universities

Somewhat

For Profit College Varies

High Priced Online Varies

Traditional Christian

College

State SchoolsCity vision serves the bottom half socioeconomically

(bottom 75% in graduate programs)

Christian

Social Services

Radically Affordable

Socially Responsible

Christian Education

City Vision Strategy

Rescue College

Urban Missions

1998-2007

City Vision 1.0

2008-14

City Vision 2.0

2015 -

20th Century Challenge: High School Graduation

Goldin, C., & Katz, L. F. (2010). The Race between Education and Technology. Cambridge, Mass.: Belknap Press.

21st Century Challenge: College Graduation

Change High School Graduate by State

Source: Hussar, W. J., & Bailey, T. M. (2014). Projections of Education Statistics to 2022. NCES

2014-051. National Center for Education Statistics.

Demographic Shifts: Race/Ethnicity

Source: Hussar, W. J., & Bailey, T. M. (2014). Projections of Education Statistics to 2022. NCES

2014-051. National Center for Education Statistics.

Source: (US. Bureau of Labor Statistics, 2014)

47% of employment in America is at high risk of being automated

away over the next decade or two (Frey & Osborne, 2013)

Debt: Distribution of Total Student Debt by

Level of Household Net Worth

Changing our Educational Trajectory

(Lumina Foundation Vision)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2025 2050 2075 2100

Straight Line Projection Growth Degree Attainment 21st Century

0%

20%

40%

60%

80%

100%

120%

2025 2050 2075 2100

Straight Line Projection By Income Quartile

Top Quartile 3nd Quartile 2nd Quartile Bottom Quartile

21st Century

Disruptive

Innovation

Opportunity

City Vision’s

Focus

Focus of

Traditional

Christian

Higher

Education

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2025 2050 2075 2100

Difference in Projected Educational Attainment

Straight Line No Change in Growth Rate of Bottom 3 Quartiles

The Problem with Only Credentialing

The 25th percentile for male college graduates has been about $4,000 to $5,000 more

than the median male high school graduate in recent years, whereas among women, the

gap has recently been around $2,000.

Source: http://libertystreeteconomics.newyorkfed.org/2014/09/college-may-not-pay-off-for-everyone.html#.VUJT69LF8ep

College Entrance, Completion & Persistence by Income Quartile

http://www.russellsage.org/research/chartbook/percentage-students-entering-and-completing-college-and-college-persistence-incom

Growth of For Profit Education

Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and

Regulation. Center for College Affordability and Productivity (NJ1).

For Profits Dominate Age 22 and above

Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and

Regulation. Center for College Affordability and Productivity (NJ1).

For Profits Dominate Black & Latino Students

Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and

Regulation. Center for College Affordability and Productivity (NJ1).

For Profits Serve Disproportionately Female Students

Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and

Regulation. Center for College Affordability and Productivity (NJ1).

Average Revenue per Student

Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and

Regulation. Center for College Affordability and Productivity (NJ1).

Average Spending Per Student

Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and

Regulation. Center for College Affordability and Productivity (NJ1).

Instructional Spending by Type

Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and

Regulation. Center for College Affordability and Productivity (NJ1).

For Profits Get Disproportionally High Federal Aid

Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and

Regulation. Center for College Affordability and Productivity (NJ1).

For Profits Highest Load Debt Per Student

Bennett, D. L., Lucchesi, A. R., & Vedder, R. K. (2010). For-Profit Higher Education: Growth, Innovation and

Regulation. Center for College Affordability and Productivity (NJ1).

Online Education = Consolidation

• Top 20 largest online schools account for one-third online market.

• Higher education overall, about 222 schools make up one-third of enrollment.

Online Higher Education Market Update - Eduventures. (n.d.). Retrieved March 16, 2015, from

http://www.eduventures.com/insights/online-higher-education-market-update/