devonshire research group, llcdevonshireresearch.com/research/devonshire research group -...

TRANSCRIPT

May 2016May 2016May 2016May 2016

Devonshire Research Group, LLCDevonshire Research Group, LLCDevonshire Research Group, LLCDevonshire Research Group, LLC

Tesla Motors, Inc.

Part II

This presentation is a research report and is for informational purposes only. Opinions expressed are solely those of Devonshire Research Group and this is not a recommendation to purchase securities discussed

herein. This presentation is confidential and may not be reproduced or distributed without the express consent of Devonshire Research Group. Please refer to the next slide for additional disclosures.

-Attorney Confidential-

Disclaimer

Devonshire Research Group, LLC (“Devonshire Research Group”) is an investment adviser to funds and accounts that are in the business of buying and selling

securities and other financial instruments.

Devonshire Research Group currently has a short position in the securities of the subject company covered herein (“Subject Company”). Devonshire Research

Group will profit if the trading prices of Subject Company’s securities decline. Devonshire Research Group may change its views about or its investment

positions in Subject Company at any time, for any reason or no reason. Devonshire Research Group may buy, sell, cover or otherwise change the form or

substance of its Subject Company investment. Devonshire Research Group disclaims any obligation to notify the market of any such changes.

The information and opinions expressed in this presentation (the “Presentation”) are based on publicly available information about Subject Company.

Devonshire Research Group recognizes that there may be non-public information in the possession of Subject Company or others that could lead Subject

Company or others to disagree with Devonshire Research Group’s analyses, conclusions and opinions. The Presentation expresses Devonshire Research

Group’s opinions, which are based upon publicly available information, inferences and deductions through its due diligence and analytical process. To the best

of its ability and belief, all information contained herein and in any oral communication is accurate and reliable, and has been obtained from public sources

Devonshire Research Group believes to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may

otherwise owe any fiduciary duty or duty of confidentiality to Subject Company. However, such information is presented “as is,” without warranty of any kind,

whether express or implied. Devonshire Research Group makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any

such information or with regard to the results to be obtained from its use.

The Presentation contains a very large measure of analysis and opinion and includes forward-looking statements, estimates, projections and opinions prepared

with respect to, among other things, Subject Company’s anticipated operating performance, access to capital markets, market conditions, cash flow, assets and

liabilities. Such statements, estimates, projections and opinions may prove to be substantially inaccurate and are inherently subject to significant risks and

uncertainties beyond Devonshire Research Group’s control. All expressions of opinion are subject to change without notice, and Devonshire Research Group

does not undertake to update or supplement any reports or any of the information, analysis and opinion contained in them.

The Presentation is not investment advice or a recommendation or solicitation to buy or sell any securities. Except where otherwise indicated, the Presentation

speaks as of the date hereof, and Devonshire Research Group undertakes no obligation to correct, update or revise the Presentation or to otherwise provide any

additional materials. Devonshire Research Group also undertakes no commitment to take or refrain from taking any action with respect to Subject Company or

any other company.

As used herein, except to the extent the context otherwise requires, Devonshire Research Group includes its affiliates and its and their respective partners,

directors, officers and employees.

2

-Attorney Confidential-

Notice of investment interests

3

As of the publication date of this report, the Devonshire Research Group LLC has a net

short position in the stock, put options, bonds, and credit swaps of Tesla Motors, Inc.

(“TSLA” or “Tesla”) and stands to realize gains in the event that the price of TSLA’s

securities declines over the long run, or if investment sentiment improves the appeal of an

expected decline in any of its securities.

Devonshire Research Group recognizes that while its strategy reflects a long term bearish

outlook for Tesla’s security instruments, the short term implication of powerful

marketing, including the power of social media tweeting by the CEO and his PR firm, well

orchestrated and heavily blogged product launches, and a deep and powerful short term

media control and attention span, suggests unpredictable short term volatility.

Devonshire Research Group LLC has a long term net short position across multiple

security instruments.

-Attorney Confidential-

Notice of non-affiliation

4

Part I of this analysis, released publicly in March 2016, was widely praised as effective and fact-driven. Critics of

the analysis allege that the work of the Devonshire Research Group is unfairly biased, due to affiliations with

industry players who seek to limit the market performance of Tesla. This is interesting, but untrue.

Devonshire Research Group hereby asserts that it does not have professional or business relationships with any of

the following organizations:

General Motors

Ford

Toyota

The City of Detroit

Koch Industries

ExxonMobil

Royal Dutch Shell

BP

CB Insights

The Illuminati

Marshall Mathers, aka “Eminem”

-Attorney Confidential-

On financial innovation and creative accounting

5

Never assume malice when stupidity will suffice.

- Hanlon’s Razor

Everything should be as simple as it can be, but not simpler.

- Occam’s Razor

-Attorney Confidential-

Executive Summary

6

� How closely does TSLA’s financing model mirror the features of common Ponzi, Pyramid, and Matrix schemes?

− Numerous cautionary examples share features with TSLA, including hype driven by “visionary leaders”

− TSLA has accepted capital from unsophisticated investors with bold claims on return and/or product value

− If TSLA fails to deliver on these claims it has the potential to enter a death spiral

− Most common death spirals do not require malicious intent, but rather excessive (even delusional) ambition

� The profitability of the Model 3 depends on TSLA’s ability to squeeze its supply chain; this is a tall order

− Sophisticated suppliers (most notably Panasonic) will fight for their share of the profit

− Panasonic’s rechargeable battery division is constrained in terms of investment capacity and profit demands

− Current suppliers of numerous strategic, high-technology components have little IP and export to the US

− Many Chinese suppliers are vulnerable to patent infringement accusations and could face ITC injunctions

� TSLA’s use of tax credits disproportionately benefits the wealthy at the expense of the average taxpayer

− This inequality is a feature of the luxury-first market penetration strategy

− The election year introduces significant risk for TSLA’s continued reliance on taxpayer subsidies

-Attorney Confidential-

Tesla has engaged in aggressive accounting that calls to mind the

experiences of Enron and WorldCom; its future is highly uncertain

7

-3

-2

-1

0

1

2

3

4

200220012000199919981997

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1996 1997 1998 1999 2000 2001

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

2012 2013 2014 2015

WorldCom Net Income WorldCom Net Income WorldCom Net Income WorldCom Net Income

(US Billions)(US Billions)(US Billions)(US Billions)

Enron Net Income Enron Net Income Enron Net Income Enron Net Income

(US Billions)(US Billions)(US Billions)(US Billions)

Tesla Motors Earnings Tesla Motors Earnings Tesla Motors Earnings Tesla Motors Earnings

Per Share (USD)Per Share (USD)Per Share (USD)Per Share (USD)

Tesla has escalated a dangerous habit of unorthodox future-earning-based financing in pursuit of the

questionably profitable and long-delayed Model 3. A misstep in the next two years risks entering a death spiral

Tesla has escalated a dangerous habit of unorthodox future-earning-based financing in pursuit of the

questionably profitable and long-delayed Model 3. A misstep in the next two years risks entering a death spiral

Originally

reported

Revised

Aug 2002

Originally

reported

Revised

Nov 2001

GAAP

Non-GAAP

Source: Devonshire Research Group considers Tesla’s decision to use non-GAAP accounting methods to be inherently aggressive; unorthodox future earnings based financing defined on slide 11

-Attorney Confidential-

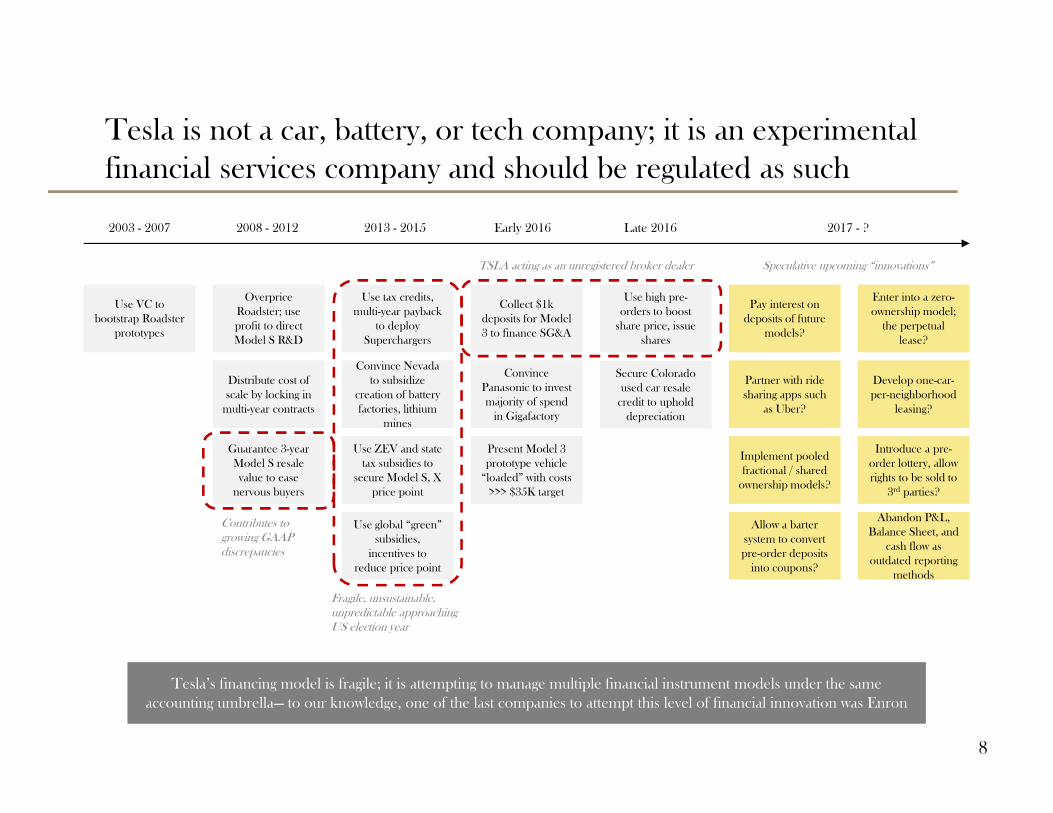

Tesla is not a car, battery, or tech company; it is an experimental

financial services company and should be regulated as such

8

Tesla’s financing model is fragile; it is attempting to manage multiple financial instrument models under the same

accounting umbrella— to our knowledge, one of the last companies to attempt this level of financial innovation was Enron

Tesla’s financing model is fragile; it is attempting to manage multiple financial instrument models under the same

accounting umbrella— to our knowledge, one of the last companies to attempt this level of financial innovation was Enron

Use ZEV and state

tax subsidies to

secure Model S, X

price point

Use tax credits,

multi-year payback

to deploy

Superchargers

Use global “green”

subsidies,

incentives to

reduce price point

Convince Nevada

to subsidize

creation of battery

factories, lithium

mines

Use high pre-

orders to boost

share price, issue

shares

Secure Colorado

used car resale

credit to uphold

depreciation

Collect $1k

deposits for Model

3 to finance SG&A

Convince

Panasonic to invest

majority of spend

in Gigafactory

TSLA acting as an unregistered broker dealer

Fragile, unsustainable, unpredictable approaching US election year

Speculative upcoming “innovations”

Use VC to

bootstrap Roadster

prototypes

Overprice

Roadster; use

profit to direct

Model S R&D

Distribute cost of

scale by locking in

multi-year contracts

Pay interest on

deposits of future

models?

Partner with ride

sharing apps such

as Uber?

Implement pooled

fractional / shared

ownership models?

Allow a barter

system to convert

pre-order deposits

into coupons?

Enter into a zero-

ownership model;

the perpetual

lease?

Develop one-car-

per-neighborhood

leasing?

Introduce a pre-

order lottery, allow

rights to be sold to

3rd parties?

Abandon P&L,

Balance Sheet, and

cash flow as

outdated reporting

methods

2003 - 2007 2008 - 2012 2013 - 2015 Early 2016 Late 2016 2017 - ?

Guarantee 3-year

Model S resale

value to ease

nervous buyers

Contributes to growing GAAP discrepancies

Present Model 3

prototype vehicle

“loaded” with costs

>>> $35K target

-Attorney Confidential-

Non-GAAP strategies to limit Model S depreciation boost stock

price at the cost of increased fragility and hidden downside risk

9Source: Edmunds.com, NADA used car guide 2015; Devonshire Research Group analysis suggests traditional accounting strategies would be sufficient without promised resale guarantees and buy-back pricing

Model 3 Model S

RVG threshold

Model S

Model 3 reveal threatens to tank Model S resale values, so Tesla hoards used vehicles to

resell under Colorado used EV credit incentive

Model S resale value guarantee closes negative feedback loop: liability grows as Model S depreciates faster

-Attorney Confidential-

Similarly, Tesla’s 400,000+ unsophisticated, unsecured, and

unpredictable Model 3 “creditors” contribute to a bank run setup

Highly Confidential 10

What could go wrong?What could go wrong?What could go wrong?What could go wrong?Probability before Probability before Probability before Probability before

Model 3 revealModel 3 revealModel 3 revealModel 3 reveal

Probability after Probability after Probability after Probability after

Model 3 revealModel 3 revealModel 3 revealModel 3 revealRationaleRationaleRationaleRationale

Quality issues force delays in Model 3 delivery 30% 75%Urgent drive for cost reduction on fixed timeline

Panasonic drags feet on Gigafactory investment 40% 60%Lack of promised partnerships, minimum purchase agreement

Tesla forced to implement Model 3 buyback guarantee 25% 35%Fear of high depreciation rates stemmingfrom quality concerns

Consortium of auto companies lobbies to remove tax credits 20% 30%Political hot-button issue, Tesla credits benefit the rich

GM raises war chest to acquire IP and litigate against Tesla 10% 20%Minimal IP ownership by Tesla and throughout its supply chain

Tessera or RPX engage in an auto IP relicensing campaign 10% 15%Brewing automotive patent war brings NPEs and related players

Sole-source parts supplier raises prices, taking inventory hostage 5% 10%Model 3 deadline gives suppliers incredible bargaining power

Factory workforce goes on strike / labor dispute 5% 10%Model 3 deadline gives labor force incredible bargaining power

Model 3 subject to regulatory scrutiny for road safety 5% 10%Rapid push to delivery will face scrutiny, especially after Model X

SEC antagonizes TSLA for improper Twitter promotion (Musk) 2% 5%Increased scrutiny surrounding critical upcoming capital raise

IP litigation results in ITC injunction on foreign part imports 2% 5%Incentive for competitors to hamstring already-weak supply network

The Model The Model The Model The Model 3 reveal 3 reveal 3 reveal 3 reveal lights lights lights lights a twoa twoa twoa two----year year year year fuse: setbacks and delays will escalate refunds on depositsfuse: setbacks and delays will escalate refunds on depositsfuse: setbacks and delays will escalate refunds on depositsfuse: setbacks and delays will escalate refunds on deposits

Tesla is operationally vulnerable to setbacks, and the deposit scheme amplifies this vulnerability.

Depositholders expect a $35k vehicle in 2017—how many will vanish if this target is revised?

Tesla is operationally vulnerable to setbacks, and the deposit scheme amplifies this vulnerability.

Depositholders expect a $35k vehicle in 2017—how many will vanish if this target is revised?

Note: probabilities are Devonshire Research Group estimates

Probability of one or more tail risk missteps: 60%60%60%60% 80%80%80%80%

-Attorney Confidential-

To understand Tesla’s business model, we must introduce novel

financial definitions

11

If a business is operated as a FEPF, investors should not carry the expectation that such an enterprise will be run

for a profit; instead, this organization should be terminated, or regulated as a social service or non-profit

If a business is operated as a FEPF, investors should not carry the expectation that such an enterprise will be run

for a profit; instead, this organization should be terminated, or regulated as a social service or non-profit

Future-earning pyramidal financing (FEPF) is a business dynamic characterized by the act of raising

capital to finance future losses rather than future returns. The assumption in this dynamic is that

the future losses will be covered by a second capital raise (similarly pyramidal) which will allow

some investors to exit profitably, although many will reinvest and / or accept losses.

When properly recognized, managed, and regulated, FEPF can be a sustainable arrangement that

operates within both the spirit and letter of the law. Examples may be found in the realm of public

services, non-profits, and social service programs. However, when performed maliciously with

intent to defraud, FEPF forms the dynamic underlying illegal Ponzi, pyramid, and matrix schemes.

Aggressive cash-negative growth ventures that rely entirely on profitability at scale occupy a

dangerous middle ground where delusion often substitutes for malice.

Future-Earning

Pyramidal Financing

(FEPF)

Loss-Tolerant

Investors

(LTI’s)

A category of investors that are capable of losing their investment in an enterprise, company, or

asset with or without their knowledge of this loss.

Financing Pyramid

Reporting

(FPR)

A form of financial reporting adopted from non-profit and venture capital investing that accurately

reflects businesses that are designed to lose money for long periods of time until subsequent

investors are secured, who must confront the needs to building a profitable business

-Attorney Confidential-

How to detect future-earning based financing: 8 key features

12

Risk factors for FEPFsRisk factors for FEPFsRisk factors for FEPFsRisk factors for FEPFs DescriptionDescriptionDescriptionDescription Strong presenceStrong presenceStrong presenceStrong presence Some presenceSome presenceSome presenceSome presence No presenceNo presenceNo presenceNo presence

Investors who contribute capital to a Investors who contribute capital to a Investors who contribute capital to a Investors who contribute capital to a

fundamentally moneyfundamentally moneyfundamentally moneyfundamentally money----losing venturelosing venturelosing venturelosing venture

FEPF finances future losses; investors in these ventures may be victims of fraud, but not always

Continual postponement of profitable operation Continual postponement of profitable operation Continual postponement of profitable operation Continual postponement of profitable operation

with fresh investor capitalwith fresh investor capitalwith fresh investor capitalwith fresh investor capital

Pyramidal financing requires future pyramidal financing to succeed; this recursive aspect is key

Offer of unusual, timeOffer of unusual, timeOffer of unusual, timeOffer of unusual, time----sensitive incentives to sensitive incentives to sensitive incentives to sensitive incentives to

increase demand among investorsincrease demand among investorsincrease demand among investorsincrease demand among investors

FEPF is not standard fundraising, and non-standard fundraising tactics are commonly used

Impressive “returns” which are projected on Impressive “returns” which are projected on Impressive “returns” which are projected on Impressive “returns” which are projected on

paper but may not be achievable at scalepaper but may not be achievable at scalepaper but may not be achievable at scalepaper but may not be achievable at scale

Loss of investor confidence will destroy the FEPF dynamic, so reinvestment rates must be kept high

Minimum return guarantees to increase Minimum return guarantees to increase Minimum return guarantees to increase Minimum return guarantees to increase

confidence of skeptical investorsconfidence of skeptical investorsconfidence of skeptical investorsconfidence of skeptical investors

Permitting investors to exit with generous terms increases odds of subsequent reinvestment

Appeal to moral sensibility with highAppeal to moral sensibility with highAppeal to moral sensibility with highAppeal to moral sensibility with high----minded minded minded minded

aspirations toward equality and generosityaspirations toward equality and generosityaspirations toward equality and generosityaspirations toward equality and generosity

Often an offsetting factor allowing investors to justify investment in a loss-making enterprise

“Disruptive” business model, often with “Disruptive” business model, often with “Disruptive” business model, often with “Disruptive” business model, often with

reasoning reasoning reasoning reasoning opaque to all but a “visionary” leaderopaque to all but a “visionary” leaderopaque to all but a “visionary” leaderopaque to all but a “visionary” leader

A common theme is that old rules no longer apply; irregularities are written off as complexities

Rapid growth leading to collapse unless tightly Rapid growth leading to collapse unless tightly Rapid growth leading to collapse unless tightly Rapid growth leading to collapse unless tightly

monitored and regulatedmonitored and regulatedmonitored and regulatedmonitored and regulated

Uncontrolled growth in these scenarios is often the catalyst for failure—control is key to legitimacy

MaliciousMaliciousMaliciousMalicious DelusionalDelusionalDelusionalDelusional SustainableSustainableSustainableSustainableOverambitiousOverambitiousOverambitiousOverambitiousTypical occurrence cases:

Source: Devonshire Research Group analysis of comparable financing models

-Attorney Confidential-

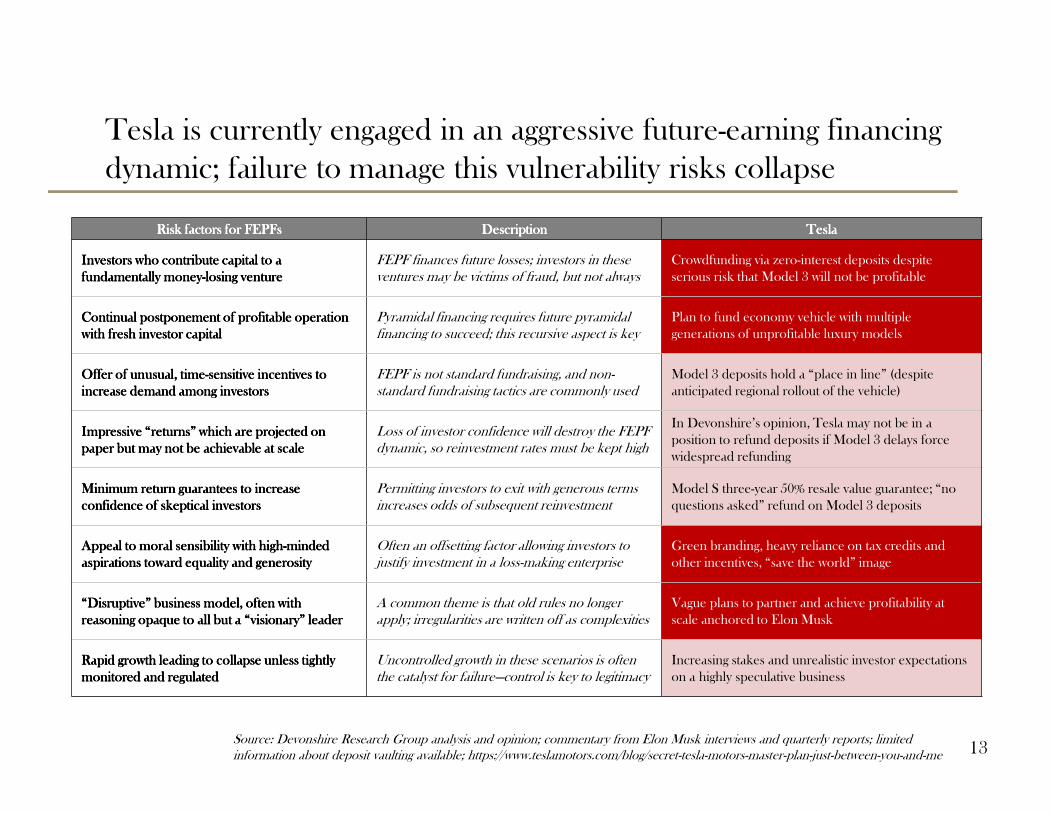

Tesla is currently engaged in an aggressive future-earning financing

dynamic; failure to manage this vulnerability risks collapse

13

Risk factors for FEPFsRisk factors for FEPFsRisk factors for FEPFsRisk factors for FEPFs DescriptionDescriptionDescriptionDescription TeslaTeslaTeslaTesla

Investors who contribute capital to a Investors who contribute capital to a Investors who contribute capital to a Investors who contribute capital to a

fundamentally moneyfundamentally moneyfundamentally moneyfundamentally money----losing venturelosing venturelosing venturelosing venture

FEPF finances future losses; investors in these ventures may be victims of fraud, but not always

Crowdfunding via zero-interest deposits despite

serious risk that Model 3 will not be profitable

Continual postponement of profitable operation Continual postponement of profitable operation Continual postponement of profitable operation Continual postponement of profitable operation

with fresh investor capitalwith fresh investor capitalwith fresh investor capitalwith fresh investor capital

Pyramidal financing requires future pyramidal financing to succeed; this recursive aspect is key

Plan to fund economy vehicle with multiple

generations of unprofitable luxury models

Offer of unusual, timeOffer of unusual, timeOffer of unusual, timeOffer of unusual, time----sensitive incentives to sensitive incentives to sensitive incentives to sensitive incentives to

increase demand among investorsincrease demand among investorsincrease demand among investorsincrease demand among investors

FEPF is not standard fundraising, and non-standard fundraising tactics are commonly used

Model 3 deposits hold a “place in line” (despite

anticipated regional rollout of the vehicle)

Impressive “returns” which are Impressive “returns” which are Impressive “returns” which are Impressive “returns” which are projected on projected on projected on projected on

paper but may not be paper but may not be paper but may not be paper but may not be achievable at achievable at achievable at achievable at scalescalescalescale

Loss of investor confidence will destroy the FEPF dynamic, so reinvestment rates must be kept high

In Devonshire’s opinion, Tesla may not be in a

position to refund deposits if Model 3 delays force

widespread refunding

Minimum return guarantees to increase Minimum return guarantees to increase Minimum return guarantees to increase Minimum return guarantees to increase

confidence of skeptical investorsconfidence of skeptical investorsconfidence of skeptical investorsconfidence of skeptical investors

Permitting investors to exit with generous terms increases odds of subsequent reinvestment

Model S three-year 50% resale value guarantee; “no

questions asked” refund on Model 3 deposits

Appeal to moral sensibility with highAppeal to moral sensibility with highAppeal to moral sensibility with highAppeal to moral sensibility with high----minded minded minded minded

aspirations toward equality and generosityaspirations toward equality and generosityaspirations toward equality and generosityaspirations toward equality and generosity

Often an offsetting factor allowing investors to justify investment in a loss-making enterprise

Green branding, heavy reliance on tax credits and

other incentives, “save the world” image

“Disruptive” business model, often with “Disruptive” business model, often with “Disruptive” business model, often with “Disruptive” business model, often with

reasoning opaque to all but a “visionary” leaderreasoning opaque to all but a “visionary” leaderreasoning opaque to all but a “visionary” leaderreasoning opaque to all but a “visionary” leader

A common theme is that old rules no longer apply; irregularities are written off as complexities

Vague plans to partner and achieve profitability at

scale anchored to Elon Musk

Rapid growth leading to collapse unless tightly Rapid growth leading to collapse unless tightly Rapid growth leading to collapse unless tightly Rapid growth leading to collapse unless tightly

monitored and regulatedmonitored and regulatedmonitored and regulatedmonitored and regulated

Uncontrolled growth in these scenarios is often the catalyst for failure—control is key to legitimacy

Increasing stakes and unrealistic investor expectations

on a highly speculative business

Source: Devonshire Research Group analysis and opinion; commentary from Elon Musk interviews and quarterly reports; limited information about deposit vaulting available; https://www.teslamotors.com/blog/secret-tesla-motors-master-plan-just-between-you-and-me

-Attorney Confidential-

While future-earning financing is often not malicious, delusional

ambition can be a different path to the same outcome

14

Unsustainable Sustainable

Large-scale

Small-scale

The The The The ffffutureutureutureuture----earning pyramidal financing landscapeearning pyramidal financing landscapeearning pyramidal financing landscapeearning pyramidal financing landscape

“Too big to fail”

Everyday fraud Acceptance of value loss

Massive fraud

� Masks fraud by mixing with

legitimate business activities

� Carefully balances growth and

risk to prolong scheme

� Escapes before scheme fully

collapses

� Vital, ubiquitous, and

nationalized public goods

� Operates outside the public

marketplace

� Limits accounting scrutiny

and speculative investment

� Targets unsophisticated /

vulnerable investors

� Encourages investor

“entrepreneurialism”

� Remains anonymous, then

vanishes

� Argues for non-financial value

proposition to offset loss

� Appeals to emotion and

instinct (branding, PR, etc.)

� Fails fast and acknowledges

limits to growth

Medium-scale

Many VC-backed startups

Aggressive-growth Unicorns

Giants poised to fail

Typical Ponzi, pyramid, and matrix schemes

Charities and public works

Delusional / Overambitious

Source: Devonshire Research Group analysis and opinion; commentary from Elon Musk interviews and quarterly reports

-Attorney Confidential-

While Tesla has bet the farm on extreme growth, insolvency is an

unacceptable fallback strategy for a publicly traded company

15

Sustainable

Large-scale

Small-scale

Notable pyramidal Notable pyramidal Notable pyramidal Notable pyramidal ffffinancing enterprisesinancing enterprisesinancing enterprisesinancing enterprises

Medium-scale

Enron

US Social Security

Fractional Reserve Banking

Televangelism

Peer to Peer & Crowd Funding

projects

Nigerian prince email scams

Multi-level marketing

Medicare

Madoff Ponzi scheme

Bitcoin Savings and Trust

Startup seed funding

WorldCom

Large charitiesRide Sharing

Shared Payment Systems

Unsustainable

Tesla MotorsTesla MotorsTesla MotorsTesla Motors

(Today)(Today)(Today)(Today)

Delusional / Overambitious

Source: Devonshire Research Group analysis and opinion; commentary from Elon Musk interviews and quarterly reports

-Attorney Confidential-

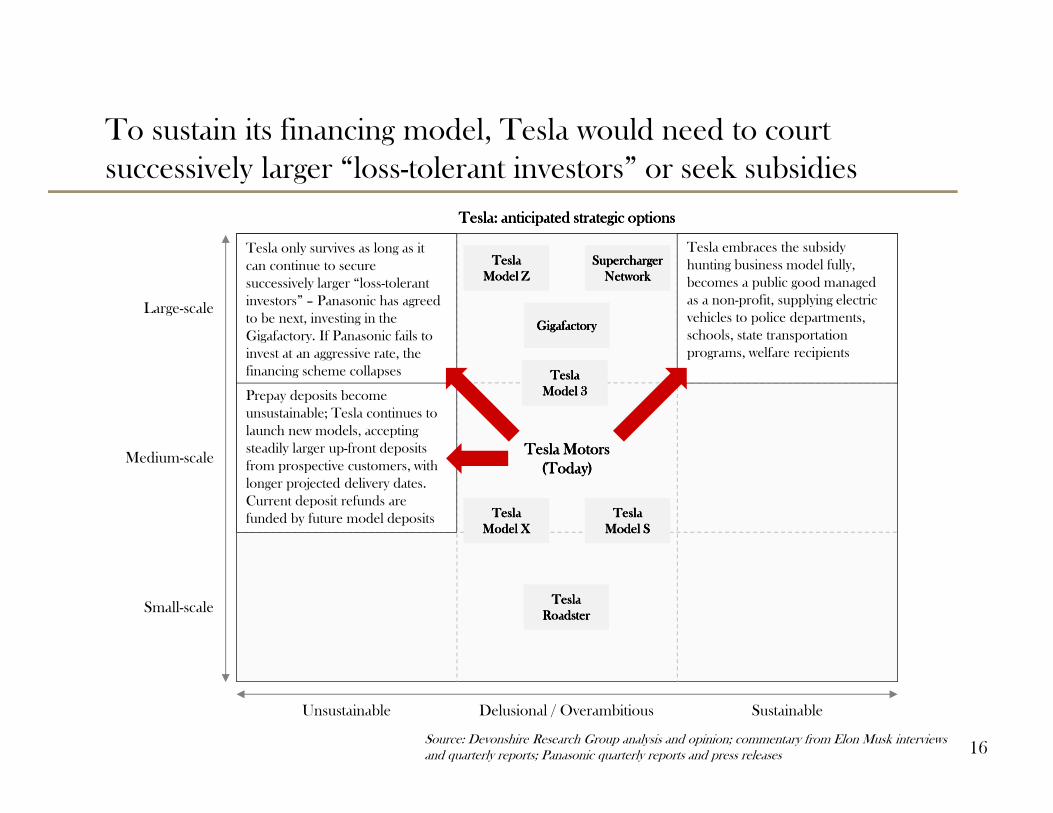

To sustain its financing model, Tesla would need to court

successively larger “loss-tolerant investors” or seek subsidies

16

Sustainable

Large-scale

Small-scale

Tesla: anticipated strategic optionsTesla: anticipated strategic optionsTesla: anticipated strategic optionsTesla: anticipated strategic options

Medium-scale

Tesla only survives as long as it

can continue to secure

successively larger “loss-tolerant

investors” – Panasonic has agreed

to be next, investing in the

Gigafactory. If Panasonic fails to

invest at an aggressive rate, the

financing scheme collapses

Tesla embraces the subsidy

hunting business model fully,

becomes a public good managed

as a non-profit, supplying electric

vehicles to police departments,

schools, state transportation

programs, welfare recipients

Prepay deposits become

unsustainable; Tesla continues to

launch new models, accepting

steadily larger up-front deposits

from prospective customers, with

longer projected delivery dates.

Current deposit refunds are

funded by future model deposits

Unsustainable

Tesla MotorsTesla MotorsTesla MotorsTesla Motors

(Today)(Today)(Today)(Today)

Tesla Tesla Tesla Tesla

Model XModel XModel XModel X

Tesla Tesla Tesla Tesla

Model XModel XModel XModel X

Tesla Tesla Tesla Tesla

RoadsterRoadsterRoadsterRoadster

Tesla Tesla Tesla Tesla

RoadsterRoadsterRoadsterRoadster

Tesla Tesla Tesla Tesla

Model SModel SModel SModel S

Tesla Tesla Tesla Tesla

Model SModel SModel SModel S

Tesla Tesla Tesla Tesla

Model ZModel ZModel ZModel Z

Tesla Tesla Tesla Tesla

Model ZModel ZModel ZModel Z

Supercharger Supercharger Supercharger Supercharger

NetworkNetworkNetworkNetwork

Supercharger Supercharger Supercharger Supercharger

NetworkNetworkNetworkNetwork

GigafactoryGigafactoryGigafactoryGigafactoryGigafactoryGigafactoryGigafactoryGigafactory

Tesla Tesla Tesla Tesla

Model 3Model 3Model 3Model 3

Tesla Tesla Tesla Tesla

Model 3Model 3Model 3Model 3

Delusional / Overambitious

Source: Devonshire Research Group analysis and opinion; commentary from Elon Musk interviews and quarterly reports; Panasonic quarterly reports and press releases

-Attorney Confidential-

Tesla is operationally vulnerable, too dependent on the success of the Model

3, and needs to prepare for the possibility of a future-earning death spiral

17

Our thesis is twofold: (1)(1)(1)(1) the likelihood of a successful Model 3 launch is low, and (2) (2) (2) (2) Tesla will be forced

to seek residual value as a heavily-subsidized (and decidedly non-luxury) public good provider

Our thesis is twofold: (1)(1)(1)(1) the likelihood of a successful Model 3 launch is low, and (2) (2) (2) (2) Tesla will be forced

to seek residual value as a heavily-subsidized (and decidedly non-luxury) public good provider

Adjustment needed

Become a public good org, exit the

public market, and reduce scrutiny;

possible government acquisition

This is the operating assumption; we believe the Model 3 will be late and will not be profitable

Aggressively court loss-tolerant

investors, and provide investors

with roadmap to profit

Growth outcome

Tesla escalates the

FEPF dynamic safely

and sustainably

Tesla escapes FEPF

dynamic with a wildly

successful Model 3

Tesla escalates

pyramidal financing

but mismanages risk

Tesla deposit system

converts to Ponzi

scheme

Historical precedent

Growth of the private pension and

old-age insurance market predating

the Social Security Act

IBM survives Great Depression

and claws back from death (due

largely to Social Security Act)

Enron and WorldCom started as

legitimate ambitious business

model innovators that went rogue

Some Ponzi schemes (e.g. Madoff)

were well-regarded and not

considered fraudulent at the time

Properly inform $1,000 deposit-

holders of their exceptionally risky

position as unsecured creditors

Likelihood

HighHighHighHigh

LowLowLowLow

LowLowLowLow

LowLowLowLow

Our thesis

Source: Devonshire Research Group analysis and opinion

-Attorney Confidential-

On the US auto industry’s impending competitive response to Tesla

18

Where's my gangstas and all my thugsThrow them hands up and show some loveAnd I Welcome you to Detroit CityI said Welcome to Detroit CityEvery place, everywhere we goMan we deep everywhere we rollAsk around and they all know TrickyThat's what's good man they all say Tricky

- Trick Trick, Welcome 2 Detroit

-Attorney Confidential-

Executive Summary

19

� How closely does TSLA’s financing model mirror the features of common Ponzi, Pyramid, and Matrix schemes?

− Numerous cautionary examples share features with TSLA, including hype driven by “visionary leaders”

− TSLA has accepted capital from unsophisticated investors with bold claims on return and/or product value

− If TSLA fails to deliver on these claims it has the potential to enter a death spiral

− Most common death spirals do not require malicious intent, but rather excessive (even delusional) ambition

� The profitability of the Model 3 depends on TSLA’s ability to squeeze its supply chain; this is a tall order

− Sophisticated suppliers (most notably Panasonic) will fight for their share of the profit

− Panasonic’s rechargeable battery division is constrained in terms of investment capacity and profit demands

− Current suppliers of numerous strategic, high-technology components have little IP and export to the US

− Many Chinese suppliers are vulnerable to patent infringement accusations and could face ITC injunctions

� TSLA’s use of tax credits disproportionately benefits the wealthy at the expense of the average taxpayer

− This inequality is a feature of the luxury-first market penetration strategy

− The election year introduces significant risk for TSLA’s continued reliance on taxpayer subsidies

-Attorney Confidential-

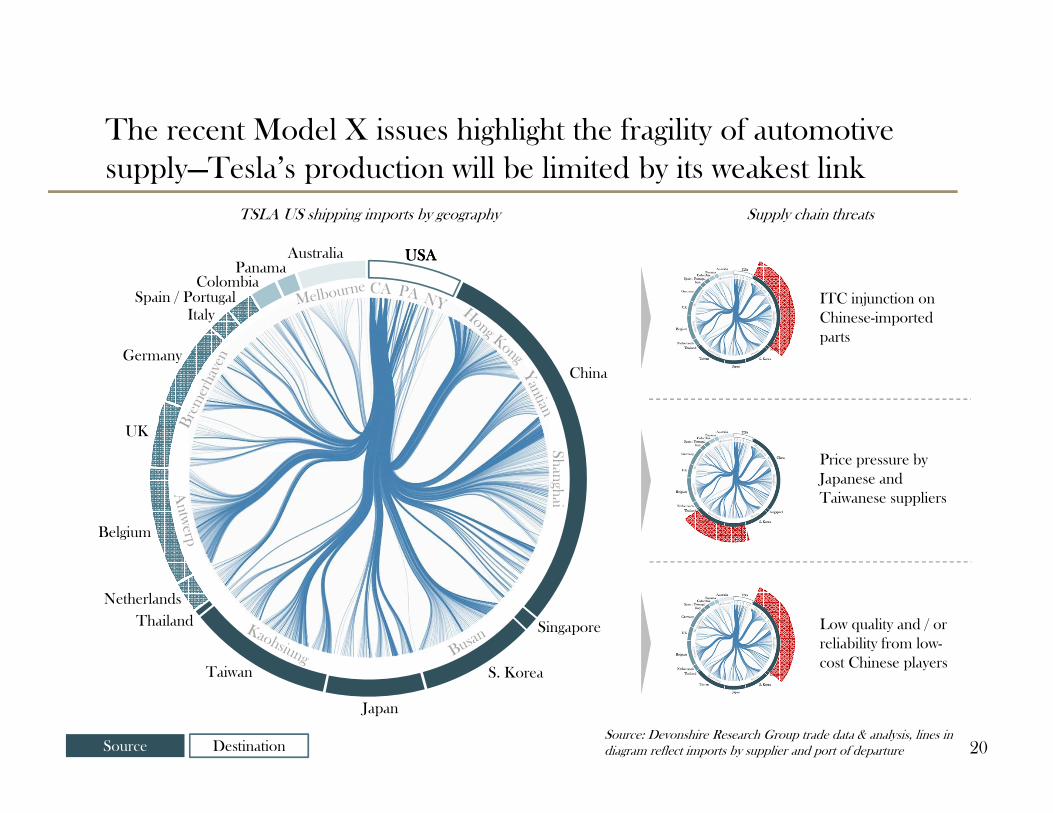

The recent Model X issues highlight the fragility of automotive

supply—Tesla’s production will be limited by its weakest link

20

USAUSAUSAUSA

China

S. Korea

Japan

Taiwan

Belgium

Netherlands

Thailand Singapore

UK

Germany

Italy

ColombiaPanama

Australia

Spain / Portugal

Sh

angh

ai

TSLA US shipping imports by geography Supply chain threats

ITC injunction on

Chinese-imported

parts

Price pressure by

Japanese and

Taiwanese suppliers

Low quality and / or

reliability from low-

cost Chinese players

Source: Devonshire Research Group trade data & analysis, lines in diagram reflect imports by supplier and port of departureDestinationSource

-Attorney Confidential-

The cost reduction needed to achieve a $35k Model 3 will

generate strain throughout the supply network

21

Cost bucketCost bucketCost bucketCost bucket Cost reductionCost reductionCost reductionCost reduction Achievable?Achievable?Achievable?Achievable? ObstaclesObstaclesObstaclesObstacles

Gross Profit 78% Likely Need offsetting sales volume, must maintain hype

Supercharger Allowance 0% Likely Will continue to build out infrastructure

Manufacturing Overhead 46% Maybe Need to realize economies of scale in production

Drivetrain 63% Unlikely Suppliers unlikely to accept price reductionSuppliers unlikely to accept price reductionSuppliers unlikely to accept price reductionSuppliers unlikely to accept price reduction

Battery Pack 65% Unlikely Requires discontinuity in battery pricing to achieveRequires discontinuity in battery pricing to achieveRequires discontinuity in battery pricing to achieveRequires discontinuity in battery pricing to achieve

Interior 43% Unlikely Suppliers unlikely to accept price reductionSuppliers unlikely to accept price reductionSuppliers unlikely to accept price reductionSuppliers unlikely to accept price reduction

Systems 0% Maybe More sensors, larger feature set expected for Model 3More sensors, larger feature set expected for Model 3More sensors, larger feature set expected for Model 3More sensors, larger feature set expected for Model 3

Tires, Brakes and Suspension 40% Unlikely Suppliers unlikely to accept price reductionSuppliers unlikely to accept price reductionSuppliers unlikely to accept price reductionSuppliers unlikely to accept price reduction

Body & Final Assembly 3% Maybe Depends on aluminum content and other design factors

( Model 3 model unit cost ) / ( Model S model unit cost )

Source: Estimates based on existing optimistic cost analyses

-Attorney Confidential-

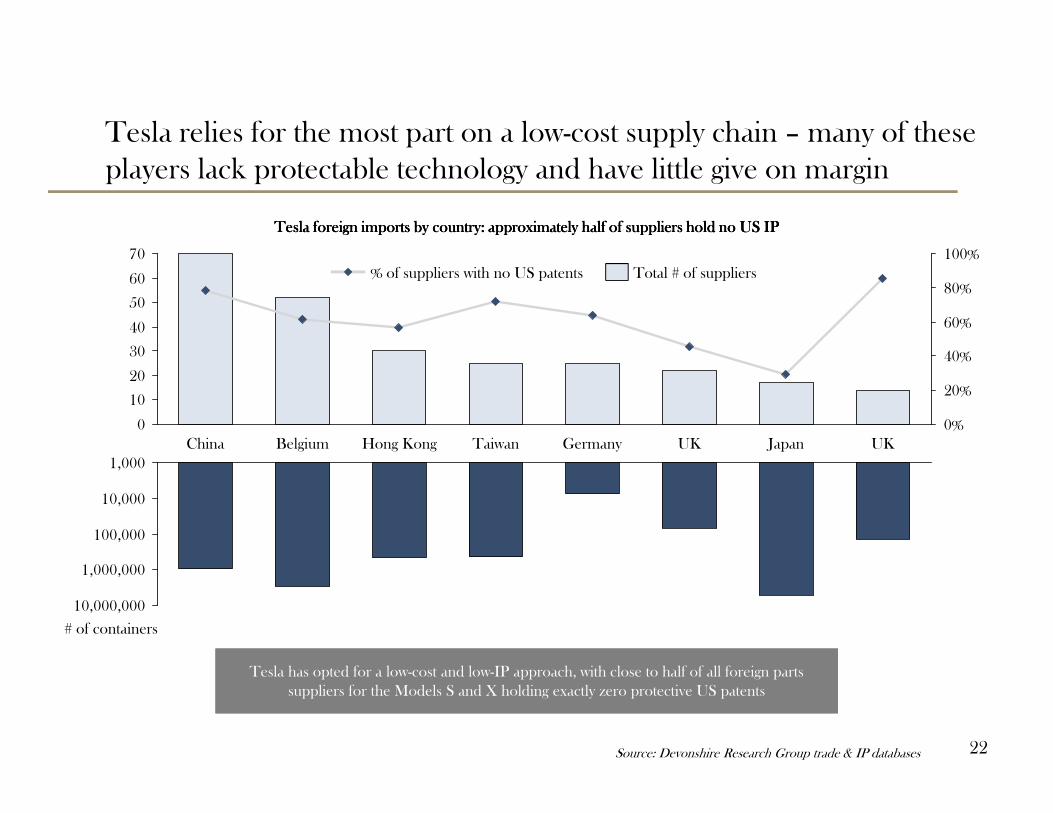

Tesla relies for the most part on a low-cost supply chain – many of these

players lack protectable technology and have little give on margin

22

0

10

20

30

40

50

60

70

40%

100%

80%

60%

20%

0%

UKJapanUKGermanyTaiwanHong KongBelgiumChina

Total # of suppliers% of suppliers with no US patents

Tesla foreign imports by country: approximately half of suppliers hold no US IPTesla foreign imports by country: approximately half of suppliers hold no US IPTesla foreign imports by country: approximately half of suppliers hold no US IPTesla foreign imports by country: approximately half of suppliers hold no US IP

Source: Devonshire Research Group trade & IP databases

1,000

10,000

100,000

1,000,000

10,000,000

# of containers

Tesla has opted for a low-cost and low-IP approach, with close to half of all foreign parts

suppliers for the Models S and X holding exactly zero protective US patents

Tesla has opted for a low-cost and low-IP approach, with close to half of all foreign parts

suppliers for the Models S and X holding exactly zero protective US patents

-Attorney Confidential-

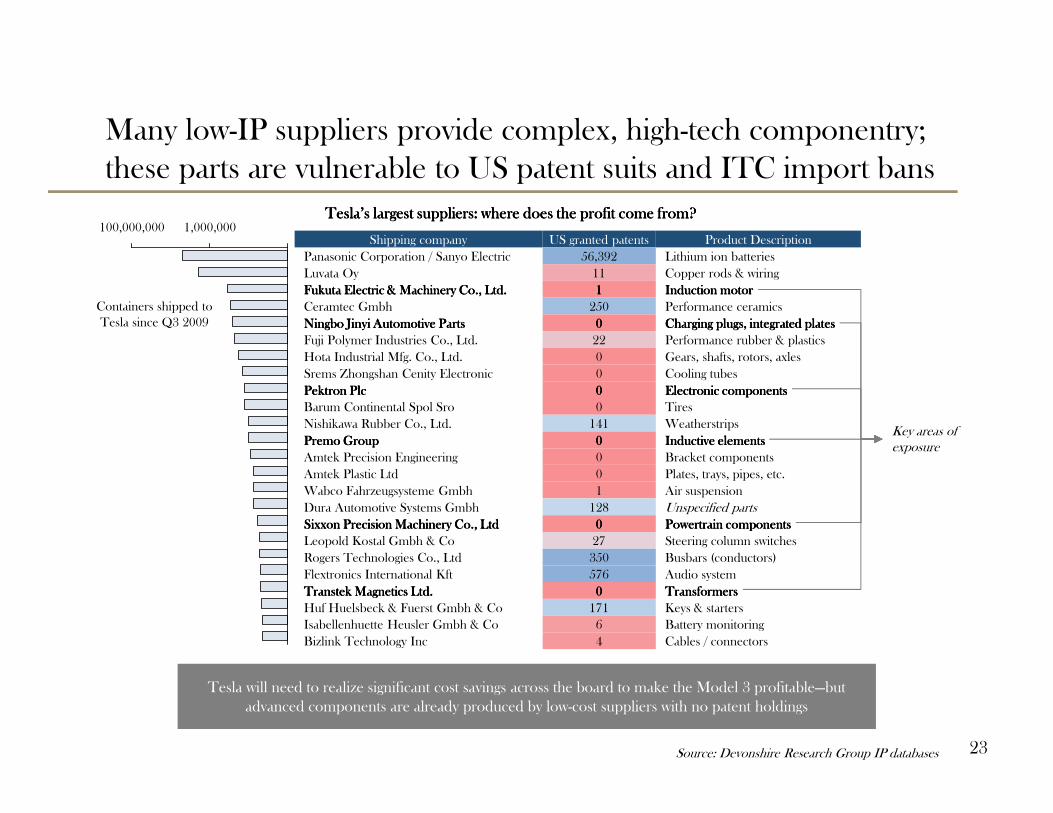

Shipping company US granted patents Product Description

Panasonic Corporation / Sanyo Electric 56,392 Lithium ion batteries

Luvata Oy 11 Copper rods & wiring

Fukuta Electric & Machinery Co., Ltd.Fukuta Electric & Machinery Co., Ltd.Fukuta Electric & Machinery Co., Ltd.Fukuta Electric & Machinery Co., Ltd. 1111 Induction motorInduction motorInduction motorInduction motor

Ceramtec Gmbh 250 Performance ceramics

Ningbo Jinyi Automotive PartsNingbo Jinyi Automotive PartsNingbo Jinyi Automotive PartsNingbo Jinyi Automotive Parts 0000 Charging plugs, integrated platesCharging plugs, integrated platesCharging plugs, integrated platesCharging plugs, integrated plates

Fuji Polymer Industries Co., Ltd. 22 Performance rubber & plastics

Hota Industrial Mfg. Co., Ltd. 0 Gears, shafts, rotors, axles

Srems Zhongshan Cenity Electronic 0 Cooling tubes

Pektron PlcPektron PlcPektron PlcPektron Plc 0000 ElectronicElectronicElectronicElectronic componentscomponentscomponentscomponents

Barum Continental Spol Sro 0 Tires

Nishikawa Rubber Co., Ltd. 141 Weatherstrips

Premo GroupPremo GroupPremo GroupPremo Group 0000 Inductive elementsInductive elementsInductive elementsInductive elements

Amtek Precision Engineering 0 Bracket components

Amtek Plastic Ltd 0 Plates, trays, pipes, etc.

Wabco Fahrzeugsysteme Gmbh 1 Air suspension

Dura Automotive Systems Gmbh 128 Unspecified parts

SixxonSixxonSixxonSixxon Precision Machinery Co., LtdPrecision Machinery Co., LtdPrecision Machinery Co., LtdPrecision Machinery Co., Ltd 0000 Powertrain componentsPowertrain componentsPowertrain componentsPowertrain components

Leopold Kostal Gmbh & Co 27 Steering column switches

Rogers Technologies Co., Ltd 350 Busbars (conductors)

Flextronics International Kft 576 Audio system

Transtek Magnetics Ltd.Transtek Magnetics Ltd.Transtek Magnetics Ltd.Transtek Magnetics Ltd. 0000 TransformersTransformersTransformersTransformers

Huf Huelsbeck & Fuerst Gmbh & Co 171 Keys & starters

Isabellenhuette Heusler Gmbh & Co 6 Battery monitoring

Bizlink Technology Inc 4 Cables / connectors

Many low-IP suppliers provide complex, high-tech componentry;

these parts are vulnerable to US patent suits and ITC import bans

23

Tesla’s largest suppliers: where does the profit come from?Tesla’s largest suppliers: where does the profit come from?Tesla’s largest suppliers: where does the profit come from?Tesla’s largest suppliers: where does the profit come from?

Tesla will need to realize significant cost savings across the board to make the Model 3 profitable—but

advanced components are already produced by low-cost suppliers with no patent holdings

Tesla will need to realize significant cost savings across the board to make the Model 3 profitable—but

advanced components are already produced by low-cost suppliers with no patent holdings

1,000,000100,000,000

Containers shipped to

Tesla since Q3 2009

Key areas of exposure

Source: Devonshire Research Group IP databases

-Attorney Confidential-

The suppliers who do own IP are not loss-tolerant and will not

budge on margins for a relatively small purchaser such as Tesla

24

1

10

100

1,000

10,000

100,000

1 10 100 1,000 10,000 100,000 1,000,000 10,000,000

US patents granted

to supplier

Containers shipped

to Tesla since Q3 ’09

Toyota Motor Corporation

Samsung Sdi Co., Ltd

Panasonic Corporation

Nishikawa Rubber Co., Ltd.

Luvata Pori Oy

LG Electronics Inc

LG Chem Ltd.Kobe Steel, Ltd.

Hongfujin Precision

Fukuta Electric & Machinery Co., Ltd

Fuji Polymer Industries Co.

Foxconn Computer

Flextronics International Kft

Ceramtec Gmbh

International Tesla Suppliers with At Least One US Granted PatentInternational Tesla Suppliers with At Least One US Granted PatentInternational Tesla Suppliers with At Least One US Granted PatentInternational Tesla Suppliers with At Least One US Granted Patent

Belgium

Italy

China

Australia

Germany

Singapore

Japan

Panama

United Kingdom

Hong Kong

Taiwan

South Korea

Country of Origin

Source: Devonshire Research Group trade & IP databases

-Attorney Confidential-

Panasonic will face organizational pressure to abandon the Tesla

partnership if its Gigafactory investment does not pay dividends

25Source: Panasonic Annual Report 2015

The automotive segment is the smallest segment at Panasonic, and EV battery sales are just one component of this revenue stream

The Gigafactory investment alone accounts for nearly three years of automotive capital expenditure—this is a hugely outsized segment investment

$1.6 B

$616 MM

2015 automotive

capital investment

Capital pledged

to Gigafactory

2.6x2.6x2.6x2.6x

Housing

26%

Devices

B2B 25%

AutomotiveAutomotiveAutomotiveAutomotive

Consumer

electronics

17%

17%

16%

45%Comfort

BatteriesBatteriesBatteriesBatteries

Safety

Chargers

28%

23%

Panasonic sales breakdown

Batteries are $3.5B of $72B total revenue

-Attorney Confidential-

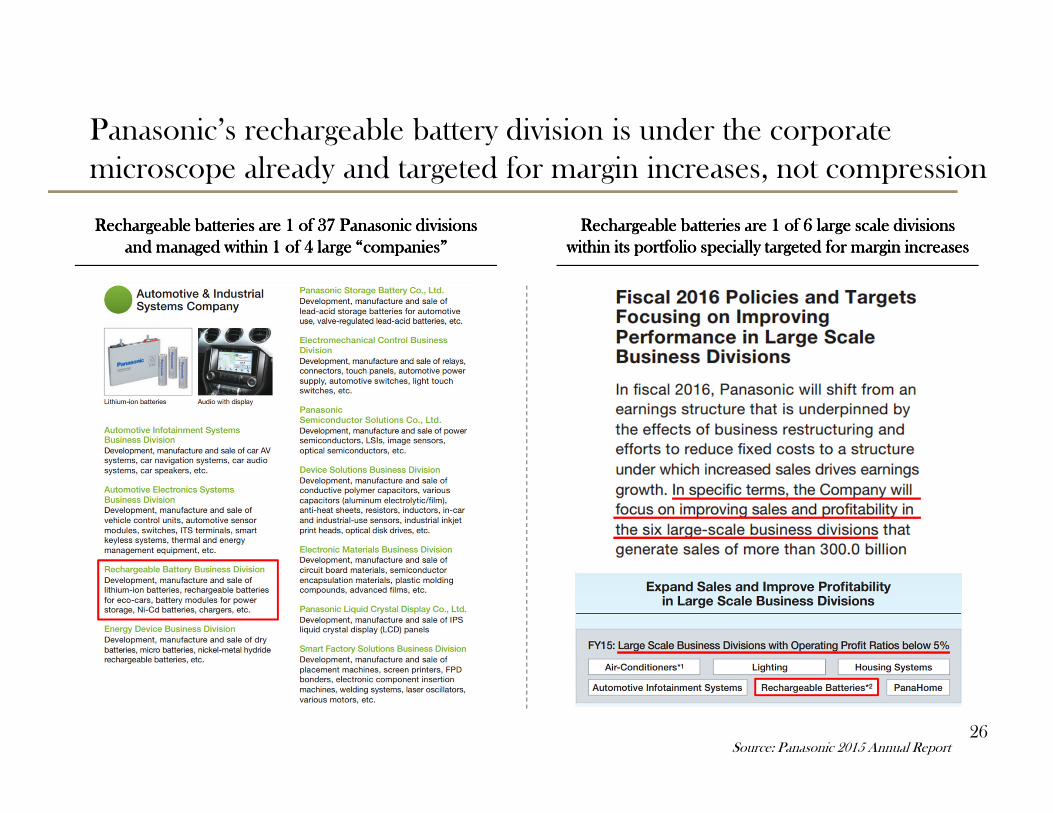

Panasonic’s rechargeable battery division is under the corporate

microscope already and targeted for margin increases, not compression

26Source: Panasonic 2015 Annual Report

Rechargeable batteries are 1 of 37 Panasonic divisions Rechargeable batteries are 1 of 37 Panasonic divisions Rechargeable batteries are 1 of 37 Panasonic divisions Rechargeable batteries are 1 of 37 Panasonic divisions

and managed within 1 of 4 large “companies”and managed within 1 of 4 large “companies”and managed within 1 of 4 large “companies”and managed within 1 of 4 large “companies”

Rechargeable batteries are 1 of 6 large scale divisions Rechargeable batteries are 1 of 6 large scale divisions Rechargeable batteries are 1 of 6 large scale divisions Rechargeable batteries are 1 of 6 large scale divisions

wwwwithin its portfolio specially targeted for margin increasesithin its portfolio specially targeted for margin increasesithin its portfolio specially targeted for margin increasesithin its portfolio specially targeted for margin increases

-Attorney Confidential-

Tesla needs a miracle in battery pricing to achieve the Model 3

target price; there is real doubt the Gigafactory will deliver

27Source: Rapidly falling costs of battery packs for electric vehicles, Nature Climate Change, 3/23/15

Data fit gives 8% annual cost reduction by leading manufacturers, suggesting Tesla will not hit

$150 / kWh until 2020—well past the promised end-of-2017 Model 3 delivery date

Data fit gives 8% annual cost reduction by leading manufacturers, suggesting Tesla will not hit

$150 / kWh until 2020—well past the promised end-of-2017 Model 3 delivery date

100

1,000

201620152008 2009 2010 2011 2012 2013 2014

$ / kWh (log scale)Model S battery pack cost estimatesModel S battery pack cost estimatesModel S battery pack cost estimatesModel S battery pack cost estimates

Generally-accepted critical pack price

Zero-margin raw material cost floor

200

400

800

150

114

$190 / kWh claimed by Tesla head of IR, 04/16

-Attorney Confidential-

Executive Summary

28

� How closely does TSLA’s financing model mirror the features of common Ponzi, Pyramid, and Matrix schemes?

− Numerous cautionary examples share features with TSLA, including hype driven by “visionary leaders”

− TSLA has accepted capital from unsophisticated investors with bold claims on return and/or product value

− If TSLA fails to deliver on these claims it has the potential to enter a death spiral

− Most common death spirals do not require malicious intent, but rather excessive (even delusional) ambition

� The profitability of the Model 3 depends on TSLA’s ability to squeeze its supply chain; this is a tall order

− Sophisticated suppliers (most notably Panasonic) will fight for their share of the profit

− Panasonic’s rechargeable battery division is constrained in terms of investment capacity and profit demands

− Current suppliers of numerous strategic, high-technology components have little IP and export to the US

− Many Chinese suppliers are vulnerable to patent infringement accusations and could face ITC injunctions

� TSLA’s use of tax credits disproportionately benefits the wealthy at the expense of the average taxpayer

− This inequality is a feature of the luxury-first market penetration strategy

− The election year introduces significant risk for TSLA’s continued reliance on taxpayer subsidies

-Attorney Confidential-

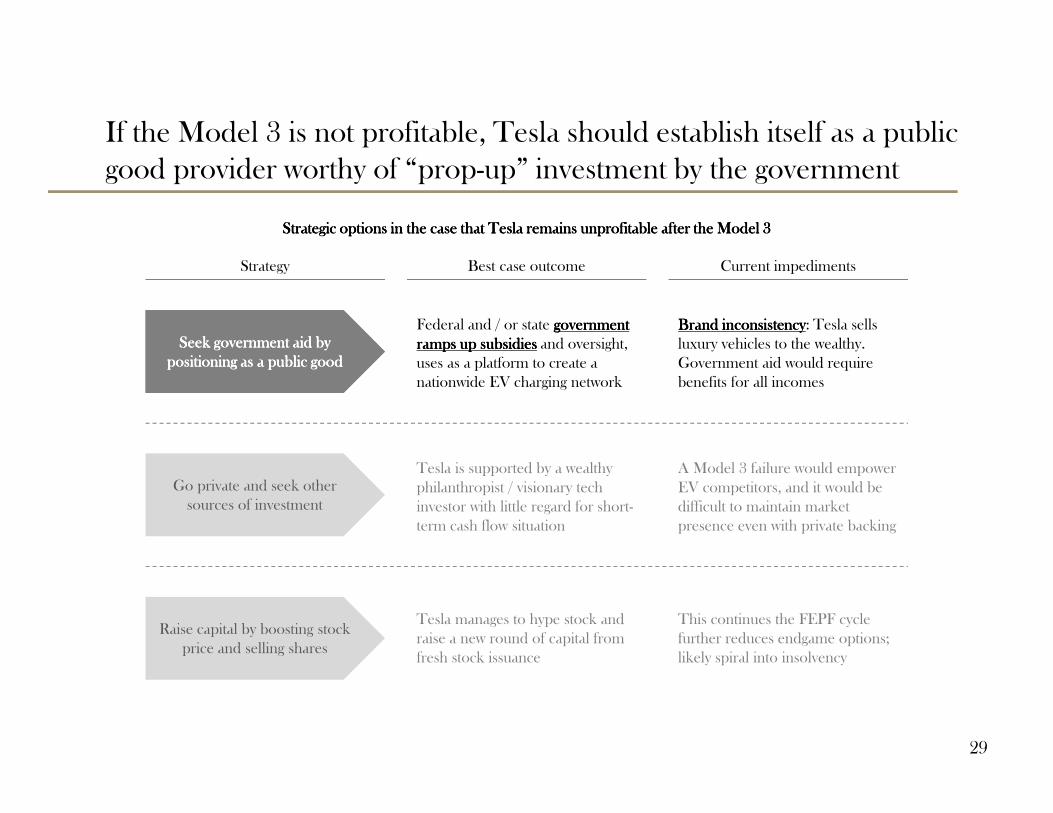

If the Model 3 is not profitable, Tesla should establish itself as a public

good provider worthy of “prop-up” investment by the government

29

Strategic options in the case that Tesla remains unprofitable after the Model 3Strategic options in the case that Tesla remains unprofitable after the Model 3Strategic options in the case that Tesla remains unprofitable after the Model 3Strategic options in the case that Tesla remains unprofitable after the Model 3

Seek government aid by Seek government aid by Seek government aid by Seek government aid by

positioning as a public goodpositioning as a public goodpositioning as a public goodpositioning as a public good

Seek government aid by Seek government aid by Seek government aid by Seek government aid by

positioning as a public goodpositioning as a public goodpositioning as a public goodpositioning as a public good

Go private and seek other

sources of investment

Raise capital by boosting stock

price and selling shares

Best case outcome Current impedimentsStrategy

Federal and / or state government government government government

ramps up subsidiesramps up subsidiesramps up subsidiesramps up subsidies and oversight,

uses as a platform to create a

nationwide EV charging network

Tesla is supported by a wealthy

philanthropist / visionary tech

investor with little regard for short-

term cash flow situation

Tesla manages to hype stock and

raise a new round of capital from

fresh stock issuance

A Model 3 failure would empower

EV competitors, and it would be

difficult to maintain market

presence even with private backing

This continues the FEPF cycle

further reduces endgame options;

likely spiral into insolvency

Brand inconsistencyBrand inconsistencyBrand inconsistencyBrand inconsistency: Tesla sells

luxury vehicles to the wealthy.

Government aid would require

benefits for all incomes

-Attorney Confidential-

EV tax credits overwhelmingly favor the wealthy; the average

taxpaying citizen will realize little, if any benefit

30Source: “The Distributional Effects of U.S. Clean Energy Tax Credits”, UC Berkeley, July 2015, data collected from 2009-2012

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0

Tax credits

Adjusted gross income (AGI)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

20-4010-20 >200<10 40-75 75-200

Average EV credit per tax return, by AGIAverage EV credit per tax return, by AGIAverage EV credit per tax return, by AGIAverage EV credit per tax return, by AGIWealth inequality of EV tax creditsWealth inequality of EV tax creditsWealth inequality of EV tax creditsWealth inequality of EV tax credits

Adjusted gross income, thousand USDCumulative taxpayer fraction, ranked by AGI

Cu

mu

lative

fra

ctio

n o

f ta

x cr

edits

/ A

GI

US

D p

er tax

ret

urn

Would any current US Presidential candidate risk extending nation-wide EV credits if this story

of inequality were to be shared with the average voter?

Would any current US Presidential candidate risk extending nation-wide EV credits if this story

of inequality were to be shared with the average voter?

-Attorney Confidential-

Tesla is contributing to this inequality, as it is exhausting its tax

credits on the luxury Models S and X

31

100

1,000

10,000

100,000

1,000,000

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000

Fiat 500e BMW i3

Nissan Leaf

Chevrolet Volt Tesla Model S

Chevrolet Spark EV

Base price

Ford Focus Electric

Kia Soul EV

Volkswagen e-Golf

Cadillac ELR

Tesla Model X

Mercedes-Benz B-Class EVMitsubishi i-MiEV

Smart Fortwo EV

Units sold

(through 12/15) Vehicles qualifying for full $7,500 federal EV tax creditVehicles qualifying for full $7,500 federal EV tax creditVehicles qualifying for full $7,500 federal EV tax creditVehicles qualifying for full $7,500 federal EV tax credit

Source: Edmunds.com, Devonshire analysis

-Attorney Confidential-

In 2013, the average Tesla owner had twice the household income

of other EV owners

32

“While the field of electric vehicles (EVs) has grown with the

Chevrolet Volt, Nissan Leaf and the Toyota Prius Plug-In, Tesla

buyers display unique differences. NVES shows that Tesla NVES shows that Tesla NVES shows that Tesla NVES shows that Tesla

owners have double the average household income of other EV owners have double the average household income of other EV owners have double the average household income of other EV owners have double the average household income of other EV

owners ($293,200)owners ($293,200)owners ($293,200)owners ($293,200). As a result, they are more likely to be adding

a Tesla to their household fleet (51%) rather than replacing a

vehicle with its purchase.”

- Strategic Vision: New Vehicle Experience Survey (2013)

-Attorney Confidential-

Tesla relies heavily on manufacturing incentives and zero-

emissions credits

33

Tesla is built on loss-tolerant public money, but this will not be a solution in perpetuity. Eventually

Tesla will need to stand on its own or accept a role as a government-sponsored public good provider

Tesla is built on loss-tolerant public money, but this will not be a solution in perpetuity. Eventually

Tesla will need to stand on its own or accept a role as a government-sponsored public good provider

SubsidySubsidySubsidySubsidy Subsidy sizeSubsidy sizeSubsidy sizeSubsidy size SourceSourceSourceSource

Gigafactory incentives $1,290 MM Nevada taxpayers

Zero-emission credits $518 MM California taxpayers

Federal EV tax credits $284 MM Federal taxpayers

CA self-generation incentive $126 MM California taxpayers

CA Alternative Energy Financing $90 MM California taxpayers

Discounted DoE loan $45 MM Federal taxpayers

State EV tax credits $38 MM California taxpayers

Source: LA Times investigation, June 2015

-Attorney Confidential-

Brand exposure: pandering to the wealthy is incompatible with the

concept of Tesla as a public good

34

Brand drivers

Modern feature setModern feature set

Quality engineeringQuality engineering

High-performance vehiclesHigh-performance vehicles

LuxuryLuxury

--

--

Issues with Model X

Disrupting auto industryDisrupting auto industry

Leading technologyLeading technology

Eventually affordableEventually affordable

VisionaryVisionary

--

Limited technology ownership

To be determined

Developing EV infrastructureDeveloping EV infrastructure

Lowering emissionsLowering emissions

Government endorsementGovernment endorsement

GreenGreen

--

Surprisingly high environmental cost

Hurts average taxpaying citizen

Brand inconsistencies

Supporters say Tesla is saving the world. We believe the reality is that Tesla helps rich people buy cars.

This brand inconsistency is a key vulnerability going into a contentious US presidential election year; is

inequality a core feature of the Tesla brand?

Supporters say Tesla is saving the world. We believe the reality is that Tesla helps rich people buy cars.

This brand inconsistency is a key vulnerability going into a contentious US presidential election year; is

inequality a core feature of the Tesla brand?

-Attorney Confidential-

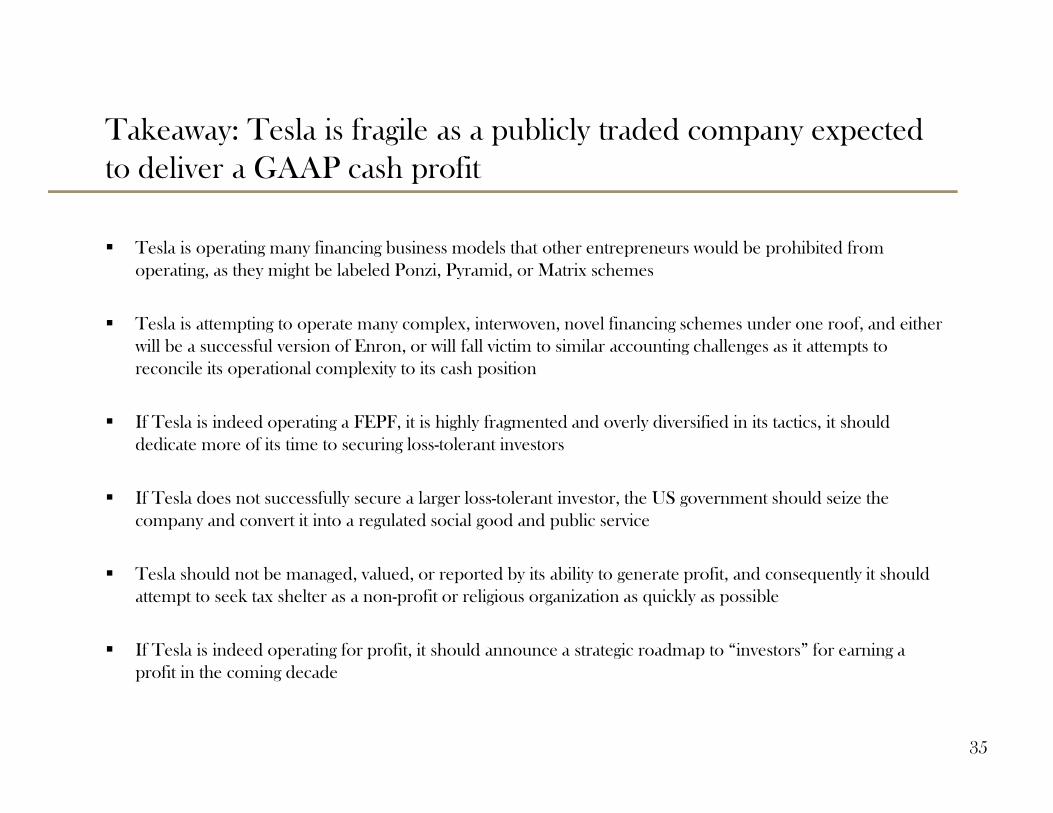

Takeaway: Tesla is fragile as a publicly traded company expected

to deliver a GAAP cash profit

� Tesla is operating many financing business models that other entrepreneurs would be prohibited from

operating, as they might be labeled Ponzi, Pyramid, or Matrix schemes

� Tesla is attempting to operate many complex, interwoven, novel financing schemes under one roof, and either

will be a successful version of Enron, or will fall victim to similar accounting challenges as it attempts to

reconcile its operational complexity to its cash position

� If Tesla is indeed operating a FEPF, it is highly fragmented and overly diversified in its tactics, it should

dedicate more of its time to securing loss-tolerant investors

� If Tesla does not successfully secure a larger loss-tolerant investor, the US government should seize the

company and convert it into a regulated social good and public service

� Tesla should not be managed, valued, or reported by its ability to generate profit, and consequently it should

attempt to seek tax shelter as a non-profit or religious organization as quickly as possible

� If Tesla is indeed operating for profit, it should announce a strategic roadmap to “investors” for earning a

profit in the coming decade

35

-Attorney Confidential-

On requisite skepticism over hyperbolic operating targets

36

But now they only block the sunThey rain and snow on everyoneSo many things I would have doneBut clouds got in my way

I've looked at clouds from both sides nowFrom up and down, and still somehowIt's cloud illusions I recallI really don't know clouds at all

- Joni Mitchell, Both Sides Now

-Attorney Confidential-

37

Thank you

For more information, please contact Devonshire Research Group, LLC at [email protected]

Image © 2016 Devonshire Research Group