determining the self sufficiency of microfinance … determining the self sufficiency of...

TRANSCRIPT

Determining the Self Sufficiency of Microfinance Institutions

by

Jacob Yaron and Ronny Manos

Yaron: School of Business, College of Management

Manos: School of Business, College of Management

Correspondence to:

Ronny Manos: School of Business, College of Management, Israel. Tel/Fax: +972 (0)3

6438753; E-mail: [email protected]

January 2007

Published: Yaron, J. and Manos, R., (2007), ‘Determining the Self Sufficiency of

Microfinance Institutions, Savings & Development, No. 2, pp 131-160

2

Determining the Self Sufficiency of Microfinance Institutions

ABSTRACT

The paper compares and discusses two commonly used methods to evaluate and measure self-

sufficiency of microfinance institutions (MFIs), namely subsidy dependence index (SDI) and

financial self sufficiency (FSS). Both the SDI and the FSS are used by the microfinance

industry as substitutes for a complete cost-benefit analysis, which demands specialised

resources and sophisticated financial methods and is therefore rarely applied. In contrast, the

SDI and FSS do not provide a complete cost–benefit analysis of the performance of MFIs.

However, they attempt to provide sufficiently meaningful performance evaluation measures

that allow society and donors, who often bear the cost of subsidising MFIs, to assess

performance. In particular the SDI and FSS evaluation methods allow comparisons to be

made among MFIs that serve similar target clientele and provide similar services. The paper

focuses on the differences between the SDI and the FSS and concludes that the latter often

underestimates the subsidy-dependence of the MFI (overestimates self-sufficiency). This

deficiency is due to inherent characteristics of the FSS methodology which the paper

elaborates on. The paper also suggests the utilization of an outreach index (OI) that should

reflect social objectives and priorities in allocating scarce public funds in supporting MFIs.

Relying on traditional financial ratios, such as return on assets (ROA) and return on equity

(ROE), is a futile practice in assessing the performance of MFIs, unless costs and income are

properly adjusted to reflect subsidies. When costs and income are not adjusted to reflect

subsidies, relying on traditional financial ratios, could often lead to meaningless or even

misleading performance assessment.

JEL Classification: G21, I38, O16

Keywords: Micro Finance Institution; Subsidy Dependence Index; Financial Self

Sufficiency; Outreach Index

3

Acronyms

CD Certificate of Deposits

CGAP Consultative Group to Assist the Poor

DCF Discounted Cash Flow

EVA Economic Value Added

FI Financial Institution

FSS Financial Self Sufficiency

IFS International Financial Statistics

MBB The MicroBanking Bulletin

MFI Micro Finance Institution

MIX Microfinance Information eXchange

OI Outreach Index

LP outstanding Loan Portfolio

ROA Return On Assets

ROE Return On Equity

RR Reserve requirements

SDFI State-owned Development Finance Institution

SDI Subsidy Dependence Index

4

1. Introduction

The microfinance industry has experienced fundamental changes since its inception in the late

1970s. From an industry dependent upon grants and subsidies, driven by political incentives,

and justified by social values, the underlining view has evolved to realise that providing

financial services to low income and poor people can be a viable business. As an example, in

the past, many governments- motivated by social views - used to cap interest rates charged on

loans to poor people. More recently, however, many policy makers have realised that capping

interest reduces the supply of loans, and results in misallocation of resources and the seizing

of big parts of subsidies embedded in concessionary loans by the relatively well to do and

influential clientele. As this practice clearly harms development, governments’ attitude

towards capping of interest rates has changed. Moreover, although most microfinance

institutions (MFIs) normally require financial assistance during earlier years, it has been

realised that to secure sustainability, to improve efficiency and to ensure ability to meet

growing demand for capital, the MFI - as it matures - must strive to become self sustainable1.

As a result, there has been a move away from State-owned Development Finance Institutions

(SDFIs) – previously dominant in many developing countries and considered the vehicle

through which social goals could be reached and priority sectors supported - towards more

diversified ownership of institutions. Indeed, SDFIs were frequently riddled with

inefficiencies and often benefited primarily the relatively rich clients at the expense of poor

people. In contrast, many of the newly emerging MFIs adopt a more economically-oriented

approach that includes sourcing finance by making and retaining earnings, attracting deposits,

increasingly borrowing from commercial sources at market rates, and tightening loan

recovery procedures to minimise bad debt. Furthermore, many commercial banks, which in

the past did not consider poor people as potential clients, now set up microfinance centres that

aim to create value by providing financial services specifically to low income households and

poor people in developing countries.

The evolution of MFIs from subsidy-based into profitable businesses has led to an increasing

number of MFIs and other entities which report and analyse the performance of MFIs, and

track MFIs’ performance progression over time. This phenomenon has highlighted the

absence of adequate assessment criteria. Indeed, in the past, poorly applied performance

indicators were relied upon to justify continuation and augmentation of SDFIs’ operations and

subsidization thereof. While indicators such as the number of people financed and amounts

lent, were applied, information was lacking on SDFIs’ losses, on their enormous arrears, on

political interventions in resource allocation, on dependence on subsidies and on ill-targeting

of clientele.

The political economy associated with concessionary lending granted to SDFIs and MFIs had

a great influence on the performance of these institutions, on their lending policies and on the

performance evaluation methods used to justify their existence. Once governments and

institutions started to understand the importance of building sustainable MFIs, initiatives to

develop well founded performance assessment criteria were embarked upon. These criteria

have since become widely-used by the MFI industry.

When endeavouring to measure the performance of MFIs there are a number of unique

features of this type of organisation that need to be considered. For example, although there

1 For example, an article titled ‘The Hidden Wealth of the Poor’ which was published in the Economist of

November 5, 2005 tells the story of the PT Bank Dagang Bali of Indonesia, which was closed in 2004 due to

fraud and insolvency. The bank used to serve poor people, many of which lost their savings as a result of the

closure.

5

may be demand by poor people for financial services, the cost of advancing many micro loans

is substantially higher than advancing a small number of bigger loans of the same overall loan

portfolio. Poor repayment rates and the impact of high inflation, which often characterise

developing countries, should also be considered. The hidden costs of grants, subsidies and

technical aid received by the MFI must likewise be properly measured. In addition, relief

from reserve requirements (RR), access to concessionary interest rates and return on equity

which is either negative or below the opportunity cost of equity capital are also unique to

many MFIs. These should not be ignored when MFI performance is measured.

Notwithstanding the difficulties involved, properly measuring the performance of MFIs may

yield some important benefits. First, measuring performance should help in transforming a

once subsidy-based industry into a profitable and sustainable one. Second, measuring

performance should make the MFI industry more attractive to private suppliers of capital thus

increasing access to sustainable sources of funds. Third, measuring performance enhances

efficiency and highlights efficient MFIs which are better positioned to achieve goals and

improve access of target clientele to a wide range of financial services. Overall, measuring

and tracking MFI performance should help to channel funds to the most efficient institutions,

thus supporting economic growth and poverty reduction.

Moreover, measuring performance is essential even for evaluating the performance of MFIs

that serve the extreme poor and have no desire or plans to become self sustainable. This is

because there are alternative ways to reach and benefit the target clientele. Measuring the

performance of MFIs should enlighten those that foot the bill of subsidies, on the cost-

effectiveness of this instrument in supporting the target clientele.

The aim of this study is to assess various performance evaluation measures that are commonly

used by the MFI industry. Section 2 reviews traditional performance measures and highlights

their shortcomings in measuring the performance of MFIs. Section 3 reviews the financial

self sufficiency index (FSS) while section 4 is devoted to the subsidy dependence index (SDI)

and to the outreach index (OI). Section 5 compares the FSS and SDI measures both

theoretically and by numerical illustrations. Section 6 concludes. It is noted at the outset that

self-sufficiency is alternatively referred to as subsidy independence or self sustainability, and

these terms are used interchangeably throughout the paper.

2. Traditional Accounting Measures of Performance

Typically upon inception - and often for many years after - MFIs rely upon scarce public

funds in the form of subsidies. Moreover, many MFIs maintain their operations on the basis

that they would receive continued subsidies indefinitely. Under these circumstances,

traditional financial ratios that are based on accounting data, unadjusted for subsidies, are

clearly inadequate to measure MFI performance. Although these traditional performance

measures may be suitable for evaluating for-profit organizations, in the case of MFIs they

provide at best a partial but often a misleading picture of performance.

Figure 1 illustrates the futility of relying on traditional financial ratios - the return on assets

(ROA) and the return on equity (ROE) - in evaluating the performance of MFIs. The

performance indicated by these two financial ratios may reflect the “true” financial outcome

of a for-profit organization that operates under commercial constraints in a competitive

market place. However, the performance of the MFI, as indicated by the unadjusted ROA and

ROE, reflects the administrative decision on the (subsidized) cost of borrowed funds. In other

words, the ROA and ROE are the residual value of the subsidies received by the MFI: they

are dependent variables disguised as independent ones.

6

Figure 1: The effect on ROA and ROE of the administrative decision on the rate of

interest paid by the MFI on its borrowed funds.

-150%

-100%

-50%

0%

50%

100%

150%

200%

0%

2%

4%

6%

8%

10

%

12

%

14

%

16

%

18

%

20

%

22

%

24

%

26

%

28

%

30

%

Interest Rate Paid by MFI on its Borrowed Funds

RO

E

-15%

-10%

-5%

0%

5%

10%

15%

20%

RO

A

Key assumptions: Equity equals 10 percent of total assets; The average annual yield obtained

on total assets is 20 percent; Administrative expenses are 6 percent of total assets.

The failure of the ROA and ROE in measuring the performance of MFIs is due to their

reliance on accounting practices that ignore the subsidies received by MFIs. Without properly

reporting and evaluating the subsidies involved, no adequate cost-benefit analysis or cost-

effectiveness analysis of the MFI can be carried out.

Furthermore, the traditional accounting measures ignore the opportunity cost of capital

employed. O’Brien (2006) suggests that in the face of the commercialization of the

microfinance industry, MFIs should adopt the valuation method used by the for-profit sector,

the discounted cash flow (DCF) method. The advantage of the DCF method over traditional

accounting measures is that it recognizes and focuses on the opportunity cost of capital.

However, as it is based on cash flows and not on accounting data, the DCF method requires

the implementation of a different data collection system to that which the organization uses to

generate its financial statements. Alternatively, the economic profit approach, a concept well-

familiar to sophisticated managers, also considers the opportunity cost of capital, while

utilizing existing accounting data to calculate profit.

The most popular performance measure, which is based on the economic profit approach, is

the economic value added (EVA) suggested by Stewart (1991). EVA is calculated as the

adjusted capital employed multiplied by the difference between the adjusted return on capital

and the weighted average cost of capital for the firm. It measures the amount by which the

profit made by the firm exceeds the return required by the suppliers of capital. EVA also

requires that accounting figures are adjusted so that profit is measured more accurately.

Indeed, Tully (1993) notes that unlike traditional accounting measures of performance, EVA

is not distorted by accounting rules.

As will be discussed later, incorporating the opportunity cost of capital into the performance

measure is even more important in the case of MFIs compared with for-profit organizations.

The SDI method endeavours to incorporate this idea, while the FSS method does not.

7

3. The FSS measure of self sustainability

Realising the inadequacy of unadjusted traditional financial ratios in measuring MFI

performance, the FSS index has been developed to assess the self-sufficiency (or subsidy

dependence) of MFIs. It is a popular assessment method used by many MFIs as well as by

some rating agencies of MFIs. Notably the FSS index is used by the Microfinance

Information eXchange (MIX), a non-profit organization concerned with supporting the MFI

industry, which regularly reports the FSS indices of leading MFIs2.

The FSS index is designed to evaluate the level of subsidy dependence of MFIs and to gauge

their progress over time towards self sufficiency. More specifically the FSS measures the

extent to which the adjusted business revenue of an MFI, including interest and fee income,

covers adjusted costs.

(1)

Expense Operating ExpenseProvision LossLoan Net Expense FinancialAdjusted

Revenue Financial Adjusted

FSS

Costs are adjusted by the FSS method as follows (for further details see chapter 8 of

Ledgerwood, 1998 and Appendix I of The MicroBanking Bulletin, (MBB), of August 2005,

or any other MBB publication):

1) Adjustment for inflation. Inflation decreases the value of monetary assets. If the MFI has

net monetary assets, then inflation erodes the real value of its equity. The FSS

methodology charges an inflation cost that is calculated as the annual inflation rate

multiplied by the difference between equity and fixed assets. The idea is that in

measuring sustainability, an MFI should maintain the real value of equity.

2) Adjustment for concessionary loans. An MFI that benefits from concessionary loans must

consider the real economic cost of subsidies embedded in such loans. Hence, to adjust for

concessionary loans, the difference between a proxy for the market deposit rate and the

average annual concessionary borrowing rate is multiplied by the value of the average

annual concessionary borrowings. This cost is added to the financial costs recorded on the

income statement.

3) Adjustment for subsidies other than in the form of concessionary loans. MFIs often

receive financial help in the form of grants or in the form of in-kind subsidies. These may

include cash donations, partial or full coverage of loan losses, technical assistance

extended at below market cost, personnel who volunteer to work for the MFI for no

salary, and so forth. The FSS methodology adjusts for the effects of these subsidies.

The FSS measures the adjusted income of the MFI relative to its adjusted costs. When

adjusted income is lower than adjusted costs, the FSS measure is below 100% and the MFI is

defined as subsidy dependent. When adjusted income exceeds adjusted cost, the MFI is

defined as self-sufficient (subsidy independent).

2 The MIX is supported by many organizations including the Consultative Group to Assist the Poor (CGAP),

Rockdale Foundation, Citigroup Foundation and many more. It collects and reports data provided by leading

MFIs, principally in its MicroBanking Bulletin (MBB), where financial data and data on self sustainability

are organized by peer groups.

8

Although the FSS is widely used (notably by MIX and the MBB), this measure of self

sufficiency suffers from four main deficiencies. The first three deficiencies relate to subsidy

elements which the FSS methodology ignores in calculating the real opportunity cost of

financial resources used by the MFI. The fourth deficiency relates to the failure of the FSS

measure to distinguish between MFIs that lend to the target clientele and those that invest in

other financial instruments. The following paragraphs explain each deficiency in detail.

A. The administration costs of mobilizing and servicing deposits.

When adjusting for the cost of funds, the FSS methodology uses the financial cost of

voluntary deposit in the country concerned as a proxy for the market cost of funds (Line 60l

of the International Monetary Fund’s International Financial Statistics - IFS). The MIX, in its

MBB publication of August 2005 notes that a different rate may better reflect the shadow cost

of subsidised loans. For instance, licensed MFIs, that are allowed to mobilize savings

deposits of their clients as an alternative source of funds, should be justified in applying a

lower shadow cost than the deposit rate reported in line 60l of the IFS. However,

administration costs or reserve requirements may increase the costs of such liabilities3.

Thus using a shadow rate to reflect the opportunity cost of subsidized borrowings correctly

highlights the cost to society of concessionary funds. However, while it is proper to consider

this rate as an important factor of the opportunity cost of concessionary borrowings, this

treatment is insufficient as it neglects to consider the administrative costs associated with

mobilizing and servicing savings. Ignoring these costs is wrong for two reasons.

First, savings facilities are expected to become more important as the microfinance industry

evolves. Indeed, although traditionally the focus of the microfinance industry has been on the

provision of microcredit, it is gradually being realised that savings facility is a financial

product that for many clients of MFIs is not less and often more important than providing

credit facilities. Holding savings accounts with MFIs, relieves many poor people from the

asymmetric information barrier they often face when trying to access credit. Specifically, the

poor often cannot offer adequate collateral and therefore cannot access credit. However,

being able to save with the MFI allows these people to create a track record that contributes to

favourable future decisions regarding their creditworthiness.

Offering savings facility also provides a source of funds for the MFI and reduces its

dependence on donors’ funds (Dowla and Alamgir, 2003). It is often the case that the natural

path of development of MFIs leads them to gradually reduce reliance on donor or state

support and built - subject to existing regulations, norms and procedures - a capital base that

increasingly relies on savings. This means that even if the costs of mobilizing and servicing

savings are currently low, they are expected to increase as the MFI matures. Moreover, as the

MFI matures, it is expected to offer more sophisticated savings services which may be more

expensive to provide. For example, Dowla and Alamgir (2003) note that as MFIs move to

offer longer-term deposit facilities the administration costs associated with providing savings

facilities become more expensive. This is because the MFI commits to making larger future

payments to savers and because longer term deposits, while improving the liquidity of the

MFI, reduce the liquidity of the saving clients4.

3 See footnote 63, page 105, Appendix 1 of the MBB of August 2005.

4 The MFI may reduce the costs of servicing savings by targeting wealthier clients. However, by so doing the

MFI diverts from its original goal of providing financial services to the poor.

9

The second reason why the administration costs of mobilizing and servicing savings cannot

be ignored is that these costs are significant even when savings accounts form only a small

fraction of the activity of the MFI. There are a number of reasons for this. First, the clients of

MFIs that offer savings facilities tend to hold small value accounts which are more costly to

maintain5. Second, these clients usually demand easy and quick access to accounts and

convenient withdrawals which, from the point of view of the MFI, is labour-intensive and

expensive. Third, MFIs that offer savings facilities usually have more savings accounts than

loan accounts. For example, Robinson (1997) notes that at BRI Indonesia there are about six

deposit accounts for every loan, while at Bank Dagang Bali there are over 30 deposit accounts

for every loan. Thus an MFI that starts to offer effective savings services can expect a solid

demand of new customers and the associated additional costs including those related to

recruiting new staff, training existing staff, enhanced reporting, and so on.

Reliable data on MFIs’ administrative costs associated exclusively with servicing deposits

and savings accounts are rare. The reason for this is accounting practice that requires

reporting on total administrative costs, irrespective of whether they occur in servicing savings

accounts, lending, or any other activities carried out by the MFI. A number of studies have

attempted to overcome this lacuna of data availability by computing the savings expense ratio

which is calculated as the administrative costs of savings measured against the outstanding

value of savings accounts. Richardson (2003) reports a savings expense ratio of 3.65% for a

group of 15 credit unions. Hirschland (2003) reports a savings expense ratio of 5% for

VYCCU, Nepal in 2000. For BRI, Indonesia, possibly the world’s best performing MFI,

Hirschland (2003) reports a savings expense ratio of 2.2% in 1996. Accordingly, assuming a

savings expense ratio in the range of 2.2% to 5%, MFIs face substantially higher costs

compared with regulated banks that serve more affluent clients with larger average value

deposits. Furthermore, this range may be compared to a nominal financial cost of deposits of

4.2%. The latter is the 2004 average nominal deposit rate for 23 MFIs whose voluntary

savings accounts amount to 20% or more of their total assets (MBB April 2006) 6

.

Thus despite the fact that reliable information on the administrative costs of servicing and

mobilizing savings by MFIs is often absent, they are evidently material. Separate reporting

on the administration costs related to the various activities of the MFI is therefore crucial in

elevating this void7. Clearly, the costs associated with providing savings facilities should not

be ignored when the shadow price of concessionary borrowings (or equity) is computed in

order to measure self sufficiency of MFIs. Using an estimated lower bound of such

administrative costs is a preferable solution to ignoring these costs altogether, as practiced by

users of the FSS methodology.

Ignoring administration costs in determining the opportunity cost of concessionary funds

would inevitably lead to significant underestimation of the subsidy dependence of the MFI.

5 The value of the average savings account held by clients of MFIs is often only a fraction of the value of the

average loan outstanding. Dowla and Alamgir (2003) report that in December 1998 members’ savings form

between 16 to 37 percent of outstanding loans for a group of MFIs in Bangladesh.

6 The average financial cost of deposit of 4.2% refers to the nominal rate and not to the real, inflation-adjusted

rate. It is the average for 23 high financial intermediation MFIs, i.e. those whose voluntary savings accounts

amount to 20% or more of their total assets. See the table on page 47 and the guide to peer groups on page 85

of the MBB of April 2006.

7 Separate reporting of the costs of the various activities can be achieved by introducing rudimentary cost

accounting. This should help the MFI to understand the cost structure of each product it offers and therefore

to more appropriately price its products. Furthermore, even if the MFI decides to utilize some subsidization,

separate reporting of the costs of each product it offers should make the MFI more attractive to donors that

are increasingly seeking institutions with sound reporting procedures.

10

This, in turn, could lead the FSS measure to indicate that a subsidy-dependent MFI has

achieved subsidy independence. Alternatively it may lead the FSS to indicate that a subsidy-

dependent MFI is closer to being self sufficient than it actually is.

B. The opportunity cost of equity

Consistent with accounting practice, the FSS considers equity capital as a cost free item. This

accounting approach misses completely the whole point of measuring self-sufficiency, which

is based on the economic concept of the opportunity cost of capital. The economic concept

requires that equity is charged with an adequate shadow price which cannot be lower than the

opportunity cost of external borrowed funds.

By ignoring the opportunity cost of equity and treating it as a cost free item, the FSS method

suffers from the same problem that led to the advent of the EVA method (Yaron, 1992 and

Schreiner and Yaron, 2001). However, there are at least three reasons why ignoring the

opportunity cost of equity has more severe implications in the case of MFIs in developing

countries compared with for-profit organizations in developed countries.

First, MFIs benefit from various forms of grants and subsidies. Their equity-to-assets ratios

can therefore vary over a wide range. A given MFI may have an equity-to-assets ratio of

100% while another MFI may have a negative equity-to-assets ratio but will continue to

operate as it relies on continued support by donors or by the state. In contrast, the equity-to-

assets ratios of firms in other industries, including for-profit banks, oscillate within narrow

ranges that are specific to the industry concerned. The wide variation in the equity-to-assets

ratios of MFIs makes ignoring the opportunity cost of equity capital a more severe problem

compared to the problem it creates when measuring and comparing the performance of firms

in other industries. Particularly, ignoring the opportunity cost of equity when assessing MFI

performance is problematic when comparing MFIs that differ in their equity-to-assets ratios or

when tracking the performance of a single MFI with an unstable equity-to-assets ratio.

Second, the equity-to-assets ratios of many MFIs tend to be high. This means that the

distortion created by ignoring the opportunity cost of equity is substantial. The MBB of April

2006 reports an average equity-to-assets ratio in 2004 of 17.1% for 23 high financial

intermediation MFIs. This equity-to-assets ratio is high compared with the equity-to-assets

ratios that regular banks normally have. The high equity-to-assets ratio of these MFIs gives an

indication of the bias created by considering equity capital as a cost free item in measuring

self sufficiency. Moreover, the other two categories of MFIs that the MBB reports upon -

those of low financial intermediation and those of non financial intermediation - had much

higher average ratios of equity-to-assets of 39.5% and 46.5% respectively. This implies that

the bias in the FSS measure is even greater for these MFIs.8

Third, most MFIs operate in developing countries where inflation and risk premiums tend to

be higher than in developed countries. Ignoring the opportunity cost of equity under such

circumstances is likely to result in substantial underestimation of the subsidy dependence of

MFIs.

Thus by ignoring the opportunity cost of equity, the FSS methodology is likely to create a

downward distortion of the opportunity cost of equity that often entails underestimation of the

subsidy dependence.

8 Low financial intermediation MFIs are those whose voluntary savings accounts are lower than 20% of total

assets. Non financial intermediation MFIs are those with no voluntary savings accounts. See the tables on

page 45 and the index of indicators and definitions on page 74 of the MMB of April 2006.

11

C. Exemption from reserve requirements

The third factor that is missing in computing the self sufficiency of an MFI, using the FSS

methodology, is exemption from RR. Such exemptions are often awarded to MFIs,

particularly to unregulated MFIs, in countries where other formal, financial institutions (FIs)

are subject to RR. Like subsidized borrowings, exemption from RR constitutes a subsidy. It

relieves entitled MFIs from an additional cost of loanable funds which other FIs bear.

Therefore, exemption from RR should be reflected in the opportunity cost of concessionary

borrowings of MFIs. The real opportunity cost of subsidized borrowings is the sum of the

deposit rate of interest plus the rate of administration cost exclusively associated with

deposits, divided by 1 minus the rate of RR. This is the approach of the SDI method but not of

the FSS method9.

D. Reaching target clientele

The FSS measures the MFI’s adjusted income against its adjusted costs. This approach gives

no consideration to whether the subsidies invested, and the income generated, are related to

lending to the target clientele. As an extreme example, imagine that two MFIs were evaluated

to have identical FSS indices. However, the identical FSS indices could conceal the fact that

MFI A had invested 80% of its assets in loans to target clientele while MFI B had invested

80% of its assets in certificates of deposits (CD). Obviously MFI B did not serve its target

clientele as well as MFI A. However, the FSS methodology missed to identify this important

gap between the two MFIs. The problem of the FSS methodology is the fact that it does not

relate the overall subsidy to an indicator that reflects the MFI’s objective, such as outstanding

loan portfolio (LP) or income obtained on LP in servicing the target clientele.

Furthermore, the FSS methodology does not distinguish between an MFI that obtained self

sufficiency by servicing target clients and an MFI that achieved self sufficiency by investing

in commercial paper instead. The extent to which the MFI has achieved its set goals is

supposed to be captured by several other indicators to be used alongside the FSS index. In

contrast to the FSS, and as discussed below, the SDI measure resolves this problem to a large

extent, without having to rely on additional indicators.

The above discussion outlines some of the deficiencies of the FSS measure. These

deficiencies are illustrated in table 1. Table 1 is followed by a discussion of an alternative

approach to measuring MFI financial performance, the SDI-OI framework.

9 For example, assuming financial cost of 6 percent, administrative cost of 4 percent and non remunerative

reserve requirement of 10 percent, the real cost of loanable funds would be (6%+4%)/(1-0.1)=11.1%

12

Table 1: The deficiencies of the FSS method

FSS indicator Interpretation of the

FSS indicator

The distortion caused by the FSS

indicator

Two MFIs with different

equity-to-assets ratios have

identical FSS measures.

The two MFIs are equal

with respect to their

self-sufficiency.

Self sufficiency levels of the MFIs

are different. The self sufficiency

level of the MFI with lower

equity-to-assets ratio is higher.

The FSS measure of an MFI

shows a positive progression

over time. The equity-to-

assets ratio of the MFI has

also increased during the

period.

The MFI has managed

to improve its self

sufficiency over the

period.

Whether the MFI has managed to

improve its self-sufficiency over

the period is actually not known.

The improvement in the FSS

measure may be due to the upward

change in the equity-to-assets

ratio, as equity is considered a cost

free item by the FSS.

The FSS measure of the MFI

is 100%

The MFI is fully self-

sufficient.

If the MFI has equity in its capital

structure, than it is subsidy

dependent.

The FSS measure of the MFI

is lower than 100%

The MFI is not fully

self-sufficient.

The actual level of self-sufficiency

of the MFI is lower than the FSS

indicates.

The FSS measure of the MFI

is greater than 100%

The MFI has reached

full self sufficiency and

beyond.

The actual level of self-sufficiency

of the MFI is not known.

The FSS measure of MFI A,

as well as its equity-to-assets

ratio are higher than that of

MFI B.

MFI A has higher level

of self sufficiency

compared with MFI B.

It is not known which of the two

MFIs has achieved higher self

sufficiency level. If a charge is

made for the opportunity cost of

equity, MFI B may appear more

self-sufficient than MFI A.

The FSS of the MFI is 100%

and the MFI has no fixed

assets. Inflation rate is high

but the deposit rate exceeds

the inflation rate.

The MFI has reached

full self-sufficiency as

its adjusted costs were

fully covered by its

adjusted income.

The FSS measure ignores the

opportunity cost of equity. The

MFI is subsidy dependent.

Two MFIs with identical FSS

measures and identical

equity-to-assets ratios. MFI A

has LP that accounts for 80%

of its total assets while MFI

B has LP which accounts for

20% of total assets.

MFI A and MFI B have

achieved the same level

of self sufficiency.

MFI A directs a higher share of its

resources to serving the target

clientele, while achieving the same

level of self sufficiency as MFI B.

Therefore, MFI A is more cost

effective which is not recognised

by the FSS.

The MFI benefited from

concessionary funds in year

1. Its FSS is below 100%. In

year 2 the MFI fully replaced

all concessionary funds. It

achieved an FSS of 100%.

The change in the FSS

measure from year 1 to

year 2 indicates an

improvement in the self

sufficiency level of the

MFI.

The progress made towards self

sufficiency is greater than reflected

by the change in the FSS. The

reason is that the FSS of year 1

overestimated the self sufficiency

level of the MFI at that time.

13

4. Using the SDI and the OI to measure MFI performance.

The FSS is an indicator that was developed to capture the level of self sufficiency of MFIs.

Prior to the introduction of the FSS, Yaron (1992) introduced a framework for assessing MFI

performance and self sufficiency. The framework, which has gained wide acceptance among

practitioners and academics, combines two primary assessment criteria, outreach and self-

sustainability. The former is measured by the OI indicator and seeks to measure the extent to

which the MFI has reached its target clientele. The latter is measured by the SDI indicator

which, like the FSS, seeks to measure the self sufficiency or self sustainability of the MFI.

Yaron (1992) argues that using the OI alongside the SDI, is conductive in evaluating the

extent to which an MFI has reached its target clientele in an efficient manner. Moreover,

using the framework gives a reliable measure of the progress made by the MFI over time

towards subsidy independence and self sufficiency. Thus using the framework should enable

the identification of those MFIs that are likely to achieve the desired goals of expanding

incomes and/or reducing poverty.

4.1. The SDI measure of self sustainability.

The SDI is designed to measure the self-sustainability level of the MFI with a single number.

It is calculated as the annual subsidy received by the MFI, divided by the income earned by

the MFI on its average annual LP. The SDI gives an indication of the percentage by which the

average yield obtained on the MFI’s LP would have to increase in order to make it subsidy

independent. It also indicates the cost to society of subsidizing the MFI, relative to the

interest plus fees paid by the target clientele to the MFI.

Calculating the SDI is imperative in evaluating the use of subsidies to support the MFI versus

assisting the target clients through non-financial intermediation. In that sense the SDI may be

assessed in terms of matching the grant received to the income generated. Particularly, the

SDI matches the subsidy granted by society, (the numerator in the SDI measure) to the value

of fees and interest payments paid by clients (the denominator).

The SDI is normally computed in two stages. In the first stage the total annual subsidy

received by the MFI is divided by the average annual LP. For a given MFI, this provides the

annual subsidy per annual dollar of LP. In the second stage the total annual subsidy received

by the MFI is divided by the interest and fee income earned on the MFI’s LP. The second

stage gives the complete SDI measure and places the total amount of subsidies received by the

MFI in the context of its activities10

.

The amount of the annual subsidy received by the MFI is defined as:

KPmEcmAS (2)

where:

S Annual subsidy received by the MFI

A MFI concessionary borrowed funds outstanding (annual average)

10

While the nominator in the SDI formula is unchanged between the two stages, the denominator sets them

apart. The denominator in the first stage is the MFI’s LP. The denominator in the second stage is the yield

(interest and fees) earned by the MFI on its LP. The complete SDI is therefore the ratio of the total annual

subsidies received by the MFI (explicit and implicit) to the income earned on its LP.

14

m The assumed interest rate that the MFI would have to pay for borrowed funds if

access to concessionary borrowing was eliminated.

c Weighted average annual concessionary rate of interest actually paid by the MFI

on its annual average concessionary borrowed funds outstanding

E Average annual equity

P Reported annual profit before tax (adjusted, when necessary, for loan loss

provisions, inflation, and so on)

K The sum of all other annual subsidies received by the MFI (such as partial or

complete coverage by the state of operational costs of the MFI).

The complete SDI is defined as:

iLP

SSDI

(3)

where:

SDI Index of subsidy dependence of the MFI

S Annual subsidy received by the MFI (see above)

LP Average annual outstanding loan portfolio of the MFI

i Weighted average yield earned on the loan portfolio of the MFI.

If it is assumed that an increase in the lending interest rate is the only change that may

compensate for loss of subsidy, then the SDI provides a sensitivity measure of the MFI’s self

sufficiency to the annual yield it charges on its loans. Particularly under this assumption, the

SDI indicates the percentage increase in the annual yield on the MFI’s LP that is needed for

full subsidy independence to be reached. Figure 2 illustrates the point. As shown in figure 2,

at a yield on loans of just under 18%, the SDI value is 0 and the MFI is fully self sufficient.

15

Figure 2. The sensitivity of the SDI to the yield that the MFI

receives on its LP

-30%

-20%

-10%

0%10%

20%

30%

40%

50%

60%70%

80%

90%

100%

10%

11%

12%

13%

14%

15%

16%

17%

18%

19%

20%

21%

22%

23%

24%

25%

Yield on lending

SD

I

However, assuming that the only factor that influences the self sustainability of the MFI is its

lending rate is unrealistic. Indeed, the SDI measure is an accurate measure of self

sustainability as it is influenced not only by the yield obtained on the MFI’s LP but also on

interest rate spreads it faces, its loan collection rate and the administration costs it incurs in

carrying out its activities. In other words, improving any of these factors, for example saving

on costs or reducing loan losses also reduces the SDI value and indicates improvement

towards subsidy independence. Furthermore, using the SDI facilitates comparisons of MFIs

that provide similar products to similar clientele. Comparisons may be carried out within a

single country or across countries to assess the subsidy dependence of the MFIs concerned. It

can also be used to track the subsidy dependence of a given MFI over time to assess whether

it has truly progressed toward self sufficiency.

The advantage of the SDI is its simplicity and the fact that it focuses exclusively on subsidies

received measured against income obtained on LP. This may be contrasted with the FSS ratio

which measures the subsidy the MFI benefits from against all income not distinguishing

between income made on LP and other income such as investment in CD. As shown in table

1, it may be the case that income was generated by means other than lending to the target

clientele. In that case two MFIs with identical FSS measures may in fact be very different in

terms of the social justification of supporting them.

Under some circumstances striving to achieve self sustainability and to completely remove all

subsidies is not politically feasible or even economically desirable. However, even under

such circumstances, calculating the SDI measure is still warranted for three basic reasons.

First, the SDI may be seen as a tool to measure subsidy dependence and improvements

thereof over time, thereby contributing to assessing the social desirability of continued

subsidization. Second, measuring the subsidies received by the MFI is always economically

and politically desirable as it should improve resource allocation. Third computing and

16

disclosing the SDIs of MFIs provide imperative basic data to the public debate on the use of

scarce public funds.

4.2. The OI measure of outreach and the benefits of integrating the OI and the SDI in

evaluating MFIs’ performance

Yaron (1992) suggests the OI as a measure of outreach to be used alongside the SDI. The OI

seeks to measure the outreach of an MFI to the target clientele - the output of the financial

support granted to the MFI. It should reflect the social desirability of the quality and quantity

of services offered. The OI should make use of several indicators in evaluating the outreach

of the MFI. Examples include number of clients, average loan size, or the percentage of

female clients. Schreiner (2002) identifies six dimensions of outreach while Francisco et al

(2007) suggest a weighting scheme that should be applied to the various dimensions and

indicators in order to reflect the relative priority assigned to each. Given the wide variety of

competing objectives, the OI measure encourages the MFI and related donors to explicitly

define quantifiable output variables that proxy for the objectives set, and to select the relative

weights of each variable reflecting their priorities.

The OI is a hybrid (arbitrary) index that should reflect the priorities and weights assigned to

its components, which may change over time. The main advantage of the OI is that it

encourages the authorities that foot the subsidy bill to clearly clarify their objectives, priorities

and precisely define the target clientele. It also allows for a more accurate measurement of

the related costs associated with well defined products that aim at achieving the MFI’s

objectives.

Integration of the SDI and the OI provides a framework that captures the social cost and the

social output utilization of subsidies by the MFI. It can highlight the idea that a subsidy is

more socially desirable to society when it is cost effective in achieving the social objectives it

was set to achieve. For example, if the social objective that a subsidy was set to achieve is to

serve poor farmers, then the same value subsidy per dollar of LP extended to poor farmers is

more valuable to society than its equivalent per dollar of LP extended to rich farmers. Policy

makers can and should define and quantify how much higher is the value they attribute to a

dollar LP granted to poor clients compared to a dollar LP extended to a rich ones.

Figure 3 summarizes the SDI-OI framework for assessing MFI performance, by listing the

characteristics of each of its two components.

17

Figure 3: The SDI-OI framework for assessing MFI outreach and self sustainability

Measuring MFI

performance

Measuring self

sustainability

Measuring

outreach

SDI

Measures subsidies

received against interest

earned by the MFI

OI

Evaluates outreach to

clients and quality of

services offered

Examples of Subsidies:

Interest rate subsidy

on concessionary

borrowed funds

Opportunity cost of

equity

Others, including:

Reserves

requirement

exemptions;

Free equipment

provided by

government/

donors;

Government’s

assumption of

loan losses;

Free training for

staff provided by

government/

donor

Government

assumption of

foreign exchange

loans

Examples of Indicators

Market Penetration

Number and annual

growth rates of

savings and loan

accounts

Value and annual

growth rates of the

LP and deposits

Number of

branches and staff

Relative Income Level

Value of average

loan and range of

loan amounts

Percentage of rural

clients

Percentage of

women clients

Quality of Services

Transaction costs to

clients

Flexibility and

suitability of

services

Distribution

network

Source: Adapted from Yaron et al (1997)

As shown in figure 3 the OI is designed to assess the outreach or the output of the MFI while

the SDI, like the FSS, is designed to capture the level of self sustainability of the MFI. In the

following section the SDI is compared to the FSS.

5. Comparing the FSS and the SDI

18

We argue that the FSS is inferior to the SDI in accurately measuring the self sufficiency level

of MFIs. Table 2 compares the two measures and highlights the strengths of the SDI method

relative to the FSS.

Table 2: Comparing the FSS and the SDI measures of self sufficiency of MFIs.

Deficiency 1 Deficiency 2

Explaining the

deficiency of

the FSS

Equity capital is considered a cost

free item (excluding adjustment for

inflation that aims at maintaining

the real value of equity).

Administrative costs related to

savings are not considered when

estimating the opportunity cost.

Implications of

using the FSS

given the

deficiency

Principal implication: Ignoring

the opportunity cost of equity

capital and hence overestimating

the level of the MFI’s subsidy

independence.

Additional implications: The

underestimation of the level of the

MFI’s subsidy dependence

increases with:

1. The equity-to-assets ratio

(equity is measured net of fixed

costs).

2. The real (inflation adjusted)

cost of capital in the country.

Principal implication:

Underestimation of the MFI’s

subsidy dependence.

Additional implications: The

underestimation of the level of the

MFI’s subsidy dependence increases

with:

1. The administration costs of

mobilizing and servicing a

dollar of outstanding savings

2. The rate of savings to total

assets ratio.

The severity of

the FSS

deficiency

The deficiency is severe as it

hinders meaningful comparisons of

self sufficiency across MFIs or a

meaningful analysis of the progress

made towards self sufficiency by an

MFI whose equity-to-assets ratio

changes over time.

The deficiency is severe given that

MFIs’ savings accounts are normally

of small value and their owners

demand liquidity. Servicing these

accounts tends to involve relatively

high administration costs per dollar

of outstanding savings.

How the issue

is resolved by

the SDI method

Charges all financial resources,

including equity, with an

opportunity cost that reflects the

actual cost of capital.

Incorporates the administration costs

related to savings into the shadow

price applied to concessionary

borrowings and equity

19

Table 2: Comparing the FSS and the SDI measures of self sufficiency of MFIs. (continued)

Deficiency 3 Deficiency 4

Explaining the

deficiency of

the FSS

Ignores exemptions from existing

RR

Does not distinguish between MFIs

that invest a large fraction of their

assets in LP and those that divert their

assets to other investments. Two such

differing MFIs may have identical FSS

values and erroneously assessed as

having identical social performance.

Implications of

using the FSS

given the

deficiency

Principal implication:

Underestimation of the MFI’s

subsidy dependence.

Additional implications: The

underestimation of the MFI’s level

of subsidy dependence increases

with the RR ratio.

Principal implication: The identical

FSS values indicate that the two MFIs

have achieved the same level of self-

sufficiency. The FSS method ignores

the fact that the MFI with a higher

share of LP is more efficient in serving

its target clientele. Thus an MFI which

is more dedicated to its target clientele

is evaluated to equal an MFI that has

drifted away from its mission.

The severity of

the FSS

deficiency

Important when RR are high.

However, many MFIs maintain

high cash reserves in order to meet

cash demand of their clients. It is

thus possible that they meet RR

even if they are exempt.

(Assuming reserves do not have to

be deposited at the central bank.)

The deficiency can be severe when

comparing the performance of MFIs

that differ significantly in the ratio of

LP to total assets. The deficiency is

also important when measuring

progress towards self sufficiency over

time and the MFI evaluated has

increased the ratio of LP to total

assets. In that case the FSS

underestimates the progress made

towards subsidy independence over

time.

How the issue

is resolved by

the SDI

method

The SDI takes into account

exemption from RR when

computing the opportunity cost of

capital and the resulted subsidy the

MFI benefits from.

The total subsidy received is measured

against: (1) the value of LP; and (2)

the yield on LP. Hence, the SDI

reflects the degree to which the MFI

uses its resources to lend and not for

other purposes.

20

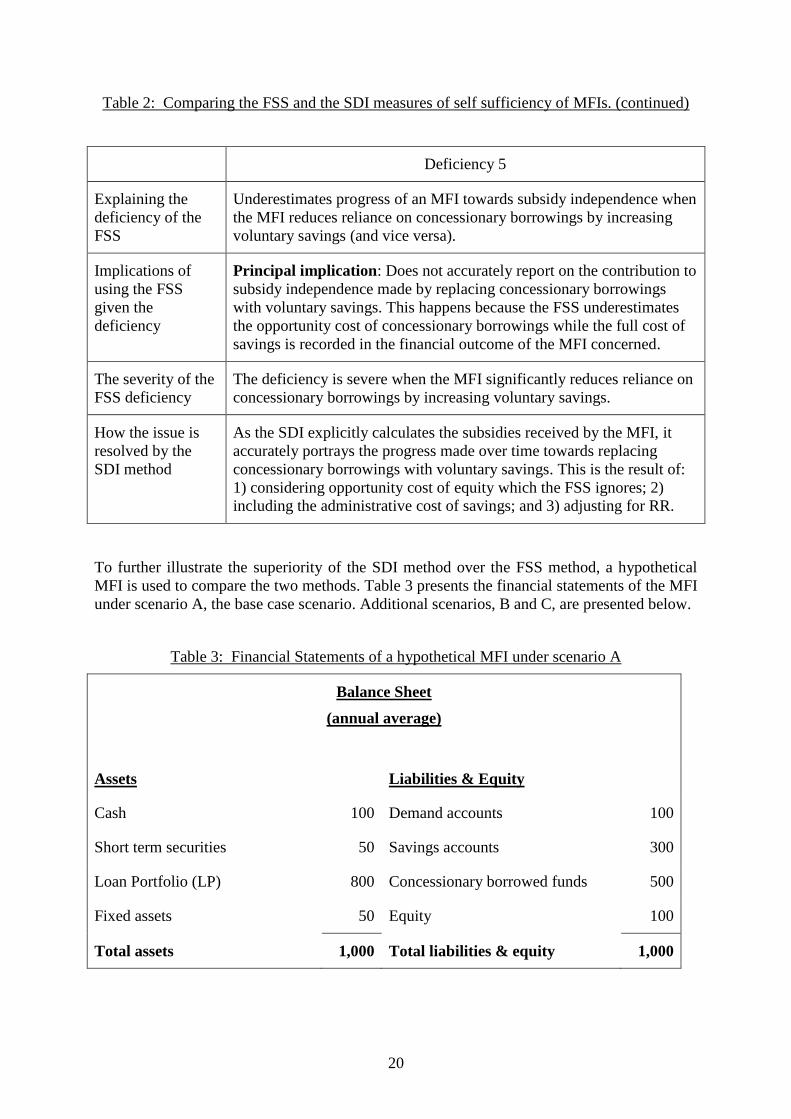

Table 2: Comparing the FSS and the SDI measures of self sufficiency of MFIs. (continued)

Deficiency 5

Explaining the

deficiency of the

FSS

Underestimates progress of an MFI towards subsidy independence when

the MFI reduces reliance on concessionary borrowings by increasing

voluntary savings (and vice versa).

Implications of

using the FSS

given the

deficiency

Principal implication: Does not accurately report on the contribution to

subsidy independence made by replacing concessionary borrowings

with voluntary savings. This happens because the FSS underestimates

the opportunity cost of concessionary borrowings while the full cost of

savings is recorded in the financial outcome of the MFI concerned.

The severity of the

FSS deficiency

The deficiency is severe when the MFI significantly reduces reliance on

concessionary borrowings by increasing voluntary savings.

How the issue is

resolved by the

SDI method

As the SDI explicitly calculates the subsidies received by the MFI, it

accurately portrays the progress made over time towards replacing

concessionary borrowings with voluntary savings. This is the result of:

1) considering opportunity cost of equity which the FSS ignores; 2)

including the administrative cost of savings; and 3) adjusting for RR.

To further illustrate the superiority of the SDI method over the FSS method, a hypothetical

MFI is used to compare the two methods. Table 3 presents the financial statements of the MFI

under scenario A, the base case scenario. Additional scenarios, B and C, are presented below.

Table 3: Financial Statements of a hypothetical MFI under scenario A

Balance Sheet

(annual average)

Assets Liabilities & Equity

Cash 100 Demand accounts 100

Short term securities 50 Savings accounts 300

Loan Portfolio (LP) 800 Concessionary borrowed funds 500

Fixed assets 50 Equity 100

Total assets 1,000 Total liabilities & equity 1,000

21

Table 3: Financial Statements of a hypothetical MFI under scenario A (continued)

Income Statement

Interest earned

On loans (15% * 800) 120

On securities (16% * 50) 8

Total Income 128

Interest paid

On savings accounts (10% * 300) 30

On borrowed funds (8% * 500) 40

Total interest paid (70)

Gross margin 58

Administrative costs (4.8% * 1,000) (48)

Profit (before tax) 10

Based on the following assumptions, table 4 below compares the FSS and SDI measures of

the hypothetical MFI:

1. Balance sheet figures are annual averages

2. Interest earned on LP is 15 percent p.a.

3. Rate of interest earned on securities is 16 percent p.a.

4. No interest is paid on demand accounts.

5. Rate of interest paid on savings accounts (the financial market rate on deposits) is 10

percent p.a.

6. Rate of interest paid on concessionary borrowed funds is 8 percent p.a.

7. The cost of mobilizing and servicing savings accounts is 2 percent of savings

8. Total cost of savings accounts (10%+2%) =12% p.a. (See assumption 5 and assumption

7. This is m in the subsidy formula of equation 2)

9. No RR exist

10. Rate of annual inflation is 0 percent.

11. Administrative cost is 4.8 percent of total assets

12. No loan losses occurred

13. No other subsidies were granted

22

Table 4: Comparison of the SDI and FSS measures of the hypothetical MFI under scenario A

The SDI

The SDI

formula is: iLP

SSDI

The subsidy,

S, is: 22010%)12100(%8%12500

12%2%10% costs servicing depositson ratemarket

])[()(

S

m

KPmEcmAS

The first

stage SDI: %75.2

800

22

LP

S

The complete

SDI is: %3.18

120

22

%15800

22

iLP

S

The FSS

Expense Operating ExpenseProvision LossLoan Net Expense FinancialAdjusted

Revenue Financial Adjusted

FSS

Adjusting the cost for concessionary

borrowings: 10%8%10500

Total adjusted costs are: 128104870

The FSS is: %100

128

128

Costs Adjusted

Revenue AdustedFSS

The top part of table 4 demonstrates how the SDI is calculated. The first stage calculation of

the SDI shows that annual subsidy per dollar of LP amounts to 2.75 cent. The complete SDI

for the MFI in the example is 18.3%. This indicates that to remove all subsidies it was

required to increase the yield obtained on LP by 18.3% (from 15%

23

to %75.17183.1%15 )11

. In other words, to eliminate the subsidy, the MFI had to achieve

interest income of 142 instead of the 120 it actually achieved. Alternatively a cost saving of

22 could have also eliminated the subsidies, as would any combination of increases in the

yield and a cost saving that amount to 22. An SDI of 18.3% also indicates that for every

dollar paid by the clients of the MFI for services rendered, 18.3 cents were granted by society

or donors.

The bottom part of table 4 shows how the FSS is calculated. The rate of inflation is assumed

to be zero and no subsidies other than those embedded in concessionary borrowings are

assumed to have been granted. Therefore the only adjustment to costs that is required is an

adjustment with respect to concessionary borrowings. The difference between the market

deposit rate (10%) and the concessionary borrowings rate (8%) is multiplied by the value of

the concessionary borrowings (500) resulting in an increase of the financial cost by $10. This

is added to the total adjusted costs in the denominator of the FSS ratio. However, while the

10% market deposit rate is included in calculating the financial cost of the MFI, the cost of

mobilizing and servicing savings (2% of the value of outstanding savings), which was

included in the SDI computation, is ignored. The FSS ratio is 100%, indicating that the MFI

has reached full self-sufficiency. This result is inconsistent with the SDI and indeed does not

accurately represent the level of the MFI’s subsidy dependence.

Three main conclusions emerge from the calculations in table 4. First, the SDI and FSS

methods deliver different results regarding the subsidy dependence of the same MFI. Second,

the FSS underestimates the subsidy dependence of the hypothetical MFI. Third, shifting from

using the FSS to using the SDI - or vice versa - is relatively easy.

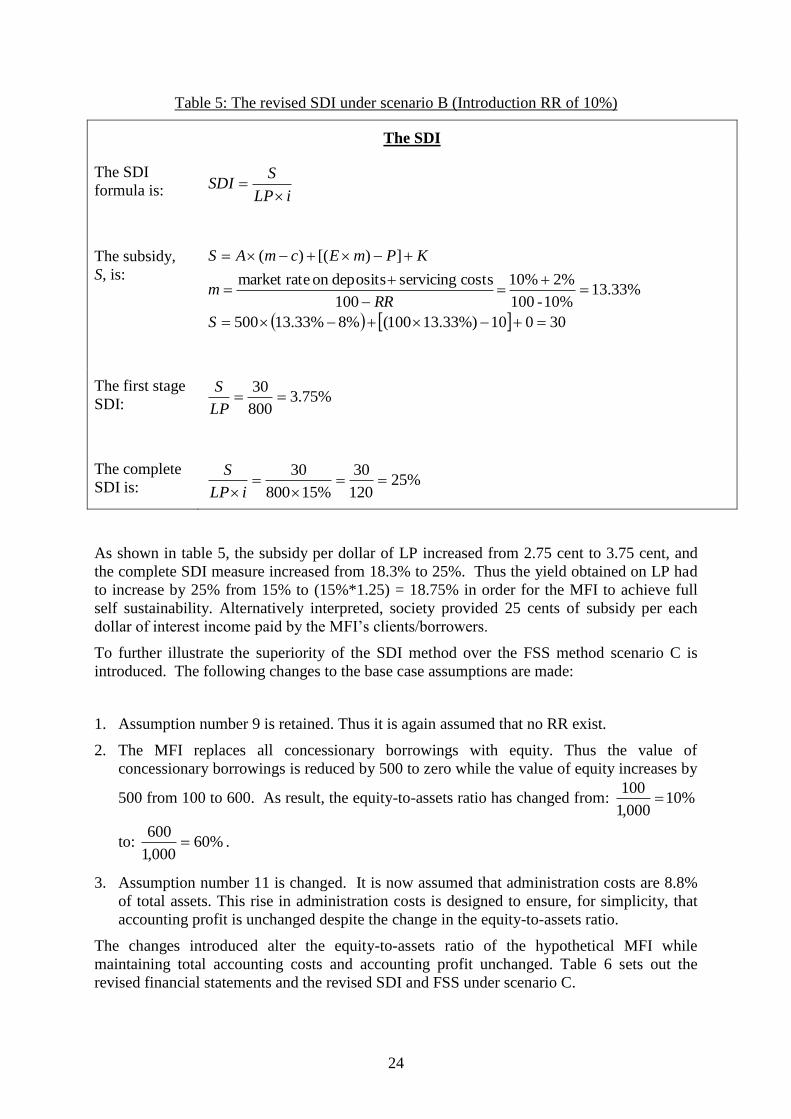

To further illustrate the superiority of the SDI over the FSS, scenario B is introduced. Under

scenario B assumption number 9, the RR assumption, is changed. It is now assumed that RR

are 10% of deposits and are non-remunerative, and the MFI enjoys exemption from RR

(which borrowers and savers bear). As the FSS ignores the subsidy implied in exemption

from RR, the FSS measure is unchanged. In contrast, as illustrated in table 5, the SDI value

has increased. The increase in the SDI measure reflects the fact that given RR, the exemption

granted to the MFI implies that it is now more subsidy-dependent.

11

Figure 2 on page 145 presents a graph of the sensitivity of the SDI measure to the yield on the MFI’s LP. This

graph is based on data related to the hypothetical MFI presented in this section. As illustrated in figure 2, the

SDI is zero and the MFI is fully self-sufficient, when the yield on LP is 17.75%.

24

Table 5: The revised SDI under scenario B (Introduction RR of 10%)

The SDI

The SDI

formula is: iLP

SSDI

The subsidy,

S, is:

30010%)33.13100(%8%33.13500

13.33%10%-100

2%10%

100

costs servicing depositson ratemarket

])[()(

S

RRm

KPmEcmAS

The first stage

SDI: %75.3

800

30

LP

S

The complete

SDI is: %25

120

30

%15800

30

iLP

S

As shown in table 5, the subsidy per dollar of LP increased from 2.75 cent to 3.75 cent, and

the complete SDI measure increased from 18.3% to 25%. Thus the yield obtained on LP had

to increase by 25% from 15% to (15%*1.25) = 18.75% in order for the MFI to achieve full

self sustainability. Alternatively interpreted, society provided 25 cents of subsidy per each

dollar of interest income paid by the MFI’s clients/borrowers.

To further illustrate the superiority of the SDI method over the FSS method scenario C is

introduced. The following changes to the base case assumptions are made:

1. Assumption number 9 is retained. Thus it is again assumed that no RR exist.

2. The MFI replaces all concessionary borrowings with equity. Thus the value of

concessionary borrowings is reduced by 500 to zero while the value of equity increases by

500 from 100 to 600. As result, the equity-to-assets ratio has changed from: %10000,1

100

to: %60000,1

600 .

3. Assumption number 11 is changed. It is now assumed that administration costs are 8.8%

of total assets. This rise in administration costs is designed to ensure, for simplicity, that

accounting profit is unchanged despite the change in the equity-to-assets ratio.

The changes introduced alter the equity-to-assets ratio of the hypothetical MFI while

maintaining total accounting costs and accounting profit unchanged. Table 6 sets out the

revised financial statements and the revised SDI and FSS under scenario C.

25

Table 6: Revised Financial Statements and comparison of SDI and FSS under scenario C

Balance Sheet

Assets Liabilities & Equity

Cash 100 Demand accounts 100

Short term securities 50 Savings accounts 300

Loan Portfolio (LP) 800 Concessionary borrowed funds 0

Fixed assets 50 Equity 600

Total assets 1,000 Total liabilities & equity 1,000

Income Statement

Interest earned

On loans (15% * 800) 120

On securities (16% * 50) 8

Total Income 128

Interest paid

On savings accounts (10% * 300) 30

On borrowed funds (8% * 0) 0

Total interest paid (30)

Gross margin 98

Administrative costs (8.8% * 1,000) (88)

Profit (before tax) 10

26

Table 6: Revised Financial Statements and comparison of SDI and FSS under scenario C

(continued)

The SDI

The SDI

formula is: iLP

SSDI

The subsidy,

S, is: 62010%)12600(%8%120

12%2%10% costs servicing depositson ratemarket

])[()(

S

m

KPmEcmAS

The first

stage SDI: %75.7

800

62

LP

S

The complete

SDI is: %7.51

120

62

%15800

62

iLP

S

The FSS

Expense Operating ExpenseProvision LossLoan Net Expense FinancialAdjusted

Revenue Financial Adjusted

FSS

Adjustment for concessionary borrowing: 0%8%100

Total adjusted costs are: 11808830

The FSS is: %5.108

118

128

Costs Adjusted

Revenue AdustedFSS

It is clear that the MFI under scenario C became less cost-effective and more subsidy

dependent (or less financially self sufficient) compared with scenario A. This is because

neither LP nor the yield obtained on LP, increased, but the administrative costs went up from

4.8% to 8.8% of total assets.

27

Comparison of scenario A in table 4 and scenario C in table 6 shows that the revised FSS

value improved from 100% to 108.5%, indicating that the MFI became more self sufficient.

In reality the opposite occurred. The main reason for this failure is that the MFI replaced

concessionary borrowings with equity. According to the FSS, the shift of 500 from

concessionary borrowings to equity fully eliminated the financial cost of concessionary

borrowings and attached a cost of zero to the increase in equity. This in turn, created a

distorted picture according to which a real increase in subsidy dependence is considered by

the FSS as improvement in self sufficiency.

In contrast to the FSS, the revised SDI value reflects the increase in subsidy dependence of

the MFI. The SDI charges a real opportunity cost to equity, while the FSS ignores the fact

that equity has an opportunity cost and therefore distorts and overestimates the MFI’s degree

of self sufficiency. The first stage SDI indicates that the subsidy per dollar of outstanding LP

increased from 2.75 cent to 7.75 cent, mirroring the substantial increase in administration

costs that were not backed by increase in LP. The complete SDI increased from 18.3% to

51.7%, a significant change of nearly 200%. The revised SDI measure indicates that the

yield on LP had to increase by 51.7%, from 15% to 22.7% for the MFI to be fully self

sufficient.

6. Conclusions

The FSS and the SDI are two popular methods used to measure the self sufficiency of MFIs.

Both methods have gained much popularity in recent years with the shift towards

commercialisation of the industry.

The current paper reviews the two methods. It finds that the FSS measure tends to

underestimate the subsidy dependence of the MFI. Alternatively put, the FSS measure tends

to overestimates the self-sufficiency of the MFI analyzed. This deficiency is demonstrated

with numerical illustrations showing that it is not a coincidence but the result of inherent traits

of the FSS methodology.

The paper discusses the main deficiencies of the FSS, which include the following:

A. When measuring the subsidy attributed to concessionary funds, the FSS methodology

ignores the significant administration costs of mobilizing and servicing deposits.

Accurate measure of the subsidy attributed to concessionary funds should consider the

administration costs associated with mobilizing and servicing deposits in determining the

opportunity cost of these funds.

B. The FSS measure treats equity as a cost free item. The only charge applies to equity

capital is a charge to account for inflation-related erosion of net monetary assets.

C. The FSS methodology ignores the cost of RR. MFIs are often exempt from RR applicable

to other FIs in the country concerned. Ignoring this exemption may therefore lead to

underestimation of the subsidy received by MFIs.

D. The FSS methodology does not distinguish between an MFI that generates its income by

lending to target clientele and an MFI that uses the subsidies received to generate income

from other sources. This is despite the fact that subsidies are clearly granted to MFIs for

the purpose of lending to the target clientele.

28

The deficiencies of the FSS methodology should convince society and donors to use the SDI

methodology to measure MFI performance. The SDI measures the value of subsidies against

the MFI’s LP and against the yield obtained on its LP. It is consistent with the objective of

supporting MFIs that benefit society, rather than supporting MFIs that “consume” subsidies

while drifting away from their mission.

The advantage of the SDI method over the FSS method is that it does not suffer from the

deficiencies that characterise the FSS method. It therefore more accurately measures the real

level of self-sufficiency of MFIs, and it tends to indicate higher level of subsidy dependence

compared with the FSS method. When real progress towards self sufficiency of an MFI is

measured over time, the SDI provides a more accurate picture of the progress compared with

the biased FSS method.

To obtain a complete view of MFI performance, the use of the OI is suggested alongside the

SDI. The OI measures the extent to which the MFI succeeded in delivering the products it was

set to deliver, to the target clientele. It is a flexible arbitrary index, designed to reflect the

priorities of those that foot the bill of supporting MFIs. The OI gives an indication of the

social desirability of supporting MFIs compared to achieving the desired social goals by other

means.

Using the SDI-OI framework should contribute substantially to understanding MFI

performance. In particular, using the SDI-OI framework is useful in highlighting the cost of

each product that is delivered by the MFI to the target clientele. Measuring the cost of each

product delivered by the MFI is important given that resources are limited, and funds

tunnelled to support MFIs could have instead been used to support the target clientele via

alternative instruments.

The SDI-OI framework should be used to review and analyze past performance as well as to

plan and budget future operations. The framework can assist in the task of allocating scarce

public funds to MFIs that are charged with achieving socially justified objectives.

29

References

Dowla, A. and Alamgir, D. (2003), ‘From Microcredit to Microfinance: Evaluation of

Savings Products by MFIs in Bangladesh’, Journal of International Development,

Vol. 15, No. 8, pp. 969-988.

Economist (2005), ‘The Hidden Wealth of the Poor’, Economist, November 5, Vol. 377 Iss.

8451, p. 3.

Francisco, M., Mascaró, Y., Mendoza, J.C. and Yaron, J. (2007), ‘Measuring Performance

and the Achievement of Social Objectives of Development Financial Institutions

(DFIs)’, World Bank Working Paper, forthcoming.

Hirschland, M. (2003), ‘Serving Small Depositors: Overcoming the Obstacles, Recognizing

the Tradeoffs’, MicroBanking Bulletin, Iss. 9, (July), pp. 3-8.

International Monetary Fund (2006), International Financial Statistics, Washington, DC:

IMF.

Ledgerwood, J. (1998), Microfinance Handbook: An Institutional and Financial Perspective,

Washington, DC: World Bank.

MIX (2005), The MicroBanking Bulletin: Special Edition on Financing, August, Iss. 11.

MIX (2006), The MicroBanking Bulletin: Focus on MFI Performance by Region, April, Iss.

12.

O’Brien, B. (2006), ‘Valuing Microfinance Institutions’, Savings and Development, Vol. 30,

No. 3, pp 275-296.

Richardson, D. (2003), ‘Going to the Barricades with Microsavings Mobilization: A View of

the Real Costs from the Trenches’, MicroBanking Bulletin, Iss. 9, (July), pp. 9-13.

Robinson, M. (1997), ‘Introducing Savings in Microfinance Institutions: When and How’,

CGAP Focus Notes, No. 8.

Schreiner, M. (2002), ‘Aspects of Outreach: A Framework for the Discussion of the Social

Benefits of Microfinance’, Journal of International Development, Vol. 14, No. 5,

pp.591-603.

Schreiner, M. and Yaron, J. (2001), Development Finance Institutions. Measuring their

Subsidy, Washington, DC: World Bank.

Stewart, G.B. (1991), The Quest for Value, New York: Harper Business.

Tully, S. (1993), ‘The Real Key to Creating Wealth’, Fortune, September 20, Vol. 128, Iss. 6,

pp. 38-44.

Yaron, J. (1992), ‘Assessing Development Finance Institutions: A Public Interest Analysis’,

World Bank Discussion Paper 174, Washington, DC: World Bank.

Yaron, J., McDonald P.B. and Piprek, G.L. (1997), ‘Rural Finance: Issues, Design, and Best

Practices’, Environmentally and Socially Sustainable Development Studies and

Monographs Series 14, Washington, DC: World Bank.