department of water affairs (dwa) and water trading entity (wte) predetermined objectives –...

TRANSCRIPT

Department of Water Affairs (DWA) and Water Trading entity (WTE) Predetermined Objectives – 2013/14March 2013

2

Reputation promise/mission

The Auditor-General of South Africa has a constitutional mandate and, as the Supreme Audit Institution (SAI) of South Africa, it exists to strengthen our country’s democracy by enabling oversight, accountability and governance in the public sector through auditing, thereby building public confidence.

3

Annual audit of reported actual performance against predetermined Annual audit of reported actual performance against predetermined objectives, indicators and targets as contained in the annual objectives, indicators and targets as contained in the annual performance report . performance report .

Annual audit of reported actual performance against predetermined Annual audit of reported actual performance against predetermined objectives, indicators and targets as contained in the annual objectives, indicators and targets as contained in the annual performance report . performance report .

Integral part of the annual regularity audit process, confirming the • Compliance with laws and regulations• Usefulness of performance reporting• Reliability of performance reporting

Integral part of the annual regularity audit process, confirming the • Compliance with laws and regulations• Usefulness of performance reporting• Reliability of performance reporting

Audit of predetermined objectives defined as:

4

Public Finance Management Act (PFMA), 1999 (Act No.1 of 1999)Public Finance Management Act (PFMA), 1999 (Act No.1 of 1999)

Treasury Regulations issued in terms of the PFMA, 2002Treasury Regulations issued in terms of the PFMA, 2002

Public Service Regulations (PSR), Part III B: (Only applicable to departments)Public Service Regulations (PSR), Part III B: (Only applicable to departments)

Guidelines, instruction notes, practice notes, issued by National TreasuryGuidelines, instruction notes, practice notes, issued by National Treasury

Framework for managing programme performance information (issued by the National Treasury in May 2007)

Framework for strategic and annual performance plans(issued by National Treasury in August 2010)

Framework for managing programme performance information (issued by the National Treasury in May 2007)

Framework for strategic and annual performance plans(issued by National Treasury in August 2010)

Legislative requirements for planning, budgeting & reporting of performance info

5

ExistenceExistence

TimelinessTimeliness

PresentationPresentation

MeasurabilityMeasurability

RelevanceRelevance

Consistency Consistency

ValidityValidity

AccuracyAccuracy

CompletenessCompleteness

Compliance with regulatory Compliance with regulatory requirementsrequirementsCompliance with regulatory Compliance with regulatory requirementsrequirements

UsefulnessUsefulnessUsefulnessUsefulness

ReliabilityReliabilityReliabilityReliability

Audit criteria

6

Understand and test the design and implementation of the performance management systems, processes, and relevant controls

Understand and test the design and implementation of the performance management systems, processes, and relevant controls 11

Test the measurability, relevance, presentation & consistency of planned and reported performance information

Test the measurability, relevance, presentation & consistency of planned and reported performance information22

Conclude on the reliability of the reported performance for selected programmes or objectives

Conclude on the reliability of the reported performance for selected programmes or objectives55

Audit approach

Test the reported performance information to relevant source documentation to verify the validity,

accuracy & completeness of reported performance information

Test the reported performance information to relevant source documentation to verify the validity,

accuracy & completeness of reported performance information44

7

Audit reporting – Management report

An audit conclusion will be prepared and included in the management reports for all departments, constitutional institutions, trading entities, public entities, Parliament and provincial legislatures

An audit conclusion will be prepared and included in the management reports for all departments, constitutional institutions, trading entities, public entities, Parliament and provincial legislatures

8

Usefulness of information: Audit findings focus on the consistency, relevance, measurability & presentation of reported performance information.

Reliability of information:

Audit findings focus on the validity, accuracy & completeness of reported performance information

REPORT ON OTHER LEGAL AND REGULATORY REQUIREMENTS

Predetermined objectives

COMPLIANCE WITH LAWS AND REGULATIONS

Report non-compliance matters in relation to the performance management and reporting processes

Audit reporting – Auditor’s report

9

1010

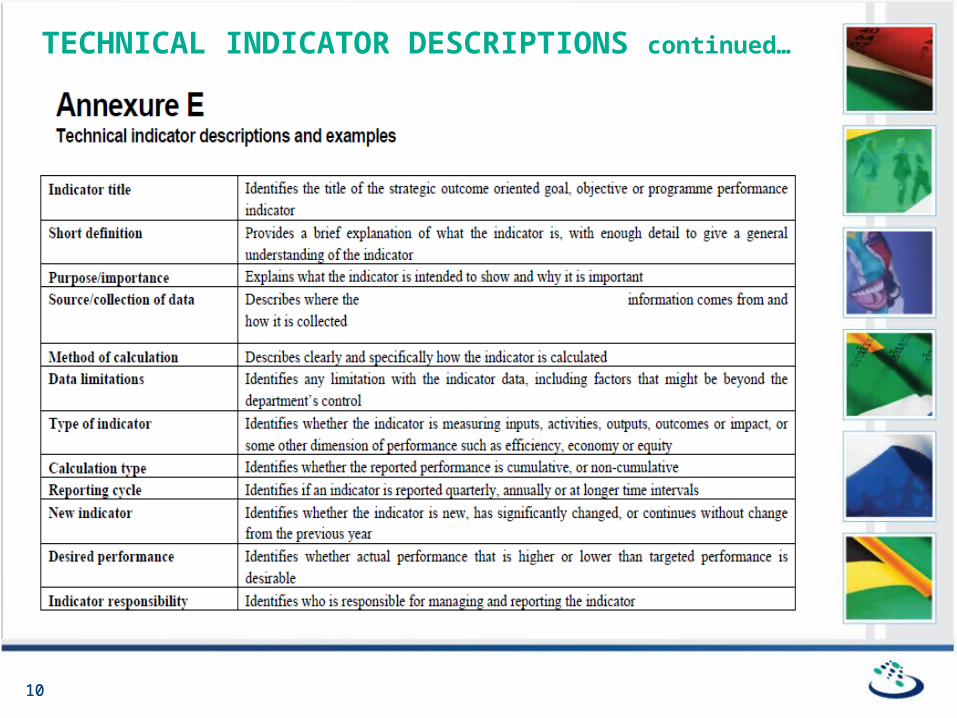

TECHNICAL INDICATOR DESCRIPTIONS continued…

11

12

Additional matters

Achievement of planned targets

•Greater than 20% of planned targets not achieved

Material adjustments to the annual

performance report

1313

OVERVIEW

• A review of the draft 2013/14 Annual Performance Plan and the related draft Strategic Plan was performed on a sample basis.

• Our focus was to assess the usefulness of the information contained in the plans in terms of the:– measurability and relevance of indicators(well-defined, verifiable,

relevant)

– measurability of targets (specific, measurable, time-bound, relevant)

• Findings and discussions.

• Conclusion in management report.

1414

Findings – Measurability of Indicators

Definition:

The indicator needs to have a clear, unambiguous definition so

that data will be collected consistently and be easy to understand

and use (supported by Appendix E).

Error rate:

56% of indicators were not well defined (WTE – Programme 1,3&4)

64% of indicators were not well defined (DWA – Programme 2&4)

WELL DEFINED

1515

Findings – Measurability of Indicators (continued)

VERIFIABLE

Definition

It must be possible to validate the processes and systems that

produce the indicator (supported by Appendix E)

Error rate:

56% of indicators were not verifiable (WTE – Programme 1,3&4)

81% of indicators were not verifiable (DWA – Programme 2&4)

1616

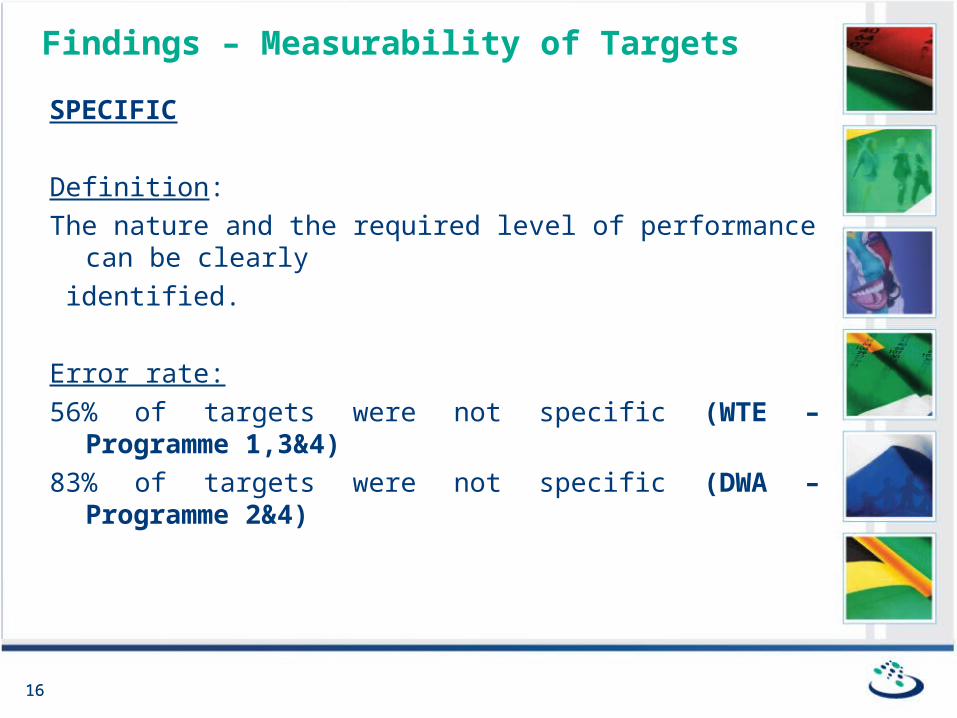

Findings – Measurability of Targets

Definition:

The nature and the required level of performance can be clearly

identified.

Error rate:

56% of targets were not specific (WTE – Programme 1,3&4)

83% of targets were not specific (DWA – Programme 2&4)

SPECIFIC

1717

Findings – Measurability of targets (continued)

MEASURABLE

Definition :

The required performance can be measured.

Error rate:

56% of targets were not measurable (WTE – Programme 1,3&4)

83% of targets were not measurable (DWA – Programme 2&4)

1818

Findings – Measurability of targets (continued)

TIME BOUND

Definition:

The time period or deadline for delivery is specified.

Error rate:

0% of targets were not time bound (WTE – Programme 1,3&4)

0% of targets were not time bound (DWA – Programme 2&4)

1919

Findings – Relevance

RELEVANCE

Definition:

Indicators : The indicator must relate logically and directly to an

aspect of the institution’s mandate and the realization of strategic

goals and objectives. Targets: The required performance is

linked to the achievement of a goal.

Error rate:

0% of indicators and related targets were not relevant (WTE&DWA)

2020

TECHNICAL INDICATOR DESCRIPTIONS

• The Framework for Strategic Plans and Annual Performance Plans as issued by NT and enforced by Instruction Note 33 requires all departments, trading entities, constitutional institutions and schedule 3A & 3C public entities to compile technical indicator descriptions (see Annexure E extract in slides) for all performance indicators included in their plans effective from the 2012/2013 reporting period.

• These technical indicator descriptions must be published on the website of the department/constitutional institution /public entity.

• WTE and DWA have compiled technical indicator descriptions for the 2013/14 year (did not have any in the 2012/13 year).

2121

CONCLUSION

• Thresholds on errors identified:– 0% to 19% No opinion

– 20% to 50% Qualified

– Above 50% Adverse or disclaimer

• The errors identified in relation to the indicators and targets in the 2013/14 plan were above the threshold for disclaimer/adverse opinion in the management report for both WTE and DWA.

2222

RECOMMENDATION

• Management to ensure clear definitions and technical standards for indicators and targets are developed

• Develop and implement standard operating procedures to report on targets

• Clearly defined roles and responsibilities linked to individual performance contracts

• A forum should be established for the portfolio to share insights and have a consistent approach.

• Continue to involve the AGSA in the planning process (allow sufficient time)

23

THANK YOU