denials, delays and deep discounts. poor insurance ... › ... · received commercial coverage •...

TRANSCRIPT

Denials, Delays and Deep Discounts. Poor Insurance Coverage for Pharmaceuticals at Launch

IN COLLABORATION WITH

IPI Supergraphic 2

For use as a graphic overlay on theedge of photos, at the given angle.Should act as a bridge between the photo and adjacent background.Please do not change the color orthe angle of the supergraphic.

Brian Cotten, Heather Martin and Jeff StewartCommercial Advisory Group Syneos Health

September 2019 / 3© Informa UK Ltd 2019 (Unauthorized photocopying prohibited.)2 / September 2019 © Informa UK Ltd 2019 (Unauthorized photocopying prohibited.)

IntroductionFDA approval is the most important milestone for a new pharmaceutical. An approved product is one of the fortunate few. Only about one in ten products tested in clinical trials is ever approved.1 For brand teams, launch is the exciting start to what may be millions of healthier patients and billions of dollars in revenue.

There is a problem. Launch year has become a nightmare of insurance denials, delays and deep discounts.

In 2018,2 there were 103 branded therapeutics approved by the US FDA. Just over half of these approvals were for new molecular entities (NMEs) – molecules that were approved for the first time. The remaining new approvals were under the 505(b)(2) pathway for new formulations or manufacturing change of an already approved molecule. These two product classes – NMEs and 505(b)(2)s – represent pharma’s first fruits of success.

Therapeutic drug purchases in the US are mediated largely by insurance companies. Large, national insurance companies such as CVS, Express Scripts, and UnitedHealthcare purchase drugs on behalf of patients. Patients, for their part, pay insurance premiums, copays and coinsurance to insurance companies to access drugs. Health insurance providers in the US do more than spread out actuarial risk. Insurance companies also play a central role in negotiating net price with innovators and in rationalizing care. The comingled roles of insurance companies – in negotiating price and in choosing which agents rationally patients can use – set up an unfortunate scenario at launch.

In short, payers don’t pay for new drugs.

We examined all 103 launches of new therapeutics from 2018 and compared these drugs with the products appearing on the early 2019 approved drug lists of large, national payers. We examined the formularies of the commercial and Medicare plans with the most covered lives separately because these books of business do not always have the same coverage decisions (Figure 1).

Of the 103 innovative products approved in 2018, no large, national payer included even half of these products on the published formulary by 2019. On the commercial book of business, CVS included only two innovative products of any kind (2% of approvals) on the published formulary. These two products were Biktarvy for HIV-1 and Erleada for prostate cancer.

Jeff Stewart Director, Commercial Advisory Group, Syneos Health Consulting

Jeff Stewart brings over 20 years of experience to his work in the Commercial Advisory Group at Syneos Health Consulting. Mr. Stewart has performed adviso-ry work for nearly all of the top-10 pharmaceutical companies in areas such as forecasting, copay card design, and launch pricing. Mr. Stewart was the first to publish rNPV, the most commonly used valuation method in life sciences.

Previously at Syneos Health, Mr. Stewart served as Head of Search and Evalu-ation and, prior to that, as Vice President, Business Development for Caldera Pharmaceuticals. Mr. Stewart earned an MBA from the University of Notre Dame, an MA in molecular biology from Princeton University, and a BS in mo-lecular biology from Brigham Young University.

Brian Cotten Associate Consultant, Commercial Advisory Group, Syneos Health Consulting

Brian Cotten brings a research background in pharmacology data analytics to his role in the Commercial Advisory Group at Syneos Health. Mr. Cotten has performed advisory work on a variety of analytics and modeling projects in areas such as copay assistance strategy, payer segmentation, and contracting strategy.

Before joining Syneos Health Consulting, Mr. Cotten worked as a Data Analyst and Technician in the Adaptive Behavior Laboratory of Columbia University, where he conducted academic and pharmaceutically funded studies of behav-ioral and motivational psychiatric conditions. Mr. Cotten earned a Bachelor’s Degree in Neurobiology from Boston University.

Heather Martin Engagement Manager, Commercial Advisory Group, Syneos Health Consulting

Heather Martin has more than a decade of experience in the biotechnology and pharmaceutical industries. She brings a research background in analyti-cal chemistry and graduate level education in business and health care policy to her role in the Commercial Advisory Group at Syneos Health Consulting. Ms. Martin has performed advisory work for a range of clients from large bio-pharmaceutical companies to startups in areas including pricing, contracting, patient access and unique channel strategies.

Before joining Syneos Health Consulting, Ms. Martin worked as a Senior Manager in both Market Access and the Chief Strategy Office at Mylan Phar-maceuticals. Ms. Martin earned a Bachelor’s Degree in Chemistry from Princ-eton University, an MBA and an MS in Health Care Policy & Management from Carnegie Mellon University.

The comingled roles of insurance companies – in negotiating price and in choosing which agents rationally patients can use – set up an unfortunate scenario at launch.

September 2019 / 5© Informa UK Ltd 2019 (Unauthorized photocopying prohibited.)4 / September 2019 © Informa UK Ltd 2019 (Unauthorized photocopying prohibited.)

Both these products were approved in February 2018. The remaining 98% of new approvals from 2018 either were approved later in the year or (apparently) for less-critical indications and did not make CVS’s most-popular commercial formulary by January 2019.

No 505(b)(2) approved in 2018 appeared on CVS’s most-popular formulary by early 2019. On the Medicare book of business, UnitedHealthcare had the lowest number of inclusions of 2018 approvals on the early 2019 formulary (6%).

It’s important to caveat that some products not appearing on the most-popular published formulary may have been accessible by patients through medical exemptions or even were approved for formulary but not published. Nonetheless, patients would not have been able to know readily through a published formulary that such drugs were accessible.

Twenty-six (26) drugs were not included on either commercial or Medicare formularies sampled. Most of these products would be expected to have patients in the US (the exceptions included moxidectin for treatment of river blindness in Africa and TPOXX for smallpox).

Eighteen (18) drugs were unique to exclusion by Medicare plans, including dermatology products Seysara and Qbrexza. Six (6) drugs were unique to exclusion by commercial formularies, including rare disease therapies Lumoxiti and Onpattro.

Figure 1: High Membership Formularies Sampled for Top Commercial and Medicare Part D Payers3

Payer Commercial Formulary Medicare Formulary

Express Scripts National Preferred Medicare Value

Kaiser N/A Comprehensive Formulary Senior

Aetna Premium Plus Medicare Comprehensive

CVS/Silverscripts Performance Standard Choice Comprehensive Formulary

Humana N/A Walmart Rx Plan

Cigna Standard 3-Tier HealthSpring Rx

United Healthcare (AARP)* N/A Medicare Rx Preferred

United Healthcare 2019 Prescription Drug List N/A

Anthem National N/A

OptumRx Select Standard N/A

*Note: AARP Medicare plans are sponsored by UnitedHealthcare

Payer Reactions to 505(b)(2) Versus NME ApprovalsMost commercial payers in this sample were more likely to favor NMEs over 505(b)(2) products. However, access scenarios differ significantly among organizations (Figure 2). Different payers had very different patterns of launch year formulary inclusion. There is a clear pattern of delays, denials, and (in our experience) deep discounts required for year one formulary inclusion by CVS, Prime, and UnitedHealthcare. Somewhat more prone to approve new products for formulary inclusion were the merged Cigna and Express Scripts. At the other extreme were Anthem, which approved 20 505(b)(2) products and 10 NMEs, and Aetna, which allowed just over half (54%) of 2018 approvals to be on its most popular early 2019 formulary.

Most products launched in 2018 faced non-coverage in sampled 2019 Medicare Part D formularies. Medicare launch coverage trended towards consistency due to more structured bidding timelines. There was a move toward the median, with the most controlled and most open commercial plans clustering toward the center in the Medicare book of business. However, in spite of Centers for Medicare and Medicaid Services (CMS) regulations, launch access was not uniform across Part D plans (Figure 3).

NME Coverage Analysis The general rule seen at launch is that launch denial is common and more so with 505(b)(2)s than with NMEs (Figure 4). This pattern is consistent with

®

TM

0

5

10

15

20

25

30

35

40

0 5 10 15 20 25

Most payers were more likely to favor NMEs over 505(b)(2) products.

# 505(B)(2) BRANDED APPROVALS COVERED (OF 38)

# N

ME

BRAN

DED

APP

ROVA

LS C

OVE

RED

(OF

56)

50% of Branded NMEs launched in 2018

50% of 505(b)(2)s launched in 2018

Optum had not updated its formulary from June 2018 to January 2019

Anthem uniquely favored 505(b)(2)products over NMEs

Open access

CVS is notorious for poor launch-year coverage

Blue Cross

®

Figure 2: Commercial Launch Coverage 2018 Branded Approvals on 2019 Formularies

September 2019 / 7© Informa UK Ltd 2019 (Unauthorized photocopying prohibited.)6 / September 2019 © Informa UK Ltd 2019 (Unauthorized photocopying prohibited.)

TM

0

5

10

15

20

25

30

35

40

0 5 10 15 20 25

Part D launch coverage was more consistent. Despite CMS regulations, launch access was not uniform across Part D plans. Most products launched in 2018 faced non-coverage in mostpublished 2019 formularies.

*Note: United Healthcare insures AARP Medicare Rx Preferred plans

# N

ME

BRAN

DED

APP

ROVA

LS C

OVE

RED

(OF

56)Part D Launch Coverage 2018 - Branded Approvals on 2019 Formularies

# 505(B)(2) BRANDED APPROVALS COVERED (OF 38)

50% of Branded NMEs launched in 2018

50% of 505(b)(2)s launched in 2018

Both UHG*and CVS/SilverScript had poor Part D launch access but with some differences from commercial

Cigna nearly aligned its Part Dand commercial launch access

ESI had much worse NME launchcoverage in Part D vs. commercial Aetna Part D launch coverage

was very different from its commercial open access

®

TM

TM

Blue Cross

®

# N

ME

BRAN

DED

APP

ROVA

LS C

OVE

RED

(OF

56)

0

5

10

15

20

25

30

35

40

Most payers covered less than 50% of NMEs within the first year of launch.

Plan Type

Commercial Medicare Part D

Prime and Anthem both covered 10 NMEs

50% of NMEslaunched in 2018

Figure 4: Commercial Versus Medicare Launch Coverage for 2018 NME Approvals on 2019 Formularies

Figure 3: Part D Launch Coverage 2018 Branded Approvals on 2019 Formularies

our experience with payers. Payers often express frustration to us with 505(b)(2) products as providing minimal perceived value to the payer and may be viewed as an attempt to circumvent loss of exclusivity rather than a formulation innovation that provides unique value to the patient, provider, or plan.

The bottom line is clear. Launch is now more challenging than ever. New entrants – both NMEs and reformulations – should expect payers to deliver denials, delays and deep discounts.

REFERENCES1 Hay M et al. Clinical development success rates for investigational

drugs. Nature Biotechnology. 2014. 32:40-51

2 1/9/2018 – 12/14/2018. FDA Orange Book. 47 505(b)(2)s and 56 NMEs.

3 For Commercial plans, CVS/Caremark and Optum Rx publically available formularies were only updated as of 11/16/2018 and 6/1/2018, respectively at the time of sampling (December 2018). Eight of the 103 approvals sampled were high priced orphan therapies, and while not covered on any sampled formularies, were covered on the Express Scripts prior approval list. OTC products were excluded from the 103 approvals in this study. Non-covered drugs include those explicitly excluded and drugs not listed in plan formularies (some drugs may have coverage decisions that do not appear on published formularies).

• Manufacturers should expect non- coverage in the launch year for both NMEs and 505(b)(2)s

• Commercial launch coverage tends to be more favorable and more variable than Medicare Part D coverage

• Despite CMS regulation, Part D plans exhibit coverage variance among major payers

• CVS/Caremark, the largest insurance com-pany in the US, showed strong disinclination to give launch coverage to any product – notably zero 505(b)(2) launch products received commercial coverage

• Innovation is not enough. Fewer than 50% of NMEs approved in 2018 received coverage in major commercial plans sampled (seven of eight plans)

• Reformulations are not favored by payers. No major plan (commercial or Part D) covered more than 50% of 505(b)(2) launches. A handful of primary care 505(b)(2) approvals received coverage, but the expectation should be for non-coverage in the launch year

• Coverage is most likely for protected classes such as HIV and oncology

IPI Supergraphic 1

For use as a background elementon white or ligh-colored backgrounds.Please do not change the color orthe angle of the supergraphic.

Syneos Health® (Nasdaq:SYNH) is the only fully integrated biopharmaceutical solutions organization. Our company, including a Contract Research Organization (CRO) and Contract Commercial Organization (CCO), is purpose-built to accelerate customer performance to address modern market realities. Created through the merger of two industry leading companies – INC Research and inVentiv Health – we bring together approx-imately 24,000 clinical and commercial minds with the ability to support customers in more than 110 coun-tries. Together we share insights, use the latest technologies and apply advanced business practices to speed our customers’ delivery of important therapies to patients. To learn more about how we are shortening the distance from lab to life®, visit syneoshealth.com.

IN COLLABORATION WITH

8 / September 2019 © Informa UK Ltd 2019 (Unauthorized photocopying prohibited.)

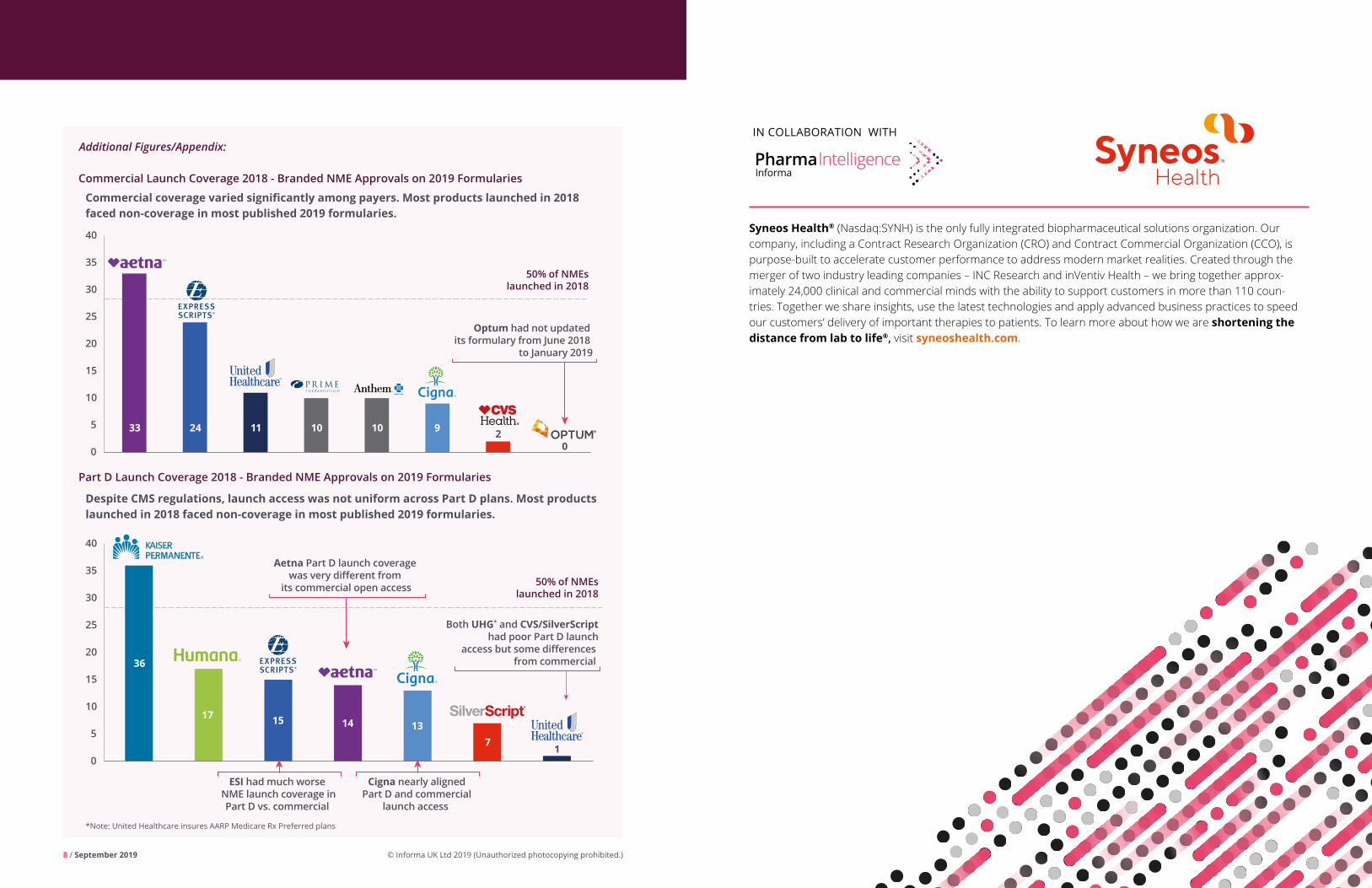

Additional Figures/Appendix:

33 24 11 10 10 9 2

0

5

10

15

20

25

30

35

40

Commercial coverage varied significantly among payers. Most products launched in 2018faced non-coverage in most published 2019 formularies.

50% of NMEslaunched in 2018

Optum had not updated its formulary from June 2018

to January 2019

0

®

Blue Cross

TM

®

50% of NMEslaunched in 2018

36

17 15 14 137

10

5

10

15

20

25

30

35

40

Despite CMS regulations, launch access was not uniform across Part D plans. Most productslaunched in 2018 faced non-coverage in most published 2019 formularies.

ESI had much worse NME launch coverage inPart D vs. commercial

Cigna nearly alignedPart D and commercial

launch access

Both UHG* and CVS/SilverScripthad poor Part D launch

access but some differences from commercial

Aetna Part D launch coverage was very different from

its commercial open access

*Note: United Healthcare insures AARP Medicare Rx Preferred plans

TM

Commercial Launch Coverage 2018 - Branded NME Approvals on 2019 Formularies

Part D Launch Coverage 2018 - Branded NME Approvals on 2019 Formularies