deepwater trends and implications for the drilling marketswiber.listedcompany.com/misc/drilling_...

TRANSCRIPT

Strategic Advisors in Global Energy

Deepwater Trends and Implications for the Drilling Market

June 12, 2008

PFC Energy

Swiber Deepwater Open Forum

Table of Contents

| Page 2

� Overview of Fundamentals – Long Term Supply and Price Implications

� Significance of Deepwater Oil and Gas in Upstream Portfolios

� Deepwater Rig Supply and Demand – Implications for Future Day Rates

� Drilling Activity Forecasts

• In spite of high oil prices, Non-OPEC conventional production has been flatto declining with the exception of the FSU.

• Oil exploration in the last 10 years (with a few exceptions like Angola, Sudan,Mauritania, Brazil) has been much less successful than in previous decades.Since 1990 reserve replacement in non-OPEC has been less that 35 percent.

• Every year, in every region (including OPEC), the world produces more oilthan it finds. It is only logical to conclude that inevitably this will lead tosupply and daily rate issues. Our current view is that absent significant

Key Messages

| Page 3

supply and daily rate issues. Our current view is that absent significantimprovements in recovery technologies or exploration results global non-OPEC liquid hydrocarbon production will struggle to grow beyond 2010 andmay in fact start to decline.

• Non-OPEC production growth between now and the end of this decade willrely heavily on production growth in Kazakhstan, Azerbaijan, Russia, Brazil,and several smaller producing countries.

• If demand continues to grow beyond 2010 and if Non-OPEC productioncapacity plateaus or falls, OPEC will have to make up the difference resultingin an inevitable increase in dependency on OPEC sources.

Global Non-OPEC Liquids & OPEC Non-Quota Liquids Supply Forecast (With Exploration)

30,000

40,000

50,000

60,000

70,000

Daily Production (mb/d)

Global Non-OPEC & OPEC Non-Quota Total Liquids Forecast with Exploration

| Page 4

0

10,000

20,000

30,000

1985

1990

1995

2000

2005

2010

2015

2020

Daily Production (mb/d)

Europe USA Middle East

Africa Canada AustralAsia

Latin America FSU/EE Canada Unconventional Heavy

OPEC & Non-OPEC NGL Biofuels GTL

Oil Shale

A combined forecast of Non-OPEC liquids and OPEC non-quota liquids suggeststhat production will grow to just around 60 million barrels per day by 2015.

Uzbekistan

Norway

Oman

New Zealand

Argentina

Congo

Colombia

Australia

Yemen

Denmark

Mexico

Chad

Canada

Brunei

Malaysia

India

China

Turkmenistan

Countries in the decline phase

Countries in the plateau phase

Non-OPEC Countries in Decline or in Plateau

| Page 5

1965 1970 1975 1980 1985 1990 1995 2000 2005

USA

Romania

Tunisia

Peru

Dem Rep Congo

Cameroon

Other Europe

Egypt

Pakistan

Papua New Guinea

Syria

UK

Gabon

Uzbekistan

The above bars show the onset and duration of documented productionpeaks or plateaus – tracking country life cycle shows an acceleration ofthe number of countries passing from peak to decline

Onset of Plateau

Duration of Plateau

Onset of Decline

Why Has Traditional Exploration Been Slow to React to High Prices?

60

80

100

120

140

160

180

200

Mean Field Size (mmbo)

Mean Field Size Country History

Mean Field Size Post-1990

| Page 6

0

20

40

60

Argentina

Pakistan

Thailand

Indonesia

India

Colombia

Oman

Peru

Gabon

Egypt

Congo

Ecuador

China

Yemen

Kazakhstan

Malaysia

Syria

Denmark

Algeria

UK

Libya

Norway

Mexico

Vietnam

Azerbaijan

Venezuela

Mean Field Size (mmbo)

Comparison of Mean Sizes for All Basin History Versus the Post 1990 Period

2,000

4,000

6,000

8,000

10,000

12,000

Differential Between Annual Volumes Produced and

Annual Vloumes Discovered (m

mbo)

Annual Reserves Disc - Annual Reserves Prod

4 per. Mov. Avg. (Annual Reserves Disc - Annual Reserves Prod)

12 Consecutive Years Where Annual Production Volumes Have Exceeded Annual

Volumes Discovered

Annual Non-OPEC Crude Production Balance (excluding FSU, USA, and Uncon. Heavy Oil)

| Page 7

-8,000

-6,000

-4,000

-2,000

0

2,000

1965

1970

1975

1980

1985

1990

1995

2000

2005Differential Between Annual Volumes Produced and

Annual Vloumes Discovered (m

mbo)

PFC Energy’s analysis indicates that countries within this group have, inaggregate, been producing 4-5 billion barrels each year more than they have beenfinding through exploration since the mid-1990s.

Concerns With OPEC Reserves

• The real issue here is that we really do not know what several key OPECcountries reserves really are because there is no way to independently verifythem as we can in most non-OPEC countries where you have foreigncompanies doing the exploration and development.

• The shape and style of these country’s remaining reserve profiles in the face ofdisappointing exploration results over the last 20 years and the fact that theyalmost exactly offset production with reserves through book keeping has toraise suspicions - A comparison of actual new discoveries and productionvolumes indicates that OPEC has been running a negative crude oil balance

| Page 8

volumes indicates that OPEC has been running a negative crude oil balancesince the early 1980s with production volumes exceeding new volumesdiscovered by approximately 6.0-8.0 billion barrels per annum

• Our analysis suggests that OPEC overall has depleted approximately 40percent of its reserve base with annual depletion levels running at 1 %/year(OPEC would argue that it is their policy to have 0% depletion) ….. If PFC’sestimated rate of depletion is correct then OPEC will reach the critical level of60% in the later part of the next decade.

OPEC Historical Annual Crude Production Balance (OPEC)

C h a r t T it le

0

2 ,0 0 0

4 ,0 0 0

6 ,0 0 0

8 ,0 0 0

1 0 ,0 0 0

Differential Betw

een Annual Volumes Produced

and Annual Vloumes Discovered (mmbo)

Annua l R eserves D iscovered - Annua l R eserves P roduced

3 p e r . Mov . Avg . (Annua l R eserves D iscovered - Annua l R eserves P roduced )

| Page 9

Like all other areas of the world, PFC Energy’s data analysis indicates that GlobalOPEC crude production is currently exceeding volumes discovered.

-1 0 ,0 0 0

-8 ,0 0 0

-6 ,0 0 0

-4 ,0 0 0

-2 ,0 0 0

0

1965

1970

1975

1980

1985

1990

1995

2000

2005

Differential Betw

een Annual Volumes Produced

and Annual Vloumes Discovered (mmbo)

80,000

100,000

120,000

Daily Production (mb/d)

80,000

100,000

120,000

Non-OPEC Crude Non-OPEC Oil Sands

Non-OPEC NGL & Condensate OPEC NGL

1.1% Growth 1.7% Growth

2.4% Growth

37-45 mmb/d

46-58 mmb/d

Call on OPEC Crude

OPEC 33-36 mmb/d

The Dilemma - The Expected Growing Gap Between Global Demand and Global Non-OPEC Supply in the Next Decade

| Page 10

0

20,000

40,000

60,000

1995

2000

2005

2010

2015

2020

Daily Production (mb/d)

0

20,000

40,000

60,000

OPEC Crude

Table of Contents

| Page 11

� Overview of Fundamentals – Long Term Supply and Price Implications

� Significance of Deepwater Oil and Gas in Upstream Portfolios

� Deepwater Rig Supply and Demand – Implications for Future Day Rates

� Drilling Activity Forecasts

Production growth will come from 5 major categories

• Unconventional heavy oil (Canada and Venezuela)

• Monetizing large gas reserves through LNG

• Deepwater E&P

• Caspian/FSU E&P

• All other

– New shallow water or onshore discoveries

Growth: Where will it Come From?

| Page 12

– Older shallow water or onshore discoveries now commerciallyviable because of oil and gas prices

– Large gas projects developed for pipeline

– Projects gained thru improved access

– Unconventional natural gas

– Others

Where Are the Large Producers Adding New Production?

3000

4000

5000

6000

7000

8000

9000Entitlement Production (mboe/day)

All Other

Russia/Caspian

Deepwater

LNG

Unc Heavy Oil

| Page 13

• The above profile shows the breakout of entitlement production (barrelsequivalent) for: XOM, BP, Shell, Chevron, CoP, Total, ENI.

• Production additions from more conventional onshore and shallow waterplays (outside of the FSU) accounts for only about 25% of new production

0

1000

2000

200020

0220

04

200620

0820

1020

1220

14

201620

1820

2020

2220

24

202620

2820

30

Entitlement Production (mboe/day)

Global Deepwater Competition Service

Location of Global Deepwater ProjectsNorth Atlantic

Total Projects: 24

MediterraneanTotal Projects: 5

| Page 14

Total Projects: 217Minimum Water Depth 1,000 feet

Gulf of MexicoTotal Projects: 130

Latin AmericaTotal Projects: 21

West AfricaTotal Projects: 54

Asia-PacificTotal Projects: 17

Global Deepwater – Who are the players?

Who are the players?

Asia-Pacific Gulf of Mexico Latin America Mediterranean North Atlantic West Africa

BHP Billiton Anadarko Chevron BG BP BP

Chevron ATP Oil & Gas Petrobras BP ConocoPhillips Chevron

ConocoPhillips BHP Billiton Repsol YPF Hess Eni CNR

Eni BP Shell Petronas ExxonMobil Devon

Mitsui Chevron RWE-Dea Gaz de France Eni

Murphy ConocoPhillips Hess ExxonMobil

Niko Devon Idemitsu Hardman

Deepwater Participants By Region (Minimum 100 Net mmboe Global Deepwater)

| Page 15

Petronas Eni Marathon Hess

Reliance ExxonMobil Murphy Petrobras

Shell Helix RWE-Dea Petronas

Woodside Hess Shell Shell

Marathon StatoilHydro StatoilHydro

Marubeni Total Total

Murphy UK

Nexen

Petrobras

Shell

StatoilHydro

Total

Woodside

Global Deepwater Reserves in Known Discoveries

6,000

9,000

12,000

15,000

mmboe

West Africa

Asia-Pacific

North Atlantic

Mediterranean

Brazil

Mean Net Deepwater Reserves by Region

(Minimum 100 Million BOE)

Deepwater Reserves: All Companies

| Page 16

While nearly 40 companies have net deepwater reserves exceeding 100 mmboe (originally recoverable)…

0

3,000

6,000

Petrobras

StatHydroBP

Shell

ExxMob

Chevron

TOTAL

Eni

Reliance

Petronas

Hess

Anadarko

Woodside

BG

ConPhil

Marathon

Murphy

Sinopec

BHP

RWE-Dea

Devon

CNOOC

NNPC

GdF

DONG

Idemitsu

ATP Oil

Marubeni

Nexen

Helix

Niko

Repsol

E.ON

Petrogal

SAPCO

CNR

Famfa

Gulf of Mexico

Global Deepwater Major Players

9,000

12,000

15,000

mmboe

West Africa

Asia-Pacific

North Atlantic

Mediterranean

Brazil

Mean Net Deepwater Reserves by Region: Tier One Competitors

(Over 1.0 Billion BOE)

Deepwater Reserves: Tier 1 Competitors

| Page 17

0

3,000

6,000

Petrobras

StatHydro

BP

Shell

ExxMob

Chevron

TOTAL

Eni

Reliance

Petronas

Brazil

Gulf of Mexico

…only ten have net deepwater reserves exceeding 1 billion boe (originally recoverable); these competitors tend to have deepwater reserves in more

than one geographic region, although a single region is typically dominant.

Global Deepwater Remaining Reserves

Deepwater Reserves: Tier 1 CompetitorsRanking By Portion of Remaining Portfolio

9,000

12,000

15,000

mmboe

80%

90%

100%

Mean Net Deepwater Reserves: Remaining vs Produced

| Page 18

0

3,000

6,000

Petrobras

StatHydro

BP

ExxMob

Chevron

Shell

TOTAL

Reliance

Eni

Petronas

50%

60%

70%

Remaining Produced % Remaining

While net volumes vary considerably across the sample of ten Tier 1 companies, for each company, remaining (yet-to-be produced) reserves

account for the bulk (60% or more) of total original volumes.

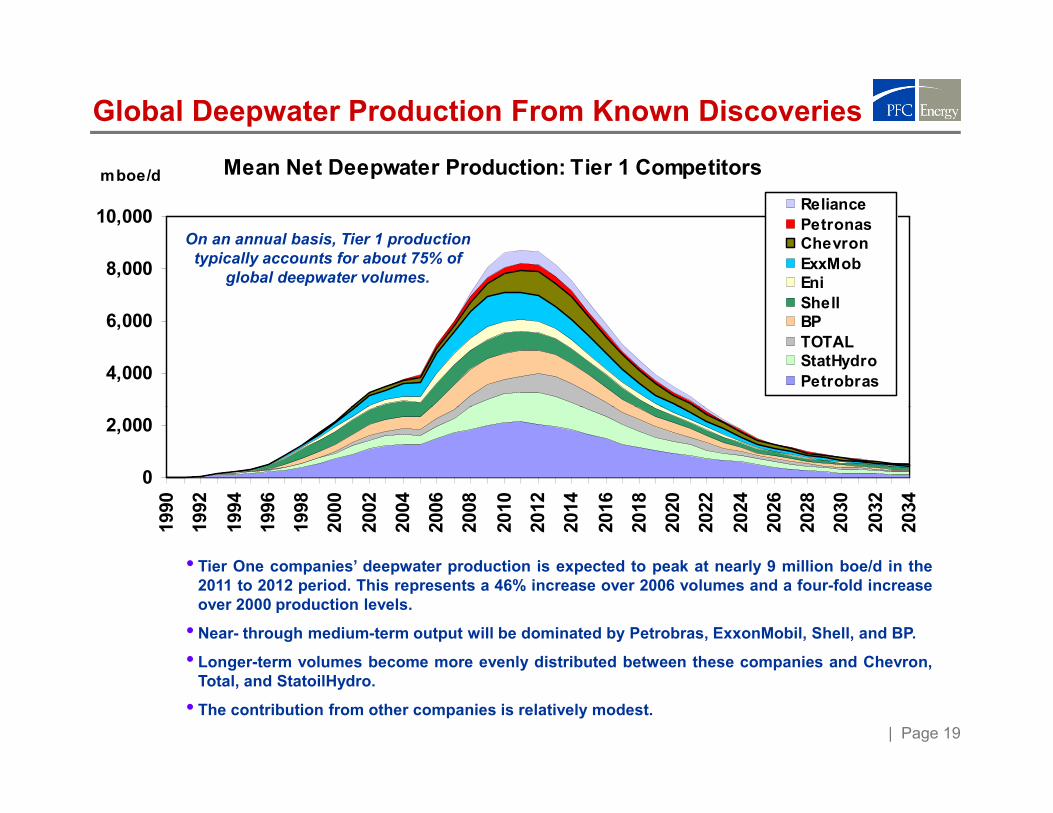

Global Deepwater Production From Known Discoveries

4,000

6,000

8,000

10,000Reliance

PetronasChevron

ExxMobEni

ShellBP

TOTALStatHydro

Petrobras

mboe/d Mean Net Deepwater Production: Tier 1 Competitors

On an annual basis, Tier 1 production typically accounts for about 75% of

global deepwater volumes.

| Page 19

0

2,000

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

• Tier One companies’ deepwater production is expected to peak at nearly 9 million boe/d in the2011 to 2012 period. This represents a 46% increase over 2006 volumes and a four-fold increaseover 2000 production levels.

• Near- through medium-term output will be dominated by Petrobras, ExxonMobil, Shell, and BP.

• Longer-term volumes become more evenly distributed between these companies and Chevron,Total, and StatoilHydro.

• The contribution from other companies is relatively modest.

Global Deepwater Competition Service

Deepwater Reserves & Capex: Tier 1 Competitors

Net Capex vs Net Oil & Gas Reserves

20,000

30,000

40,000

50,000

Net Capex ($mm)

Petrobras

BP

StatoilHydro

Shell

ExxMobTotal

Chevron

| Page 20

Comparative spending is commensurate with relative volumetric positioning.

0

10,000

20,000

0 3,000 6,000 9,000 12,000 15,000

Net Capex ($mm)

Net Reserves (mmboe)

ChevronEni

ReliancePetronas

Net Cash Flow: Tier 1 Competitors

Global Deepwater Net Cash Flow

0

30,000

60,000

90,000

120,000

150,000

180,000

$mmWest Africa

Asia-Pacific

North Atlantic

Mediterranean

Latin America

Gulf of Mexico

Mean Net Cash Flow by Region ($50 Oil)

| Page 21

Deepwater Portfolio Net Cash Flow

Global NCF Range ($50 Oil): $11.4 billion to $177.2 billion

Note: Results are based on full cycle data (includes exploration and appraisal spending).

0

Petrobras

BP

Shell

ExxMob

Chevron

StatHydro

TOTAL

Eni

Reliance

Petronas

As is the case with reserves, for Tier 1 competitors a single region is often dominant with respect to Net Cash Flow.

Net NPV10: Tier 1 Competitors

Global Deepwater Value

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

$mmWest Africa

Asia-Pacific

North Atlantic

Mediterranean

Latin America

Gulf of Mexico

Mean Net NPV10 by Region ($50 Oil)

| Page 22

Deepwater Portfolio NPV10

Global NPV10 Range ($50 Oil): $3.6 billion to $31.0 billion

Note: Results are based on full cycle data (includes exploration and appraisal spending).

0

Petrobras

BP

Shell

ExxMob

Chevron

StatHydro

TOTAL

Eni

Reliance

Petronas

As is the case with reserves, for Tier 1 competitors a single region is typically dominant with respect to NPV10.

Global Deepwater Competition Service

Comparative Net Cash Flow: Tier 1 Competitors

• Total NCF for Tier Onecompanies’ deepwaterdevelopments is projected to reach$42 billion in 2012.

• On a cumulative basis, the grouplikely reached payout (positivecumulative NCF) in 2003.

• For the typical Tier One-10,000

0

10,000

20,000

30,000

40,000

50,000

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

Reliance

EniPetronasChevronTOTALStatoilHydroPetrobras

ExxMobShellBP

$mm

$Bn

Global Deepwater Portfolio Net Cash Flow: Tier One Competitors

| Page 23

Note: Assumes $50 oil

• For the typical Tier Onecompany (as measured on amedian basis), cumulative NCFassociated with deepwaterprojects reached a negative $1.1billion in 1998, with payout likelyoccurring in 2004.

• Among all Tier One competitors,only Reliance (with a relatively newdeepwater portfolio) has yet toreach both maximum negative NCFand payout.

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

Maximum Cumulative Development Portfolio Net Cash

Flow vs Payout Timing

1996

1998

2000

2002

2004

2006

2008

2000 2002 2004 2006 2008 2010 2012

Maximum Negative CNFC

Payout (Year)

BPExxMob

Shell

Chevron

Median

Eni

TOTAL

StatoilHydroPbras

Reliance

Petronas

Table of Contents

| Page 24

� Overview of Fundamentals – Long Term Supply and Price Implications

� Significance of Deepwater Oil and Gas in Upstream Portfolios

� Deepwater Rig Supply and Demand – Implications for Future Day Rates

� Drilling Activity Forecasts

Rig Fleet Status – New Builds 2008-2011

| Page 25

PFC Energy’s Unique Solution: Integrated Supply –Demand Model for Offshore Drilling Rigs

DAY RATE FORECAST BY DAY RATE FORECAST BY

Development Well Forecast

Development Well Forecast

Oil and Gas Supply Forecasts

Oil and Gas Supply Forecasts

E&P Spending Forecast

E&P Spending Forecast

IOC/NOC Portfolios and Strategies

IOC/NOC Portfolios and Strategies

Exploration Well Forecast

Exploration Well Forecast

New Source Project Models

New Source Project Models

Historical Historical utilization and

Actual Contracted Actual Contracted

Rig Demand

DAY RATE FORECAST BY DAY RATE FORECAST BY

Development Well Forecast

Development Well Forecast

Oil and Gas Supply Forecasts

Oil and Gas Supply Forecasts

E&P Spending Forecast

E&P Spending Forecast

IOC/NOC Portfolios and Strategies

IOC/NOC Portfolios and Strategies

Exploration Well Forecast

Exploration Well Forecast

New Source Project Models

New Source Project Models

Historical Historical utilization and

Actual Contracted Actual Contracted

Rig Demand PFC Energy’s Added Value

| Page 26

DAY RATE FORECAST BY WATER DEPTH AND REGION

DAY RATE FORECAST BY WATER DEPTH AND REGION

Actual/Forecast Rig Count

by Water Depth and Location

Actual/Forecast Rig Count

by Water Depth and Location

New Build ProgramsNew Build Programs RetirementsRetirementsUpgradesUpgrades

Historical utilization and

day rate algorithms

utilization and day rate algorithms

Relocation and switching:Arbitrage algorithms

Relocation and switching:Arbitrage algorithms

Actual Contracted Rigs and

Contracted Rates

Actual Contracted Rigs and

Contracted Rates

Rig Supply

DAY RATE FORECAST BY WATER DEPTH AND REGION

DAY RATE FORECAST BY WATER DEPTH AND REGION

Actual/Forecast Rig Count

by Water Depth and Location

Actual/Forecast Rig Count

by Water Depth and Location

New Build ProgramsNew Build Programs RetirementsRetirementsUpgradesUpgrades

Historical utilization and

day rate algorithms

utilization and day rate algorithms

Relocation and switching:Arbitrage algorithms

Relocation and switching:Arbitrage algorithms

Actual Contracted Rigs and

Contracted Rates

Actual Contracted Rigs and

Contracted Rates

Rig SupplyReadily Available

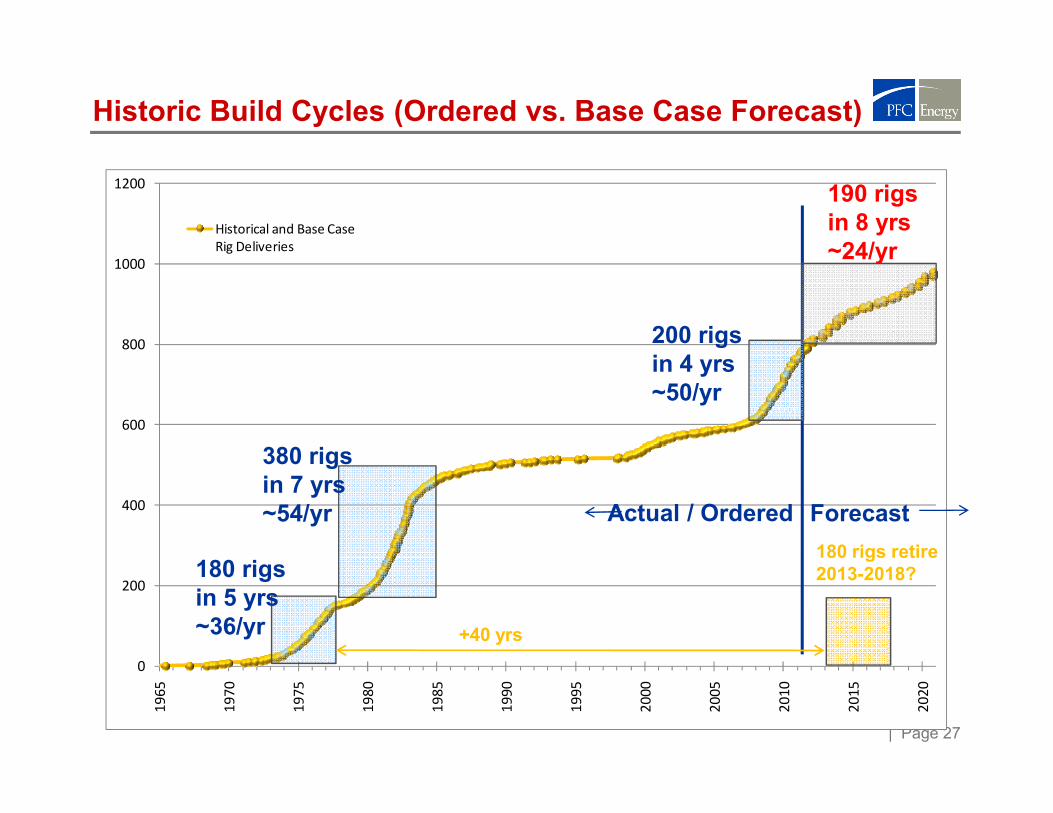

Historic Build Cycles (Ordered vs. Base Case Forecast)

800

1000

1200

Historical and Base Case

Rig Deliveries

200 rigs in 4 yrs ~50/yr

190 rigs in 8 yrs ~24/yr

| Page 27

0

200

400

600

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15

20

20

380 rigs in 7 yrs ~54/yr

180 rigs in 5 yrs ~36/yr

Actual / Ordered Forecast

180 rigs retire 2013-2018?

+40 yrs

Table of Contents

| Page 28

� Overview of Fundamentals – Long Term Supply and Price Implications

� Significance of Deepwater Oil and Gas in Upstream Portfolios

� Deepwater Rig Supply and Demand – Implications for Future Day Rates

� Drilling Activity Forecasts

Projected Well Counts: West Africa

| Page 29

Projected Well Counts: Asia

0

50

100

150

200

250

300

350

Nu

mb

er

of

We

lls

Well Count 2000-2018 | Indonesia

Deep

Shallow

0

50

100

150

200

250

300

350

Nu

mb

er

of

We

lls

Well Count 2000-2018 | India

Deep

Shallow

| Page 30

0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

0

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

0

50

100

150

200

250

300

350

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Nu

mb

er

of

We

lls

Well Count 2000-2018 | Malaysia

Deep

Shallow

Projected Well Counts: Brazil

| Page 31

Deepwater Wells w/o Contracted Rigs, 2010-2014

60

80

100

120

140

160

| Page 32

0

20

40

Che

vron

She

ll

BP

TOTA

LEx

xonM

obil

ONGC

Pet

rona

sPet

robr

asCon

ocoP

hillips

Hes

sRel

ianc

e

San

tos

Mur

phy

Asia Pacific West & South Africa Brazil

Strategic Advisors in Global Energy

PFC Energy consultants are present in the following locations:

� Bahrain

� Beijing

� Buenos Aires

� Calgary

� Houston

Main regional offices:

Asia

PFC Energy, Kuala LumpurLevel 27, UBN Tower #21

10 Jalan P. Ramlee

50250 Kuala Lumpur, MalaysiaTel (60 3) 2172-3400

Fax (60 3) 2072-3599

Middle East

PFC Energy, BahrainManama Center

Entrance 4 - Office 705

Kingdom of Bahrain

Tel (973) 1721-5106 Fax (973) 1721-5108

� Houston

� Kuala Lumpur

� Lausanne

� London

� Mumbai

� New York

� Paris

� San Francisco

�Washington, D.C.

North America

PFC Energy, Washington D.C.1300 Connecticut Avenue, N.W. Suite 800

Washington, D.C. 20036, USA

Tel (1 202) 872-1199

Fax (1 202) 872-1219

PFC Energy, Houston4545 Post Oak Place, Suite 312

Houston, Texas 77027-3110, USA Tel (1 713) 622-4447

Fax (1 713) 622-4448

Europe

PFC Energy, France19 rue du Général Foy

75008 Paris, France

Tel (33 1) 4770-2900

Fax (33 1) 4770-5905

PFC Energy International, Lausanne19, Boulevard de la Forêt1009 Pully, Switzerland

Tel (41 21) 721-1440

Fax: (41 21) 721-1444

www.pfcenergy.com | [email protected] regional offices are shown in blue.