decision making from a management … · decision making from a management accounting perspective...

TRANSCRIPT

1

DECISION MAKING FROM A MANAGEMENT ACCOUNTINGPERSPECTIVE INCORPORATING ENVIRONMENTAL CONSIDERATIONS:

A SOUTH AFRICAN CASE STUDY

Margaret J Nieuwoudt (School of Accountancy, University of Pretoria, South Africa)Greg J Plant (School of Accountancy, University of Pretoria, South Africa)Mike N Nieuwoudt (Independent mechanical design contractor)

2

DECISION MAKING FROM A MANAGEMENT ACCOUNTINGPERSPECTIVE INCORPORATING ENVIRONMENTAL CONSIDERATIONS:

A SOUTH AFRICAN CASE STUDY

ABSTRACT

This case study entails the consideration of environmental issues in the decision makingprocess and reflecting on the perceptions as to the quantum of the environmental costsincurred.

KeywordsManagement accounting, decision making model, environmental costs, capital budgeting

3

INTRODUCTION AND METHODOLOGY

Businesses should not regard themselves as operating in a vacuum, but should ratherview themselves as being part of society (The South African Institute of CharteredAccountants (SAICA), 1997). They are therefore accountable to their stakeholders thatinclude employees and the broader community (Association of Chartered CertifiedAccountants (ACCA) 1999; De Villiers 1999). Business decisions that impact on theenvironment should therefore be transparent and supported by a decision-making processshowing due care and consideration to minimising environmental risks and potentialfuture costs. The cornerstone of environmental legislation in South Africa is the SouthAfrican National Environmental Management Act (NEMA 1998). This has its origins inthe Bill of Rights contained in the Constitution (1996) that guarantees the right to anenvironment that is not harmful to a person’s health and well being, as well as theprotection of the natural environment.

The underlying principles of environmental law are the polluter pays-principle and theprecautionary principle (Kidd 1997; Frangos 1999). These principles indicate theexistence of a potential legal liability when making decisions involving the environment.By being transparent when making decisions as well as investing in environmentally safeprocesses, businesses will minimise legal actions against them as well as liabilitiesemanating from prosecutions.

The main focus and issue of this paper is to obtain insights into the decision makingprocess and how the environment is (or is not) taken into consideration when a capitalinvestment decision is undertaken. Secondly, and secondary to the main focus of thepaper, an attempt is made to establish perceptions as to the “true” environmental costsincurred on the project. The issues raised above will be addressed through an analysis ofa real-life situation (a case study). Briefly, this case study involves the expansion of afacility and simultaneously making the facility more environmentally friendly.

Notwithstanding the fact that a case study approach limits the generalisation ofconclusions to all businesses, greater clarity and insight are obtained regarding the issueswhich pertained to the decision and the impact thereof on the manner in which thedecision was arrived at. Humphrey and Scapens (1996) indicate a lack of objectivitywhen using a case study approach. They indicate that case studies representinterpretations by the researcher as to the nature of the organisation or social “reality”and thus no researcher can claim to provide an objective assessment of events. Parker andRoffey (1997) in referring to the literature regarding methodology themes and the use ofcase studies, suggest that case studies represent one distinct methodology (groundedtheory) for generating theories that offer the prospect of reflecting some of thecomplexity and richness of the environments within which accounting and managementare practiced. They furthermore indicate that the researcher, rather than commencing witha theory which he or she attempts to verify, commences with an area of study and allowrelevant theoretical constructs to emerge from the process of study. After havingidentified the relevant area of study, Humphrey and Scapens (1996) note that atheoretical framework is regarded as the essential starting point for any case study beingundertaken. They conclude furthermore that the case study is an issue-driven, problemsolving approach for developing socially informed theories of accounting practice.

4

In applying a case study approach, the following strategy, based on the works ofHumphrey and Scapens (1996), Parker and Roffey (1997) and Nieto and Pérez (2000),has to be followed:1. Identify a research area / phenomenon2. Compile a theoretical framework3. Gain evidence through various techniques4. Analyse the evidence5. Make deductions regarding the phenomenon which might be the start of a emerging

theory

The research areaIn the case study in question, the research area is the consideration of environmentalissues in the decision making process and reflecting on the perceptions as to the quantumof the environmental costs incurred.

The theoretical framework for addressing the decision making processThe theoretical framework used as point of departure for addressing the research area inquestion is the decision making process referred to in the works of various authors (Drury,2000; Harrison and Pelletier, 2000; Chartered Institute of Management Accountants(CIMA), 1999; Neale and Pike, 1992; Hastings, 1996):

1. The identification of objectives and possibly the resetting of objectives2. Searching for possible alternative courses of action3. Identifying the states of nature which could affect the outcome of the decision

being made/constraints4. Evaluating the alternatives5. Selecting a course of action and implementing the choice6. Assessment of the choice

EvidenceOne of the authors, a mechanical engineer, was a member of the design team involved indesigning the new facility, and thus had access to all evidence regarding the projectwhich was required in carrying out the case study. He was furthermore the link betweenthe project team and management, and the other two authors. The latter mentionedauthors gathered evidence by means of interviews using two open-ended questions: How did the decision making process unfold, taking (or not taking) environmental

factors into account? What portion of the costs incurred on the project was incurred in respect of the

environment (testing quantification perceptions)?

Answers to these questions were obtained from the project and design team. The projectand design team consisted of a number of independent sub-contractors. This enhanced theobjectivity of the information gathered.

Authorisation for disclosing information in the case study regarding the process used(technical detail) and the decision making process applied, was sought from allstakeholders involved. However limitations were imposed on the disclosure ofinformation relating to the details of the process and the information generated by theprocess as these pose a trade risk.

5

Analysing the evidence and making deductions from the evidenceIn analysing the evidence, accounting researchers should seek explanations with regard tothe research phenomenon, as to what factors influenced it, how and why (Nieto and Pérez,2000; Parker and Roffey, 1997) to reflect some of the complexity and richness withinwhich accounting and management are practiced.

BACKGROUND TO THE CASE

The De Beers Kimberley Acid Laboratories (hereafter referred to as KAL) resorts underthe Geology Division and is located outside Kimberley in the Northern Cape. The facilityis used mainly for the treatment and analysis of geological samples from existing mines,potential new mines, and third party clients. The main purpose of this facility is thegeneration of information ranging from exploration information to informationfacilitating efficient mine management.

The KAL has been operational for thirteen years, and is in its present form, licensed bythe Department of Environmental Affairs and Tourism (DEAT) to process geologicalsamples with Hydrofluoric Acid (HF), Hydrochloric Acid (HCl) and other hazardousmaterials. These acids on their own and when mixed are dangerous. HF is known to belife threatening if not controlled properly. These acids and materials are stored on site insufficient quantities for process requirements.

Stringent operating procedures and full-suit protective clothing have ensured an enviablesafety record and no serious incidents that posed a threat to the safety of personnel or tothe environment were experienced during the period of operation according tomanagement. Regular monitoring of the air quality and ground water quality isundertaken to ensure that pollutant levels remain within the levels allowed by the site-operating license.

THE LITERATURE REVIEW REGARDING THE DECISION MAKINGPROCESS

Businesses are confronted with a plethora of objectives that need to be met (Drury, 2000;Samuels et al 1995). These objectives range from satisfying the economic objective ofmaximising profit to social and environment objectives. The existence of such multipleobjectives however is problematic. The economic objective of maximising profit is inconflict with the social and environmental objectives (Gray, 2000; Smith and Labell1997; Seitz and Ellison, 1999). Decision-making would therefore result in a trade-offbetween these objectives, as all cannot be satisfied to the same extent.

As a result of the diversity of the objectives considered, and the strategies that need to bedevised in order for the business to achieve them, various authors call for a multi-disciplinary approach to be applied by businesses when making decisions (Boyce 2000;Putterill, Maguire and Sohal, 1996).

Strategic decisions should be made in ways that are heedful and mindful of the differentconstraints that can have an affect on the successful outcome of the decision (Harrisonand Pelletier, 2000). They indicate that the success of the decision will also depend on theset of management attitudes towards the process and the decision.

6

Any strategic decision to be taken involves relating the position of the business currentlyto the opportunities and threats in the external environment (Harrison and Pelletier, 2000).Implicit in this would be the identification of the constraints that will impact on orhamper the success of the outcome of the decision being considered. This process resultsin strategies being formulated to address objectives set and taking in account thelimitations posed by the internal and external environments (Hastings, 1996). Decisionmakers can be limited by certain factors that exist in the external environment, namelyeconomic constraints, socio-political factors and technology as well as by other factors ofan internal nature namely imperfect information, time, cost constraints and cognitivelimitations. Given these limitations, decision makers have to exercise judgement ratherthan computations in satisfying the outcomes of the decision.

When considering long-term decisions, one must refer to the capital budgeting processwhich is very similar to the process indicated in the theoretical framework set out earlier(Drury, 2000; Chartered Institute of Management Accountants (CIMA), 1999; Neale andPike, 1992). In addition to the planning process that precedes the investment decision, theevaluation of the capital investment, the authorisation of the project and the post-implementation audit of the decision, are highlighted.

A great deal of attention in the literature is placed on the financial evaluation of thedecision being made (Drury, 2000; Samuel et al., 1995; Chartered Institute ofManagement Accountants (CIMA), 1999; Neale and Pike, 1992; Prendergast, 1998;Hastings, 1996; Putterill, Maguire and Sohal, 1996; Maccarrone, 1996; Neale and Letza,1996). Various models are identified which can be used which include net present value(NPV), internal rate of return (IRR), modified internal rate of return (MIRR), paybackand accounting rate of return. Hastings (1996) indicates that additional criteria such asmeasuring flexibility, throughput and customer satisfaction should also be considered.

As Neale and Letza (1996), there appears to be a pre-occupation with such evaluationmodels in academic research in trying to determine the most optimal method ofevaluating projects. This they termed “misplaced emphasis”. They note however that inrecent research, it would appear that the realisation has come about that the decisionmaking which will have long term implications, in other words capital budgeting, is farmore complex than merely focusing on the financial appraisal of the project.

Resultantly, deviations from using complex financial models for the purpose of strategicplanning as well as decision-making have been observed. Dunk (1999), in referring to theworks of various academics, cites the investment appraisal systems utilised by manycompanies as significantly handicapping the making of investments in new technologies,which inevitably results in the companies not realising their competitive advantage. Thisview is supported by Drury and Tayles (1997). Traditional financial appraisal techniquesapplied when evaluating a project tend to be biased towards the short-term. FurthermoreDunk (1999) concludes that a short-termistic approach to cost cutting, can havedetrimental effects on the long-term performance of the company.

The conventional management accounting wisdom underpinning these financial appraisaltechniques is deeply entrenched in neo-classical economic theory that advocates profitmaximization and efficiency in the allocation of resources (Shotter 2000). According to

7

Shotter (2000), a number of these neo-classical economic assumptions are now beingquestioned by economists and academics.

Bromley (2000) criticises decisions based solely on financial models as they do notinclude other “truth rules” such as fairness, prudence, honesty, loyalty, expediency, cost-effectiveness and practicality, to name but a few. He suggests that decisions are based onsentiment as well. Sentiment is the application of reason to choice and action, where thereasons for choices made are the result not of computations performed but rather dueconsideration. According to Bromley (2000), taking cognicance of all of this could eludeone to think that the words of Frank Ramsey ring true, namely that the world has beeninhabited by people, who can calculate but do not think. Gouws and Lucouw (1999)agree that models on their own do not provide information, but rather due considerationand theoretical underpinning also play a role.

Prendergast (1998) cites a number of real-life examples where large businesses hadattempted to evaluate projects on financial grounds but had failed abysmally. Heindicates the importance of project authorisation and that amongst others, independentconsultants should be used in this regard.

Gray (2000) too criticises businesses for basing decisions purely on the economicoutcome of the decision, disregarding sustainability from a social and environmentalimpact perspective.

Any decision being made, which will have a resultant impact on the environment,requires an appraisal to take place in terms of which the decision is evaluated in terms ofdiverse performance indicators, rather than indicators such as payback periods andreturns on investment (ACCA 1999). Such indicators are often non-financial in nature.

The final stages in the decision making process applicable to capital investment decisionsis the control phase (Drury, 2000; Chartered Institute of Management Accountants(CIMA), 1999; Neale and Pike, 1992). According to Drury (2000) two aspects areimportant: Obtaining approval for the implementation of the project prior to implementing it;

and Ongoing controls during and after development, over costs and ensuring that the

envisaged benefits have in fact materialised (in other words a post-implementation audit).

THE DECISION MAKING PROCESS ADOPTED IN THE CASE IN QUESTION

The authors attempted to address each of the initial three stages of the theoreticalframework in isolation but found that these stages were too interrelated to be addressedseparately.

IDENTIFICATION OF THE OBJECTIVES, ALTERNATIVES ANDCONSTRAINTSThe present facility has a capacity to treat up to 25 tons (using 8 digesters) of samplematerial per annum. As a result of a growth in demand for samples to be treated, thepresent capacity of the facility needed to be upgraded to 50 tons per annum (requiring 16

8

digesters), with a projected future processing capacity requirement of up to 75 tons perannum (requiring 24 digesters) being envisaged within two to three years. A delay in thetreatment of samples causes a delay in management information being made available,which result in a delay in making management decisions.

The company at this stage considered dealing with the project as a turnkey project. Apreliminary estimate of the cost to expand from the current 8 to the envisaged 16digesters by adding an additional 8 digesters was approximately ZAR2,5 million. Twooutside parties were approached to submit proposals for the design of the expansion. Atthat stage it became evident that two constraints existed. Neither party had the technicalcapacity to deliver a turnkey project on their own. Secondly, the concept of a turnkeyproject would not be feasible to due the project being of such a small scale in monetaryterms.

The objectives therefore had to be reassessed. Due to the complexities surrounding thehazardous materials involved, it was decided to form a multi-disciplinary project teamincluding the two outside parties initially approached. The project team consisted of - thedesign team, the client, the project sponsor and project manager (quantity surveyor withexpertise in the field of costing as well as relevant technical experience). The client, DeBeers Geological Division, requested a capital expansion. The project sponsor, De BeersCorporate Headquarters, would be the liaison between the client and the design team.

An environmental need was also identified in that the treatment of larger quantities ofsamples with the present facilities might lead to deterioration in environmental conditionsdue to scrubbing and effluent system overloads. It was further envisaged that the SouthAfrican legislated allowable environmental impact may be made more stringent in thefuture, and that any expansion must pre-empt this by meeting the latest internationalstandards.

The major constraint of the expansion project was that operation of the present facilitymay not be interrupted for more than one week during construction. The informationgained from treated samples has to flow uninterrupted for the reasons mentioned above.

The usual budgetary constraints applied initially, but were relaxed, as shown later in thispaper, to cater for the longer term good of the KAL and its environment. It is important tonote that when dealing with hazardous materials and installations, it is internationallyaccepted best practice to subject such installations to a hazardous operations study(HAZOP) prior to commencing construction of the installation. The design team wouldtherefore design the new facility with the HAZOP in mind. A HAZOP was performed atthe end of the preliminary design stage. It is important to note that the HAZOP wasrepeated at the end of the final design stage.

The objective of the HAZOP is primarily to address two issues – firstly the safety of theemployees in a facility such as the one in question, and secondly to consider theenvironmental impact.

9

As part of the HAZOP-study, the project team has to identify ways of dealing with theproblems identified. This can result in changes being recommended to the process design,which then requires a further HAZOP taking place.

During the aforementioned study, which takes approximately 2-3 days, an independentexternal facilitator is brought into the process. In the case in question, the facilitator is aspecialist who is versed in the nuclear and hazardous acid environment. It is thefacilitator’s task to work through the process design and critically evaluating it by posing“what if?” questions to the design team. At this stage the facilitator must know thestandards that they intend to use on meeting. The results of the HAZOP are documentedin formal records, which are kept. Any potential problems in the design are identified inthis process. It is fundamental to note that the costs of the project are determined at thisstage and are driven by the preliminary design and subsequent HAZOP. The premiumplaced on human and environmental safety is thus very evident. Another aspect that hasto be kept in mind, as the mechanical engineer stated, is that when working withhazardous installations and materials the choices are limited. This will have an impact onthe evaluation of the financial feasibility of the project. (The cost of the HAZOP studyand design costs which can be linked to the environment in terms of the definition givenlater in the paper, amounted to ZAR40 000 and ZAR150 000 respectively.)

The preliminary design is therefore prepared with the HAZOP as backdrop there to.Adequate measures have to be in place in the design, otherwise the HAZOP will indicaterisk areas, which will need to be addressed and require the project team to go back to thedrawing board. As a result, one can conclude that it is implicit that the cost of facility isdriven by the design of the facility, and that these costs can now be quantified for the firsttime. These costs would be used as a point of departure for capital budgeting purposes.

Taking the effects of the mixture of the two acids identified earlier into account, thetechnology and materials available, limited the amount of flexibility in the design of theplant. This lack of flexibility would thus contribute to the costs that would have to finallybe incurred in respect of the project.

The project team applied international standards as a benchmark during the designprocess, as it is expected that the existing South African environmental standards are toundergo significant changes in future.

The two areas where alternatives did exist were in the manner in which capacity was tobe expanded, and in the control of the digestion process that at present is a full manualoperation. To expand the capacity, the present facility could simply be duplicated for theimmediate need, with a further expansion, taking place at a later date for the projectedgrowth. However, the environmental targets would require an extensive upgrade of thepresent facility that would have required it to shut down operations for an extensiveperiod, again causing the sample backlog to accumulate.

The alternative was to plan a new processing building, housing the full compliment ofacid digestion equipment for the projected need. The present facility would be keptoperational until the new facility had been fully commissioned, after which processingcould be switched over to the new facility with the minimum loss of processing time. Thepresent building could then be decommissioned, and eventually used for other purposes.At the same time the envisaged building could be planned to bring in the lowering of the

10

present safety risks by separating different process areas to different floors, resulting in athree-level building.

The new facility could have been operated under the same manual procedures as thepresent facility, with the associated risks. The alternative of remote and/or automatedcontrol was however evaluated, partly to reduce operators’ safety risk and due to theincrease in the availability of control systems and equipment as a result of electronicrevolution. After evaluation of the benefits, risks and costs, a decision was made toimplement a remote control system utilizing PLC’s and front-end operator computers.This also made it possible to easily include several safety interlocks in the process.

A fully automated control system was however rejected on the basis of cost and the lackof flexibility for processing options that arise in a facility of this nature.

SELECTING A COURSE OF ACTION AND IMPLEMENTING THE CHOICE

The decision to expand the existing facility by erecting a new facility which would housethe full complement of 24 digesters, and which would comply with internationalenvironmental standards, was taken. The new sample acid processing facility for theKAL is presently under construction and is located adjacent to the present facility on thesame premises. The present facility is still processing at full capacity, and will do so untilfinal commissioning of the new facility.

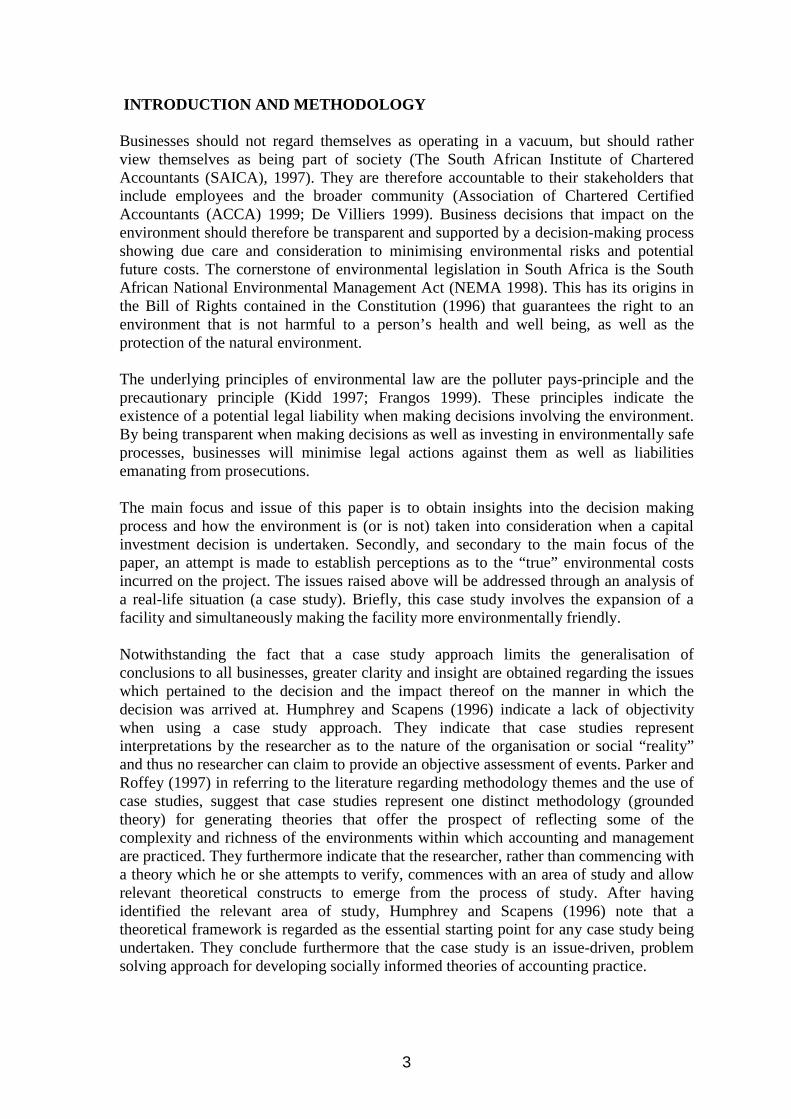

The new facility can best be described by means of a simplified operating flow diagram.There are six main functional areas to the facility, and these are identified in the overviewof the facility shown in Figure 1. These areas are the Acid Storage Facility, Water SupplySystem, Compressed Air Supply System, Processing Building, Fume Scrubbing System,and Effluent Treatment System.

Acid StorageNew tanks have recently been installed and are of sufficient capacity to meet theprojected requirements. These tanks are installed in bunded areas, which have sufficientcapacity to retain any acid spills from the tanks and to route such spills to the effluenttreatment system should they occur. These tanks are ventilated to the fume scrubbingsystem to ensure that no acid evaporation can be released directly to the atmosphere. Thepumps used to transfer acid to the process building are also inside the bunded areas, andare of the pressure control pneumatic diaphragm type that ensures the least risk of pumpfailure in the case of incorrect operating procedures being followed.

Water SupplyThe primary municipal potable water supply cannot be coupled directly on line to theacid processing facility. If HF acid comes in contact with the water, especially in no-flowconditions, it can migrate against the normal direction of flow and pollute other users ofwater on the premises. It is also necessary to always have sufficient water on hand tocounter acid accidents, and an interruption in the main water supply is always a

11

possibility. A 30 kiloliter water storage tank is thus used both to ensure sufficient water isalways on hand, and to act as a migration buffer to prevent accidental acid migration tothe primary water supply. An electrically driven pump and pressurisation accumulator,supplies water pressure to the facility.

The cost of isolating the water supply from the main municipal water supply amounted toapproximately ZAR10 000.

Compressed Air SupplyCompressed air is required for the agitation of the digestion process in the digestervessels, for driving the acid and effluent pumps and other acid related utility functions,for operating control valves and instruments for the remote functioning of the plant, andto supply breathing air to operating personnel in full protective suits. The same acidmigration danger however exists with compressed air lines as exists for the water supply.The acid utility and instrument / breathing air supplies were thus separated by using twodifferent compressor units. Being of a lower pressure but high flow regime, high-pressurefans (blowers) as a third air source supply the process air requirement.

ZAR50 000 was spent installing an additional compressor.

Process BuildingThe process building comprises three levels. The top level is used for the storage ofprepared samples to be digested. This floor is free of any acid or acid processing. Accessto this floor is via an external stairway and entrance. Samples are fed to the digestervessels on the center floor via sealable chutes before any acid is allowed into thedigesters.

The center floor houses the twenty four acid digester vessels, as well as a dual acidbatching system for loading the digesters with predetermined batches of HF and HCl acid.Each digester is also supplied with water for processing and rinsing. All acid containingvessels are connected via fume extraction ducting to the fume scrubbing system. The airin this volume is also continuously extracted via the scrubbing system at a rate of four airchanges per hour.

This area is the most likely to be exposed to hot acids and hot acid fumes, and personnelaccess is strictly controlled. The floors, walls and ceilings are protected against acidfumes and short duration acid spills to ensure long-term building integrity. A fullyequipped wet change room is used for changing into and out of protective clothing, and isthe only access route into and out of this processing area. An acid injury first aid room isadjacent to the wet change room and immediate treatment can be given to acid injuries.No access is normally required during the acid digestion cycle, which can last up to half aday. If personnel have to enter, they are fully clothed in fresh air supplied acid proof fullsuits. Personnel exiting this area always go through a decontamination safety shower toensure that no acid is transferred to other personnel areas.

12

Most of the remote control equipment and instrumentation is also found on this floor. Theprocess control room is situated in a separate room on this floor, but is isolated from theprocessing area. Access to the control room is via an external entrance.

The ground floor of the building houses twenty four fume cupboards in which thedigested samples from each reactor is individually sieved to retain the residual solids.The effluent goes directly from these cupboards into the effluent lines to the effluenttreatment system. Fume extraction to the scrubber is done from inside the cupboards. Byextracting from the cupboards the flow of air is always into the cupboards from the areawhere operating personnel stand. This secondary processing was previously done in anopen space in the old facility building, without the additional safety provided by fumecupboards. The building protection, access arrangements, and personnel safety clothingand equipment are the same as for the center floor.

ZAR460 000 was spent on making the process building safer and ZAR400 000 was spentimplementing the remote control facility.

Fume Scrubbing SystemThe fume scrubbing system was designed to scrub all fumes generated in the wholefacility. Though a cheaper water scrubber would have been good enough to meet presentlegislation, it was decided to erect an alkaline (20% KOH) packed bed scrubber capableof removing the worst case operating acid fumes to residual levels lower than thatrequired by the latest international standards. The scrubber is furthermore of a suck-through design to eliminate the possibility of leakage of unscrubbed fumes to theatmosphere. The scrubbing fan is mounted at ground level to ensure proper maintenanceand quick repairs if required. Scrubbed air is exhausted through a 14 meter high stack toensure thorough dispersal of the very small amounts of acid fumes that may still bepresent.

ZAR87 000 was spent on the installing of a more effective scrubbing system.

Effluent Treatment SystemThe effluent treatment system consists of effluent lines, the neutralisation system, and theevaporation ponds. The effluent piping transfers all effluents under gravity to theneutralising tank situated in a sunken sump. A premixed alkaline mixture of water andlime performs the neutralisation of effluent in the tank. The capacity of the neutralisingtank is sufficient to treat all effluent from a maximum operating day with spare capacityavailable for other possible incidents. No acid processing is allowed to take place unlessthe neutralisation system is ready to receive the expected volume of effluent.

A slightly more advanced neutralising facility was initially investigated. While theselected system still receives acidious liquids via the effluent piping over a distance ofapproximately 40 meters, the advanced system would utilize a ring feed circulating aKOH mixture to facilitate neutralisation at the point of effluent discharge from theprocessing equipment, giving the advantage of no acidious waste exiting the process

13

building. The disadvantage would however be an additional ZAR500 000 per year inoperating costs. Evaluations showed that the risk of the simpler system leaking effluentbefore neutralisation would be very low due to the short effluent line distance. Additionalmeasures were however taken to safeguard the effluent line against possible damage anddeterioration. The selected system can also be upgraded to a circulating system at a laterstage if the risk profile were to change.

After neutralisation, the content of the neutralising tank is pumped to the evaporationponds, where it is left for a sufficient period of time for the water to evaporate. The inertsolid dry waste is then removed from the pond to an approved waste site by truck. A thirdpond, presently under construction, expands the capacity of the two present evaporationponds. Once in operation, the two older ponds will be refurbished, and a fourth pond maybe added.

ZAR73 000 was spent on upgrading the evaporation ponds.

A SUMMARY OF THE CASE

The initial need identified was one of expansion and the primary constraint was that themanner in which such expansion was to take place should not interrupt the currentprocess by more than one week.

The following strategic factors played a role on the decision arrived at, as to whichalternative to implement. These were:

Production targets – the current production capacity was identified as beinginadequate to meet the future production demand requirements.

To minimise the extent of the interruption in production caused by any expansionor upgrading.

Risk management policy – by developing a more environmentally friendly facility,the company would be able to reduce its overall risk as well as environmentalprosecutions.

Regulatory reasons – the company had benchmarked the process at the KALagainst international standards. It was of strategic importance to the company thatthe Kimberley Plant complies with these standards. The existing/old plant alreadycomplied with South African standards. The need was identified to comply withthe international standards or best practices in anticipation of the South Africanstandards being amended at some point in time.

Societal awareness – an increasing awareness in South Africa and globally of theneed to conserve the environment and to limit the impact on the environment ofproduction processes.

The objectives identified would have a major impact on the different alternatives, themanner in which these were evaluated, and the final decision arrived at.

Various alternatives were identified to potentially address the objectives identified duringthe planning process:

14

Expanding the existing plant – a high premium was placed on the value of theinformation, which is the output of the process. It was estimated that the processwould have to be interrupted for a period of approximately 3 months, whichwould mean the resulting opportunity cost would be high.

Building a new plant that is safer for the employees and which would complywith international environmental standards. This alternative would pre-empt anychanges to South African legislation, which might take place in the foreseeablefuture with regard to allowable emission levels.

The importance of expanding production capacity as economically as possible with theleast interruption of the process, complying with international environmental standardsand improving the efficiency of the production process through the technology in use andmaking it safer, meant that the alternative to merely expand the present facility would nothave achieved the objectives identified.

The following environmental improvements in contrast to the existing process, were builtinto the new facility design: Making the process safer by limiting human involvement which could be

addressed by implementing a remote control system, which by implication wouldmean the environmental clean-ups would be easier and that human health riskswould be limited;

Improving the air supply, both for human purposes and for the productionprocess;

Isolating the water supply from the main municipal water supply; and Address the pollution caused by the production process in the form of effluent

emitted and the emission of acid fumes.

The mindset of management changed from the initial objective to merely expand thecurrent facility to finally erecting a new standalone facility. This change came about as aresult of the preliminary study and design that indicated the initial objective was notfeasible regarding: The time required to shut down the existing plant for upgrading, which would

take 3 months; and Projections that a further incremental expansion would be required in the short

term.

The project team and client settled for a long-term approach. They opted for the moreexpensive alternative which would not only result in an increase in capacity, but also animprovement in the technology used and the process becoming more environmentallyfriendly. A potential trade-off between saving costs on the one hand, and not achievingthe strategic objectives identified on the other, was averted.

The decision to invest was based on the budget for the additional expansions andimprovements being authorised. The base case budget was adjusted for the cost of theincremental expansion and improvements to safety and environmental aspects of thefacility. These adjustments were negotiated with De Beers Corporate Headquarters andthe adjusted budget, within which the team then had to operate, was approved. It is ouropinion that the project team and client could motivate the acceptance of the decisionwithout performing a formal financial appraisal based on an appraisal model due to: the size of the project in monetary terms; and the strategic objectives which had been formulated.

15

During the design and construction phases, controls were in place which ensured that theteam would seek approval from management prior to going ahead with any changes todesign specifications; and in instances where budgeted costs were going to be exceeded.

Before signing off the project, it is the responsibility of the quantity surveyor on the teamto prepare a final report in which the budgeted costs and actual costs of the project arecompared. This is therefore a further control measure in place.

Once the plant becomes operational, the opportunity exists for management to perform apost-implementation audit or review of the project to ensure that the objectives identifiedhave in fact been achieved.

ENVIRONMENTAL COSTS

No generally accepted definition for the term environmental accounting or environmentalcosts exists (Public Accounts and Estimates Committee 1998; ACCA 1999). As this partof the case study relates to perceptions, we asked the design and budget group to estimatewhat percentage of the total costs were environmental costs. The estimates variedbetween 20% and 65% depending on what their perception of an environmental cost was.The one extreme of the range, based on the concept that basically all the costs relate tothe environment and are capable of being classified as an environmental cost as these aredictated by environmental law and good practice. This was the perception of themechanical engineer. The other extreme of the range was that environmental costs andprocess costs need to be separated. The project manager, a quantity surveyor, concludedthat the use of costing information would become less reliable and less useful tomanagement if these two costs were not treated separately. Both the mechanical engineerand the quantity surveyor agreed that the concept of environmental cost should bedefined in order to be able to assess the cost thereof. The information obtained from theliterature study conducted was bounced off the mechanical engineer and the quantitysurveyor to obtain their perceptions and to be able to propose an acceptable definition.

LITERATURE STUDY VERSUS PERCEPTIONS OF THE MECHANICALENGINEER AND THE QUANTITY SURVEYOR

Excluding social (external) costsAccording to Howes (1999) defining what constitutes an environmental cost, may proveproblematic if external costs are taken into account. Social costs are the values placed onthe externalities (pollution) and thus represent the monetary value of harm done to theenvironment. Gray, Owens and Maunders (1987) warn that there is a large element ofsubjectivity in determining what, is to be included in social costs. Given this element ofsubjectivity, the value will be based on the judgement of the measurer. At this stage it isimportant to differentiate between external costs and internal costs. External costs arecosts to society (also called social costs) for which no compensation exists. It is a freegood to the business in the absence of any payment for pollution. Internal costs are thosecosts paid for.

Both the mechanical engineer and the quantity surveyor agreed that there is a differencebetween reporting to management and reporting to the public. When reporting tomanagement, the issue will be to only report on internal costs, namely costs paid for.

16

Internal environmental costs (excluding regulatory costs)Environmental costs according to Ansari et al (1997) are both regulatory and voluntarycosts incurred to control, assess, prevent and correct failures from actions that potentiallyhave an adverse impact on human, animal or plant life. They include pollutants in the air,soil and water.

According to the quantity surveyor, in the case of the project in question, the process hadto be licensed before it would be allowed to operate. Without a licence, no operationswould in other words be possible. As the current operations are licensed, the operationscomply with local standards. Only voluntary costs should be regarded as environmentalcosts. The mechanical engineer disagreed with the above and shared Ansari et al’s viewsthat regulatory costs should also be included.

AllocationAccording to Schaltegger and Müller (1997), the identification of environment-relatedinternal costs poses few problems, as long as these costs are solely for the purpose ofenvironmental protection. The following is a summary of Schaltegger and Müller'sviews:

• The identification of environment-related internal costs poses few problems, as long asit is solely for purposes of environmental protection. Such is the case with "end-of-pipe" technologies, which are clean-up devices installed after the core productionequipment. Scrubbers and waste treatment plants are typically examples, which canhelp concentrate toxic substances and/or reduce toxic impacts.

• The identification and measurement of environment-related costs is much moredifficult with regard to "integrated technologies" (also called "clean technologies").These are more efficient production technologies that reduce pollution at source,before it occurs (e.g. new equipment that uses 50% less energy and creates 20% lesstoxic effluents than the old). Environmental issues were already integrated when theequipment was developed. Because of this, the following question arises: what part ofthe equipment (assets) and the maintenance expenditure is environment driven? Themain criterion for answering this question is the cost difference in relation to theenvironmentally next (less) favourable solution.

• However, the costs should not be considered environment-related if the integratedtechnology is simply current state of the art, and has been installed for no other reasonthan the routine replacement of old equipment.

The quantity surveyor agreed whole-heartedly with Schaltegger and Miller’s views. Thisimplies that the incremental costs incurred in making the facility safer andenvironmentally friendly can be regarded as a “true” environmental cost.

New environment cost classification and allocation of these costsEnvironmental costs to be used for management decisions for this project are defined asonly being:• Internal costs (costs paid for);• Only voluntary costs are taken into account (the cost of complying with existing

regulatory standards are regarded as process costs);

17

• The identification and measurement of the environmental costs will be based on thecost difference in relation to the environmentally next (less) favourable solution;

• Incremental cost incurred to control, assess, prevent and correct failures thatpotentially have an adverse known impact on the environment; and

• The routine replacement of old equipment will not be regarded as environmental costs.

Environmental costs according to Ansari et al (1997) can be classified according towhether they were incurred so as to comply with regulations (known as compliancecosts) or whether they were incurred in terms of the initiative of the entity to creategoodwill or to satisfy societal requirements (known as voluntary costs). In the case of thecompany concerned, the existing plant already complied with local standards. Theadditional environmental costs incurred can therefore be seen as being voluntary innature as the company voluntarily decided to make the facility safer and to comply withthe stricter international standards.

IDENTIFICATION AND MEASUREMENT OF ENVIRONMENTAL COSTS

The environmental costs can now be allocated by applying activity based costingprinciples as recommended by Ansari et al (1997). Total quality management (TQM)recommends the same approach when reporting on costs incurred to establish qualitywithin a business (Drury, 2000). This approach involves identifying and reporting on theprevention costs, appraisal costs, internal failure costs and external failure costs. A directlink or causal relationship must therefore exist between the cost incurred and the activityto which it is allocated. The following is an allocation of the capital outlay directlyattributable to the environment that the company in question incurred (in South AfricanRand (ZAR)):

Assessment Prevention Control FailureHAZOP’sDesign costsCompressed air supply – additionalcompressorWater supplyBuildingRemote control facility costScrubbing systemEffluence system

40 000150 000

50 00010 000

460 000400 000

87 00073 000

Total cost 40 000 1 070 000 160 000 0

The final approved budget was set at ZAR6 million.

Discussion of the different environmental costs incurred

Assessment costsThe assessment costs in this case only comprised the ZAR40 000 spent on the HAZOPsessions held.

Prevention costsThe prevention costs are considered to be those costs incurred in making the processmore environmentally friendly and less hazardous. They are the costs incurred in thefollowing areas of the process: Compressed air supply – where ZAR50 000 was spent installing an additional

compressor.

18

Acid storage – since this part of the plant had been upgraded three years prior tothe current upgrade, this section of the plant is to be taken over without any majormodifications.

Water supply – ZAR10 000 was spent isolating the water supply from the mainmunicipal water supply.

Process building – the following was spent: ZAR300 000 was spent splitting the process into three floors so as to

minimize environmental risks; ZAR60 000 was spent on the acid proofing of the process building; ZAR20 000 was spent on emergency showers; ZAR80 000 was spent on ventilation to regulate the air flow in the process

building as the existing system would not have resulted in compliancewith standards; and

ZAR400 000 was spent installing the remote control facility so that humaninvolvement in certain parts of the digestive process could be eliminated.

Control costsThese were the costs incurred to control the hazardous materials emanating from theprocess, namely the pollutants.

Scrubbing system – ZAR87 000 was spent on installing a more effectivescrubbing system.

Effluent system – ZAR73 000 was spent on upgrading the evaporation ponds.

External failure costsNo external failure costs have to date been incurred since the plant is firstly not yetoperational and secondly one would expect with the given expenditure on assessment,prevention and control costs, that failure costs would be kept to a minimum.

The aforementioned costs were all capital in nature. No change in operating costs whichcan be attributed to the environment will take place. The expected increase in theoperating costs of the plant, can be ascribed to an increase in production volumes and aretherefore linked to, and vary, according to the production volumes.

CONCLUSION

In the case in question it is evident that the decision making process applied followed thesuggested theoretical framework. The process indeed started with focus being placed onthe strategic objectives of the company and the identification of the alternatives to beconsidered. No formal financial appraisal in the form of a formal financial appraisalmodel took place, which left the authors with the question, why? What can be learnt fromthis phenomenon?

In processes where the output of the process is a tangible product, a formal financialappraisal of the alternative(s) should take place. In instances where the output of theprocess is not a tangible product, such as was the case in the case study in question, itbecomes difficult to apply the formal financial appraisal models due to the difficulty ofquantifying certain variables. Furthermore, when the project is in monetary termsinsignificant in comparison to the total capital expenditure of the company, theperforming of a formal financial appraisal in terms of the accepted formal financialappraisal models becomes irrelevant.

19

It is a pre-requisite for processes which impact on the environment and which require dueconsideration of the effects on the environment to be taken into account when making thedecision, that such consideration be incorporated into the preliminary designspecifications of the project.

Projects involving installations where hazardous processes take place, require theperforming of HAZOP studies prior to the project being authorised. The HAZOP studyacts as a verification mechanism to ascertain whether in fact the environmental impact ofthe project has in fact been considered and addressed in the project design. As a result ofthis buffer, any short-cuts taken in the preliminary design process would immediately beidentified. Such studies should be facilitated by an independent third party.

As a result of the number of design stages which a facility, such as the case in question, issubjected to, a realistic budget cannot be drawn up until the preliminary design was doneand verified by the HAZOP study. The final design will dictate the costs. As wasidentified in the case study, the final budget was significantly different to initial budget,which indicated that the latter had been but a futile exercise.

In respect of projects where environmental costs are to be incurred, the incrementrepresenting the environmental costs must be disentangled from the process costs, so thatuseful information can be provided to management for decision making purposes. Onlythe voluntary costs should be measured as environmental costs. This view differs fromthat which should be reported to external stakeholders, which is the case whenenvironmental costs and impacts are reported to the public. They wish to know theexternal environmental costs (cost of pollution) being the social cost factor. Shareholderson the other hand would more than likely want to know the cost of complying withenvironmental regulations.

REFERENCES

Association of Chartered Certified Accountants (ACCA), 1999. EnvironmentalExpenditure in Corporate Reports and Accounts. A report prepared for DG XI andDGXV of the European Commission. London: Association of Chartered CertifiedAccountants.

Ansari, S., Bell, J., Klammer, T. and Lawrence, C. 1997. Measuring and ManagingEnvironmental Costs. Richard D. Irwin Inc.company: United States of America

Boyce, G. 2000. Public discourse and decision making: Exploring possibilities forfinancial, social and environmental accounting. Accounting Auditing & AccountabilityJournal, Vol13 Issue 1.http://www.emerald-library.com/brev/0591ab1.htm

Bromley, D.W., 2000. The two realms of reason: Calculations and sentiment. Paperpresented at the 7th Ulvön Conference on Environmental Economics, Ulvön, Sweden,June 18-21, 2000.

Chartered Institute of Management Accountants (CIMA), 1999. Study Text: Strategicfinancial management. Sixth edition. London: BPP Publishing Limited.

20

Constitution of the Republic of South Africa, 1996. Act 108 of 1996.

De Villiers, C.J. 1999. The decision by management to disclose environmentalinformation: A research note based on interviews. Meditari Accounting Research. Vol. 71999. P33-48.

Drury, C., 2000. Management & Cost Accounting, fifth edition. London: Business Press,Thomson Learning.

Drury, C., and Tayles, M. 1997. The misapplication of capital investment appraisaltechniques. Management Decision. Vol. 35 Issue 2.http://www.emerald-library.com/brev/00135bal.htm

Dunk, A.S., 1999. An examination of the role of financial investment appraisal methodsin the context of international environmental regulation. The Montreal Protocol andCFC substitutes in domestic refrigeration. Accounting Auditing & AccountabilityJournal, Vol. 12 Issue 2.http://www.emerald-library.com/brev/0592bc1.htm

Frangos, J. 1999. Environmental science and the law. Environmental and Planning LawJournal. Vol. 16 issue 2. [email protected]

Gouws, D. G., and Lucouw, P. 1999. The process beyond the numbers and ratios.Meditari Accounting Research. Vol. 7. P99-122.

Gray, R. 2000. Social and Environmental Responsibility, Sustainability andAccountability. Paper presented at the IIR Environmental Accounting and ReportingSymposium, Johannesburg, South Africa, 13-14 September 2000.

Gray, R., Owens, D. and Maunders, K. 1987. Corporate Social Reporting: Accountingand accountability. London: Prentice Hall.

Harrison, E.F., and Pelletier, M.A. 2000. Levels of strategic decision success.Management Decision. Vol. 38 Issue 2.http://www.emerald-library.com/brev/00138bel.htm

Hastings, S. 1996. A strategy evaluation model for management. Management Decision.Vol. 34 Issue 1. http://www.emerald-library.com/brev/00134acl.htm

Howes, R. January 1999. Accounting for environmentally sustainable profits.Management Accounting. p 32-33.

Humphrey, C., and Scapens, R.W. 1996. Methodological themes Theories and CaseStudies of organizational accounting practices: limitation or liberation? Accounting. Vol.9 Issue 4. http://www.emerald-library.com/brev/05909ddl.htm

Kidd, M., 1997. Environmental Law: A South African guide. Cape Town: Juta.

Maccarrone, P. 1996. Organizing the capital budgeting process in large firms.Management Decision. Vol. 34 Issue 6. http://www.emerald-library.com/brev/00134fel.htm

21

National Environmental Management Act (NEMA). 1998. Act 107 of 1998. Republic ofSouth Africa. Government Gazette: Government Printer.

Neale, C.W., and Pike, R.H. 1992. Management Accounting Handbook edited by ColinDrury. Oxford: Butterworth Heinemann.

Neale, C.W., and Letza, S. 1996. Improving the quality of project appraisal andmanagement: an exercise in organizational learning. The Learning Organization. Vol. 3Issue 3. http://www.emerald-library.com/brev/11903ccl.htm

Nieto, M., and Pérez, W. 2000. The development of theories from the analysis of theorganisation: case studies by he pattern of behaviour. Management Decision. Vol. 38Issue 10. http://www.emerald-library.com/brev/00138jel.htm

Parker, L.D., and Roffey, B.H. 1997. Methodological themes Back to the drawing board:revisiting grounded theory and the everyday accountant’s and manager’s reality.Accounting Auditing & Accountability Journal, Vol. 10 Issue 2.http://www.emerald-library.com/brev/05910bd1.htm

Prendergast, P. 1998. Capital projects: wishful thinking and worse! ManagementAccounting (British). Vol. 76 No. 10. p41-42.

Public Accounts and Estimates Committee, 1998. Public Accounts and EstimatesCommittee, 1998, Environmental Accounting and Reporting Issues Paper no3. Victoria:Parlement.

Putterill, M., Maguire, W., Sohal, A.S. 1996. Advanced manufacturing technologyinvestment: criteria for organizational choice and appraisal. Integrated ManufacturingSystems. Vol. 7 Issue 5. http://www.emerald-library.com/brev/06807eb1.htm

Samuels, J. M., Wilkes, F.M. and Brayshaw, R. E., 1995. Management of CompanyFinance. 6th edition. London: Chapman & Hall.

Schaltegger, S. and Muller, K. Spring 1997. Calculating the True Profitability ofPollution Prevention. Greener Management International. Vol. 61, p53-68.

Seitz, N. and Ellison, M. 1999. Capital Budgeting and Long-Term Financial Decisions,Third edition. Orlando: Harcourt Brace College Publishers.

Smith, R and Lambell, J. 1997. Accounting for the environment: The role of strategicmanagement accounting. Management Accounting. February 1999. p34-35.

Shotter, M. 2000 (forthcoming). The influence of neo-classical economics onmanagement accounting education. South African Journal of Accountability andAuditing Research (SAJAAR).

The South African Institute of Chartered Accountants, 1997. Corporate GovernanceGuide: Stakeholder Communication in the Annual Report. Johannesburg: The SouthAfrican Institute of Chartered Accountants.

22

Figure 1

AcknowledgementsThe authors want to acknowledge the permission given for, and assistance with this paperreceived from Messrs. Owen Garvie (De Beers - KAL), Adriaan la Grange (De Beers -CHQ) and Leonard van der Dussen (VDDB - Project Managers). Furtheracknowledgement is given to the project design team of Megchem Projects (Secunda –Mechanical and Piping Design), Nitrophen Chemicals (Pretoria – Process Design),Nomatex (Johannesburg – Control Design), Semane (Johannesburg – Civil Design) andDBM Design (Centurion – Architectural Design).

COMPRESSEDAIR SUPPLY

ACID STORAGE

WATER SUPPLY

PROCESS BUILDING SCRUBBING SYSTEM

EFFLUENT SYSTEM

KIMBERLEY ACID LABORATORIESSimplified Operating Flow Diagram