death, taxes, and rising health care costs

DESCRIPTION

Death, Taxes, and Rising Health Care Costs. Robert E. Hurley, Ph.D. Virginia Commonwealth University. Session Overview. Cost pressures The move to managed care Early success; later decline Consequences for States Private sector responses Tasks before you. - PowerPoint PPT PresentationTRANSCRIPT

Death, Taxes, and Rising Health Care Costs

Robert E. Hurley, Ph.D.Virginia Commonwealth University

Hurley # 2

Session Overview

Cost pressures The move to managed care Early success; later decline Consequences for States Private sector responses Tasks before you

Hurley # 3

The Elusive Pursuit of Sustainable, Affordable Health Care Coverage

Purchasers of health benefits have long struggled to expand coverage, promote access, and contain costs—simultaneously

Public policymakers have assisted efforts with a variety of policy interventions to try to affect health care markets

States have pursued many strategies: certificate of need, rate regulation, investment in safety net providers, reform of insurance markets, mandated benefits and services, expanded public coverage, consumer protection initiatives

Cost containment, in particular, has proven to be elusive

Hurley # 4

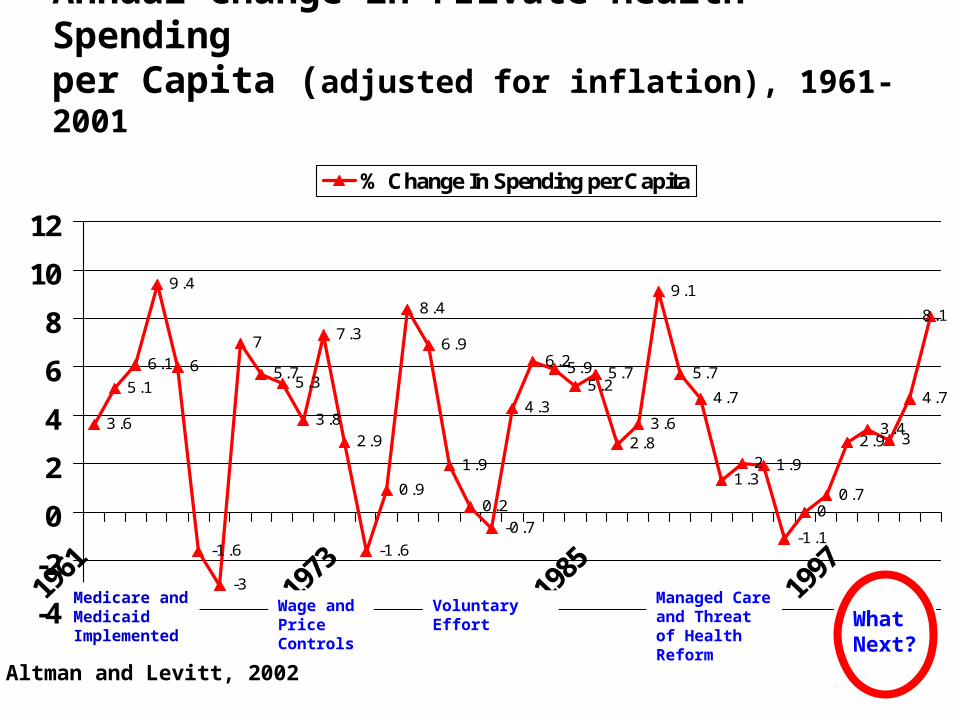

Annual Change in Private Health Spending per Capita (Adjusted for Inflation), 1961-2001

3.6

5.16.1

9.4

6

-1.6

-3

75.75.3

3.8

7.3

2.9

-1.6

0.9

8.4

6.9

1.9

0.2-0.7

4.3

6.25.95.25.7

2.83.6

9.1

5.74.7

1.32 1.9

-1.10

0.7

2.93.43

4.7

8.1

-4

-2

0

2

4

6

8

10

12% Change in Spending per Capita

Medicare and Medicaid Implemented

Voluntary Effort

Managed Care and Threat of Health Reform

Wage and Price Controls

Altman and Levitt, 2002

9.1

• Aged (>65)• Disabled• Low income

• Employee • Dependents

Insurancecarrier/Health

plan/TPADirectPurchase

DirectPurchase

Health Care Providers

Government Employer80 mil. 170 mil.

Uninsured = 45 mil.

The U.S. Health System ― A Simplified View

Hurley # 6

Employer/Sponsored Indemnity Coverage

A system built around spending someone else’s money . . .and an unmanaged system, at that

Employer sponsorship―subsidized premiums and limited cost sharing, health benefits as non-cash compensation shielded from income tax

Indemnity―freedom of choice of providers, providers fees not negotiated, little/no medical management, varied benefit packages

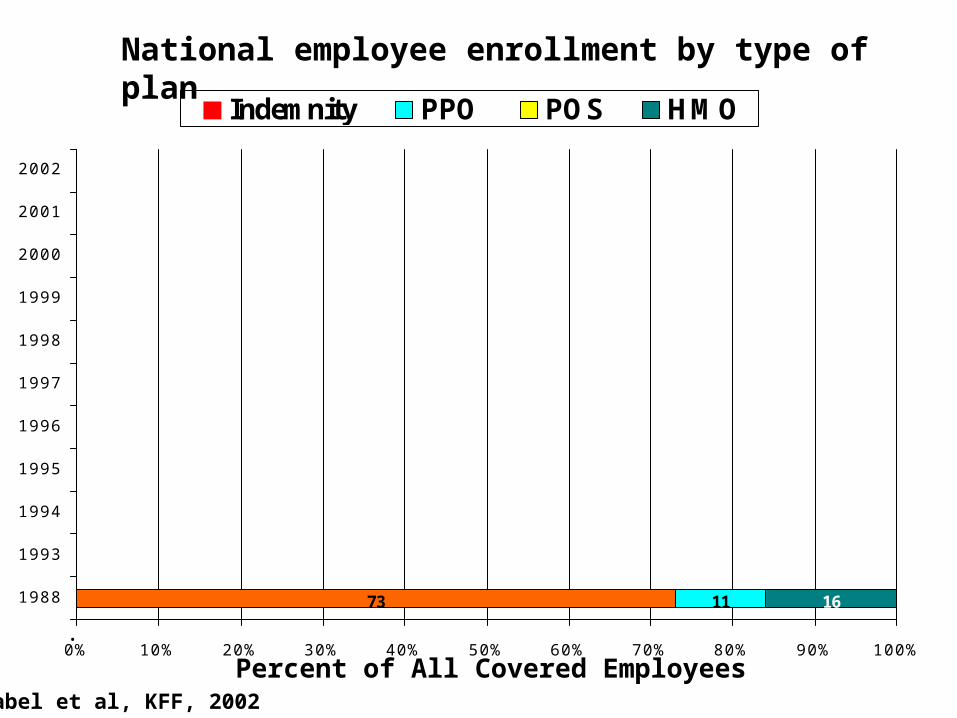

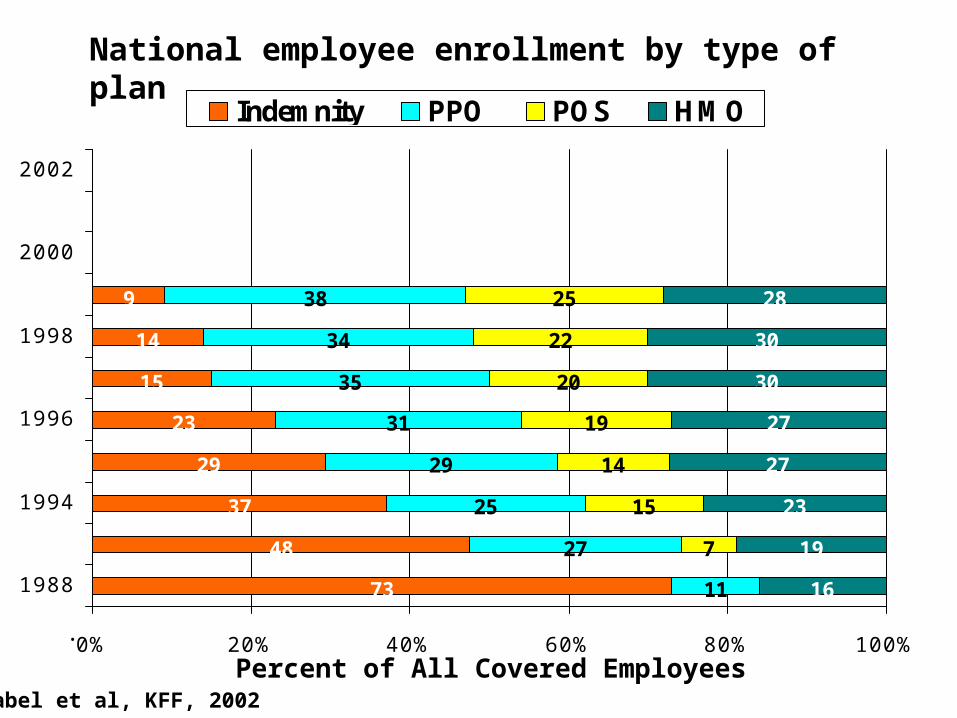

73 11 16

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

1988

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Indemnity PPO POS HMO

Percent of All Covered Employees.

National employee enrollment by type of plan

Gabel et al, KFF, 2002

Hurley # 8

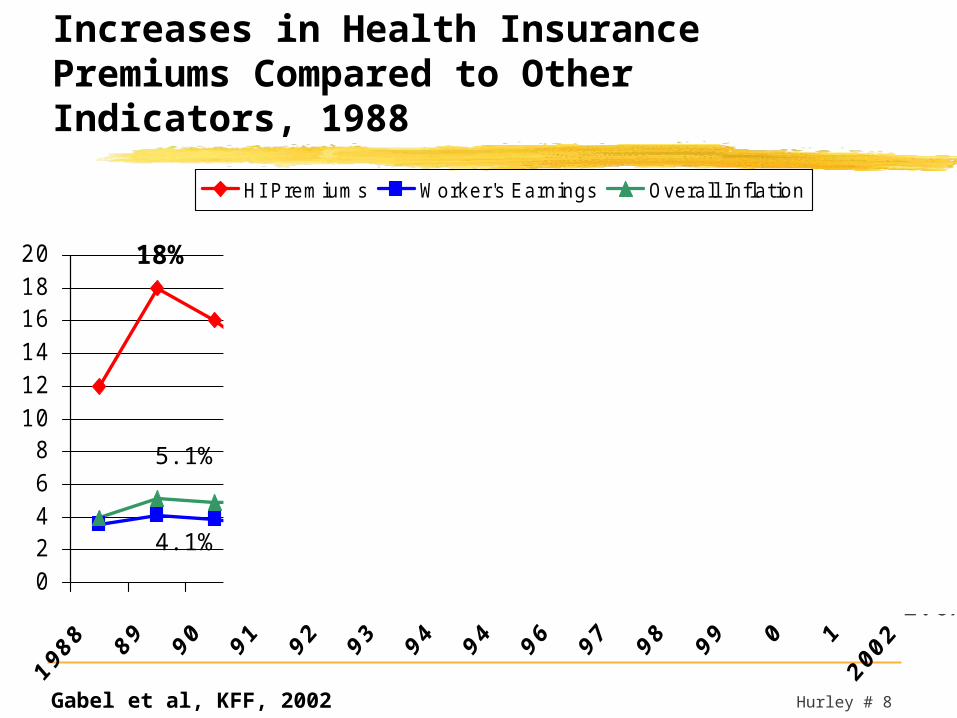

Increases in Health Insurance Premiums Compared to Other Indicators, 1988

02468

101214161820

HI P remiums Worker's Earnings Overall Inflation

18%

12.7%8.5%

8.3%

4.8% 3.4%

1.6%

Gabel et al, KFF, 2002

5.1%

4.1%

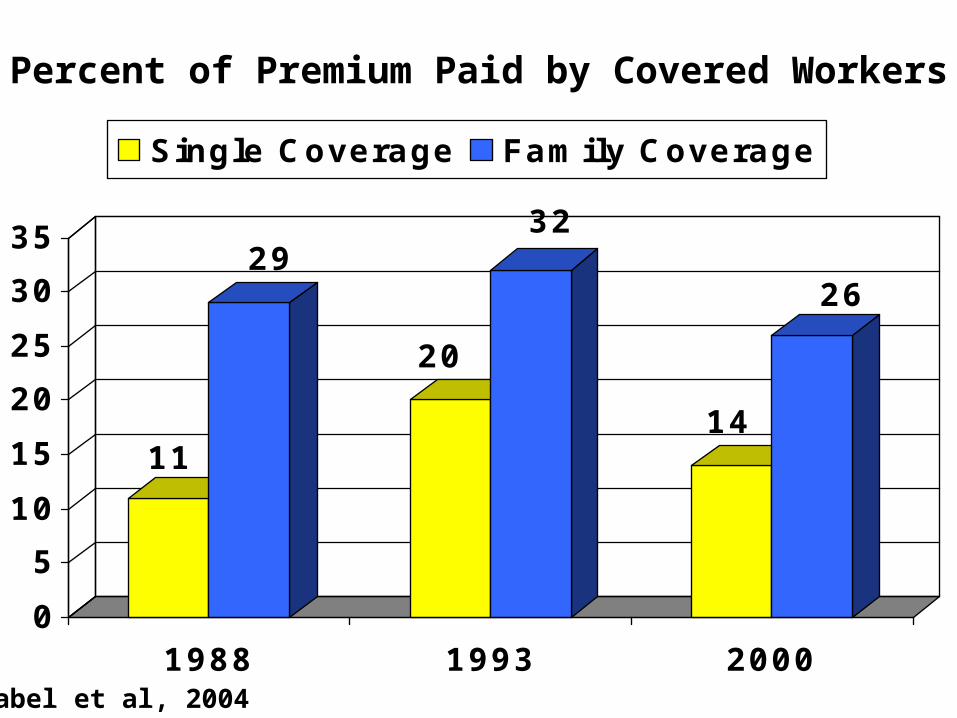

Percent of Premium Paid by Covered Workers

11

29

20

32

14

26

05

101520253035

1988 1993 2000

Single Coverage Family Coverage

Gabel et al, 2004

Hurley # 10

The Purchaser Revolution

The employers make their move

Hurley # 11

Purchasers Attempt To Promote Competition via Managed Care

Private purchasers embraced managed care to exert more control over health benefits and costs

Managed care organizations (MCOs) charged with being aggressive purchasing agents

MCOs design/develop products to match purchaser (and consumer) demands with provider capacity and capabilities

Products to promote competitive dynamics to curb cost growth/improve efficiency/reduce cost shifting

Hurley # 12

From Indemnity to Managed Care

Indemnity—freedom of choice of providers, providers fees not negotiated, little/no medical management, varied benefit packages

Managed care—network-based delivery systems, negotiated payments, medical management, typically richer benefits HMO—narrower networks, aggressive medical

management, some risk-based payment PPO—broader networks, limited medical management,

discounted prices payment POS—HMO with out-of-network options (“leaky HMO”)

73

48

37

29

23

15

14

9

11

27

25

29

31

35

34

38

7

15

14

19

20

22

25

16

19

23

27

27

30

30

28

0% 20% 40% 60% 80% 100%

1988

1994

1996

1998

2000

2002

Indemnity PPO POS HMO

Percent of All Covered Employees.

National employee enrollment by type of plan

Gabel et al, KFF, 2002

Hurley # 14

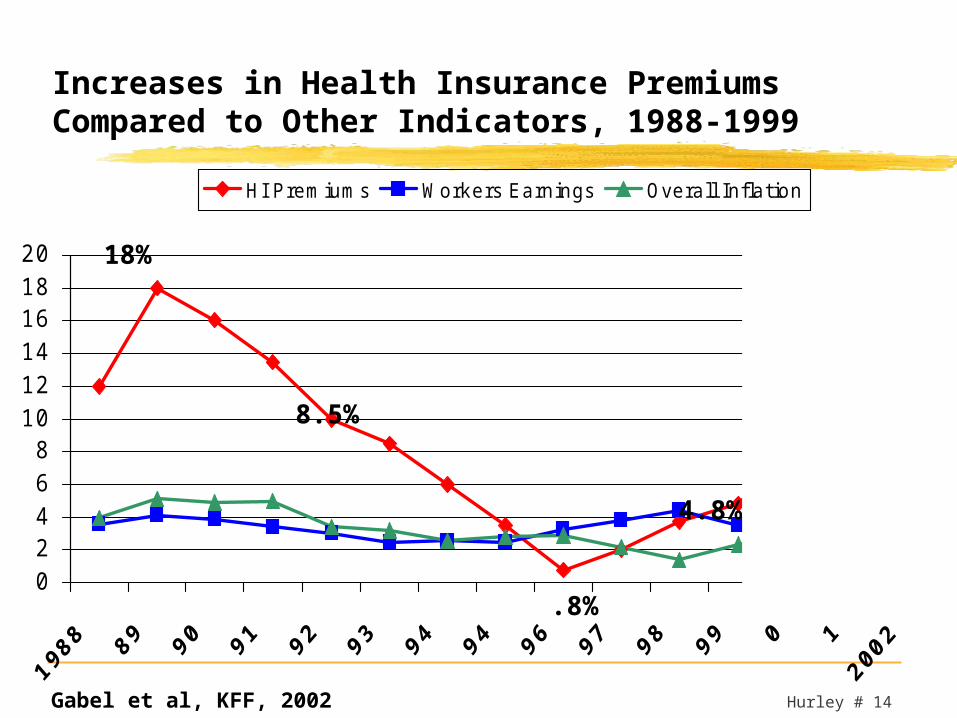

Increases in Health Insurance Premiums Compared to Other Indicators, 1988-1999

02468

101214161820

HI P remiums Workers Earnings Overall Inflation

18%

12.7%8.5%

8.3%

4.8% 3.4%

.8% 1.6%

Gabel et al, KFF, 2002

Hurley # 15

State Governments In 1990s Hitched Their Wagons to Managed Care and Market-based Models

State employee health benefits programs came to rely extensively on managed care products

By 2000, more than half (56%) of Medicaid beneficiaries enrolled in managed care arrangements

Many States enrolled SCHIP eligible children in managed care plans

Sustainability of coverage expansions conditioned on expectation of controlling cost increases

States promoted coverage and benefit expansions with various mandates on health plans

Hurley # 16

Bringing on a Counterrevolution

Suppression of cost-shifting Consumer and provider backlash “Uncontrollable cost pressures” Declining public payments

Hurley # 17

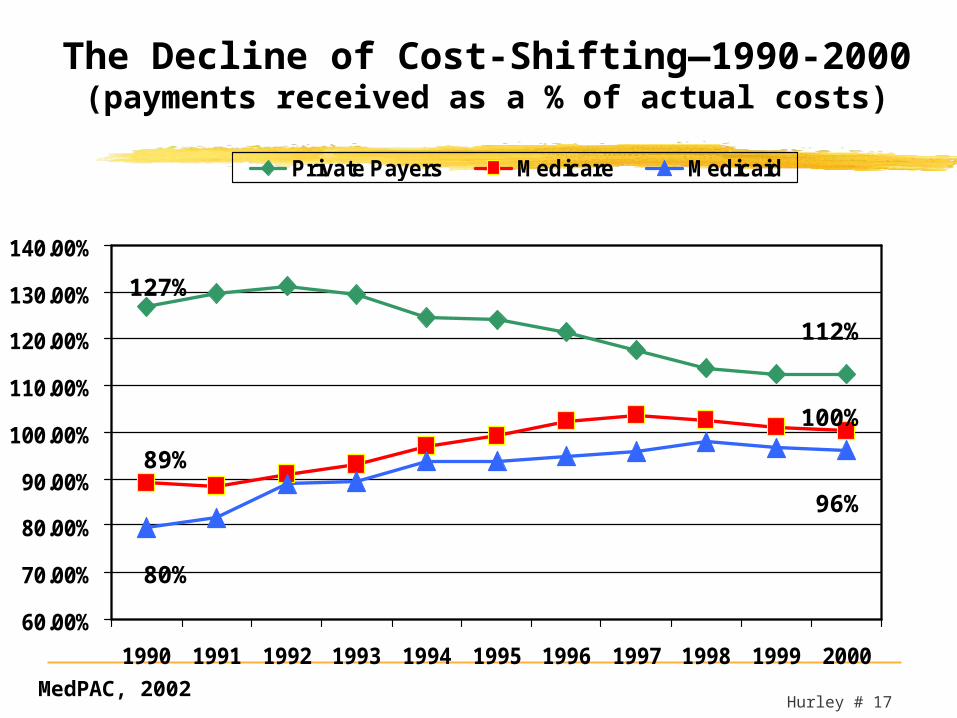

The Decline of Cost-Shifting—1990-2000(payments received as a % of actual costs)

60.00%

70.00%

80.00%

90.00%

100.00%

110.00%

120.00%

130.00%

140.00%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Private Payers Medicare Medicaid

127%

89%

80%

112%

100%

96%

MedPAC, 2002

Hurley # 18

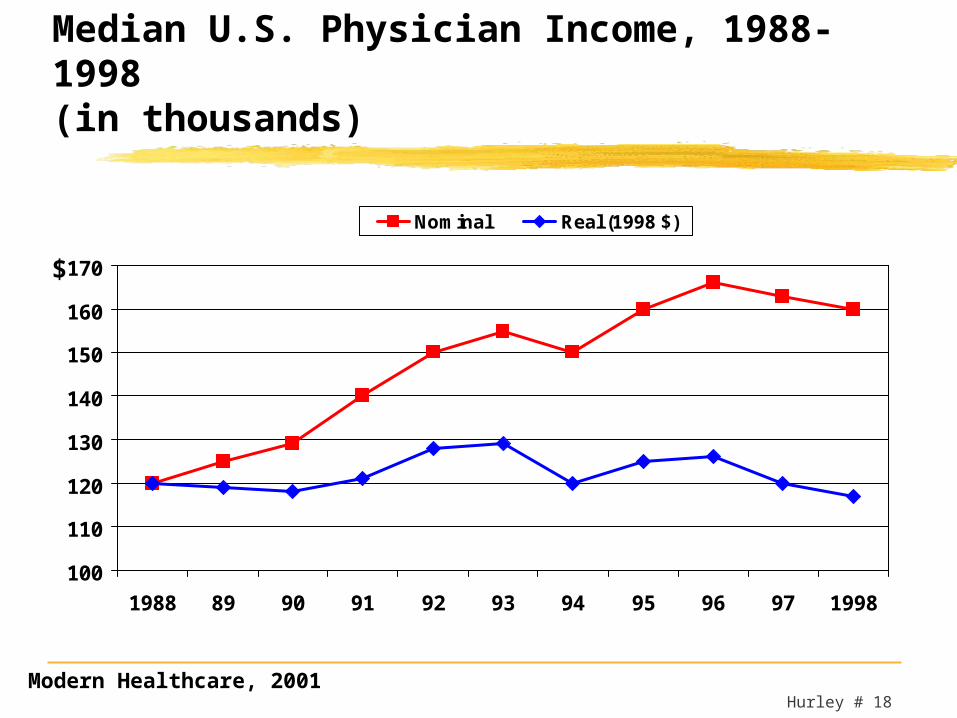

Median U.S. Physician Income, 1988-1998 (in thousands)

100

110

120

130

140

150

160

170

1988 89 90 91 92 93 94 95 96 97 1998

Nominal Real (1998 $)

$

Modern Healthcare, 2001

Hurley # 19

Percent of Groups with “Unfavorable” Rating(Kaiser Family Foundation, National Survey of Prescription Drugs, Sept. 2000)

17%25%26%28%

44%57%57%

71%

0% 20% 40% 60% 80%

Doctors

Hospitals

Banks

Airlines

Pharm Cos

Oil Cos

HMOs

Tobacco Cos

Hurley # 20

Percent Increase in Rx Spending vs. Total Health Care Spending, 1990-2002

10.25 9.759

7.25

5.5 5 4.9 4.8 5 5.6 5.9 6.65.5

12.1 1210.5

8.75 910.5

13.2514

15.316.9 17.3

15.9 15.3

02468

101214161820

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Total HC Rx

Percent

Source: HCFA/CMS

Hurley # 21

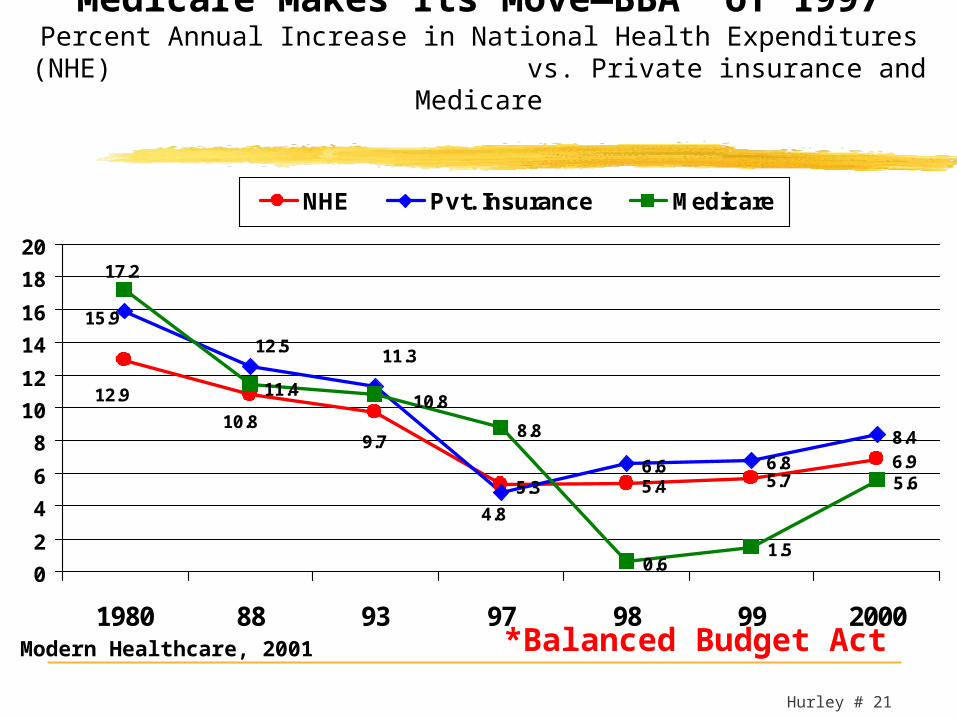

Medicare Makes Its Move—BBA* of 1997Percent Annual Increase in National Health Expenditures (NHE)

vs. Private insurance and Medicare

5.3 5.4 5.76.96.6 6.88.48.8

0.61.5

5.6

9.710.8

12.9

4.8

11.312.515.9

10.811.4

17.2

02468

101214161820

1980 88 93 97 98 99 2000

NHE Pvt. Insurance Medicare

*Balanced Budget ActModern Healthcare, 2001

Hurley # 22

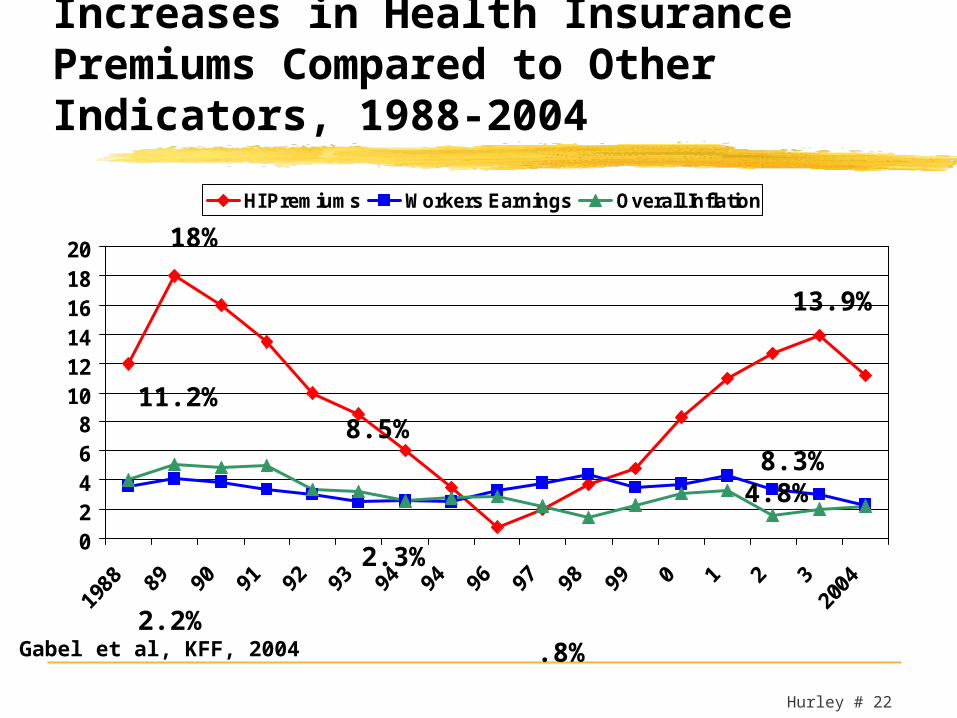

Increases in Health Insurance Premiums Compared to Other Indicators, 1988-2004

02468

101214161820

HI Premiums Workers Earnings Overall Inflation

18%

13.9%

11.2% 8.5% 8.3% 4.8%

2.3% 2.2%

.8%

Gabel et al, KFF, 2004

Hurley # 23

Contemporary Picture

Premium increases remain near or at double digits

Private coverage likely to continue to decline Private-sector managed care plans lose traction

in cost control efforts with providers Continued increases in major cost drivers: labor,

technology, pharmacy, malpractice, and administrative cost

Public payers continue to shift more pressure to private payers

Increased consumer cost participation inevitable

Hurley # 24

Managed Care—Managing to Hold On

Broader networks/looser products (PPO) Targeted disease management

programs to focus on high-cost users Incentive-based compensation systems

for providers to promote quality Expanded consumer cost sharing and

consumer engagement in choices Raising premiums faster than costs

73

48

37

29

23

15

14

9

8

7

4

5

11

27

25

29

31

35

34

38

41

48

52

54

7

15

14

19

20

22

25

22

22

18

17

16

19

23

27

27

30

30

28

29

23

24

26

0% 20% 40% 60% 80% 100%

1988

1994

1996

1998

2000

2002

Indemnity PPO POS HMO

Percent of All Covered Employees.

National employee enrollment by type of plan

Gabel et al, KFF, 2002

Hurley # 26

Implications for State Policymakers

Sharply rising health care expenses affect:

1. State employee benefits costs2. Medicaid and SCHIP expenditures3. Coverage expansions—past and future4. Financing for safety net providers 5. Sustainability of private coverage—

potentially increasing enrollment in public programs

6. Demands for both deregulation and new regulation

Hurley # 27

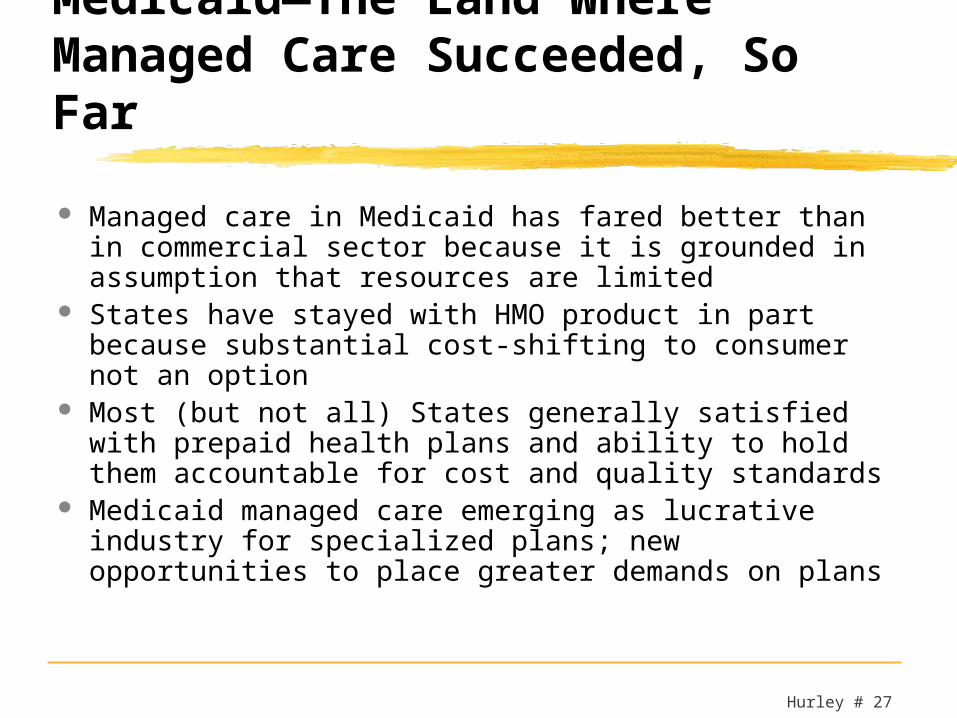

Medicaid—The Land Where Managed Care Succeeded, So Far

Managed care in Medicaid has fared better than in commercial sector because it is grounded in assumption that resources are limited

States have stayed with HMO product in part because substantial cost-shifting to consumer not an option

Most (but not all) States generally satisfied with prepaid health plans and ability to hold them accountable for cost and quality standards

Medicaid managed care emerging as lucrative industry for specialized plans; new opportunities to place greater demands on plans

Hurley # 28

The Private Sector Response Disenchanted with managed care organizations,

growing doubts about their ability to affect health care markets

Belief that expanded coverage/benefits with reduced out of pocket costs for employee/consumer is THE problem and needs to be reversed

Drumbeat building for a variety of “consumer directed health product” (CDHP) designs

Is this inspiration or desperation?

Percentage of Large Employers (>200 workers) Planning Selected Benefit Changes in Next Year

9

41

52

52

55

83

59

48

48

45

17

91Restrict eligibility

Reduce dependentsubsidy

Increase officecopays

Increasedeductibles

Increaser Rx costs

Raise employeepremium

Likely Not likely

Gabel et al, KFF, 2004 Likely= Very/Somewhat likely; Not=Other

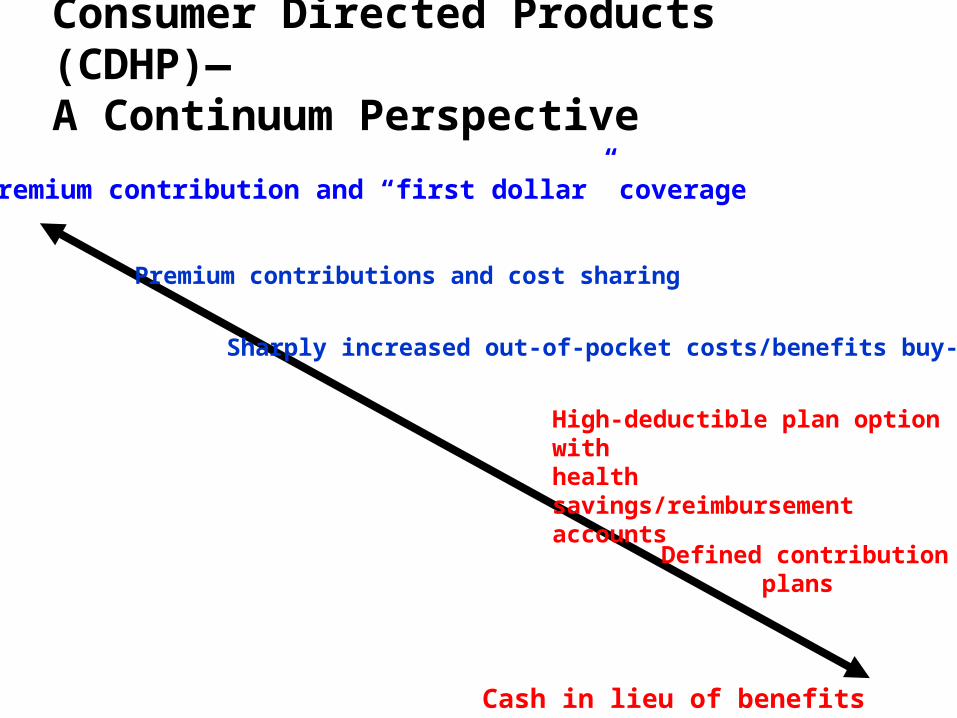

Consumer Directed Products (CDHP)—

A Continuum PerspectiveNo premium contribution and “first dollar” coverage

Cash in lieu of benefits

Premium contributions and cost sharing

Sharply increased out-of-pocket costs/benefits buy-down

High-deductible plan option withhealth savings/reimbursement accounts

Defined contribution plans

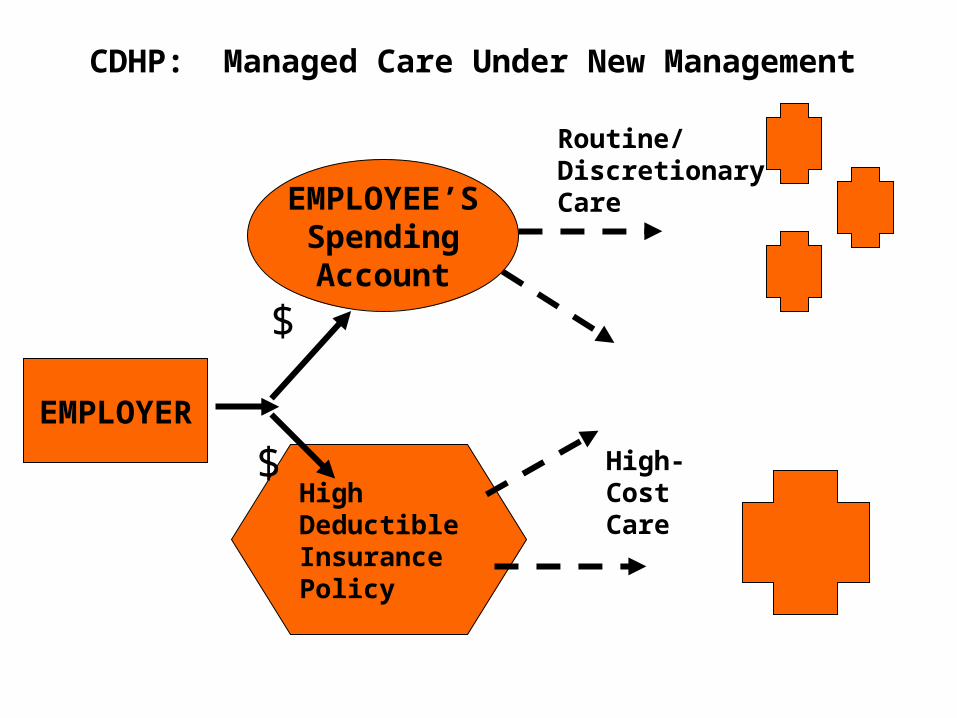

CDHP: Managed Care Under New Management

EMPLOYEE’SSpendingAccount

EMPLOYER

High DeductibleInsurancePolicy

$

$

Routine/DiscretionaryCare

High- CostCare

Hurley # 32

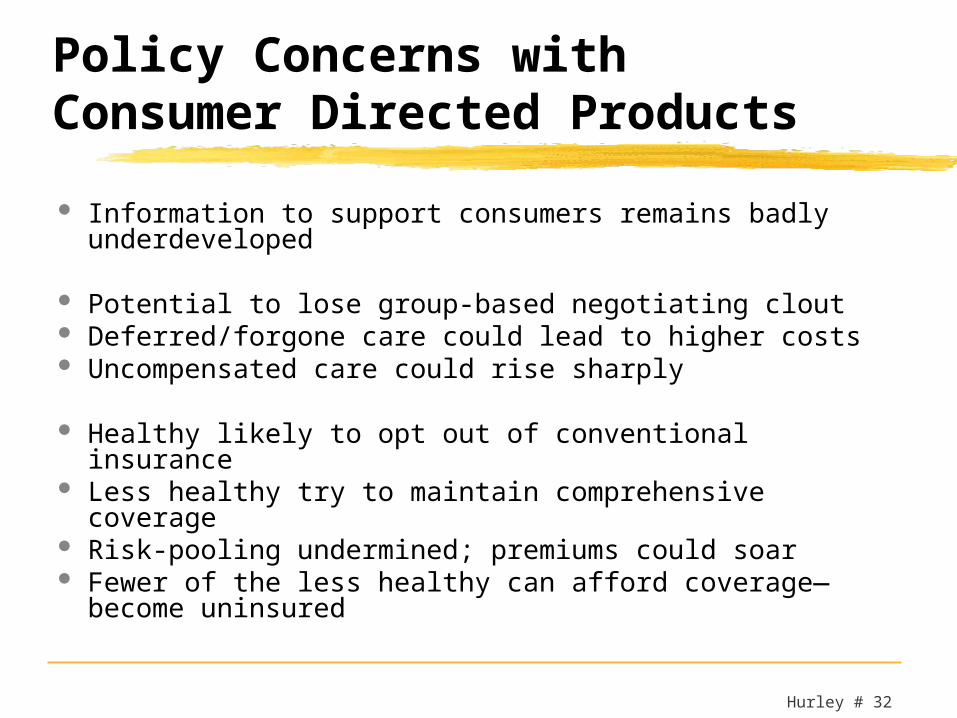

Policy Concerns with Consumer Directed Products

Information to support consumers remains badly underdeveloped

Potential to lose group-based negotiating clout Deferred/forgone care could lead to higher costs Uncompensated care could rise sharply

Healthy likely to opt out of conventional insurance Less healthy try to maintain comprehensive coverage Risk-pooling undermined; premiums could soar Fewer of the less healthy can afford coverage—

become uninsured

Hurley # 33

The Tasks Before You

Sustain past coverage expansions and explore new configurations of public and private arrangements

Review strategies for purchasing care for Medicaid and SCHIP beneficiaries

Revisit benefit designs and delivery system options for State employees

Re-appraise regulatory and other interventions to bolster private insurance markets

Consider consequences of consumer directed products

Annual Change in Private Health Spending per Capita (adjusted for inflation), 1961-2001

3.6

5.16.1

9.4

6

-1.6

-3

75.75.3

3.8

7.3

2.9

-1.6

0.9

8.4

6.9

1.9

0.2-0.7

4.3

6.25.95.25.7

2.83.6

9.1

5.74.7

1.32 1.9

-1.10

0.7

2.93.43

4.7

8.1

-4

-2

0

2

4

6

8

10

12% Change In Spending per Capita

Medicare and Medicaid Implemented

Voluntary Effort

Managed Care and Threat of Health Reform

Wage and Price Controls

WhatNext?

Altman and Levitt, 2002

“You can always count on the Americans to do the right thing, after exhausting all other alternatives.”

Winston S. Churchill