data-driven strategy for new payment models data-driven strategy for new payment models mark sharp,...

TRANSCRIPT

1

Data-Driven Strategy for New Payment Models

Mark Sharp, CPAPartner

Objectives

• Understand new payment model reforms and bundling arrangements

• Learn how these new payment models can impact your agencies

• Consider strategies that can help you succeed within the new payment models

ACO Accountable Care Organization

APM Advanced Payment Models

BPCI Bundled Payment for Care Improvement

CJR Comprehensive Care for Joint Replacement

CMMI Center for Medicare & Medicaid Innovation

DRG Diagnosis Related Group

FFS Fee for Service

HHA Home Health Agency

HHVBP Home Health Value Based Purchasing

IRF Inpatient Rehabilitation Facility

MSA Metropolitan Statistical Area

PFS Physician Fee Schedule

PGP Physician Group Practice

SNF Skilled Nursing Facility

Common Acronyms

2

0

10

20

30

40

50

60

70

80

90

100

2011 2015 2016 2018

HHS goal of 30% of traditional FFS Medicare payments through Advanced Payment Models by the end of 2016 and 50% by the end of 2018

%

Medicare

Payments FFS

APM

Future of Medicare Payments

AccountableCare

BPCIPrimary Care

TransitionMedicaid and

CHIPAcceleration

ModelsSpeed Adoptionof Best Practices

ACOs Model 1Advanced Primary

Care InitiativeReduce Avoidable Hospitalizations

State Innovation Models

Beneficiary Engagement Model

Advanced PaymentACOs

Model 2Comprehensive

Primary Care Initiative

Financial Alignment Incentive for

Medicare and Medicaid

Frontier Community Health

Integration

Community BasedCare Transitions

ACO Investment Model

Model 3FQHC Advanced

Primary Care Practice

Strong Start forMothers and

Newborns

Health Care Innovation Rounds

Health Care Actionand Learning

Network

Next Generation ACO

Model 4Graduate Nurse

Education

MedicaidPrevention of

Chronic Diseases

Health PlanInnovation Initiative

Innovative Advisors Program

Pioneer ACOTransforming

Clinical Practice

Medicaid Emergency Psychiatric

Demonstration

Million HeartsCJR

CMMI Advanced Payment Models

Bundled Payment Popularity

Source: CMMI Website

0

100

200

300

400

500

600

700

800

900

1000

Participants in CMMI Payment Models

Bundled Payment Popularity

3

Collaborative relationships and gainsharing with physicians and

post-acute providers

Financial accountability for two of the most common DRGs: 469 & 470

Target prices derived from historical claims data

Episodes lasting 90 days post-discharge

2 Quality Measures + Voluntary PRO

CJR Model

67MSAs

MSAs in CJR Model

• Medicare shared savings program

• Bundled Payments

Hospitals bear financial accountability

All providers continue to be paid under current methodologies

• DRG

• Per diem

• Episodes

Retrospective reconciliation against target prices

CJR Financial Accountability

4

• Bundled payments

Inpatient vs post-acute payments

Risk and variability is often highest in post-acute setting

• Pressure towards vertical integration

Ownership vs partnership

Financial Accountability in Bundles

• From 67 MSAs to ALL MSAs

• From hips and knees to:• Cardiac procedures

• COPD

• CHF

• AMI

• Pneumonia

What’s Next?

• Pilot for home health only

• Per CMS, pilot will– Incentivize Medicare agencies to provide higher

quality and more efficient care

– Test whether a payment incentive of up to 8% significantly improves provider performance

– Test the use of new quality measures in the home health setting

– Enhance the current public reporting process

HHVBP Pilot

12 // 2015 AHHC Home Health Intensive Conference

5

• All Medicare-certified agencies in nine states

HHVBP Pilot States

• Financial bonus pool funded by payment reductions to others– Performance and outcome standards are

established to determine which providers receive bonus payments

– Those that do not meet the standards are left with lower payment rates

– Those that out perform the standards receive financial rewards

• Current congressional consideration for nation-wide VBP for all post-acute providers

HHVBP Pilot Overview

• Performance scores based on the following measures– 9 outcomes measures

– 5 patient satisfaction measures

– 3 process measures

– Ranked within common sized cohorts

– Scores for achievement and/or improvement

HHVBP Performance Scoring

6

• Starting in 2016– Baseline year of 2015

– Payment adjustments made to the final Medicare claims paid during the payment adjustment year

HHVBP Pilot Years

Performance YearPayment

Adjustment YearMax Pay Adjust

(up or down)

2016 2018 3%

2017 2019 5%

2018 2020 6%

2019 2021 7%

2020 2022 8%

17 // 2015 AHHC Home Health Intensive Conference

Success Today and Tomorrow

18 // 2015 AHHC Home Health Intensive Conference

Success Today and Tomorrow

Increase efficiency

in providing care

Improve outcomes

TRIPLE AIM

Improve the patient experience

7

Success in APMs

• It’s not a sprint…it’s a marathon

• Understand current state

• Develop a strategy

• Don’t need to go it alone

• Data access and horsepower

• Leadership buy-in

• Challenge traditional thinking

Success in APMs

• Identify and manage the high risk patients

• Ongoing patient monitoring

• Effective care transitions care and triage practices

• Excellent communication and coordination

• Define and communicate the value proposition

• Physician involvement can be key

What’s Going

To Happen?

What Should We

Do About It?

What Are The

Implications?

Strategic Management Model

8

Road to APM Success

Direction from Leadership

• Define and communicate the vision

• Develop culture of change

• Establish the behavior and performance expectations

• Ensure access to necessary resources

• Identify known barriers and manage resistance

1

Patients

Physicians

Post-Acute Providers

1 2

Ris

k S

trati

ficati

on

Data Analytics

9

Patients in the Population

Average CJR Episode Payments

CJR Episode Outliers

10

Post-Acute Care Providers

Longitudinal View

Physician Analysis

11

Competitor Analysis

A B C D E F G H I J

A B C D E F G H I J

COLLABORATORS, GAINSHARING AND QUALITY

1 2 3

Physicians Skilled Nursing Home Health

Collaborators, Gainsharing & Quality

Development of Collaborators

12

Collaborators and Gainsharing

1 2 3 4

• Leverage data to perform a gap analysis and identify best practices

• Establish baseline: value stream mapping

• Coordinate with current orthopedic programs

• Present findings to Steering Committee

• Develop work groups and provide targeted training

• “Prehab”

• Acute Care

• Care Transitions/PAC

• IT

• Finance

• Discharge selection tool

• PAC Provider Scorecards

Care Redesign

1 2 3 4 5

Monthly progress reports

Key metrics dashboard

Data Custodian

Target price calculation

Reconciliation

Monitoring Progress

13

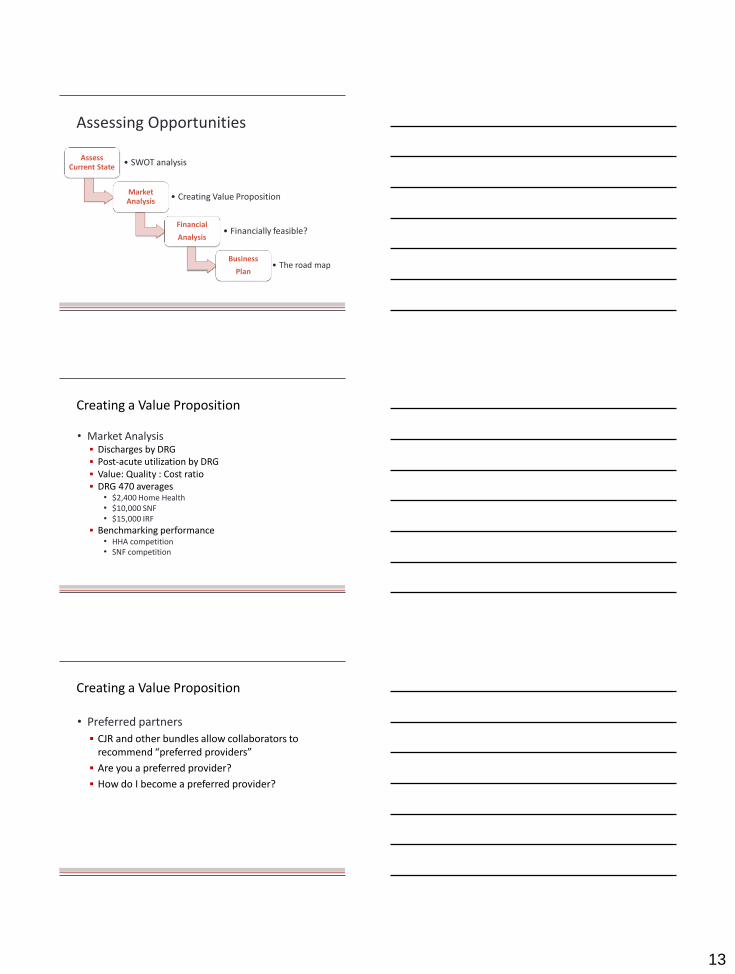

Assessing Opportunities

Assess Current State

• SWOT analysis

Market Analysis

• Creating Value Proposition

Financial

Analysis• Financially feasible?

Business

Plan• The road map

• Market Analysis Discharges by DRG Post-acute utilization by DRG Value: Quality : Cost ratio DRG 470 averages

• $2,400 Home Health• $10,000 SNF• $15,000 IRF

Benchmarking performance• HHA competition• SNF competition

Creating a Value Proposition

• Preferred partners

CJR and other bundles allow collaborators to recommend “preferred providers”

Are you a preferred provider?

How do I become a preferred provider?

Creating a Value Proposition