crisis in a fog or what hopes the russian pharma for? - rafm 2015_demidov_ims health.pdf · crisis...

TRANSCRIPT

0

Кризис в тумане или на что надеется

российский фармрынок в 2015 году

IMS General manager Russia&CIS

04.06.2015

Crisis in a fog or what hopes the Russian pharma for?

Nickolai Demidov

Russia entered a period of economic turmoil (1 / 1)

-3,8% 0,6% 1,3% 3,4% 4,3%

2015E

42,0

2014

43,7

2013

43,4

2012

42,9

2011

41,5

2010

39,8

Russian GDP dynamics, trillion rubles

GDP, Constant prices, Trillion RUB

Comments

Macroeconomic outlook is worsening due to

drop in the oil prices

economic sanctions

Healthcare spending level will remain unchanged (4,1% of GDP)

Potential increase (1,4% of GDP) initially planned by the government will not be realized

G

enera

l tr

ends

Econom

ic c

risis

Source: EIU, IMF, Ministry of health, IMS Health analysis

1 Russian pharmaceutical market at a crossroad

2015E

93,7%

2014

99,0%

2013

103,2%

2012

104,6%

2011

100,5%

2010

105,9% Real disposable income dynamics, % change to the previous year

Unemployment rate dynamics, % of economically active population

-0,8 p.p.

0,0 p.p. -1,0 p.p.

2010

7,3%

+0,9 p.p.

+0,1 p.p.

2013

5,5%

2012

5,5%

2011

6,5%

2014

5,6% 6,5%

2015E

Disposable income growth is no more supporting the consumption and doesn’t help to compensate inflation

Unemployment forecast is showing threat to reach the worst level since 2009

But we also should keep in

mind that official forecast

especially for negative

trends are commonly more

cautious

2

Week macroeconomic outlook, evident negative tendencies and high uncertainty with the future leave the business uncertain regarding the future Context of first 5 months

• after 3 months of market volatility kind of break began in April 2015 - is it a major trend or just a respite?

• decrease of domestic income, and some subjective predictions that “people will be short of money already in summer” - true or false?

• short term benefits for wholesalers – then painfully landing from the peak of roller coaster or it’s a year of whlsaller?

• feverish regulation, obvious lack of agreement between the branches of government – should we wait for any support from state in order to sustain the crisis?

• In general: there are evidences that Russian pharma put on hold in terms of enhancement of investments though strategic projects go on

Ma

rket re

actin

g to

crisis

O

OP

se

cto

r tr

en

ds

2

Russian pharmaceutical market at a crossroad

How ph companies react?

• Budgets frozen and under constant revision, though pharma is strongly #1 at TV

increasing interest to calculations of immediate effect, ROI and factors determining

But decrease of common excepted ROI?

• Price increase

Rx EDL – toughly restrained by regulation

Rx&OTC non EDL - restrained naturally by elasticity

• Revision of partnership with whs and chains

with whsl: reinforce of financial and shipments volumes and frequency

with chains: Promo – seeking for optimal minimum

G

en

era

l tr

en

ds

3

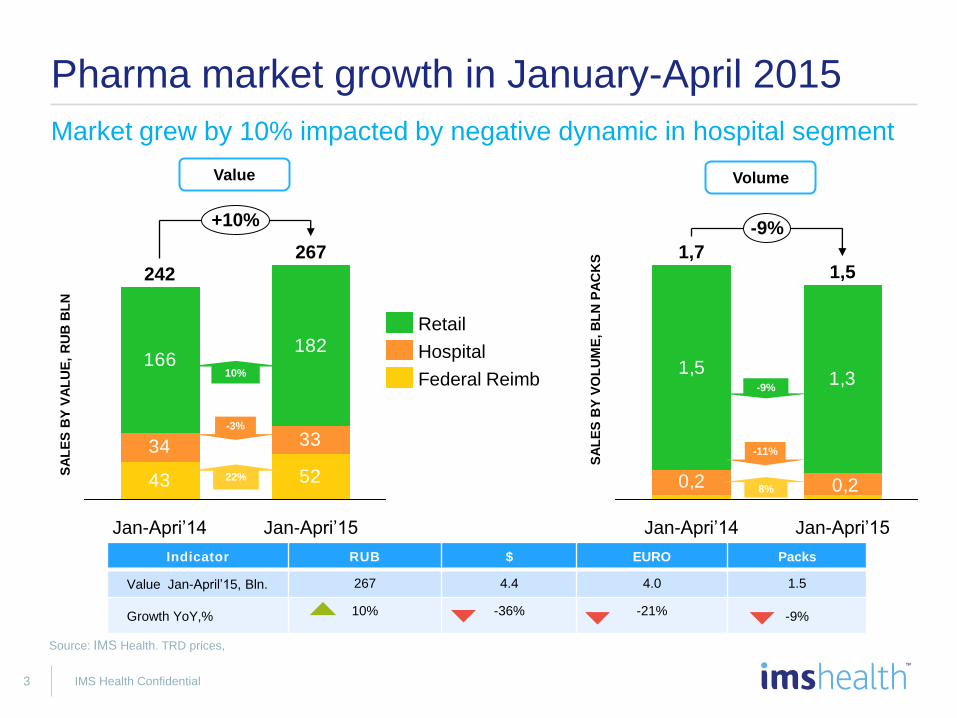

Indicator RUB $ EURO Packs

Value Jan-April’15, Bln. 267 4.4 4.0 1.5

Growth YoY,% 10% -36% -21% -9%

IMS Health Confidential

Pharma market growth in January-April 2015

43 52

34 33

166182

+10%

Jan-Apri’15

267

Jan-Apri’14

242

Retail

Federal Reimb

Hospital

SA

LE

S B

Y V

AL

UE

, R

UB

BL

N

22%

Value Volume

SA

LE

S B

Y V

OL

UM

E, B

LN

PA

CK

S

0,2

1,51,3

0,2

1,5

Jan-Apri’14 Jan-Apri’15

-9%

1,7

8%

Source: IMS Health. TRD prices,

Market grew by 10% impacted by negative dynamic in hospital segment

10%

-3%

-9%

-11%

Retail out-of-pocket market growth in Jan-Apr 2015 vs. Jan-Apr 2014

81,3 88,4

84,6 93,8

+9,6%

YTD4_2014

193,5

11

YTD4_2013

176,6

10,7 0,12 0,12

0,45 0,41

1,03 0,94

-8%

YTD4_2014

1,47

YTD4_2013

1,59

Food supplements

Rx

OTC

Value Volume

6,1%

10,9%

8,6%

+1,3%

-8,3%

-8,9%

SA

LE

S B

Y V

ALU

E,

RU

B B

LN

SA

LE

S B

Y V

OLU

ME

, B

LN

PA

CK

S

Source: IMS Health. TRD prices

© 2014 IMS Health Incorporated or its affiliates. All rights reserved 4

OTCs grow faster by value but dropped deeper with volumes consumed

5 IMS Health Confidential

Medical Devices+Parapharma sales dynamics in Q1 2015 vs. Q2 2014, TRD prices

Tonometers+

Thermometers

Glucometers+

Test-strips

Insulin.syringes+

needles

1.426

1.258 1.264

+24%

1.297

Condoms+

Lubricants

84

+10%

Incontinence

care

0%

+10%

Enteral nutrition

1.157

1.434

55

706

990

128 141

+40%

+54%

Q1 2015

Q1 2014

Va

lue

in m

io R

UR

, in

wh

ls p

rice

s

6 IMS Health Confidential

Retail market monthly sales and growth structure in January-April 2015

Dec Nov Oct Sep Aug Jul Jun May Apr Mar Feb Jan

2015 2014 2013

VA

LU

E (

TR

D)

Total

Growth

10%

New

products

1,9%

Volume

10,9%

Structure

0,6%

Price

20,3%

Drop-out

products*

-0,1

Growth components*

Source: IMS Health. Data at TRD prices, drop-out products are excluded due to low figures

Market keeps growing being driven by inflation

• Jan-Apr 2015 wasn’t similar to previous year

• Restore of purchase in February after peak in December’14

Price increase again drives sales on OOP market…

Price increase tuned back as major growth component though EDL price regulation

• Eliminated switch to better/more expensive factor (Structure)

• Still have positive effect from new products launches

• Volumes decrease is strongly negative factor pulling the growth down

7 IMS Health Confidential

Retail market growth in January-April 2015

Dec Nov Oct Sep Aug Jul Jun May Apr Mar Feb Jan

2015 2014 2013

VA

LU

E (

TR

D)

Source: IMS Health. Data at TRD prices, drop-out products are excluded due to low figures

Market keeps seasonality, every year consistently over past years

• Jan-Apr 2015 wasn’t similar to previous year

• Restore of purchase in February after peak in December’14

• Volumes strongly dropped

• declining trend

• no hint for further improvement

• summer is expected to be “cold”

Price increase drives sales on OOP market while volumes of pharmaceuticals

sold are declining

2015 2014 2013

Dec Nov Oct Sep Aug Jul Jun May Apr Mar Feb Jan

VO

LU

ME

(T

RD

)

Monthly dynamics in Jan’13-Apr’15 by value, RUB

Monthly dynamics in Jan’13-Apr’15 by volume, packs

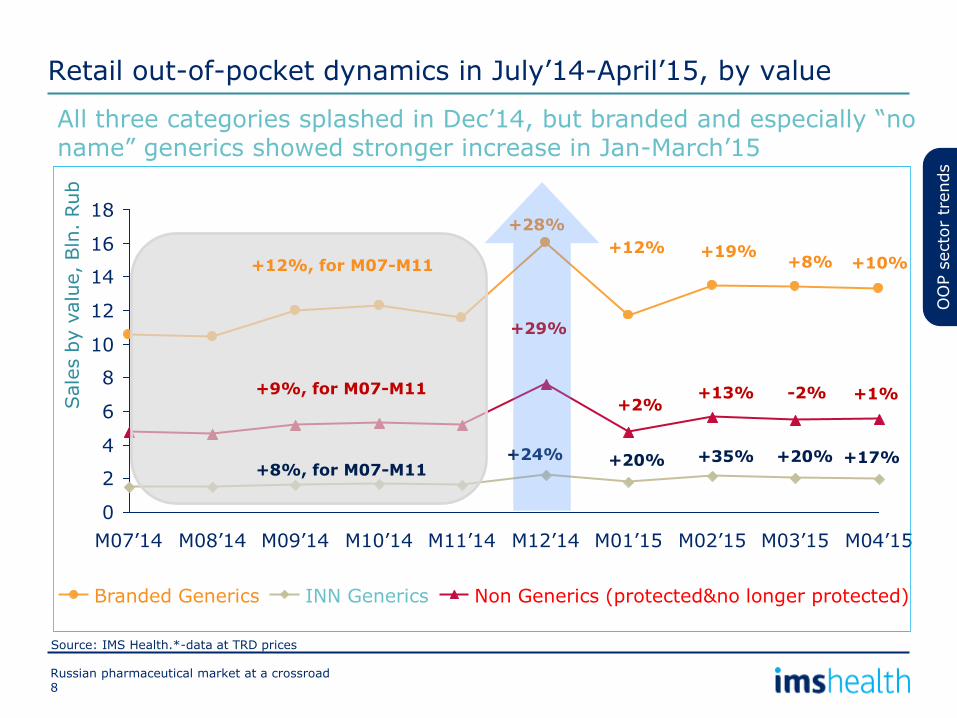

Retail out-of-pocket dynamics in July’14-April’15, by value

Source: IMS Health.*-data at TRD prices

OO

P s

ecto

r tr

ends

18

16

14

12

10

8

6

4

2

0

M04’15 M03’15 M02’15 M01’15 M12’14 M11’14 M10’14 M09’14 M08’14 M07’14

Sale

s b

y v

alu

e, Bln

. Rub

Non Generics (protected&no longer protected) Branded Generics INN Generics

All three categories splashed in Dec’14, but branded and especially “no name” generics showed stronger increase in Jan-March’15

+12%, for M07-M11

+28%

+12% +19%

+8%, for M07-M11 +24% +20% +35%

+9%, for M07-M11

+29%

+2% +13%

+8%

+20%

-2%

8 Russian pharmaceutical market at a crossroad

+10%

+17%

+1%

Retail out-of-pocket dynamics in July’14-April’15, by volume

Source: IMS Health.*-data at TRD prices

OO

P s

ecto

r tr

ends

120

100

80

60

40

20

0

M03’15 M02’15 M01’15 M12’14 M11’14 M10’14 M09’14 M08’14 M07’14 M04’15

Sale

s b

y v

olu

me, M

ln. packs

Non Generics (protected&no longer protected) Branded Generics INN Generics

After rapid increase in December, there is likely to be a trend break/ swing in Dec’14/Jan’15

+5%, for M07-M11

-4%, for M07-M11

+2%, for M07-M11

+9%

-8% -1%

+8%

-4%

+9%

+12%

-13% +4%

-11%

-6%

-17%

9 Russian pharmaceutical market at a crossroad

-9%

-10%

-13%

10

Essential Drug List

(EDL)

IMS Health Confidential

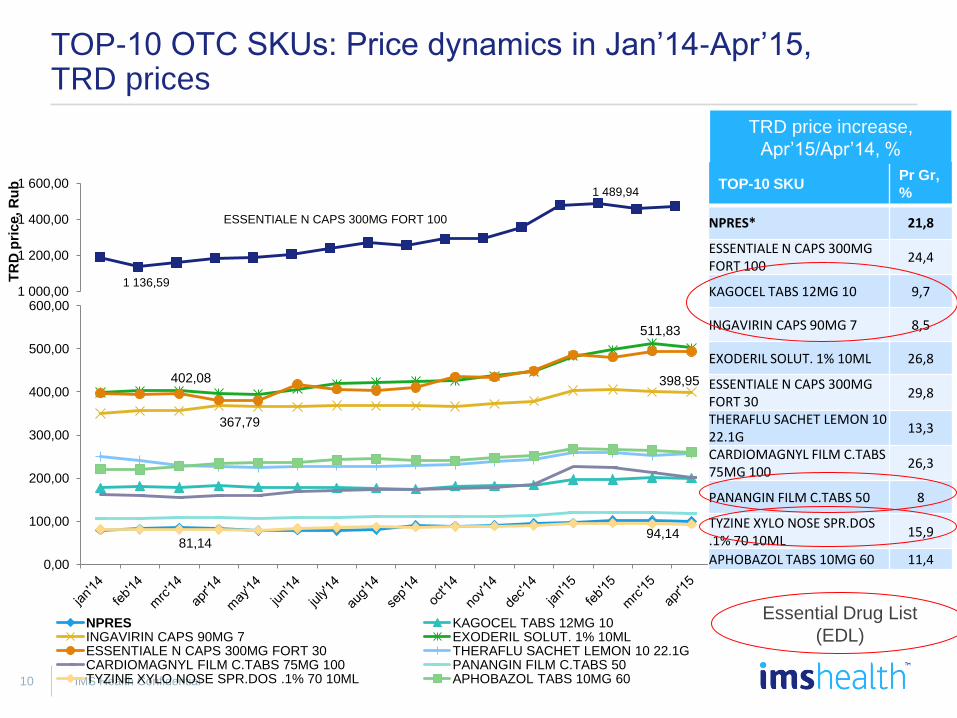

TOP-10 OTC SKUs: Price dynamics in Jan’14-Apr’15, TRD prices

1 136,59

1 489,94

1 000,00

1 200,00

1 400,00

1 600,00

TR

D p

ric

e, R

ub

ESSENTIALE N CAPS 300MG FORT 100

367,79

398,95 402,08

511,83

81,14 94,14

0,00

100,00

200,00

300,00

400,00

500,00

600,00

NPRES KAGOCEL TABS 12MG 10 INGAVIRIN CAPS 90MG 7 EXODERIL SOLUT. 1% 10ML ESSENTIALE N CAPS 300MG FORT 30 THERAFLU SACHET LEMON 10 22.1G CARDIOMAGNYL FILM C.TABS 75MG 100 PANANGIN FILM C.TABS 50 TYZINE XYLO NOSE SPR.DOS .1% 70 10ML APHOBAZOL TABS 10MG 60

TOP-10 SKU Pr Gr,

%

NPRES* 21,8

ESSENTIALE N CAPS 300MG FORT 100

24,4

KAGOCEL TABS 12MG 10 9,7

INGAVIRIN CAPS 90MG 7 8,5

EXODERIL SOLUT. 1% 10ML 26,8

ESSENTIALE N CAPS 300MG FORT 30

29,8

THERAFLU SACHET LEMON 10 22.1G

13,3

CARDIOMAGNYL FILM C.TABS 75MG 100

26,3

PANANGIN FILM C.TABS 50 8

TYZINE XYLO NOSE SPR.DOS .1% 70 10ML

15,9

APHOBAZOL TABS 10MG 60 11,4

TRD price increase,

Apr’15/Apr’14, %

11 IMS Health Confidential

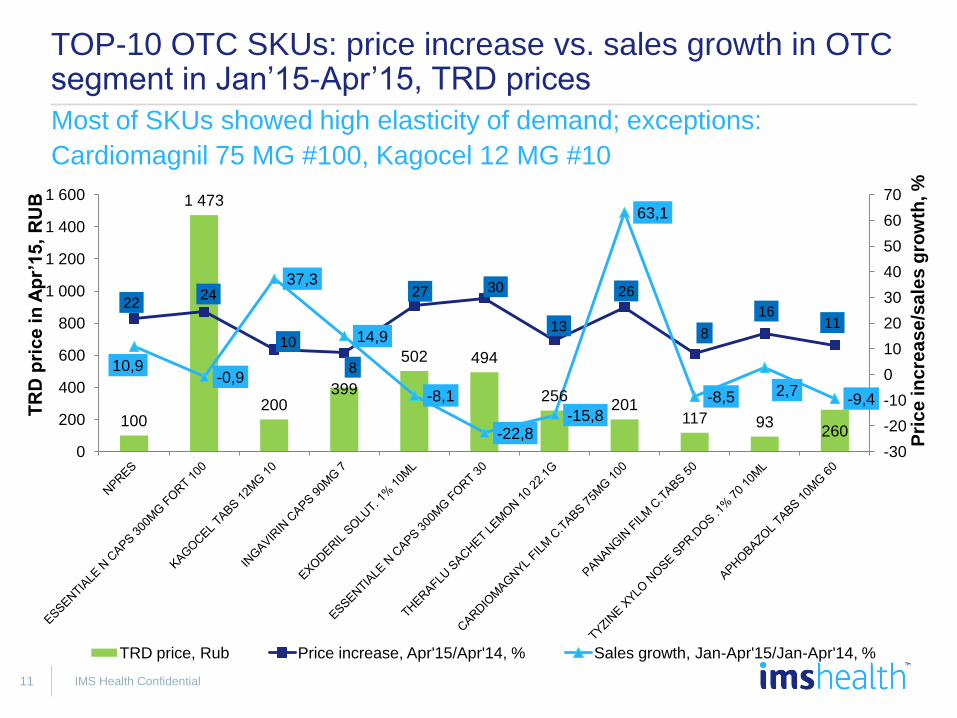

TOP-10 OTC SKUs: price increase vs. sales growth in OTC segment in Jan’15-Apr’15, TRD prices

100

1 473

200 399

502 494

256 201

117 93 260

22 24

10

8

27 30

13

26

8

16 11

10,9 -0,9

37,3

14,9

-8,1

-22,8 -15,8

63,1

-8,5 2,7 -9,4

-30

-20

-10

0

10

20

30

40

50

60

70

0

200

400

600

800

1 000

1 200

1 400

1 600

Pri

ce

in

cre

as

e/s

ale

s g

row

th, %

TR

D p

ric

e in

Ap

r’1

5,

RU

B

TRD price, Rub Price increase, Apr'15/Apr'14, % Sales growth, Jan-Apr'15/Jan-Apr'14, %

Most of SKUs showed high elasticity of demand; exceptions:

Cardiomagnil 75 MG #100, Kagocel 12 MG #10

12

Essential Drug List

(EDL)

IMS Health Confidential

TOP-10 Rx SKUs: Price dynamics in Jan’14-Apr’15, TRD prices

TOP-10 SKU Pr Gr,

%

PRESC 18,6

ALFLUTOP AMP. 10MG 10 1ML

28,0

NISE TABS 100MG 20 41,4

DUPHASTON C.TAB 10MG 20 3,3

ACTOVEGIN AMP. 200MG 5 5ML

18,4

HEPTRAL ENTER.C.TABS 400MG 20

3,6

PREDUCTAL MV C.TAB MR 35MG 60

8,8

OMEZ CAPS 20MG 30 6,4

NIMESIL GRAN F/SUSP 100MG 30 2G

20,8

YAZ FILM C.TABS 28 13,6

CONCOR FILM C.TABS 5MG 50 7,3

TRD price increase,

Apr’15/Apr’14, %

1381

1768

1462

1 515

1 200

1 300

1 400

1 500

1 600

1 700

1 800

ALFLUTOP AMP. 10MG 10 1ML

HEPTRAL ENTER.C.TABS 400MG 20

446 578

528

618

702 673

500

661,12 604

728

874 827

0

100

200

300

400

500

600

700

800

900

PRESC NISE TABS 100MG 20 DUPHASTON C.TAB 10MG 20 ACTOVEGIN AMP. 200MG 5 5ML PREDUCTAL MV C.TAB MR 35MG 60 OMEZ CAPS 20MG 30 NIMESIL GRAN F/SUSP 100MG 30 2G YAZ FILM C.TABS 28 CONCOR FILM C.TABS 5MG 50

13 IMS Health Confidential

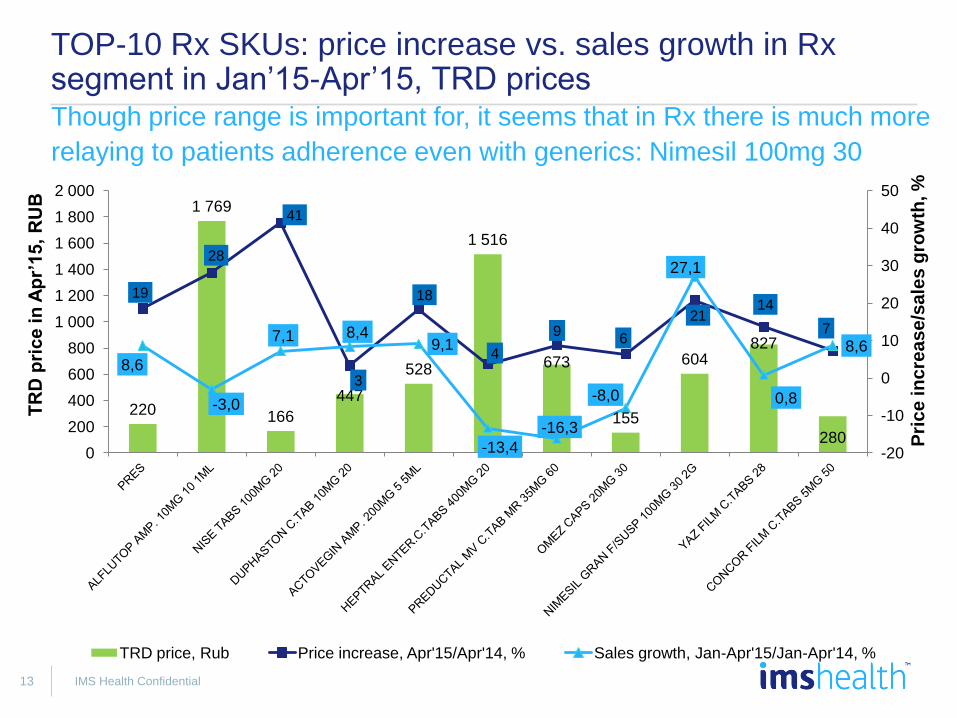

TOP-10 Rx SKUs: price increase vs. sales growth in Rx segment in Jan’15-Apr’15, TRD prices

220

1 769

166

447

528

1 516

673

155

604 827

280

19

28

41

3

18

4

9 6

21 14

7

8,6

-3,0

7,1 8,4 9,1

-13,4

-16,3

-8,0

27,1

0,8

8,6

-20

-10

0

10

20

30

40

50

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

Pri

ce

in

cre

as

e/s

ale

s g

row

th, %

TR

D p

ric

e in

Ap

r’1

5,

RU

B

TRD price, Rub Price increase, Apr'15/Apr'14, % Sales growth, Jan-Apr'15/Jan-Apr'14, %

Though price range is important for, it seems that in Rx there is much more

relaying to patients adherence even with generics: Nimesil 100mg 30

Out of pocket market is expected to grow by 12-18%

Source: IMS Health. Data at TRD prices, drop-out products are excluded due to low figures

0,8%

0,2%

8,7%

Total Growth

10%

New products*

Volume Structure Price

0,5% 0,0%

0,8%

2,4%

7,1%

7,1%

Total Growth

13%

New products*

Volume Structure Price

0,0%

Structural shift and price increase of Non-EDL drive retail market

Out of pocket market growth components in EDL segment in 2014

Out of pocket market growth components in Non-EDL segment in 2014

585

523

30

Base

12-18%

Upside

2015E

615

2014

Out of pocket market growth, Bn RUB

OO

P s

ecto

r tr

ends

Mark

et

gro

wth

14 Russian pharmaceutical market at a crossroad

Importance of pharmacy chains is growing due to business consolidation and capture of significant market share

Context

• Pharmacy chains in Russia accumulated around 61% of total retail sales(in value term) in 1Q 2015 and this trend is expected to continue due to announced plans of key players for further organic and in-organic growth

• Pharmacy business consolidation through M&A process is expected to continue (Top10 chains accumulate 20% of total retail market)

• Marketing unions and other type of virtual chains already become a strong tool for negotiation with suppliers

• In the crisis period chains aim to optimize their operational business through:

o Enlarged number of promotional contracts with manufactures

o Revision of product assortment with focus on more profitable / high margin products

o Reduction in product purchases in 2015 to improve the turnover of products

o Revision of payment & delivery terms with distributors & manufactures

o Closure of unprofitable pharmacies

Pharm

acy c

hain

s &

dis

trib

uto

rs

Source: IMS Health; SCI; 20 interviews with chains

OO

P s

ecto

r tr

ends

15 Russian pharmaceutical market at a crossroad

AVE Group became № 1 in retail Market , while Dr.Stoletov is the most profitable by sale p.outlet due to discounter Ozerki

Chain

mark

et

overv

iew

Vita 0,9

Pharmakor

2,3

Rigla 3,1

A.V.E Group(+36,6;Stariy Lekar) 3,3

1,2 Farmland

1,1

A5 Group

2,0

2,1 Implozia**

PharmaImpeks

Raduga (+Pervaya Pomosh)

1,5

2,1 Doctor Stoletov(+Ozerki)

457

266

490

524

875

1.600

316

1.039

1.233

783

Top10 chains 1Q 2015 market share,%

Number of outlets

4,2

9,9

6,1

6,8

5,3

3,5

15,6

7,2

6,6

10,0

Ø 7,5

Gross sales per outlet, mln RUB

20% 7.583

Russian pharmaceutical market at a crossroad

Source: IMS Health

133%

28%

21%

12%

15%

14%

41%

10%

10%

5%

Pharm

acy c

hain

s &

dis

trib

uto

rs

OO

P s

ecto

r tr

ends

16 Russian pharmaceutical market at a crossroad

Distributor segment is quickly consolidating through M&A

Context

• Distributors in Russia accumulated around 82% of total direct drug sales(in value term) in 1 Q 2015

• As in Retail sector, consolidation process through M&A is also continuing in Distributor segment (Ave Group bought Oriola;R-Pharm and SIA Int.)

• The leading distributor Katren is continuing rapidly growth (+42%), leaving behind previous leader, Protek

• In the crisis period distributors aim to optimize their business through:

Increase the level of concentration through further M&A deals

Further process automation of warehouses

Expanding the geographical presence in regions

Revision of product assortment with focus on more profitable / high margin products

Increase the direct sales

Source: IMS Health; SCI; 20 interviews with chains

Pharm

acy c

hain

s &

dis

trib

uto

rs

OO

P s

ecto

r tr

ends

17 Russian pharmaceutical market at a crossroad

The sector is highly concentrated-TOP 10 distributors generate 82% of total direct drug sales with >50% by 4 main players

18

Chain

mark

et

overv

iew

TOP10 distributors by direct drug sales (in value) ,1Q 2015 %

• The growth of pharmaceutical market is 9% year-on-year (1Q2015 vs 1Q2014)

• The distributors is concentrated- the vast majority of sales is accumulated by TOP 10 players with a wide geographical coverage and

• Katren is a leading distributor with significant MS and growth by +42% comparing to previous year

3,6 4,9

Alliance Healthcare

7,5

-6%

-3%

+52%

+6%

+34%

0%

-2%

+79%

-6%

+42% Katren

1,6 1,6

Protek

2,1 3,2

Rosta

3,1 3,3

Pulse

SIA Int

8,6 8,5

R-Pharm

5,5 9,8

Pharmkomplekt

7,5

10,8

BSS

14,3 13,5

Medexport

13,3 18,9

11,5

2014

2013

Source: IMS Health SCI 2015

Sum=82%

Pharm

acy c

hain

s &

dis

trib

uto

rs

OO

P s

ecto

r tr

ends