creating best-tasting solutions - purecircle€¦ · cases of zero-calorie carbonated soft drinks...

TRANSCRIPT

CREATING BEST-TASTING SOLUTIONS

Full Year Results 2018

Presented by

Paul Selway-Swift

Magomet Malsagov

Rakesh Sinha

18 September 2018

1

DISCLAIMER

• This document, w hich is personal to the recipient and has been issued by PureCircle

Limited (the “Company”), comprises w ritten materials/slides for presentations to be held

in September 2017. This document does not constitute or form part of any offer or

invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any

shares in the Company, nor shall any part of it nor the fact of its distribution form part of

or be relied on in connection w ith any contract or investment decision relating thereto,

nor does it constitute a recommendation regarding the securities of the Company.

• This document has not been verif ied, does not purport to contain all information that a

prospective investor may require and is subject to updating, revision and amending. The

information and opinions contained in this document are provided as at the date of this

presentation and are subject to change w ithout notice. In furnishing this document, the

Company does not undertake or agree to any obligation to provide the attendees w ith

access to any additional information or to update this document or to correct any

inaccuracies in, or omissions from, this document that may become apparent.

• No reliance may be placed for any purposes w hatsoever on the information or opinions

contained in this document or on its completeness. No representation or w arranty,

express or implied, is given by or on behalf of the Company its directors, off icers or

employees or any other person as to the accuracy or completeness of the information or

opinions contained in this document and no liability w hatsoever is accepted by the

Company or any of its members, directors, off icers or employees nor any other person

for any loss how soever arising, directly or indirectly, from any use of such information or

opinions or otherw ise arising in connection therew ith.

• This document and its contents are confidential and may not be reproduced,

redistributed or passed on, directly or indirectly, to any other person or published, in

w hole or in part, for any purpose. This presentation is for information purposes only and

is directed only at, in the United Kingdom, qualif ied investors w ho are persons w ho ( i)

have professional experience in matters relating to investments falling w ithin Article

19(1) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005

(the “Order"); (ii) are persons falling w ithin Article 49(2)(a) to (d) ("high net w orth

companies, unincorporated associations, etc") of the Order; or (iii) are persons to w hom

it may otherw ise be law fully communicated (all such persons together being referred to

as "Relevant Persons"). By attending the presentation to w hich this document relates or

by accepting this document, you w ill be take to have represented, w arranted and

undertaken that you are a Relevant Person.

• Certain statements, beliefs and opinions in this document, are forw ard-looking, w hich

reflect the Company’s or, as appropriate, the Company’s directors’ current expectations

and projections about future events. By their nature, forw ard-looking statements involve

a number of risks, uncertainties and assumptions that could cause actual results or

events to differ materially from those expressed or implied by the forw ard-looking

statements. These risks, uncertainties and assumptions could adversely affect the

outcome and f inancial effects of the plans and events described herein. Forw ard-looking

statements contained in this document regarding past trends or activities should not be

taken as a representation that such trends or activities w ill continue in the future. The

Company does not undertake any obligation to update or revise any forw ard-looking

statements, w hether as a result of new information, future events or otherw ise. You

should not place undue reliance on forw ard-looking statements, w hich speak only as of

the date of this document.

• By attending the presentation to w hich this document relates or by accepting this

document in any other w ay you agree to be bound by the foregoing provisions.

2

Presented by

Magomet Malsagov, Chief Executive Officer

OVERVIEW

3

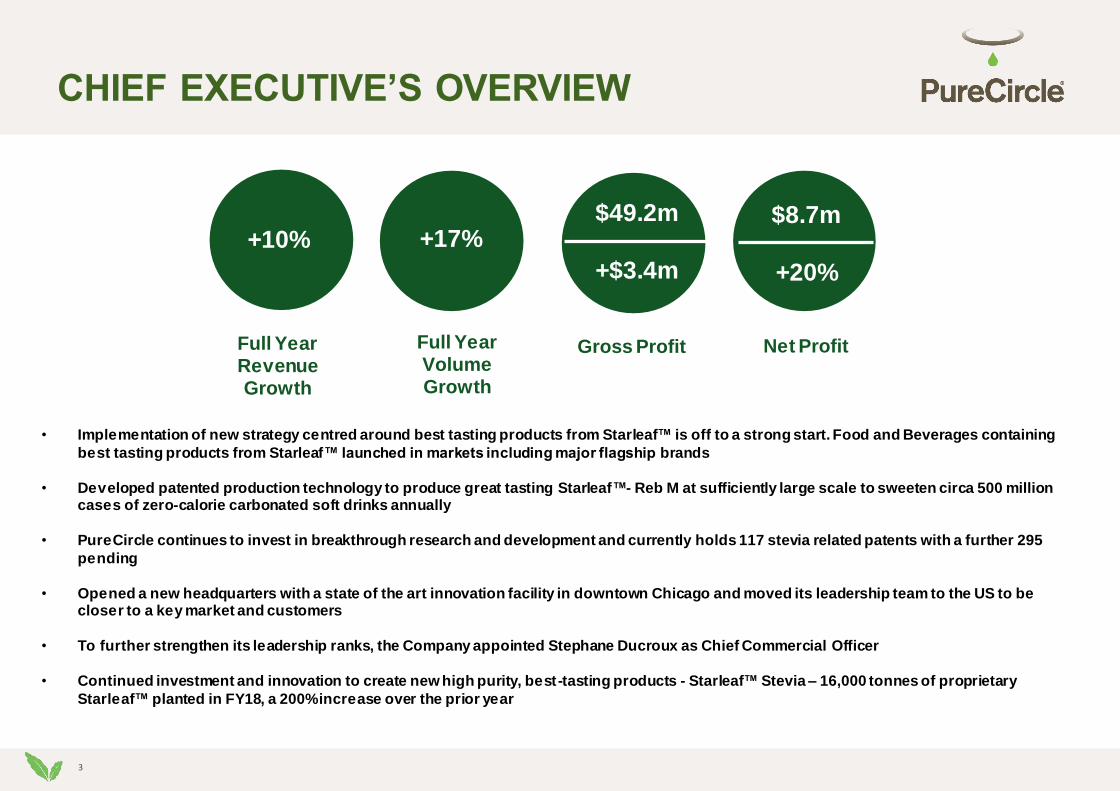

CHIEF EXECUTIVE’S OVERVIEW

• Implementation of new strategy centred around best tasting products from Starleaf™ is off to a strong start. Food and Beverages containing

best tasting products from Starleaf™ launched in markets including major flagship brands

• Developed patented production technology to produce great tasting Starleaf™- Reb M at sufficiently large scale to sweeten circa 500 million cases of zero-calorie carbonated soft drinks annually

• PureCircle continues to invest in breakthrough research and development and currently holds 117 stevia related patents with a further 295

pending

• Opened a new headquarters with a state of the art innovation facility in downtown Chicago and moved its leadership team to the US to be closer to a key market and customers

• To further strengthen its leadership ranks, the Company appointed Stephane Ducroux as Chief Commercial Officer

• Continued investment and innovation to create new high purity, best-tasting products - Starleaf™ Stevia – 16,000 tonnes of proprietary

Starleaf™ planted in FY18, a 200% increase over the prior year

+10%$49.2m

+$3.4m

$8.7m

+20%

Full Year Revenue Growth

Full Year Volume Growth

Gross Profit Net Profit

+17%

4

NEW PRODUCT LAUNCHES Continue to roll out globally

2,934

1,759

1,587

1,497

1,295

1,172

1,030

997

729

708

1

2

3

4

5

6

7

8

9

10

Global new product launches with stevia Top 10 global category by number of product launches

80% of launches

occurred in the past 5

years

2 yr CAGR

12%

23%

17%

20%

12%

19%

4%

8%

13%

15%

1 2 3 4 5 6 7 8 9 10

251 368494

988

1,315

2,2312,408

2,792

3,144

MEA +43% -5%

LTAM +48% +48%

NTAM +17% -22%

Europe +13% +24%

APAC +25% +31%

5 yr CAGR 1yr

T otal +23% +20%

13%

Total Stevia Launches 3,769

*PureCircle Fiscal Year = July 2008 – June 2009, etc.

5

OUR GLOBAL FOOTPRINT

6

HOW WE CREATE VALUE

We have successfully

commercialised a

portfolio that includes

natural sweeteners,

flavours and specialty

ingredients based on

high purity stevia.

PureCircle has deep

expertise across the

value chain, from

seedling to sweetener.

Research & Development (R&D)Multi-disciplinary approach spanning plant breeding, agronomy, biotechnology, biochemistry,

food technology and sensory analysis

Commercialisation• Scientific and Regulatory Affairs

• Sales & Marketing

7

WE TAKE MEASURES TO PROTECT OUR IP

• 12 new patents granted in last 12 months

• 117 granted patents and c.295 pending patent applications worldwide

• Steviol glycosides production (extraction, new sweetener technology, fermentation etc.)

• Steviol glycosides sweetener and flavor compositions

• Steviol glycosides use and applications

• Stevia varieties

8

Lowest Carbon Footprint Lowest Water Footprint Lowest Land Footprint

12-82% 88% 1/5Less carbon than other natural sweeteners. Less water than other natural sweeteners. Size of Delaware = Amount of stevia

needed to replace 20% of today’s sugar consumption.

2015 Carbon Study

KgCo2-e/kg SE*

Comparative Carbon Footprints

2015 Carbon Study

Liters/Kg SE*

Comparative Water Footprints

At least Uses

the land of sugar cane

12% 48% 82%WATER

SUSTAINABILITY:Impact of PureCircle stevia vs. sugar

9

OUR COMMITMENT TO STEVIA: Farming communities

10

FINANCIALREVIEW

Presented by

Rakesh Sinha, Chief Financial Officer

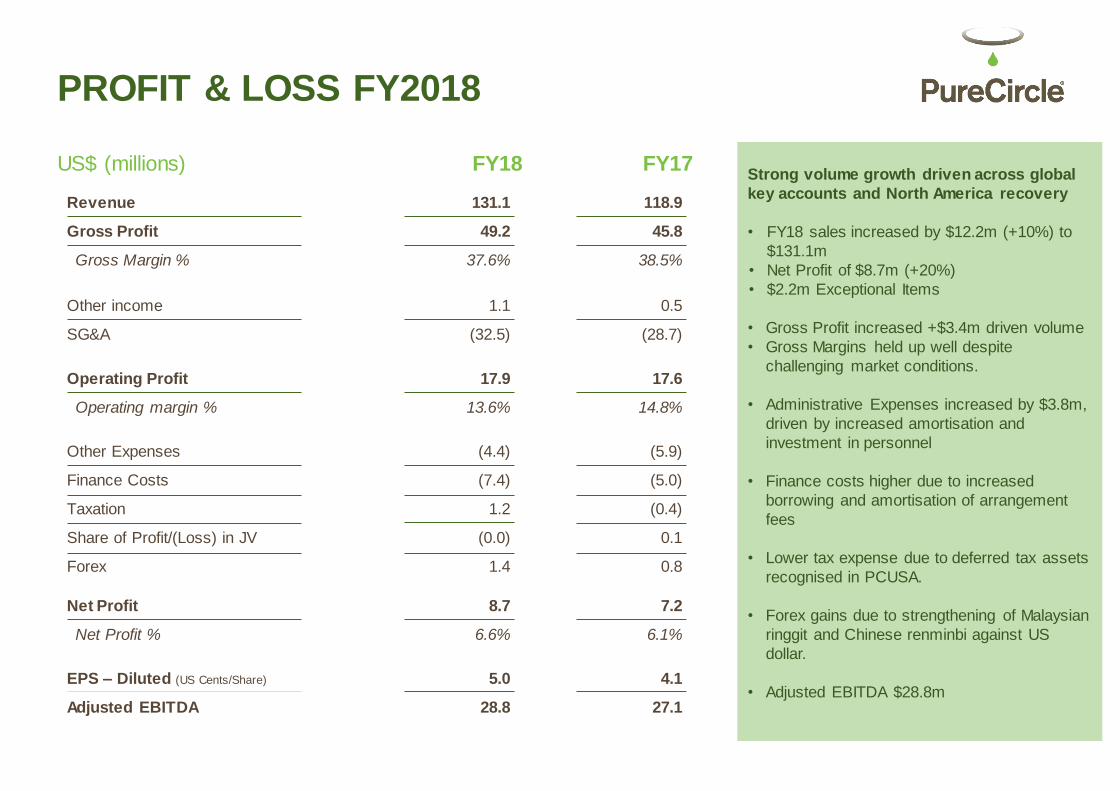

Revenue

Gross Profit

Gross Margin %

US$ (millions)

Other income

SG&A

Operating Profit

Operating margin %

Other Expenses

Finance Costs

Taxation

Share of Profit/(Loss) in JV

Forex

Net Profit

Net Profit %

PROFIT & LOSS FY2018

FY18 FY17

EPS – Diluted (US Cents/Share)

Adjusted EBITDA

118.9

45.8

38.5%

0.5

(28.7)

17.6

14.8%

(5.9)

(5.0)

(0.4)

0.1

0.8

7.2

6.1%

4.1

27.1

131.1

49.2

37.6%

1.1

(32.5)

17.9

13.6%

(4.4)

(7.4)

1.2

(0.0)

1.4

8.7

6.6%

5.0

28.8

Strong volume growth driven across global

key accounts and North America recovery

• FY18 sales increased by $12.2m (+10%) to

$131.1m

• Net Profit of $8.7m (+20%)

• $2.2m Exceptional Items

• Gross Profit increased +$3.4m driven volume

• Gross Margins held up well despite

challenging market conditions.

• Administrative Expenses increased by $3.8m,

driven by increased amortisation and

investment in personnel

• Finance costs higher due to increased

borrowing and amortisation of arrangement

fees

• Lower tax expense due to deferred tax assets

recognised in PCUSA.

• Forex gains due to strengthening of Malaysian

ringgit and Chinese renminbi against US

dollar.

• Adjusted EBITDA $28.8m

DIVERSIFIED REVENUE STREAMS

• Breakthrough and Custom

Blends grew 3x

• North America returned to growth following CBP impact

• Underlying EMEA

performance strong at 12%

• Latin America impacted by

the local economic environment. Increased use

of Artificial Sweeteners observed.

• South Asia grew 42%

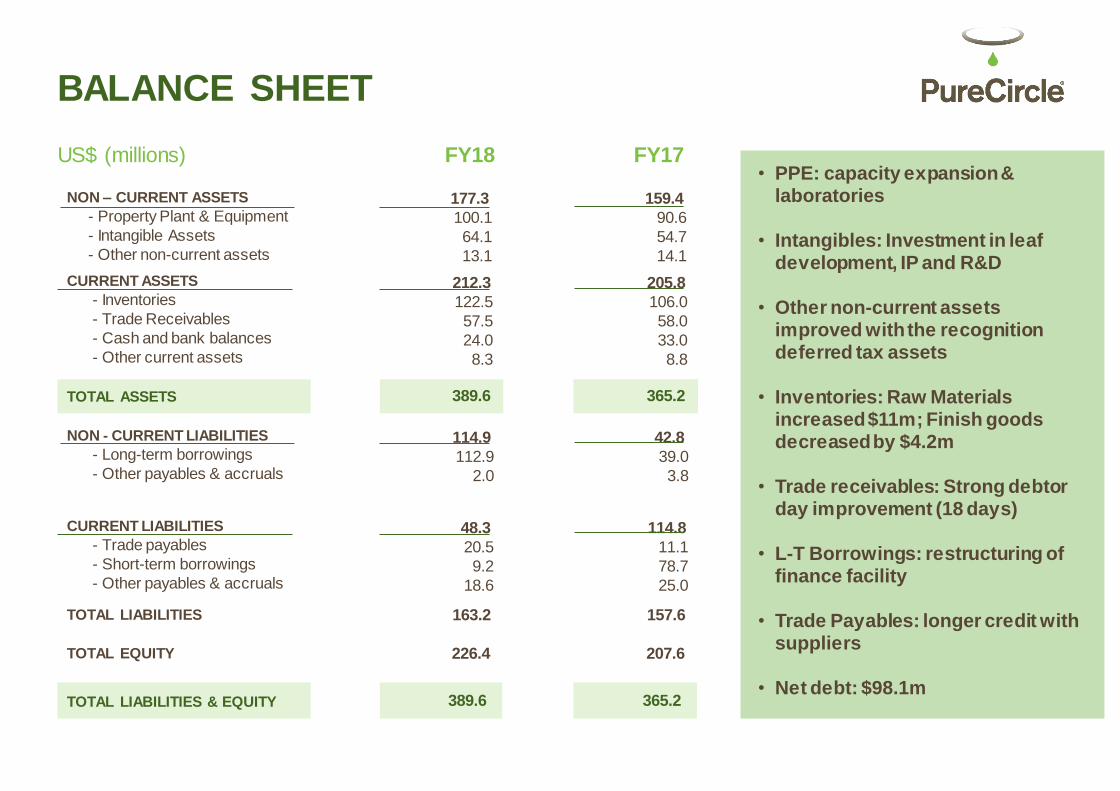

NON – CURRENT ASSETS

- Property Plant & Equipment

- Intangible Assets

- Other non-current assets

TOTAL EQUITY

TOTAL LIABILITIES & EQUITY

BALANCE SHEET

NON - CURRENT LIABILITIES

- Long-term borrowings

- Other payables & accruals

CURRENT ASSETS

- Inventories

- Trade Receivables

- Cash and bank balances

- Other current assets

TOTAL ASSETS

CURRENT LIABILITIES

- Trade payables

- Short-term borrowings

- Other payables & accruals

TOTAL LIABILITIES

177.3

100.1

64.1

13.1

226.4

389.6

212.3

122.5

57.5

24.0

8.3

389.6

114.9

112.9

2.0

48.3

20.5

9.2

18.6

163.2

US$ (millions) FY18 FY17• PPE: capacity expansion &

laboratories

• Intangibles: Investment in leaf development, IP and R&D

• Other non-current assets improved with the recognition deferred tax assets

• Inventories: Raw Materials increased $11m; Finish goods decreased by $4.2m

• Trade receivables: Strong debtor day improvement (18 days)

• L-T Borrowings: restructuring of finance facility

• Trade Payables: longer credit with suppliers

• Net debt: $98.1m

159.4

90.6

54.7

14.1

207.6

365.2

205.8

106.0

58.0

33.0

8.8

365.2

42.8

39.0

3.8

114.8

11.1

78.7

25.0

157.6

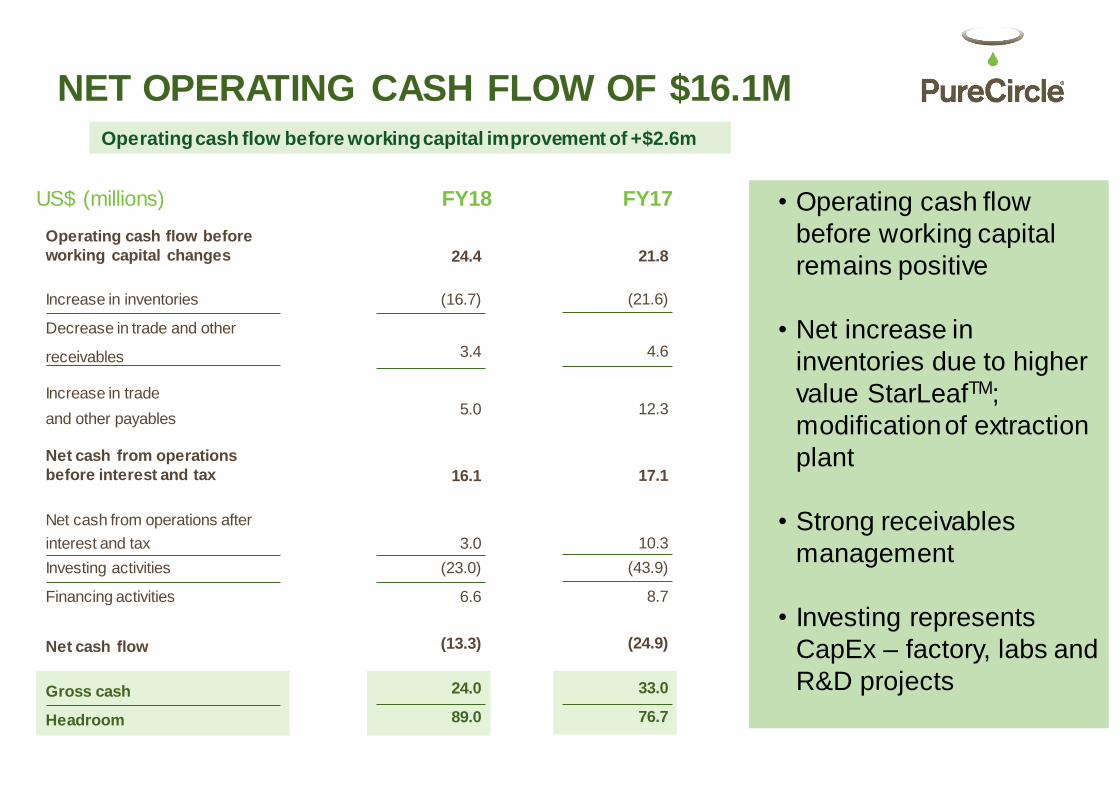

Operating cash flow before

working capital changes

US$ (millions) FY18 FY17

24.4

Increase in inventories

Decrease in trade and other

receivables

Increase in trade

and other payables

(16.7)

3.4

5.0

Net cash from operations

before interest and tax 16.1

Net cash from operations after

interest and tax

Investing activities

Financing activities

3.0

(23.0)

6.6

Net cash flow (13.3)

Gross cash

Headroom

24.0

89.0

Operating cash flow before working capital improvement of +$2.6m

NET OPERATING CASH FLOW OF $16.1M

21.8

(21.6)

4.6

12.3

17.1

10.3

(43.9)

8.7

(24.9)

33.0

76.7

• Operating cash flow

before working capital

remains positive

• Net increase in

inventories due to higher

value StarLeafTM;

modification of extraction

plant

• Strong receivables

management

• Investing represents

CapEx – factory, labs and

R&D projects

1515

Evolution of StrategyStarleafTM Stevia

16

FOOD AND BEVERAGE INDUSTRY: In need of sweetener innovation

• Global obesity crisis

• Sugar tax (passed/proposed)

• Activist advocacy groups

• Good for me

• Good for others

• Good for the planet

proposed new labelhighlighting

calories and added sugars

• Sugar

• Artificial sweeteners

RISING PUBLIC

HEALTH CONCERNSCONSUMERS REDEFINE

HEALTH & WELLBEINGSWEET

UNDER FIRE

17

WE HAVE MOVED BEYOND Reb A taste challenges

REB A

DELAYED ONSETB

ITT

ER

INTENSELINGER

1818

STEVIA LEAF HAS MORE TO OFFER THAN REB A

• 40+ Steviol glycosides in the leaf

• Taste synergies

• Each with unique attributes

19

19

Zero-calorie sweetness from nature…now with

a more sugar-like taste

20

WE ARE SCALING UP STARLEAFTM:Traditional, non-GMO, intelligent plant breeding

Conventional

Variety

2002

StarleafTM Stevia

Variety

2017>20x most sugar-like

glycosides(Reb M, Reb D, others)

vs. conventional leaf

PureCircle Reb A

Variety

20107x Reb A vs.

conventional leaf

21

GLOBAL STARLEAFTM SCALE UP & DIVERSIFICATION PLAN

1 2 3 4

DiversificationScale Up

PureCircle Reb A Variety

StarleafTM Variety

China

Zambia

US

India/Other

1 2 3 4

22

• Rich in extracts with more sugar-like in taste. Fuller

sweetness without linger and aftertaste

• Easier to work with, shorter development times

• Less processed vs. other plant based sweeteners

STARLEAFTM: What It Means For Our Customers

23

New Technology

• As stevia matures from seedling to full-

grown plant, the sweet parts of the

stevia leaf (called glycosides) are

formed.

• The leaf naturally produces enzymes

which convert Reb A to Reb D and then

to Reb M.

• We start with purified stevia leaf extract

with low Reb M and, by adding

enzymes, the maturation of Reb M is

completed, just as the leaf does

naturally.

• This produces a non-GMO stevia leaf

sweetener with high sweetness quality

and no bitterness.

Approvals

• USA

• Canada

• Ecuador

• Peru

• Columbia

• Malaysia

Fema approved as a Flavor (Global)

In Progress:

• Australia (estimate 2019)

• NZ (estimate 2019)

• EU (estimate early 2020)

• JECFA (estimate end of 2020)

• China (estimate 2020)

• Brazil (estimate 2020)

NEW REB M SWEETENER TECHNOLOGY

FY2018Reb M Sweeteners

• Launched StarleafTM Reb M which

produces Reb M from other stevia

sweeteners in the plant

• Reb M is the variant of stevia

sweetener which has the most sugar-

like taste.

• PureCircle has enough Reb M to

sweeten 500M cases of zero-calorie

CSDs

• Targeting to double capacity of Reb M

in 3 years

24

MARKET DRIVERS

Powerful and dynamic

Presented by

Magomet Malsagov, Chief Executive Officer

25

• Worldwide obesity has more than doubled since 1980.

• In 2014, 1.9+ billion adults were overweight. Of these 600+ million were obese.

• Estimated that Worldwide diabetes will impact 1 in 10 adults by 2045 – 629 million.

• Consumers seeking natural sustainable sources for their sweeteners.

http://www.who.int/mediacentre/factsheets/fs311/en/

http://www.diabetesatlas.org/, 7th Ed.

CONSIDERABLE GROWTH In the stevia market

• Stevia approved in Brazil and India. Now 5 billion consumers have access to stevia.

• Sugar taxes being imposed in major markets.

• As of 2018, 80% of the countries that passed taxes did so in the last two years.

• F&B industry now publicly committing to reduce added sugar and artificial sweeteners from their product portfolios.

• Stevia increasingly being used as part of the solution.

• Mintel report: > 17,000 products now launched with stevia: > 80% within the last four fiscal years.

• All major F&B categories now adopting across all geographic regions.

Global obesity and

diabetes continue to

increase

Potential of stevia market materially enhanced

Growing number of products adopting stevia

Growth prospects for the market has grown considerably versus 12 months ago

26

EMERGENCE OF SUGAR TAXAnd labelling is gaining prominence

* N.B. Unverified content – for guidance only.

Sugar drink taxes in effect

Barbados

Belgium

Brunei

Cambodia

Chile

Dominica

Fiji

France

Hungary

Ireland

Laos

Mauritius

Mexico

Nauru

US AREAS

Albany

Berkeley

Boulder

Oakland

Philadelphia

San Francisco

Seattle, Washington

Taxes Proposed/raised for discussion

Australia

Canada

India

Indonesia

Malay sia

Singapore

New Zealand

UAE

Vietnam

Russia

Saudi Arabia

Warning Label/Nutrition Label in Effect

(Not Shown on M ap)

Algeria

Canada

Brunei

Ecuador

Egy pt

Norway

PeruPhilippines

Portugal

Samoa

St. HelenaThailand

UK

South Af rica

Spain

Sri LankaTurkey

Malay sia

Peru

Portugal

Singapore

Taiwan

UK

27

• Joint (FAO & WHO) Expert Committee on Food

Additives (JECFA) approved all Steviol Glycosides

(50+) , including minor sugar-like tasting molecules

from stevia leaf and published the amended

specification (JECFA 20) in December 2017.

• Codex Alimentarius adopted the amended Steviol

Glycoside specification in July 2018, which facilitates

the approval of sugar-like tasting molecules from

stevia leaf in major Latin America, Asia and Africa

markets in near future.

• At present, all Steviol Glycosides from Stevia leaf can

be used in the food & beverage applications in the

US, Canada, Australia, New Zealand, Israel, Brazil;

other authorities will follow.

• Reb M & Reb D derived from Reb A in Stevia leaf

extract is approved in the US, Canada, Mexico and a

few other countries

• New flavor with Stevioside is approved by FEMA in

2017-18

REGULATORY PROGRESS In expanding the use of stevia

28

CHOICE FOR ALTERNATIVE SWEETENERSUse of stevia in new product launches accelerating

Approximately 1 out of 3 new products sweetened with a high intensity sweetener used stevia in 2018*Source: Mintel NPD

Why Choose Stevia?

• No natural alternative to stevia

• Stevia is a force for good in the world

• Much smaller land, carbon and water footprint than sugar

• Highly efficient and cost effective source of sweetness, and 100% natural alternative to sugar with great taste

• No calories, tooth friendly

• Low glycaemic index, safe for diabetics

* N.B. Source Mintel NPD

Stevia moved ahead of Aspartame

29

SUMMARY & OUTLOOK

Significant opportunities for growth

30

SUMMARY & OUTLOOK

Business is back on track with double-digit growth

Market trends in favour of continued robust growth

Everything we do is about helping our customers achieve their goals of reducing sugar/calories/cost of ingredients without compromising taste through high purity stevia solutions

Our innovation pipeline is strong

Our newly evolved StarleafTM strategy enables us to provide the best tasting solutions for our food and beverage customers looking to reduce sugar naturally

We have a unique market position – no one knows more about the stevia leaf than we do

3131

Q&A