costing aand viability of an agri-business

TRANSCRIPT

AAsssseessssmmeenntt GGuuiiddee PPrriimmaarryy AAggrriiccuullttuurree

CCoossttiinngg aanndd vviiaabbiilliittyy ooff aann aaggrrii--bbuussiinneessss

NQF Level: 3 US No: 116237

The availability of this product is due to the financial support of the National Department of Agriculture and the AgriSETA.

Assessor: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Workplace / Company: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Commodity: . . . . . . . . . . . . . . . . . . . Date: . . . . . . . . . . . . . . . . . .

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 22

Version: 01 Version Date: July 2006

BBeeffoorree wwee ssttaarrtt…… his assessment guide contains all necessary activities and instructions that will enable the assessor and

learner to gather evidence of the learner’s competence as required by the unit standard. This guide was designed to be used by a trained and accredited assessor whom is registered to assess this specific unit standard as per the requirements of the AgriSETA ETQA.

Prior to the delivery of the program the facilitator and assessor must familiarise themselves with content of this guide, as well as the content of the relevant Learner Workbook.

The assessor, facilitator and learner must plan the assessment process together, in order to offer the learner the maximum support, and the opportunity to reflect competence.

The policies and procedures that are required during the application of this assessment are available on the website of the AgriSETA and should be strictly adhered to. The assessor must familiarise him/herself with this document before proceeding.

This guide provides step-by-step instructions for the assessment process of:

This unit standard is one of the building blocks in the qualification listed below. Please mark the qualification you are currently assessing, because that will be determined by the context of application:

Title ID Number NQF Level Credits Mark

National Certificate in Animal Production 49048 3 120

National Certificate in Plant Production 49052 3 120

Please mark the learning program you are enrolled in:

Are you enrolled in a: Y N

Learnership?

Skills Program?

Short Course?

TT

Title: Explain costing and the viability of an agri-business.

US No: 116237 NQF Level: 3 Credits: 3

PPlleeaassee NNoottee::

This Unit Standard 116237 Assessment Guide must be read in conjunction with the generic Assessor Guide as prescribed and published by the AgriSETA.

NNoottee ttoo AAsssseessssoorr::

If you are assessing this module as part of a full qualification or learnership, please ensure that you have familiarized yourself with the content of the qualification.

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 33

Version: 01 Version Date: July 2006

As a group, mention all the activities on the farm that you would calculate as a cost to your project. Remember to keep in mind these would include on farm and off-farm activities. Hand in this part to your facilitator or assessor.

Discuss this in groups, and write these on a flip-chart. This action would from part of your formative assessment in class.

Model Answer(s): See Learner guide: page 7: and Log table on page 10. Each production would be different depending on the particular environment. Discuss this with the facilitator and the assessor should come to a conclusion following discussion with the facilitator.

Complete a log table for your crop, and mark the activities you would select which will be reflected in your budget.

Discuss how you would change this log table to fit your specific production cycle. This would enable you to determine the income for this income source in your final budget.

Model Answer(s): The assessor should develop this memorandum in communication with the facilitator.

Instructions to learner:

Discuss with your group 11 SSOO 11

Learner Guide: Page 8 Facilitator Guide: Page 12

Instructions to learner:

Group activity 22 SSOO 11

Learner Guide: Page 10 Facilitator Guide: Page 12

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 44

Version: 01 Version Date: July 2006

1. Distinguish between variable costs and fixed costs.

Model Answer(s): Fixed costs: rent of land, water and salaries. Variable costs: consumables, chemicals, electricity , telephone, The facilitator should, together with the assessor, work on a number of examples within the context of the learner.

2. Give an example of a “fixed cost” of the farm. Why is it a fixed cost?

Model Answer(s): E.g. monthly mortgage payment. Doesn’t fluctuate in value from month to month.

3. Give an example of a “variable cost” of the farm. Why is it a variable cost?

Model Answer(s): E.g. Casual wages. Some times more casuals are employed than other times, so the wage bill varies.

4. Give an example of a “direct cost” of the farm. Why is it a direct cost?

Model Answer(s): E.g. Plants for orchards. Farm has to plant it to gain a crop & it is directly involved in the production.

5. Give an example of an “indirect cost” of the farm. Why is it an indirect cost?

Model Answer(s): E.g. Management salaries. Its contribution is for more than just the final product produced.

Instructions to learner:

Answer the questions 33 SSOO 22

Learner Guide: Page 14 Facilitator Guide: Page 13

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 55

Version: 01 Version Date: July 2006

Complete the template for Gross margin statement and explain what the following terms mean to your group? – Fixed costs, variable costs, sources of income, material costs, labour costs, direct and indirect costs. Have a look at the example provided in the learner workbook.

Model Answer(s): See example given in Learner guide. The facilitator should work together with the assessor in order to design a model answer within the context of the learner.

Complete Template 2.4, an income statement. Study the example given in the learner guide and complete the template after a discussion in groups.

Model Answer(s): There is no specific answer.

Instructions to learner:

Study Template 2.1 in the Learner guide and complete Template 2.2. 44

SSOO 22 Learner Guide: Page 16 Facilitator Guide: Page 13

Instructions to learner:

Group activity 55 SSOO 22 Learner Guide: Page 19 Facilitator Guide: Page 13

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 66

Version: 01 Version Date: July 2006

Explain to a partner what information is given on the balance sheet below, how it works and why such a balance sheet is drawn up:

Model Answer(s): What assets the farm owns and what it is worth. What the farms owes money for. What the owner’s equity is at present?

The learner was required to answer the following questions:

1. What is an “asset” of a farm?

Model Answer(s):

Anything owned by an individual that has a cash value. This includes property, goods, savings or investments.

2. What is a “liability” of a farm?

Model Answer(s): The state of being legally obliged and responsible. Indebtedness: an obligation to pay money to another party.

3. What is “owner’s equity” of a farm?

Model Answer(s): Assets – Liabilities; also known as the owner’s net worth.

Instructions to learner:

Individual exercise 66 SSOO 33

Learner Guide: Page 24 Facilitator Guide: Page 14

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 77

Version: 01 Version Date: July 2006

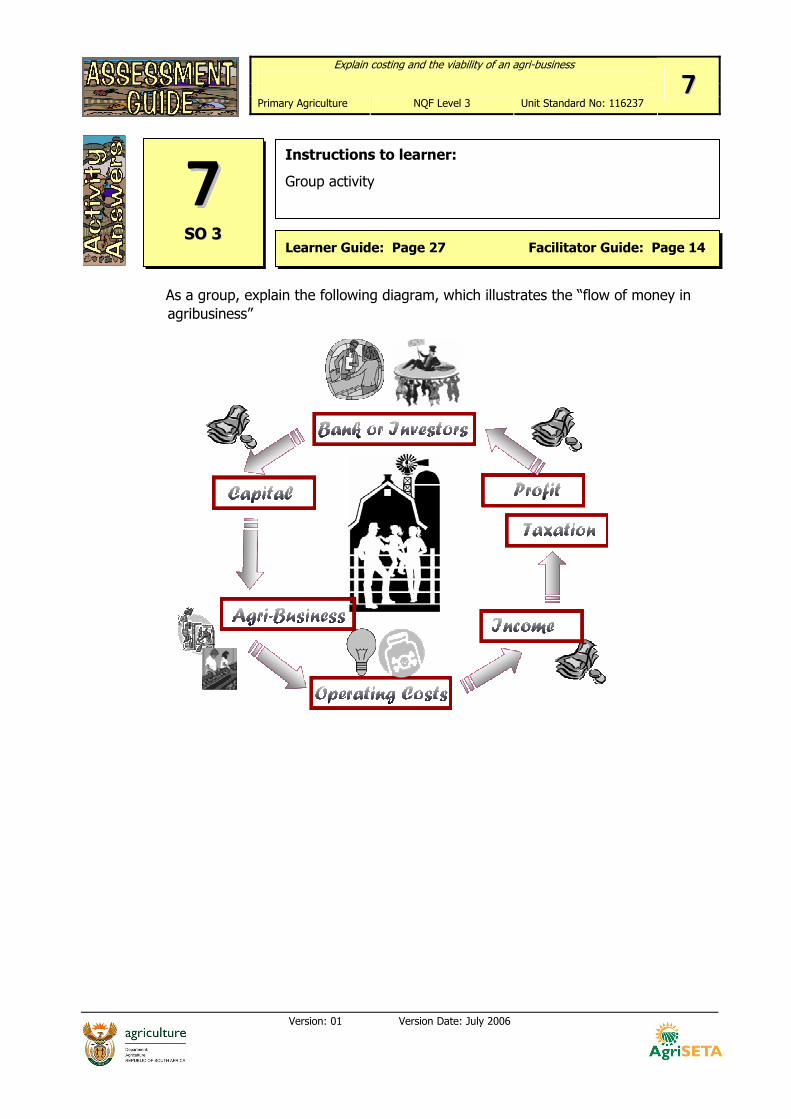

As a group, explain the following diagram, which illustrates the “flow of money in agribusiness”

Instructions to learner:

Group activity 77 SSOO 33

Learner Guide: Page 27 Facilitator Guide: Page 14

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 88

Version: 01 Version Date: July 2006

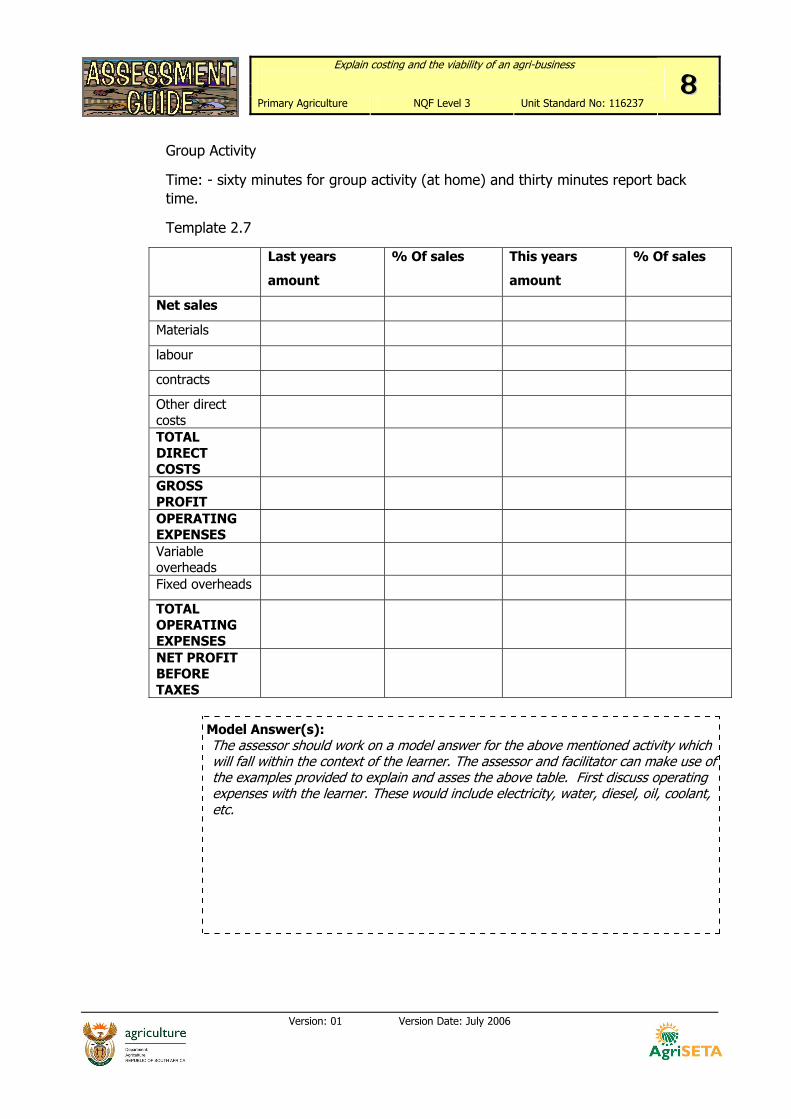

Group Activity

Time: - sixty minutes for group activity (at home) and thirty minutes report back time.

Template 2.7

Last years

amount

% Of sales This years

amount

% Of sales

Net sales

Materials

labour

contracts

Other direct costs

TOTAL DIRECT COSTS

GROSS PROFIT

OPERATING EXPENSES

Variable overheads

Fixed overheads

TOTAL OPERATING EXPENSES

NET PROFIT BEFORE TAXES

Model Answer(s): The assessor should work on a model answer for the above mentioned activity which will fall within the context of the learner. The assessor and facilitator can make use of the examples provided to explain and asses the above table. First discuss operating expenses with the learner. These would include electricity, water, diesel, oil, coolant, etc.

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 99

Version: 01 Version Date: July 2006

Discuss (in your groups) the necessity to have a twelve-month budget and not only an annual budget. This is applicable to agricultural businesses where income and expenses vary over the twelve months. It is also important to notice that an agricultural operation often owes money to various entities, and the repayments of the interest need to be budgeted for. It could happen that in some months a loss may be budgeted for.

Model Answer(s): Twelve-month budgets assist the learner or farmer to be able to cater for the whole of

the production cycle until the end of the financial year. They’re maybe unforeseen

costs and additional expenses. Interest paid over the months need to be budgeted for

as well as the payback of loans. Design additional model answers, from where the

learner originates.

Instructions to learner:

Work with a co-worker 88 SSOO 44

Learner Guide: Page 34 Facilitator Guide: Page 15

MMyy NNootteess …… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 1100

Version: 01 Version Date: July 2006

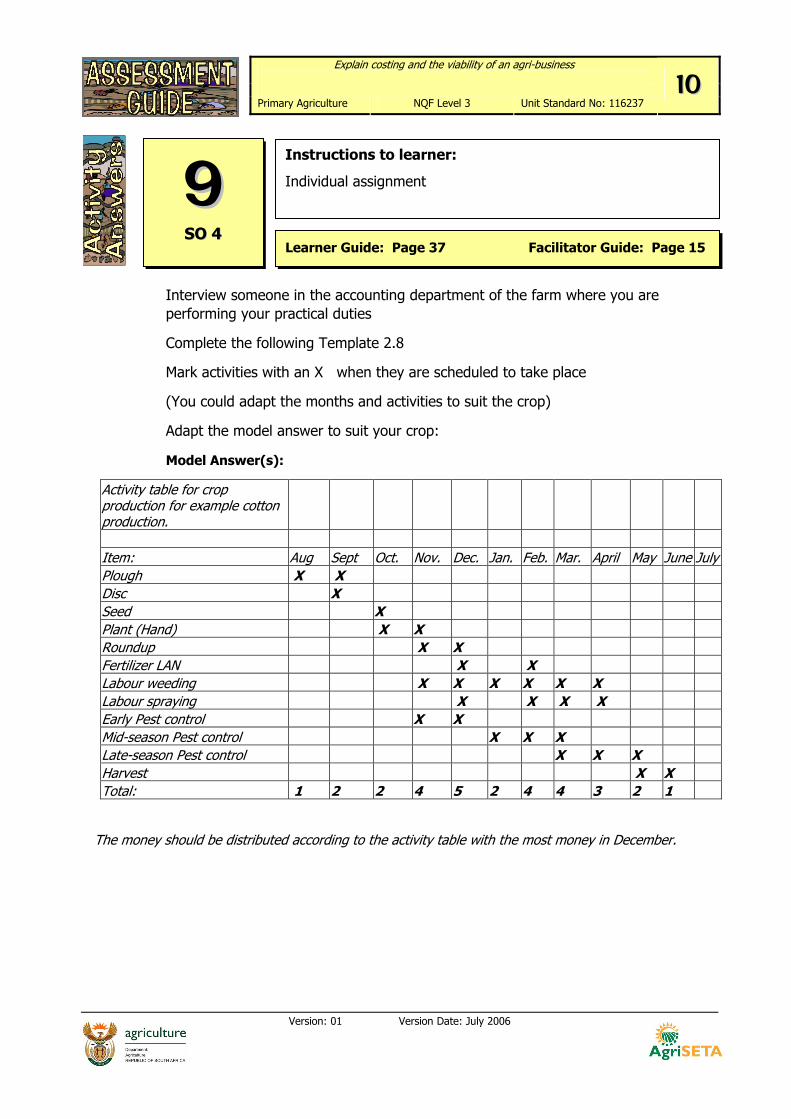

Interview someone in the accounting department of the farm where you are performing your practical duties

Complete the following Template 2.8

Mark activities with an X when they are scheduled to take place

(You could adapt the months and activities to suit the crop)

Adapt the model answer to suit your crop:

Model Answer(s):

Activity table for crop production for example cotton production. Item: Aug Sept Oct. Nov. Dec. Jan. Feb. Mar. April May June JulyPlough X X Disc X Seed X Plant (Hand) X X Roundup X X Fertilizer LAN X X Labour weeding X X X X X X Labour spraying X X X X Early Pest control X X Mid-season Pest control X X X Late-season Pest control X X X Harvest X X Total: 1 2 2 4 5 2 4 4 3 2 1

The money should be distributed according to the activity table with the most money in December.

Instructions to learner:

Individual assignment 99 SSOO 44

Learner Guide: Page 37 Facilitator Guide: Page 15

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 1111

Version: 01 Version Date: July 2006

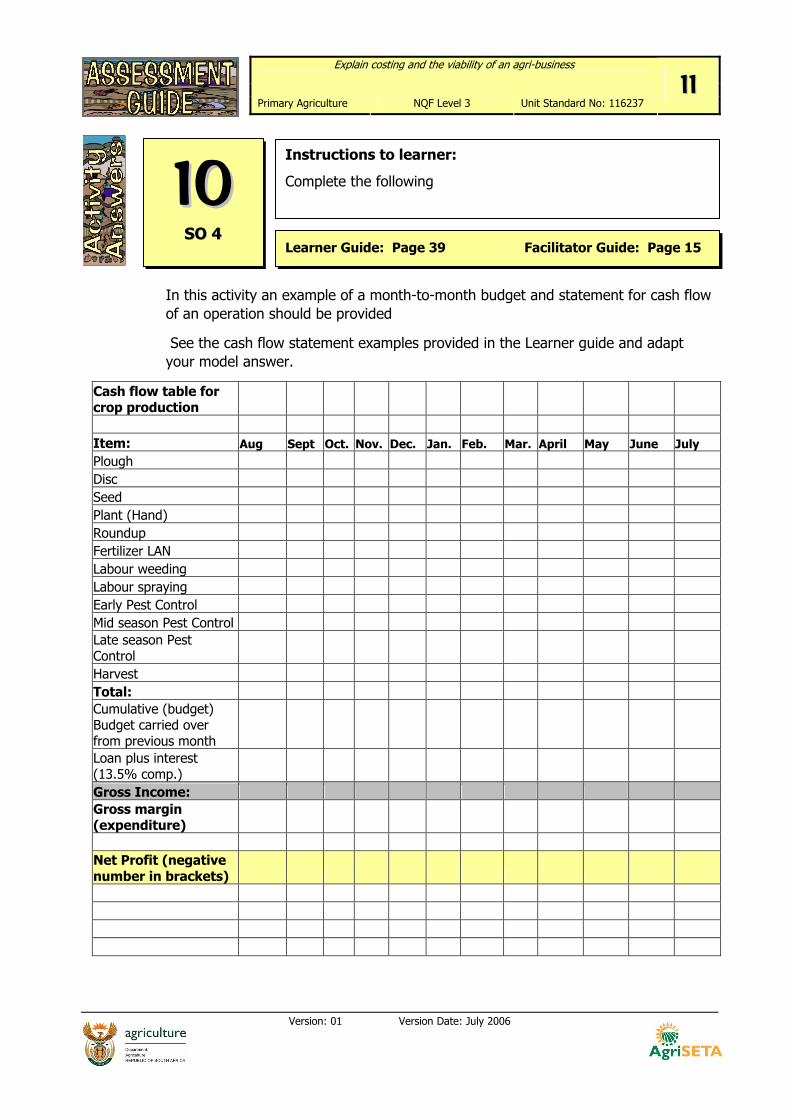

In this activity an example of a month-to-month budget and statement for cash flow of an operation should be provided

See the cash flow statement examples provided in the Learner guide and adapt your model answer.

Cash flow table for crop production Item: Aug Sept Oct. Nov. Dec. Jan. Feb. Mar. April May June July Plough Disc Seed Plant (Hand) Roundup Fertilizer LAN Labour weeding Labour spraying Early Pest Control Mid season Pest Control Late season Pest Control Harvest Total: Cumulative (budget) Budget carried over from previous month Loan plus interest (13.5% comp.) Gross Income: Gross margin (expenditure) Net Profit (negative number in brackets)

Instructions to learner:

Complete the following 1100 SSOO 44

Learner Guide: Page 39 Facilitator Guide: Page 15

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 1122

Version: 01 Version Date: July 2006

In addition ask the learners

1. Why is it important for a farm to make a profit? How is profit determined?

Model Answer(s): Profit is the aim of a business. Without profit, business cannot expand and grow Determine profit by calculating income vs. expenses.

Explain to your group what the different terminology means in a balance sheet. See if you can explain to each other how the assets are calculated and what you understand under Non-current and Current liabilities.

Model Answer(s): The assessor is referred to the Learner guide to get answers to the above mentioned activity.

Instructions to learner:

Speak to an expert on the farm and find out 1111 SSOO 44

Learner Guide: Page 41 Facilitator Guide: Page 15

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 1133

Version: 01 Version Date: July 2006

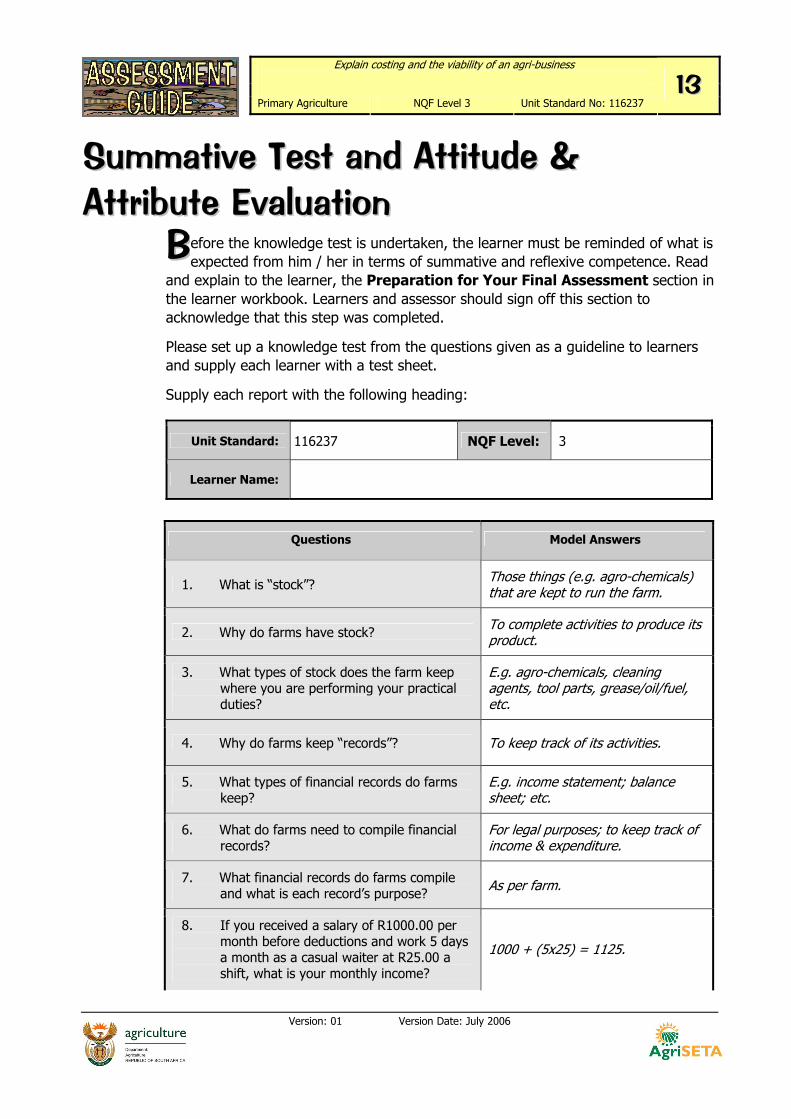

SSuummmmaattiivvee TTeesstt aanndd AAttttiittuuddee && AAttttrriibbuuttee EEvvaalluuaattiioonn

efore the knowledge test is undertaken, the learner must be reminded of what is expected from him / her in terms of summative and reflexive competence. Read

and explain to the learner, the Preparation for Your Final Assessment section in the learner workbook. Learners and assessor should sign off this section to acknowledge that this step was completed.

Please set up a knowledge test from the questions given as a guideline to learners and supply each learner with a test sheet.

Supply each report with the following heading:

Questions Model Answers

1. What is “stock”? Those things (e.g. agro-chemicals) that are kept to run the farm.

2. Why do farms have stock? To complete activities to produce its product.

3. What types of stock does the farm keep where you are performing your practical duties?

E.g. agro-chemicals, cleaning agents, tool parts, grease/oil/fuel, etc.

4. Why do farms keep “records”? To keep track of its activities.

5. What types of financial records do farms keep?

E.g. income statement; balance sheet; etc.

6. What do farms need to compile financial records?

For legal purposes; to keep track of income & expenditure.

7. What financial records do farms compile and what is each record’s purpose? As per farm.

8. If you received a salary of R1000.00 per month before deductions and work 5 days a month as a casual waiter at R25.00 a shift, what is your monthly income?

1000 + (5x25) = 1125.

BB

Unit Standard: 116237 NQF Level: 3

Learner Name:

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 1144

Version: 01 Version Date: July 2006

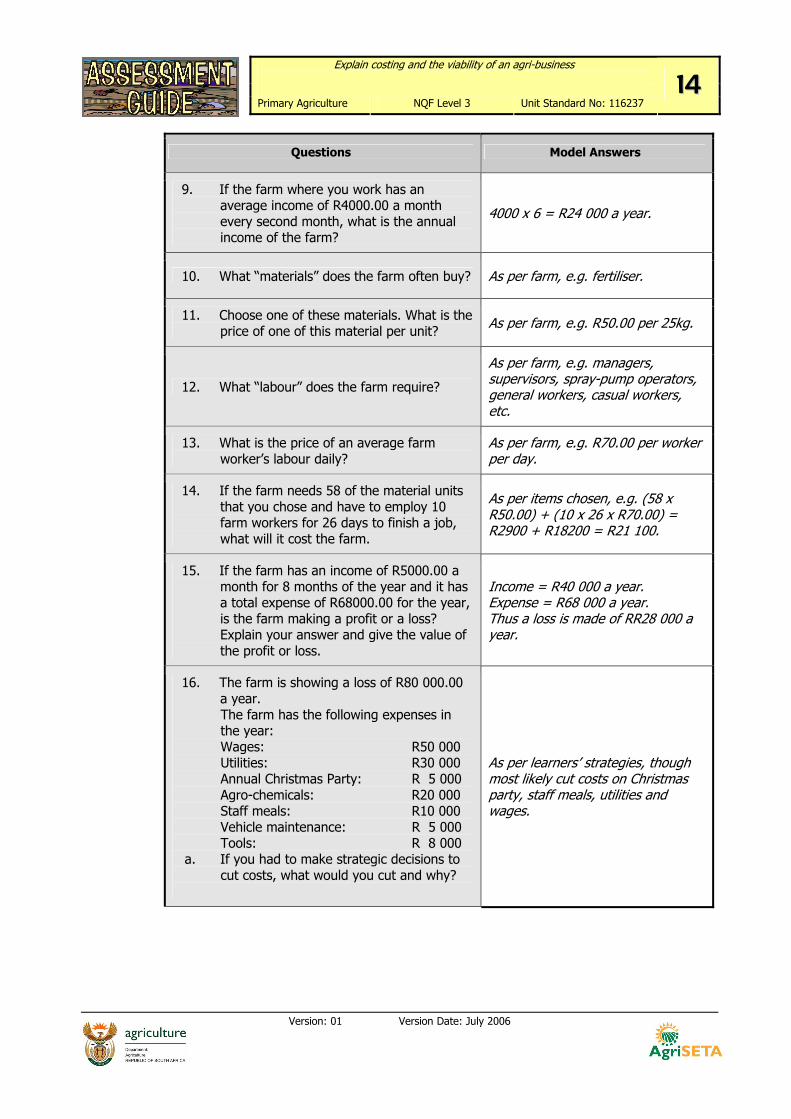

Questions Model Answers

9. If the farm where you work has an average income of R4000.00 a month every second month, what is the annual income of the farm?

4000 x 6 = R24 000 a year.

10. What “materials” does the farm often buy? As per farm, e.g. fertiliser.

11. Choose one of these materials. What is the price of one of this material per unit? As per farm, e.g. R50.00 per 25kg.

12. What “labour” does the farm require?

As per farm, e.g. managers, supervisors, spray-pump operators, general workers, casual workers, etc.

13. What is the price of an average farm worker’s labour daily?

As per farm, e.g. R70.00 per worker per day.

14. If the farm needs 58 of the material units that you chose and have to employ 10 farm workers for 26 days to finish a job, what will it cost the farm.

As per items chosen, e.g. (58 x R50.00) + (10 x 26 x R70.00) = R2900 + R18200 = R21 100.

15. If the farm has an income of R5000.00 a month for 8 months of the year and it has a total expense of R68000.00 for the year, is the farm making a profit or a loss? Explain your answer and give the value of the profit or loss.

Income = R40 000 a year. Expense = R68 000 a year. Thus a loss is made of RR28 000 a year.

16. The farm is showing a loss of R80 000.00 a year. The farm has the following expenses in the year: Wages: R50 000 Utilities: R30 000 Annual Christmas Party: R 5 000 Agro-chemicals: R20 000 Staff meals: R10 000 Vehicle maintenance: R 5 000 Tools: R 8 000

a. If you had to make strategic decisions to cut costs, what would you cut and why?

As per learners’ strategies, though most likely cut costs on Christmas party, staff meals, utilities and wages.

Explain costing and the viability of an agri-business

Primary Agriculture NQF Level 3 Unit Standard No: 116237 1155

Version: 01 Version Date: July 2006

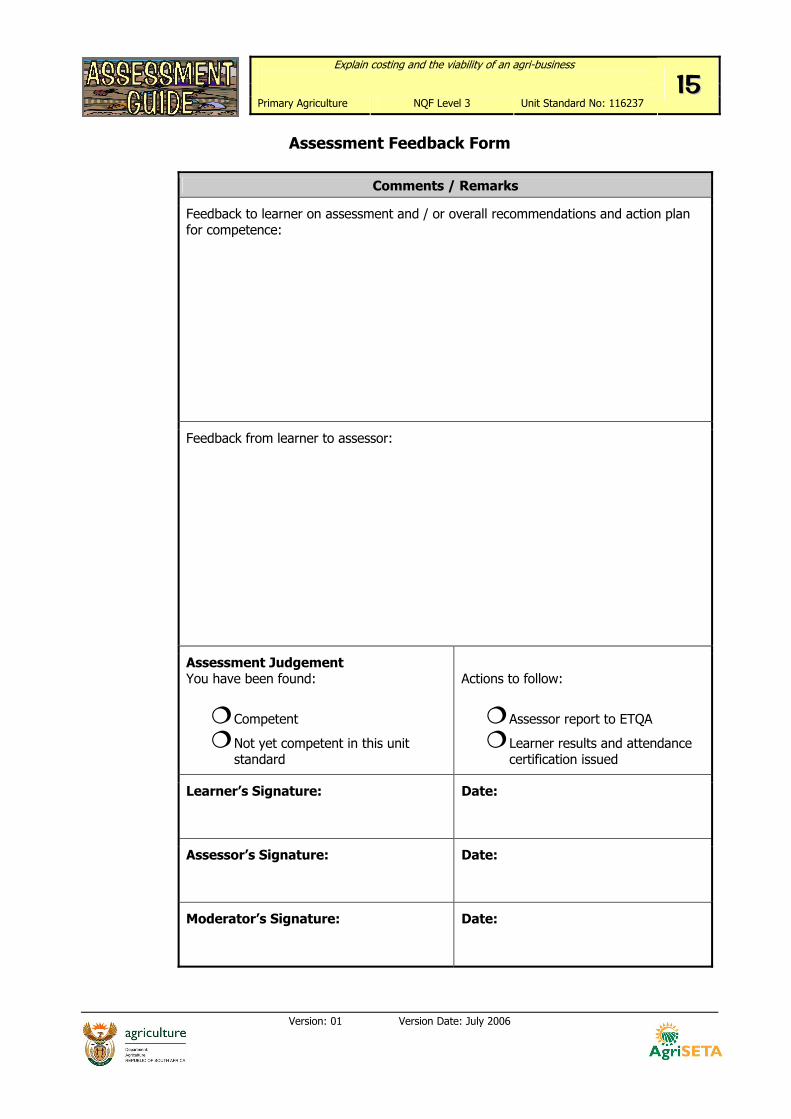

Assessment Feedback Form

Comments / Remarks

Feedback to learner on assessment and / or overall recommendations and action plan for competence:

Feedback from learner to assessor:

Assessment Judgement You have been found:

Competent

Not yet competent in this unit standard

Actions to follow:

Assessor report to ETQA

Learner results and attendance certification issued

Learner’s Signature:

Date:

Assessor’s Signature:

Date:

Moderator’s Signature:

Date: