corporate presentation september 2017 - amazon s3 · corporate presentation september 2017. ......

TRANSCRIPT

Corporate Presentation

September 2017

Disclaimers

General Advisory

The information contained in this presentation does not purport to be all-inclusive or contain all information that readers may require. Prospective investors are encouraged to conduct their own analysis and review of Source Energy

Services Ltd. (“Source” or the “Company”) and of the information contained in this presentation. Without limitation, prospective investors should read the entire record of publicly filed documents relating to Source, consider the advice

of their financial, legal, accounting, tax and other professional advisors and such factors they consider appropriate in investigating and analyzing Source. An investor should rely only on the information provided by Source and is not

entitled to rely on parts of that information to the exclusion of others. Source has not authorized anyone to provide investors with additional or different information, and any such information, including statements in media articles

about Source, should not be relied upon. In this presentation, unless otherwise indicated, all dollar amounts are expressed in Canadian dollars.

An investment in the securities of Source is speculative and involves a high degree of risk that should be considered by potential investors. Source’s’ business is subject to the risks normally encountered in the oil and gas industry

and, more specifically, the frac sand sector of the oilfield services industry, and certain other risks that are associated with Source’s’ stage of development. An investment in Source’s securities is suitable only for those purchasers

who are willing to risk a loss of some or all of their investment and who can afford to lose some or all of their investment.

Forward-Looking Statements

Certain statements contained in this presentation constitute “forward-looking information” or “forward-looking statements” (collectively, “forward-looking statements”) within the meaning of applicable Canadian and United States securities laws relating

to, without limitation, expectations, intentions, plans and beliefs, including information as to the future events, results of operations and Source’s future performance (both operational and financial) and business prospects. In certain cases, forward-

looking statements can be identified by the use of words such as “expects”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes”, “plans”, “seeks”, “projects” or variations of such words and phrases, or state that certain actions, events or results

“may” or “will” be taken, occur or be achieved. Such forward-looking statements reflect Source’s beliefs, estimates and opinions regarding its future growth, results of operations, future performance (both operational and financial), and business

prospects and opportunities at the time such statements are made, and Source undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or circumstances should change. Forward-looking statements are

necessarily based upon a number of estimates and assumptions made by Source that are inherently subject to significant business, economic, competitive, political and social uncertainties and contingencies. Forward-looking statements are not

guarantees of future performance. In particular, this presentation contains forward-looking statements pertaining, but not limited, to: changes to laws and regulations affecting Source’s business; expectations regarding the price of proppants and

sensitivity to changes in such prices; expectations regarding the supply of proppants; outlook for operations; expectations respecting future competitive conditions; industry activity levels; industry conditions pertaining to the frac sand industry; frac sand

costs as a portion of total well costs, logistics costs as a proportion of frac sand landed costs and Source’s objectives, strategies and competitive strengths.

By their nature, forward-looking statements involve numerous current assumptions, known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of Source to differ materially from those

anticipated by Source and described in the forward-looking statements.

With respect to the forward-looking statements contained in this presentation, assumptions have been made regarding, among other things: proppant market prices; future oil, natural gas and natural gas liquids prices; future global economic and

financial conditions; future commodity prices, demand for oil and gas and the product mix of such demand; levels of activity in the oil and gas industry in the areas in which Source operates; the continued availability of timely and safe transportation for

Source’s products, including without limitation, rail accessibility; the maintenance of Source’s key customers and the financial strength of its key customers; the maintenance of Source’s significant contracts or their replacement with new contracts on

substantially similar terms and that contractual counterparties will comply with current contractual terms; operating costs; that the regulatory environment in which Source operates will be maintained in the manner currently anticipated by Source; future

exchange and interest rates; geological and engineering estimates in respect of Source’s resources; the recoverability of Source’s resources; the accuracy and veracity of information and projections sourced from third parties respecting, among other

things, future industry conditions and product demand; demand for horizontal drilling and hydraulic fracturing and the maintenance of current techniques and procedures, particularly with respect to the use of proppants; Source’s ability to obtain

qualified staff and equipment in a timely and cost-efficient manner; the regulatory framework governing royalties, taxes and environmental matters in the jurisdictions in which Source conducts its business and any other jurisdictions in which Source

may conduct its business in the future; future capital expenditures to be made by Source; future sources of funding for Source’s capital program; Source’s future debt levels; the impact of competition on Source; and Source’s ability to obtain financing

on acceptable terms; and, where applicable, each of those assumptions set forth in the footnotes provided herein in respect of particular forward-looking statements

A number of factors, risks and uncertainties could cause results to differ materially from those anticipated and described herein including, among others: the effects of competition and pricing pressures; risks inherent in key customer dependence;

effects of fluctuations in the price of proppants; risks related to indebtedness and liquidity, including Source’s leverage, restrictive covenants in Source’s debt instruments and Source’s capital requirements; risks related to interest rate fluctuations and

foreign exchange rate fluctuations; changes in general economic, financial, market and business conditions in the markets in which Source operates; changes in the technologies used to drill for and produce oil and natural gas; Source’s ability to

obtain, maintain and renew required permits, licenses and approvals from regulatory authorities; the stringent requirements of and potential changes to applicable legislation, regulations and standards; the ability of Source to comply with unexpected

costs of government regulations; liabilities resulting from Source’s operations; the results of litigation or regulatory proceedings that may be brought against Source; the ability of Source to successfully bid on new contracts and the loss of significant

contracts; uninsured and underinsured losses; risks related to the transportation of Source’s products, including potential rail line interruptions or a reduction in rail car availability; the geographic and customer concentration of Source; the ability of

Source to retain and attract qualified management and staff in the markets in which Source operates; labour disputes and work stoppages and risks related to employee health and safety; general risks associated with the oil and natural gas industry,

loss of markets, consumer and business spending and borrowing trends; limited, unfavourable, or a lack of access to capital markets; uncertainties inherent in estimating quantities of mineral resources; sand processing problems; and the use and

suitability of Source’s accounting estimates and judgments.

Although Source has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in its forward-looking statements, there may be other factors, including those described under the

heading “Risk Factors” in Source’s final prospectus dated April 6, 2017 (the “Final Prospectus”), that cause actions, events or results not to be as anticipated, estimated or intended. There can be no assurance that forward-looking statements will

materialize or prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. The forward-looking statements contained in this presentation are expressly qualified by this cautionary statement.

Readers should not place undue reliance on forward-looking statements. These statements speak only as of the date of this presentation. Except as may be required by law, Source expressly disclaims any intention or obligation to revise or update any

forward-looking statements or information whether as a result of new information, future events or otherwise.

2

> SOURCE IS A LEADING FULLY INTEGRATED CANADIAN PROPPANT PROVIDER

Source’s Integrated Platform

3

Mining &

Processing

Rail

Shipping

Transload

StorageDelivery Wellsite

▪ Northern White

resource base

▪ Closed-loop wet plants

can operate year round

▪ Annual production

capacity of over three

million metric tonnes

▪ Fleet of over 1280 railcars

▪ Unit train capable

▪ CN origin-destination

paired

▪ Only Source railcars in

fleet – does not manage

customer railcars

▪ Owned and operated

▪ Largest WCSB network

▪ 3.3 million metric

tonnes of throughput

capacity

▪ Identified expansion

opportunities of 1.5

million metric tonnes of

throughput capacity

▪ Logistics team

manages third party

trucking companies to

coordinate deliveries

▪ Active dispatch

monitoring to minimize

load times and pre-

loading of trailers

▪ Captures additional

margins for logistics

services

▪ Sahara provides capability to

ship and store inventory

directly at the wellsite

▪ Source field solutions team

provides wellsite logistics and

quality control

▪ Presence at the wellsite

provides additional revenue

opportunities

Robust

North

American

Market

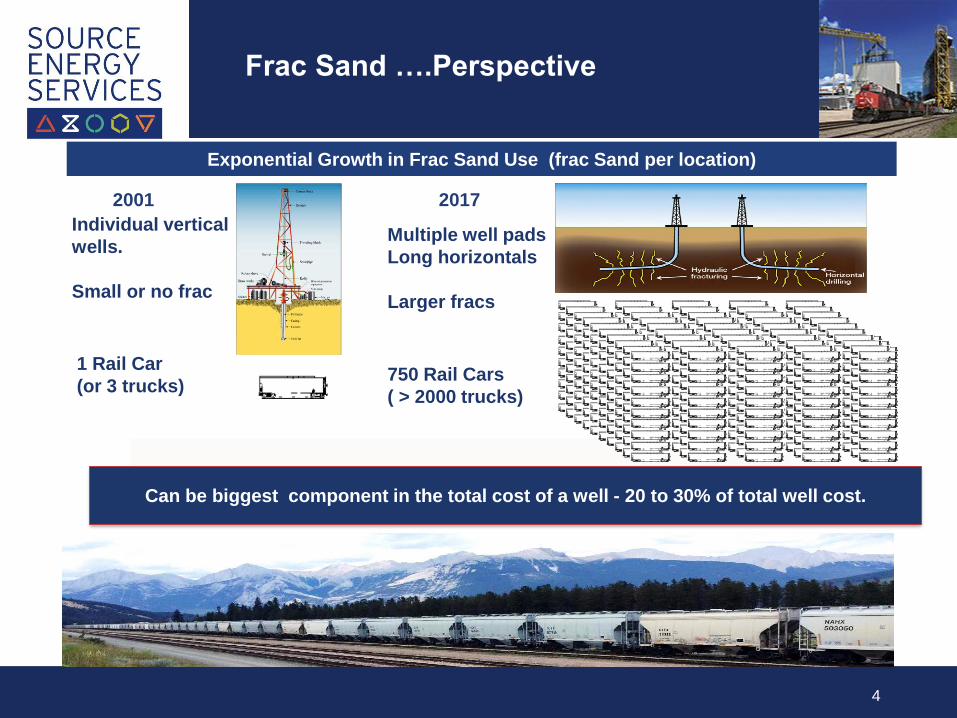

Frac Sand ….Perspective

4

1 Rail Car

(or 3 trucks) 750 Rail Cars

( > 2000 trucks)

Exponential Growth in Frac Sand Use (frac Sand per location)

Individual vertical

wells.

Small or no frac

2001 2017

Multiple well pads

Long horizontals

Larger fracs

Can be biggest component in the total cost of a well - 20 to 30% of total well cost.

A Leading Canadian Integrated

Proppant Supplier

5

1 – Slide Notes

SOURCE – FOCUSED ON SOLVING CANADA’S PROPPANT CHALLENGES

CN Rail Network

Source Terminals

Source Mines(1)

Wellsite Storage

Terminalling & Direct

to Wellsite Solutions

Rail Transport &

Transloading

Frac Sand

Mining & Processing

Challenges for Canadian Proppant Delivery

• Over 1,700 miles from mine to wellsite

• Limited rail line access

• Seasonal weather challenges

• Remote locations

Duvernay

Montney

Other Shale Plays

The Importance of Logistics

6Cost of logistics can represent more than 80% of cost of sand landed in WCSB

Mining

Rail Shipping

Transloading

Trucking to Well

Well Site Storage &

Handling

Rail Car

Leasing

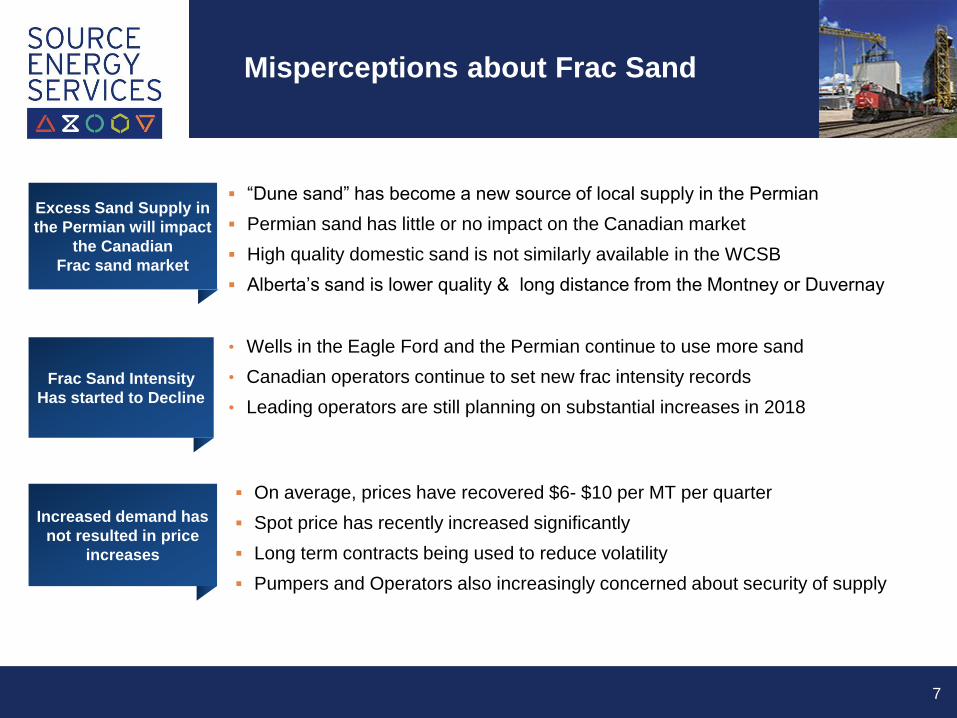

Misperceptions about Frac Sand

7

▪ “Dune sand” has become a new source of local supply in the Permian

▪ Permian sand has little or no impact on the Canadian market

▪ High quality domestic sand is not similarly available in the WCSB

▪ Alberta’s sand is lower quality & long distance from the Montney or Duvernay

Excess Sand Supply in

the Permian will impact

the Canadian

Frac sand market

▪ On average, prices have recovered $6- $10 per MT per quarter

▪ Spot price has recently increased significantly

▪ Long term contracts being used to reduce volatility

▪ Pumpers and Operators also increasingly concerned about security of supply

Increased demand has

not resulted in price

increases

• Wells in the Eagle Ford and the Permian continue to use more sand

• Canadian operators continue to set new frac intensity records

• Leading operators are still planning on substantial increases in 2018

Frac Sand Intensity

Has started to Decline

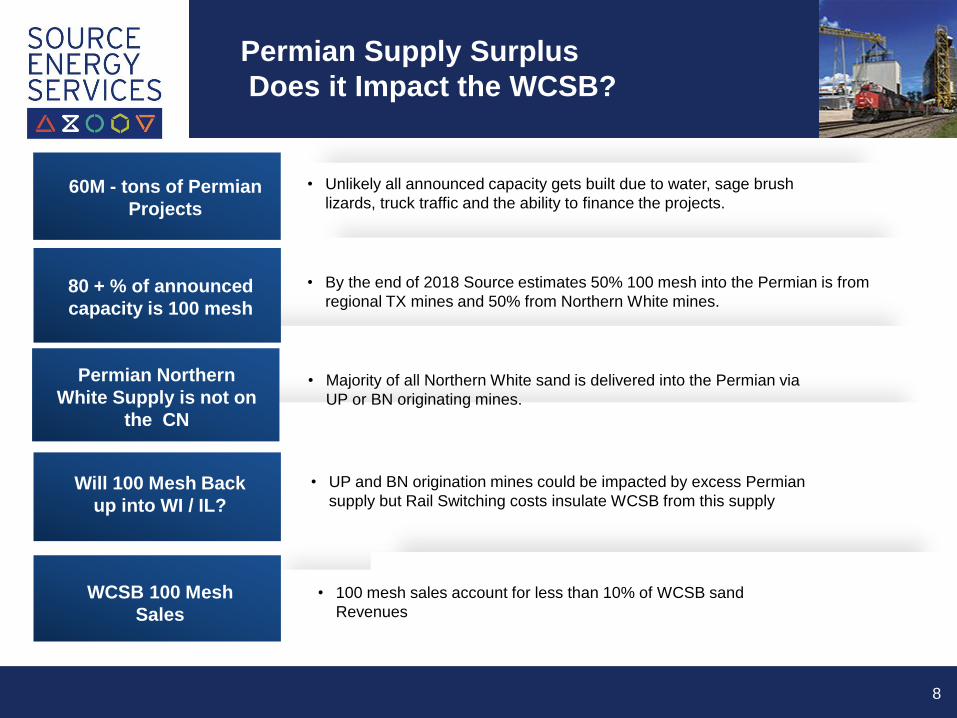

Permian Supply Surplus

Does it Impact the WCSB?

8

• Unlikely all announced capacity gets built due to water, sage brush

lizards, truck traffic and the ability to finance the projects.

Increasing Horizontal

Well Count

Will 100 Mesh Back

up into WI / IL?

Permian Northern

White Supply is not on

the CN

80 + % of announced

capacity is 100 mesh

60M - tons of Permian

Projects

• By the end of 2018 Source estimates 50% 100 mesh into the Permian is from

regional TX mines and 50% from Northern White mines.

• Majority of all Northern White sand is delivered into the Permian via

UP or BN originating mines.

• UP and BN origination mines could be impacted by excess Permian

supply but Rail Switching costs insulate WCSB from this supply

Estimated Impact

to SHLE

WCSB 100 Mesh

Sales

• 100 mesh sales account for less than 10% of WCSB sand

Revenues

Capex forecasted to increase by approximately 55%

from 2016 – 2017 for key Canadian resource plays(2)

Industry moving to longer laterals to improve rate &

recovery via increased reservoir contact

Stages per well have increased >40%

basin-wide since 2013(1)

Increased proppant intensity driving improved economics

Increasing Horizontal

Well Count

Longer Laterals

Tighter

Stage Spacing

Increasing

Proppant per Stage

Drivers of Increasing

Proppant Demand in the WCSB

9

Established Industry Trends Result in

Increased Proppant Demand

1, 2 – Slide Notes

Canadian Proppant Demand is Expected

to Grow

3.2mm MT 5.9mm MT

(see slide 9 for details)

2015 2018E Midpoint

Intensity increases will

likely result in 2018

volumes in excess of

recent estimates

Canadian Proppant Demand

- Continuing to Increase-

10> PROPPANT DEMAND POISED TO INCREASE DUE TO INCREASED FRAC INTENSITY

AND WELL COUNT

1, 2, 3, 4 – Slide Notes

Estimated Canadian Proppant Demand by Play(1)(2)(3)(4)

Million Metric Tonnes

2.4

3.7

3.2

2.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2013 2014 2015 2016 2017E 2018E

Historical Completion Intensity Modern Completion Intensity

Montney

Duvernay

Deep Basin

Viking

Cardium

Bakken/Torquay

Midale/Shaunavon

Higher Frac Intensity

Lower Frac Intensity

90th Percentile

Proppant Intensity

(Q1 2016 Data)

Flat

Proppant Intensity

(Q1 2016 Data)

5 leading operators

report well intensity of

> 5,000 MT in Q1 17(3)

P90 projections for

2018 could exceed

9.0 MM Tonnes

2018 Potential based on

2017 intensity increases

Sand Pricing in the WCSB

11

• Increase in WCSB frac sand demand has resulted in strong

price response

• Prices have recovered $6 - $10 per MT per quarter

• Some operators have commented about 40% price increases

in 2017

• Spot pricing in Montney rumored to be as high as $225 per

MT

• Customers are entering into contacts that protect them from

price volatility and afford greater certainty of supply

Current Pricing Trends

Expectations for Continued Growth

12

Gross Margin

Slide Notes 1,2,3,4 Actual Forecast

Disclaimers

Non-IFRS Measures

In addition to using financial measures prescribed by International Financial Reporting Standards (“IFRS”), references are made in this presentation to “Adjusted

EBITDA”, “EBITDA” and “Adjusted Gross Margin”, which are measures that do not have any standardized meaning as prescribed by IFRS. Accordingly, Source’s use of

such terms may not be comparable to similarly defined measures presented by other entities and comparisons should not be made between such measures provided

by the Company and by other companies without also taking into account any differences in the way that the calculations were prepared.

Adjusted EBITDA represents, for the period presented, EBITDA as adjusted to add back or deduct, as applicable, the following expenses, costs, charges or benefits

incurred in such period which in management’s view are not indicative of the underlying business performance: (a) finance expense excluding interest expense; (b)

Management Fee; (c) fair value adjustment of the Shareholder loan; (d) loss (gain) on asset disposal; (e) loss (gain) on impairment; (f) transaction and professional

fees; (g) loss (gain) on derivative liability; and (h) gain on settlement of deferred revenue (i) stock based compensation. The reconciliation of Net Income to EBITDA and

Adjusted EBITDA is found in Source’s final prospectus dated April 6, 2017 on page FS42 for the years ended December 31, 2014, 2015 and 2016. The reconciliation

of Net Income to EBITDA and Adjusted EBITDA for the three and six ended June 30, 2017 and June 30,2016 is found in Source’s second quarter MD&A. Source’s

prospectus and second quarter MD&A are found on SEDAR and on the Company’s website.

EBITDA represents, for the period presented, net income (loss) plus: (a) income taxes; (b) interest expense; (c) cost of sales – depreciation; (d) depreciation; and (e)

amortization, in each case to the extent deducted from net income in such period determined on a combined basis in accordance with IFRS.

Adjusted Gross Margin represents, for the period presented, gross margin plus costs of sales – depreciation. The reconciliation of gross margin to adjusted gross

margin for the years ended December 31, 2014, 2015 and 2016 is found in Source’s final prospectus dated April 6, 2017 on page FS42. The reconciliation of Gross

Margin to Adjusted Gross Margin for the three and six ended June 30, 2017 and June 30,2016 is found in Source’s second quarter MD&A. Source’s prospectus and

second quarter MD&A are found on SEDAR and on the Company’s website.

13

Slide Notes

14

Slide 5 (The Leading Canadian Integrated Proppant Supplier)--------

1) Includes the Sumner Facility and the Blair Facility.

Slide 12 (Canadian Proppant Demand is Increasing)---------------------

1.)The demand for proppant for 2016 is estimated by multiplying the

historical number of wells drilled based on data provided by geoSCOUT

as of January 25, 2017 in each play by the average amount of proppant

pumped per well, by play, using data for the first quarter of 2016 to

calculate proppant intensity from the data (based on data provided by

the Well Completions & Frac Database as of January 18, 2017).

2) This forecast is based on the assumption that an increase in

producers’ overall capital expenditures will yield a proportional increase

in the number of wells drilled. However, the actual increase in wells

drilled could differ from the increase in capital expenditures in the event

of a relatively greater increase in non-drilling capital expenditures, such

as facility construction or maintenance.

3.) Source’s production capacity, distribution capacity and gross margin

beyond 2017 are based on management’s estimates. The increase in

production includes the potential expansion of the Blair Mine. The

distribution increase includes the previously announced terminal

expansions being completed.

4) Although Source believes the above assumptions and forecasts to be

reasonable, there can be no assurance that these assumptions and

forecasts are accurate, and, as such, undue reliance should not be

placed thereon. See “Forward-Looking Statements” herein and “Risk

Factors” in the Final Prospectus.