corporate presentation...corporate presentation march 2018. 2 forward-looking statements this...

TRANSCRIPT

CORPORATE PRESENTATION

March 2018

2

Forward-looking Statements

This presentation contains projections and

other forward-looking statements within the

meaning of Section 27A of the U.S.

Securities Act of 1933 and Section 21E of

the U.S. Securities Exchange Act of 1934.

These projections and statements reflect the

Company’s current views with respect to

future events and financial performance. No

assurances can be given, however, that

these events will occur or that these

projections will be achieved, and actual

results could differ materially from those

projected as a result of certain factors. A

discussion of these factors is included in the

Company’s periodic reports filed with the

U.S. Securities and Exchange Commission.

Contact:

Karen AciernoDirector – Investor [email protected]

Cimarex Energy Co.1700 Lincoln Street, Suite 3700Denver, CO 80203303-295-3995

3

Who is Cimarex?

1 As of February 14, 20182 As of and for the twelve months ended 12/31/17. See Appendix for non-GAAP definitions and reconciliations to nearest comparable GAAP measure.

Market Cap1 $ 10 billion

Debt/Adj. EBITDA2 1.3x

Production (4Q 17) 201 MBOE/d

Proved Reserves (YE 17) 559 MMBOE

— % Natural gas 48%

— % Proved Developed 83%

— R/P Ratio 8.0x

Quarterly Dividend $0.16/share

4

Returns drive our decisions

Balanced portfolio of assets

– Premier position in the Delaware Basin and Mid-Continent region

– Flexibility through commodity cycles

Continuous idea generation

Strong, disciplined execution

Solid financial position

– Conservative debt levels and ample liquidity

– $401 million in cash at December 31, 2017

What’s Important

5

Improved well performance

– Enhanced completion design

– Allows tighter development well spacing

Six successful spacing pilots announced in 2017

– Additional spacing tests underway

14-wells/section Lower Wolfcamp in Culberson County

18-wells/section Upper Wolfcamp in Reeves County

Wolfcamp and Avalon tests in Lea County, NM

Woodford spacing in Lone Rock

Result: infill development that preserves returns while adding locations (NPV)

2017 Achievements

6

Debt-adjusted production growth per share of 15% year-over-year

Oil led the way growing 27% and grew 36% 4Q17 vs 4Q16

Total E&D capital – $1.28 billion

– D&C capital of $980 million

– 98 net wells brought on production

Proved reserves – 559 MMBOE

– Increase of 16%: PUDs now17% of total proved

– Replaced 211% of 2017 production

30%

25%

45%

Oil NGL Natural Gas

2017 Growth in Production and Reserves

Proved Reserves(MMBOE)

416

522485 482

559

2013 2014 2015 2016 2017

Oil NGL Natural Gas

Daily Production(MBOE)

Total190 MBOE/D

7

26

18

30

24

47

1QA 2QA 3QA 4QA Wells Drilling &Waiting on

Completion at12/31/17Permian Basin Mid-Continent

2017 Net Wells Online

98 net wells completed in 2017

8

High return projects expected to generate 2018 production growth of 11 – 16%

Oil expected to grow 21 – 26% in 2018

– Oil growth estimated at 29 – 34% 4Q18 vs 4Q17

Return driven production growth continues in 2018

Daily Production(MBOE)

30%31% 28%

30%33%

145

164 161

190

211-221

2014 2015 2016 2017 2018E

Oil NGL Natural Gas

9

E&D Capital of $1.6 – 1.7 billion

– 29% increase from 2017

– Within cash available

D&C Capital $1.3 – 1.4 billion

– 82% of Total E&D capital

– Permian Basin ~70%

– Mid-Continent Region ~30%

Additional $80 – 90 million budgeted for midstream

Currently operating 14 rigs

– Ten in Permian

– Four in Mid-Continent

2018 Capital Investment Program

Wolfcamp

Bone Spring

Avalon

Woodford

Meramec

Other

D&C Capital$1.3 – 1.4 billion

10

13

32

51

31

48

1QE 2QE 3QE 4QE Wells Drilling &Waiting on

Completion at12/31/18

Permian Basin Mid-Continent

2018 Net Wells Online

127 net wells planned in 2018

11

2018 Delaware Basin Plans

Wolfcamp

Avalon

Bone Spring

$890 – 940mm

Total D&C Capital

Reeves

Culberson

Lea

Eddy

Ward

Economies of Scale

Multi-well

Single well

83 Net Wells

Wells Drilled by Area

~90% multi-well drilling or takes advantage of existing facilities

12

~216,000 net acres in the fairway

Multiple Wolfcamp Targets

– Culberson/White City Area

~100,000+ net acres

Upper & Lower Wolfcamp

JDA with Chevron

– Reeves County

~63,000 net acres

Upper Wolfcamp

– Lea County

~32,000 net acres

– Ward County

~16,000 net acres

188 total Wolfcamp wells drilled

– 103 long laterals (>7,000’)

Delaware Basin Wolfcamp Overview

2017/18 wells

Lower Wolfcamp

Upper Wolfcamp

Bone Spring

13

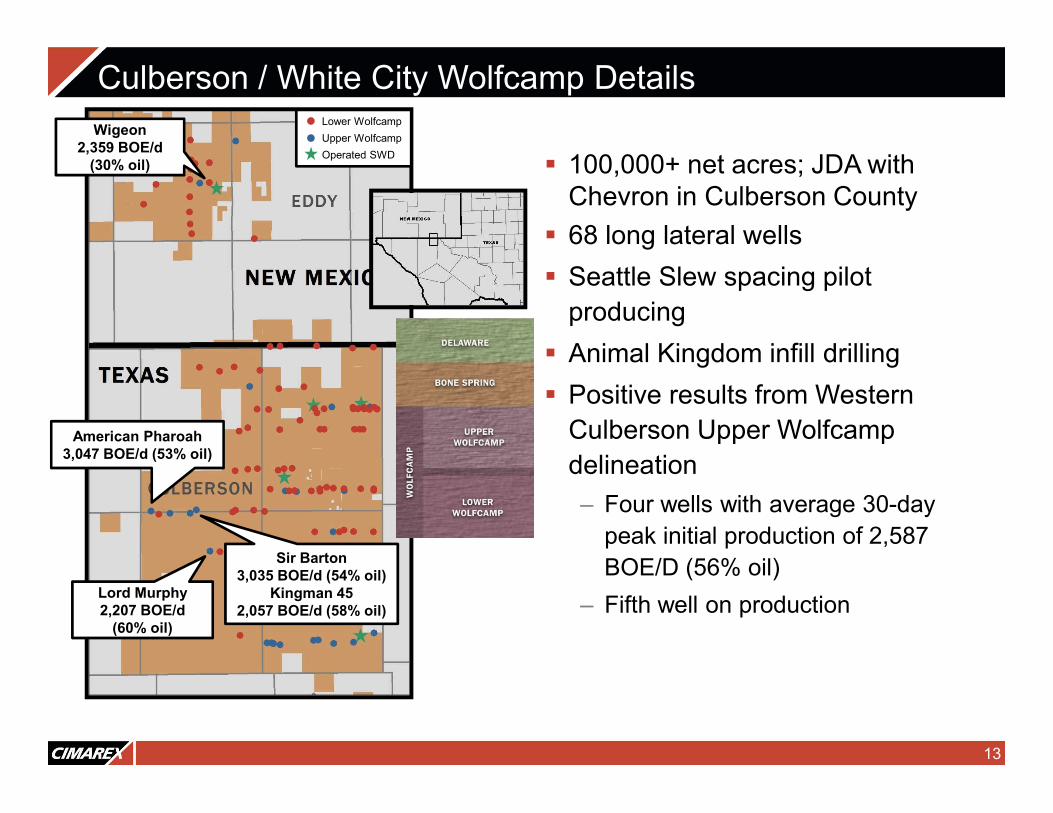

100,000+ net acres; JDA with Chevron in Culberson County

68 long lateral wells

Seattle Slew spacing pilot

producing

Animal Kingdom infill drilling

Positive results from Western

Culberson Upper Wolfcamp

delineation

– Four wells with average 30-day

peak initial production of 2,587

BOE/D (56% oil)

– Fifth well on production

Culberson / White City Wolfcamp DetailsLower Wolfcamp

Upper Wolfcamp

Operated SWD

American Pharoah3,047 BOE/d (53% oil)

Wigeon2,359 BOE/d

(30% oil)

Lord Murphy2,207 BOE/d

(60% oil)

Sir Barton3,035 BOE/d (54% oil)

Kingman 452,057 BOE/d (58% oil)

14

Changes to completion design have resulted in better wells

Fifteen wells with new frac design have average 30-day peak IP of 2,172 BOE/D (52% oil)

– ~30% increase in first year cumulative production

Now testing new landings within Upper Wolfcamp zone

Improving Upper Wolfcamp Results

0

100

200

300

400

500

600

700

0 60 120 180 240 300 360

Days

Old Completion New Completion

Cumuative Production(MBOE)

Culberson Area Long Lateral Upper Wolfcamp

15

Production Improvement - Upper Wolfcamp

731

871

1,239

1,482

1,749

0

500

1,000

1,500

2,000

2013 2014 2015 2016 2017

5,058 5,309 6,926 8,409 9,750Average Lateral

Length (ft)

180 day Average Daily Production per Well(BOE)

Delaware Basin Upper Wolfcamp Wells

16

Resilient Long Lateral ReturnsCulberson Long Lateral Wolfcamp

0%

50%

100%

150%

200%

$30 $40 $50 $60 $70

Realized Oil Price

Upper Wolfcamp - $2/Mcf Lower Wolfcamp - $2/Mcf

Upper Wolfcamp - $1/Mcf Lower Wolfcamp - $1/Mcf

BTAX IRR*

*Assumes full NGL recovery, NGL price is 30% of oil price

17

Tim Tam infill wells generated 67%+ ATAX return

Infills have surpassed parent wells in both landing zones

Results lead to 14 wells per section test

– Animal Kingdom now drilling

-

100

200

300

400

500

600

700

0 60 120 180 240 300 360

Days

Parent well (lower landing)

Tim Tam Infill well (lower landing)

Parent well ( upper landing)

Tim Tam Infill well (upper landing)

Culberson County – Tim Tam Development

1,756’

1,756’200’

Low

er

Wolfca

mp

Tim Tam spacing

Cumulative Production(MBOE)

Lower Wolfcamp

1,216’

1,216’225’

Low

er

Wolfca

mp

Animal Kingdom spacing

225’

18

Similar, strong early cumulative per well production testing 6, 8 or 12 wells per section

Upper Wolfcamp development to begin in 2018

– Two developments planned

0

100

200

0 60 120 180

Days

Gato average well (6 wells/section)

Sunny's average well (8 wells/section)

Seattle Slew average well (12 wells/section)

Culberson County – Upper Wolfcamp Development

Extrapolated Average Cumulative Production per 7,500 ft well (MBOE)

19

32 long lateral wells

– Targeting Upper Wolfcamp

26 – 10,000 ft laterals producing

– Average 30-day peak IP of 1,774 BOE/D (49% oil)

Two downspacing pilots producing

– Wood State (12 wells/section)

– Pagoda State (16 wells/section)

Snowshoe development drilling

– 8 wells; 3 landings (18 wells/section)

Reeves County Focus Area

Wood State

Snowshoe

Pagoda State

Upper Wolfcamp

Operated SWD

20

Upper Wolfcamp

– 10,000 ft laterals

Wood State: 6 wells testing 12 wells per section

– Surpassed Big Timber, previously best long lateral to date

– Average well performing 28% above parent well

Pagoda State: 4 wells testing 16 wells per section

– Average well performing 20% above parent well

Reeves County – Strong Infill Well Results

Pagoda spacing

680’

680’

340’

Uppe

r W

olfc

am

p

Wood State spacing

880’

880’

340’

Uppe

r W

olfca

mp

0

100

200

300

400

500

600

0 60 120 180 240 300 360

Days

Big Timber well

Wood State parent well

Average Wood State well

Average Pagoda State well

Daily Production(MBOE)

21

Exciting multi-pay area

$225 million capital spend in 2018

Avalon activity

– 24,000 net prospective acres

– Triste Draw infill spacing pilot currently drilling

Wolfcamp activity

– 32,000 net prospective acres

– Hallertau infill spacing pilot waiting on completion

Lea County

Red Hills

Red Tank

Triste Draw

Hallertau

Upper Wolfcamp

Avalon

Bone Spring

22

Mid-Continent Basin 2018 Outlook

MeramecWoodford

$370 – 420 million

Total D&C Capital

Meramec

Lone Rock

Other Woodford

Economies of Scale

Multi-well

Single well

43 Net Wells

Activity by Area

~75% multi-well drilling takes advantage of existing facilities

23

Meramec and Woodford Stacked Targets

Meramec: 116,500 net prospective acres

– 100% HBP

Woodford: 136,500 net undeveloped acres (88% HBP)

Mid-Continent Overview

Cana core

Meramec play outline

Woodford play outline

24

52 wells producing with average lateral length of ~7,100 ft– Average 30-day IP of 1,742 BOE/D

(38% oil)

Thirteen – 10,000 ft lateral wells brought online in 2017– Average 30-day IP of 2,383 BOE/D

(37% oil)

28 downspacing pilots online or underway in the play– XEC has interest or data on all but

four

Formulating development plans in the 14N-10W area– Stacked Meramec & Woodford

– Operated almost all of the 24,000 acres leased

– Average 62% working interest

Meramec – The Big Picture

5,000 ft Meramec

10,000 ft Meramec

Meramec play outline

Tillman BIA 1H2,389 BOE/d

(45% oil)

Dupree BIA 1H2,877 BOE/d

(56% oil)

Rocky 1-17H1,912 BOE/d

(67% oil)

Woolfolk 2H2,878 BOE/d

(18% oil)

14N10W

Mike Com 1H4,353 BOE/d

(10% oil)

25

2018 developments

– Steve O - developing remaining section with 8 well spacing

– Lehman - developing remaining section with 8 well spacing

– Miss Mary - testing landing zone with 8 well spacing

Future14N-10W develoment

– Stacked Meramec/Woodford

– Successfully tested 19 wells per section (Leon Gundy)

– Positive results with zone completion sequence at Woolfolk/NIB

Another zone completion test planned

Meramec Development Plans

5,000 ft Meramec

10,000 ft Meramec

Meramec play outline

14N10W

Steve O

Lehman

Miss Mary

Woolfolk /NIB

Mike Com 1H

26

Long history of activity

Emerging Lone Rock play yielding best results to date

Clyde Copeland high density spacing pilot yielding good results

Formulating development plans in the 14N-10W area

Long lateral Leota Jacobs infill deferred to 2019

Woodford Activity

Operated well

Non-operated well

Clyde Copeland

Lone Rock

14N10W

Leota Jacobs

27

Increased density pilot

– 8 wells testing 16 and 20 wells per section

Results positive for future well spacing

– Interference testing on-going

Clyde Copeland Results

0

50

100

150

200

0 30 60 90 120 150 180

Days

Average well (20 well spacing)

Average well (16 well spacing)

Average parent well (9 well spacing)

Cumulative Production(MBOE)

Woodford

Osage

330’16 well spacing

80’

528’20 well spacing

Clyde Copeland development

28

Best Woodford returns in portfolio

~16,000 net contiguous acres

Multiple completion design factors enhance productivity

Infill testing:

– Shelly testing 8 and 12 wells per section (currently drilling)

– JD Hoppinscotch testing 8 wells per section in Woodford

Lone Rock Activity

Shelly

Hines Federal 1H17.2 MMcfed (38% oil)

Meyers 1H13.4 MMcfed (24% oil)

Jimmie Com10.2 MMcfed (22% oil)

Woodford

0

100

200

300

0 30 60 90 120 150 180 210

Days

1st Gen (~1,440 lb/ft)

2nd Gen (~2,800 lb/ft)

3rd Gen (~2,800 lb/ft)

Average Cumulative Production per Well(MBOE)

Woodford 440’

12 well spacing

660’

8 well spacing

Shelly Spacing

JD Hoppinscotch

Woodford640’

JD Hoppinscotch Spacing

160’

Meramec

29

Solid returns from large portfolio

Strong financial position

– $401 million of cash on the balance sheet at 12/31/17

Emphasis on execution

– Preserve returns in inflationary environment

Idea generation

– Technical enhancements to completion design

– Testing even tighter infill well spacing

Ultimate field optimization provides best returns to shareholders

Well-positioned for 2018

30

Appendix

31

2018 Guidance

First Quarter Full Year

Daily Production (BOE) 198 – 207 211 – 221

% Oil 33%

Capital Expenditures ($billion)

E & D $1.6 – 1.7

D & C $1.3 – 1.4

Midstream $0.08 – 0.09

Expenses ($/BOE)

Production $3.75 – 4.35

Transportation, processing & other $3.20 – 3.80

DD&A and ARO accretion $7.50 – 8.10

General and administrative $1.20 – 1.50

Taxes other than income (% of oil and gas revenue) 5.0 – 5.5%

32

Hedges as of February 14, 20182018 2019

First Quarter

Second Quarter

Third Quarter

Fourth Quarter

First Quarter

Second Quarter

Third Quarter

OIL

WTI Oil Collars1

Volume (Bbl/d) 29,000 29,000 25,000 19,000 13,000 13,000 6,000

Weighted Average Floor 47.28 47.83 47.48 48.63 48.92 48.92 50.00

Weighted Average Ceiling 56.33 57.93 57.76 58.80 61.04 61.04 66.82

WTI Swaps2

Volume (Bbl/d) 13,000 14,000 14,000 9,000 6,000 6,000 1,000

Weighted Average Differential3 (0.72) (0.72) (0.72) (0.59) (0.51) (0.51) (0.70)

GAS

PEPL Collars4

Volume (MMBtu/d) 130,000 120,000 90,000 60,000 50,000 50,000 20,000

Weighted Average Floor 2.57 2.39 2.33 2.28 2.23 2.23 1.98

Weighted Average Ceiling 2.93 2.70 2.56 2.49 2.46 2.46 2.16

El Paso Perm Collars5

Volume (MMBtu/d) 90,000 90,000 70,000 50,000 40,000 40,000 20,000

Weighted Average Floor 2.52 2.22 2.14 2.06 1.98 1.98 1.65

Weighted Average Ceiling 2.84 2.48 2.32 2.23 2.14 2.14 1.80

Total Natural Gas Collars

Volume (MMBtu/d) 220,000 210,000 160,000 110,000 90,000 90,000 40,000

Notes:1 WTI refers to West Texas Intermediate oil prices as quoted on the New York Mercantile Exchange 4 PEPL refers to Panhandle Eastern Pipe Line Tex/OK Mid-Continent as quoted on Platt’s Inside FERC 2 Index price on basis swaps is WTI Midland as quoted by Argus Americas Crude 5 El Paso Perm refers to El Paso Permian Basin index as quoted on Platt’s Inside FERC3 Index price on basis swaps is WTI NYMEX less weighted average differential shown in table

33

Permian Region Production

Daily Production(MBOE)

68

74

81

99

94

87

80

85 86 85

96

107105

112

0

25

50

75

100

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17

Oil NGL Natural Gas

34

Mid-Continent Region Production

Daily Production(MBOE)

6864

5856

54

64

70

65

5963

70

85 8588

0

25

50

75

Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17

Oil NGL Natural Gas

35

Efficiency Gains Continue in LOE

$0.81 $0.62 $0.49 $0.44

$1.63 $1.49

$1.30 $1.17

$0.83

$0.61

$0.28 $0.37

$1.97

$1.45

$1.15 $1.11

$1.25

$0.83

$0.73 $0.68

$6.48

$5.00

$3.95 $3.77

2014 2015 2016 2017

Compressor Rental & Repair Labor/OtherWater Disposal Repairs, Maintenance, Chemicals & RentalsWorkovers

$/BOE

36

Non-GAAP Reconciliation

Reconciliation of Net Income to EBITDA and Adjusted EBITDA1

($ in Millions) 2014 2015 2016 2017

Net income (loss) $ 526 $(2,580) $ (409) $ 494

Income tax expense (benefit) 310 (1,472) (214) 188

Interest expense, net of capitalized 37 55 62 52

DD&A and ARO accretion 786 741 400 462

EBITDA 1,659 (3,256) (161) 1,196

Impairment of oil and gas - 4,033 758 -

Adjusted EBITDA 1,659 778 597 1,196

1The above table provides a reconciliation from generally accepted accounting principles (GAAP) net income (loss) to non-GAAP EBITDA and non-GAAP adjusted EBITDA, which excludes ceiling test impairments

Debt Adjusted Shares (Using trailing 12-mo (TTM) stock price)

2016 2017

Basic shares outstanding (in 000s) 95,124 95,437

Debt adjusted shares outstandingYE Debt, net

TTM stock price847,124

115.071,099,466

114.00

Equivalent shares issued using TTM stock price 7,362 9,644

Debt adjusted shares using TTM stock price 102,485 105,082

37

Non-GAAP Reconciliation

Reconciliation of cash flow from operations1

Three months Ended Dec 31

($ in Millions) 2017 2016

Net cash provided by operating activities $ 341 $ 185

Change in operating assets and liabilities

16 34

Adjusted cash flow from operations $ 357 $ 219

Finding & development (F&D) cost

2017

Additions to proved reserves (MMBOE)

Revisions of previous estimates (10.0)

Extensions & discoveries 156.8

Purchase of reserves 0.2

Total Additions (all sources) 147.0

Total Capital ($MM) $ 1,281

F&D Costs (all sources) ($/BOE) $ 8.71

Drilling F&D cost (extensions & discoveries) ($/BOE) $ 8.17

Debt/Cap calculation

($ in Millions)Dec 31,

2017

Long-term debt (principal) $ 1,500

Stockholders equity 2,568

Total capitalization 4,068

Long-term debt/total capitalization 37%

Debt/Adjusted EBITDA calculation

Twelve monthsEnded Dec 31

($ in Millions) 2015 2016 2017

Long-term debt (principal)

$1,500 $1,500 $1,500

Adjusted EBITDA 778 597 1,196

Debt/Adjusted EBITDA 1.9x 2.5x 1.3x

1Management uses the non‐GAAP measure of adjusted cash flow from operations as a means of measuring the company's ability to fund its capital program and dividends, without fluctuations caused by changes in current assets and liabilities, which are included in the GAAP measure of cash flow from operating activities. Management believes this non‐GAAP measure provides useful information to investors for the same reasons, and that it is also used by professional research analysts in providing investment recommendations pertaining to companies in the oil and gas exploration and production industry.

38

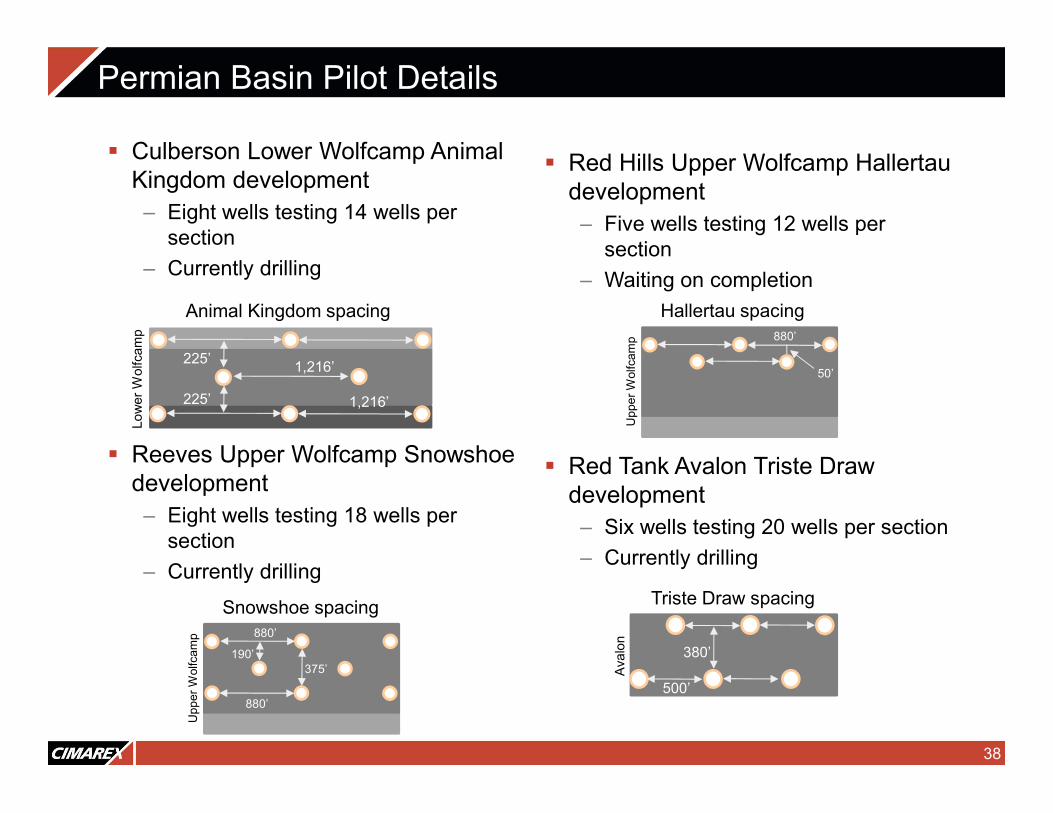

Culberson Lower Wolfcamp Animal Kingdom development

– Eight wells testing 14 wells per section

– Currently drilling

Reeves Upper Wolfcamp Snowshoe development

– Eight wells testing 18 wells per section

– Currently drilling

Red Hills Upper Wolfcamp Hallertaudevelopment

– Five wells testing 12 wells per section

– Waiting on completion

Red Tank Avalon Triste Draw development

– Six wells testing 20 wells per section

– Currently drilling

Permian Basin Pilot Details

1,216’

1,216’225’

Low

er

Wolfca

mp

Animal Kingdom spacing

225’

Snowshoe spacing880’

880’

375’

Upp

er

Wolfc

am

p

190’

500’

380’

Ava

lon

Triste Draw spacing

Hallertau spacing880’

Uppe

r W

olfca

mp

50’