corporate governance report - … · 4 amp capital: corporate governance report | february 2016 ceo...

TRANSCRIPT

CORPORATE GOVERNANCE REPORT: ESG insights & proxy voting FEBRUARY 2016

2 AMP Capital: Corporate Governance Report | February 2016

In this issue...AMP Capital’s approach to ESG: The what, why and how

3

CEO pay: How much is too much?

4

Gender diversity: Will the gender diversity of boards reach 30 per cent?

7

Paris Climate Conference: What to make of the Paris Agreement

10

Shareholder engagement: Current themes

12

Overview of proxy voting: > Australia > International > Externally-managed portfolios

131618

Meet the ESG investment research team 19

AMP Capital: Corporate Governance Report | February 2016 3

AMP Capital’s approach to ESG: the what, why and how AMP Capital is one of the longest-standing managers of responsible investment funds in Australia.

Understanding how a range of environmental, social and governance (ESG) factors may affect an investment has long been an integral part of AMP Capital’s investment process.

Long before becoming one of Australia’s first signatories to the Principles for Responsible Investment in 2007, AMP Capital dedicated specific resources to understanding the impact of ESG factors. The key motivation for considering ESG issues within an investment process is to gain deeper insight into areas of risk and opportunity that could materially impact the value or performance of an investment.

As such, AMP Capital complements fundamental investment analysis with a thorough consideration of environmental, social and governance factors. ESG investment analysts pride themselves on digging deeper into the ESG risks and opportunities that each company faces. Over the long-term, factors such as a company’s governance, leadership and their attitude towards risk are likely to have a greater influence on company value and share-price performance than the tangible factors that are traditionally considered by investment analysts.

For many years now, AMP Capital has compared the ESG attributes of individual companies and considered how these factors impact relative value and the long-term sustainability of company earnings. Our research focuses on a broad range of factors such as demographic trends, climate change, technological advances, risk management, supply-chain management, employee engagement, leadership, company culture, board diversity and occupational health and safety performance.

Unsurprisingly, when company earnings rely on them taking short-cuts and exploiting under-priced pollution, under-paid labour or weak regulation, the current level of their earnings may not be sustainable.

A deep dive into how a company is managing its ESG risks and opportunities can deliver investment insights that lead to better informed investment decisions and potentially higher returns1.

It is a major task to identify the relevant industry-level drivers and then assess how each company manages those drivers. In order to gain new insights, and a competitive advantage, analysts must look beyond the information routinely reported by companies.

WHICH ESG FACTORS ARE IMPORTANT?

The bulk of a company’s value is typically, and increasingly, driven by a range of intangible factors. These drivers can generally be split into two categories: sustainability drivers that relate to the entire industry (such as the relevant demographic, regulatory and technological change) and intangible drivers that focus on each company’s response.

While the specific sustainability drivers and their relative importance will tend to vary from industry to industry, there is a clear correlation between how effectively a company manages them and financial returns.

Before embarking on ESG analysis, it makes sense to take a step back and consider the factors driving earnings growth at the industry level. When determining which intangible drivers are most relevant to a particular industry, an ESG analyst would consider:

> Environmental factors: How likely is it that the value of a company in this sector will be influenced by how well they perform as a steward of the natural environment?

> Social criteria: How likely is it that the value of a company in this sector will be impacted by how a company manages relationships with its employees, suppliers, customers and the communities where it operates?

> Governance: How likely is it that the value of a company in this sector will be impacted by the quality of its leaders, the fairness of its pay structures, the audits and internal controls, and finally the rights of shareholders?

Pleasingly, AMP Capital’s commitment to ESG research has been rewarded with clear evidence of a strong correlation between AMP Capital’s proprietary ESG assessment of companies and their financial return. For this reason, AMP Capital believes thorough analysis of intangible drivers – or ESG research – is an important element of fundamental stock research.

The key motivation for considering ESG issues within an investment

process is to gain deeper insight into areas of risk and opportunity

The greatest driver of company value is not what you can see, but what lies beneath the surface.

4 AMP Capital: Corporate Governance Report | February 2016

CEO pay: How much is too much?

AMP Capital’s research shows:

> The average CEO in the S&P/ASX200 was paid a total of $3.8 million in 2014, 47 times the amount paid to the average Australian receiving a full time wage2.

> Total pay3 among the CEOs in our sample in the S&P/ASX200 ranged between $360,000 and $13.1 million. The lowest pay was in the consumer discretionary sector and was paid by a recent admission to the S&P/ASX 200. The company with the highest pay was in the financial services sector where pay is consistently high across the company and is closely tied to performance.

> The sector with the highest average total CEO pay was the energy sector, with CEOs in that sector paid three times the amount paid to CEOs in the lowest paid sector (IT), on average.

> In the energy and industrials sectors, CEOs are paid three times more, on average, than the next highest paid executive in the company.

> The smallest premium is paid to CEOs in the financial sectors suggesting that executives in that sector may be highly paid across the board.

> While pay of team members (referred to as Key Management Personnel, or KMP4, in the statutory accounts) across the S&P/ASX 200 seems markedly lower than CEO pay, KMP pay is 18 times the average Australian full-time wage.

> CEO fixed pay across sectors is much more consistent than total pay, which suggests that the size and value of equity incentives causes the large discrepancy across sectors. Most average fixed pay amounts range between $1 million and $2 million a year.

> There is a correlation between high levels of CEO pay and the size of the company.

Executive pay is inevitably one of the most controversial aspects of proxy voting season.

While media attention is often paid to the absolute size of executive pay packets, as investors we take a measured approach to remuneration structures and consider the size of pay in the context of each company, its industry, and the economy as a whole.

Context is important because at its most basic level, executive remuneration is an investment of shareholder funds in the management team. As a shareholder, AMP Capital believes that remuneration should therefore be fair, reasonable, and aligned with shareholder interests.

For some time, we have considered the way in which boards are setting and reviewing executive pay. It appears that a significant factor when CEO pay is set and reviewed is the amount that peers are paying rather than the value that a particular individual provides.

We have suspected that this is the case because when we identify high levels of executive pay, company directors often explain that pay has been set at that level to ensure consistency with sector peers. We are often told that independent benchmarking studies have been conducted domestically and globally to ensure that pay packages are fair when compared with what CEOs would receive elsewhere.

Company directors often add that executive searches are now global, and executives need to be paid at least as much as their peers to entice them to take the position or remain in the position.

We have some sympathy with this position and acknowledge that in some circumstances it may be necessary to pay what others are paying to ensure that the best executive for the position is hired or retained. However, we believe that executive pay should be structured from a broader perspective - the value that a CEO provides - and that benchmarks and sector comparisons should be one part of the calculation rather than the entire equation.

Ultimately, executive remuneration should be fair payment for the role for which the executive has been hired rather than a salary package based on what every other CEO is being paid.

As the question of ‘CEO value’ is often lost in discussions that link CEO pay with sector peers and/or market capitalisation, AMP Capital began to consider this issue by collecting pay data on CEOs and KMP for the 2013/14 and 2014/15 financial years.

KRISTEN LE MESURIER Senior ESG Analyst, Investment ResearchAMP Capital

AMP Capital: Corporate Governance Report | February 2016 5

Our aim was to assess the size of executive pay across the S&P/ASX 200 and detect trends, including how much CEOs are being paid compared with the second most highly paid executive, and how much CEOs are being paid compared with the average executive included in the KMP.

The hope is that this study adds to the industry discussion on appropriate levels of executive pay by providing a slightly different perspective on the factors boards may consider when setting and reviewing CEO pay. Our intention is not to comment on whether executive pay levels are too high or too low. We are reflecting on whether current executive pay levels reflect a fair assessment of value.

HOW MUCH VALUE DO CEOs PROVIDE?

Most shareholders, including AMP Capital, would agree that CEOs deserve to be paid a premium for running a listed company in Australia.

The CEO is responsible for developing and implementing high-level strategies, making significant corporate decisions, managing short and long-term performance, overseeing the overall operations and resources of the company, optimising returns and capital levels, reporting to the board and being accountable to shareholders. In addition, CEOs are the public face of the company and set its tone and culture.

Every facet of the CEO’s role is crucial to investors. While it is important the CEO delivers on each responsibility, the question becomes: how much value do these skills generate for shareholders, and other stakeholders, and how much should the CEO be paid for them?

AMP Capital recognises the difficulty in setting pay when a new CEO begins, particularly in the context of a global search, historically highly-paid sectors, and the need to compensate executives for the loss of incentives that would otherwise have vested if they had stayed at their previous employer. However, we would encourage companies not to simply allow history to determine the future; we would rather see boards set executive pay with reference to the value that those executives provide. Some companies have taken this approach in the last year as new CEOs have commenced and reset executive pay at a lower level.

CEO PAY DIFFERS ACROSS SECTORS

Our research showed that while the average key executive at major Australian companies is paid $1.4 million a year, more than half of all CEOs receive double the amount that the next highest paid executive at their company receives (see above). This implies that, on average, CEOs are considered to be worth twice as much as the second most highly paid executive, who is often the CFO or manager of a significant business division.

In some sectors, CEOs are paid three times more than the next highest paid executive. This is the case in the energy sector, for example. This is an interesting result that warrants investigation. Why is the premium so much higher, on average, for energy CEOs relative to other sectors, and is this a fair representation of value?

Having considered the data in detail, we cannot see a reason for this premium particularly when the second highest paid executive in the energy sector is paid $2 million which is significantly more than the sample average of $1.44 million.

The chart above also shows the varying sizes of average CEO pay across sectors. Total pay, which consists of fixed pay plus an accounting measure of short-term and long-term pay, differs widely across sectors. The energy, financials, consumer staples and materials sectors each pay their CEOs, on average, above the $4 million sample average per year.

CEOs in the energy sector, for example, received average total pay of $6 million in 2014, with five of the six CEOs being paid more than $5.7 million in 2014. In the finance sector, CEOs received average total pay of $4.5 million in 2014, but the use of an average conceals the vast range of pay within that sector – total pay ranged between $467,000 and $13.1 million in 2014 – as well as the high levels of pay for some CEOs. Eight of the 28 financial companies included in this study paid their CEOs more than $6 million and four companies paid their CEOs more than $10 million in 2014.

Average total pay for CEOs in each sector relative to the next highest paid

$-

$1

$2

$3

$4

$5

$6

$7

Millions

Avg. CEO total pay Avg. next highest paid exec Avg total KMP pay excl CEO Avg. CEO pay - S&P/ASX200

Consumer discretionary

Consumer staples

Energy Financials Healthcare Industrials IT Materials Tele-communication

services

Utilities

Source: AMP Capital

...executive remuneration should be fair payment for the role for which

the executive has been hired, rather than a salary package based on what

every other CEO is being paid.

6 AMP Capital: Corporate Governance Report | February 2016

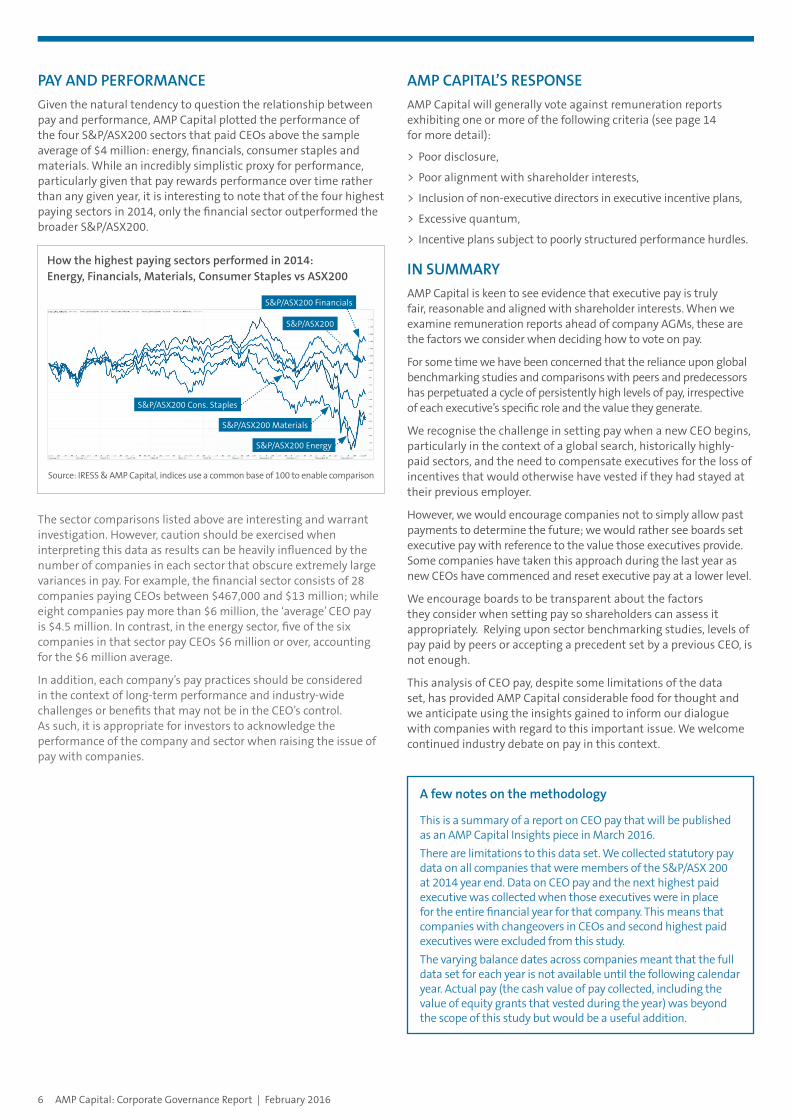

PAY AND PERFORMANCE

Given the natural tendency to question the relationship between pay and performance, AMP Capital plotted the performance of the four S&P/ASX200 sectors that paid CEOs above the sample average of $4 million: energy, financials, consumer staples and materials. While an incredibly simplistic proxy for performance, particularly given that pay rewards performance over time rather than any given year, it is interesting to note that of the four highest paying sectors in 2014, only the financial sector outperformed the broader S&P/ASX200.

How the highest paying sectors performed in 2014: Energy, Financials, Materials, Consumer Staples vs ASX200

Source: IRESS & AMP Capital, indices use a common base of 100 to enable comparison

AMP CAPITAL’S RESPONSE

AMP Capital will generally vote against remuneration reports exhibiting one or more of the following criteria (see page 14 for more detail):

> Poor disclosure,

> Poor alignment with shareholder interests,

> Inclusion of non-executive directors in executive incentive plans,

> Excessive quantum,

> Incentive plans subject to poorly structured performance hurdles.

IN SUMMARY

AMP Capital is keen to see evidence that executive pay is truly fair, reasonable and aligned with shareholder interests. When we examine remuneration reports ahead of company AGMs, these are the factors we consider when deciding how to vote on pay.

For some time we have been concerned that the reliance upon global benchmarking studies and comparisons with peers and predecessors has perpetuated a cycle of persistently high levels of pay, irrespective of each executive’s specific role and the value they generate.

We recognise the challenge in setting pay when a new CEO begins, particularly in the context of a global search, historically highly-paid sectors, and the need to compensate executives for the loss of incentives that would otherwise have vested if they had stayed at their previous employer.

However, we would encourage companies not to simply allow past payments to determine the future; we would rather see boards set executive pay with reference to the value those executives provide. Some companies have taken this approach during the last year as new CEOs have commenced and reset executive pay at a lower level.

We encourage boards to be transparent about the factors they consider when setting pay so shareholders can assess it appropriately. Relying upon sector benchmarking studies, levels of pay paid by peers or accepting a precedent set by a previous CEO, is not enough.

This analysis of CEO pay, despite some limitations of the data set, has provided AMP Capital considerable food for thought and we anticipate using the insights gained to inform our dialogue with companies with regard to this important issue. We welcome continued industry debate on pay in this context.

The sector comparisons listed above are interesting and warrant investigation. However, caution should be exercised when interpreting this data as results can be heavily influenced by the number of companies in each sector that obscure extremely large variances in pay. For example, the financial sector consists of 28 companies paying CEOs between $467,000 and $13 million; while eight companies pay more than $6 million, the ‘average’ CEO pay is $4.5 million. In contrast, in the energy sector, five of the six companies in that sector pay CEOs $6 million or over, accounting for the $6 million average.

In addition, each company’s pay practices should be considered in the context of long-term performance and industry-wide challenges or benefits that may not be in the CEO’s control. As such, it is appropriate for investors to acknowledge the performance of the company and sector when raising the issue of pay with companies.

S&P/ASX200 Financials

S&P/ASX200

S&P/ASX200 Cons. Staples

S&P/ASX200 Materials

S&P/ASX200 Energy

A few notes on the methodology

This is a summary of a report on CEO pay that will be published as an AMP Capital Insights piece in March 2016.

There are limitations to this data set. We collected statutory pay data on all companies that were members of the S&P/ASX 200 at 2014 year end. Data on CEO pay and the next highest paid executive was collected when those executives were in place for the entire financial year for that company. This means that companies with changeovers in CEOs and second highest paid executives were excluded from this study.

The varying balance dates across companies meant that the full data set for each year is not available until the following calendar year. Actual pay (the cash value of pay collected, including the value of equity grants that vested during the year) was beyond the scope of this study but would be a useful addition.

AMP Capital: Corporate Governance Report | February 2016 7

Director quality and board effectiveness continues to be the most important governance issue for shareholders.

AMP Capital has long been interested in board composition. When assessing boards, we take into account the combination of director skills, the time each director can commit to the role, and their ability to act independently and in the best interests of the company and shareholders. As part of this, we also consider the issue of gender diversity.

Back in the 1990s, when AMP Capital began to more closely evaluate governance issues, we noted the homogeneity of directors on Australian boards and accepted all-male boards as the norm. Today, our thinking has progressed considerably. After accepting poor diversity as ‘normal’, we progressed to see improving gender diversity as the ‘right’ thing to do. Now we firmly believe it is the ‘smart’ and ‘necessary’ thing to do.

In 2010, AMP Capital found that 60 per cent of the Australian companies we invested in on behalf of clients had no women directors and immediately began to raise the issue in our regular engagement with company chairmen. Since that time, we have continued to monitor and report on the gender diversity of boards.

It has been pleasing to witness the steady increase in the number of women now seated on the boards of Australia’s largest companies. Where, in 2010, 60 per cent of companies AMP Capital held had no women directors, in 2015 this number had fallen considerably to 21 per cent.

Fortuitously, our focus on this issue coincided with the introduction of a range of other initiatives directed at improving gender diversity in Australian workplaces. Some notable examples include:

> In July 2010, the ASX Corporate Governance Council introduced Diversity Recommendations calling each listed entity to report on an “if not why not’ basis, the nature of their diversity policy, the measurable objectives and the actual proportion of women at different levels of the organisation.

Despite seeing improvements in the level of reporting each year, the data clearly shows companies continue to struggle with setting measurable objectives and increasing the number of women in their organisations.

> The Australian Institute of Company Directors’ Chair’s Mentoring Program was established in 2010 to bring together senior listed-company chairs and senior directors to mentor emerging female directors. Mentees benefit from the connections, skills and knowledge shared by their chairman mentors, while at the same time chairmen build connections with a high-quality pool of potential female directors.

> Australia’s Male Champions of Change (MCC) initiative brings together men of power and influence to form high-profile coalitions to achieve change on gender equality issues in organisations and communities.

Gender diversity: Will the gender diversity of boards reach 30 per cent?

KARIN HALLIDAY Senior Manager, Corporate GovernanceAMP Capital

Since forming the first groups in 2010, the MCC’s stated objective has been to identify and implement progressive, high-impact actions that disrupt the status quo and create meaningful and lasting change.

Acknowledging that today the levers of power in nations and in organisations largely rest in the hands of men, it is important men be engaged to drive and accelerate change.

> In 2012, the Federal Government established the Workplace Gender Equality Agency to promote and improve gender equality in Australian workplaces. Today any Australian employer, with 100 or more employees, is required to submit to the WGEA a report covering standardised reporting of the following six gender-equality indicators:

1. Gender composition of the workforce 2. Gender composition of governing bodies 3. Pay-parity between men and women 4. Availability and utilisation of flexible working arrangements 5. Consultation with employees on gender equality issues 6. Sex-based harassment and discrimination

As a result of this reporting, Australians now have access to an unprecedented picture of gender equality in our workplaces5.

> In May 2015, the 30% Club Australia was launched with the primary objective of campaigning for 30 per cent women on ASX 200 boards by 2018. Globally this organisation uses collaborative and concerted business-led efforts to help accelerate progress towards better gender balance at all levels of organisations. Believing that gender balance on boards not only encourages better leadership and governance but contributes to better all-round board performance, the 30% Club aims to develop a diverse pool of talent for all businesses.

*Based on the Australian companies held in portfolios managed by AMP Capital

Fewer companies now have no women directors*.

2010 2011 2012 2013 2014 2015

70%

60%

50%

40%

30%

20%

10%

0%

Boards with no women Boards with one women Boards with two or more women

8 AMP Capital: Corporate Governance Report | February 2016

LINKING GOVERNANCE QUALITY AND GENDER DIVERSITY

The business case for improving gender diversity at senior levels of organisations is continually being strengthened as a result of a greater understanding and acceptance of its positive impact on company performance.

In addition to the link with performance, AMP Capital has found companies with two or more women directors tend to exhibit better governance, with fewer issues around board composition, the quantum and structure of remuneration, audit integrity and also related-party transactions.

While there is bound to be a degree of causality, past analysis conducted by AMP Capital concluded that companies with two or more women directors tend to be better governed.

The March 2014 edition of this report noted AMP Capital’s observations of a clear relationship between each company’s governance quality and the number of women that sit on its board.

When comparing companies with no women directors against those with two or more, we found that on average companies with poor gender diversity:

> Experienced almost triple the related-party issues.

> Had twice the board composition concerns including concerns relating to a lack of board independence

> Were twice as likely to have an affiliated chairman.

> Had twice the remuneration concerns.

AMP Capital’s observations support the view that companies that promote gender diversity at board level benefit from the different perspectives women bring to the table. When issues are approached from different points of view, it is likely discussions will be more robust and decisions more rewarding.

Interestingly, when looking back over earlier voting records, there was also clear evidence that AMP Capital supported fewer resolutions at companies with no women directors, the most striking difference being lower votes in support of remuneration.

Having said that, the relationship with governance quality was less prevalent in 2015 than it had been previously most likely due to the fact far fewer companies now have no women directors.

WHICH COMPANIES HAVE NO WOMEN DIRECTORS?

Since 2010, AMP Capital has made a note of which companies have no women directors. As it is disappointing to see many companies appear on this list year after year, we have shared the names of companies (below) where there has not been a woman director in the past two years.

While the companies listed below operate in a range of sectors of the economy, the metals and mining sector features most prominently.

The following companies had no women directors at the time of their 2014 and 2015 annual general meetings:

Altium Ltd

Aveo Group

AP Eagers Ltd

Alliance Aviation Services Ltd

Austal Ltd

Evolution Mining Ltd

Freedom Foods Group Ltd

GWA Group Ltd

Karoon Gas Australia Ltd

Monadelphous Group Ltd

Mesoblast Ltd

Mayne Pharma Group Ltd

National Storage REIT

Northern Star Resources Ltd

Qube Holdings Ltd

Regis Resources Ltd

Select Harvests Ltd

Syrah Resources Ltd

Vocus Communications Ltd

Webjet Ltd

Western Areas Ltd

Analysis of the diversity policies of the companies listed above shows:

> Approximately half have no diversity policy, no diversity targets and/or make no mention of the gender diversity of the board.

> Approximately one-quarter have mentioned that gender diversity is important but have weak policies and/or no disclosed strategy for improving the gender diversity at board level.

> Approximately one-quarter have appropriate policies, acknowledge the importance of gender diversity and mention plans to:

− remove barriers to improved diversity (for example, through the selection process), or

− provide training and succession planning aimed at improving gender diversity.

Note: Two companies initially on this list, Technology One Ltd and Village Roadshow Ltd, have since appointed a woman director to their board.

Fewer medium-size companies now have no women directors*

30

25

20

15

10

5

0

ASX 100 ASX 200 ASX 300 All Ords (ex300)

2014 2015

*Based on the Australian companies held in portfolios managed by AMP Capital

In Australia women now fill 20.2% of board seats*

7.7%

10.5%

12.7%

14.1%

17.9%

20.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2010 2011 2012 2013 2014 2015

% Women

*Based on the Australian companies held in portfolios managed by AMP Capital

AMP Capital: Corporate Governance Report | February 2016 9

NEW DIRECTORS

A review of the profiles of women who have recently been appointed to their first ASX board seat shows these directors bring a broad range of skills, experience and expertise to the table.

For many years, company chairmen argued that the failure to appoint women directors was as a direct result of an insufficient number of women possessing the relevant executive or technical expertise. While metals and mining companies continue to feature prominently in the list of companies with no women directors, it is pleasing to see many of the new women joining boards in 2015 have come from mining, medical and scientific backgrounds.

Where in the past women directors often possessed specific skills in human relations, the most recent appointees have had diverse backgrounds including:

> Senior executive careers with ASX 100 companies including resources companies.

> Leadership of industry bodies.

> Experience with not-for-profit organisations.

> Experience working for international companies.

> Banking, finance and investment advisory.

> Politics and law.

> Science, technology, engineering and mathematics (including IT and telecommunications).

> Property management

WHERE TO FROM HERE?

AMP Capital considers it paramount for investors to consider and understand the composition of a company’s board and senior management team, and frequently discusses the issue in our engagement with companies.

As society changes, a company’s success is more and more likely to depend on their ability to attract and maintain the best people, drawing equally from the talents of both men and women.

In order for the companies we invest in to expose themselves to a better pool of director or management candidates, we encourage them to address roadblocks such as unconscious bias and to cast the net more widely when recruiting.

For the pool of talented women to be developed and recognised, there needs to be clear focus on pay parity and the opportunities for women to gain executive experience. More recently, AMP Capital has begun to investigate what role the ability to work flexibly plays in improving the gender diversity of workplaces particularly where the opportunity to work flexibly is equally accessible to both men and women.

Having recently became a member of the 30% Club Investors’ Working Group, AMP Capital will also help coordinate the investment community’s approach to the diversity issue. Initially, companies will be encouraged to respond to voluntary targets. However where the response is inadequate, companies should not be surprised if shareholders begin to use AGM voting to help bring about the required change.

To date, AMP Capital has not resorted voting against the re-election of directors at companies with zero or little gender diversity. This is, however, an action we may consider in the future, particularly where companies show no signs of addressing this issue.

The 30% Club is campaigning for ASX 200 boards to be 30 per cent women by 2018. While good progress has been made, there is some way to go before women make up 30 per cent of every Australian board of directors.

AMP Capital has begun to investigate the role the ability to work flexibly plays in

improving the gender diversity of workplaces, particularly where the opportunity to work flexibly

is equally accessible to both men and women.

...companies that promote gender diversity at board level benefit

from the different perspectives women bring to the table.

*Based on the Australian companies held in portfolios managed by AMP Capital

4+ Boards 3 Boards 2 Boards 1 Board

300

250

200

150

100

50

02012 2013 2014 2015

Most women directors occupy one board seat*

10 AMP Capital: Corporate Governance Report | February 2016

What to make of the Paris Climate Change Agreement

As testimony to the global nature and potential magnitude of the climate change challenge, the opening day of the Paris Climate Change talks attracted 150 presidents and prime ministers, the largest ever single-day gathering of heads of state.

This ambitious December 2015 gathering of stakeholder representatives sought to reach agreement on the best way forward to address the challenge, recognising that current commitments could only be expected to limit global warming to somewhere between 2.7-3.5 degrees Celsius (C).

Perhaps the biggest surprise of the Paris talks was the acceptance of a call from small nations, most vulnerable to climate change, to declare warming should be halted at 1.5C and recognition that this would significantly reduce the risks and impacts of climate change. Going into the conference, those who were perhaps sceptical of international agreements might have expected, or hoped, for a watering down of the climate change goal of limiting to temperature rise to 2C. The fact that nations agreed to try to achieve a smaller increase in rising temperatures (1.5C) puts significant moral and ultimately political pressure on countries to ratchet up their climate change initiatives.

By the end of the event more than 190 countries had agreed that greenhouse gas emissions should peak as soon as possible, reaffirmed the goal of limiting global temperature increase well below 2C, and had committed to regularly report on their emissions and where possible provide improved targets.

Other aspects of the agreement were generally as expected including:

> Establish binding commitments by all parties to make “nationally determined contributions” (NDCs), (greenhouse gas emission reduction targets) and to pursue domestic measures aimed at achieving them.

> Commit all countries to report regularly on their greenhouse gas emissions and “progress made in implementing and achieving” their NDCs, and to undergo international review.

> Commit all countries to submit new emission reduction targets (NDCs) every five years, with the clear expectation that the new targets will “represent a progression” beyond previous ones.

For the investors, the Agreement provides a clear signal that the transition to a low-carbon economy is underway and that there is an intention to speed up the process. The exact process for achieving a low-carbon economy will depend on the policy decisions of each country and so while the direction on emissions has been clarified there remains regulatory and policy uncertainty. However, a couple of aspects of the Agreement will help facilitate capital flows, including:

> Require parties engaging in international emissions trading to avoid “double counting”. While avoiding any direct reference to the use of market-based approaches - a concession to a handful of countries that oppose them - the agreement recognises that parties may use “internationally transferred mitigation outcomes” to achieve emission reductions.

> Developed countries are still urged to provide US$100 billion finance annually by 2020 for the mitigation and adaption in developing countries.

WHAT WAS DISCUSSED?

The key areas for discussion at the Paris conference included:

> Mitigation – Further emission reduction targets and allocation of emission budget.

> Adaptation – Steps to prepare for the expected impacts of climate change, even under a 2C scenario.

> Financing – Who is going to pay for mitigation and adaptation, especially for any loss or damage?

> Capacity building – Development and transfer of technology and policy capacity.

> Compliance and implementation – Next steps for countries making further emission reduction targets.

These are discussed in more detail below.

1. Mitigation

The Agreement recognised the common but differentiated responsibility of developed and developing companies to reduce emissions. Inherent in this is that developing country emissions may rise before decreasing, with the “aim to reach global peaking of greenhouse gas emissions as soon as possible” and a longer term collective goal of achieving “a balance between anthropogenic emissions by sources and removals by sinks of greenhouse gases in the second half of this century”, ie net global emissions are zero in the second half of this century.

In terms of individual country emissions reductions, the Paris Agreement requires countries to:

> Pursue domestic measures aimed at achieving emission reduction targets, i.e. “Nationally Determined Contributions” (NDCs).

> Report regularly on their emissions and “progress made in implementing and achieving” their NDCs, and to undergo international review.

French foreign minister and president-designate of COP21 Laurent Fabius (centre), raises hands with UN secretary general Ban Ki Moon and French president François Hollande. Photograph: Francois Guillot/AFP/Getty Images

IAN WOODS Head of ESG ResearchAMP Capital

...the Agreement provides a clear signal that the transition to a

low-carbon economy is underway.

AMP Capital: Corporate Governance Report | February 2016 11

> Submit new NDCs every five years, with the clear expectation that they will “represent a progression” beyond previous ones.

The last point is important as the Agreement clearly establishes that current emission reduction targets will need to be increased to meet the climate change goal. This will put further pressure on governments to reduce fossil fuel subsidies and have policies which reduce fossil fuel use. Clearly this will have implications for investments in the energy and utility sectors.

The outstanding issue going forward is how the global emission budget is to be allocated between countries. Our view is that a ‘contraction and convergence’6 allocation based on emission per capita will ultimately form the basis of any allocation. Such an allocation would mean that Australia will need to reduce its greenhouse gas emissions by more than 90 percent by 2050, which requires significant structural changes to the Australian economy and challenging some of our incumbent industries.

2. Adaptation

There was also a clear linkage between reducing emissions and the costs of preparing for climate impacts, with the recognition that “greater levels of mitigation can reduce the need for additional adaptation efforts, and that greater adaptation needs can involve greater adaptation costs”. We think this is important because adaptation (rather than reducing emissions) is more important to many developing countries especially because they do not see themselves as responsible for the problem in the first place i.e. historical emissions. For investors it highlights that long-life assets, such as property and infrastructure, will need to understand and prepare for the impact of a changing climate.

3. Financing

The question of who is going to pay for the investment required to reduce emissions was always going to be a key sticking point and in particular how much developed countries were going to support developing countries and what mechanism can be used to facilitate private capital.

One of the key issues is fossil fuel subsidies, with governments spending more than US$500 billion per year of public resources a year to keep domestic prices for oil, gas and coal artificially low. The removal of fossil fuel subsidies was not part of the formal agreement but more than 40 countries, including the US, New Zealand and many EU countries, have argued for the removal of subsidies as removing fossil fuel subsidies would reduce greenhouse gas emission by 10 per cent by 2050. The removal of subsidies would free up resources to invest in social and physical capital such as education, healthcare and infrastructure, while levelling the playing field for renewable energy. This represents a significant move in government spending, especially in developing countries where subsidies are more common, which may provide some opportunities for investors in emerging markets.

4. Capacity building

The Agreement doesn’t explicitly call for carbon markets but various parties and investors did call for market-based mechanisms. These markets will play an important part in technology transfer into developing countries and stimulate low carbon investments in developed countries. The Agreement does call for a new mechanism, similar to the Clean Development Mechanism (CDM) under the Kyoto Protocol, enabling emission reductions in one country to be counted toward another country’s emission reductions. However, the role of “CDM type” credits is in doubt as any mechanism needs to deliver “an overall mitigation” in global emissions, which means it will differ from the offsetting concept established under Kyoto’s Clean Development Mechanism. Given now all countries have a role in reducing emissions, the likelihood that countries will allow CDM projects is increasingly doubtful.

The development of deeper and broader carbon markets will certainly facilitate capital flows in low emission technologies and potentially develop a new substantial financial market and a new asset class for institutional investors.

5. Compliance and implementation

From an international law perspective, the Paris Agreement comes into force when 55 parties contributing 55 per cent of global greenhouse gas emissions ratify the Agreement. This is a low hurdle for international agreements.

As part of the Agreement, a working group was established to give guidance on features of climate pledges and economy-wide greenhouse gas accounting. This is important because consistency on greenhouse gas accounting offers policymakers a comparable baseline between countries to implement climate policy in the future. Agreement on greenhouse gas accounting will be important for the establishment of and confidence in a transparent carbon market.

The first global stocktake of how well the Agreement is being implemented will take place in 2023 and every five years thereafter. Countries need to submit new NDCs every five years, starting in 2018, with the clear expectation that they will “represent a progression” beyond previous ones.

Parties engaging in international emissions trading need to avoid “double counting”, i.e. emissions, or emissions reductions, that occur in one country which are “sold” to another country either change the originating countries’ emission reduction target or cannot be used in reaching their own reduction target.

SO WHAT?

To achieve a temperature increase of less than 2C means that countries will have to set far more ambitious emission reduction goals, particularly those countries that had committed to 2030 reduction targets going into the Paris conference. This covers most countries including Australia, the European Union, Canada, Japan and South Korea.

An increase in Australia’s emission reduction target is likely to require:

> A further increase in the amount of renewable energy and the renewable energy target.

> An increased focus on energy efficiency, especially in buildings.

It also casts further doubt on whether the current form of “Direct Action” and “Safeguard Mechanism” is the best way to achieve emission reductions.

While AMP Capital has as a positive view of investment opportunities in infrastructure, it is acknowledged some specific sectors may be negatively impacted. Particular investment implications of the Agreement includes:

> A more negative outlook for thermal coal miners and oil sands producers and associated rail, port and pipeline infrastructure.

> Increasing pressure to retire coal-fired generation globally, and potentially earlier retirement for some than currently planned.

> Further subdued increases and potential for decline in electricity demand impacting electricity infrastructure.

> Continued favourable policies towards investment in renewables and other low-emission technology.

> Underlying support for those involved in light materials and or energy storage such as aluminium businesses and lithium miners.

With the Paris Agreement achieved, the focus for investors is on domestic policy choices and implementation to achieve stated and increasingly stringent emission reduction targets.

12 AMP Capital: Corporate Governance Report | February 2016

AMP Capital continues to be actively committed to encouraging good corporate governance at the companies held in portfolios we manage.

While our lodgement of proxy votes has an impact on governance, we believe communication, either via letters or our meetings with company directors, to be a far more constructive and effective form of shareholder activism. Since the introduction of the two-strikes rule on executive pay, there has been a significant increase in the number of companies seeking to engage with shareholders.

In a year, it is not unusual for AMP Capital to have 50 specific meetings with companies on governance issues and to have written to a further 50 companies outlining the rationale for the decision not to support a company-proposed resolution. We continue to be pleased with companies’ positive response to these letters, with many companies addressing our specific concerns and improving governance practices in subsequent years.

Some visible improvements have included: greater disclosure and transparency, the appointment of independent directors; improved terms for incentive plans, and the abolition of termination benefits for non-executive directors.

Many company chairmen have accepted our invitation to discuss governance matters further, meeting with us personally to address issues of concern. AMP Capital values these interactions with companies, not only for the ability to ensure remuneration is fair and aligned with our interests but also because the interaction provides the opportunity to raise broader ESG issues.

A good example of this is where remuneration discussions at some companies turned into constructive dialogue on topics such as succession planning, supply chain risks, diversity, safety and various aspects of risk management.

ESG: BROADER STAKEHOLDER ENGAGEMENT

In addition to governance-focussed meetings, the AMP Capital ESG research team had more than 80 meetings with companies. Most of these meetings were undertaken with our mainstream investment analysts, reinforcing the link between investment analysis decisions and ESG issues. The response from companies was mixed but we have noticed a general acknowledgement that companies need to be prepared to discuss these issues with investors. The continuity of the ESG focus by a large investor and our linkage with ‘mainstream’ investment meetings has also helped us reinforce the increasing importance that investors are placing on ESG issues.

More specifically, current key thematic engagements have focussed on corporate governance (including remuneration and the composition and gender diversity of boards), supply chain management / labour rights, climate change, unconventional gas and improved ESG disclosure.

AMP Capital has again been involved in various ESG forums and media opportunities to share insights with regard to our views on ESG issues. The AMP Capital ESG Research team participated in around 100 non-company meetings where we either actively engaged other investors or other stakeholders or took the opportunity to develop a better understanding of an industry or key ESG issue.

These activities reflect our broader objective of improving the ESG performance of all companies and the investment industry generally, not just the ones we may have chosen to invest in on behalf of our clients.

Shareholder Engagement

AMP Capital: Corporate Governance Report | February 2016 13

Proxy voting – Australian equities

RECENT VOTING HIGHLIGHTS

As the financial year-end for the majority of Australian companies is June 30, most annual general meetings are held in October and November. The second half of the calendar year is traditionally the busiest time for proxy voting in Australia.

While most resolutions were supported, AMP Capital often lodged votes against resolutions when concerned with overly generous or poorly aligned pay structures and poor board composition

AMP Capital also specifically took no action on resolutions where we are excluded from voting. This situation arises when, for example, we have participated in share issues on behalf of our clients and are therefore deemed to have a conflict of interest and are excluded from voting to ratify that transaction.

Source: AMP Capital voting statistics

0

5

10

15

20

25

10% not supported, reasons include- poor or non-existent performance hurdles- too short term- includes both non-executive director and company executives in same plan- too generous- poor disclosure of terms- non-recourse financing- automatic vesting on change of control

16% not supported, reasons include:- concerns regarding terms of non-salary compensation- poor disclosure- unsatisfactory director retirement and executive termination benefits

7% not supported, reasons include:- new fee levels were too high- board too large or ‘poorly’ composed- NEDs continue to accrue retirement benefits.

Incentive related compensation

Non-executive directorremuneration

Remuneration Reports

Binding votes Non binding votes

30

Perc

ent

of r

esol

uti

ons

not

su

pp

orte

d in

th

ese

cata

gori

es

4% not supported, reasons include:- too many affiliates- no independent - poor committee composition- need for more relevant skills- board too large

Director Election

Resolutions not supported by AMP Capital in 2015 (includes abstentions)

279 MEETINGS 1453 RESOLUTIONS

For 90%

Against 4%

Abstain 5%

Excluded 1%

Board composition

Board composition continues to be one of the most important corporate governance issues for shareholders. Despite its significance, we acknowledge it is often difficult for shareholders to determine whether they have the right boards governing their companies, with an effective composition of skills, knowledge and independence. The short biographies available in annual reports provide little detail and without being present in the boardroom, shareholders cannot observe the dynamics of the board nor its overall effectiveness.

In any proxy season, most company meetings are annual general meetings at which shareholders vote on the election or re-election of directors. Votes against directors generally reflect concerns such as poor board attendance, an insufficient number of independent directors to represent public shareholders and broader issues related to poor governance.

Once again, AMP Capital supported the majority of directors seeking re-election in 2015. Those not supported were predominantly self-nominated, non-board-endorsed candidates who we considered not ideal candidates.

Companies where AMP Capital voted against at least one company-endorsed director during this period include:

Harvey Norman Holdings Ltd

Healthscope Ltd

News Corporation

Nine Entertainment Ltd

Origin Energy Ltd

In addition, AMP Capital specifically abstained from re-electing directors at several other companies. In these cases there may have been a better representation of independent directors, albeit still a minority, and/or this was the first time the issue of board composition had been raised with the particular company. We will generally endeavour to communicate our specific concerns to the company involved.

AUSTRALIAN EQUITIES (2015)

14 AMP Capital: Corporate Governance Report | February 2016

Remuneration reports

Since the introduction of non-binding votes on remuneration reports in 2005, Australian investors now have a mechanism by which to review and comment on the approach to remuneration used by the companies in which they invest. The impact of a shareholder’s ‘against’ vote on remuneration is now greater since the introduction of the two-strikes rule.

When reviewing the appropriateness of remuneration reports, AMP Capital generally considers a wide range of factors.

Remuneration reports should be concise and facilitate a clear understanding of the company’s remuneration policy, providing evidence that the policy is both fair and reasonable and is aligned with shareholder interests.

In particular, we look for criteria such as the clarity of disclosure, satisfactory short and long-term incentive and termination arrangements and also appropriate non-executive director remuneration.

The remuneration reports AMP Capital voted against over this period were:

Abacus Property Group

Automotive Holdings Group Ltd

Myer Holdings Ltd

News Corporations

Premier Investments Ltd

Ten Network Holdings Ltd

UGL Ltd

Village Roadshow Ltd

Webjet Ltd

In general, AMP Capital will vote against remuneration reports that exhibit one or more of the following criteria: poor disclosure, poor alignment with shareholder interests, inclusion of non-executive directors in executive incentive plans, excessive quantum and poorly structured performance hurdles (e.g. absolute rather than relative, not sufficiently challenging, too short term, purely accounting-based, allowing too many opportunities for re-testing etc.).

During this period the specific reasons for voting against remuneration reports included:

> Overly generous retention benefits, coupled with generous new grants.

> Low performance hurdles, e.g. vesting well below earnings guidance.

> Retrospectively changing performance hurdles and/or start-dates, or using board discretion to vest incentives when hurdles not met.

> Overly-generous quantum.

> Poor alignment.

> Structural concerns, especially where they potentially incentivise behaviour that is contrary to the best interests of shareholders (such as making acquisitions or beating budget- with no reference to the longer-term benefit to shareholders of meeting these targets).

> Boards unlimited discretion to allow incentives to vest upon a CEO’s termination.

> Overly complex incentive structures that would potentially fail to motivate or retain key management personnel.

> Poor disclosure.

In the past, AMP Capital has expressed concern with regard to excessive termination payments (both actual and potential) made to some departing senior executives particularly where actual payments bear little resemblance to previously agreed limits.

What is the two-strikes rule?

The two-strikes rule is legislation giving shareholders the ability to vote on whether to ‘spill’ an entire board of directors (that is, remove the board of directors) over remuneration concerns. Two strikes occurs when 25 percent or more of shareholders vote against the adoption of the remuneration report in two consecutive years.

Share and option incentive plans

Once again, AMP Capital has lodged votes against a range of incentive-related resolutions where the terms were considered to be overly generous and/or poorly aligned with shareholder interests. Over the period, AMP Capital voted against at least one incentive-related resolution at meetings of the following companies:

Abacus Property Group

Cromwell Property Group

Flexigroup Ltd

Liquefied Natural Gas Ltd

Prime Media Group

Qube Holdings Ltd

Recall Holdings Ltd

Saracen Mineral Holdings Ltd

Seek Ltd

Sonic Healthcare Ltd

Ten Network Holdings Ltd

As investors, we seek to invest in companies that will provide the best relative share market performance over the long-term and as such we prefer a significant portion of the CEO’s remuneration to be aligned with that goal.

The underlying reasons for not supporting long-term incentive related resolutions include:

> Poor disclosure of the terms of the incentive plans

> Plans are shorter than the desired three-year minimum

> Plans had no performance hurdles or hurdles that lacked sufficient alignment with the interests of shareholders

> Proposed plan amendments would increase the value to employees, without any corresponding benefit to shareholders

> Participation of NEDs in executive schemes

> Plans showed no improvement, despite the company having received comments/input and the matter being not supported previously.

AMP Capital continues to consider how incentive grants should respond upon a change of control at the company. We became interested in this feature several years ago after seeing instances where company executives and directors engaged in behaviour that could potentially destroy shareholder value while themselves reaping significant personal gains.

AMP Capital: Corporate Governance Report | February 2016 15

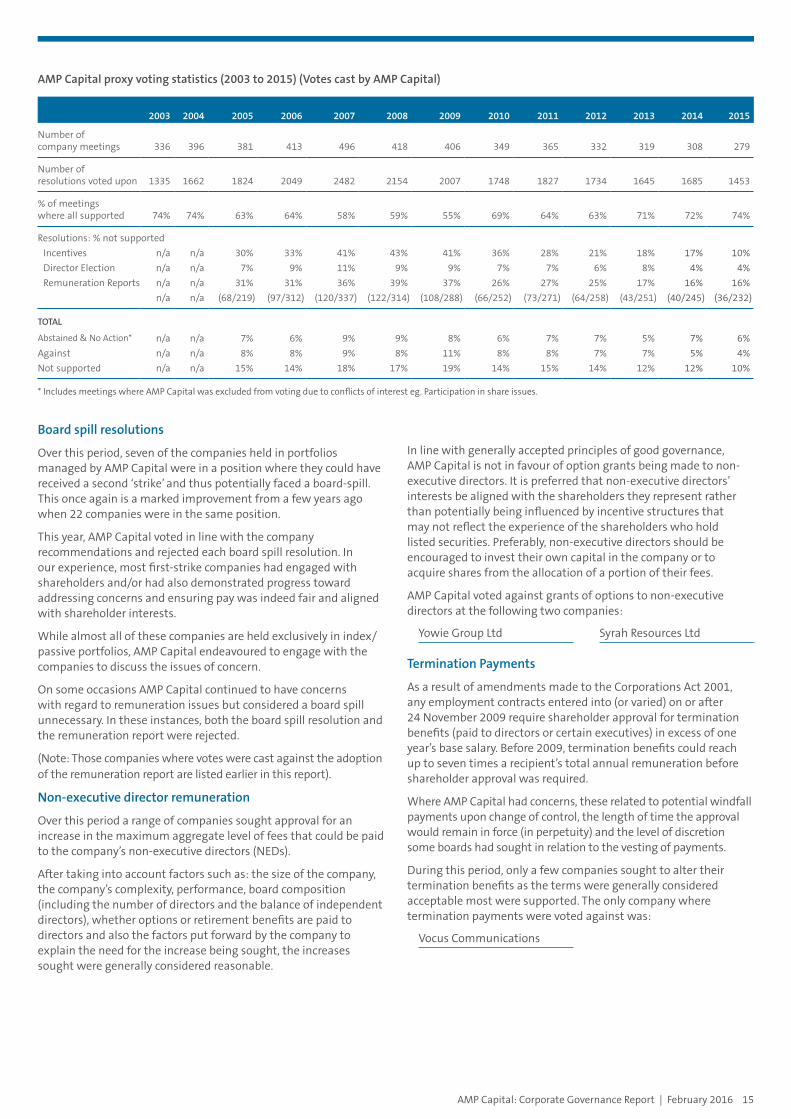

Board spill resolutions

Over this period, seven of the companies held in portfolios managed by AMP Capital were in a position where they could have received a second ‘strike’ and thus potentially faced a board-spill. This once again is a marked improvement from a few years ago when 22 companies were in the same position.

This year, AMP Capital voted in line with the company recommendations and rejected each board spill resolution. In our experience, most first-strike companies had engaged with shareholders and/or had also demonstrated progress toward addressing concerns and ensuring pay was indeed fair and aligned with shareholder interests.

While almost all of these companies are held exclusively in index/ passive portfolios, AMP Capital endeavoured to engage with the companies to discuss the issues of concern.

On some occasions AMP Capital continued to have concerns with regard to remuneration issues but considered a board spill unnecessary. In these instances, both the board spill resolution and the remuneration report were rejected.

(Note: Those companies where votes were cast against the adoption of the remuneration report are listed earlier in this report).

Non-executive director remuneration

Over this period a range of companies sought approval for an increase in the maximum aggregate level of fees that could be paid to the company’s non-executive directors (NEDs).

After taking into account factors such as: the size of the company, the company’s complexity, performance, board composition (including the number of directors and the balance of independent directors), whether options or retirement benefits are paid to directors and also the factors put forward by the company to explain the need for the increase being sought, the increases sought were generally considered reasonable.

In line with generally accepted principles of good governance, AMP Capital is not in favour of option grants being made to non-executive directors. It is preferred that non-executive directors’ interests be aligned with the shareholders they represent rather than potentially being influenced by incentive structures that may not reflect the experience of the shareholders who hold listed securities. Preferably, non-executive directors should be encouraged to invest their own capital in the company or to acquire shares from the allocation of a portion of their fees.

AMP Capital voted against grants of options to non-executive directors at the following two companies:

Yowie Group Ltd Syrah Resources Ltd

Termination Payments

As a result of amendments made to the Corporations Act 2001, any employment contracts entered into (or varied) on or after 24 November 2009 require shareholder approval for termination benefits (paid to directors or certain executives) in excess of one year’s base salary. Before 2009, termination benefits could reach up to seven times a recipient’s total annual remuneration before shareholder approval was required.

Where AMP Capital had concerns, these related to potential windfall payments upon change of control, the length of time the approval would remain in force (in perpetuity) and the level of discretion some boards had sought in relation to the vesting of payments.

During this period, only a few companies sought to alter their termination benefits as the terms were generally considered acceptable most were supported. The only company where termination payments were voted against was:

Vocus Communications

AMP Capital proxy voting statistics (2003 to 2015) (Votes cast by AMP Capital)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Number of company meetings 336 396 381 413 496 418 406 349 365 332 319 308 279

Number of resolutions voted upon 1335 1662 1824 2049 2482 2154 2007 1748 1827 1734 1645 1685 1453

% of meetings where all supported 74% 74% 63% 64% 58% 59% 55% 69% 64% 63% 71% 72% 74%

Resolutions: % not supported

Incentives n/a n/a 30% 33% 41% 43% 41% 36% 28% 21% 18% 17% 10%

Director Election n/a n/a 7% 9% 11% 9% 9% 7% 7% 6% 8% 4% 4%

Remuneration Reports n/a n/a 31% 31% 36% 39% 37% 26% 27% 25% 17% 16% 16%

n/a n/a (68/219) (97/312) (120/337) (122/314) (108/288) (66/252) (73/271) (64/258) (43/251) (40/245) (36/232)

TOTAL

Abstained & No Action* n/a n/a 7% 6% 9% 9% 8% 6% 7% 7% 5% 7% 6%

Against n/a n/a 8% 8% 9% 8% 11% 8% 8% 7% 7% 5% 4%

Not supported n/a n/a 15% 14% 18% 17% 19% 14% 15% 14% 12% 12% 10%

* Includes meetings where AMP Capital was excluded from voting due to conflicts of interest eg. Participation in share issues.

16 AMP Capital: Corporate Governance Report | February 2016

For the last 20 years, AMP Capital has focussed the attention of its corporate governance and proxy voting activity on the Australian companies held in portfolios we manage. In 2006, the process for voting shares held in our Asian funds was formalised then after the AMP Capital-Brookfield joint venture was dissolved in 2012 responsibility for voting the Global Listed Real Estate (REIT) and Global Infrastructure Funds was also brought in-house.

The Corporate Governance Report now provides a snapshot of the voting of shares held in our internally-managed global portfolios.

Proxy voting – International portfolios

Top 5 countries where resolutions were not supported

GREIT GLIF Asian Equity

United States 30% United States 40% China 38%

France 17% France 13% Hong Kong 14%

Japan 16% Thailand 7% Cayman Is.* 13%

Australia 13% Philippines 6% Bermuda* 8%

Hong Kong 6% Italy 6% Indonesia 7%

Other 17% Other 27% Other 21%

*Note: These companies are predominantly based in China and Hong Kong

AMP Capital’s experience and tradition of taking seriously the responsibility of investing our clients’ money has held us in good stead as we have broadened our international proxy voting remit to align with the expansion of our global investment capabilities.

Key governance issues such as non-executive director remuneration, share and option incentive plans, and board independence impact listed companies throughout the world. Our experience in dealing with these issues locally has helped us to be able to vote on resolutions of internationally listed companies.

There are notable differences in the governance culture throughout different regions in the world. For example:

> Board structure: Whilst most Australian listed companies would avoid a combined Chairman/CEO structure, this structure is far more common in US-listed companies. While AMP Capital is committed to the basic principles of good governance and as far as possible would not support structures that sacrifice the independence or accountability of the board, the context of a company’s situation is also taken into account before votes are cast.

> Disclosure: As offshore companies often have less comprehensive disclosure of governance-related factors than companies listed in Australia, our governance team will often draw on the insights and experience of our internal network of portfolio managers and the analysts who deal with the companies on a day-to-day basis. In addition, the research and advice provided by proxy advisers is also taken into consideration. Despite having this broad ability to source information, there will still be times when we possess insufficient information to make an informed voting decision and on these occasions we may specifically abstain from lodging a vote on a particular resolution.

WHY RESOLUTIONS WERE NOT SUPPORTED

Resolutions not supported by AMP Capital during the 2014/15 financial year related mainly to the election and re-election of directors, the ratification of share issues, ratification of specific incentive structures and support being sought for undisclosed resolutions.

Once again, our analysis shows a significant number of AMP Capital’s concerns could have been averted through improved disclosure. Pleasingly, many countries are making progress in this regard and have introduced a range of guidelines addressing the issue of disclosure.

VOTING FOR 2016 CALENDAR YEAR

0%

20%

40%

60%

80%

100%

90%

70%

50%

30%

10%

GREIT GLIF Asian Equity

Renumeration Other General MandateFinancial Statement Director Election Auditor Amend Articles

Categories of votes cast “Against Management”

AMP Capital: Corporate Governance Report | February 2016 17

GLOBAL REIT & GLOBAL LISTED INFRASTRUCTURE FUNDS

The two tables presented below summarise the particular governance concerns that led AMP Capital to vote against resolutions tabled at meetings of the Global Listed Real Estate Investment Trusts (GREIT) and the Global Listed Infrastructure Securities (GLIF) held in the AMP Capital portfolios.

As can be seen from this summary, an oft-recurring concern relates to the appropriateness of company directors particularly with regard to their independence and also the amount of time they have available to commit to their role as director.

Director Election Renumeration Share issue

Rela

ted

Part

y

Redu

ced

shar

ehol

der r

ight

s

Exce

ssiv

e bo

ard

disc

reti

on

Oth

er

Ind

epen

den

ce

Ove

r-b

oard

ing

Oth

er

Qu

antu

m

Stru

ctu

re

Too

dilu

tive

Dis

clos

ure

USA 4&9

France 7

Brazil 8

Thailand 9

Switzerland

Philippines 9

Hong Kong

Italy

Indonesia 1 9

UK

Canada

Spain

Japan 8

Portugal 1

Mexico

Australia

China

Turkey

For 93%

Against 5%

Abstain 1%

Other 1%

191 MEETINGS153 COMPANIES1749 RESOLUTIONS

1 Lack of information or poor track-record2 Poor attendance record3 Terms of proposed merger4 General lack of alignment with shareholder interests5 Terms of proposal to pay dividend in scrip and approval for political donations6 Terms of stock issue to fund property purchase7 Poison Pill8 Lack of appropriate skill/independence9 Poor disclosure, insufficient information

GLOBAL LISTED INFRASTRUCTURE FUNDS (2015)

177 MEETINGS164 COMPANIES1403 RESOLUTIONS

For 94%

Against 3%

Abstain 2%

Other 1%

GLOBAL LISTED REIT FUNDS (2015)

Director Election Renumeration Share issue

Rela

ted

Par

ty

Redu

ced

shar

ehol

der r

ight

s

Exce

ssiv

e b

oard

dis

cret

ion

Oth

er

Ind

epen

den

ce

Ove

r-b

oard

ing

Oth

er

Qu

antu

m

Stru

ctu

re

Too

dilu

tive

Dis

clos

ure

Canada 1

USA

France 2

Japan 3

Australia

New

Zealand

Hong Kong

Italy 4

Cayman Is. 2

UK 5

Singapore 6

18 AMP Capital: Corporate Governance Report | February 2016

Externally-managed portfolios

For 88%

Against 9%

Abstain 1%

Other 2%

* Note: AMP Capital has direct visibility over the voting activity of the majority of our external managers. This data provides a high level summary of those votes.

Approximately 88% of votes cast by external managers were cast in line with recommendations made by company boards.

47 MANAGERS4623 MEETINGS3854 COMPANIES44,581 RESOLUTIONS

Reasons for voting against resolutions:

China: The vast majority of unsupported resolutions related to stock issuance that was either dilutive, excessively discounted or at an unspecified price. Others included the election of directors where there was a lack of independence or who were over-boarded, overly generous share option schemes and financial agreements between companies that may not be in the best interests of shareholders.

Hong Kong: Concerns during this period included the election of directors that were over-boarded, lacked independence or had a poor attendance record. Other resolutions not supported included; the issuance of stock at terms not disclosed or not in the interests of current shareholders, amendments to Articles of Association contrary to the interests of shareholders, share buy backs at undisclosed prices and a scheme of arrangement executed at a historic low share price.

Bermuda and Cayman Islands: Many companies held in our international portfolios are listed in the Cayman Islands or Bermuda. Governance concerns at those companies included: poor board composition, poor audit independence/quality, related party transactions, issuance of stock at overly discounted or undisclosed prices, and providing directors with wide ranging, undisclosed powers.

Indonesia: In the main concerns related to: the election of non-independent directors, excessive remuneration and poor disclosure when amending Articles of Association, proposing acquisitions, appointing directors and/or auditors, providing financial guarantees.

Taiwan: Concerns included: unfettered discretion given to directors, excessively discounted stock issuance or insufficient disclosure of terms, allowing directors to hold positions in competitor companies opening the risk of conflicts of interests, and the proposed election of directors with insufficient disclosure.

Republic of Korea: Concerns included: directors that were not independent or that had a poor record of attendance, shareholders being asked to accept unaudited financial statements, and amendments to Articles of Association that are not in shareholders’ interests.

Philippines: Concerns included: poor board independence, over-boarded directors and unfettered discretion given to directors.

India: Concerns included: a lack of disclosure of audit fees, being asked to vote to adopt new Articles of Association with insufficient information, directors being slated that have poor attendance or that are not independent, and remuneration packages that are against shareholder interests.

Singapore: Concerns included: non-executive directors taking part in share option schemes, and shareholders being asked to support directors that have affiliates on committees, are not independent and/or have poor attendance.

Financial year 2015/16

120 MEETINGS183 COMPANIES1829 RESOLUTIONS

ASIAN EQUITIES (2015) EXTERNAL MANAGERS* (2015)

For many years, AMP Capital has offered clients the ability to invest in a range of multi-manager funds. These funds are designed to provide a single investment solution, blending a range of specialist investment managers in a single fund.

These funds aim to provide diversification across asset classes, manager types and manager styles, with the aim of achieving growth with smoother returns by negotiating the ups and downs of the market.

As AMP Capital actively manages the selection of investment managers (for multi-manager funds), we are constantly assessing and implementing new opportunities with the potential to improve the risk and return outcomes of clients’ portfolios.

External managers exercise votes on the shares they hold on our behalf. However, AMP Capital monitors the voting and where concerns with regard to a specific governance issue, we can choose to override votes cast by the external manager. Further, AMP Capital also undertakes periodic reviews of our external managers with regard to their approach to considering ESG issues. Where possible, we seek opportunities to meet and discuss their approaches to voting and ESG integration more broadly.

ASIA

AMP Capital: Corporate Governance Report | February 2016 19

Team Profiles

Dr Ian Woods joined AMP Capital in December 2000, and since that time has focussed on how the issues of sustainability and ESG relate to financial investment and the investment risks. Ians’ background is in environmental and risk consulting both in Asia/Pacific region and Europe. Ian assesses the management of intangible assets of companies on the Australian Securities Exchange through the assessment of ESG issues and in engaging with these companies in the areas of corporate social responsibility and sustainability.

Ian also undertakes assessment of greenhouse gas risk issues for the wider AMP Capital Investment teams and has undertaken a number of studies in this area. He holds a PhD in Chemical Engineering from the University of Sydney, a Master of Environmental Law and a Master of Business Administration from the Australian Graduate School of Management.

IAN WOODS Head of ESG ResearchPhD Chem Eng MBA MEL AMP Capital 13 years, Industry 25 years [email protected]

Karin Halliday was appointed to her current position with AMP Capital in May 2000. She is responsible for determining how AMP Capital votes on behalf of the firm and its clients at all meetings held by the Australian companies in which AMP Capital invests. In doing so, Karin also monitors various aspects of corporate governance in many Australian companies.

Prior to this Karin had a range of Portfolio Management roles within AMP Capital Investors between June 1987 and June 1998, where she managed a wide range of Australian–based share trusts and was responsible the Australian and international share component of a range of separately managed portfolios. Karin joined AMP in January 1984. Karin has more than 30 years of experience in the industry and recently completed the Australian Institute of Company Directors’ Company Director Course.

KARIN HALLIDAY Manager, Corporate GovernanceBBus, FFin, GAICD AMP Capital 30 years, Industry 29 years [email protected]

Richard was appointed to his current role of ESG Team Assistant Analyst in January 2015. Prior to joining AMP Capital in 2013 as a Business Operations Manager, Richard worked in a number of roles in both asset management and investment banking.

Richard started work in the financial services industry in 1995 with Standard Chartered in its Treasury team. Since then, Richard has held a number of roles including running the operational side of a hedge fund as well as working in a wide variety of roles in leading financial firms such as Goldman Sachs, HSBC and UBS in both London and Sydney. He holds a Bachelor of Arts (Honours) in Economics from Royal Holloway, University of London. Richard brings solid project management and governance experience to the ESG team.

RICHARD STANTON ESG Team Assistant AnalystBA (Hons), Economics AMP Capital 3 years, Industry 20 years [email protected]

Kristen joined the ESG Investment Research Team in October 2015 with responsibility for the analysis of ESG issues and sustainability drivers across a number of sectors, as well as company engagement on ESG practises at the board level. Kristen has a diverse background with experience across ESG research and corporate governance, sell-side investment advisory and commercial litigation.

Kristen joined AMP Capital from APP Securities, where she was Associate Director, Financials on the institutional desk, providing sell-side research to large institutions on banks, insurers and diversified financials. Prior to this, Kristen was a Senior Analyst with Ownership Matters, a corporate governance advisory firm where her clients included large fund managers. Before entering the investment industry, Kristen was a commercial litigator at Piper Alderman and ran large cases in the Supreme and Federal Courts for insurance and transport companies. Kristen started her career as a business journalist with Fairfax, writing on small and mid-cap companies for The Age, The Sydney Morning Herald and BRW.

Kristen holds bachelor degrees in Commerce and Law from the University of Sydney and has just completed her Master of Laws at the same institution.

KRISTEN LE MESURIER Senior ESG Analyst, Investment ResearchB Com, B Laws (Hons), Commerce and Law AMP Capital 0.5 years, Industry 3 years [email protected]