corporate governance developments developments john - pwc

TRANSCRIPT

CorporateGovernanceDevelopments

www.pwc.com

Developments(Audit Committee Focus)

June 2013

John Roche

Proposed to cover

Recent UK corporate governance changes for listed companies/funds

Challenges and questions for Audit Committees

Updates on “auditor reform” UK, EU etc

Local auditor oversight regime

PwC

Assessment of your auditor and audit quality

2June 2013Corporate Governance Developments

Landscape for listed entities and audit committeesOnly some things!

EU FinancialReporting Reform

EU Audit Reform

CompetitionCommission

Enquiry in UK

** Adopted

PwC

Enquiry in UK

EU CorporateGovernance

Reform

UK CorporateGovernanceChanges**

G8/G20/EUtax evasion and

avoidancedebate

IAASB Optionsfor Future Auditors

Report

3June 2013Corporate Governance Developments

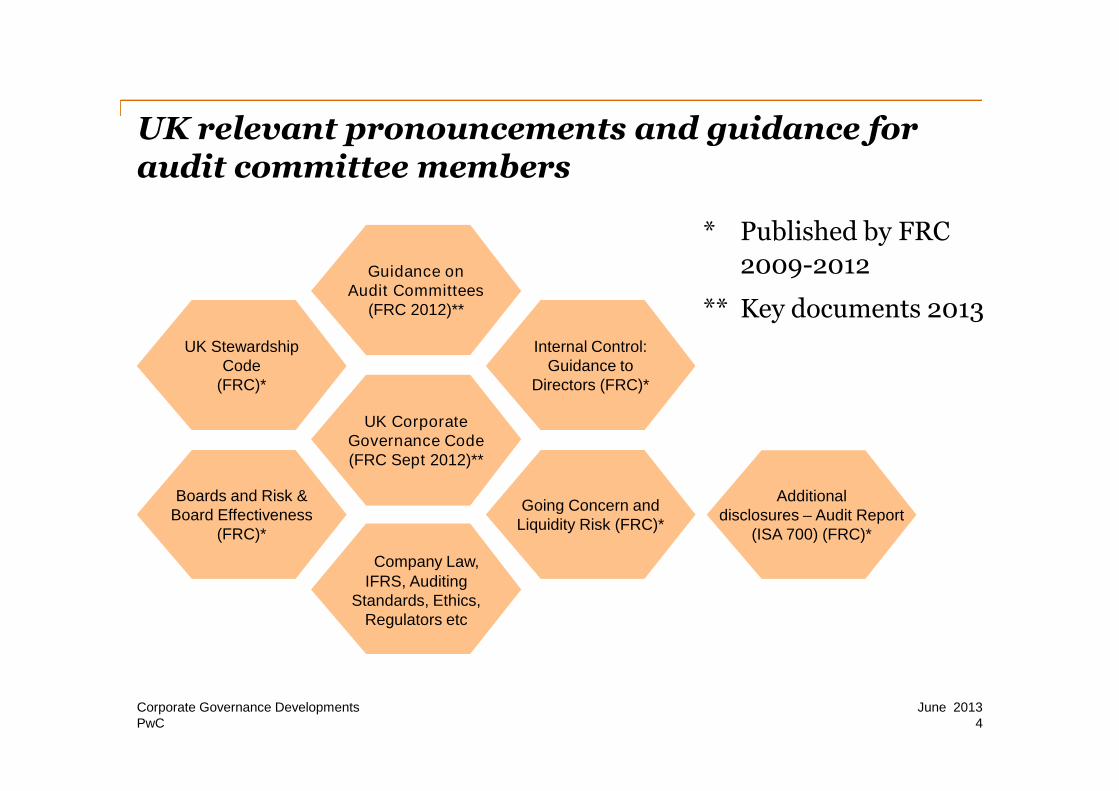

UK relevant pronouncements and guidance foraudit committee members

UK StewardshipCode

(FRC)*

Guidance onAudit Committees

(FRC 2012)**

Internal Control:Guidance to

Directors (FRC)*

* Published by FRC

2009-2012

** Key documents 2013

PwC

Boards and Risk &Board Effectiveness

(FRC)*

UK CorporateGovernance Code(FRC Sept 2012)**

Going Concern andLiquidity Risk (FRC)*

Company Law,IFRS, Auditing

Standards, Ethics,Regulators etc

4June 2013Corporate Governance Developments

Additionaldisclosures – Audit Report

(ISA 700) (FRC)*

Recent UK corporate governancechanges

UK Corporate Governance Code andGuidance on Audit Committees

PwC 5June 2013Corporate Governance Developments

New UK Corporate Governance CodeAll getting more challenging – key changes

Directors’ statement that the annualreport is “fair, balanced andunderstandable”…when requested bythe Board the Audit Committeeshould provide advice on this

Need to consider the annual report

From the user’s perspective, doesthe annual report communicateeffectively the business model,strategy and objectives, risk andcontrol, and performance andreward and all their linkages?

From the user’s perspective, doesthe annual report communicateeffectively the business model,strategy and objectives, risk andcontrol, and performance andreward and all their linkages?

PwC

Need to consider the annual reportand accounts, taken as a whole, isfair etc and provides necessaryinformation for shareholders toassess the company’s performance,business model and strategy

Consistency of front and back endand proper review done

reward and all their linkages?

What brief will the board give theAC to advise?

How does management keep ACinformed on performance andstrategy?

Who is responsible for making thenecessary checks?

reward and all their linkages?

What brief will the board give theAC to advise?

How does management keep ACinformed on performance andstrategy?

Who is responsible for making thenecessary checks?

6June 2013Corporate Governance Developments

New UK Corporate Governance CodeAll getting more challenging – key changes

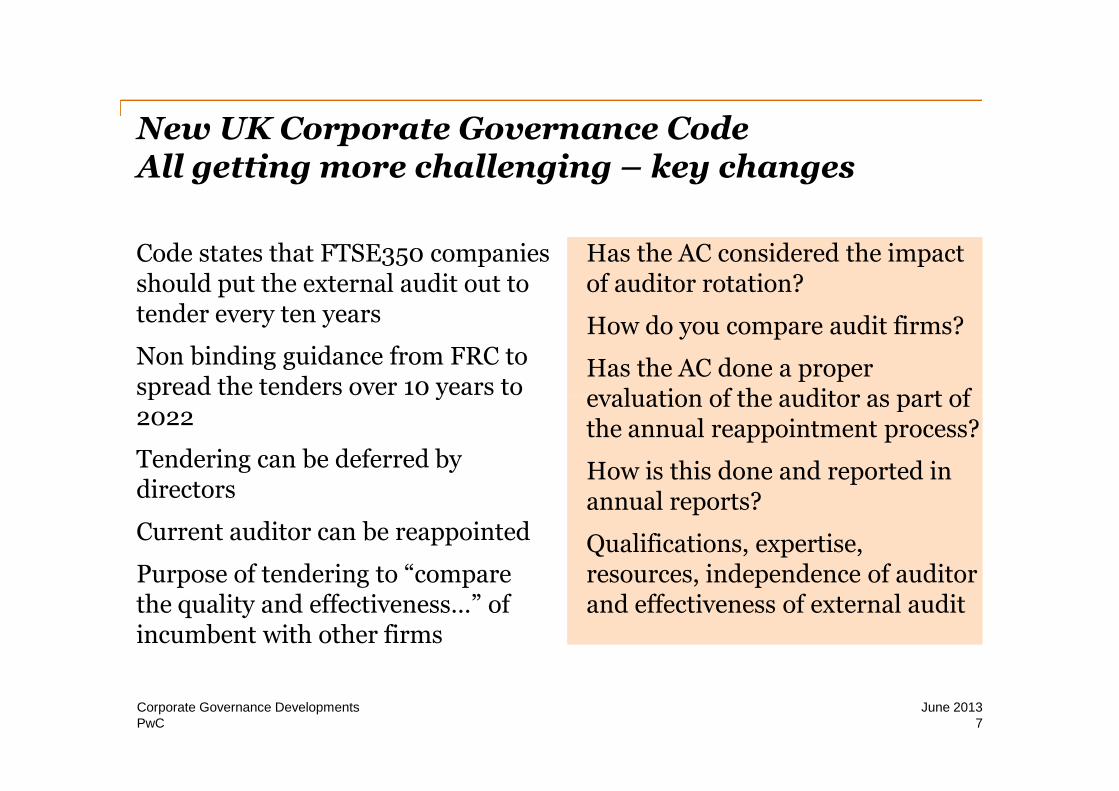

Code states that FTSE350 companiesshould put the external audit out totender every ten years

Non binding guidance from FRC tospread the tenders over 10 years to

Has the AC considered the impactof auditor rotation?

How do you compare audit firms?

Has the AC done a properevaluation of the auditor as part of

Has the AC considered the impactof auditor rotation?

How do you compare audit firms?

Has the AC done a properevaluation of the auditor as part of

PwC

spread the tenders over 10 years to2022

Tendering can be deferred bydirectors

Current auditor can be reappointed

Purpose of tendering to “comparethe quality and effectiveness…” ofincumbent with other firms

evaluation of the auditor as part ofthe annual reappointment process?

How is this done and reported inannual reports?

Qualifications, expertise,resources, independence of auditorand effectiveness of external audit

evaluation of the auditor as part ofthe annual reappointment process?

How is this done and reported inannual reports?

Qualifications, expertise,resources, independence of auditorand effectiveness of external audit

7June 2013Corporate Governance Developments

New UK Corporate Governance CodeFRC guidance on tendering

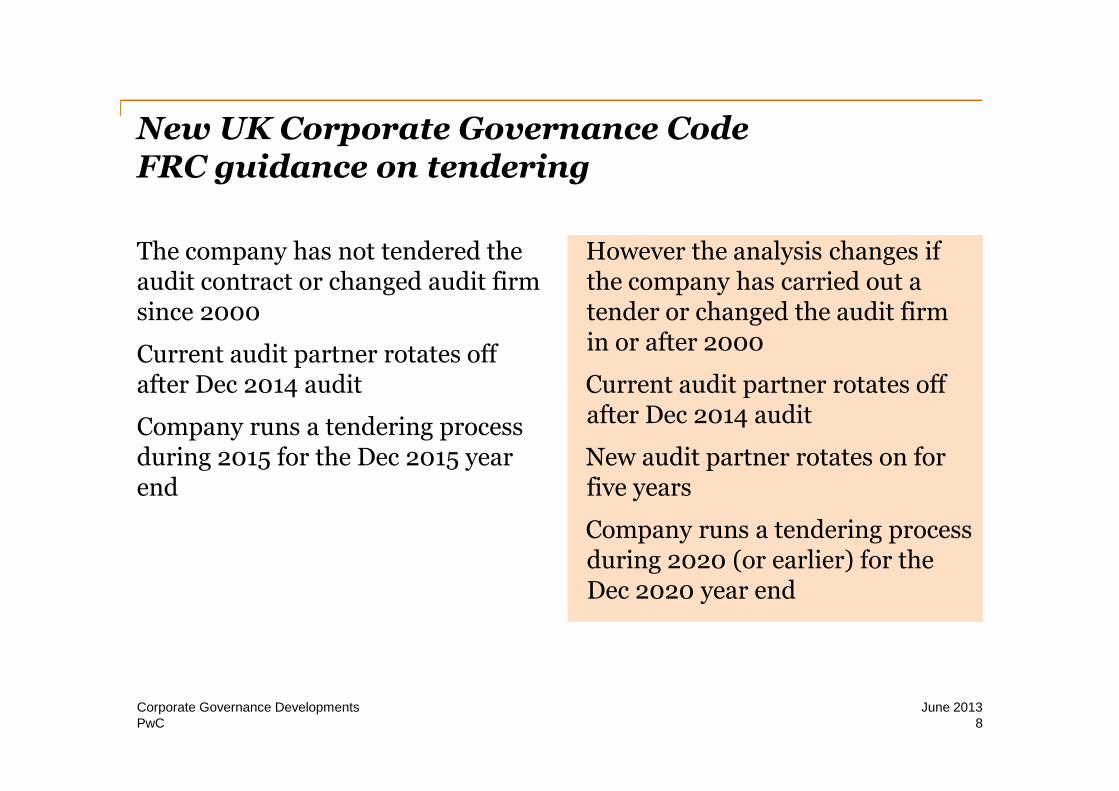

The company has not tendered theaudit contract or changed audit firmsince 2000

Current audit partner rotates offafter Dec 2014 audit

However the analysis changes ifthe company has carried out atender or changed the audit firmin or after 2000

Current audit partner rotates off

However the analysis changes ifthe company has carried out atender or changed the audit firmin or after 2000

Current audit partner rotates off

PwC

after Dec 2014 audit

Company runs a tendering processduring 2015 for the Dec 2015 yearend

Current audit partner rotates offafter Dec 2014 audit

New audit partner rotates on forfive years

Company runs a tendering processduring 2020 (or earlier) for theDec 2020 year end

Current audit partner rotates offafter Dec 2014 audit

New audit partner rotates on forfive years

Company runs a tendering processduring 2020 (or earlier) for theDec 2020 year end

8June 2013Corporate Governance Developments

New UK Corporate Governance CodeAll getting more challenging – key changes

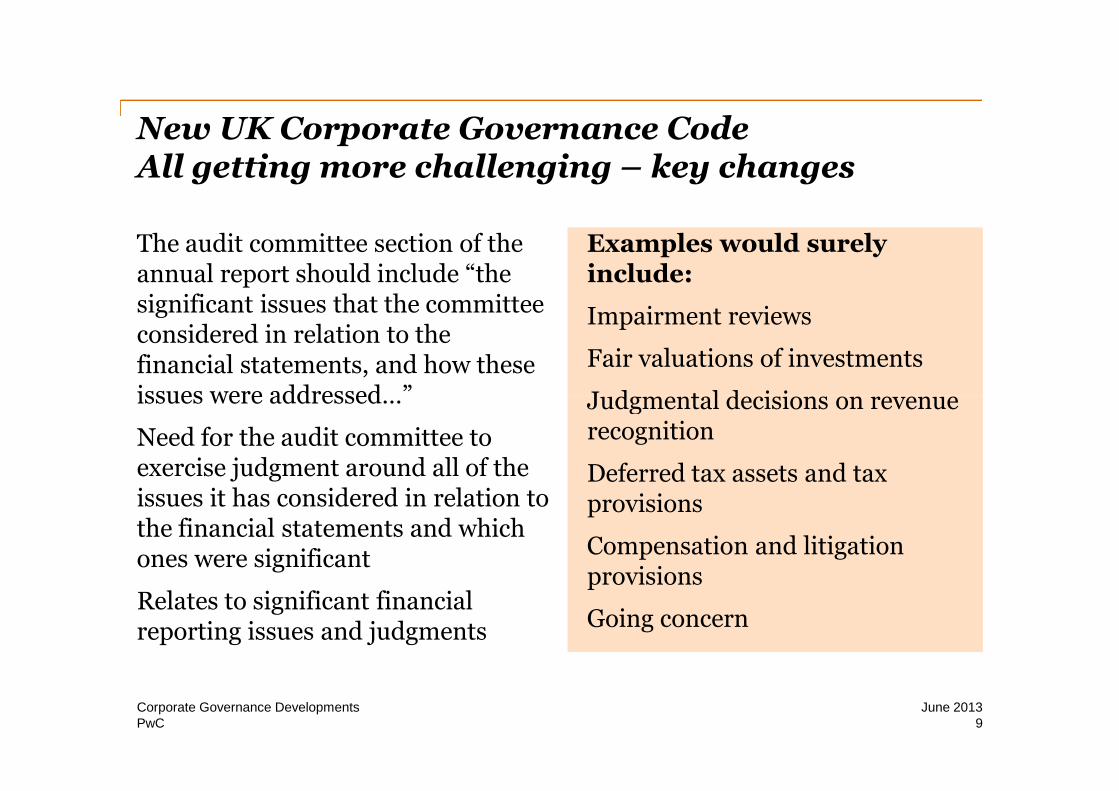

The audit committee section of theannual report should include “thesignificant issues that the committeeconsidered in relation to thefinancial statements, and how theseissues were addressed…”

Examples would surelyinclude:

Impairment reviews

Fair valuations of investments

Judgmental decisions on revenue

Examples would surelyinclude:

Impairment reviews

Fair valuations of investments

Judgmental decisions on revenue

PwC

issues were addressed…”

Need for the audit committee toexercise judgment around all of theissues it has considered in relation tothe financial statements and whichones were significant

Relates to significant financialreporting issues and judgments

Judgmental decisions on revenuerecognition

Deferred tax assets and taxprovisions

Compensation and litigationprovisions

Going concern

Judgmental decisions on revenuerecognition

Deferred tax assets and taxprovisions

Compensation and litigationprovisions

Going concern

9June 2013Corporate Governance Developments

September 2012 FRC Guidance on AuditCommittees…new Bible

Summary of role of AC

Names and qualifications of members of AC

Number of AC meetings

Significant issues considered and howaddressed

PwC 10June 2013Corporate Governance Developments

addressed

How assessed effectiveness of the externalaudit process, approach to reappointment,tenure of audit firm, last tender date etc

Non audit services and independence/objectivity safeguards

Diversity – so who is sitting around your boardtable?

PwC 11June 2013Corporate Governance Developments

Diversity – so who is sitting around your boardtable?

PwC 12June 2013Corporate Governance Developments

Challenges and questions for auditcommittees

(Copied from Chartered Accountants Ireland publication Jan 2013)

PwC 13June 2013Corporate Governance Developments

Challenges for 2013

Financial reporting process

Audit market reform

Finance talent management –who is your finance function andhow are you comforted it works

Regulation and compliance

Evaluation of effectiveness of theaudit committee and externalaudit process

Continued poor economic outlook

PwC

Interaction with external auditor

Interaction with internal audit(whose internal audit?)

Oversight of internal controls andrisk management

IT and systems risk

and impact on business, keypartners used in outsourcing,liquidity, funding, performanceetc

14June 2013Corporate Governance Developments

Some important questions?

What information AC receive onstability of key business partners?

Role of AC in reviewing fundingand liquidity issues?

Does “management” monitoraccounting policy changes and

External auditor evaluated?

External auditor challengedsignificant managementestimates?

Competence of your financefunction?

PwC

accounting policy changes andimpacts on business andaccounts?

Strategy or plan in place to adoptnew standards?

How does the AC keep abreast ofregulatory developments?

Considered auditor rotation/tendering?

function?

Tools to monitor risk andemerging risks?

Information on key systems andreliance on those?

AC comfortable aware of keybusiness compliancerequirements?

15June 2013Corporate Governance Developments

Updates on “audit reform” UK, EU etc

PwC 16June 2013Corporate Governance Developments

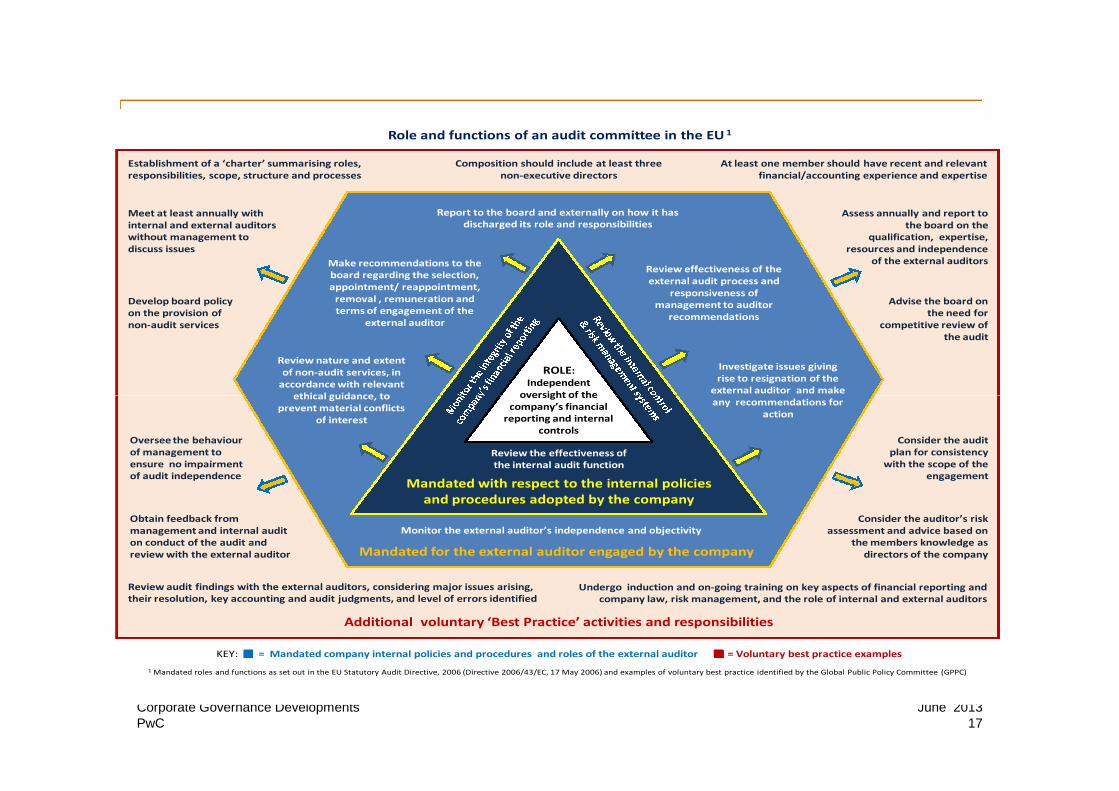

Make recommendations to theboard regarding the selection,appointment/ reappointment,

removal , remuneration andterms of engagement of the

external auditor

Review effectiveness of theexternal audit process and

responsiveness ofmanagement to auditor

recommendations

Review nature and extentof non-audit services, in

accordance with relevantethical guidance, to

Investigate issues givingrise to resignation of the

external auditor and make

Role and functions of an audit committee in the EU 1

ROLE:Independent

oversight of the

Report to the board and externally on how it hasdischarged its role and responsibilities

Establishment of a ‘charter’ summarising roles,responsibilities, scope, structure and processes

Composition should include at least threenon-executive directors

At least one member should have recent and relevantfinancial/accounting experience and expertise

Meet at least annually withinternal and external auditorswithout management todiscuss issues

Assess annually and report tothe board on the

qualification, expertise,resources and independence

of the external auditors

Develop board policyon the provision ofnon-audit services

Advise the board onthe need for

competitive review ofthe audit

PwC 17June 2013Corporate Governance Developments

ethical guidance, toprevent material conflicts

of interest

Monitor the external auditor’s independence and objectivity

external auditor and makeany recommendations for

action

Mandated for the external auditor engaged by the company

Review the effectiveness ofthe internal audit function

Mandated with respect to the internal policiesand procedures adopted by the company

oversight of thecompany’s financial

reporting and internalcontrols

Additional voluntary ‘Best Practice’ activities and responsibilities

Undergo induction and on-going training on key aspects of financial reporting andcompany law, risk management, and the role of internal and external auditors

Oversee the behaviourof management toensure no impairmentof audit independence

Review audit findings with the external auditors, considering major issues arising,their resolution, key accounting and audit judgments, and level of errors identified

Consider the auditplan for consistency

with the scope of theengagement

Consider the auditor’s riskassessment and advice based on

the members knowledge asdirectors of the company

Obtain feedback frommanagement and internal auditon conduct of the audit andreview with the external auditor

1 Mandated roles and functions as set out in the EU Statutory Audit Directive, 2006 (Directive 2006/43/EC, 17 May 2006) and examples of voluntary best practice identified by the Global Public Policy Committee (GPPC)

KEY: = Mandated company internal policies and procedures and roles of the external auditor = Voluntary best practice examples

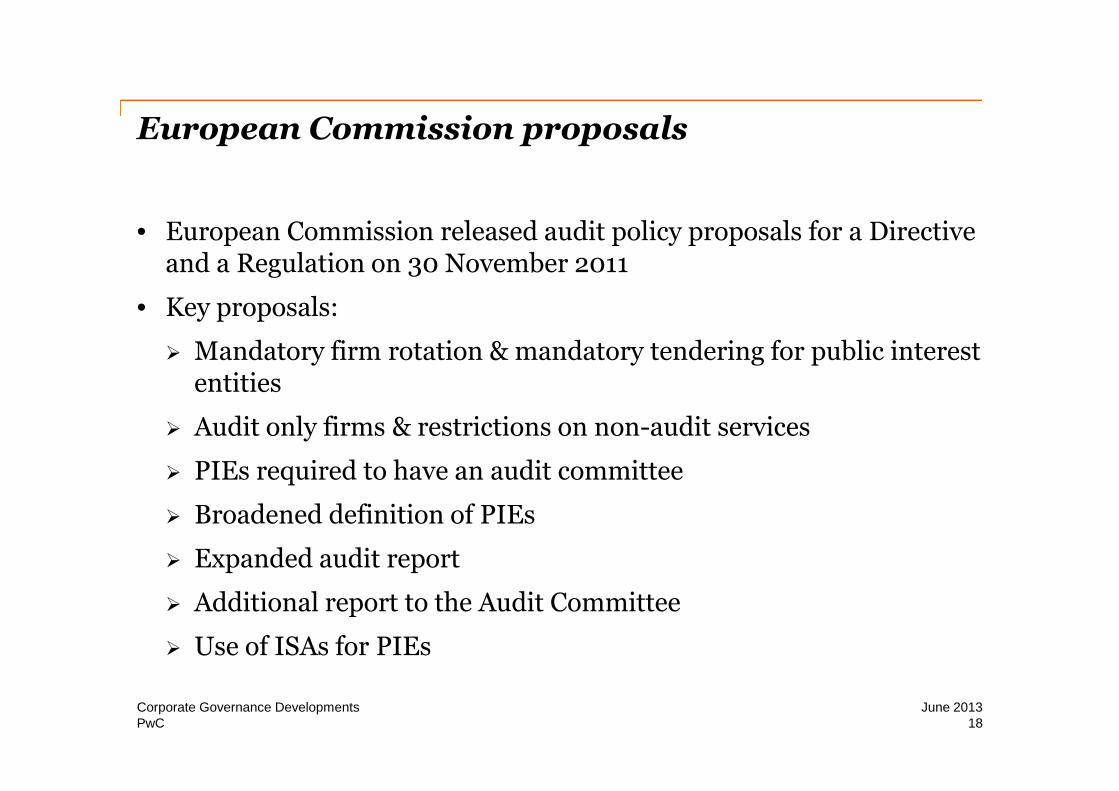

European Commission proposals

• European Commission released audit policy proposals for a Directiveand a Regulation on 30 November 2011

• Key proposals:

Mandatory firm rotation & mandatory tendering for public interestentities

PwC

entities

Audit only firms & restrictions on non-audit services

PIEs required to have an audit committee

Broadened definition of PIEs

Expanded audit report

Additional report to the Audit Committee

Use of ISAs for PIEs

18June 2013Corporate Governance Developments

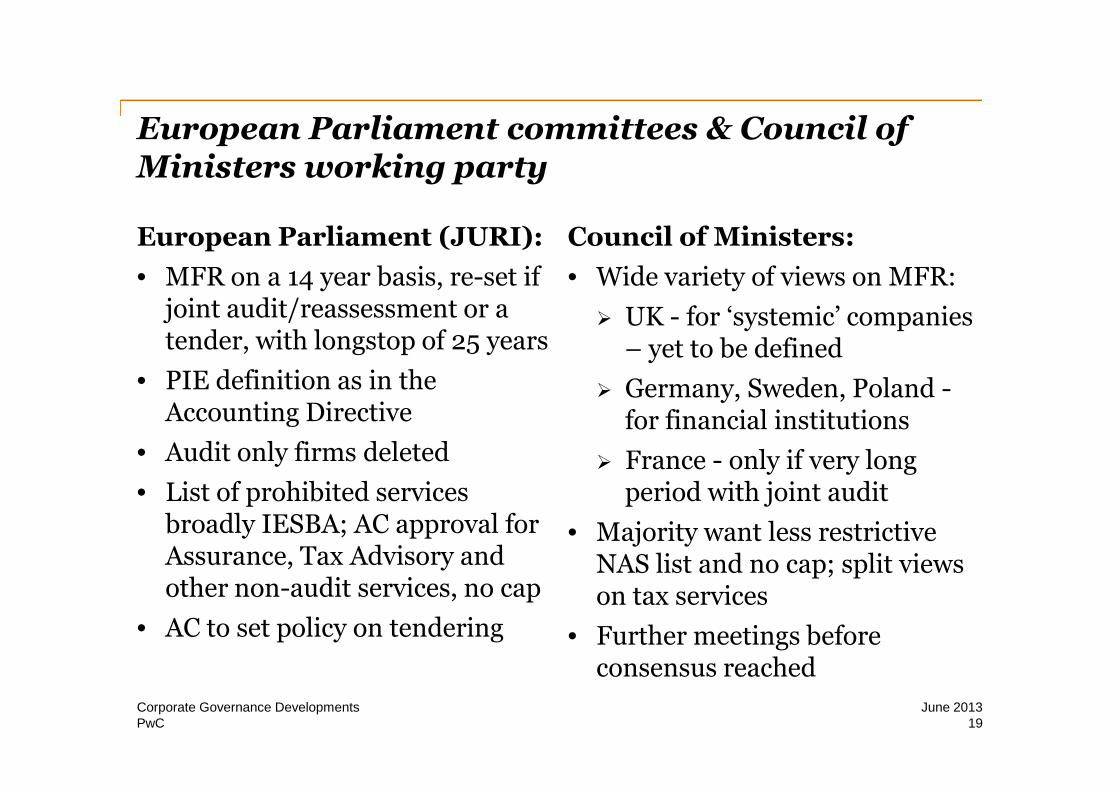

European Parliament committees & Council ofMinisters working party

European Parliament (JURI):

• MFR on a 14 year basis, re-set ifjoint audit/reassessment or atender, with longstop of 25 years

• PIE definition as in the

Council of Ministers:

• Wide variety of views on MFR:

UK - for ‘systemic’ companies– yet to be defined

Germany, Sweden, Poland -

PwC

Accounting Directive

• Audit only firms deleted

• List of prohibited servicesbroadly IESBA; AC approval forAssurance, Tax Advisory andother non-audit services, no cap

• AC to set policy on tendering

Germany, Sweden, Poland -for financial institutions

France - only if very longperiod with joint audit

• Majority want less restrictiveNAS list and no cap; split viewson tax services

• Further meetings beforeconsensus reached

19June 2013Corporate Governance Developments

Competition CommissionEurope was perhaps waiting to see this…

Same audit firm for more than 20 years…

Significant hurdles in way to compare offering ofcurrent auditor with competitors

Difficult for companies to judge audit quality inadvance due to nature of the audit

31% ofFTSE100

20% of

PwC

Companies and audit firms invest in mutualrelationship which is hard to walk away from

Management face significant time costs to selectand educate a new auditor

Mid tier firms face experience/reputation barriersto expand and selection in FTSE350 market

Auditors in the pockets of management whenservicing management demand

20% ofFTSE250

20June 2013Corporate Governance Developments

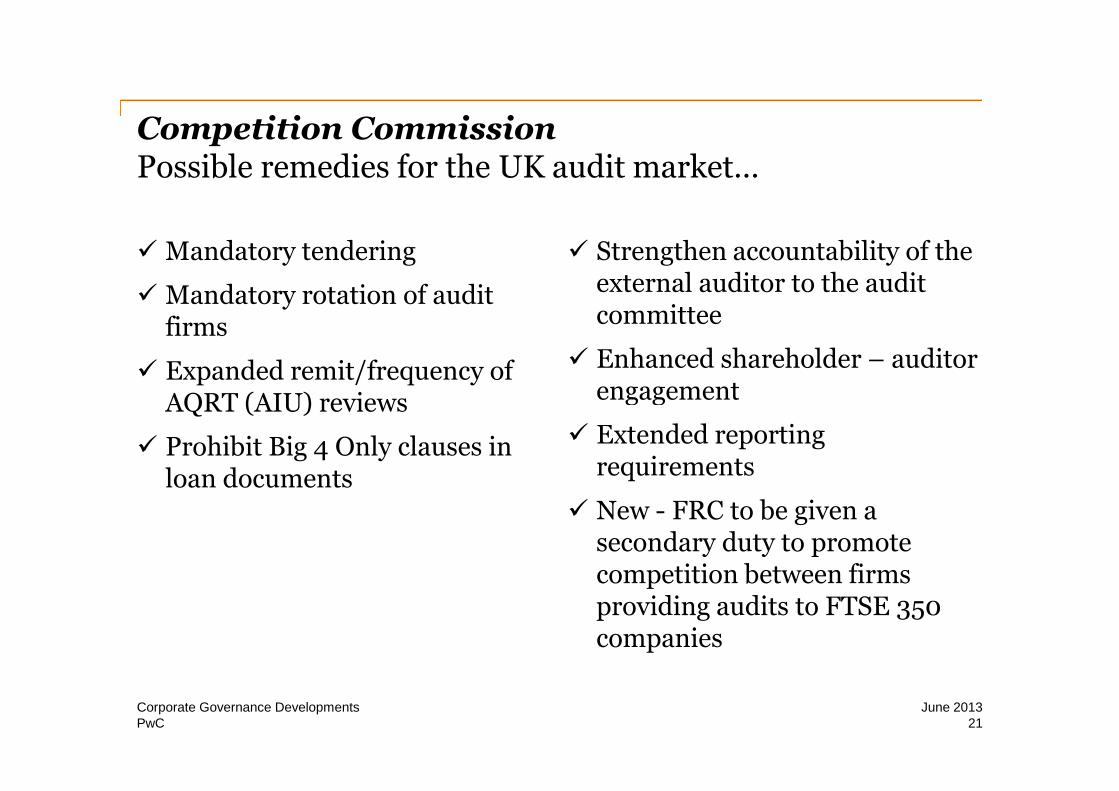

Competition CommissionPossible remedies for the UK audit market…

Mandatory tendering

Mandatory rotation of auditfirms

Expanded remit/frequency ofAQRT (AIU) reviews

Strengthen accountability of theexternal auditor to the auditcommittee

Enhanced shareholder – auditorengagement

PwC

AQRT (AIU) reviews

Prohibit Big 4 Only clauses inloan documents

engagement

Extended reportingrequirements

New - FRC to be given asecondary duty to promotecompetition between firmsproviding audits to FTSE 350companies

21June 2013Corporate Governance Developments

Local audit oversight regime

PwC 22June 2013Corporate Governance Developments

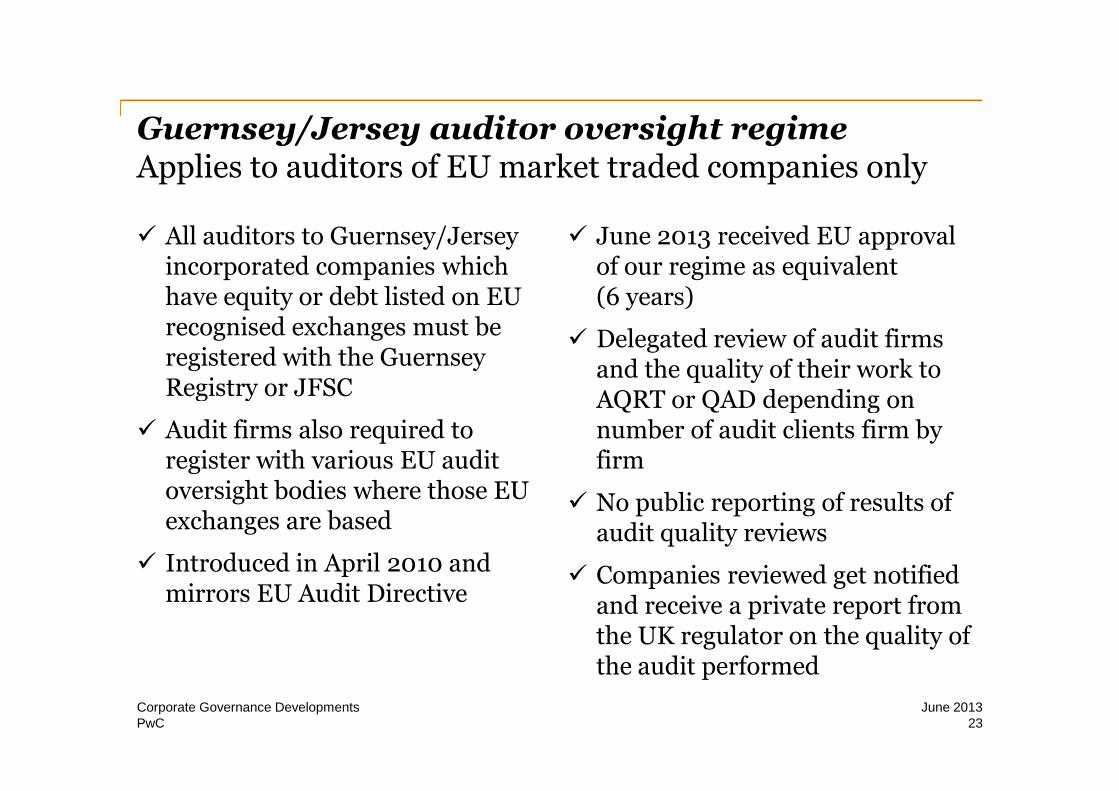

Guernsey/Jersey auditor oversight regimeApplies to auditors of EU market traded companies only

All auditors to Guernsey/Jerseyincorporated companies whichhave equity or debt listed on EUrecognised exchanges must beregistered with the GuernseyRegistry or JFSC

June 2013 received EU approvalof our regime as equivalent(6 years)

Delegated review of audit firmsand the quality of their work toAQRT or QAD depending on

PwC

Registry or JFSC

Audit firms also required toregister with various EU auditoversight bodies where those EUexchanges are based

Introduced in April 2010 andmirrors EU Audit Directive

AQRT or QAD depending onnumber of audit clients firm byfirm

No public reporting of results ofaudit quality reviews

Companies reviewed get notifiedand receive a private report fromthe UK regulator on the quality ofthe audit performed

23June 2013Corporate Governance Developments

Assessment of auditor and quality

PwC 24June 2013Corporate Governance Developments

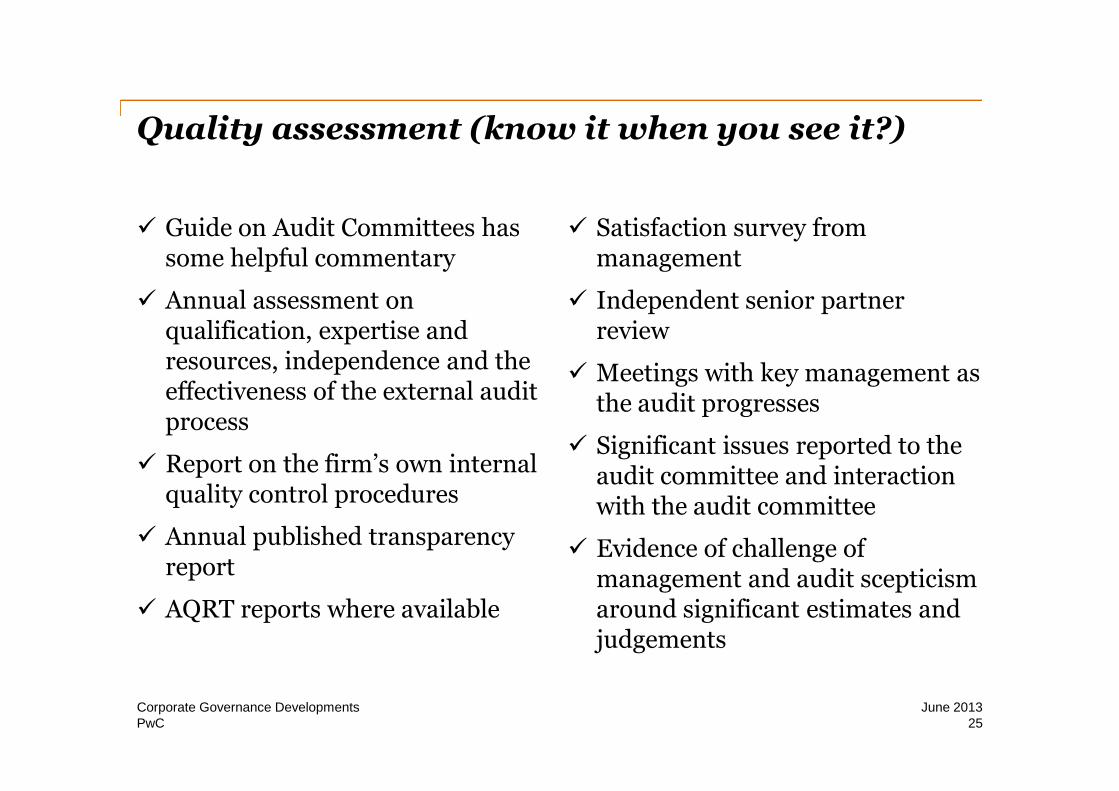

Quality assessment (know it when you see it?)

Guide on Audit Committees hassome helpful commentary

Annual assessment onqualification, expertise andresources, independence and theeffectiveness of the external audit

Satisfaction survey frommanagement

Independent senior partnerreview

Meetings with key management asthe audit progresses

PwC

effectiveness of the external auditprocess

Report on the firm’s own internalquality control procedures

Annual published transparencyreport

AQRT reports where available

the audit progresses

Significant issues reported to theaudit committee and interactionwith the audit committee

Evidence of challenge ofmanagement and audit scepticismaround significant estimates andjudgements

25June 2013Corporate Governance Developments

This publication has been prepared for general guidance on matters of interest only, and doesnot constitute professional advice. You should not act upon the information contained in thispublication without obtaining specific professional advice. No representation or warranty(express or implied) is given as to the accuracy or completeness of the information containedin this publication, and, to the extent permitted by law, PricewaterhouseCoopers CI LLP, itsmembers, employees and agents do not accept or assume any liability, responsibility or duty ofcare for any consequences of you or anyone else acting, or refraining to act, in reliance on theinformation contained in this publication or for any decision based on it.

© 2013 PricewaterhouseCoopers CI LLP. All rights reserved. ‘PricewaterhouseCoopers’ and‘PwC’ refers to the Channel Island firm of PricewaterhouseCoopers CI LLP or, as the contextrequires, the PricewaterhouseCoopers global network or other member firms of the network,each of which is a separate and independent legal entity. PricewaterhouseCoopers CI LLP, alimited liability partnership registered in England with registered number OC309347, providesassurance, advisory, and tax services. The registered office is 1 Embankment Place, LondonWC2N 6RH and its principal place of business is 37 Esplanade, St. Helier, Jersey JE1 4XA.