cormorant east - society of petroleum engineers uk east rob... · rob kuyper, taqa bratani, 27...

TRANSCRIPT

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Cormorant East UKCS record for oil field development: 85 days from discovery to first oil

Rob Kuyper – Development Manager TAQA Bratani

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Outline

• The “Contender” prospect

• The challenges

• Block ownership, Field boundaries, Tax, Economics

• Tax intermezzo

• Stay awake

• DECC help

• Timeline and results

• Key points to take away 2

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

TAQA Operated Assets - Northern North Sea

3

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

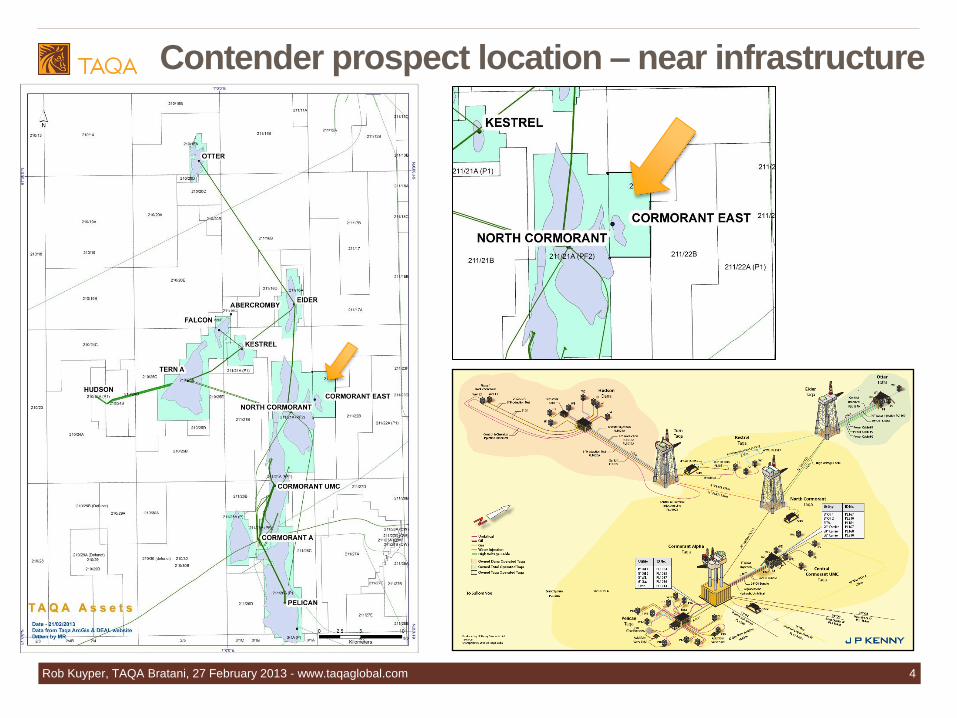

Contender prospect location – near infrastructure

4

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Contender prospect location – known Brent play

North Cormorant

“Block IV”

Contender

Brent reservoir

• “Slump block”

off North Cormorant

Key risks:

• Oil fill

• Rock properties:

diagenesis

5

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Faults difficult to interpret

Contender prospect location – difficult seismic

6

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Contender opportunity Drillable from recently reactivated rig on North Cormorant platform

7

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Challenge 1: Block ownership

• Contender prospect in block without TAQA equity

• Contender prospect too small to justify own development

• TAQA owns infrastructure that can drill and produce the prospect

Solution:

TAQA drills well and earns equity. Contender partners benefit from development Win-win

211/21a

(TAQA)

211/22a (NW)

(no TAQA)

North Cormorant

Block IV Contender prospect

8

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

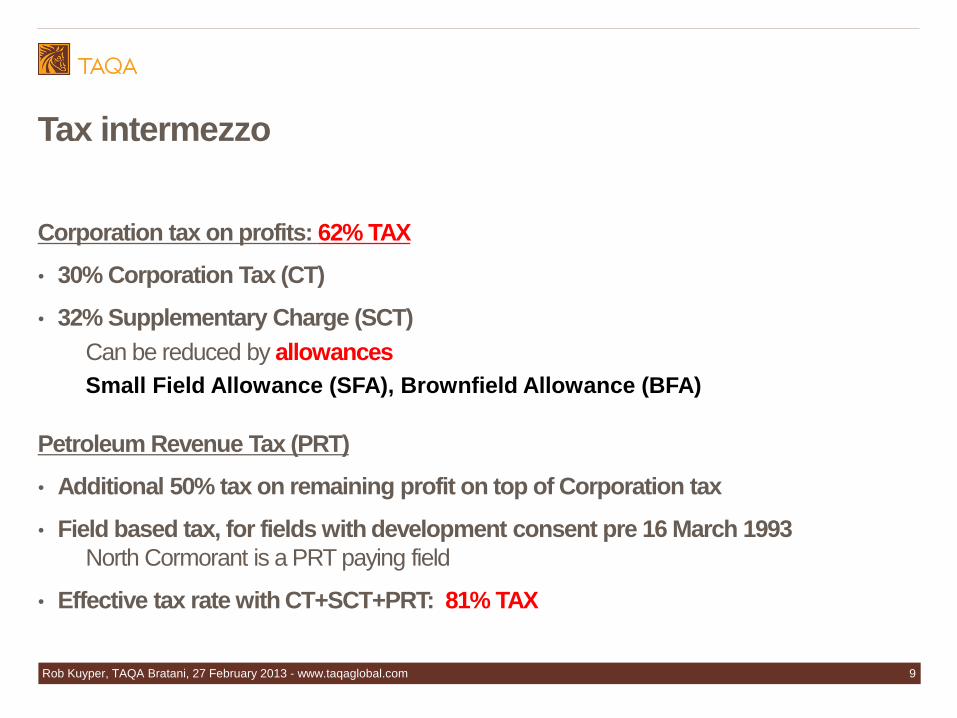

Tax intermezzo

Corporation tax on profits: 62% TAX

• 30% Corporation Tax (CT)

• 32% Supplementary Charge (SCT)

Can be reduced by allowances

Small Field Allowance (SFA), Brownfield Allowance (BFA)

Petroleum Revenue Tax (PRT)

• Additional 50% tax on remaining profit on top of Corporation tax

• Field based tax, for fields with development consent pre 16 March 1993

North Cormorant is a PRT paying field

• Effective tax rate with CT+SCT+PRT: 81% TAX

9

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Tax intermezzo

Options to help economically marginal developments like Contender

1. Small Field Allowance

• For new fields with FDP reserves below appr 40-50 mln stb oil

• Up to £150 mln allowance on SCT (so 32% x £150 mln = £48 mln less tax),

to be earned through production revenue

2. “Redetermination of oil field boundaries on economic grounds”

• Carve-out part of a PRT-paying field,if development is commercially

difficult

• Allows an unexploited part of a previously determined PRT-liable field to

be a new, separate field

Note that “Brown Field Allowance” was only introduced 7 Sep 2012

https://www.gov.uk/oil-and-gas-taxation

10

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Challenge 2: Field boundaries

• Contender prospect just outside North Cormorant field area

• Drilling a North Cormorant well would normally get PRT-relief on costs.

• Contender exploration would not be economically attractive without this relief.

Solution:

Extend North Cormorant field boundary to include Contender Win-win

Original

North

Cormorant

field area

North Cormorant

extension area

Top Brent Depth Map

11

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

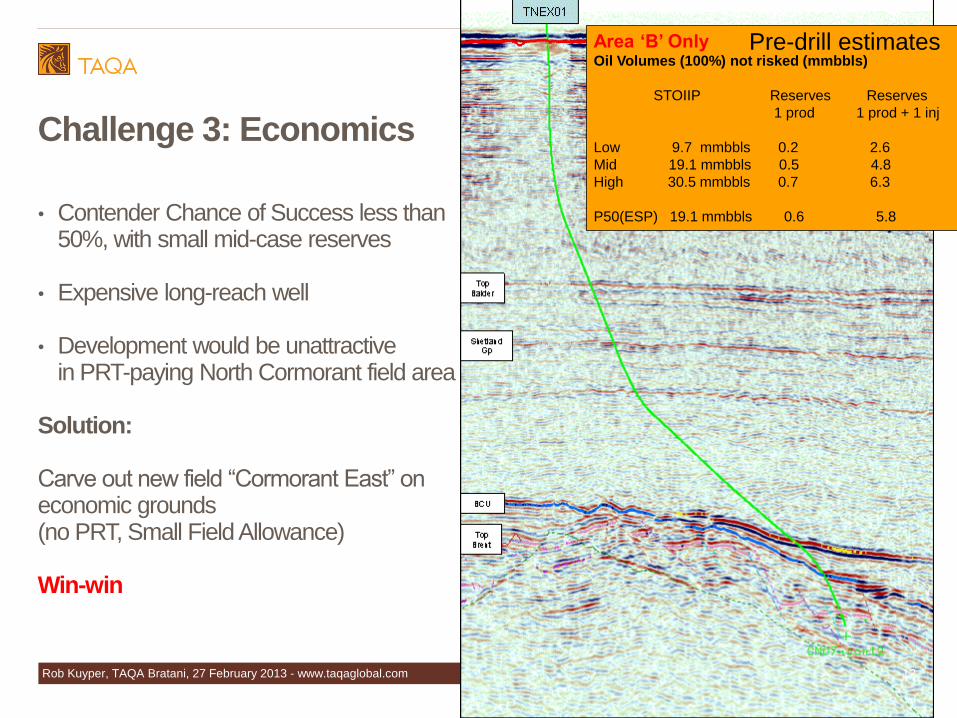

Challenge 3: Economics

• Contender Chance of Success less than 50%, with small mid-case reserves

• Expensive long-reach well

• Development would be unattractive in PRT-paying North Cormorant field area

Solution:

Carve out new field “Cormorant East” on economic grounds (no PRT, Small Field Allowance) Win-win

Area ‘B’ Only Oil Volumes (100%) not risked (mmbbls)

STOIIP Reserves Reserves

1 prod 1 prod + 1 inj

Low 9.7 mmbbls 0.2 2.6

Mid 19.1 mmbbls 0.5 4.8

High 30.5 mmbbls 0.7 6.3

P50(ESP) 19.1 mmbbls 0.6 5.8

Pre-drill estimates

12

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

DECC support

• Extend North Cormorant PRT boundary to include Contender prospect

PRT relief on Contender well

• Review and support Field Development Plan before discovery

• Cormorant East carve out from North Cormorant PRT area on economic grounds

PRT-exempt development

Small Field Allowance for new field

In summary Contender drilling and Cormorant East development would not have been commercially attractive without the above support by DECC.

No development = no profit = no tax income Win-win

13

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Timeline How to achieve 85 days between discovery and new field production?

• Farm-in agreement – April 2011

• All development preparations worked before well spud

• Permits, Licences, Authorisations, Notifications and Consents

• Field Development Plan and Field Determinations (carve out)

• All development equipment ordered before well spud

• Completion, ESP, hookup – re-usable in case of failure

• Well spud September – oil found on 17th October 2012

• Direct turn-around in DECC, while completing the well

• First oil on 10th January 2013

14

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Well results

Contender well found

• Thick Tarbert sand

• Fully oil filled

• Good reservoir properties

• 10-30 MMstb oil in place?

However…

• Crossed a fault into Triassic below Tarbert: no further Brent sands

• More reservoir and volumes expected downdip and in other fault blocks

15

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

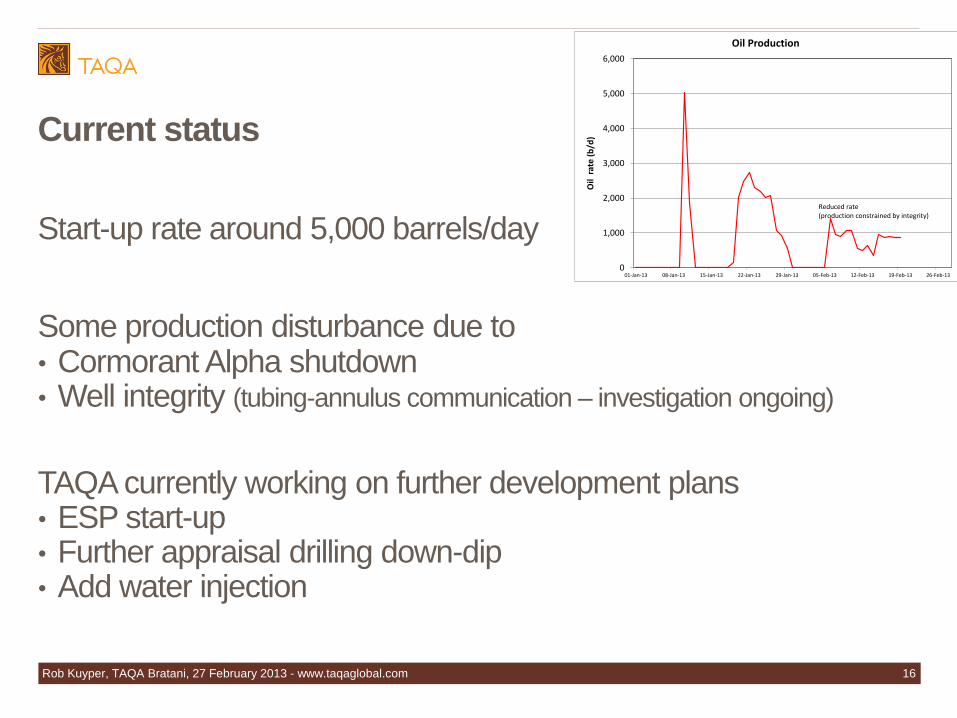

Current status

Start-up rate around 5,000 barrels/day

Some production disturbance due to • Cormorant Alpha shutdown • Well integrity (tubing-annulus communication – investigation ongoing)

TAQA currently working on further development plans • ESP start-up • Further appraisal drilling down-dip • Add water injection

0

1,000

2,000

3,000

4,000

5,000

6,000

01-Jan-13 08-Jan-13 15-Jan-13 22-Jan-13 29-Jan-13 05-Feb-13 12-Feb-13 19-Feb-13 26-Feb-13

Oil

rat

e (

b/d

)

Oil Production

Reduced rate(production constrained by integrity)

16

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

What did we learn? Key points to take away

• Plan for development while exploring

• Short timeline to first oil

• Mature basin: infrastructure will not be there forever

• Normally limited regret costs

• Know tax options

• Allowances and options available to make marginal developments

commercial

• Most of the time, there are ‘win-win’ scenarios

17

Rob Kuyper, TAQA Bratani, 27 February 2013 - www.taqaglobal.com

Acknowledgements

• SPE

• DECC

• Cormorant East partners

TAQA Bratani Limited

Dana Petroleum (E&P) Limited

Antrim Resources (N.I.) Limited

First Oil Expro Limited

Bridge Energy UK Limited

18