corep/finrep a technical insight - arkk solutions · 2015-05-09 · corep/finrep overview josef...

TRANSCRIPT

COREP/FINREP A Technical Insight

26 June 2013, London

PRESENTERS

COREP/FINREP OVERVIEW Josef Macdonald AND TECHNICAL BRIEFING External Consultant

Michal Skopowski External Consultant

COREP EXPERIENCE Richard Metcalfe

Director, London

AGENDA

1) UNDERSTANDING THE REQUIREMENTS

2) TECHNICAL BRIEFING

3) CHALLENGES

1) UNDERSTANDING THE REQUIREMENTS

FINANCIAL MARKETS SUPERVISION IN EU

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

European Banking Authority

European Insurance and Occupa/onal Pensions Authority

European Securi/es and

Markets Authority

supervisory colleagues

supervisory colleagues

supervisory colleagues

chairperson chairperson chairperson

un/l 2011 un/l 2011 un/l 2011

European System of Financial

Supervisors (ESFS)

European Systemic Risk Board (ESRB)

micro level

macro level

Single Supervisory Mechanism (SSM) will affect the current status quo: -‐ ECB involved in

monetary policy as well as supervision

-‐ ECB involved in micro-‐ and macro level supervision

-‐ Rela/on between EBA and ECB not in every scenario clear

-‐ Equilibrium between EBA, EIOPA and ESMA poten/ally affected

SUPERVISORY REPORTING LEVELS

NSA

CI

CI

CI

EBA

NSA

CI

CI

CI

Level 1 Level 2

ITS and DPMs Taxonomies

Source: Andreas Weller EBA XBRL 26, Dublin (adapted diagram)

DEPENDENCIES BETWEEN FRAMEWORKS AND INSTITUTIONS FOR BANKING SECTOR IN EU

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

JEGR

Data Model Taxonomy

common sta/s/cal requirements

Interna/onal standards

THREE PILLARS APPROACH FOR BASEL III

Basel III

Pillar I Minimum capital

requirements and Ra7os For example: • Own funds • Credit, market, opera7onal

risk requirements • Minimum capital ra7os • Minimum liquidity ra7os • Minimum leverage ra7o • Regulatory repor7ng

Pillar II Risk management and

supervision For example: • Stress tes7ng • Pruden7al supervision • Risk management • Capital buffers • Corporate governance • Supervisory colleges

Pillar III Market discipline

For example: • Public disclosure • Reconcilia7on of regulatory

capital to accoun7ng framework

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

INTERNATIONAL vs EUROPEAN LAW

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

Basel 2 2004

Basel 2,5 2009

Basel 3 2010

CRD (Direc/ve 2006/49/EC)

In force since Jan. 1, 2007

CRD III (Direc/ve 2010/76/EU)

In force since Dec. 31, 2011

CRR/CRD IV (Direc/ve and Regula/on)

In force since ???

CRD II (Direc/ve 2009/111/EC)

In force since Dec. 31, 2010

• Large exposures • Hybrid capital

instruments • Liquidity risk

management • Cross border

supervision

• Higher risk for resecuri/sa/on in banking book

• Securi/sa/on in trading book

• Stressed VAR • Incremental default

and migra/on risk (IRC)

• Remunera/on policies (i.e. earnings above 1 mn EUR)

• Defini/on of capital • Credit risk approach • Opera/onal risk

Regula/on: • Upgrade of capital defini/on • Single rule book • Credit valua/on adjustment • Charge for CCPs • Liquidity coverage • Counterparty credit risk • Leverage ra/o • Wrong-‐way risk (EAD) Direc/ve • Capital buffers • Enhanced governance and

supervision • Sanc/ons • SIFI

• Exemplary shordalls of CRD I-‐III: • Systemic risk was not appropriately addressed • Excessive leverage • Insufficient liquidity • Not adequate and low quality of own funds • Procyclical effects

LACK OF COMPARABILITY OF DATA FOR CRD I-III REPORTING

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

Basel II

EC 2006/48 & 49 …

Country 1

NBP 1

Report 2 Report 1

------------------------------------

Country 3 Country 2 Country 27

NCB 2 FSA 3 NBB 27

Report 3

----------------------------------------------------------------------------------------------------------------------------------------------------------------

Transi/on into na/onal legisla/on

(na7onal op7ons)

European Law 9X,XX% best prac/ces + EU requirements

OBLIGATORY but so far mostly DIRECTIVES!

Na/onal implementa/on

Challenge! RelaPons between

informaPon models. Necessity to introduce single rule book based on regulaPon (not only

direcPve)

Global best prac/ces

Report 27

---------------------------------------------------------------------------------------------------------------------------------------------------------------- To

be replaced

by Single ru

le boo

k un

der

CRD

IV/CRR

– ITS!!!

GOAL OF CRR/SINGLE RULES BOOK (OWN FUNDS PERSPECTIVE)

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

Quality

• Must absorb losses (separately for going-‐ and gone-‐concern) • Strict criteria depending on ability to absorb losses (not just a type of instrument, elimina/on of Tier 3, reduc/on of Tier 2)

• Regulatory adjustments

Consistency

• Simple defini/ons/criteria harmonized between countries

• Regula/on is binding in its en/rety and directly applicable in all Member States

Transparency

• Clear rela/on to financial reports • Comparison between jurisdic/ons

THE FRAMEWORKS

COREP FINREP

Capital Adequacy Group Solvency

Credit Risk IP Losses

Opera/onal Risk Market Risk

Large Exposures

Primary Statements Assets & Liabili/es

Financial Asset Disclosures & Off Balance Sheet

Income & Equity Financial & Non-‐Financial Disclosures, OBS Leverage

Liquidity Coverage Net Stable Funding

Asset Encumbrance

Forbearance Non-‐performance

...

...

...

...

Source: Owen Jones EBA EuroFiling, London, 19 June 2013

MODULES

Source: Owen Jones EBA, Eurofiling, London

COREP FINREP

Capital Adequacy Group Solvency

Credit Risk Opera/onal Risk Market Risk

Leverage Ra/o Liquidity Coverage Net Stable Funding

Ra/o

Large Exposures

Part 1 Part 2 Part 3 Part 4 Part 5

COREP LE

COREP FINREP

2) TECHNICAL BRIEFING

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

TECHNICAL BRIEFING

UNDERSTAND …

" Templates " DPM

" Taxonomies

" Validation

" Rendering … AND THEIR ROLES IN PRODUCING XBRL FILINGS

ITS

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

OVERVIEW OF THE COMPONENTS

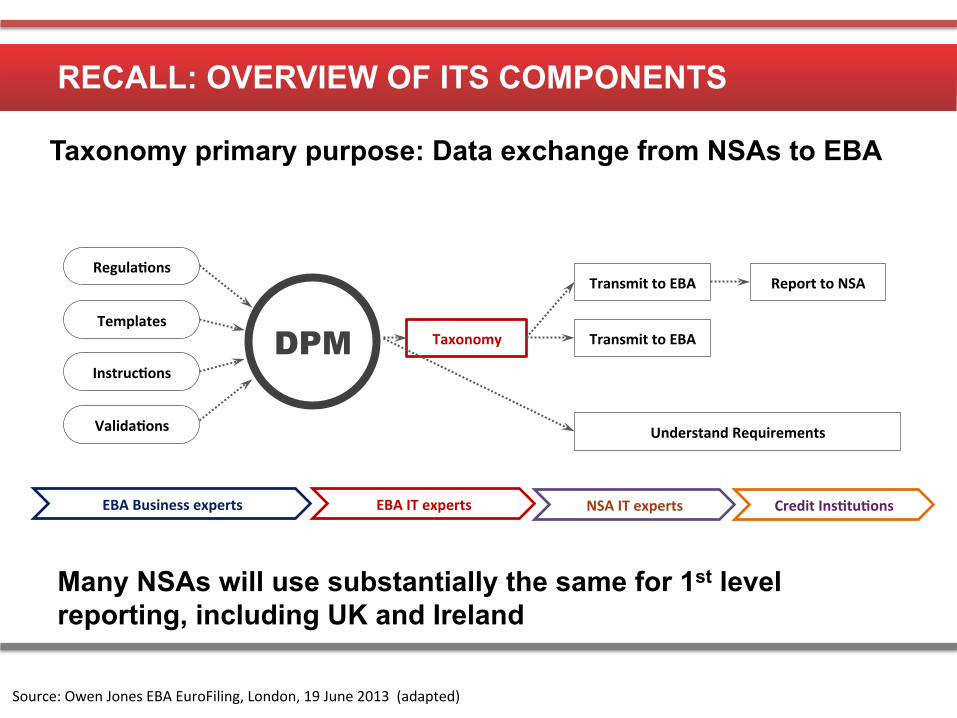

DPM

EBA Business experts EBA IT experts

RegulaPons

Templates

InstrucPons

ValidaPons

Taxonomy

NSA IT experts

Transmit to EBA

Transmit to EBA

Understand Requirements

Credit InsPtuPons

Report to NSA

Taxonomy primary purpose: Data exchange from NSAs to EBA

Many NSAs will use substantially the same for 1st level reporting, including UK and Ireland

Source: Owen Jones EBA EuroFiling, London, 19 June 2013 (adapted)

HOW TO NAVIGATE THE TEMPLATES

§ Data is collected in Excel template § Templates vs Tables

§ Simple (2-D)

§ Complex (nested headers, fixed sheets (Z-axes), open tables and open sheets )

HOW TO UNDERSTAND THE DPM

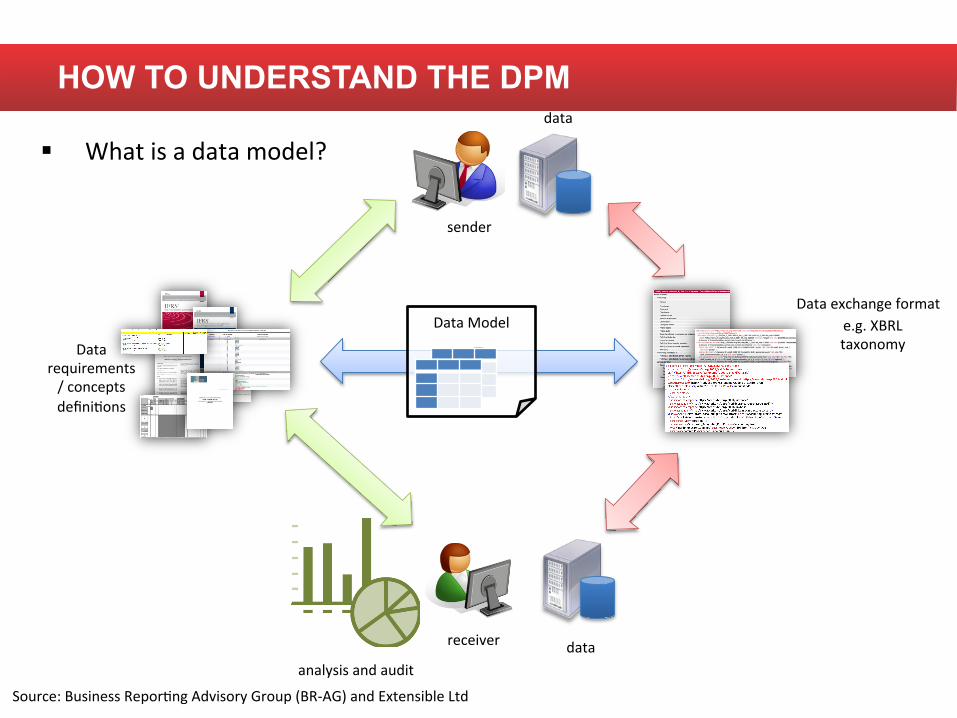

§ What is a data model?

receiver

analysis and audit data

Data requirements / concepts defini/ons

sender

Data exchange format

? Data Model e.g. XBRL

taxonomy

data

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

What is the difference between form and data centric defini/on of a data model?

"form centric" based on presenta/on that expresses meaning (interpreta/on in certain contexts)

"data centric" explicit defini/on irrespec/ve of

presenta/on (every term fully understood by its own with all proper/es included in

defini/on)

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

HOW XBRL AND TAXONOMIES ARE USED

What is ?

communica/on (encoding and decoding) of informa/on:

sentences build according to certain syntax (grammar) and seman/cs (meaning)

informa/ve repor/ng: exchange of

aggregated data for analysis and decision making

a flexible framework: allows for customiza/on and applica/on in different repor/ng

scenarios independent from legal regula/ons

designed for descrip/on and exchange of

business related data (includes all

required characteris/cs and func/onali/es for this applica/on)

20

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

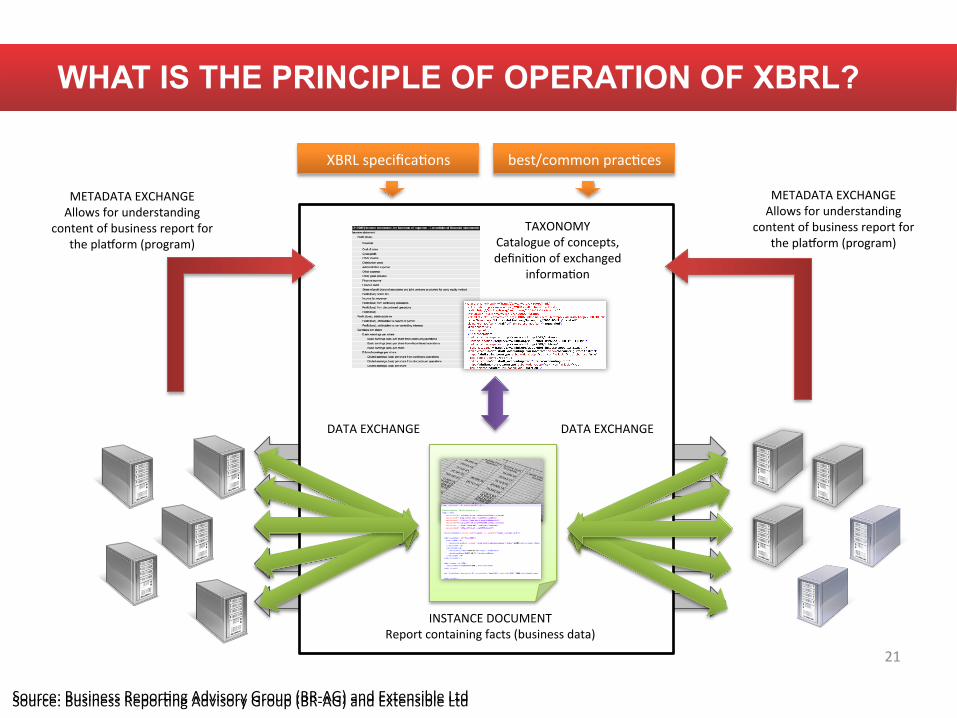

WHAT IS THE PRINCIPLE OF OPERATION OF XBRL?

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

TAXONOMY Catalogue of concepts, defini/on of exchanged

informa/on

INSTANCE DOCUMENT Report containing facts (business data)

XBRL specifica/ons best/common prac/ces

METADATA EXCHANGE Allows for understanding

content of business report for the pladorm (program)

DATA EXCHANGE DATA EXCHANGE

METADATA EXCHANGE Allows for understanding

content of business report for the pladorm (program)

21

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

WHAT GOES WHERE IN XBRL?

a business term (financial

concept) and all its proper/es

en/ty

value

unit

XBRL Taxonomy XBRL Instance

context

22 Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

EBA XBRL TAXONOMY: CONTENTS OF EACH MODULE

Source: Owen Jones EBA EuroFiling, London, 19 June 2013

COREP FINREP

51 Templates 81 Tables

669 Valida/ons

Expected file size 30-‐100MB

2 Templates 2 Tables

13 Valida/ons

Expected file size 1-‐100MB+

68 Templates 77 Tables

658 Valida/ons

Expected file size 5-‐10MB

COREP LE

COREP FINREP

EBA XBRL TAXONOMY: CHARACTERISTICS

§ “Very dimensional” • 286 Primary Items • 101 Dimensions, 1500

members • 43 of 32000 data points

use only 1 dimension, none use 0

• Large 1800 files, 100 MB

Source: Owen Jones EBA EuroFiling, London, 19 June 2013 (adapted)

WHAT IS THE LINK BETWEEN DATA MODEL AND TAXONOMY?

25

Data Model XBRL Taxonomy

Business Experts

Mapping document

IT Experts

95%

tools and processes

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

HOW TO VALIDATE FILINGS

§ XML and XBRL validations

§ Business Rules

§ Formula Linkbase

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

COREP CA TEMPLATE VALIDATION RULE EXAMPLE

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

graphical representa/on

error documenta/on/message

expression in form of DPM proper/es

HOW TO VISUALISE THE XBRL

§ XBRL instances contain embedded relational information

§ Data and Tags can be viewed i) using Table Linkbase

ii) through an XBRL viewer

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

COREP CA TEMPLATE “RENDERING” EXAMPLE

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

tabular view DPM proper/es

rendering nodes

RECALL: OVERVIEW OF ITS COMPONENTS

DPM

EBA Business experts EBA IT experts

RegulaPons

Templates

InstrucPons

ValidaPons

Taxonomy

NSA IT experts

Transmit to EBA

Transmit to EBA

Understand Requirements

Credit InsPtuPons

Report to NSA

Taxonomy primary purpose: Data exchange from NSAs to EBA

Many NSAs will use substantially the same for 1st level reporting, including UK and Ireland

Source: Owen Jones EBA EuroFiling, London, 19 June 2013 (adapted)

HOW TO PREPARE XBRL FILINGS

ERP REPORT WRITER

Portal

ERP

1. Receiver provides XBRL enabled excel, word, PDF templates

2. Outsourcing (printer, consultant, vendor to prepare reports )

3. Bolt-‐on (tools to transform your reports into XBRL at the last stage )

4. Integrate (build XBRL into company’s business repor/ng supply chain)

Portal

Portal

Portal

Benefits Challenges

• no implementa/on costs • need for manual work (rekeying data)

• error prone • no benefit outside of this

par/cular repor/ng context?

• comprehensive support • low risk • no knowledge required

• lack of control • possibly high cost • lack of internal capabili/es

• simplified approach • poten/al cost-‐saving • control over result

• comprehensive approach • cost-‐saving (mid-‐long) • control over result • automated processing • enhanced repor/ng • high data quality

• upfront investment • level of complica/on

• knowledge required • /me risk • significant effort for change

update

31 Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

3) CHALLENGES

CHALLENGES

§ Aggressive Timelines

§ Changing Regulations

§ Data Quality

§ Immature Technologies

§ Readability” and Visualisation

§ “Volume, Size, Complexity

§ Availability and Performance of Tools

§ Data Collection and Integration

§ Taxonomy Maintenance

§ Error messaging

Filer concerns

EBA concerns

Other concerns

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd

“Possible Concerns”: EBA

§ “Extensive use of Table Linkbase

§ Specification is still fluid

§ Implementations are currently “patchy”

§ The taxonomy being reviewed is based on the previous PWD

§ Volume of data, size of instance files, complexity of tables

§ Performance of tools

§ Availability of tools suitable for the reporting process

§ Manual entry / tagging will not be plausible

§ Integration with accounting / risk management / regulatory reporting

systems needed”

Source: Owen Jones EBA EuroFiling, London, 19 June 2013 (adapted)

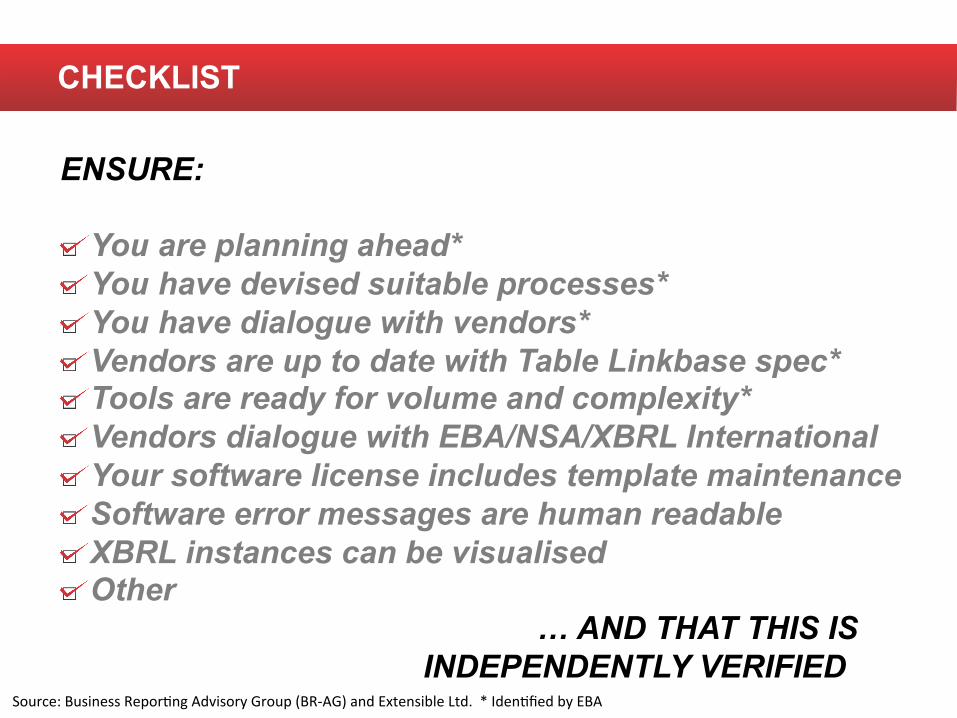

CHECKLIST

ENSURE: " You are planning ahead* " You have devised suitable processes* " You have dialogue with vendors* " Vendors are up to date with Table Linkbase spec* " Tools are ready for volume and complexity* " Vendors dialogue with EBA/NSA/XBRL International " Your software license includes template maintenance " Software error messages are human readable " XBRL instances can be visualised " Other

… AND THAT THIS IS INDEPENDENTLY VERIFIED

Source: Business Repor/ng Advisory Group (BR-‐AG) and Extensible Ltd. * Iden/fied by EBA

ConsulPng • Readiness

Assessments/ Requirements gathering

• Implementa/on • User training

Tools • Sosware solu/on • Pre-‐mapped templates + Maintenance

TesPng • Use cases • Issues Reports • Analysis

SOLUTIONS AND SERVICES

Contact Details

Max Gerrard 0207 036 2910

6 7 -‐ 7 0 C h a r l ode Ro ad , L o ndon E C 2A 3 P E

Ma x . g e r r a r d@a r k k s o l uPon s . c om

www.arkksoluPons.com