copyright © 2007 institute for divorce financial analysts dollars and sense of divorce what...

TRANSCRIPT

Copyright © 2007 Institute for Divorce Financial Analysts

Dollars and Sense

of DivorceWhat financial advisors need to know.

Presenter: Diana Shepherd, CDFA™

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

SOME STATISTICS

Effect of no-fault divorce (1985) 35% of first marriages and 41% of second

marriages end in divorce More than half of all common-law unions

break down within five years 70,000+ divorces granted annually in Canada The divorce rate for Canada is 38.3 per 100

marriages Quebec has the highest divorce rate in Canada: 49.7 Newfoundland and Labrador has the lowest rate: 17.1

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Three Sources of Money in Divorce

Family Property Spousal Support Child Support

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Family Property

• Each party to a marriage is entitled to 50% of the value of property gained during the time of the marriage

• This is not the same as 50% of each asset acquired during the marriage

Although it is ultimately up to the lawyer to advise on property rights, as a financial planner, you should be aware that:

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Spousal Support

• Taxable to the receiving spouse

• Tax deductible to the paying spouse

• Generally calculated on the difference between the two spouses’ income

• No specific rules. However, there are Spousal Support guidelines that many lawyers and judges use.

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Child Support

• Neither taxable nor tax deductible• Based on which parent has custody for

60% or more of the time• Offset against each spouse’s income• There are strict tables that outline the

amounts payable• Covers food, clothing, and shelter

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Child Support (Continued)

• The amount of support does not cover “Section 7 expenses”: extra expenses for the child that are usually covered by percentage of income

• Support is paid until the child is no longer in school (including a first undergraduate degree)

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Family Property

• Ownership• Division

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Matrimonial Home

Other Assets

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

FAMILY PROPERTY

1. Liquid assets

2. Real Estate

3. Businesses

4. Furniture

5. Collections etc.

6. Pensions

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

DIVIDE PROPERTY

1. 50/50 if owned or used2. Exceptions3. Marriage Contract

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

SPOUSAL SUPPORT

• Long marriage – look at comparable lifestyle

• Priority given to child support

• Periodic vs. lump-sum payments

• Third-party payments

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

RETIREMENT ACCOUNTS

• RRSPs• Canada Pension Plan• Old Age Security• Company Pension

(private pension)

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

RRSP ROLLOVER

• Only allowed if there is a divorce and a divorce decree or separation agreement

• Funds are transferred directly from one plan to another

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

CPP (Canada Pension Plan)

Can be divided Credit Splitting

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

OAS (Old Age Pension)

Benefit starts over age 65 Must be Canadian citizen Must apply for benefit

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

PRIVATE PENSIONS

“If and When” approach

Lump-sum payment

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

LUMP-SUM METHOD

Present Value List in assets Discount Rate Tax Liability

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Pensions• Need for valuation• Federal vs.

Provincial• Age • Income stream• Asset

• Where do you as an advisor fit into this picture?

• How can you help clients understand the value of an asset?

Copyright © 2007 Institute for Divorce Financial Analysts

Helping clients understand their financial reality – today and in the future

Making an informed financial settlement helps the client move on to

the next phase of his/her life

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Kate and Kenneth

• Kate is 46 years old

• Kenneth is 52 years old

• Married 18 years

• Two sons: ages 11 and 7

• Kate’s take-home pay is $21,600

• Kenneth’s take-home pay is $132,000

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Kate and Kenneth

• Home equity $180,000

• Mutual Funds $ 92,000

• RRSPs $212,000• Business $180,000

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

KATE

Home equity $180,000

1/2 Mutual Funds $ 46,000

1/2 RRSPs $106,000

Total $332,000

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

KENNETH

1/2 Mutual Funds $ 46,000

1/2 RRSPs $106,000

Business $180,000

Total $332,000

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Kenneth’s Offer to Kate

50% of the assets$1,000/month child support$1,500/month spousal

support for five years

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

K E N N E T H

A g e N e t S a l a r y C P P S p o u s a l C h i l d E x p e n s e s T a x L i a b i l i t y C a s h F l o w L i q u i d A s s e t s R R S P B u s i n e s s N e t W o r t h5 2 4 . 0 0 % 2 . 0 0 % 5 y e a r s 1 1 y e a r s 4 . 0 0 % 4 0 % 5 . 5 0 % 7 . 5 0 % 4 . 0 0 %5 2 $ 1 3 2 , 0 0 0 $ 1 8 , 0 0 0 $ 1 2 , 0 0 0 $ 4 2 , 0 0 0 ( $ 7 , 2 0 0 ) $ 6 7 , 2 0 0 $ 4 6 , 0 0 0 $ 1 0 6 , 0 0 0 $ 1 8 0 , 0 0 0 $ 3 3 2 , 0 0 05 3 $ 1 3 7 , 2 8 0 $ 1 8 , 0 0 0 $ 1 2 , 0 0 0 $ 4 3 , 6 8 0 ( $ 7 , 2 0 0 ) $ 7 0 , 8 0 0 $ 1 1 5 , 7 3 0 $ 1 2 5 , 9 5 0 $ 1 8 7 , 2 0 0 $ 4 2 8 , 8 8 05 4 $ 1 4 2 , 7 7 1 $ 1 8 , 0 0 0 $ 1 2 , 0 0 0 $ 4 5 , 4 2 7 ( $ 7 , 2 0 0 ) $ 7 4 , 5 4 4 $ 1 9 2 , 8 9 5 $ 1 4 7 , 3 9 6 $ 1 9 4 , 6 8 8 $ 5 3 4 , 9 7 95 5 $ 1 4 8 , 4 8 2 $ 1 8 , 0 0 0 $ 1 2 , 0 0 0 $ 4 7 , 2 4 4 ( $ 7 , 2 0 0 ) $ 7 8 , 4 3 8 $ 2 7 8 , 0 4 8 $ 1 7 0 , 4 5 1 $ 2 0 2 , 4 7 6 $ 6 5 0 , 9 7 55 6 $ 1 5 4 , 4 2 1 $ 1 8 , 0 0 0 $ 1 2 , 0 0 0 $ 4 9 , 1 3 4 ( $ 7 , 2 0 0 ) $ 8 2 , 4 8 7 $ 3 7 1 , 7 7 9 $ 1 9 5 , 2 3 5 $ 2 1 0 , 5 7 5 $ 7 7 7 , 5 8 85 7 $ 1 6 0 , 5 9 8 $ 1 2 , 0 0 0 $ 5 1 , 0 9 9 $ 9 7 , 4 9 9 $ 4 7 4 , 7 1 4 $ 2 2 1 , 8 7 7 $ 2 1 8 , 9 9 8 $ 9 1 5 , 5 8 95 8 $ 1 6 7 , 0 2 2 $ 1 2 , 0 0 0 $ 5 3 , 1 4 3 $ 1 0 1 , 8 7 9 $ 5 9 8 , 3 2 2 $ 2 5 0 , 5 1 8 $ 2 2 7 , 7 5 7 $ 1 , 0 7 6 , 5 9 85 9 $ 1 7 3 , 7 0 3 $ 9 , 0 0 0 $ 5 5 , 2 6 9 $ 1 0 9 , 4 3 4 $ 7 3 3 , 1 0 8 $ 2 8 1 , 3 0 7 $ 2 3 6 , 8 6 8 $ 1 , 2 5 1 , 2 8 36 0 $ 1 8 0 , 6 5 1 $ 9 , 0 0 0 $ 5 7 , 4 8 0 $ 1 1 4 , 1 7 1 $ 8 8 2 , 8 6 3 $ 3 1 4 , 4 0 5 $ 2 4 6 , 3 4 2 $ 1 , 4 4 3 , 6 1 16 1 $ 1 8 7 , 8 7 7 $ 9 , 0 0 0 $ 5 9 , 7 7 9 $ 1 1 9 , 0 9 8 $ 1 , 0 4 5 , 5 9 2 $ 3 4 9 , 9 8 5 $ 2 5 6 , 1 9 6 $ 1 , 6 5 1 , 7 7 36 2 $ 1 9 5 , 3 9 2 $ 9 , 0 0 0 $ 6 2 , 1 7 0 $ 1 2 4 , 2 2 2 $ 1 , 2 2 2 , 1 9 7 $ 3 8 8 , 2 3 4 $ 2 6 6 , 4 4 4 $ 1 , 8 7 6 , 8 7 66 3 $ 2 0 3 , 2 0 8 $ 6 4 , 6 5 7 $ 1 3 8 , 5 5 1 $ 1 , 4 1 3 , 6 4 0 $ 4 2 9 , 3 5 2 $ 2 7 7 , 1 0 2 $ 2 , 1 2 0 , 0 9 46 4 $ 2 1 1 , 3 3 6 $ 6 7 , 2 4 3 $ 1 4 4 , 0 9 3 $ 1 , 6 2 9 , 9 4 1 $ 4 7 3 , 5 5 3 $ 2 8 8 , 1 8 6 $ 2 , 3 9 1 , 6 8 16 5 $ 2 1 9 , 7 9 0 $ 6 9 , 9 3 3 $ 1 4 9 , 8 5 7 $ 1 , 8 6 3 , 6 8 1 $ 5 2 1 , 0 7 0 $ 2 9 9 , 7 1 3 $ 2 , 6 8 4 , 4 6 46 6 $ 1 3 , 6 0 0 $ 7 2 , 7 3 0 ( $ 5 9 , 1 3 0 ) $ 2 , 1 1 6 , 0 4 0 $ 5 6 0 , 1 5 0 $ 3 1 1 , 7 0 2 $ 2 , 9 8 7 , 8 9 26 7 $ 1 3 , 8 7 2 $ 7 5 , 6 4 0 ( $ 6 1 , 7 6 8 ) $ 2 , 1 7 3 , 2 9 2 $ 6 0 2 , 1 6 1 $ 3 2 4 , 1 7 0 $ 3 , 0 9 9 , 6 2 36 8 $ 1 4 , 1 4 9 $ 7 8 , 6 6 5 ( $ 6 4 , 5 1 6 ) $ 2 , 2 3 1 , 0 5 5 $ 6 4 7 , 3 2 3 $ 3 3 7 , 1 3 7 $ 3 , 2 1 5 , 5 1 56 9 $ 1 4 , 4 3 2 $ 8 1 , 8 1 2 ( $ 6 7 , 3 7 9 ) $ 2 , 2 8 9 , 2 4 8 $ 6 9 5 , 8 7 3 $ 3 5 0 , 6 2 2 $ 3 , 3 3 5 , 7 4 27 0 $ 1 4 , 7 2 1 $ 8 5 , 0 8 4 ( $ 7 0 , 3 6 3 ) $ 2 , 3 4 7 , 7 7 7 $ 7 4 8 , 0 6 3 $ 3 6 4 , 6 4 7 $ 3 , 4 6 0 , 4 8 77 1 $ 1 5 , 0 1 5 $ 8 8 , 4 8 8 ( $ 7 3 , 4 7 2 ) $ 2 , 4 0 6 , 5 4 1 $ 8 0 4 , 1 6 8 $ 3 7 9 , 2 3 3 $ 3 , 5 8 9 , 9 4 2

P r i n t

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

�

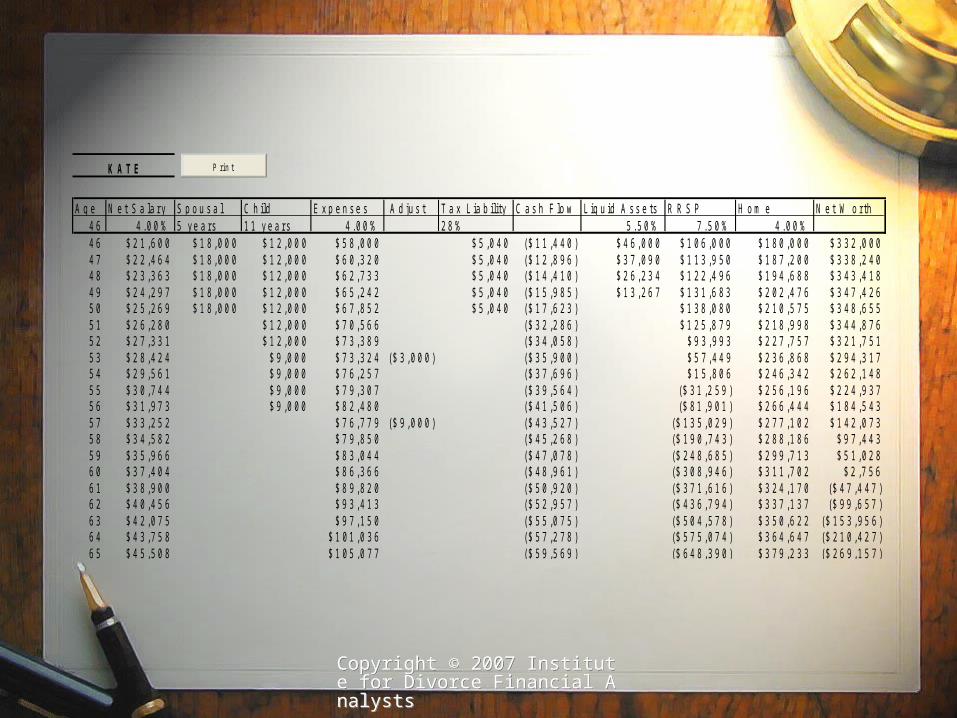

K A T E

A g e N e t S a l a r y S p o u s a l C h i l d E x p e n s e s A d j u s t T a x L i a b i l i t y C a s h F l o w L i q u i d A s s e t s R R S P H o m e N e t W o r t h4 6 4 . 0 0 % 5 y e a r s 1 1 y e a r s 4 . 0 0 % 2 8 % 5 . 5 0 % 7 . 5 0 % 4 . 0 0 %4 6 $ 2 1 , 6 0 0 $ 1 8 , 0 0 0 $ 1 2 , 0 0 0 $ 5 8 , 0 0 0 $ 5 , 0 4 0 ( $ 1 1 , 4 4 0 ) $ 4 6 , 0 0 0 $ 1 0 6 , 0 0 0 $ 1 8 0 , 0 0 0 $ 3 3 2 , 0 0 04 7 $ 2 2 , 4 6 4 $ 1 8 , 0 0 0 $ 1 2 , 0 0 0 $ 6 0 , 3 2 0 $ 5 , 0 4 0 ( $ 1 2 , 8 9 6 ) $ 3 7 , 0 9 0 $ 1 1 3 , 9 5 0 $ 1 8 7 , 2 0 0 $ 3 3 8 , 2 4 04 8 $ 2 3 , 3 6 3 $ 1 8 , 0 0 0 $ 1 2 , 0 0 0 $ 6 2 , 7 3 3 $ 5 , 0 4 0 ( $ 1 4 , 4 1 0 ) $ 2 6 , 2 3 4 $ 1 2 2 , 4 9 6 $ 1 9 4 , 6 8 8 $ 3 4 3 , 4 1 84 9 $ 2 4 , 2 9 7 $ 1 8 , 0 0 0 $ 1 2 , 0 0 0 $ 6 5 , 2 4 2 $ 5 , 0 4 0 ( $ 1 5 , 9 8 5 ) $ 1 3 , 2 6 7 $ 1 3 1 , 6 8 3 $ 2 0 2 , 4 7 6 $ 3 4 7 , 4 2 65 0 $ 2 5 , 2 6 9 $ 1 8 , 0 0 0 $ 1 2 , 0 0 0 $ 6 7 , 8 5 2 $ 5 , 0 4 0 ( $ 1 7 , 6 2 3 ) $ 1 3 8 , 0 8 0 $ 2 1 0 , 5 7 5 $ 3 4 8 , 6 5 55 1 $ 2 6 , 2 8 0 $ 1 2 , 0 0 0 $ 7 0 , 5 6 6 ( $ 3 2 , 2 8 6 ) $ 1 2 5 , 8 7 9 $ 2 1 8 , 9 9 8 $ 3 4 4 , 8 7 65 2 $ 2 7 , 3 3 1 $ 1 2 , 0 0 0 $ 7 3 , 3 8 9 ( $ 3 4 , 0 5 8 ) $ 9 3 , 9 9 3 $ 2 2 7 , 7 5 7 $ 3 2 1 , 7 5 15 3 $ 2 8 , 4 2 4 $ 9 , 0 0 0 $ 7 3 , 3 2 4 ( $ 3 , 0 0 0 ) ( $ 3 5 , 9 0 0 ) $ 5 7 , 4 4 9 $ 2 3 6 , 8 6 8 $ 2 9 4 , 3 1 75 4 $ 2 9 , 5 6 1 $ 9 , 0 0 0 $ 7 6 , 2 5 7 ( $ 3 7 , 6 9 6 ) $ 1 5 , 8 0 6 $ 2 4 6 , 3 4 2 $ 2 6 2 , 1 4 85 5 $ 3 0 , 7 4 4 $ 9 , 0 0 0 $ 7 9 , 3 0 7 ( $ 3 9 , 5 6 4 ) ( $ 3 1 , 2 5 9 ) $ 2 5 6 , 1 9 6 $ 2 2 4 , 9 3 75 6 $ 3 1 , 9 7 3 $ 9 , 0 0 0 $ 8 2 , 4 8 0 ( $ 4 1 , 5 0 6 ) ( $ 8 1 , 9 0 1 ) $ 2 6 6 , 4 4 4 $ 1 8 4 , 5 4 35 7 $ 3 3 , 2 5 2 $ 7 6 , 7 7 9 ( $ 9 , 0 0 0 ) ( $ 4 3 , 5 2 7 ) ( $ 1 3 5 , 0 2 9 ) $ 2 7 7 , 1 0 2 $ 1 4 2 , 0 7 35 8 $ 3 4 , 5 8 2 $ 7 9 , 8 5 0 ( $ 4 5 , 2 6 8 ) ( $ 1 9 0 , 7 4 3 ) $ 2 8 8 , 1 8 6 $ 9 7 , 4 4 35 9 $ 3 5 , 9 6 6 $ 8 3 , 0 4 4 ( $ 4 7 , 0 7 8 ) ( $ 2 4 8 , 6 8 5 ) $ 2 9 9 , 7 1 3 $ 5 1 , 0 2 86 0 $ 3 7 , 4 0 4 $ 8 6 , 3 6 6 ( $ 4 8 , 9 6 1 ) ( $ 3 0 8 , 9 4 6 ) $ 3 1 1 , 7 0 2 $ 2 , 7 5 66 1 $ 3 8 , 9 0 0 $ 8 9 , 8 2 0 ( $ 5 0 , 9 2 0 ) ( $ 3 7 1 , 6 1 6 ) $ 3 2 4 , 1 7 0 ( $ 4 7 , 4 4 7 )6 2 $ 4 0 , 4 5 6 $ 9 3 , 4 1 3 ( $ 5 2 , 9 5 7 ) ( $ 4 3 6 , 7 9 4 ) $ 3 3 7 , 1 3 7 ( $ 9 9 , 6 5 7 )6 3 $ 4 2 , 0 7 5 $ 9 7 , 1 5 0 ( $ 5 5 , 0 7 5 ) ( $ 5 0 4 , 5 7 8 ) $ 3 5 0 , 6 2 2 ( $ 1 5 3 , 9 5 6 )6 4 $ 4 3 , 7 5 8 $ 1 0 1 , 0 3 6 ( $ 5 7 , 2 7 8 ) ( $ 5 7 5 , 0 7 4 ) $ 3 6 4 , 6 4 7 ( $ 2 1 0 , 4 2 7 )6 5 $ 4 5 , 5 0 8 $ 1 0 5 , 0 7 7 ( $ 5 9 , 5 6 9 ) ( $ 6 4 8 , 3 9 0 ) $ 3 7 9 , 2 3 3 ( $ 2 6 9 , 1 5 7 )

P r i n t

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Kate & Kenneth's Net Worth ChartVersion 1

($200,000)

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$1,800,000

$2,000,000

$2,200,000

$2,400,000

$2,600,000

$2,800,000

$3,000,000

46 48 50 52 54 56 58 60 62 64 66

Kate's Age (years)

Ne

t W

ort

h (

$)

Kate

Kenneth

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Scenario #2

Increase spousal support to $2,500 per month for 10 years

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Kate & Kenneth's Net Worth ChartVersion 2

(vs. Kate's Age)

($200,000)

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$1,800,000

$2,000,000

$2,200,000

$2,400,000

$2,600,000

$2,800,000

$3,000,000

46 48 50 52 54 56 58 60 62 64 66

Kate's Age (years)

Ne

t W

ort

h (

$)

Kate

Kenneth

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Scenario #3

What would it take to equalize net cash flow the first year?

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Scenario #3

• $5,000/month spousal support for five years

• Then $4,000/month for five years

• Then $3,000/month for five years

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Kate & Kenneth's Net Worth ChartVersion 3

($200,000)

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$1,800,000

$2,000,000

$2,200,000

$2,400,000

$2,600,000

$2,800,000

$3,000,000

46 48 50 52 54 56 58 60 62 64 66

Kate's Age (years)

Ne

t W

ort

h (

$)

Kate

Kenneth

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

Helping your clients understand

• By being able to help them see what their financial future looks like if they choose one settlement over another, you are providing a unique and vital service

• Clients who know what their lives will look like post-divorce usually find the process more palatable and less stressful

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

What not to do

• Do not give legal advice!

• Do not recommend settlement options!

• Do not try to value pensions or other assets!

Copyright © 2007 Institute for Divorce Financial AnalystsCopyright © 2007 Institute for Divorce Financial Analysts

What you can do• With specialized knowledge, you can

assist your clients in making informed decisions

• You can advise on tax issues• You can advise on retirement issues• You can work as team member in the

various process of Mediation, Collaborative Divorce, and Arbitration

Copyright © 2007 Institute for Divorce Financial Analysts

QUESTIONS ????

Debbie Hartzman (CFP, CLU, CDFA) is here to help answer your technical questions.