conversion technologies market impact assessment ciwmb board meeting september 22, 2004 susan v....

TRANSCRIPT

CONVERSION TECHNOLOGIES MARKET

IMPACT ASSESSMENT

CIWMB Board Meeting

September 22, 2004

Susan V. CollinsHilton Farnkopf & Hobson, LLC

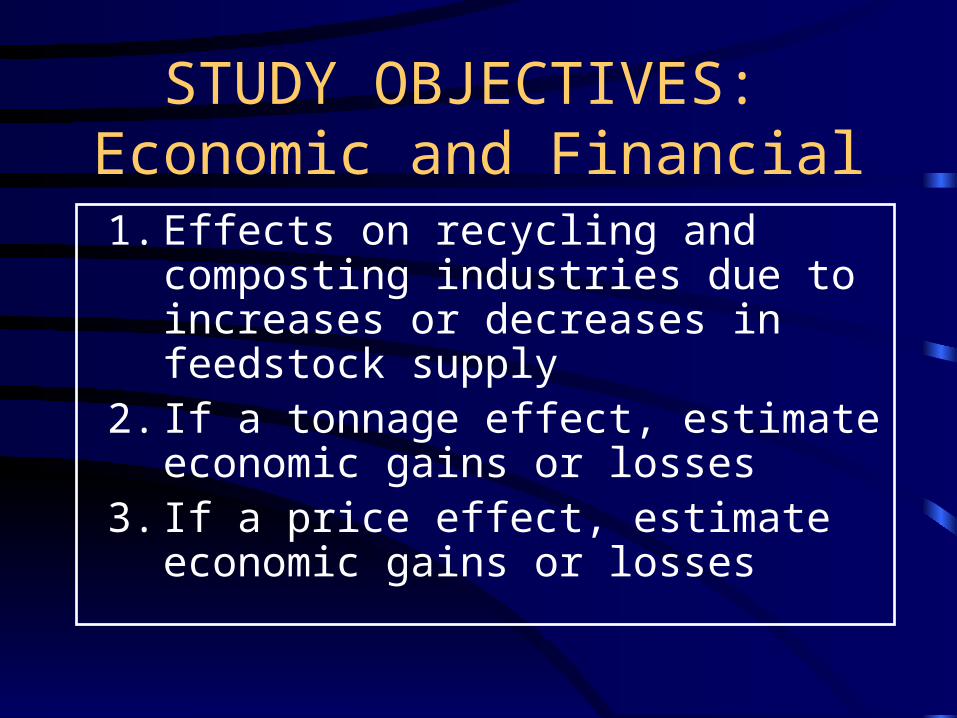

STUDY OBJECTIVES: Economic and Financial

1. Effects on recycling and composting industries due to increases or decreases in feedstock supply

2. If a tonnage effect, estimate economic gains or losses

3. If a price effect, estimate economic gains or losses

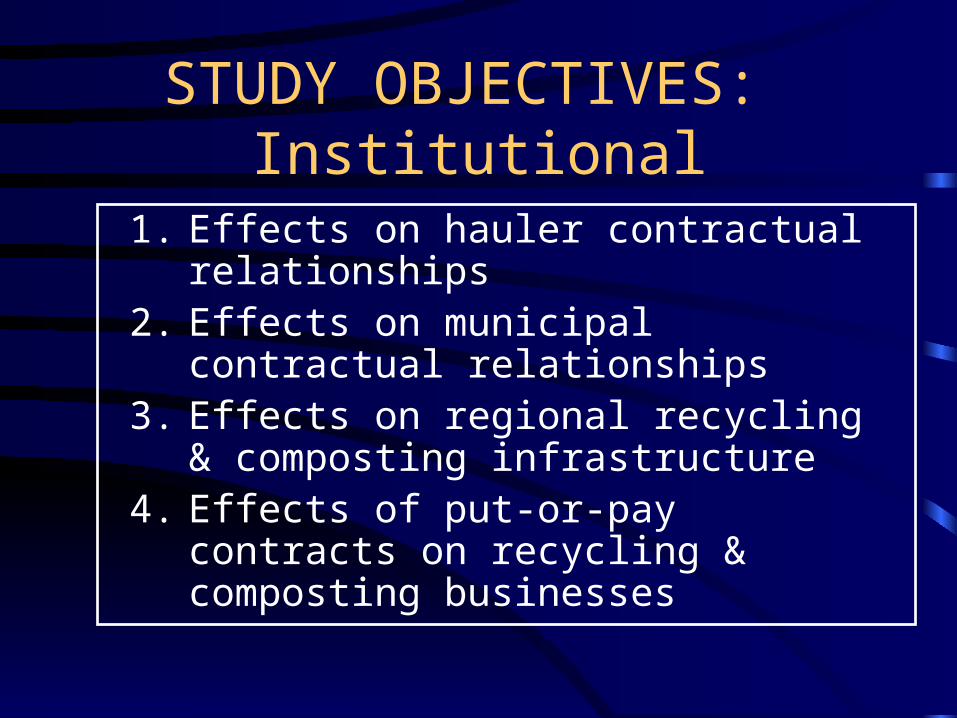

STUDY OBJECTIVES: Institutional

1. Effects on hauler contractual relationships

2. Effects on municipal contractual relationships

3. Effects on regional recycling & composting infrastructure

4. Effects of put-or-pay contracts on recycling & composting businesses

OVERALL APPROACH

• Develop key modeling assumptions

• A financial model was developed to perform calculations

• Develop baseline projections for recycling and composting

• Estimate impacts of CT on recycling and composting

DATA GATHERING: Quantities and Prices

• Waste composition (CIWMB Database)

• Quantities of paper, plastics and organics recycled (in-state and exports)

• Pricing of recyclables, organics and landfill fees

• New diversion program plans

• Jobs and revenues per ton for targeted industries

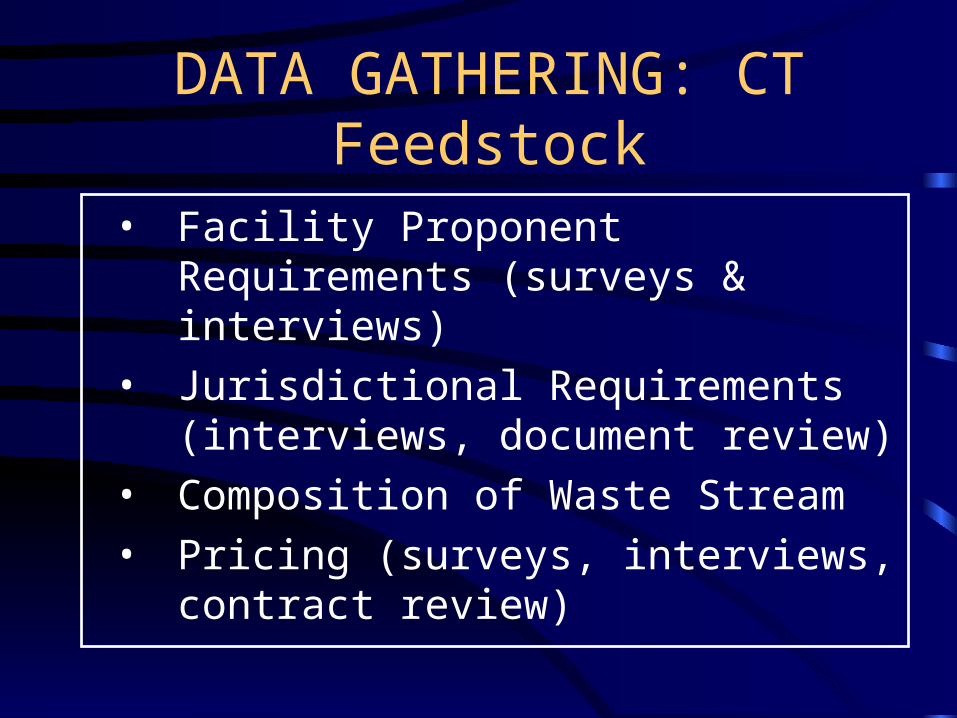

DATA GATHERING: CT Feedstock

• Facility Proponent Requirements (surveys & interviews)

• Jurisdictional Requirements (interviews, document review)

• Composition of Waste Stream

• Pricing (surveys, interviews, contract review)

DATA GATHERING: Institutional Arrangements

• Municipal contracts with haulers• Haulers’ contracts with facilities• Recycling facility contracts• MRF and landfill throughput and

capacity

MARKET FINDINGS IN A NUTSHELL

• Recycling: positive impact • Composting/mulching: neutral

impact• Landfills: negative impact• Details, reasons and other

possibilities to follow….

GENERAL ASSUMPTIONS: Assumed Annual Capacities (tons per year, each region)

2003 2010

Acid Hydrolysis 493, 500 822,500

Gasification 658,000 987,000

Catalytic Cracking 16,450 16,450

TOTAL 1,167,950 1,825,950

Assumed CT Capacities as a Percentage of Landfill Volumes

2003 2010

Greater Los Angeles Area

7% 11%

San Francisco Bay Area

22% 33%

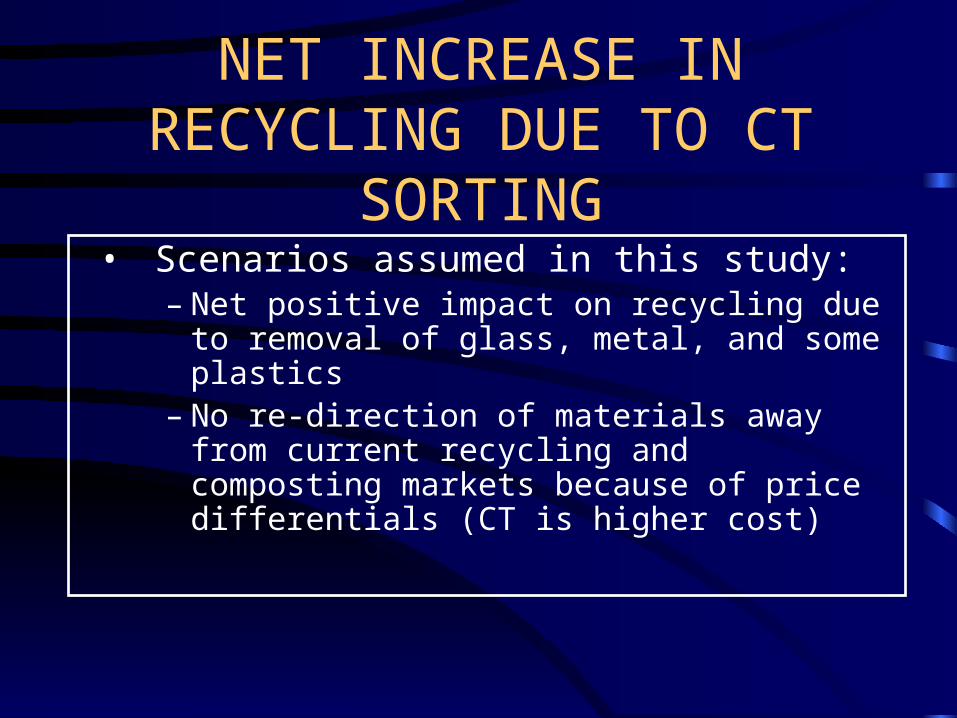

NET INCREASE IN RECYCLING DUE TO CT SORTING

• Scenarios assumed in this study: – Net positive impact on recycling due to

removal of glass, metal, and some plastics– No re-direction of materials away from

current recycling and composting markets because of price differentials (CT is higher cost)

CT PRICING & HISTORY

• No operating facilities in US currently; two in development in 2004 (CA & NY)

• Development costs of $40 to 70 million

• Tipping fees of $25 to $65 per ton

• Specific feedstock requirements with put-or-pay provisions highly likely

WHY WOULDN’T PAPER, PLASTICS AND ORGANICS

MOVE TO CT?

• Paper and plastics markets currently have positive prices; CT facilities expect a tipping fee

• CT prices are competitive with landfill prices, which require no sorting or separate collection

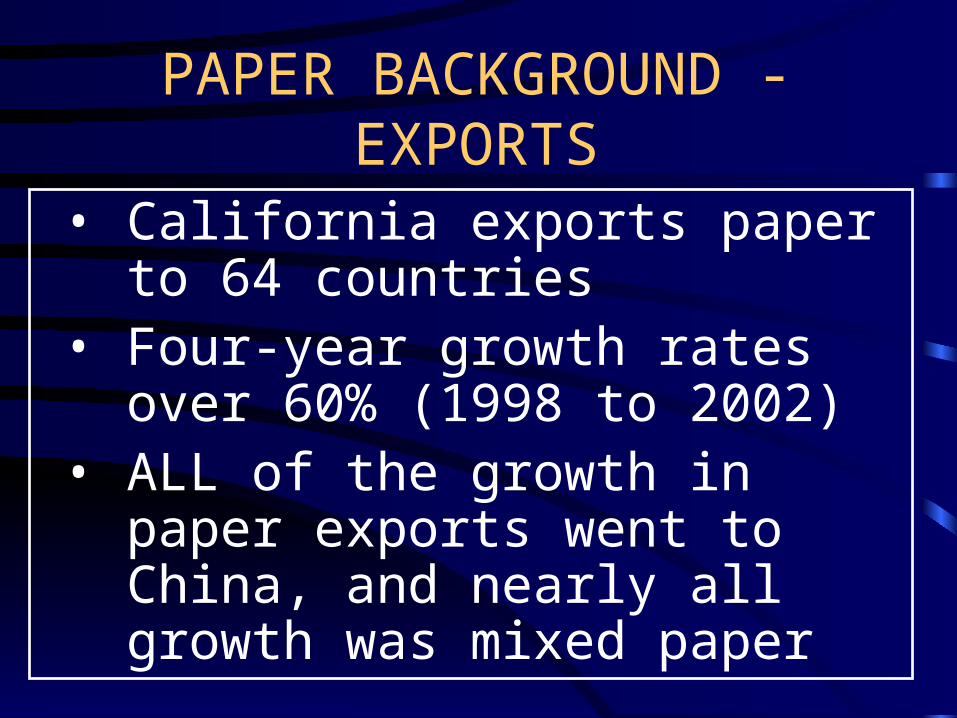

PAPER BACKGROUND - EXPORTS

• California exports paper to 64 countries

• Four-year growth rates over 60% (1998 to 2002)

• ALL of the growth in paper exports went to China, and nearly all growth was mixed paper

GREEN WASTE TO CT: UNLIKELY

• Assuming no diversion credit is given for CT, it is unlikely that green waste will be re-directed to CT facilities

– Jurisdictions will continue to require diversion credit (composting or ADC)

– Contract prices are sometimes significantly lower than gate rates

– Sufficient refuse tonnage exists at higher prices for CT to use refuse as feedstock

GREEN WASTE TO CT: UNLIKELY, 2

• Organics may be re-directed to CT:– If separate collection is changed to co-

collection with refuse for cost savings– If tipping fees are similar to landfills, but

CT facility is closer (cost savings)– If CT offers reduced rates for organics

HOW CT COULD CHANGE INSTITUTIONAL ARRANGEMENTS

• Municipalities can change arrangements if political will and contract flexibility

• Contract haulers can use CT, but need authority to do so for some contracted hauling

• Open Competition and self-haul have most flexibility, but least volume, and least ability to guarantee volumes to a CT operator

MUNICIPALITIES LOOKING AT CT

• City and County of LA, Santa Barbara County, Coachella Valley

• Benefits: alternative energy source, reduced use of landfills, local alternative, increased diversion through sorting

• Want to achieve 50% first

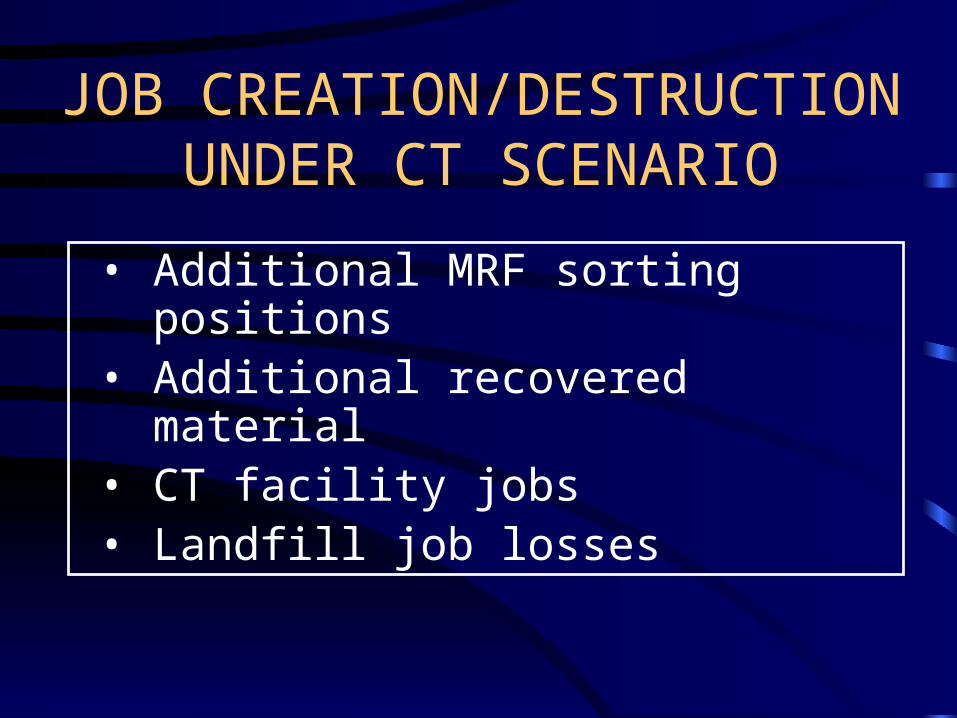

JOB CREATION/DESTRUCTION UNDER CT SCENARIO

• Additional MRF sorting positions • Additional recovered material• CT facility jobs• Landfill job losses

DIVERSION CREDIT ISSUES

1. No credit or up to 10% credit: no dismantling of recycling and green waste programs

2. Full diversion credit: cost savings from dismantling separate recycling and green waste collection

SENSITIVITIES

• No facilities operating in U.S.; some assumptions based on operating information from facility proponents or independent estimates

• Market conditions can change quickly; results are very sensitive to market condition assumptions

• Assumed current diversion activities would continue

• Number of jobs, revenues per 1,000 tons