consumption and house prices in the great recession: model meets evidence

TRANSCRIPT

Consumption and House Pricesin the Great Recession: Model Meets Evidence

Greg Kaplan

Kurt Mitman

Gianluca Violante

UCLNovember 9, 2016

Three questions

1. What shock(s) drove the boom-bust in ph?

• Credit conditions vs expectations about future growth in ph

2. Why the corresponding boom-bust in C?

• Channels: Collateral vs wealth effects

3. Could a debt-forgiveness policy have cushioned the bust?

• Study large-scale Principal Reduction program

1

Three questions

1. What shock(s) drove the boom-bust in ph?

• Credit conditions vs expectations about future growth in ph

2. Why the corresponding boom-bust in C?

• Channels: Collateral vs wealth effects

3. Could a debt-forgiveness policy have cushioned the bust?

• Study large-scale Principal Reduction program

1

Three questions

1. What shock(s) drove the boom-bust in ph?

• Credit conditions vs expectations about future growth in ph

2. Why the corresponding boom-bust in C?

• Channels: Collateral vs wealth effects

3. Could a debt-forgiveness policy have cushioned the bust?

• Study large-scale Principal Reduction program

1

Methodology

• Model: aggregate shocks move equilibrium ph

• Parameterize: match cross-sectional and lifecycle micro data

• Simulate boom-bust

• Compare against aggregate time-series data

• House prices• Consumption• Rent-price ratio

• Home ownership• Leverage• Foreclosures

• Compare against micro data

• Counterfactuals to address our questions

2

Methodology

• Model: aggregate shocks move equilibrium ph

• Parameterize: match cross-sectional and lifecycle micro data

• Simulate boom-bust

• Compare against aggregate time-series data

• House prices• Consumption• Rent-price ratio

• Home ownership• Leverage• Foreclosures

• Compare against micro data

• Counterfactuals to address our questions

2

Methodology

• Model: aggregate shocks move equilibrium ph

• Parameterize: match cross-sectional and lifecycle micro data

• Simulate boom-bust

• Compare against aggregate time-series data

• House prices• Consumption• Rent-price ratio

• Home ownership• Leverage• Foreclosures

• Compare against micro data

• Counterfactuals to address our questions

2

Methodology

• Model: aggregate shocks move equilibrium ph

• Parameterize: match cross-sectional and lifecycle micro data

• Simulate boom-bust

• Compare against aggregate time-series data

• House prices• Consumption• Rent-price ratio

• Home ownership• Leverage• Foreclosures

• Compare against micro data

• Counterfactuals to address our questions2

Preview of main results

1. Sources of boom-bust in ph and C

• Main driver is beliefs, not change in credit conditions

• Credit conditions important for ownership, leverage andforeclosure

2. Transmission mechanism to household consumption

• Mostly a wealth effect, not collateral effect

3. Effectiveness of mortgage modification program

• Big effect on foreclosures, but negligible impact on ph and C

3

Preview of main results

1. Sources of boom-bust in ph and C

• Main driver is beliefs, not change in credit conditions

• Credit conditions important for ownership, leverage andforeclosure

2. Transmission mechanism to household consumption

• Mostly a wealth effect, not collateral effect

3. Effectiveness of mortgage modification program

• Big effect on foreclosures, but negligible impact on ph and C

3

Preview of main results

1. Sources of boom-bust in ph and C

• Main driver is beliefs, not change in credit conditions

• Credit conditions important for ownership, leverage andforeclosure

2. Transmission mechanism to household consumption

• Mostly a wealth effect, not collateral effect

3. Effectiveness of mortgage modification program

• Big effect on foreclosures, but negligible impact on ph and C

3

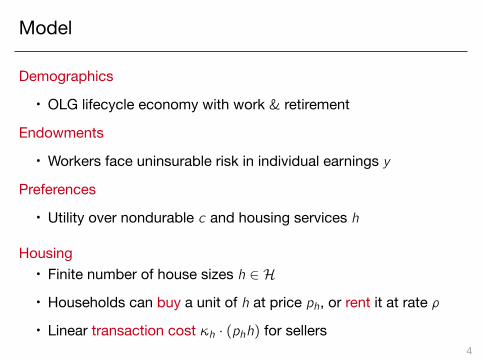

Model

Model

Demographics

• OLG lifecycle economy with work & retirement

Endowments

• Workers face uninsurable risk in individual earnings y

Preferences

• Utility over nondurable c and housing services h

Housing• Finite number of house sizes h ∈ H

• Households can buy a unit of h at price ph, or rent it at rate ρ

• Linear transaction cost κh · (phh) for sellers4

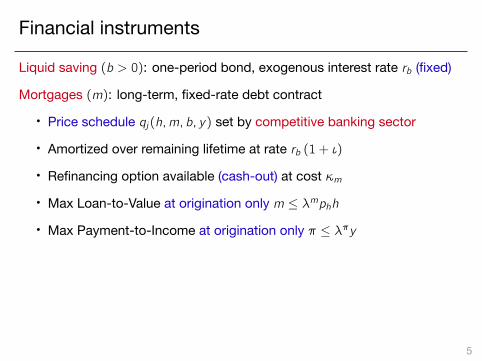

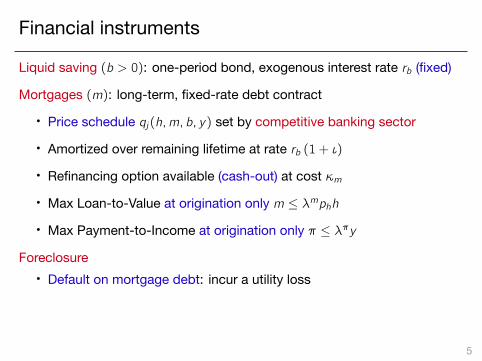

Financial instruments

Liquid saving (b > 0): one-period bond, exogenous interest rate rb (fixed)

Mortgages (m): long-term, fixed-rate debt contract

• Price schedule qj(h,m, b, y) set by competitive banking sector

• Amortized over remaining lifetime at rate rb (1 + ι)

• Refinancing option available (cash-out) at cost κm

• Max Loan-to-Value at origination only m ≤ λmphh

• Max Payment-to-Income at origination only π ≤ λπy

Foreclosure• Default on mortgage debt: incur a utility loss

HELOCs (b < 0)

• One-period borrowing (b ≥ −λbphh), at rate rb (1 + ι), non-defaultable

• Collateralized by housing, b ≥ −λbphh

5

Financial instruments

Liquid saving (b > 0): one-period bond, exogenous interest rate rb (fixed)

Mortgages (m): long-term, fixed-rate debt contract

• Price schedule qj(h,m, b, y) set by competitive banking sector

• Amortized over remaining lifetime at rate rb (1 + ι)

• Refinancing option available (cash-out) at cost κm

• Max Loan-to-Value at origination only m ≤ λmphh

• Max Payment-to-Income at origination only π ≤ λπy

Foreclosure• Default on mortgage debt: incur a utility loss

HELOCs (b < 0)

• One-period borrowing (b ≥ −λbphh), at rate rb (1 + ι), non-defaultable

• Collateralized by housing, b ≥ −λbphh

5

Financial instruments

Liquid saving (b > 0): one-period bond, exogenous interest rate rb (fixed)

Mortgages (m): long-term, fixed-rate debt contract

• Price schedule qj(h,m, b, y) set by competitive banking sector

• Amortized over remaining lifetime at rate rb (1 + ι)

• Refinancing option available (cash-out) at cost κm

• Max Loan-to-Value at origination only m ≤ λmphh

• Max Payment-to-Income at origination only π ≤ λπy

Foreclosure• Default on mortgage debt: incur a utility loss

HELOCs (b < 0)

• One-period borrowing (b ≥ −λbphh), at rate rb (1 + ι), non-defaultable

• Collateralized by housing, b ≥ −λbphh

5

Financial instruments

Liquid saving (b > 0): one-period bond, exogenous interest rate rb (fixed)

Mortgages (m): long-term, fixed-rate debt contract

• Price schedule qj(h,m, b, y) set by competitive banking sector

• Amortized over remaining lifetime at rate rb (1 + ι)

• Refinancing option available (cash-out) at cost κm

• Max Loan-to-Value at origination only m ≤ λmphh

• Max Payment-to-Income at origination only π ≤ λπy

Foreclosure• Default on mortgage debt: incur a utility loss

HELOCs (b < 0)

• One-period borrowing (b ≥ −λbphh), at rate rb (1 + ι), non-defaultable

• Collateralized by housing, b ≥ −λbphh

5

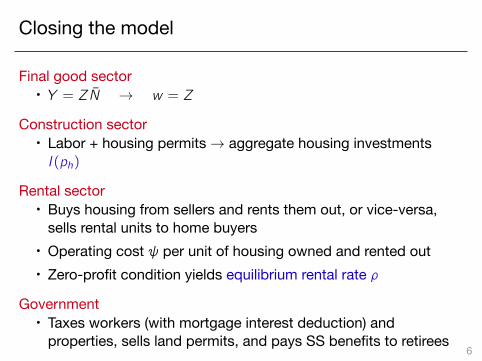

Closing the model

Final good sector• Y = ZN̄ → w = Z

Construction sector• Labor + housing permits→ aggregate housing investmentsI(ph)

Rental sector• Buys housing from sellers and rents them out, or vice-versa,

sells rental units to home buyers• Operating cost ψ per unit of housing owned and rented out• Zero-profit condition yields equilibrium rental rate ρ

Government• Taxes workers (with mortgage interest deduction) and

properties, sells land permits, and pays SS benefits to retirees6

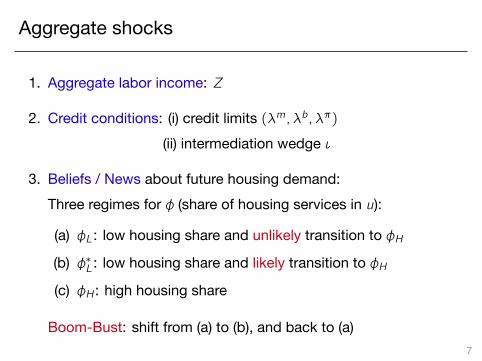

Aggregate shocks

1. Aggregate labor income: Z

2. Credit conditions: (i) credit limits (λm, λb, λπ)(ii) intermediation wedge ι

3. Beliefs / News about future housing demand:Three regimes for ϕ (share of housing services in u):

(a) ϕL: low housing share and unlikely transition to ϕH(b) ϕ∗L: low housing share and likely transition to ϕH(c) ϕH: high housing share

Boom-Bust: shift from (a) to (b), and back to (a)

7

Aggregate shocks

1. Aggregate labor income: Z

2. Credit conditions: (i) credit limits (λm, λb, λπ)(ii) intermediation wedge ι

3. Beliefs / News about future housing demand:Three regimes for ϕ (share of housing services in u):

(a) ϕL: low housing share and unlikely transition to ϕH(b) ϕ∗L: low housing share and likely transition to ϕH(c) ϕH: high housing share

Boom-Bust: shift from (a) to (b), and back to (a)7

Parameterization

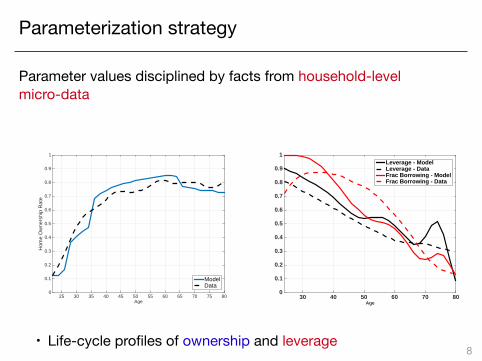

Parameterization strategy

Parameter values disciplined by facts from household-levelmicro-data

Age25 30 35 40 45 50 55 60 65 70 75 80

Hom

e O

wne

rshi

p R

ate

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

ModelData

Age30 40 50 60 70 80

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1Leverage - ModelLeverage - DataFrac Borrowing - ModelFrac Borrowing - Data

• Life-cycle profiles of ownership and leverage8

Parameterization strategy

Parameter values disciplined by facts from household-levelmicro-data

• Distributional stats: mortgages, housing wealth, renters, andconsumption

Moment Empirical value Model ValueFraction homeowners w/ mortgage 0.66 0.57

Aggr. mortgage debt / housing value 0.42 0.36

P10 LTV ratio for mortgagors 0.15 0.14

P50 LTV ratio for mortgagors 0.57 0.59

P90 LTV ratio for mortgagors 0.92 0.92

Aggr. home-ownership rate 0.66 0.67

P10 house value / earnings 0.90 1.0

P50 house value / earnings 2.1 2.0

P90 house value / earnings 5.5 4.5

Avg.-size owned house / rented 1.5 1.4

Avg. earnings owners / renters 2.05 2.02

BPP consumption insurance coef 0.36 0.43 8

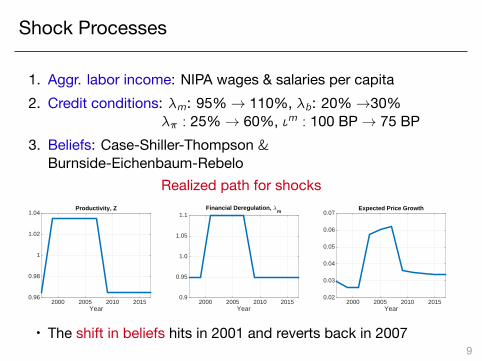

Shock Processes

1. Aggr. labor income: NIPA wages & salaries per capita2. Credit conditions: λm: 95%→ 110%, λb: 20%→30%

λπ : 25%→ 60%, ιm : 100 BP→ 75 BP3. Beliefs: Case-Shiller-Thompson &

Burnside-Eichenbaum-Rebelo

Realized path for shocks

Year2000 2005 2010 2015

0.96

0.98

1

1.02

1.04Productivity, Z

Year2000 2005 2010 2015

0.9

0.95

1.0

1.05

1.1Financial Deregulation, 6

m

Year2000 2005 2010 2015

0.02

0.03

0.04

0.05

0.06

0.07Expected Price Growth

• The shift in beliefs hits in 2001 and reverts back in 2007

9

Shock Processes

1. Aggr. labor income: NIPA wages & salaries per capita2. Credit conditions: λm: 95%→ 110%, λb: 20%→30%

λπ : 25%→ 60%, ιm : 100 BP→ 75 BP3. Beliefs: Case-Shiller-Thompson &

Burnside-Eichenbaum-RebeloRealized path for shocks

Year2000 2005 2010 2015

0.96

0.98

1

1.02

1.04Productivity, Z

Year2000 2005 2010 2015

0.9

0.95

1.0

1.05

1.1Financial Deregulation, 6

m

Year2000 2005 2010 2015

0.02

0.03

0.04

0.05

0.06

0.07Expected Price Growth

• The shift in beliefs hits in 2001 and reverts back in 20079

Q1What caused the boom-bust in ph and C?

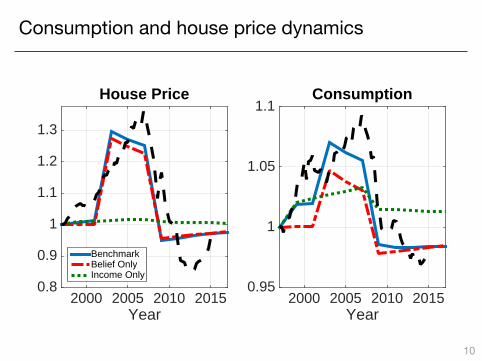

Consumption and house price dynamics

Year2000 2005 2010 2015

0.8

0.9

1

1.1

1.2

1.3

House Price

ModelData

Year2000 2005 2010 2015

0.95

1

1.05

1.1Consumption

10

Consumption and house price dynamics

Year2000 2005 2010 2015

0.8

0.9

1

1.1

1.2

1.3

House Price

BenchmarkBelief Only

Year2000 2005 2010 2015

0.95

1

1.05

1.1Consumption

10

Consumption and house price dynamics

Year2000 2005 2010 2015

0.8

0.9

1

1.1

1.2

1.3

House Price

BenchmarkBelief OnlyIncome Only

Year2000 2005 2010 2015

0.95

1

1.05

1.1Consumption

10

Consumption and house price dynamics

Year2000 2005 2010 2015

0.8

0.9

1

1.1

1.2

1.3

House Price

BenchmarkBelief OnlyIncome OnlyCredit Only

Year2000 2005 2010 2015

0.95

1

1.05

1.1Consumption

10

Beliefs vs actual change in preferences

Year2000 2005 2010 2015

0.8

0.9

1

1.1

1.2

1.3

House Price

BenchmarkDemand Only

Year2000 2005 2010 2015

0.9

0.95

1

1.05

1.1Consumption

• Preference shock: similar rise in ph, but C falls!

11

Beliefs vs actual change in preferences

Year2000 2005 2010 2015

0.8

0.9

1

1.1

1.2

1.3

House Price

BenchmarkDemand Only

Year2000 2005 2010 2015

0.9

0.95

1

1.05

1.1Consumption

• Preference shock: similar rise in ph, but C falls!11

Dynamics of rent-price ratio

Year2000 2005 2010 2015

0.7

0.8

0.9

1

1.1

Benchmark

12

Dynamics of rent-price ratio

Year2000 2005 2010 2015

0.7

0.8

0.9

1

1.1

BenchmarkBelief OnlyIncome OnlyCredit Only

ρ = ψ + ph −(1− δh − τh1 + rb

)Eph

[p′h]

• Belief about future appreciation essential12

Dynamics of home ownership

Year2000 2005 2010 2015

0.95

1

1.05

1.1Benchmark

13

Dynamics of home ownership

Year2000 2005 2010 2015

0.95

1

1.05

1.1BenchmarkBelief OnlyIncome OnlyCredit Only

• Loosening of credit limits drives rise in home-ownership13

Change in home ownership by age: data and model

Age30 40 50 60

Log-

chan

ge (

rela

tive

to m

ean)

-0.05

0

0.05

0.1

0.15Boom

DataModel

Age30 40 50 60

Log-

chan

ge (

rela

tive

to m

ean)

-0.15

-0.1

-0.05

0

0.05Bust

DataModel

• It’s the young who go in/out of housing market14

Dynamics of leverage and foreclosure

Year2000 2005 2010 2015

0.8

1

1.2

1.4

1.6

1.8Leverage

Year2000 2005 2010 2015

0

0.01

0.02

0.03

0.04Foreclosure rate

Benchmark

15

Dynamics of leverage and foreclosure

Year2000 2005 2010 2015

0.8

1

1.2

1.4

1.6

1.8Leverage

Year2000 2005 2010 2015

0

0.01

0.02

0.03

0.04Foreclosure rate

BenchmarkBelief OnlyIncome OnlyCredit Only

• Credit loosening is key for constant leverage pre-boom• Interaction belief-credit important for foreclosure

15

Why credit shock does not affect ph

• Max LTV/PTI ratios affect housing demand if renters (extensivemargin) or home-owners (intensive margin) are constrained inhousing choice

1. UP: Rental market relaxes these constraints

2. DOWN: Long-term mortgage debt relaxes these constraints

16

Why credit shock does not affect ph

• Max LTV/PTI ratios affect housing demand if renters (extensivemargin) or home-owners (intensive margin) are constrained inhousing choice

1. UP: Rental market relaxes these constraints

2. DOWN: Long-term mortgage debt relaxes these constraints

• Are we missing the ‘credit supply’ aspect of the shock, i.e.cheap credit flowing to low-quality borrowers?

1. Endogenous relaxation in lending standards in response tobelief-driven boom

16

Cheaper credit for ‘low-quality’ borrowers

Leverage0.7 0.8 0.9 1 1.1

End

ogen

ous

Bor

row

ing

Rat

e (1

/qm

-1)

0.04

0.06

0.08

0.1

0.12

0.14No shocksCredit OnlyAll Shocks

• Also lenders expect prices to rise and default rates to fall17

Model Meets (New) Micro Evidence

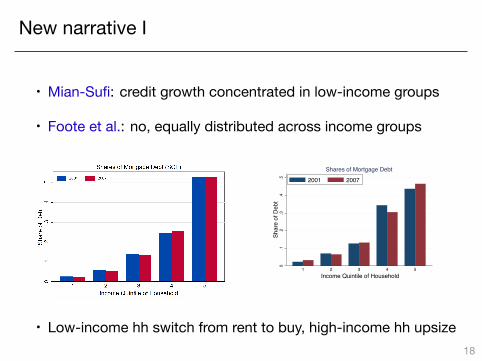

New narrative I

• Mian-Sufi: credit growth concentrated in low-income groups

• Foote et al.: no, equally distributed across income groups

0.1

.2.3

.4.5

Shar

e of

Deb

t

1 2 3 4 5 Income Quintile of Household

Shares of Mortgage Debt

2001 2007

• Low-income hh switch from rent to buy, high-income hh upsize

18

New narrative I

• Mian-Sufi: credit growth concentrated in low-income groups

• Foote et al.: no, equally distributed across income groups

0.1

.2.3

.4.5

Shar

e of

Deb

t1 2 3 4 5

Income Quintile of Household

Shares of Mortgage Debt

2001 2007

• Low-income hh switch from rent to buy, high-income hh upsize18

New narrative II

• Mian-Sufi: mortgage origin. concentrated in subprime groups

• Adelino et al.: no, equally distributed across groups

0.2

.4.6

.8Sh

are

of D

ebt

Above Median Below MedianDefault Risk

Shares of Originated Mortgage Debt2001 2007

• Young hh switch from rent to buy, older hh upsize

19

New narrative II

• Mian-Sufi: mortgage origin. concentrated in subprime groups

• Adelino et al.: no, equally distributed across groups

0.2

.4.6

.8Sh

are

of D

ebt

Above Median Below MedianDefault Risk

Shares of Originated Mortgage Debt2001 2007

• Young hh switch from rent to buy, older hh upsize19

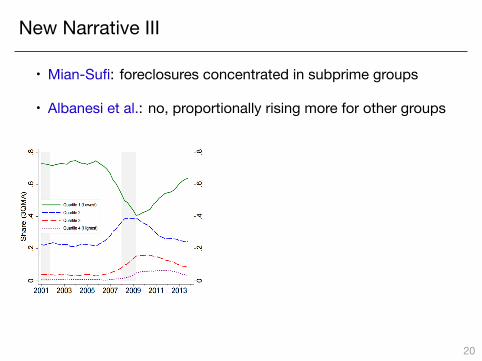

New Narrative III

• Mian-Sufi: foreclosures concentrated in subprime groups

• Albanesi et al.: no, proportionally rising more for other groups

0.2

.4.6

.81

Shar

e of

For

eclo

sure

s

2004 2006 2008 2010 2012Year

IncomeQuintile=1 IncomeQuintile=2 IncomeQuintile=3 IncomeQuintile=4 IncomeQuintile=5

• Everyone levers up, including middle-income households

20

New Narrative III

• Mian-Sufi: foreclosures concentrated in subprime groups

• Albanesi et al.: no, proportionally rising more for other groups

0.2

.4.6

.81

Shar

e of

For

eclo

sure

s2004 2006 2008 2010 2012

Year

IncomeQuintile=1 IncomeQuintile=2 IncomeQuintile=3 IncomeQuintile=4 IncomeQuintile=5

• Everyone levers up, including middle-income households20

Q2How does the fall in ph transmit to C?

Deleveraging or wealth effect in the bust?-.3

-.2-.1

0.1

Chan

ge in

Log

Con

sum

ptio

n

0 .05 .1 .15Debt as a Fraction of Total Wealth

Renters Owners

-.3-.2

-.10

.1Ch

ange

in L

og C

onsu

mpt

ion

0 .1 .2 .3 .4Housing Share of Total Wealth

Renters Owners

Deleveraging: WEAK Wealth effect: STRONG

• Consistent with Kaplan-Mitman-Violante (2016): ’Non-durableConsumption and Housing Net Worth in the Great Recession:Evidence form Easily Accessible Data’

21

Deleveraging or wealth effect in the bust?-.3

-.2-.1

0.1

Chan

ge in

Log

Con

sum

ptio

n

0 .05 .1 .15Debt as a Fraction of Total Wealth

Renters Owners

-.3-.2

-.10

.1Ch

ange

in L

og C

onsu

mpt

ion

0 .1 .2 .3 .4Housing Share of Total Wealth

Renters Owners

Deleveraging: WEAK Wealth effect: STRONG

• Consistent with Kaplan-Mitman-Violante (2016): ’Non-durableConsumption and Housing Net Worth in the Great Recession:Evidence form Easily Accessible Data’

21

Q3Could a massive debt forgiveness program

have cushioned the bust?

Counterfactual principal reduction program

All homeowners with LTV >95%: forgive excess debt

Year2000 2005 2010 2015

0.8

1

1.2

House Price

Bench.Mod.

Year2000 2005 2010 2015

0.95

1

1.05

1.1Consumption

Year2000 2005 2010 2015

0

0.01

0.02

0.03

Foreclosure rate

Year2000 2005 2010 2015

0.8

1

1.2

1.4

1.6

Leverage

• Beneficiaries account for small share of C + do not foreclose

22

Counterfactual principal reduction program

All homeowners with LTV >95%: forgive excess debt

Year2000 2005 2010 2015

0.8

1

1.2

House Price

Bench.Mod.

Year2000 2005 2010 2015

0.95

1

1.05

1.1Consumption

Year2000 2005 2010 2015

0

0.01

0.02

0.03

Foreclosure rate

Year2000 2005 2010 2015

0.8

1

1.2

1.4

1.6

Leverage

• Beneficiaries account for small share of C + do not foreclose22

Summary: what did we learn from the model?

1. Shift in expected house appreciation key to boom-bust in ph

2. This explanation is consistent with recent micro evidence

3. ∆ph transmits to ∆C through wealth effects

4. Principal reduction program would not have mitigated drop in C

Thanks!

23

Summary: what did we learn from the model?

1. Shift in expected house appreciation key to boom-bust in ph

2. This explanation is consistent with recent micro evidence

3. ∆ph transmits to ∆C through wealth effects

4. Principal reduction program would not have mitigated drop in C

Thanks!

23