consultation paper on the review of … 1 of 41 consultation paper on the review of inclining block...

TRANSCRIPT

Page 1 of 41

CONSULTATION PAPER ON THE

REVIEW OF INCLINING BLOCK

TARIFFS FOR ELECTRICITY

DISTRIBUTORS

Published on 21 September 2012

Page 2 of 41

TABLE OF CONTENTS

1. Introduction ............................................................................................................. 4

2. NERSA Mandate ..................................................................................................... 5 3. Background ............................................................................................................. 5 4. Review of compliance to the EPP ......................................................................... 11 5. Municipal Data: Development of IBTs ................................................................. 13 6. Review of the structure of IBTs ............................................................................ 15

7. Potential Financial Implications of IBT ................................................................ 18 8. Multiple Household Dwellings ............................................................................. 24

9. Issue regarding customers with irregular usage .................................................... 27 10. Issues regarding resellers ...................................................................................... 28 11. Technical Challenges ............................................................................................ 30 12. Alternate Options: Other tariff structures to be considered .................................. 33

13. Seasonally differentiated tariffs to address cash flow issues ................................ 35 14. Impact of price /tariffs signal due to customers implementing EE measures, and

the impact these measures have on the licensees revenues ................................... 37 15. Any Other Comments ........................................................................................... 39 16. Appendix 1 ............................................................................................................. 40

Page 3 of 41

Abbreviations

c/kWh Cent per kilowatt hour

CPI Consumer Price Index

DOE Department of Energy

DPLG Department of Provincial and Local Government

EEDSM Energy Efficiency and Demand Side Management

EPP The South African Electricity Supply Industry: Electricity

Pricing Policy GN 1398 of 19 December 2008

ERA Electricity Regulation Act (Act No. 4 of 2006)

FBE Free Basic Electricity

IBT Inclining Block Tariff

LRAM Long Run Adjustment Mechanism

M&V Measurement & Verification

MYPD Multi Year Price Determination

NERSA National Electricity Regulator of South Africa

TOU Time-of-Use

WACC Weighted Average Cost of Capital

Page 4 of 41

SECTION 1

1. Introduction

The National Energy Regulator of South Africa (NERSA) has embarked on a

consultation process, to review the Inclining Block Tariffs (IBT) for electricity

distributors. This consultation process is in line with the Energy Regulator

decision to consult on the key issues being faced by licensees with regards to

IBT implementation. The aim is to finalise the review by 13 December 2012. In

this consultation process and prior to the decision, the Energy Regulator will

embark on a due process involving stakeholder consultation. As part of this

process, NERSA is requesting stakeholders to comment on the issues raised in

this consultation paper.

NERSA will collate all comments received which will be taken into consideration

when the decision is made. NERSA will also hold a public hearing on 24 October

2012 wherein representations may be made by interested and affected parties.

The timelines for this consultation and decision-making process is outlined in the

table below:

TIMELINES FOR THE REVIEW OF THE INCLINING BLOCK TARIFFS FOR ELECTRICITY DISTRIBUTORS

ACTIVITY/TASK

DATE

Publication of Inclining Block Tariff s

consultation paper on the NERSA

website for stakeholder comments

21 September 2012

Closing Date for stakeholder comments 11 October 2012

Public Hearing1 24 October 2012

Electricity Subcommittee to consider

the Draft Reasons for Decision on the

04 December 2012

1 Details regarding logistics (venue and time) will be communicated in due course

Page 5 of 41

review of the Inclining Block Tariffs

Energy Regulator‟s Decision on the

review of the Inclining Block Tariffs

13 December 2012

Table 1: Timelines for the approval of the review of IBTs

Stakeholders are requested to send their comments on the issues raised in this

document to the email address: [email protected]

2. NERSA Mandate

The National Energy Regulator of South Africa (NERSA) is a regulatory authority

established as a juristic person in Terms of Section 3 of the National Energy

Regulator Act, 2004 (Act No.40 of 2004). NERSA‟s mandate is to regulate the

electricity, piped-gas and petroleum pipelines in terms of the Electricity

Regulation Act, 2006(Act No.4 of 2006), Gas Act, 2001(Act No.48 of 2001)and

the Petroleum Pipelines Act, 2003(Act No.60 of 2003) and the Petroleum

Pipelines Levies Act, 2004 (Act No.28 of 2004)

In terms of Section 4(a)(ii) of the Electricity Regulation Act (Act No.4 of 2006)

“the Regulator must regulate prices and tariffs.”

3. Background

On 25 June 2009, within Eskom‟s interim price increase decision, NERSA

approved for Inclining Block Tariffs to be implemented in MYPD2. The decision of

the Energy Regulator was as follows: The approved price increase on the

average standard tariffs includes a limited price increase of 15% to both Eskom

and municipalities‟ poor customers (i.e. Homelight 1 & 2 tariffs). It must be noted

that this is an interim measure until the implementation of inclining block rate

tariffs for protection of the poor. The full implementation will occur in the Multi-

Year price Determination 2 (MYPD2).

Following the above mentioned decision, NERSA commenced with an

international benchmark study on the design of an Inclining Block Tariff (IBT) for

domestic/ residential customers. This study included utilities and regulators such

Page 6 of 41

as BC Hydro, Nova Scotia Power Incorporated, Royal Thai Government

(Thailand), Georgia Environmental Protection Division and locally in South Africa

within the water sector.

In addition, NERSA held a joint workshop with the six metropolitan municipalities,

Eskom and vending system suppliers to collect their views on a range of matters

from the design of the blocks, one-part tariffs versus two part tariffs, systems

challenges, transition/implementation timelines and other issues.

During the analysis of the MYPD 2 decision, NERSA subsequently also

investigated various other options of providing protection to low-income tariff

customers as proposed by Eskom in the MYPD2 application. The table below

highlights these options:

OPTIONS

REASONS FOR NON-SELECTION

1. Capping Increase to the low income customers: Differentiated Pricing

• This option resulted in major revenue losses to licensees, especially licensees which have a predominantly residential customer base

• It also does not always target the people for whom it is intended

2. Increasing the Free Basic Electricity (FBE) Allocation from 50kWh to 70kWh or even 100 kWh

• The authority responsible for the FBE allocation levels is the DoE together with DPLG and the National Treasury.

• NERSA therefore did not have the mandate and/or authority to enforce this option

3. Introduction of Real Time Pricing

• This would require major system changes with regards to metering with high costs and may even result in much higher prices for low income customers

Table 2: Options Considered for Low Income Customer Protection

Page 7 of 41

Unlike the IBT, none of the options in the table above are provided for in the

Electricity Pricing Policy (EPP), although the FBE is dealt with under separate

provisions of Government‟s social programs. The principle of an IBT is

specifically provided for and supported by the “South African Electricity Supply

Industry: Electricity Pricing Policy GN 1398 of 19 December 2008“ (EPP) which

states that: : “Low income tariff customer subsidization: Charging an appropriate

tariff structure that allows for maximum subsidization at low consumption levels

with gradually reducing cross-subsidies as the consumption levels increase.”

For these reasons the IBT was selected as the most preferred and viable option.

Moreover, during the study on the design and structure of the IBT it was found

that an IBT rate structure would allow the achievement of:

1) protecting low income tariff customers, and;

2) promoting energy efficiency.

3.1 Design Principles of an IBT

The following key design principles were applied by NERSA to develop the

current inclining block rate structure:

the need to ensure stability, simplicity and understandability and

transparency;

the need to utilize appropriate metering and supply technology;

the customers ability to pay;

equity: preserving a degree of cross-subsidies to ensure support to low

income customers;

the requirement to shield low income customers from the impact of

unacceptably high price increases;

the need to ensure revenue neutrality to the utility i.e. the utility should

neither make a profit nor a loss in revenue because of changes in tariff

structures.

Page 8 of 41

In order to keep in line with the design principle that the tariff should be easy and

economical to administer/implement it was decided to limit the IBT to a 4 block

tariff structure.

3.2 Development of an IBT

The table below summarizes the 4 Blocks, consumptions levels, the basis for the

block range used in the development of the IBT during the MYPD2 period for

both Eskom and municipalities:

Blocks Consumption Levels Basis of Block Range

Block 1 1-50 KWh Equal to FBE

Block 2 51-350 KWh Cushion low income large families (and multiple households) that may spill over from Block 1

Block 3 351-600 kWh Presumed average household consumption informed by National Treasury assumption

Block 4 >600kWh Remainder Table 3: Block Design

The next step was to set the residential/ domestic benchmarks based on the

abovementioned IBT design. In order to determine the residential benchmarks,

the baseline point had to be determined. The residential/domestic benchmarks

were determined on the basis as summarized below:

Page 9 of 41

Block Consumption

Levels

2009/10

Baseline Benchmark

per RED Rationale for the

baseline point

Basis of benchmark

increase

Block 1 1-50 kWh Domestic Indigent

To ensure that the increases in this benchmarks category remain within inflation level and provides protection to the low income customers.

Limited to CPI ( as allowed for Eskom)

Block 2 51-350 kWh Domestic Indigent

Maintain the objective of low income customer tariff subsidization for those customers who spill over from first block by retaining same baseline for both block 1 and 2.

CPI + % equal to or less than Eskom Real WACC% allowed

Block 3 351-600 kWh Domestic Low

To ensure that the increases of average consumption households are limited to the average guideline increases

Average (fully distributed) cost

Block 4 >600 kWh Domestic High

Higher end of the residential benchmarks and representative of the marginal cost for additional supply plus a contribution to the subsidy in the lower blocks

Domestic High benchmark plus guideline increase(Long Run Marginal Cost + Residual Revenues)/ contribution to subsidy)

Table 4: Baseline benchmarks and basis of benchmark increases

3.3 The Decision

On 24 February 2010 (as part of the MYPD 2 decision), NERSA approved the

implementation of Inclining Block Tariffs (IBTs) for domestic/ residential

customers, concurrently with the 2010/11 price increase. The IBTs where based

on the aforementioned design principles. The decision was taken in order to

Page 10 of 41

provide for cross-subsidies for low income domestic customers and was

therefore applicable to both Eskom and municipalities.

The application of the above inputs resulted in the following 2011/12 benchmark

energy charges for municipal distributors (i.e. excluding the fixed charges) and

approved rates for Eskom (excluding VAT):

c/kWh Block 1 Block 2 Block 3 Block 4

RED 12 58 - 63 67 - 72 93 - 98 109 - 114

RED 2 58 -63 67 - 72 93 - 98 111 - 116

RED 3 58 -63 67 - 72 93 - 98 109 - 114

RED 4 58 -63 66 - 71 90 - 95 109 - 114

RED 5 58 -63 67 - 72 93 - 98 109 - 114

RED 6 58 -63 66 - 71 90 - 95 109 - 114

Eskom Approved Block Rates

57.65 66.16 96.05 105.35

Table 5: IBT Municipal Benchmarks & Eskom approved rates (2011/12)

2 This refers to the historic Regional Electricity Distribution boundaries.

Page 11 of 41

SECTION 2

After the aforementioned decision by NERSA, Eskom and some municipalities

indicated that they faced various challenges/issues with regards to the

implementation of the IBTs. NERSA therefore has decided to embark on a

stakeholder consultation process in order to provide an opportunity to address

issues raised by electricity distributors and other stakeholders such as the South

African Local Government Association (SALGA) and the Association of Municipal

Electricity Undertakers (AMEU).

This section of the consultation paper therefore sets out the key issues on the

Inclining Block Tariffs as raised by stakeholders. The consultation paper is

structured with each issue being broken down into a discussion on the overview

of the issue, NERSA research and initial views, and questions to stakeholders.

Stakeholders are requested to comment particularly on the questions to

stakeholders. However, comments may not be limited to these questions only.

4. Review of compliance to the EPP

4.1 Overview

In developing the inclining block rate tariffs NERSA ensured that the principles of

developing the IBTs does support the EPP policy principles. NERSA has also

taken into consideration the challenges indicated by licensees and is willing to

embark on a consultation process to this regard.

Stakeholders have indicated that NERSA had not taken into consideration some

of the policy positions identified in the EPP when developing the IBTs.

A list of the key policy positions indentified by some of the stakeholders is as

follows:

Page 12 of 41

1. Stakeholders have indicated that in developing the IBT structures NERSA

did not take into consideration the fact that the electricity tariffs should reflect

the efficient costs of rendering an electricity service.

2. Stakeholders state that domestic tariffs should be cost reflective and should

be able to offer a suite of supply options with progressive capacity-

differentiated tariffs and connection fees.

3. Stakeholders have outlined that cross-subsidies should have a minimal

impact on price of electricity to consumers in the productive sector of the

economy.

4. Stakeholders have indicated that a single energy rate tariff is NOT an IBT

structure.

4.2 NERSA Research & Initial Approach

One of the electricity sectors objectives is to improve social equity by addressing

the requirements of the low income. The EPP states that low income customers

should be charged an appropriate tariff structure that allows for maximum

subsidisation at low consumption levels with gradually reducing cross subsidies

as the consumption level increases. The EPP also states that the domestic tariffs

should be more cost reflective, that cross subsidies should be made transparent

and licensees are required to publicise the average level of cross subsidy

between customer categories.

4.3 Questions to Stakeholders

Stakeholder Question 1: Stakeholders are requested to comment on any other

policies (e.g. the EPP) that they feel that NERSA did not consider when

developing the IBT structure.

Page 13 of 41

5. Municipal Data: Development of IBTs

5.1 Overview

In order to ensure that proper analysis and approval of municipal tariff

applications is achieved, NERSA requires correct and complete information on

which the tariffs are to be based (or determined). To this end, a need for

consistent and quality information is imperative. The required information for

tariff analysis and approval includes both qualitative and quantitative data and

must be in a form that is consistent with NERSA‟s objectives in so far as tariff

principles are concerned and as stipulated in the ERA.

Stakeholders have advised that one of the shortcomings of the current IBT

design is the fact that Eskom data was used to develop a national strategy on

IBTs and that this data is not relevant to the individual municipalities.

5.2 NERSA Research & Initial Approach

It must be noted that it is a great challenge collecting relevant and accurate

information from municipalities that could be utilized by NERSA in conducting

studies for purposes of IBT implementation. This is particularly the case with

medium and small sized municipalities. Data for the six metros is normally

available and reliable however using this data alone would also not be an ideal

representative of all municipalities. The NEDLAC paper (A study into

approaches to minimize the impact of electricity price increases on the poor)

further supports the issue regarding the lack of quality data from municipalities

and states that the quality of data for Eskom was generally good although the

availability of data on electricity prices, costs consumption and subsidies for

municipal distributors by category of consumer was generally very poor.

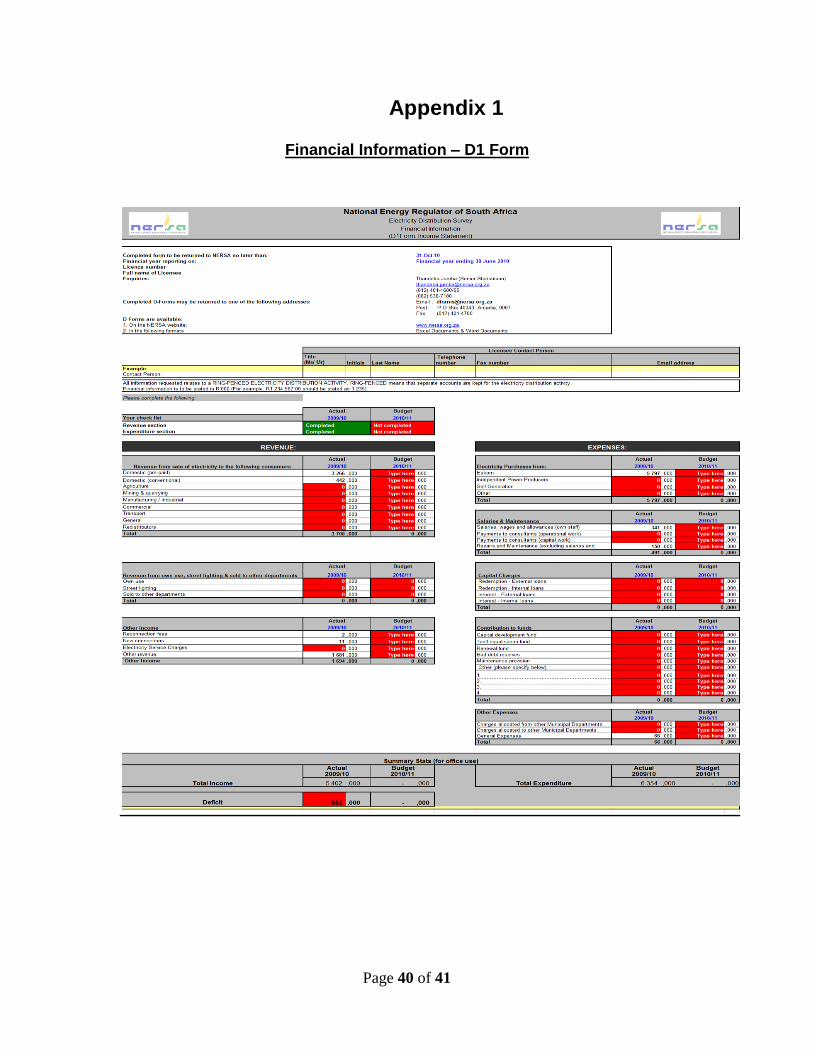

Appendix 1 is an example of the quality of data that NERSA currently receives

from municipal distributors. The data submitted was inaccurate and incomplete

for purposes of tariff analysis. For example: The Market Information Form (D2

Page 14 of 41

Form) – under the breakdown of consumer classification, requires that the

municipality input information regarding its customer numbers and consumption

(split into the various customer categories). This information is vital in tariff

setting as it allows NERSA to determine the customer category in which the

municipality recovers most of its revenues. In this case, the municipality only

reflects having domestic prepaid customers; however the actual tariff application

submitted by the municipality requests for approval for domestic conventional

metered customers, commercial and industrial customers.

Also on the Income Statement Form (D1 Form) – although in the D2 Form the

municipality reflected having only domestic prepaid customers, the D1 Form

shows revenue from sale of electricity for both prepaid and conventional meters.

The information also shows that the municipality experiences high level of deficits

whereas revenues from sale of electricity for other customer categories are not

accounted for. This is but one of the many inaccuracies and inconsistent

information that is submitted by municipalities.

Consequently, in the absence of quality information from municipalities, NERSA

uses the best available estimates to analyse and determine appropriate tariff

levels and structures for the specific municipalities.

Furthermore, NERSA does consider a municipality‟s unique characteristics and

challenges as presented by various municipalities during the tariff approval

process. NERSA allows deviations to the benchmarks, guideline and even IBT

structures. Municipalities that have presented extraordinary cases to NERSA,

supported by appropriate data, facts, reason and evidence have always been

granted approval to deviate from the set levels and structures.

Information(or closest estimates) that would be required from municipalities

needing to deviate from the benchmarks, guideline, IBT structures and those

Page 15 of 41

experiencing revenue losses as a result of IBT implementation include (but is not

limited to) the following:

1. Customer numbers (split into the IBT blocks)

2. Consumption levels (e.g. broken down into the different customer groupings

and consumption split into the blocks)

3. Revenues collected from the various IBT blocks

4. Subsidies for municipal distributors by category of consumer

5.3 Questions to Stakeholders

Stakeholder Question 2:

What data will be ideal to build a representative benchmark consumption level for

municipalities? Should NERSA use the data of the metropolitan municipalities to

determine the IBT structures? Should NERSA consider a municipality‟s individual

circumstances? Or due to the lack of quality data, should NERSA use a national

average based on Eskom‟s data?

6. Review of the structure of IBTs

6.1 Overview

There are various stakeholder views with regard to the number of blocks in the

current IBT structure. One view is that the current IBT structure has too many

blocks and the rates have not been optimally determined. Some stakeholders are

also of the view that the current structure of the IBT results in it not reaching the

“poorest of the poor” and also results in affluent customers being subsidized.

The other view is that the blocks are too few and that additional blocks should be

incorporated into the IBT structure.

This section discusses the issues relating to the structure of the IBT i.e. the

number of blocks, the consumption levels set for each block and the associated

rate levels set for each block.

Page 16 of 41

6.2 NERSA Research & Initial Approach

The NERSA IBT structure was based on international best practice where it was

found that countries that implemented IBTs opted for a tariff structure ranging

from two blocks to four blocks, in accordance with the principles of simplicity and

economical administration. During the workshop alluded to earlier in this

document with the six metropolitan municipalities, Eskom and meter vendors on

the Inclining Block Tariff (prior to approval of the structure by NERSA), the

metropolitan municipalities indicated that they preferred a tariff structure with

more than four blocks, or/ and raising the fourth block from 600kWh/month to a

higher monthly consumption amount, but no consensus was reached on what the

consumption level should be increased to.

In order to maintain the design principle that the tariff should be easy and

economical to administer/implement NERSA decided to limit the IBT to a 4 block

telescopic tariff structure. The telescopic IBT structure allows for consumers to

get the first block at the low price with large customers seeing a more efficient

(higher) price in the higher blocks. A non-telescopic IBT structure is one where

the low consumption customers pay the lower price for all units consumed whilst

the large consumption users pay the higher price for all units consumed.

The IBT was furthermore structured to ensure protection to low income

consumers who are “generally” also classified as low consumption customers.

Other low consumption customers (whether affluent or not) would also benefit

from the IBT structure, which is a tariff principle which is supported as this means

that these customers are placing less pressure on the electricity system. The

lower consumption by these customers leads to lower costs for the licensee.

It must further be noted that the IBT structure allows for quantified cross-

subsidies to be spread across the customer base. The differentiated pricing

mechanisms used previously (i.e. were increases to low income customers were

capped at 15% etc), which most licensees implemented to offer protection to low

Page 17 of 41

income households, also required for levels of cross-subsidies but did not allow

for these cross-subsidy levels to be quantified and transparent. The IBT therefore

allows for a more transparent pricing mechanism.

With regards to the current structure of the IBT (i.e. no of blocks etc), during the

analysis of municipal tariffs for the 2010/11 and 2011/12 financial year, it was

found that some municipalities requested for different IBT structures. These

structures have been based on additional blocks but no requests were made for

fewer IBT blocks.

NERSA acknowledges that a „one size fits all‟ approach is not the ideal situation.

However, in the absence of quality information from municipalities, and in order

to determine the most appropriate IBT structure, NERSA opted for the approach

of using the NERSA IBT structure as a guideline. This approach has been

practiced by NERSA in the assessment of the IBTs in the 2011/12 financial year,

whereby NERSA has approved different IBT structures for some municipalities

(based on the motivation for the differing structure as provided by the

municipality and supported by quality data). Although the IBT structure of the

municipality may have been different, NERSA ensured that the tariff still

supported the primary objective of ensuring protection to low income customers.

This was done by ensuring that the Block 1 and/ or Block 2 rates were increased

by the basis of the block increases as illustrated in Table 4 above (i.e. Block 1

increased by CPI and Block 2 increased by CPI plus % equal to Eskom‟s Real

WACC% allowed).

One approach or option to be considered with regards to the structure of the

Inclining Block Tariff would be to maintain the existing IBT block structure as a

guideline in determining IBTs. NERSA would however consider alternative IBT

structures (i.e. more or less blocks) provided that the municipality is able give

sufficient motivation for the deviation from the guideline. This motivation must be

supported by sufficient evidence and adequate data and information. This

Page 18 of 41

standardization will also allow for rationalization of tariff structures in place by

electricity distributors and will also allow for the like-for-like comparison of tariffs

amongst the various licensees/distributors.

6.3 Questions to Stakeholders

Stakeholder Question 3: What in your views would be the ideal IBT tariff structure

for implementation by licensees and why?

Stakeholder Question 4: Do licensees prefer an IBT structure with fewer or more

blocks? Please motivate accordingly.

Stakeholder Question 5: If NERSA continues with issuing the IBT guidelines and

benchmarks, would the approach of using the 4 block IBT structure as a

guideline be acceptable (with those licensees requiring a different tariff structure

motivating for such a structure)? Would it not be beneficial to have a standard

IBT structure to allow for comparison of tariffs between licensees?

Stakeholder Question 6: What would be the ideal approach to be adopted by

NERSA in setting the benchmark rates for the blocks (NERSA current approach

highlighted in Table 4 above)? What would be the principles that should be

adopted in order to set these benchmark rates whilst still achieving the objective

of protection of low income customers?

7. Potential Financial Implications of IBT

7.1 Overview

Licensees are concerned that the introduction of the NERSA IBT

structure/guideline may potentially result in direct revenue losses due to apparent

inconsistencies with current revenue management practices. The following are

Page 19 of 41

some of the revenue management practices that according to licensees may

potentially be negatively impacted.

1. The implementation of the NERSA IBT guideline without allowance for

some level of discretion may potentially lead to direct revenue losses to

licensees due to the fact that the unit prices (bands) for respective blocks

may in some cases be lower than what some licensees historically charge

their respective sub-categories of domestic customers for consumption

within the respective bands.

2. Licensees further claim that such potential revenue losses may directly

affect their surplus from electricity sales unless mechanisms are put in

place to compensate them through various forms of cross subsidization.

Licensees are also concerned that their lack of an appropriate domestic

customer mix results in revenue losses due to the low cost of electricity at

low levels of electricity consumption by domestic customers.

In terms of the current IBT guidelines, domestic customers should get the

first 350kWh/ month at relatively low tariffs. The tariff is slightly higher for

customer consumption between the 350kWh/month and 600kWh/month

and even higher for units‟ consumption in excess of the threshold of

600kWh/month to compensate for low end tariffs. Licensees may suffer

further revenue losses because the tariffs in terms of the IBT guidelines

for consumption in excess of the threshold of 600kWh/ month may well be

below respective historic tariffs to such high end customers. This may

therefore potentially result in unintentional subsidies to high end

customers at the expense of the licensees‟ revenues.

3. Licensees are also concerned that they may potentially lose revenue in

cases where they have a large number of domestic customers with

Page 20 of 41

irregular consumption patterns (should the IBT guideline restrict them to

single energy rate consumption based tariffs).

Similarly licensees are concerned that a single energy rate domestic tariff

will potentially inhibit their ability to effectively respond to their own

successes in implementing Energy Efficient Demand Side Management

(EEDSM). Effective implementation of EEDSM will inevitably result in

reduced demand and associated reduction in bulk purchases costs.

Implementation of EEDSM normally results in reduction in sales volume

which unless the licensee has an effective two part tariff may result in

disproportional loss in revenue. While successful implementation of

EEDSM will inevitably lead to revenue loss it should also lead to a

proportional reduction in the bulk purchase cost such that the licensee

remains revenue neutral, net revenue that is.

7.2 NERSA Research & Initial Approach

The initial design of the IBT structure was based on a licensee with a certain

profile in mind i.e. the appropriate customer mix and numbers, etc. Due to

differences in domestic customer mix, individual licensees were allowed

discretion in implementing the IBT guideline. Individual licensees‟ were on

condition that they provided supporting documents, in accordance with their

special circumstances allowed some discretion in implementing the NERSA

IBT guideline/structure. Some licensees therefore applied for higher tariffs per

block. The main reason for this was due to licensees arguing that the

consumption of majority of their residential customers generally do not

consume greater than 350kWh/month (Block 2) whereas they historically

charged such customers tariffs higher than the prescribed IBT guideline.

Licensees further argued that this is the range were they generate more than

50% of their revenue from domestic customers.

Page 21 of 41

The potential revenue loss stems from the fact that a particular licensee for

example, has a lifeline tariff for qualifying customers of 78.52c/kWh whereas

the corresponding IBT guideline ranges between 68.00c/kWh to 71.00c/kWh

for all domestic customers. The guideline therefore extends the benefit to

customers that would otherwise not have been on a lifeline tariff. NERSA has

therefore allowed these licensees to exercise discretion in implementing the

IBT guidelines to ensure that the licensee does not potentially suffer some

form of revenue loss with respect to the price and to ensure that a larger

number of domestic customers do not benefit from the subsidized price

instead of only customers on the lifeline tariff of the licensee concerned.

Similarly customers on a domestic tariff of a well known licensee with an

assumed average consumption of 725kWh/month would have paid a

weighted average price of 88.14 c/kWh only (as illustrated in Table 7 below)

had the licensee concerned not have applied for discretion in implementing

the IBT guideline.

Table 6: Tariff based on the IBT guideline

The licensee concerned was however allowed to implement the IBT guideline

with variation whereby it was allowed higher block sizes and higher tariffs per

block as well as a fixed basic charge. As a result the licensee will sell the

same 725kWh/month at an average tariff of 124.08c/kWh as illustrated in

Table 8 below. The licensee will as a result not suffer any revenue loss

725

Size Usage Tariff (/kWh)

Block 1 50 50 675 63 31.50

Block 2 350 300 375 71 213.00

Block 3 600 250 125 95 237.50

Block 4 3000 125 0 114 142.50

624.50

2 14.50

639.00

88.14 Average Tariff

Assumed usage

Sub-total

DSM Levy

Total Charge for the Month

Page 22 of 41

directly attributable to the IBT guideline due to the fact that NERSA allows

some flexibility in the implementation of the IBT guideline.

Table 7: Tariff based on variation on IBT guideline

With regards to IBTs and the need for a cross-subsidy mechanism, the

intention with the IBT design was that the high-end domestic tariffs would

compensate for the low-end tariffs. This however is dependent on an

appropriate level of domestic customer mix and the licensees‟ marginal cost

being in line with upper limit of the IBT band for consumption in excess of the

monthly threshold of 600kWh/month. Licensees with a high proportion of low

consumption domestic customers may potentially suffer net revenue losses

as they may not have sufficient numbers of high consumption domestic

customers to compensate for subsidized prices at lower levels of

consumption. In this regard, NERSA further allowed for cross-subsidies from

the rest of the customer base to deal with such revenue losses (i.e. cross-

subsidies from the commercial and industrial customer base).

In terms of revenue losses due to customers with irregular usage 3and

EEDSM measures being implemented, NERSA has allowed licensees to

implement two part IBT4 tariffs. This tariff structure was allowed to ensure that

3 This refers to customers such as holiday homes etc.

4 A tariff structure with a fixed monthly charge plus energy charges with IBT blocks

725

Size Usage Remainder Tariff (c/kWh) Price (H)

Block 1 500 500 225 79.31 396.55

Block 2 1,000 225 0 80.65 181.46

Block 3 2,000 - 0 81.99 -

Block 4 3,000 - 0 83.98 -

307.04

885.05

0.02 14.50

899.55

124.08

DSM Lvey (c/kWh

Total Charge for the months

Sub-total

Assumed usage

Average Tariff c/KWh

Basic Fixed Charge

Page 23 of 41

the licensee was still able to maintain the ability to effectively compensate for

both the variable and fixed cost components of its cost structure.

The above approaches used indicates that NERSA has allowed such

arguments on a case by case basis based on the soundness of each

business case provided and on condition that the licensee provided NERSA

with the necessary information (as per the information requirements set out in

Section 4: Municipal Data – Development of IBTs) in order for NERSA to

undertake its own independent analysis. Furthermore, these above the

benchmark level rates were accepted on the basis that the objectives of the

IBTs were still maintained. In the interest of ensuring revenue neutrality

licensees were for example allowed variations to the block sizes, the

maximum tariff per block and even allowed a two-tier tariff for higher end

customers.

7.3 Questions to Stakeholders

Stakeholder Question 7: What are other mechanisms that can be used to protect

under/over recovery of revenue due the implementation of IBTs? Does the IBT

guideline unintentionally benefit high-end domestic customers? If so, how can

this be dealt with?

Stakeholder Question 8: In cases where the licensees‟ customers are

disproportionately distributed (majority customers falling in a certain block), how

should the blocks be structured without losing the IBTs primary objectives of

protection of low income households?

Page 24 of 41

8. Multiple Household Dwellings

8.1 Overview

In South Africa, many low income customer areas have multiple family

households i.e. there are many families living in one household. These

households are supplied by a single electricity supply point which results into a

higher combined usage.

Due to there being multiple families in one household, it leads to the household

having high levels of consumption. With the current IBT structure, it means that

these customers (if these households remain connected through to one meter

per multiple family household) will be consuming in either block 3 or 4 which has

higher tariff rates associated with it. These customers will therefore not

necessarily receive the benefit of the protection from high prices as intended by

the IBT while there consumption is read as that of one customer.

8.2 NERSA Research & Initial Approach

The supply of electricity to multiple households in South Africa has various

challenges. As highlighted above, one of the challenges is passing on the

intended benefits of the IBTs to these customers. Another challenge is that, due

to these customers having only one meter per household, they are not able to

receive the benefits of the FBE mechanism (i.e. these multiple households only

receive 50kWh/ month free, rather than each family or dwelling receiving the FBE

units).

However, the issue regarding multiple household dwellings is an issue that is not

unique to South Africa. This issue has been raised in many countries, during the

introduction of IBTs, in both the electricity and water sectors. These countries

include Australia (Victoria), United Kingdom (Wales). The approaches adopted

by these Regulators together with other approaches are discussed below:

Page 25 of 41

1. The Essential Services Commission (The Regulator in Victoria) dealt with

the issue of multiple households that are being serviced by a single meter by

applying the consumption tiers/levels on a pro-rata basis (Pro rata option).

This essentially means that the Regulator had to determine or approximate

how many families existed per multiple family household. Each

family/customer within the household was then billed separately i.e. the IBT

was then applied for each family thus allowing each family to benefit from

the IBT structure. This therefore allowed for these multiple households not to

be burdened with high electricity bills.

This option is considered acceptable as it will allow for each multiple family

to receive the intended benefits of the IBT tariff structure. However, one of

the practical challenges of adopting this approach would be the detailed

administration required. This approach would require that the licensee have

a detailed understanding of each multiple family household (i.e. number of

families in each household etc.) and would further require that the licensee

verify this information on an ongoing basis.

2. Other regulators in the United Kingdom opted for increasing the consumption

levels of its Block 1 or 2 to ensure that the lower prices applicable in these

blocks would ensure that the multiple households are not unduly punished

for consumption that falls out of their control (alternate tariff structure option).

This option would allow for the setting of the consumption level at an

average level. Due to the average levels of consumption set, this option

would not allow for each family to be accurately billed. This option would

however be more practical and easier to implement.

3. Another option to be considered in South Africa would be to ensure that

each family with the multiple household dwelling has its own meter installed

in order to track consumption per family unit. This will allow for proper

Page 26 of 41

implementation of the IBT structure and will further facilitate the

administration of the FBE mechanism as each family will then be able to

receive the FBE benefits it is entitled to.

The benefits of this option needs to be considered together with the

challenges and costs associated with it. Licensees state that the challenge

they face is that the licensee has to incur costs to reconfigure circuits to

cater for individual metering and customers cannot afford the added costs to

embrace the benefits of IBTs.

8.3 Questions to Stakeholders

Stakeholder Question 9: What is the most practical solution that licensees would

consider to enable multiple household customers to benefit from the IBT, as

those that are individually metered do?

Stakeholder Question 10: How do licensees currently apply the FBE mechanism

to this customer group and would this solution (if any) also work in resolving the

challenge around the implementation of IBTs for this customer category?

Stakeholder Question 11: Are multiple households easily identifiable by

licensees, in order for these customers to be placed on an alternate tariff

structure?

Stakeholder Question 12: What are the estimated costs associated with

reconfiguring circuits to allow for individual metering? Would the benefits

outweigh the costs?

Page 27 of 41

9. Issue regarding customers with irregular usage

9.1 Overview

Various municipal areas in South Africa have customers with irregular or

intermittent usage. These are normally holiday homes etc, where customers use

their households for very few months of the year. However, during these months

of occupation, consumption can be high.

Stakeholders argue that with the IBT structure, these customers will enjoy the

benefit of low electricity bills during months where there is little or no usage

thereby creating a revenue shortfall.

9.2 NERSA Research & Initial Approach

This category of customers have a historic (i.e. prior to the implementation of

IBTs) pattern of irregular and intermittent usage. It is therefore evident that even

in the past, during months of low or intermittent usage, the revenues collected

from the energy charge component of the tariff would still have been limited. The

revenue required from this customer category is therefore maintained through the

fixed charge component of the tariff.

With regards to this challenge, NERSA would prefer to draw knowledge from how

this issue was dealt with by electricity distributors/licensees in South Africa that

have customers with irregular usage. For the 2011/12 financial year, distributors

that faced this challenge of introducing IBTs for customers with intermittent

usage opted for an IBT tariff structure with a fixed charge. Some licensees opted

to embed the fixed charge into the block rates whilst some opted for the simpler

approach of retaining a separate fixed charge component to the tariff structure.

These licensees have identified this customer group and set an IBT tariff

specifically for this group of customers. By retaining the fixed charge component

in their tariff structure the licensee was able to ensure revenue neutrality.

Page 28 of 41

NERSA‟s initial approach is therefore that the IBT is a structure that can be

implemented for this customer category provided that the cost to supply these

customers is retained through the fixed charge.

9.3 Questions to Stakeholders

Stakeholder Question 13: Is the aforementioned approach of retaining the fixed

charge in the tariff structure appropriate in resolving the issue regarding

customers with intermittent usage? Alternatively, is there any other approach that

should be considered to deal with this challenge?

10. Issues regarding resellers

10.1 Overview

The following is a summary of the issues regarding IBTs and resellers:

1. A block of flats where the landlord contracts for a point of supply with the

supply authority and sells on to the tenants who are metered by the

landlord.

2. A complex of dwellings (townhouses) where the supply authority gives one

point of supply and the developer/body corporate then takes the

responsibility to supply, meter and bill the tenants/subtitle owners. This is

done directly or by using a contracted agent.

In the above cases the supply authority in past times might have given the supply

on a “Home Bulk” tariff which was designed for this situation or if the supply point

was big enough a “Bulk” supply tariff similar in structure to the Megaflex tariff.

The problems arise when the “Home Bulk” tariff has been converted to an IBT

tariff. This means that in these cases where the old flat rate has been converted

to an IBT the largest part of the usage will be billed at the highest (Block 4) rate

to the landlord who then must somehow pass this on to the end user who is then

effectively charged for all usage at a rate close to the block 4 rate. The more end

Page 29 of 41

users there are the more closely their rate will move towards the block 4 rate

because the higher the percentage of the landlords power will be in the block 4

rate.

At this point there are two important points need to be made.

1. NERSA‟s initial position is that the end user supplied by a reseller should

be no worse off than if directly supplied by the supply authority.

2. IBT‟s were designed for single dwellings or a single user behind the meter.

Therefore any solution needs to take this into account.

10.2 NERSA Research & Initial Approach

NERSA is currently busy with the issue of Resellers and is busy holding

stakeholder workshops prior to publishing a consultation paper on the whole

reseller issue and inputs from both will be considered in resolving the problems

stated above.

In terms of possible solutions to the above problems there seem to be the

following options:

1. Just simply rule that IBT‟s will not apply where there are multiple end

users behind the supply authority meter.

2. Specify that the supply authority has an appropriate tariff/“special tariff” as

for the reseller is in fact not a domestic customer and should not be

treated as though it is a special domestic customer who has to be on the

IBT tariff. The reseller customers as domestic end users can best be

suited on tariffs in line with the IBT structure/guideline. The reseller should

be on a tariff commensurate to its profile as a customer taking delivery at a

higher volumes such that it is in a position to charge the final consumers

tariffs in line with the IBT guideline and still been able to recover its cost.

This is based on the presumption that it is indeed the cost of supply to a

customer while a profile similar to the reseller is lower than the cost of

supply to traditional domestic customers.

Page 30 of 41

3. Use a “Home Bulk” type tariff which adjusts the block sizes to the number

of end users.

Option 1 does not meet the requirement of the end user being treated the same.

Option 2 is not as unreasonable as it sounds and some licensees have adopted

this approach recognizing that the reseller to provide a service which the licensee

would otherwise have to provide. Therefore they give them a discount on their

tariff. This actually seems to be the simplest and fairest method. Option 3 would

be very complex to administer and use and in addition would eliminate individual

price signals.

10.3 Questions to Stakeholders

Stakeholder Question 14: As a reseller/trader, do you encounter any challenges

in your implementation of the NERSA approved IBTs rates? You are kindly

requested to list all your challenges and suggest possible solutions to those

problems.

Stakeholder Question 15: As a reseller/trader, are you currently charging your

customers in line with the NERSA-approved IBT rate? If so, are you

implementing the IBT for all your customer categories, or if not, what is your

current practice?

Stakeholder Question 16: Which option stated above is considered acceptable

and practical to implement?

11. Technical Challenges

11.1 Overview

The IBT requires that customer consumption needs to be tracked on a monthly

basis in order to allocate the consumption to the relevant block. This would allow

for customers to be charged at the rates applicable to their consumption levels

Page 31 of 41

and to be billed accurately. Prepaid vending systems and billing systems

therefore need to be able to accommodate for these requirements.

Furthermore, it has been stated that the IBT creates further billing issues as at

least 10% of all conventional domestic meter readings are being estimated each

month. The application of IBT rates makes the process of estimation and

correction more complex.

11.2 NERSA Research & Initial Approach

During consultation with various meter suppliers in South Africa, it was identified

that current vending systems that most licensees have would be able to support

IBTs. However, the vending system software would need to be updated in order

to record consumption. Updating the vendor software would require less time and

results in lower costs to amend vending systems to accommodate for IBTs, than

originally estimated.

The aforementioned points raised by the meter suppliers are acknowledged.

NERSA does however note that there are some (albeit few) licensees that still

have old vending systems in place that would not be able to accommodate the

IBTs. Furthermore, the billing systems of some licensees also require updating in

order to accommodate for billing of conventional metered customers.

Due consideration will be given to those licensees still struggling to upgrade its

systems, however this will be assessed in line with the fact that licensees have

had sufficient time to upgrade their systems (NERSA decision to introduce IBTs

announced in February 2010). Licensees are urged to engage with their vending

suppliers to find suitable solutions to these vending issues. Liaising with other

licensees that have successfully upgraded systems for implementation of IBTs is

also encouraged.

Page 32 of 41

With regards to the issue regarding the reading of meters, there are various

options to consider in addressing this issue:

1. Option 1: Reading of meters on a monthly basis

2. Option 2: Approach adopted by Eskom.

3. Option 3: Installation of smart meters

Option 1 would be an acceptable approach and would allow for customers to be

billed based on actual consumption every month and there would therefore be no

need for estimates, etc. However, given the current challenges with meter

readings (gaining entry into properties etc), the practicality of implementing such

an option should be considered.

Option 2 refers to the current method adopted by Eskom. Eskom reads meters

every 3 months in line with the requirements of its Electricity Supply contract. For

month 1 and 2 Eskom bills the customer based on estimates. In month 3, the

actual meter reading occurs. Eskom then re-bills the customer for the three

months based on the actual results. The re-billing is system generated and

therefore there is no complexity in this regard. However, the bill to the customer

for month 3 contains all the calculations regarding the re-billing and therefore

does create a level of complexity as it could create customer confusion. NERSA

notes this challenge but views it as a challenge that could be overcome.

Option 3 is considered as an ideal approach and would allow electricity

distributors to read meters as and when required. This option would also allow for

accurate meter readings and billing on a monthly basis, with no adjustments to

bills being required. Although the cost of smart meters may be significantly high,

this option is considered, as the more effective and efficient way forward.

Licensees should therefore consider this option as a long term solution.

Page 33 of 41

11.3 Questions to Stakeholders

Stakeholder Question 17: For those licensees still experiencing system

challenges please provide the details regarding such challenges (with the

exception of those highlighted above). What is considered as sufficient time to

address vendor/system challenges? (i.e. 2 years, 3 years etc).

Stakeholder Question 18: With regards to the reading of meters, which option is

considered the most appropriate way forward? Please provide reasons for the

option selected.

12. Alternate Options: Other tariff structures to be

considered

12.1 Overview

This section aims to deal with whether the IBT is appropriate as the only tariff

structure for residential customers or whether the IBT should be considered

along with a suite of other residential tariffs. This could include a single energy

rate tariff, a two part tariff (energy rates and fixed charges and the Time-of-Use

tariff (TOU) for residential customers consuming more than 1000kWH.

Stakeholders have also supported the need for additional tariff structures to be

made available for residential customers. It has also been stated that FBE

allocation to customers should be increased from 50kWh/month to increase relief

to these customers.

12.2 NERSA Research & Initial Approach

The IBT has been proven by various international utilities to be an appropriate

and effective tariff structure to protect customers from high price increases.

Page 34 of 41

Keeping this in mind, it is also necessary to ensure that customers have a choice

of the tariff structures available to them. The need to offer customers a suite of

supply options therefore needs to be explored and considered.

Government Gazette No. 31250 states that „An end user or customer with a

monthly consumption of 1000kWh and above must have smart system and be on

time of use tariff no later than 01 January 2012.‟ This therefore means that

alternate tariff structures need to be in place for residential customers.

Based on the above requirement and other aforementioned issues, it is

suggested that the following tariff structures be considered for residential

customers:

1. Single energy rate life line tariff: This is applicable for customers

consuming below 1000kWh per month and where it is impossible to

implement IBTs. This tariff structure will only be considered as a last resort

and where it has been proven that due to exceptional circumstances the

licensee is unable to implement IBTs.

2. Inclining Block Tariffs: This tariff structure is applicable for all residential

customers consuming less than 1000kWh per month, with the exception of

the above.

3. Time-of-Use Tariffs: As per the aforementioned regulations, this tariff is

applicable for residential customers consuming more than 1000kWh per

month.

With regards to the issues on increasing the FBE allocation to customers, it must

be stated that the Free-Basic Electricity (FBE) policy consumption level is

currently set at 50kWh/month. The FBE policy states that the Department of

Energy (DoE) in consultation with the Department of Provincial and Local

Government (DPLG) and the National Treasury (NT) will determine the extent of

provision of free basic electricity which can be funded through inter-governmental

Page 35 of 41

transfers on an annual basis. The abovementioned authorities are therefore

responsible for the final decision on the increase in consumption levels for FBE.

This therefore falls outside the mandate of NERSA.

12.3 Questions to Stakeholders

Stakeholder Question 19: Are the aforementioned tariff structures considered

appropriate for implementation for residential customers? Should the suite of

tariffs include other options? If yes, what should these options be?

Stakeholder Question 20: Would the introduction of many tariff structures for

residential customers not defeat the aim of rationalization of tariffs, as required

by the EPP?

13. Seasonally differentiated tariffs to address cash flow issues

13.1 Overview

This section aims to discuss the issues regarding the Eskom Time-of-Use (TOU)

tariffs and the cash-flow impact this creates for municipalities. Municipalities

state that the high Eskom price differentiation, which reflects the Eskom cost

differences between high demand and low demand season, causes major cash

flow problems. Municipalities further advise that for this reason they have been

applying seasonally differentiated tariffs to address cash flow issues and to

signal to customers the higher electricity costs associated with the high demand

season. It is further stated that the domestic consumption in the high demand

season (winter) makes up close to 50% of total. The NERSA IBT does not cater

for this necessary feature.

Page 36 of 41

13.2 NERSA Research & Initial Approach

The NERSA understanding of the aforementioned issue is that municipalities

purchase from Eskom on a TOU tariff are passing on the TOU signals onto

domestic customers to address cash flow issues.

The NERSA analysis of tariff applications from municipalities prior to the

introduction of IBTs indicates that most municipalities did not have time-of-use

tariffs for domestic/ residential customers. The residential tariffs implemented by

municipalities therefore did not allow for the TOU signals to be passed through to

the end consumer. The introduction of IBTs therefore does not exacerbate the

cash flow issues of municipalities and that this issue would have existed had the

single and two part tariffs still been in place.

As discussed in Section 11: Alternate Options: Other tariff structures to be

considered, NERSA supports the introduction of TOU tariffs for domestic

customers consuming more than 1000kWh/month.

NERSA acknowledges the issue of seasonally differentiated or cash flow

problems but is of the view that this is not due to the introduction of IBTs. This

issue can be addressed more successfully through the introduction of TOU tariffs

for larger users.

13.3 Questions to Stakeholders

Stakeholder Question 21: How does the introduction of IBTs further affect the

cash flow situation of municipalities? Would this issue not have prevailed even

with the single and two part tariff structures in place? Please also suggest ways

in which municipalities with majority low consumption (residential) users could

address this issue.

Page 37 of 41

14. Impact of price /tariffs signal due to customers

implementing EE measures, and the impact these measures

have on the licensees revenues

14.1 Overview

NERSA through tariff determination must enable an efficient licensee to recover

the full cost of its licensed activities, including a reasonable margin or return

based on forecasted sales. With the impact of the implementation of EEDSM

measures and high price increases, the actual sales decrease below the

forecasted levels and the licensee/ electricity distributor earns less revenue. Due

to this licensees may not be able to recover all of its fixed costs and could result

in the licensee not encouraging energy efficiency.

14.2 NERSA Research & Initial Approach

The issue regarding migration of customers to alternate energy sources and the

effects of EEDSM are considered to be challenges faced by licensees,

irrespective of the tariff structure in place (i.e. this is not specifically created by

IBTs). The research below therefore aims to address the issue from an overall

tariff perspective.

It is common that all over the world that the successful implementation of energy

efficiency programs lowers a licensees revenues and it is clear that this will

discourage licensees to invest in EE programs. There are about three major

approaches for dealing with loss revenue due to EEDSM:

1. Full or Per-Customer Adjustment Revenue Decoupling5: Full or Per-

Customer Adjustment Revenue Decoupling adjusts a licensees revenues

for any deviation between expected and actual sales regardless of the

reason (technical losses or EEDSM) for the deviation.

5 NARUC: Decoupling For Electric & Gas Utilities: Frequently Asked Questions (FAQ)

Page 38 of 41

2. Net Lost Revenue Recovery, Lost Revenue Adjustments, or Conservation

and Load Management Adjustment Clauses: This mechanism adjusts net

changes in revenues only for sales deviations that can be proven or

demonstrated to have resulted from conservation and load- management

programs.

3. Straight-Fixed Variable Rate Design: This mechanism eliminates all

variable distribution charges and costs are recovered through a fixed

delivery services charge or an increase in the fixed customer charge

alone.

In the event of decreased sales due to EEDSM, NERSA is considering

implementation of the decoupling mechanism. The Decoupling mechanism is the

rate adjustment mechanism that separates an electric utility‟s fixed cost recovery

from amount of electricity it sells. If sales increase, rates drop in the next period;

if sales decrease, rates increase to compensate.

Out of other available methods, NERSA will also consider the Lost Revenue

Adjustment Mechanism (LRAM).LRAM is where the licensee is compensated for

the lost margins resulting from its programs to promote EE. The LRAM can be

implemented at the end of each financial year of the licensee and allow the

licensee to recover a portion of loss revenue due to the implementation of

EEDSM. This will be tracked programs which can be measured and verified. The

cost of M&V shall be included in all EEDSM cost allocation.

14.3 Questions to Stakeholders

Stakeholder Question 22: What is the best method that can be adopted by

NERSA to assist licensees, in case of any revenue loss due to EEDSM?

Stakeholder Question 23: Who should pay the cost of doing M&V, if the project is

funded outside MYPD budget?

Page 39 of 41

Stakeholder Question 24: If sales decrease, should the price per unit of energy

go up and when should the price be adjusted?

15. Any Other Comments

Stakeholder Question 25: Stakeholders are requested to make any other

comments on issues relating to Inclining Block tariffs, not addressed elsewhere in

the consultation paper.

Stakeholders are requested to comment in writing on the Review of the

Inclining Block Tariffs Consultation Paper for Electricity Distributors.

Written comments can be forwarded to [email protected]; hand-

delivered to 526 Vermeulen (Madiba) Street, Arcadia, Pretoria or posted to

P.O Box 40343, Arcadia, 0083, Pretoria, South Africa. The closing date for

the comments is the 11 October 2012 at 16H00.

For more information and queries on the above please contact Ms Porcia

Makgopela and Ms Priya Singh at the National Energy Regulator of South

Africa, Kulawula House, 526 Vermeulen (Madiba) Street, Arcadia, Pretoria.

Tel: 012-401 4600

Fax: 012 401 4700

End.

Page 40 of 41

16. Appendix 1

Financial Information – D1 Form

Page 41 of 41

Appendix 1 (continued)

Market Information – D2 Form