comprehensive annual financial report june 30, 2003colscf.cityofls.net/content/cafrfy03.pdf ·...

TRANSCRIPT

CITY OF LEE’S SUMMIT, MISSOURI

Comprehensive Annual Financial Report

June 30, 2003

CITY OF LEE’S SUMMIT, MISSOURI

COMPREHENSIVE ANNUAL FINANCIAL REPORT

For the fiscal year ended

June 30, 2003

Prepared by:

Department of Finance

CITY OF LEE’S SUMMIT, MISSOURI

Table of Contents

Page

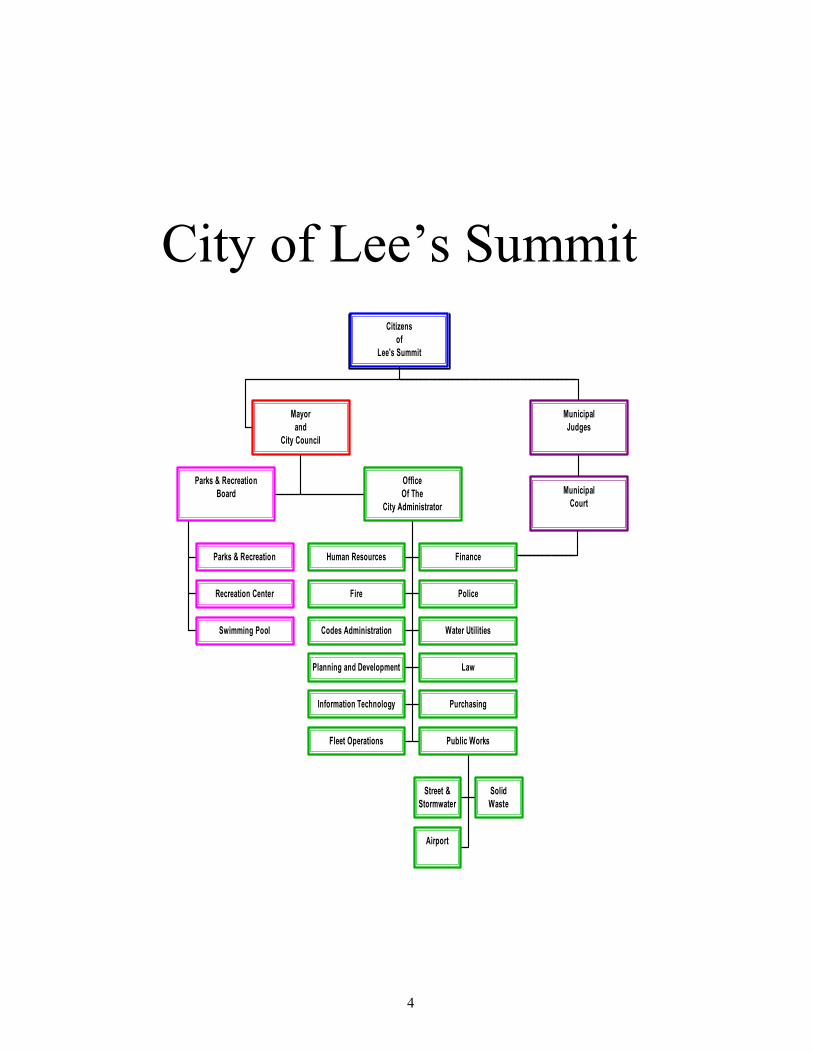

Introductory Section: Principal Officials 3 Organizational Chart 4 Letter of Transmittal 6-13 GFOA Certificate of Achievement 14

Financial Section: Independent Auditors’ Report 18-19

Management’s Discussion and Analysis 20-27

Basic Financial Statements: Government-Wide Statement of Net Assets 29 Statement of Activities 30

Fund Financial Statements Governmental Funds: Balance Sheet 31

Reconciliation of the Governmental Funds Balance Sheet to the Statement of Net Assets 32

Statement of Revenues, Expenditures, and Changes in Fund Balances 33

Reconciliation of the Change in Fund Balances of Governmental Funds to the Statement of Activities 34

Proprietary Funds: Statement of Net Assets 35 Statement of Revenues, Expenses, and Changes in Fund Net Assets 36 Statement of Cash Flows 37

Notes to Basic Financial Statements 38-59

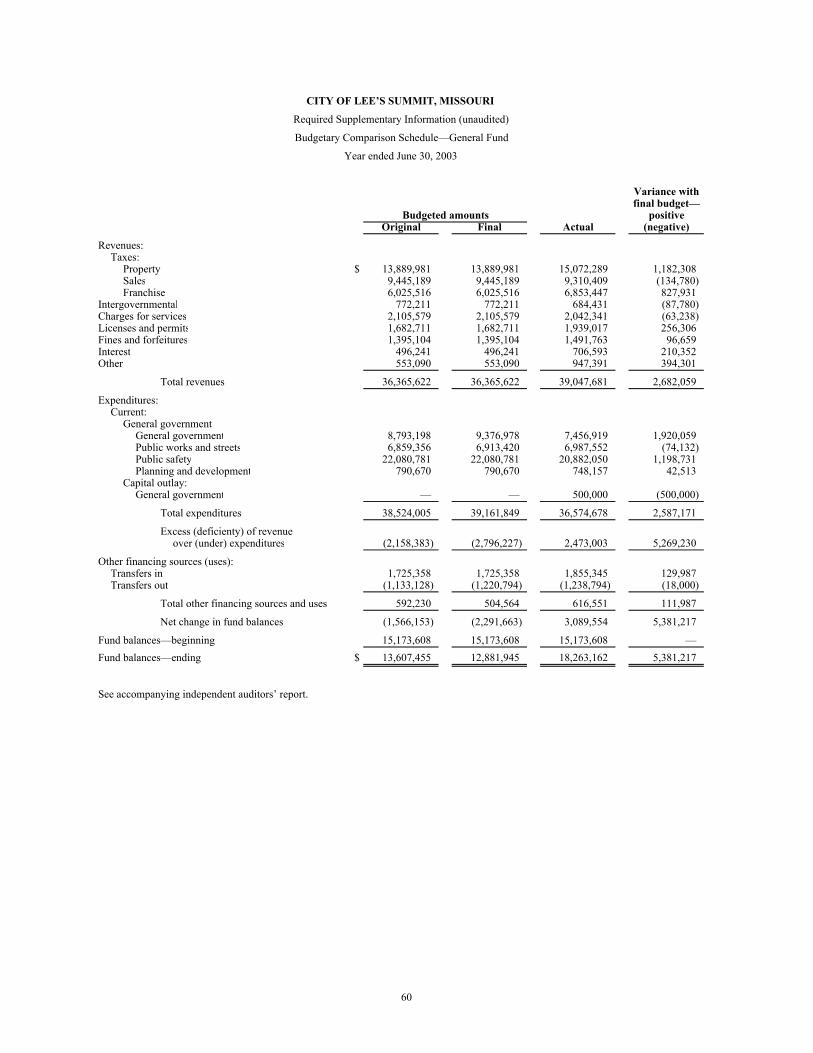

Required Supplementary Information Budgetary Comparison Schedule—General Fund 60 Notes to Budgetary Comparison Schedule—General Fund 61 Schedule of Funding Progress—Retirement Plan 62

Supplementary Information Combining Balance Sheet—Nonmajor Governmental Funds 63 Combining Statement of Revenues, Expenditures, and Changes in

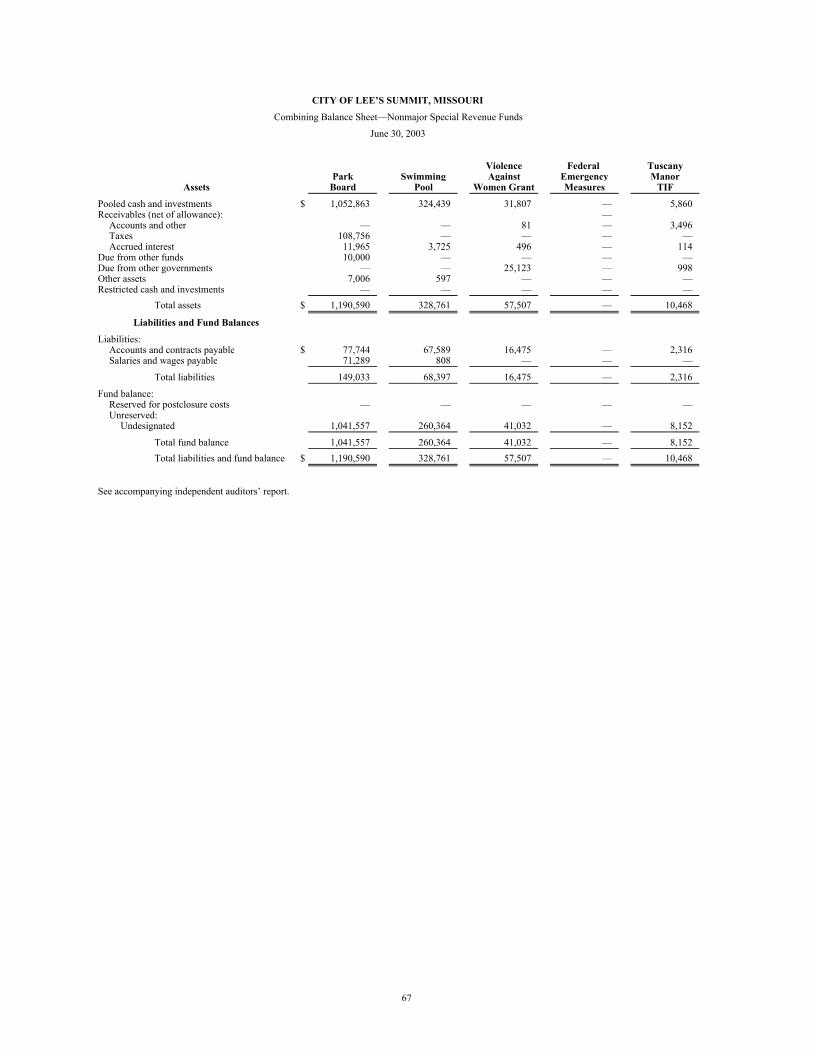

Fund Balances—Nonmajor Governmental Funds 64 Combining Balance Sheet—Nonmajor Special Revenue Funds 67-68

Page

Supplementary Information (continued) Combining Statement of Revenues, Expenditures, and Changes in

Fund Balances—Nonmajor Special Revenue Funds 69-70 Budgetary Comparisons—Special Revenue Funds 71-76 Combining Balance Sheet—Nonmajor Capital Projects Funds 79-80 Combining Statement of Revenues, Expenditures, and Changes in

Fund Balances—Nonmajor Capital Projects Funds 81-82 Budgetary Comparison Schedule—Debt Service Fund 83 Budgetary Comparison Schedule—Park Development Fund 84 Budgetary Comparison Schedule—Road and Bridge Excise/Sales

Tax Fund 85 Combining Balance Sheet—Nonmajor Enterprise Funds 87 Combining Statement of Revenues, Expenses, and Changes in

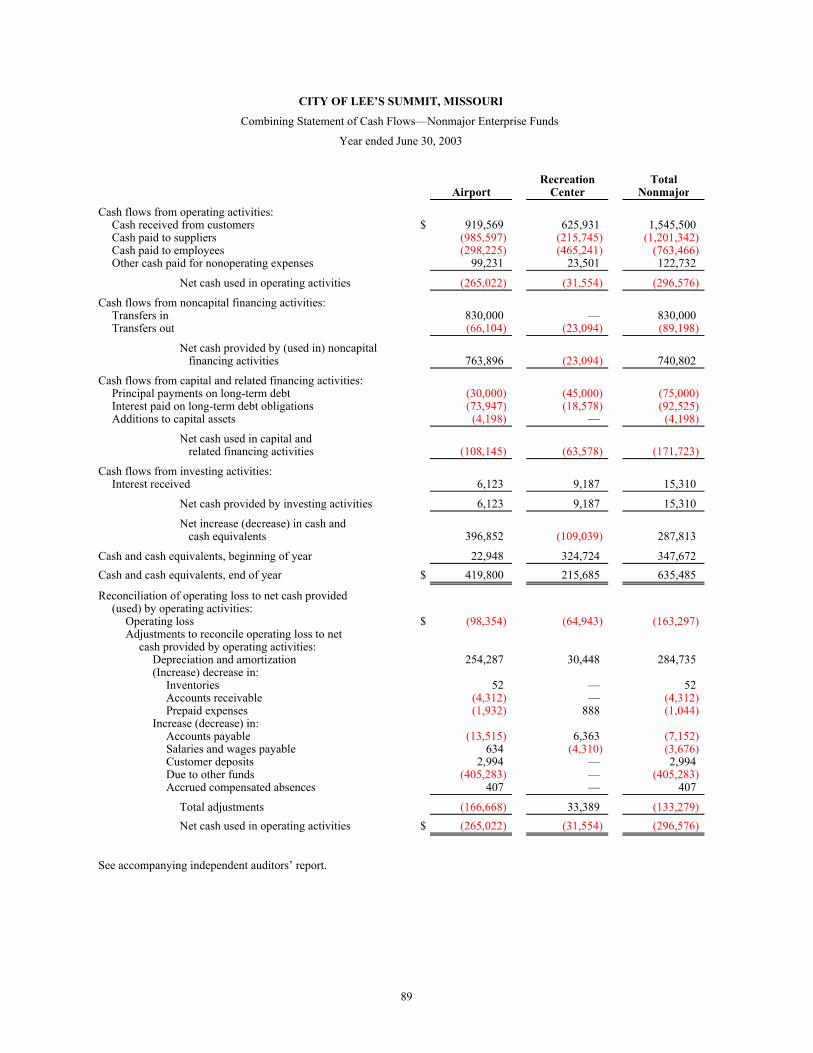

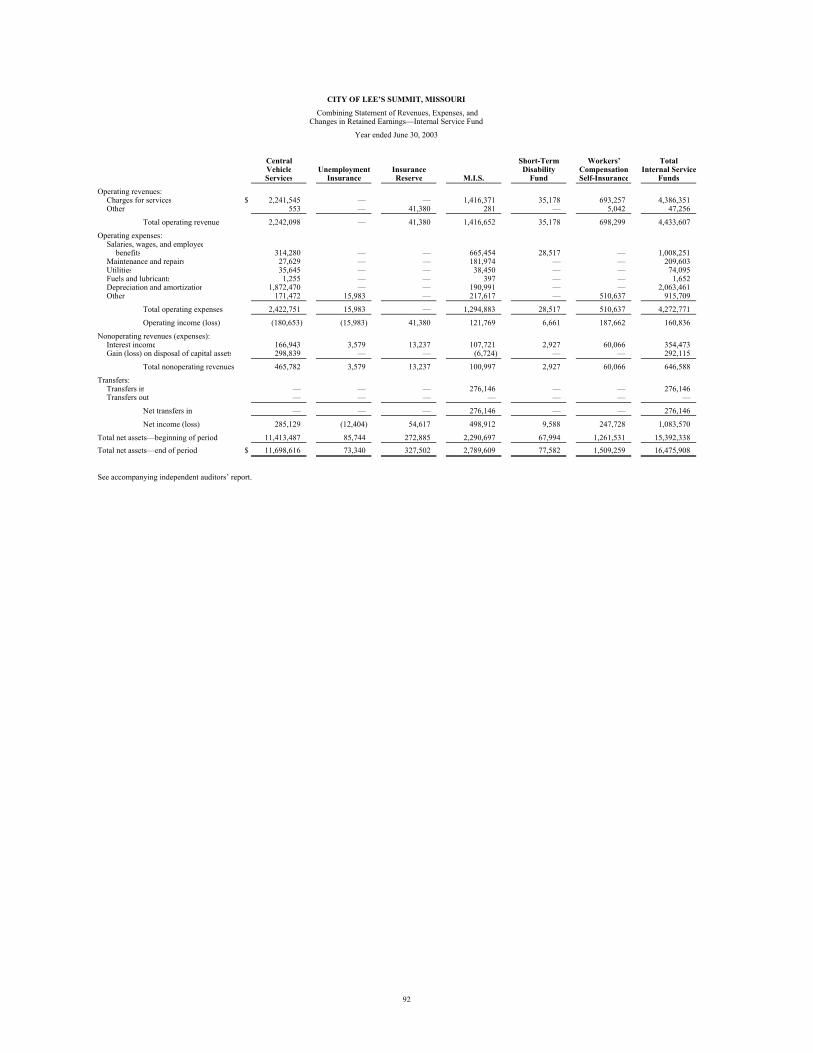

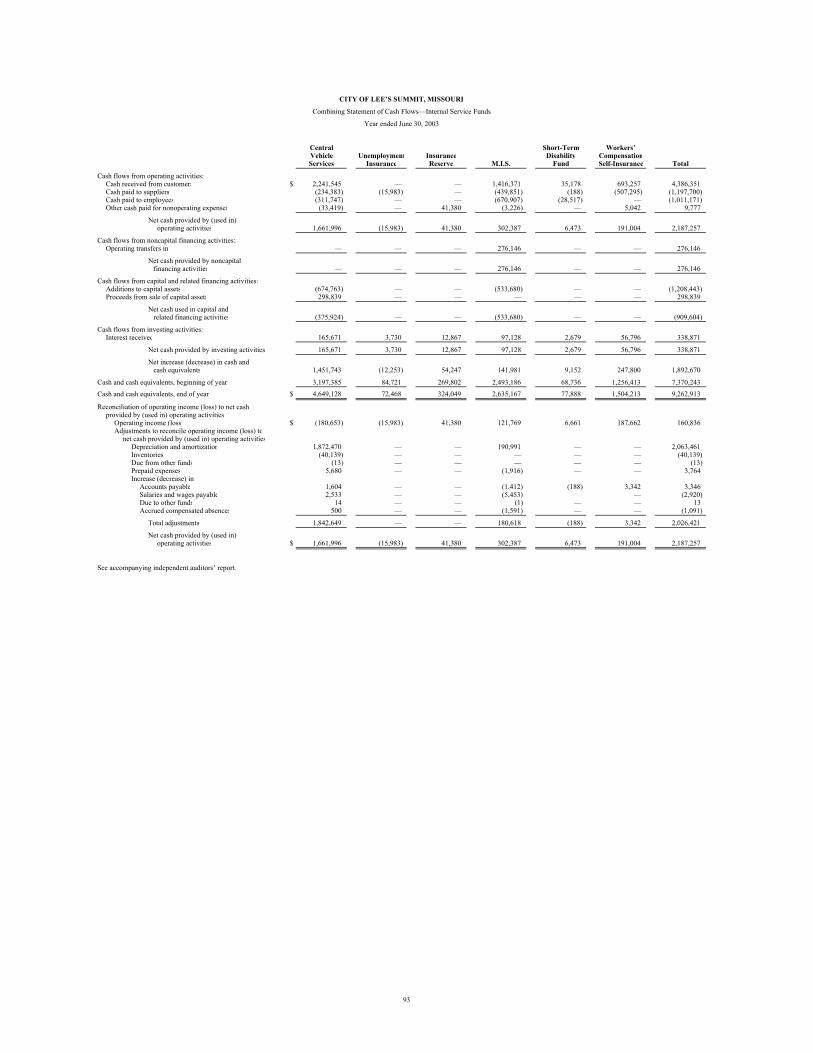

Retained Earnings—Nonmajor Enterprise Funds 88 Combining Statement of Cash Flows—Nonmajor Enterprise Funds 89 Combining Balance Sheet—Internal Service Funds 91 Combining Statement of Revenues, Expenses, and Changes in

Retained Earnings—Internal Service Funds 92 Combining Statement of Cash Flows—Internal Service Funds 93

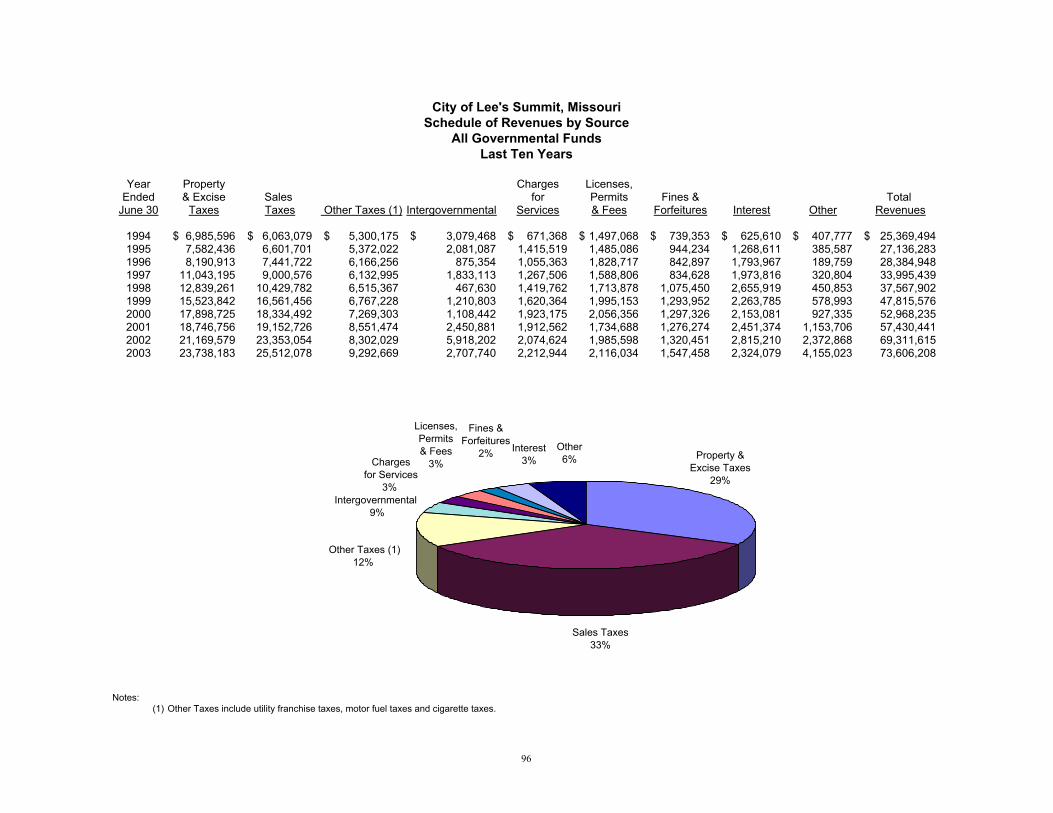

Statistical Section (Unaudited): Schedule of Expenditures by Function—All Governmental Fund Types 95 Schedule of Revenues by Source—All Governmental Funds 96 Schedule of General Fund Revenues and Other Financing Sources 97 Schedule of General Fund Expenditures and Other Financing Uses by Function 98 Property Tax Levies and Collections 99 Schedule of Revenue Bond Coverage—Combined Waterworks and

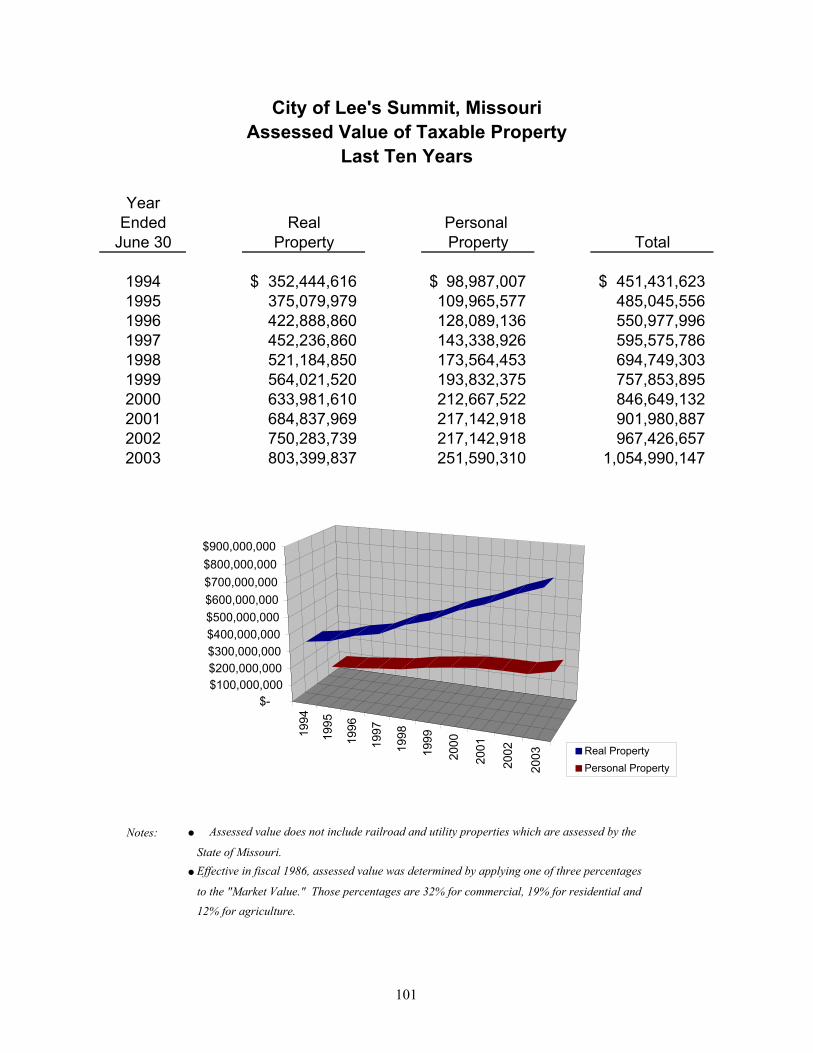

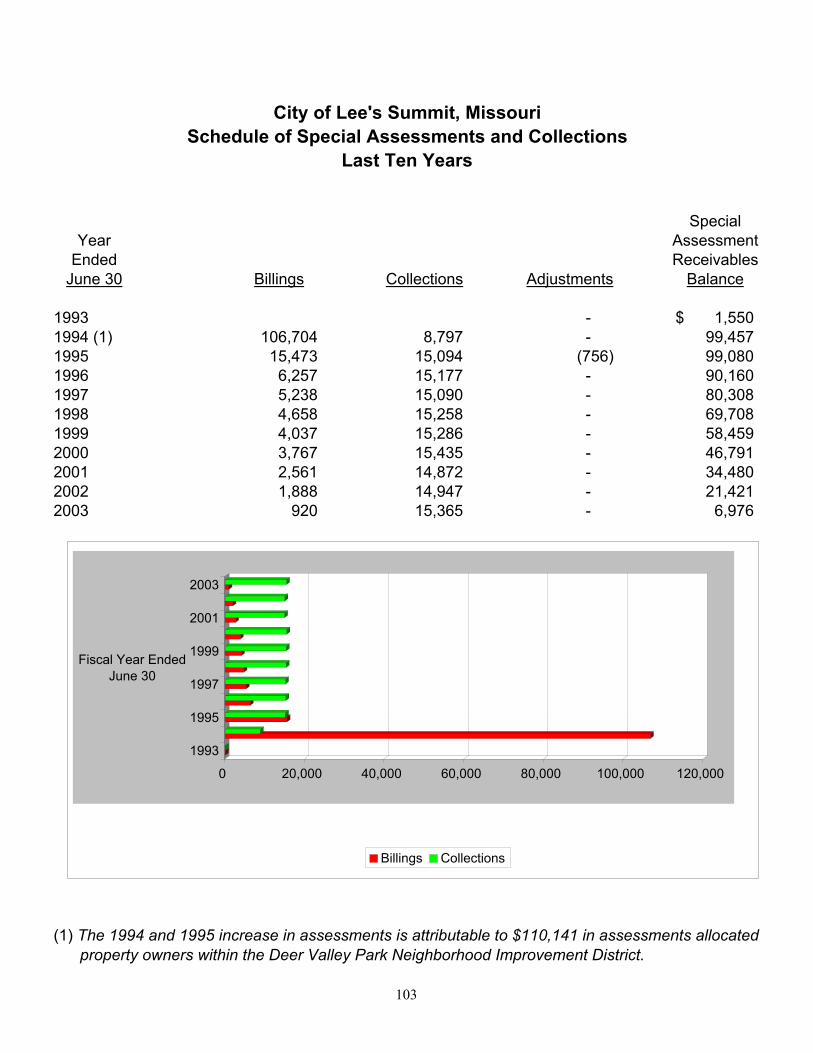

Sewerage System Fund 100 Assessed Value of Taxable Property 101 Property Tax Rates—Direct and Overlapping Governmental Units 102 Schedule of Special Assessments and Collections 103 Schedule of Construction Permits Issued 104 Computation of Legal Debt Margin 105 Computation of Direct and Estimated Overlapping Debt 106 Ratio of Annual Debt Service Expenditures for General Bonded Debt to

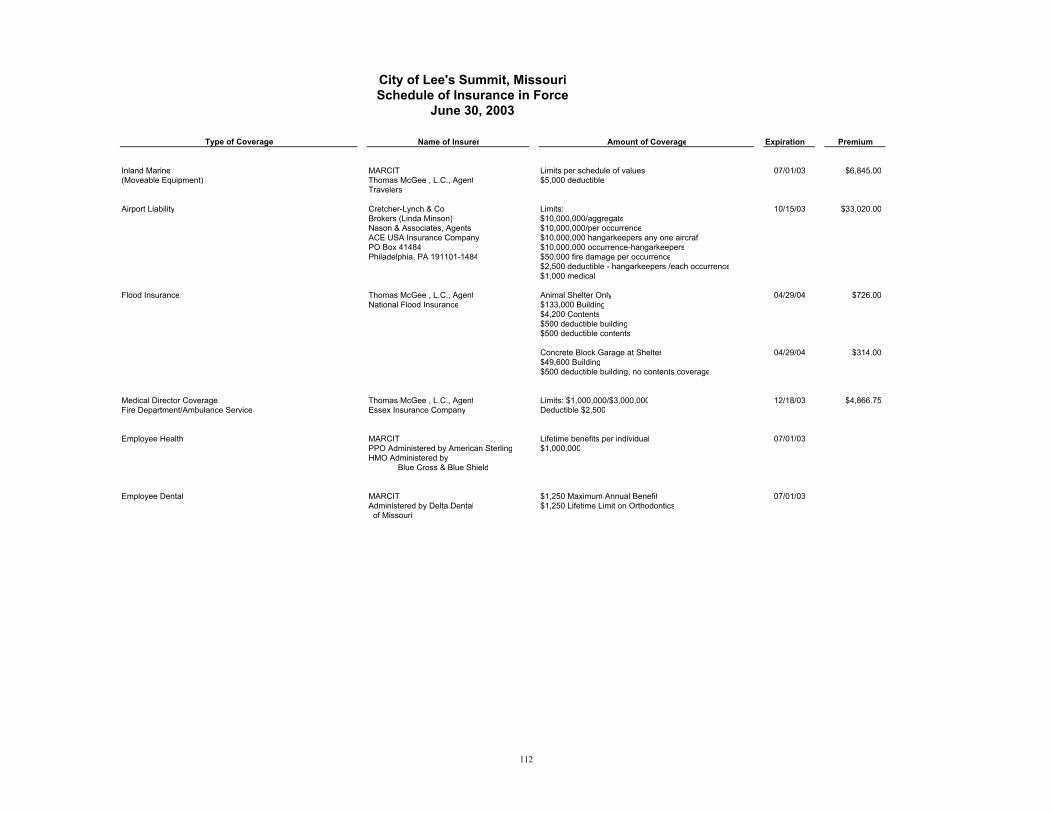

Total “General” Expenditures 107 Ratio of Net Bonded Debt to Assessed Value and Net Bonded Debt Per Capita 108 Schedule of Principal Taxpayers 109 Miscellaneous Statistics 110 Schedule of Insurance in Force 111-112

(This page left blank intentionally)

Introductory Section

________________________________________________________________________________

3

THE CITY OF LEE’S SUMMIT

MAYOR

Karen R. Messerli

DISTRICT 1 DISTRICT 3 James Hallam Joseph C. Spallo Christine Bushyhead Ed Cockrell

DISTRICT 2 DISTRICT 4 Randall L. Rhoads James Freeman III Ron Williams Tess Hurley

FINANCE & PERSONNEL COMMITTEE

James Hallam, Chairman Tess Hurley

Joseph C. Spallo Ron Williams

ADMINISTRATION Shelley Temple-Kneuvean, Acting City Administrator

Stephen A. Arbo, Assistant City Administrator Conrad E. Lamb, Finance Director

Darlene Pickett, Asst. Finance Director Thomas Solberg, Fire Chief

Robert Handley, City Attorney Kenneth T. Conlee, Police Chief

J. Thomas Lovell, Parks Administrator Charles Owsley, Public Works Director Mark Schaufler, Water Utilities Director

Robert G. McKay, Community Development Director Gary Bradley, Assistant to the City Administrator

INDEPENDENT CERTIFIED PUBLIC ACCOUNTANTS

KPMG LLP

4

City of Lee’s Summit

Parks & Recreation

Recreation Center

Swimming Pool

Parks & RecreationBoard

Human Resources Finance

Fire Police

Codes Administration Water Utilities

Planning and Development Law

Information Technology Purchasing

Fleet Operations

Street &Stormwater

SolidWaste

Airport

Public Works

OfficeOf The

City Administrator

Mayorand

City Council

MunicipalCourt

MunicipalJudges

Citizensof

Lee's Summit

(This page left blank intentionally)

6 (Continued)

December 1, 2003

The Honorable Mayor and City Councilmembers:

Transmitted herewith is the annual financial report for the City of Lee’s Summit, Missouri (the City) for the fiscal year ended June 30, 2003. The Finance Department prepared this report and responsibility for both the accuracy of the presented data and the completeness and fairness of the presentation, including all disclosures, rests with the City. We believe the data, as presented, is accurate in all material aspects; that it is presented in a manner designed to fairly set forth the financial position and results of operations of the City, as measured by the financial activity of its various funds; and that all disclosures necessary to enable the reader to gain the maximum understanding of the City’s financial affairs have been included.

The comprehensive annual financial report is presented in three sections: introductory, financial, and statistical. The introductory section includes a list of principal officials, the City’s organizational chart, this transmittal letter, and a Certificate of Achievement for Excellence in Financial Reporting. The financial section includes the auditors’ report, management’s discussion and analysis, basic and fund financial statements, notes to the basic financial statements, and required supplementary information. The statistical section includes selected financial and demographic information, generally presented on a multiyear basis.

For purposes of preparing this comprehensive annual financial report, all funds and account groups that are controlled by or dependent on, the City of Lee’s Summit are included. This comprises such services as public safety, public works, parks and recreation, water and sanitary sewerage utility, aviation and sanitary landfill disposal of refuse. Determination as to control by, or dependence on, the City is on the basis of generally accepted accounting principles which includes consideration of budget adoption, taxing authority, outstanding debt secured by revenues or general obligations of the City, or the City’s obligation to fund any deficit that may occur. Based on this criteria, all fund types which apply are included as part of this annual report. In addition, the Lee’s Summit Municipal Building Authority is included in the City’s reporting entity as a blended component unit.

GAAP requires that management provide a narrative introduction, overview, and analysis to accompany the basic financial statements in the form of Management’s Discussion and Analysis (MD&A). This letter of transmittal is designed to complement MD&A and should be read in conjunction with it. The City of Lee's Summit’s MD&A can be found immediately following the report of the independent auditors.

Profile of the Government

The City was organized on December 1, 1868 under the laws of the state of Missouri. The City became a Charter City on April 2, 1996 when voters approved the Home Rule Charter. The charter established a

7 (Continued)

government in which the City Council, consisting of eight members, two per district, elected by their respective district’s citizens, performs the legislative duties of the City. The City Council meets on the first three Thursdays of each month in regular session and has an additional “Work or Study Session” before the regular meeting on the second Thursday of each month. The executive power in the City is vested in the Mayor, who is recognized as the head of the City for all legal and ceremonial purposes. The Mayor is elected at large by the city electorate. The City Administrator is the chief administrative officer of the City. The City Administrator is appointed by the Mayor with the advice and consent of a majority of the City Council.

The City is a suburb encompassing approximately 64 square miles in the southeastern section of the Kansas City, Missouri metropolitan area. The City is well served by several interstate, federal, and state highways. Interstate 470, which rings the southeastern part of the Kansas City metropolitan area, which connects with Interstates 70 and 435, dissects the City of Lee’s Summit. In planning for the future, the City uses as a guide the Interstate 470-corridor study when looking for guidance regarding growth and land use in and along the highway system. These interstates also connect with Interstates 35 and 29, thereby giving Lee’s Summit excellent access to the entire metro area. Two federal highways, U.S. 50 and U.S. 40 and two state highways, M-291 and M-150, also connect Lee’s Summit to Kansas City and the surrounding area. Amtrak and the Missouri Pacific Railroads also serve the City. The Lee’s Summit Municipal Airport has both north/south and crosswind directional runways.

Utility service in the city is mixed between public and private companies. Water and sanitary sewerage utilities are operated by the Water Utilities Department of the City. Water and sewerage rates are established to meet the total revenue requirements of the utilities. Natural gas is supplied by the Missouri Gas Energy Company (MGE), electricity by Missouri Public Service Company (Aquila), and traditional telephone service by Southwestern Bell. There are several companies providing cellular phone service.

The four major commercial television networks, four independent local stations as well as public television and two cable television companies service the City, and a number of AM and FM stations broadcast throughout the area.

In addition to the Kansas City Star daily newspaper and its supplemental Southland Star published on Saturdays, the City is served by the Lee’s Summit Journal. The Lee’s Summit Journal is delivered on Wednesday and Friday afternoons.

Education

The City of Lee’s Summit boundaries overlap several school districts. The Lee’s Summit R-7 School District represents 92% of the total area and is classified AAA (highest rating) by the State Department of Education. The school district’s enrollment has increased from 2,928 pupils in 1960 to 14,838 in 2002. Fall 2003 enrollment saw an increase of 386 students. The school district expects similar growth to continue. The R-7 School District has 15 elementary schools, three middle schools and two high schools. Lee’s Summit West High School, located in southwest Lee’s Summit, is scheduled to open in fall 2004. The district also operates an Early Childhood Center, Parents as Teachers program, an Alternative School, and Summit Technology Academy. Within city limits, the Blue Springs School District also has an elementary school and middle school.

The Longview campus of The Metropolitan Community Colleges is located in the City and is experiencing similar growth in enrollments.

The Mid-Continent Public Library system has two facilities in Lee’s Summit, one in the east central section and one in the west central part of the City.

8 (Continued)

In addition, Lee’s Summit residents have easy access to the Kansas City metropolitan area’s 15 colleges and universities, seven community colleges, 10 technical institutes and five seminaries.

Recreation, Cultural and Religious Facilities

Lee’s Summit has 26 municipal parks covering 1,140 acres of parkland. Recreational facilities at these parks include: athletic fields for youth and adult softball, baseball and soccer, lighted tennis courts, picnic shelters, nature trails, a 50-meter swimming pool, an inline skating rink, handball/racquetball courts, basketball courts, volleyball courts, horseshoe courts, a 22,000-square-foot recreation center, two small community centers and numerous playgrounds.

The Park Board, recognizing the affects of population growth, continues to make significant improvements in the existing parks and recreation facilities. Those projects are being funded through lease purchase financing, user fees, and property taxes. As a part of their “Legacy for Tomorrow” plan, the Parks and Recreation Department was successful with a three-eighths cent sales tax question on the November 1997 ballot to fund the acquisition and construction of a 700-acre city park, neighborhood parks and the 38-mile greenway.

In July 1998, the City purchased approximately 700 acres for a multipurpose city park on the City’s eastern city limits. The park, named Legacy Park, was completed in spring 2003. Facilities at the park include a soccer complex, a boy’s baseball complex, and a girl’s softball complex. Each complex includes restroom/concession facilities, vending, parking, walkways, and landscaping. Also included in construction of this phase is realigned Blackwell Road, 1.5 miles of bikeway, lake development, environmental mitigation measures, and internal roadways.

The next phase of Legacy Park is the Legacy Park Community Center. The 53,000 square foot facility will be located on the east edge of the lake in Legacy Park. Facilities will include leisure indoor pool with slide, play features, and hot tub. Other activity areas include gymnasium, fitness center, racquetball courts, and running track. Locker rooms will include a family changing area as well as conventional locker room facilities. Community areas will include a divisible community room suitable for meetings and receptions for up to 275 people and a catering kitchen. The facility will include office space for center personnel and a baby-sitting area for patrons. The Community Center is scheduled to open in the fall of 2003

The park system is complimented by a professional park and recreation staff that provides planning, maintenance, development, administration, and recreation services. There are many different recreation programs offered throughout the year by the staff as well as through partnerships with local organizations. These opportunities include youth baseball, softball, soccer, football, inline skating, swimming, tennis, gymnastics and basketball; adult (men, women and coed) softball, soccer, basketball and volleyball; senior adult trips and tours, special classes and luncheons; musical festivals; summer day camps, safety town; and numerous instructional programs. A full range of activities for the physically and mentally challenged is made possible through a partnership with Jackson County’s Special Recreation Division.

Lake Jacomo, Longview Lake, Blue Springs Lake, and Prairie Lee Lake are located in county parks within the city limits of Lee’s Summit and offer numerous recreational activities such as boating, fishing, skiing, and swimming. Lee’s Summit residents and the Kansas City metropolitan area enjoy these lakes.

Lee’s Summit has over 50 churches of various denominations.

Commerce, Industry and Employment

The City’s commercial and industrial tax base continues to grow, along with the City’s strong housing numbers. Several commercial projects were started or completed during fiscal year 2003.

9 (Continued)

The City of Lee’s Summit has a broad spectrum of major employers. They include companies that manufacture everything from plastic containers to tools to electronic components. In addition to manufacturing, there are a wide variety of services such as customer service centers for pharmaceuticals and telecommunications firms, data management and processing centers and educational institutions. There are 17 business sites in Lee’s Summit with 200 employees or more, and 8 business sites with over 500 employees.

John Knox Village is a taxpaying retirement village for middle- and upper-income persons and is compromised of approximately 2,000 units. The village is continuously renovating many of its residential units.

The City has seen its retail sales tax base increase significantly in the past two years. The pattern of retail development in Lee’s Summit follows closely with major traffic routes. The new 800,000 square foot Summit Woods Crossing is located adjacent to US 50 Highway, just south of I-470. It includes anchor tenants such as Lowe’s, Kohl’s, Best Buy, Target, and specialty stores such as Eddie Bauer and Borders Books. Smaller centers are scattered throughout the city, generally along Highway M-291 and US 50.

Major Initiatives

The following table sets forth average annual unemployment figures for Lee’s Summit and for the state of Missouri, obtained from the Bureau of Labor Statistics, compared to national figures:

Year

Area Unemployment

Rate

Statewide Unemployment

Rate

United States Unemployment

Rate

2003 3.8% 5.8% 6.4% 2002 3.3% 5.5% 5.9% 2001 2.7% 4.8% 4.6% 2000 1.9% 3.3% 4.0% 1999 2.2% 3.8% 4.3%

The City of Lee’s Summit continues to be an active and growing community. 2,154 building permits were issued in calendar year 2002 (including alternations, additions and demolitions); this places Lee’s Summit as one of the fastest growing cities in the state of Missouri. Assessed valuations have increased an average of 13.2% yearly over the last five years.

The City’s population has grown from 28,416 in 1980, 47,253 in 1990, and to 70,700 in the 2000 census to an estimated population of 76,043 as of December 2002. The population is expected to increase an average of six citizens per day.

Capital projects of just over $40.5 million were constructed during the year using proceeds of General Obligation Bonds, Revenue Bonds, Certificates of Participation, water and sewer connection fees, transportation sales and excise taxes together with grant funds for buildings, landfill expansion, street, airport, water and sewer improvements.

Financial Information

Management of the City is responsible for establishing and maintaining internal control designed to ensure that the assets of the government are protected from loss, theft or misuse and to ensure that adequate accounting data are compiled to allow for the preparation of financial statements in conformity with generally accepted accounting principles (GAAP). The internal control is designed to provide reasonable, but not absolute, assurance that these objectives are met. The concept of reasonable assurance

10 (Continued)

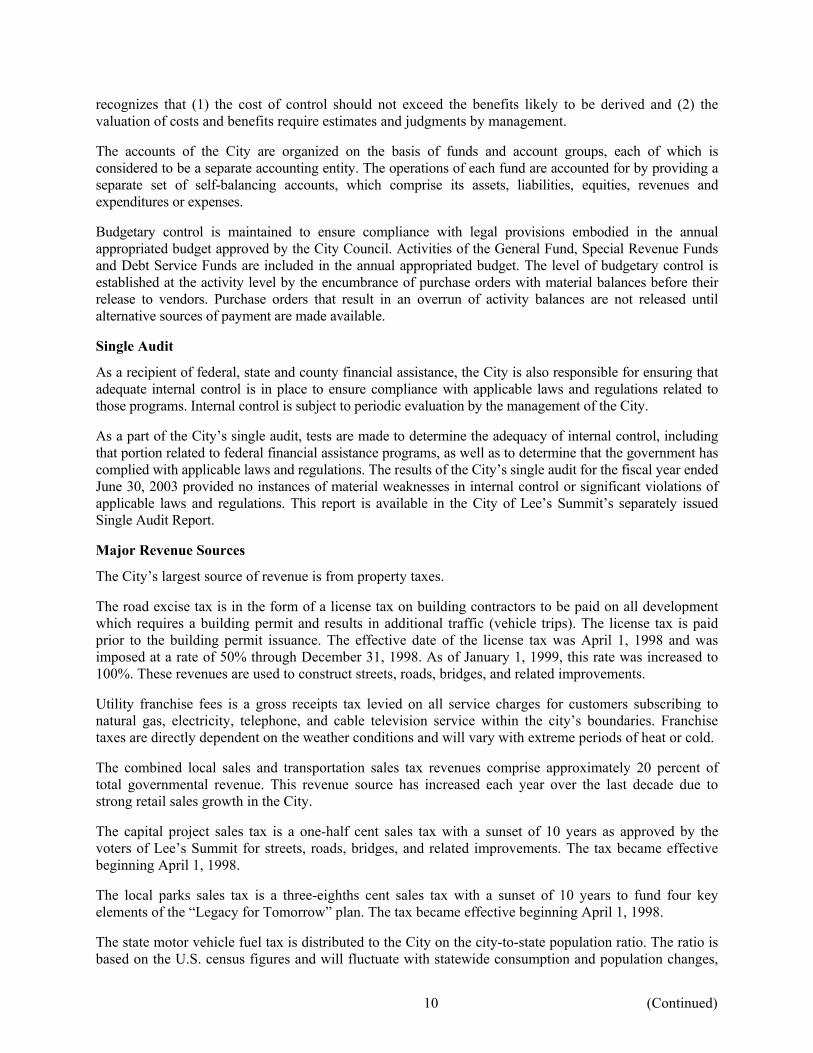

recognizes that (1) the cost of control should not exceed the benefits likely to be derived and (2) the valuation of costs and benefits require estimates and judgments by management.

The accounts of the City are organized on the basis of funds and account groups, each of which is considered to be a separate accounting entity. The operations of each fund are accounted for by providing a separate set of self-balancing accounts, which comprise its assets, liabilities, equities, revenues and expenditures or expenses.

Budgetary control is maintained to ensure compliance with legal provisions embodied in the annual appropriated budget approved by the City Council. Activities of the General Fund, Special Revenue Funds and Debt Service Funds are included in the annual appropriated budget. The level of budgetary control is established at the activity level by the encumbrance of purchase orders with material balances before their release to vendors. Purchase orders that result in an overrun of activity balances are not released until alternative sources of payment are made available.

Single Audit

As a recipient of federal, state and county financial assistance, the City is also responsible for ensuring that adequate internal control is in place to ensure compliance with applicable laws and regulations related to those programs. Internal control is subject to periodic evaluation by the management of the City.

As a part of the City’s single audit, tests are made to determine the adequacy of internal control, including that portion related to federal financial assistance programs, as well as to determine that the government has complied with applicable laws and regulations. The results of the City’s single audit for the fiscal year ended June 30, 2003 provided no instances of material weaknesses in internal control or significant violations of applicable laws and regulations. This report is available in the City of Lee’s Summit’s separately issued Single Audit Report.

Major Revenue Sources

The City’s largest source of revenue is from property taxes.

The road excise tax is in the form of a license tax on building contractors to be paid on all development which requires a building permit and results in additional traffic (vehicle trips). The license tax is paid prior to the building permit issuance. The effective date of the license tax was April 1, 1998 and was imposed at a rate of 50% through December 31, 1998. As of January 1, 1999, this rate was increased to 100%. These revenues are used to construct streets, roads, bridges, and related improvements.

Utility franchise fees is a gross receipts tax levied on all service charges for customers subscribing to natural gas, electricity, telephone, and cable television service within the city’s boundaries. Franchise taxes are directly dependent on the weather conditions and will vary with extreme periods of heat or cold.

The combined local sales and transportation sales tax revenues comprise approximately 20 percent of total governmental revenue. This revenue source has increased each year over the last decade due to strong retail sales growth in the City.

The capital project sales tax is a one-half cent sales tax with a sunset of 10 years as approved by the voters of Lee’s Summit for streets, roads, bridges, and related improvements. The tax became effective beginning April 1, 1998.

The local parks sales tax is a three-eighths cent sales tax with a sunset of 10 years to fund four key elements of the “Legacy for Tomorrow” plan. The tax became effective beginning April 1, 1998.

The state motor vehicle fuel tax is distributed to the City on the city-to-state population ratio. The ratio is based on the U.S. census figures and will fluctuate with statewide consumption and population changes,

11 (Continued)

as they become measurable. The motor vehicle license and sales tax is based on the location where the property is titled and not where the sale takes place.

The City actively applies for many federal and state pass-through grant funds that may be available. Many of these grants are designed to provide start-up funds or are for limited periods of time.

The county urban road system money is collected by Jackson County and is used to fund road and bridge projects that are maintained mutually by the City and county. This money is committed for the City’s share of county improvements to the View High Drive interchange and Colbern Road improvements completed in recent years.

Cash Management

The City pools the cash from all funds and invests these amounts in overnight accounts, certificates of deposit, mortgage-backed securities, and instruments carrying the full faith and guarantee of the federal government. The maturities of the investments range from 30 days to 3 years, with an average maturity of 20 months. The average yield on investments was 3.4 percent. Time deposits are collateralized at 105% of market value with either the City or a third party holding the collateral.

The City has executed Depository Collateral Agreements, which should satisfy the requirements of the Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA) regarding deposits in excess of FDIC insurance.

Enterprise Funds

The City operates four Enterprise Funds: the Combined Waterworks and Sewerage System, the Airport, the Solid Waste Management (Sanitary Landfill) and the Recreation Center.

These funds are used to account for operations that are financed and operated in a manner similar to private business enterprises where the stated intent is that the costs (expenses, including depreciation) of providing goods or services to the general public on a continuing basis be financed or recovered primarily through user charges and where periodic determination of revenues earned, expenses incurred and/or net income is deemed appropriate of capital maintenance, public policy, management control, accountability or other purposes.

Combined Waterworks and Sewerage System

The City’s combined Water and Sewer System revenues include water and sewer connection fees intended to fund significant capital improvement projects identified in their respective master plans. The rate structure provides a capital improvement funding mechanism to upgrade and replace existing transmission and collection lines.

The City purchases its water from the City of Independence, Missouri (54.15%) and the City of Kansas City, Missouri Water Department (45.85%). Sewage treatment is provided by the Little Blue Valley Sewer District, which charges member cities on a volume treated basis. The City of Lee's Summit represents approximately 25 percent of the Little Blue Valley metro sewer district.

Airport

The City operates the Lee’s Summit Municipal Airport, which is designated by the Federal Aviation Authority as a reliever airport for the Kansas City metropolitan area. It is designed to reduce congestion at larger air carrier airports by providing general aviation pilots with alternate landing facilities. It is further classified as a general aviation utility airport serving planes with gross weights of less than 12,500 pounds and landing speeds less than 121 knots. The airport is equipped with two runways, each approximately 4,000 feet long, and supports an estimated 103,800 takeoffs and landings of personal and business purposes per year.

12 (Continued)

Solid Waste Management (Sanitary Landfill)

The Solid Waste Management facility (Landfill) remains one of the few municipally operated sites for solid waste disposal in the Kansas City metropolitan area. The expansion of the original area should provide solid waste disposal well into the 21st century. The City provides drop-off recycling services and also is a metropolitan area household hazardous waste drop-off site for the regional program.

Recreation Center

The Recreation Center is a multipurpose recreational facility that is self-supporting for both operations and the debt service on the construction costs. The Center offers summer day camp for children, volleyball, soccer, basketball and tennis leagues and instruction, as well as numerous other activities and programs.

Awards

The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to the City of Lee’s Summit, Missouri for its comprehensive annual financial report for the fiscal year ended June 30, 2002. This was the 25th consecutive year that the government achieved this prestigious award. In order to be awarded the Certificate of Achievement, a government must publish an easily readable and efficiently organized comprehensive annual financial report. This report must satisfy both generally accepted accounting principles and applicable legal requirements.

A Certificate of Achievement is valid for a period of one year only. We believe our current report continues to meet the Certificate of Achievement Program’s requirements, and we are submitting it to the GFOA to determine its eligibility for another certificate.

In addition, the government also received the GFOA’s Distinguished Budget Presentation Award for its annual budget document beginning July 1, 2002. In order to qualify for the Distinguished Budget Presentation Award, the government’s budget document was judged to be proficient in several categories, including as a policy document, a financial plan, an operations guide, and a communications device.

Risk Management

The City is a member of the Mid-America Regional Council Insurance Trust (MARCIT). MARCIT consists of municipal and county governments located in western and central Missouri. MARCIT is a not-for-profit corporation that addresses the insurance needs for entities in the metropolitan Kansas City area.

MARCIT’s coverage includes a health/dental pool, which was started in July 1984, and a property/casualty pool, which was started in December 1984.

In addition to the insurance coverage provided by MARCIT, the City has established several risk control measures through the City Safety Committee in an effort to minimize accident-related losses.

Independent Audit

City policy requires an annual audit to be made of the financial statements of the various funds and account groups. This audit is performed by an independent certified public accounting firm selected by the City Councilmembers. The City’s auditor is KPMG LLP.

13

Acknowledgments

The preparation of this report was accomplished through the efforts of the staff of the Finance Department in cooperation with the City’s auditors, KPMG LLP. Special recognition should go to Assistant Finance Director, Darlene Pickett, for all of her hard work and coordination in compiling the City’s financial data. Our sincere thanks to all of those who assisted.

Respectfully submitted,

Shelley Temple-Kneuvean Conrad E. Lamb Acting City Administrator Finance Director

(This page left blank intentionally)

Financial Section

____________________________________________________________________________________

(This page left blank intentionally)

18 KPMG LLP, a U.S. limited liability partnership, is the U.S. member firm of KPMG International, a Swiss cooperative.

KPMG LLP 1000 Walnut, Suite 1600 P.O. Box 13127 Kansas City, MO 64106

Independent Auditors’ Report

The Honorable Mayor and Members of the City Council City of Lee’s Summit, Missouri:

We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City of Lee’s Summit, Missouri (the City), as of and for the year ended June 30, 2003, which collectively comprise the City’s basic financial statements as listed in the accompanying table of contents. These financial statements are the responsibility of the City’s management. Our responsibility is to express opinions on these financial statements based on our audit.

We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinions.

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City of Lee’s Summit, Missouri as of June 30, 2003 and the respective changes in financial position and cash flows, where applicable, thereof for the year then ended in conformity with accounting principles generally accepted in the United States of America.

As discussed in note 1 to the basic financial statements, the City adopted the provisions of the Governmental Accounting Standards Board Statement No. 34, Basic Financial Statements—and Management’s Discussion and Analysis—for State and Local Governments; Statement No. 37, Basic Financial Statements—and Management’s Discussion and Analysis—for State and Local Governments: Omnibus; Statement No. 38, Certain Financial Statement Note Disclosures; and Interpretation No. 6, Recognition and Measurement of Certain Liabilities and Expenditures in Governmental Fund Financial Statements, during the year ended June 30, 2003.

In accordance with Government Auditing Standards, we have also issued a report, dated December 1, 2003, on our consideration of the City’s internal control over financial reporting and our tests of its compliance with certain provisions of laws, regulations, contracts, and grants. That report is an integral part of an audit performed in accordance with Government Auditing Standards, and should be read in conjunction with this report in considering the results of our audit.

19

The management’s discussion and analysis, budgetary comparison information and schedule of funding progress on pages 20 through 27 and 60 through 62, respectively, are not a required part of the basic financial statements but are supplementary information required by accounting principles generally accepted in the United States of America. We have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the required supplementary information. However, we did not audit the information and express no opinion on it.

Our audit was performed for the purpose of forming an opinion on the financial statements that collectively comprise the City of Lee’s Summit’s basic financial statements. The introductory section, supplementary information, and statistical section are presented for purposes of additional analysis and are not a required part of the basic financial statements. The supplementary information has been subjected to the auditing procedures applied in the audit of the basic financial statements and, in our opinion, are fairly stated, in all material respects, in relation to the basic financial statements taken as a whole. The introductory section and statistical section have not been subjected to the auditing procedures applied in the audit of the basic financial statements and, accordingly, we express no opinion on them.

Kansas City, Missouri December 1, 2003

20 (Continued)

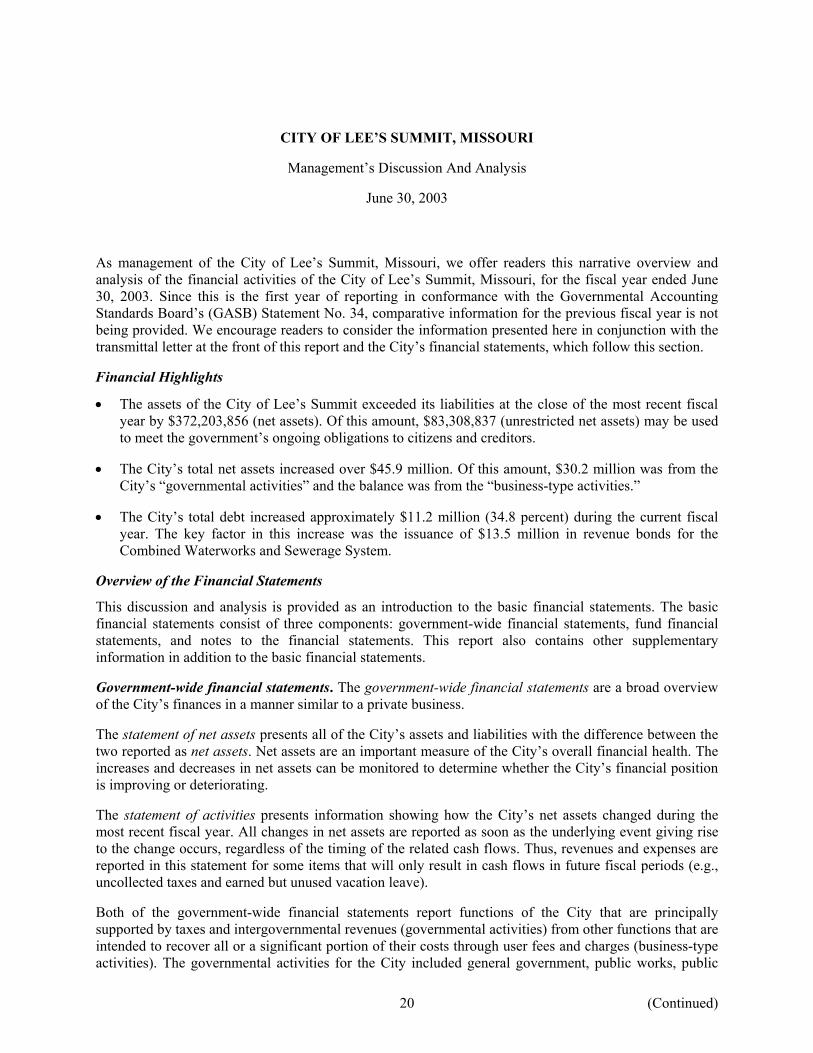

CITY OF LEE’S SUMMIT, MISSOURI

Management’s Discussion And Analysis

June 30, 2003

As management of the City of Lee’s Summit, Missouri, we offer readers this narrative overview and analysis of the financial activities of the City of Lee’s Summit, Missouri, for the fiscal year ended June 30, 2003. Since this is the first year of reporting in conformance with the Governmental Accounting Standards Board’s (GASB) Statement No. 34, comparative information for the previous fiscal year is not being provided. We encourage readers to consider the information presented here in conjunction with the transmittal letter at the front of this report and the City’s financial statements, which follow this section.

Financial Highlights

• The assets of the City of Lee’s Summit exceeded its liabilities at the close of the most recent fiscal year by $372,203,856 (net assets). Of this amount, $83,308,837 (unrestricted net assets) may be used to meet the government’s ongoing obligations to citizens and creditors.

• The City’s total net assets increased over $45.9 million. Of this amount, $30.2 million was from the City’s “governmental activities” and the balance was from the “business-type activities.”

• The City’s total debt increased approximately $11.2 million (34.8 percent) during the current fiscal year. The key factor in this increase was the issuance of $13.5 million in revenue bonds for the Combined Waterworks and Sewerage System.

Overview of the Financial Statements

This discussion and analysis is provided as an introduction to the basic financial statements. The basic financial statements consist of three components: government-wide financial statements, fund financial statements, and notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements.

Government-wide financial statements. The government-wide financial statements are a broad overview of the City’s finances in a manner similar to a private business.

The statement of net assets presents all of the City’s assets and liabilities with the difference between the two reported as net assets. Net assets are an important measure of the City’s overall financial health. The increases and decreases in net assets can be monitored to determine whether the City’s financial position is improving or deteriorating.

The statement of activities presents information showing how the City’s net assets changed during the most recent fiscal year. All changes in net assets are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of the related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods (e.g., uncollected taxes and earned but unused vacation leave).

Both of the government-wide financial statements report functions of the City that are principally supported by taxes and intergovernmental revenues (governmental activities) from other functions that are intended to recover all or a significant portion of their costs through user fees and charges (business-type activities). The governmental activities for the City included general government, public works, public

21 (Continued)

safety, planning and development, and parks and recreation. The business-type activities for the City include the combined waterworks and sewerage system, municipal airport, sanitary landfill, and recreation center.

Fund financial statements. A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The City uses fund accounting to ensure compliance with finance-related legal requirements. These funds are divided into two categories: governmental funds and proprietary funds.

Governmental funds. Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating the City’s near-term financing requirements.

Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the government’s near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities.

Proprietary funds. The City uses two different types of proprietary funds. Enterprise funds are used to report the same functions presented as business-type activities in the government-wide financial statements. Internal service funds are an accounting device used to accumulate and allocate costs internally among the City’s various functions. The City uses internal service funds to account for its fleet of vehicles and equipment, management information systems, and self-insurance activities. Because these services predominately benefit governmental rather than business-type functions, they have been included within the governmental activities in the government-wide financial statements.

Notes to the financial statements. The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements.

Other information. In addition to the basic financial statements and accompanying notes, this report also contains certain required supplementary information regarding budgetary and pension information. The combining statements for the nonmajor funds and internal service funds are presented immediately following the required supplementary information on pensions.

Government-wide Financial Analysis

In accordance with GASB Statement No. 34, the City is not required to restate prior periods for the purpose of providing comparative information. However, comparative analysis of government-wide information will be presented in future years when prior year information is available.

22 (Continued)

NET ASSETS

The following table reflects the condensed Schedule of Net Assets as of June 30, 2003:

Governmental Business-typeactivities activities Total

Current and other assets $ 99,823,986 41,121,888 140,945,874Capital assets 188,294,358 164,271,414 352,565,772

Total assets 288,118,344 205,393,302 493,511,646

Long-term liabilities outstanding 35,961,547 39,545,326 75,506,873Other liabilities 33,826,113 11,974,804 45,800,917

Total liabilities 69,787,660 51,520,130 121,307,790

Net assets:Invested in capital assets, net of debt 153,564,358 129,296,414 282,860,772Restricted 6,034,247 — 6,034,247Unrestricted 58,732,079 24,576,758 83,308,837

Total net assets $ 218,330,684 153,873,172 372,203,856

City of Lee’s Summit Net Assets

At the end of the current fiscal year, the City is able to report positive balances in all three categories of net assets, both for the government as a whole, as well as for its separate governmental and business-type activities.

The City’s combined net assets increased to $372.2 million from $326.3 million as a result of the increase in net assets reflected in the next table. The City’s unrestricted net assets for governmental activities were $58.7 million. Total unrestricted net assets were $24.6 million with the business-type activities.

By far the largest portion of the City’s net assets (76 percent) reflects its investment in capital assets (e.g. land, buildings, machinery, and equipment), less any related debt used to acquire those assets that are still outstanding. The City uses these capital assets to provide services to citizens; consequently, these assets are not available for future spending. Although the City’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities.

An additional portion of the City’s net assets (2 percent) represents resources that are subject to external restrictions on how they may be used. The remaining balance of unrestricted net assets ($83.3 million) may be used to meet the government’s ongoing obligations to citizens and creditors.

The City’s net assets increased by $45.9 million during the current fiscal year. Over one half of this increase represents the increase in governmental activities alone.

23 (Continued)

Changes in Net Assets

The following table reflects the revenues and expenses from the City’s activities for the year ended June 30, 2003:

Governmental Business-typeactivities activities Total

Revenues:Program revenues:

Charges for services $ 2,212,944 28,311,806 30,524,750Operating grants and contributions 3,198,388 — 3,198,388Capital grants and contributions — 8,765,475 8,765,475

General revenues: — Property taxes 26,612,349 — 26,612,349Sales and use taxes 24,353,572 — 24,353,572Other revenue 18,736,605 2,506,723 21,243,328

Total revenues 75,113,858 39,584,004 114,697,862

Expenses:Public works 6,055,225 — 6,055,225Public safety 20,683,212 — 20,683,212Parks and recreation 5,282,539 — 5,282,539Planning and development 748,157 — 748,157General government 11,380,283 — 11,380,283Interest on long-term debt 1,872,843 — 1,872,843Combined waterworks and sewerage system — 19,016,233 19,016,233Sanitary landfill — 1,816,037 1,816,037Airport — 1,193,449 1,193,449Recreation Center — 731,802 731,802

Total expenses 46,022,259 22,757,521 68,779,780

Increases in net assets before transfers 29,091,599 16,826,483 45,918,082Transfers 1,129,640 (1,129,640) —

Increase (decrease) in net assets 30,221,239 15,696,843 45,918,082

Net assets, beginning 188,109,445 138,176,329 326,285,774Net assets, ending $ 218,330,684 153,873,172 372,203,856

Governmental Activities

Governmental activities increased the City’s net assets by $30.2 million. Property taxes, the largest governmental category, were $26.6 million or 35.4%. For the fiscal year ended June 30, 2003, revenues totaled $114.6 million (governmental and business-type). Revenues from governmental activities totaled $75.1 million or 65.5% of the total City revenues.

24 (Continued)

Net Cost of City of Lee’s Summit Governmental Activities

Certain revenues are generated that are specific to governmental program activity. These totaled $5,411,332. The following table shows expenses and program revenues of the governmental activities for the year ended June 30, 2003:

Total costs Net costsof services of services

Public works $ 6,055,225 5,135,615Public safety 20,683,212 20,557,853Parks and recreation 5,282,539 5,107,549Planning and development 748,157 (716,444)General government 11,380,283 8,653,511Interest on long-term debt 1,872,843 1,872,843

Total $ 46,022,259 40,610,927

As previously noted, expenses from governmental activities totaled $46.0 million. However, net costs of these services were $40.6 million. The difference represents direct revenues received from charges for services of $2.2 million and operating grants and contributions of $3.2 million. Taxes and other revenues of $69.6 million were collected to cover these net costs.

Business-type Activities

Business-type activities increased the City’s net assets by $15.7 million. Key elements of this increase are as follows:

• The Combined Water and Sewerage system recorded an increase of $14.6 million in net assets for the year, which is attributed to capital contributions of $8.7 million and net revenues of $5.9 million. Charges for services increased almost 12% due to 3% water and 5% sewer rate increases designed to provide additional resources to meet debt service requirements. Revenues also increased as a result of an increase in demand due to population growth and below normal rainfall.

• The Sanitary Landfill fund recorded an increase of $500,000 in net assets for the year, which is attributed to management of costs versus revenues. Landfill operations resulted in a net income amount of $527,715. This amount is net of a transfer out to the General Fund for general and administrative expenses of $177,394 and a transfer to the Landfill Post-Closure Fund of $250,000 to fund future landfill closure costs. The City lowered tipping fees in order to remain competitive with other landfills. Daily tonnage is being closely monitored to ensure that the life of the landfill lasts well into the 21st century. The Landfill continues to fund the debt service on the General Obligation Bonds, which were issued to acquire, develop, and equip the facility. Principal payments for the year totaled $25,000, with the debt being retired in 2003.

Financial Analysis of the City’s Funds

The General Fund is the chief operating fund of the City. The fund balance of the General Fund at June 30, 2003 was $18.3 million or 50% of actual expenditures. This represents an increase of $3.1 million or a 20% increase over the previous year’s balance. The City experienced increases in sales, franchise and property taxes due to new growth. The City recognizes the need for a fund balance that can adequately absorb any downturn in economic events to avoid changes and reductions in service levels. The City Council is firmly committed to maintaining at a minimum, an amount equal to 20% of expenditures in the General Fund balance.

25 (Continued)

The Debt Service Fund ended the year with a balance of $6.0 million, a decrease of $900,000 or 13%. As of June 30, 2003, the City has issued all of the $25.8 million general obligation debt authorized by the electorate in November 1995 and 2000. The City, in accordance with these “No Tax Increase” bond elections, has held the tax levy constant and monitors fluctuations in fund balance for future no tax increase bond issues. On November 5, 2002, the voters approved another “No Tax Increase” bond issue for $37 million in general obligation bonds to provide for the construction of downtown improvements including new streets, streetscape, and a new City Hall. In addition, the bond issue approval provides for construction of a seventh fire station and related equipment, storm warning sirens, a new Animal Control Shelter and road improvements to 3rd Street from View High to Pryor. The City issued $25.5 million of these bonds in August 2003.

General Fund Budgetary Highlights

Differences between the original and the final amended budget can be summarized as follows:

• The total original expenditure budget of $38,524,000 increased to $39,162,000 (an increase of $638,000).

• The total original budget for other financing uses, net of $592,000, decreased to ($1,220,794).

Actual revenues were $2,682,000 more than budgeted. Sales tax revenue was $1,182,000 more than budgeted as a result of the continued success of the new Summit Woods shopping center. Revenue from franchise tax was $828,000 more than anticipated.

The general government budget increased $584,000 and the public works and streets budget increased $54,000. These increases were to be appropriated from the undesignated fund balance. During the year, however, revenues exceeded budgetary estimates and expenditures were less than budgetary estimates, thus eliminating the need to draw upon existing fund balance.

Capital Asset and Debt Administration

Capital Assets

The City’s investment in capital assets for its governmental and business-type activities as of June 30, 2003, amounts to $352,565,772 (net of accumulated depreciation). This investment in capital assets includes land, buildings and systems improvements, collections systems, machinery and equipment, park facilities and infrastructure. Capital assets increased $39 million during the period.

Major capital events during the current fiscal year included the following:

• Continued progress on the Tudor/Scruggs Road project from M-291 to Blackwell Parkway and related M-291 intersection improvements totaling almost $12,700,000.

• Continued progress on the Chipman Road Phase I project totaling over $2,500,000.

• Substantial completion and the opening of Legacy Park in spring 2003 totaling almost $10,175,000.

• Continued progress on the Community Center at Legacy Park totaling almost $2,900,000.

• Various system additions and improvements were completed in the Combined Waterworks and Sewerage Fund at a cost of over $9,154,000.

26 (Continued)

City of Lee’ Summit Capital Assets(amounts expressed in thousands, net of depreciation)

Governmental Business-typeactivities activities Total

2003 2002 2003 2002 2003 2002

Land $ 9,399 9,361 4,600 4,599 13,999 13,960 Construction in progress 18,275 26,734 8,674 18,003 26,949 44,737 Buildings 14,960 10,076 2,308 1,466 17,268 11,542 Improvements 13,655 1,616 147,394 124,951 161,049 126,567 Machinery and equipment 9,701 9,502 1,295 1,430 10,996 10,932 Infrastructure 122,304 105,546 — — 122,304 105,546

Total $ 188,294 162,835 164,271 150,449 352,565 313,284

These capital assets are funded by traditional bond financing, impact fees, and user charges.

Debt Administration

The City, at the end of fiscal 2003, had a total of $72 million of outstanding obligations. This was an increase of $4.6 million or 6.8% from the previous year.

The additional obligations incurred during the fiscal year were not general obligations of the City. The increase in obligations for the business-type activities funds was due to the issuance of $13.5 million in revenue bonds by the combined waterworks and sewerage fund.

City of Lee’ Summit Outstanding Debt(amounts expressed in thousands)

Governmental Business-typeactivities activities Total

2003 2002 2003 2002 2003 2002

General obligation bonds $ 18,170 22,690 — 25 18,170 22,715 Revenue bonds 865 1,050 33,805 22,439 34,670 23,489 Certificates of participation 15,695 17,480 884 914 16,579 18,394 State revolving loan fund — — 2,783 3,035 2,783 3,035

Total $ 34,730 41,220 37,472 26,413 72,202 67,633

As of June 30, 2003, the City’s total issued General Obligation (G.O.) Bonded Debt was $18,170,000 and authorized and unissued debt was $37,000,000. The City has statutory authority to issue debt equal to 20% of the City’s total assessed valuation or $210,998,031. This, less our outstanding debt, authorized and unissued debt, and available cash, leaves a legal debt margin of $160,168,203, which is 75.9% of the City’s total bonding capacity. Bonded debt, net of available debt service funds, amounted to approximately $182 per capita and represented 1.3% of the assessed value of taxable property.

General Obligation Bonds retired in fiscal year 2003 totaled $4,545,000. Of this amount, $25,000 was for landfill acquisition costs and was retired by the City’s Sanitary Landfill Fund.

The City’s most recent General Obligation Bonds have been rated Aa2 by Moody’s Investors Service. Bonds so rated are judged to be of upper grade. Factors contributing to the upgrade include a strong development pattern, favorable financial performance that reflects an expanding local economy, debt position, General Fund balance, and strong voter support.

27

The total revenue bond amount outstanding at June 30, 2003 was $34,945,000, which included $28,310,000 for the Combined Water and Sewer Utility and $5,565,000 of Water Pollution Control. Also included is $865,000 of Building and Equipment Refunding and Improvement Revenue Bonds. These bonds are payable solely from the revenue derived from the operations of the respective funds and are considered to be self-liquidating.

The Combined Water and Sewer Utility Fund retired $2,212,500 of their principal amount outstanding this year. This represents 8.8% of their operating revenues.

The City is participating in the Missouri Leveraged State Water Pollution Control Revolving Fund Program with the issuance of $9,695,000 in December 1990. The bonds are limited obligations of the State Environmental Improvement and Energy Resources Authority, secured by City bonds, and the Reserve Security in an amount equal to fifty percent (50%) of the outstanding principal. The Reserve Security is funded with amounts drawn from federal capitalization grants and state matching funds held in a reserve fund. This provides interest income that can be used to reduce the interest expense that would normally be incurred.

The City’s Combined Water and Sewer Revenue Bonds carry an A1 rating from Moody’s Investors Service.

The City has $16,590,000 in Certificates of Participation outstanding. In July 1998, the City purchased approximately 700 acres for a multipurpose city park on the City’s eastern city limits issuing $2,400,000 in certificates of participation. This debt service is structured as interest only with the principal amount paid in the tenth year. In September 2000, the City issued $955,000 in certificates of participation to acquire, construct, furnish, equip, and install improvements consisting of four airplane hangars and related site improvements at the Lee’s Summit Municipal Airport. In December of 2001, the City issued $15,080,000 in certificates of participation for Legacy Park construction and related road improvements.

Requests for Information

This financial report is designed to provide the reader a general overview of the City’s finances. Questions or requests for more information concerning any of the information provided in this report should be directed to Conrad Lamb, Finance Director, City of Lee’s Summit, PO Box 1600, 207 SW Market Street, Lee’s Summit, MO 64063.

Basic Financial Statements

____________________________________________________________________________________

CITY OF LEE’S SUMMIT, MISSOURI

Statement of Net Assets

June 30, 2003

Primary governmentGovernmental Business-type

Assets activities activities Total

Cash and investments $ 57,724,702 35,626,968 93,351,670 Property taxes receivable 24,838,504 — 24,838,504 Accounts receivable 2,792,068 3,066,406 5,858,474 Accrued interest receivable 780,420 448,756 1,229,176 Internal balances 1,839,279 (1,839,279) — Inventories 67,531 306,298 373,829 Other assets and prepaid expenses 25,481 381,292 406,773 Due from other government agencies 4,341,342 — 4,341,342 Restricted assets:

Cash and cash equivalents 7,414,659 3,131,447 10,546,106 Capital assets:

Nondepreciable 27,673,966 13,273,866 40,947,832 Depreciable, net 160,620,392 150,997,548 311,617,940

Total assets 288,118,344 205,393,302 493,511,646

Liabilities

Accounts payable and other current liabilities 9,360,527 7,530,612 16,891,139 Accrued liabilities 2,139,953 232,161 2,372,114 Deferred revenue 22,325,633 25,906 22,351,539 Liabilities payable from restricted assets

Customer deposits — 323,625 323,625 State revolving loan funds — 270,000 270,000

Long-term liabilities:Due within one year 7,340,000 1,080,000 8,420,000 Due in more than one year 28,621,547 39,545,326 68,166,873 Payable from restricted assets—

State revolving loan fund — 2,512,500 2,512,500

Total liabilities 69,787,660 51,520,130 121,307,790

Net Assets

Invested in capital assets, net of related debt 153,564,358 129,296,414 282,860,772 Restricted for:

Debt service 6,028,041 — 6,028,041 Other 6,206 — 6,206

Unrestricted 58,732,079 24,576,758 83,308,837 Total net assets $ 218,330,684 153,873,172 372,203,856

See accompanying notes to basic financial statements.

29

CITY OF LEE’S SUMMIT, MISSOURI

Statement of Activities

Year ended June 30, 2003

Net (expenses) revenues andProgram revenues changes in net assets

Operating CapitalCharges for grants and grants and Governmental Business-type

Functions/Programs Expenses services contributions contributions activities activities Total

Governmental activities:Public works $ 6,055,225 — 919,610 — (5,135,615) — (5,135,615) Public safety 20,683,212 — 125,359 — (20,557,853) — (20,557,853) Parks and recreation 5,282,539 170,603 4,387 — (5,107,549) — (5,107,549) Planning and development 748,157 — 1,464,601 — 716,444 — 716,444 General government 11,380,283 2,042,341 684,431 — (8,653,511) — (8,653,511) Interest on long-term debt 1,872,843 — — — (1,872,843) — (1,872,843)

Total governmental activities 46,022,259 2,212,944 3,198,388 — (40,610,927) — (40,610,927)

Business-type activities:Waterworks and sewerage

system 19,016,233 24,704,763 — 8,728,294 — 14,416,824 14,416,824 Sanitary landfill 1,816,037 2,533,889 — — — 717,852 717,852 Airport 1,193,449 447,665 — 37,181 — (708,603) (708,603) Recreation center 731,802 625,489 — — — (106,313) (106,313)

Total business-type activities 22,757,521 28,311,806 — 8,765,475 — 14,319,760 14,319,760 Total primary government $ 68,779,780 30,524,750 3,198,388 8,765,475 (40,610,927) 14,319,760 (26,291,167)

General revenues: Property taxes 26,612,349 — 26,612,349 Sales and use taxes 24,353,572 — 24,353,572 Franchise fees 6,853,447 — 6,853,447 License, permits, fines, and forfeitures 3,663,492 — 3,663,492 Revenues from use of money and property 2,874,493 1,606,106 4,480,599 Other revenue 5,345,173 900,617 6,245,790

Transfers 1,129,640 (1,129,640) —

Total general revenues and transfers 70,832,166 1,377,083 72,209,249

Changes in net assets 30,221,239 15,696,843 45,918,082

Net assets—beginning 188,109,445 138,176,329 326,285,774 Net assets—ending $ 218,330,684 153,873,172 372,203,856

See accompanying notes to basic financial statements.

30

CITY OF LEE’S SUMMIT, MISSOURI

Governmental Funds Balance Sheet

June 30, 2003

Road and Nonmajor TotalDebt Park Bridge Excise/ Governmental Governmental

Assets General Service Development Sales Tax Funds Funds

Pooled cash and investments $ 15,359,594 5,342,455 3,563,388 14,313,365 9,882,987 48,461,789 Receivables (net of allowance):

Accounts and other 1,361,300 — — — 1,430,768 2,792,068 Taxes 24,422,969 306,779 — — 108,756 24,838,504 Accrued interest 190,033 73,167 72,229 157,278 194,472 687,179

Due from other funds 1,946,060 — — — 10,000 1,956,060 Due from other governments 513,342 329,190 — 451,346 3,047,464 4,341,342 Inventories 1,023 — — — — 1,023 Prepaid insurance 5,183 — — — — 5,183 Other assets 4,422 — — — 7,603 12,025 Restricted cash and investments 137,690 — 5,112,043 — 2,164,926 7,414,659

Total assets $ 43,941,616 6,051,591 8,747,660 14,921,989 16,846,976 90,509,832

Liabilities and Fund Balances

Liabilities:Accounts and contracts payable $ 1,845,666 — 2,204,925 1,653,169 3,501,661 9,205,421 Salaries and wages payable 1,505,006 — — — 77,221 1,582,227 Accrued interest payable — 23,550 — — 5,288 28,838 Deferred revenue 22,325,633 — — — — 22,325,633 Due to other funds 2,149 — — — 117,100 119,249

Total liabilities 25,678,454 23,550 2,204,925 1,653,169 3,701,270 33,261,368

Fund balances:Reserved for:

Postclosure costs — — — — 1,900,201 1,900,201 Prepaids and inventories 6,206 — — — — 6,206

Unreserved:Designated for debt service — 6,028,041 — — — 6,028,041 Undesignated 18,256,956 — 6,542,735 13,268,820 — 38,068,511

Unreserved, reported in nonmajor funds:Special revenue funds — — — — 2,473,916 2,473,916 Capital projects funds — — — — 8,771,589 8,771,589

Total fund balances 18,263,162 6,028,041 6,542,735 13,268,820 13,145,706 57,248,464 Total liabilities and fund balances $ 43,941,616 6,051,591 8,747,660 14,921,989 16,846,976 90,509,832

See accompanying notes to basic financial statements.

31

CITY OF LEE’S SUMMIT, MISSOURI

Reconciliation of the Governmental Funds Balance Sheetto the Statement of Net Assets

June 30, 2003

Fund balances—total governmental funds $ 57,248,464

Capital assets used in governmental activities are not financialresources and, therefore, are not reported in the funds:

Governmental capital assets $ 213,737,006 Less accumulated depreciation (32,699,972)

181,037,034

Interest on long-term debt is not accrued in governmental funds,but rather is recognized as expenditure when due (488,000)

Internal service funds are used by management to chargethe costs of certain activities to individual funds. The assetsand liabilities of the internal service funds are included in the governmental activities in the statement of net assets 16,475,908

Long-term liabilities, including bonds payable, claims and judgements,and accrued compensated absences, are not due and payable in the current period and, therefore, are not reportedin the funds, net of unamortized premiums/discounts (35,942,722)

Net assets of governmental activities $ 218,330,684

See accompanying notes to basic financial statements.

32

CITY OF LEE’S SUMMIT, MISSOURI

Governmental Funds Statement of Revenues, Expenditures, and Changes in Fund Balances

Year ended June 30, 2003

Road and Nonmajor TotalDebt Park Bridge Excise/ Governmental Governmental

General Service Development Sales Tax Funds FundsRevenues:

Taxes:Property $ 15,072,289 5,143,676 — — 4,808,756 25,024,721 Sales 9,310,409 3,338,963 — 4,654,792 7,049,408 24,353,572 Franchise 6,853,447 — — — — 6,853,447 License tax — — — 1,587,628 — 1,587,628

Intergovernmental 684,431 — 4,387 — 2,509,570 3,198,388 Charges for services 2,042,341 — — — 170,603 2,212,944 Licenses and permits 1,939,017 — — — 177,017 2,116,034 Fines and forfeitures 1,491,763 39,978 — — 15,717 1,547,458 Interest 706,593 246,117 373,561 596,614 597,135 2,520,020 Other 947,391 2,656 89,000 67,712 3,600,414 4,707,173

Total revenues 39,047,681 8,771,390 466,948 6,906,746 18,928,620 74,121,385

Expenditures:Current:

General government 7,456,919 — — — 1,336,674 8,793,593 Public works and streets 6,987,552 — — — — 6,987,552 Public safety 20,882,050 — — — — 20,882,050 Planning and development 748,157 — — — — 748,157 Parks and recreation — — — — 2,411,972 2,411,972

Debt service:Principal retirements — 6,305,000 — — 185,000 6,490,000 Interest and fiscal charges — 1,861,813 1,783 — 97,997 1,961,593

Capital outlay:General government 500,000 — — — 4,422 504,422 Public works and streets — — — 5,804,767 18,028,990 23,833,757 Public safety — — — — 18,510 18,510 Parks and recreation — — 6,389,172 — 5,124 6,394,296

Total expenditures 36,574,678 8,166,813 6,390,955 5,804,767 22,088,689 79,025,902

Excess (deficiency) of revenuesover (under) expenditures 2,473,003 604,577 (5,924,007) 1,101,979 (3,160,069) (4,904,517)

Other financing sources (uses):Transfers in 1,855,345 2,095,216 3,641,835 2,945,114 1,293,419 11,830,929 Transfers out (1,238,794) (3,604,938) (2,095,216) — (4,038,487) (10,977,435)

Total other financing sourcesand uses, net 616,551 (1,509,722) 1,546,619 2,945,114 (2,745,068) 853,494

Net change in fund balances 3,089,554 (905,145) (4,377,388) 4,047,093 (5,905,137) (4,051,023)

Fund balances—beginning 15,173,608 6,933,186 10,920,123 9,221,727 19,050,843 61,299,487 Fund balances—ending $ 18,263,162 6,028,041 6,542,735 13,268,820 13,145,706 57,248,464

See accompanying notes to basic financial statements.

33

CITY OF LEE’S SUMMIT, MISSOURI

Reconciliation of the Change in Fund Balancesof Governmental Funds to the Statement of Activities

June 30, 2003

Net change in fund balances—total governmental funds $ (4,051,023)

Amounts reported for governmental activities in thestatement of activities is different because:

Governmental funds report capital outlays as expenditures. However, inthe statement of activities the cost of those assets is allocated overtheir estimated useful lives and reported as depreciation expense. Thefollowing is the detail of the amount by which capital outlays exceededdepreciation in the current period:

Capital outlay $ 30,750,985 Less: capital outlay not capitalized (182,005)

Capital outlay capitalized 30,568,980

Depreciation (4,334,943)

26,234,037

The issuance of long-term debt (e.g., bonds, loan, leases) provides currentfinancial resources to governmental funds, while the repayment of theprincipal of long-term debt consumes the current financial resourcesof governmental funds. Also, governmental funds report the effect of issuance costs, premiums, discounts, and similar items when debt is first issued, whereas these amounts are deferred and amortized in the statement of activities. In the statement of activities, interest is accruedon outstanding bonds, whereas in the governmental funds, an interestexpenditure is reported when due. The following is the detail of the neteffect of these differences in the treatment of long-term debt andrelated items:

Repayment of principal (bonds, loans, capitalized lease obligations) 6,490,000 Claims and judgments 500,000 Compensated absences (124,095) Interest 88,750

6,954,655

Internal service funds are used by management to charge the costsof various activities internally to individual funds. The net expenseof certain activities of internal service funds is reported withgovernmental activities. 1,083,570

Change in net assets of governmental activities $ 30,221,239

See accompanying notes to basic financial statements.

34

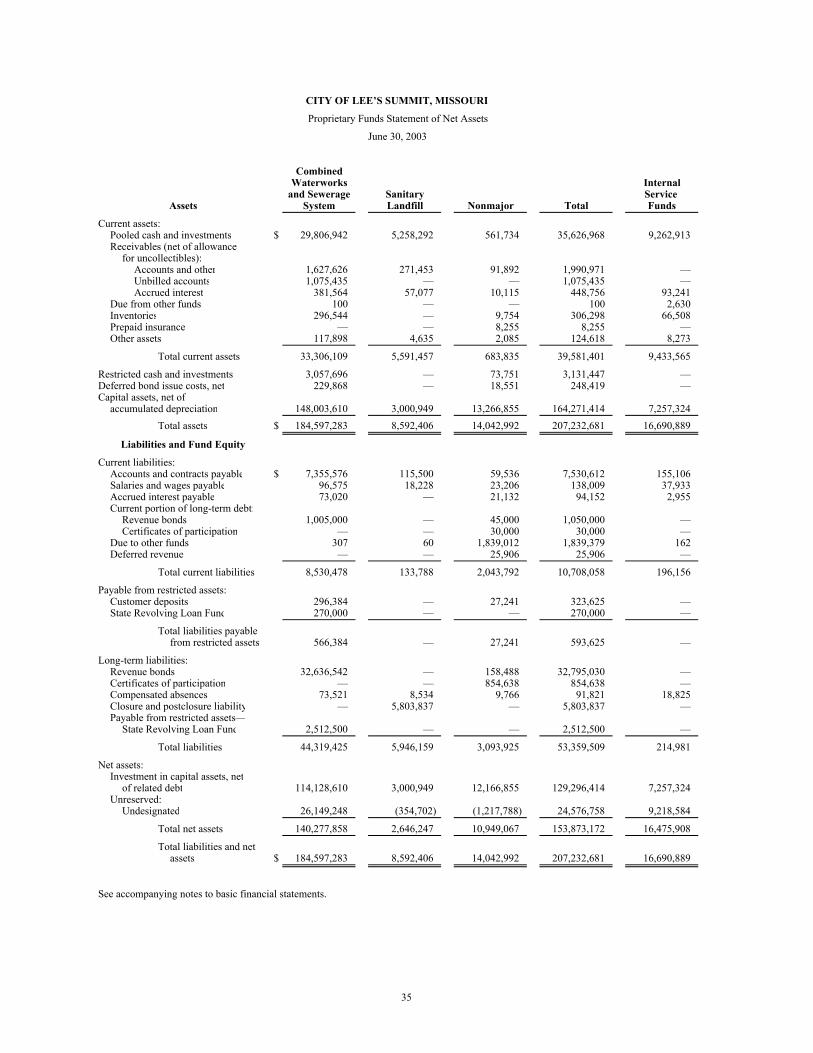

CITY OF LEE’S SUMMIT, MISSOURI

Proprietary Funds Statement of Net Assets

June 30, 2003

CombinedWaterworks Internal

and Sewerage Sanitary Service Assets System Landfill Nonmajor Total Funds

Current assets: Pooled cash and investments $ 29,806,942 5,258,292 561,734 35,626,968 9,262,913

Receivables (net of allowance for uncollectibles):

Accounts and other 1,627,626 271,453 91,892 1,990,971 — Unbilled accounts 1,075,435 — — 1,075,435 — Accrued interest 381,564 57,077 10,115 448,756 93,241

Due from other funds 100 — — 100 2,630 Inventories 296,544 — 9,754 306,298 66,508 Prepaid insurance — — 8,255 8,255 — Other assets 117,898 4,635 2,085 124,618 8,273

Total current assets 33,306,109 5,591,457 683,835 39,581,401 9,433,565

Restricted cash and investments 3,057,696 — 73,751 3,131,447 — Deferred bond issue costs, net 229,868 — 18,551 248,419 — Capital assets, net of

accumulated depreciation 148,003,610 3,000,949 13,266,855 164,271,414 7,257,324 Total assets $ 184,597,283 8,592,406 14,042,992 207,232,681 16,690,889

Liabilities and Fund Equity

Current liabilities:Accounts and contracts payable $ 7,355,576 115,500 59,536 7,530,612 155,106 Salaries and wages payable 96,575 18,228 23,206 138,009 37,933 Accrued interest payable 73,020 — 21,132 94,152 2,955 Current portion of long-term debt:

Revenue bonds 1,005,000 — 45,000 1,050,000 — Certificates of participation — — 30,000 30,000 —

Due to other funds 307 60 1,839,012 1,839,379 162 Deferred revenue — — 25,906 25,906 —

Total current liabilities 8,530,478 133,788 2,043,792 10,708,058 196,156

Payable from restricted assets:Customer deposits 296,384 — 27,241 323,625 — State Revolving Loan Fund 270,000 — — 270,000 —

Total liabilities payablefrom restricted assets 566,384 — 27,241 593,625 —

Long-term liabilities:Revenue bonds 32,636,542 — 158,488 32,795,030 — Certificates of participation — — 854,638 854,638 — Compensated absences 73,521 8,534 9,766 91,821 18,825 Closure and postclosure liability — 5,803,837 — 5,803,837 — Payable from restricted assets—

State Revolving Loan Fund 2,512,500 — — 2,512,500 —

Total liabilities 44,319,425 5,946,159 3,093,925 53,359,509 214,981

Net assets:Investment in capital assets, net

of related debt 114,128,610 3,000,949 12,166,855 129,296,414 7,257,324 Unreserved:

Undesignated 26,149,248 (354,702) (1,217,788) 24,576,758 9,218,584

Total net assets 140,277,858 2,646,247 10,949,067 153,873,172 16,475,908

Total liabilities and netassets $ 184,597,283 8,592,406 14,042,992 207,232,681 16,690,889

See accompanying notes to basic financial statements.

35

CITY OF LEE’S SUMMIT, MISSOURI

Proprietary Funds Statement of Revenues, Expenses, and Changes in Fund Net Assets

Year ended June 30, 2003

CombinedWaterworks Internal

and Sewerage Sanitary Service System Landfill Nonmajor Total Funds

Operating revenues: Charges for services $ 24,704,763 2,533,889 1,073,154 28,311,806 4,386,351 Material sales 163,299 — — 163,299 —

Fuel sales — — 474,695 474,695 — Other 131,988 7,903 122,732 262,623 47,256

Total operating revenues 25,000,050 2,541,792 1,670,581 29,212,423 4,433,607

Operating expenses:Salaries, wages, and employee

benefits 3,141,431 678,266 759,790 4,579,487 1,008,251 Water purchases 4,591,804 — — 4,591,804 — Sewer services 3,530,560 — — 3,530,560 — Maintenance and repairs 375,516 177,362 86,482 639,360 209,603 Utilities 394,466 11,243 49,352 455,061 74,095 Fuels and lubricants 40,879 66,227 347,807 454,913 1,652 Depreciation and amortization 2,912,394 116,960 284,735 3,314,089 2,063,461 Post-closure expense — 277,994 — 277,994 — Other 1,815,483 487,197 305,712 2,608,392 915,709

Total operating expenses 16,802,533 1,815,249 1,833,878 20,451,660 4,272,771

Operating income (loss) 8,197,517 726,543 (163,297) 8,760,763 160,836

Nonoperating revenues (expenses):Interest income 1,354,461 229,354 22,291 1,606,106 354,473 Interest expense (2,205,607) (788) (91,373) (2,297,768) — Gain (loss) on disposal of capital assets (8,093) — — (8,093) 292,115 Grant reimbursements — — 37,181 37,181 —

Total nonoperating revenues (expenses) (859,239) 228,566 (31,901) (662,574) 646,588

Net income (loss) beforetransfers and contributedcapital 7,338,278 955,109 (195,198) 8,098,189 807,424

Contributed capital 8,728,294 — — 8,728,294 — Transfers in — — 830,000 830,000 276,146 Transfers out (1,443,048) (427,394) (89,198) (1,959,640) —

Net income 14,623,524 527,715 545,604 15,696,843 1,083,570

Total net assets—beginning of year 125,654,334 2,118,532 10,403,463 138,176,329 15,392,338 Total net assets—end of year $ 140,277,858 2,646,247 10,949,067 153,873,172 16,475,908

See accompanying notes to basic financial statements.

36

CITY OF LEE’S SUMMIT, MISSOURI

Proprietary Funds Statement of Cash Flows

Year ended June 30, 2003

Enterprise Funds Combined

Waterworks Internaland Sewerage Sanitary Service

System Landfill Nonmajor Total Funds

Cash flows from operating activities:Cash received from customers $ 24,958,373 2,700,444 1,545,500 29,204,317 4,386,351 Cash paid to suppliers (3,139,054) (672,246) (1,201,342) (5,012,642) (1,197,700) Cash paid to employees (5,370,837) (1,006,710) (763,466) (7,141,013) (1,011,171) Other cash paid for nonoperating expenses 131,988 7,903 122,732 262,623 9,777

Net cash provided by (used in) operating activities 16,580,470 1,029,391 (296,576) 17,313,285 2,187,257

Cash flows from noncapital financing activities:Transfers in — — 830,000 830,000 276,146 Transfers out (1,443,048) (427,394) (89,198) (1,959,640) —

Net cash provided by (used in) noncapital financing activities (1,443,048) (427,394) 740,802 (1,129,640) 276,146

Cash flows from capital and related financing activities:Principal payments on long-term debt (2,212,500) (25,000) (75,000) (2,312,500) — Proceeds from issuance of long-term debt 13,500,000 — — 13,500,000 — Interest paid on long-term debt obligations (2,228,008) (1,050) (92,525) (2,321,583) — Additions to capital assets (9,635,959) (696,920) (4,198) (10,337,077) (1,208,443) Increase in payables from restricted assets 79,069 — — 79,069 — Capital contributions 1,833,182 — — 1,833,182 — Proceeds from sale of capital assets — — — — 298,839

Net cash provided by (used in) capital and related financing activities 1,335,784 (722,970) (171,723) 441,091 (909,604)

Cash flows from investing activities:Interest received 1,286,599 228,609 15,310 1,530,518 338,871

Net cash provided by investing activities 1,286,599 228,609 15,310 1,530,518 338,871

Net increase in cash and cash equivalents 17,759,805 107,636 287,813 18,155,254 1,892,670

Cash and cash equivalents, beginning of year 15,104,833 5,150,656 347,672 20,603,161 7,370,243 Cash and cash equivalents, end of year $ 32,864,638 5,258,292 635,485 38,758,415 9,262,913

Reconciliation of operating income (loss) to net cash provided(used) by operating activities:

Operating income (loss) $ 8,197,517 726,543 (163,297) 8,760,763 160,836 Adjustments to reconcile operating income (loss) to net

cash provided by operating activities:Depreciation and amortization 2,912,394 116,960 284,735 3,314,089 2,063,461 Other nonoperating expenses 8,093 — — 8,093 — (Increase) decrease in:

Inventories 2,301 — 52 2,353 (40,139) Accounts receivable (221,580) 51,693 (4,312) (174,199) — Due from other government agencies 322,238 — — 322,238 — Due from other funds 900 — — 900 (13) Unbilled revenue (30,267) — — (30,267) — Prepaid expenses 8,627 (342) (1,044) 7,241 3,764

Increase (decrease) in:Accounts payable 5,377,871 13,313 (7,152) 5,384,032 3,346 Salaries and wages payable (616) 6,020 (3,676) 1,728 (2,920) Customer deposits — — 2,994 2,994 — Due to other funds (1) — (405,283) (405,284) — Accrued landfill closure/postclosure care costs — 113,460 — 113,460 — Estimated liability for incurred but unreported claims — — — — 13 Accrued compensated absences 2,993 1,744 407 5,144 (1,091)

Total adjustments 8,382,953 302,848 (133,279) 8,552,522 2,026,421

Net cash provided by (used in) operating activities $ 16,580,470 1,029,391 (296,576) 17,313,285 2,187,257

See accompanying notes to basic financial statements.

37

CITY OF LEE’S SUMMIT, MISSOURI

Notes to Basic Financial Statements

June 30, 2003

(Continued) 38

(1) Summary of Significant Accounting Policies

(a) Reporting Entity

The City of Lee’s Summit, Missouri (the City) was incorporated in 1868 and covers an area of approximately 64 square miles in Jackson and Cass Counties, Missouri. Lee’s Summit is a charter city operating under an elected Mayor-City Council form of government. The City Administrator is the chief administrative officer of the City. The City provides services to more than 70,000 residents in many areas, including law enforcement, fire protection, water and sewer services, community enrichment and development, and various social services. Educational services are provided by separate governmental entities.

The accounting and reporting policies of the City conform to accounting principles generally accepted in the United States of America (GAAP) applicable to local governments. The following represent the more significant accounting and reporting policies and practices of the City.