competitive alternatives, 2014

TRANSCRIPT

Competitive

Alternatives

KPMG’s Guide to International

Business Location Costs

Volume II Report – 2014 Edition

competitivealternatives.com

Corporate Sponsors

KPMG LLP, in association with MMK Consulting Inc., has conducted an analysis of the relative costs of doing business in 10 countries in North America, Europe, and Asia Pacific. This report was made possible through the support of our research contributors and sponsors, as identified in this report.

The analysis in this publication is based on cost information collected primarily between July 2013 and January 2014. Taxes reflect tax rates in effect on January 1, 2014, and also incorporate any announced changes at that time to take effect at specified later dates. Exchange rates and other cost factors will, of course, change over time. Tax rates and other tax-related information are also subject to change as a result of new legislation, judicial decisions, and administrative pronouncements.

All information provided is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation.

© 2014 MMK Consulting Inc. All rights reserved.

No part of this publication may be reproduced, reprinted, stored in a retrieval system, or transmitted, in part or whole, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the authors.

Electronic copies of this report, as well as additional information in respect of this report, are available at CompetitiveAlternatives.com.

Competitive Alternatives

KPMG’s Guideto

International Business Location Costs

2014 Edition

Volume II: Appendices

Appendices

A. Details of Study Methodology...........................................................A.1 to A.6Discusses the study methodology and key business model assumptions underlying the analysis contained in this report.

B. Tax Assumptions and Comparisons..................................................B1. to B.22Presents the tax rate assumptions used for each location in the comparative analysis, along with summary measures of tax burden resulting from the analysis.

C. Other Competitiveness Factors: Regional Data and Data Source Notes..............................................................................C.1 to C.8Contains detailed regional and local data, along with detailed data source notes to support the analysis of other competitiveness factors presented in Chapter 6 of the study report.

D. Selected Bibliography and Sources of Data.....................................D.1 to D.15Contains a listing of sources used in respect of each city to gather recent data for input to this study.

Appendix ADetails of Study Methodology

© 2014 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The value of any major study depends on the quality of the study design, the data assembled, and the analytical methodology. This appendix provides further details of the methodology of the Competitive Alternatives study, including:

� Design of the Competitive Alternatives Cost Model

� Identification of the key location-sensitive cost components

� Definition of the standard business operations

� Specification of common business model assumptions

� Methodology for estimating labor costs

� Methodology for estimating transportation/distribution costs for each operation

� Methodology for estimating taxes.

Competitive Alternatives

Cost Model

This report utilizes the Competitive Alternatives Cost Model, a proprietary model which can analyze costs for businesses in many different types of business operations across multiple geographic locations.

The model uses two streams of information:

� Standardized operating specifications for each business operation

� Current business investment and operating cost data for each location.

By combining this information for each operation and location, the model produces pro forma estimates of annual costs and cash flows for a new business facility in each location. Outputs from the Cost Model include standard financial and project evaluation reports including:

� Ten-year income statements

� Ten-year balance sheets

� Ten-year cash flow statements

� Net present value of cash flows

� Corporate income tax calculations.

These reports form the basis of the cost comparisons contained in this report. The result is a snapshot of business costs in each location, scaled relative to the significance of each cost item during the establishment, ramp-up, and full operation phases of a new business operation, over ten years.

Standard Business Operations

As described in Chapter 4, 19 industry-specific standard business operations were specified for analysis in this report. These business operations have been defined according to a number of standard investment and operating specifications, including:

� Land and building requirements

� Machinery and equipment requirements

� Inventory

� Financing (debt/equity) and working capital requirements

� Annual sales revenues

� Workforce requirements

� Raw material and component inputs

� Research and development expenditures

� Electricity and natural gas requirements

� Product distribution requirements.

Summaries of the standardized parameters for each of the 19 industry-specific business operations can be found online at CompetitiveAlternatives.com/industries.

Competitive Alternatives, 2014 EditionA . 2

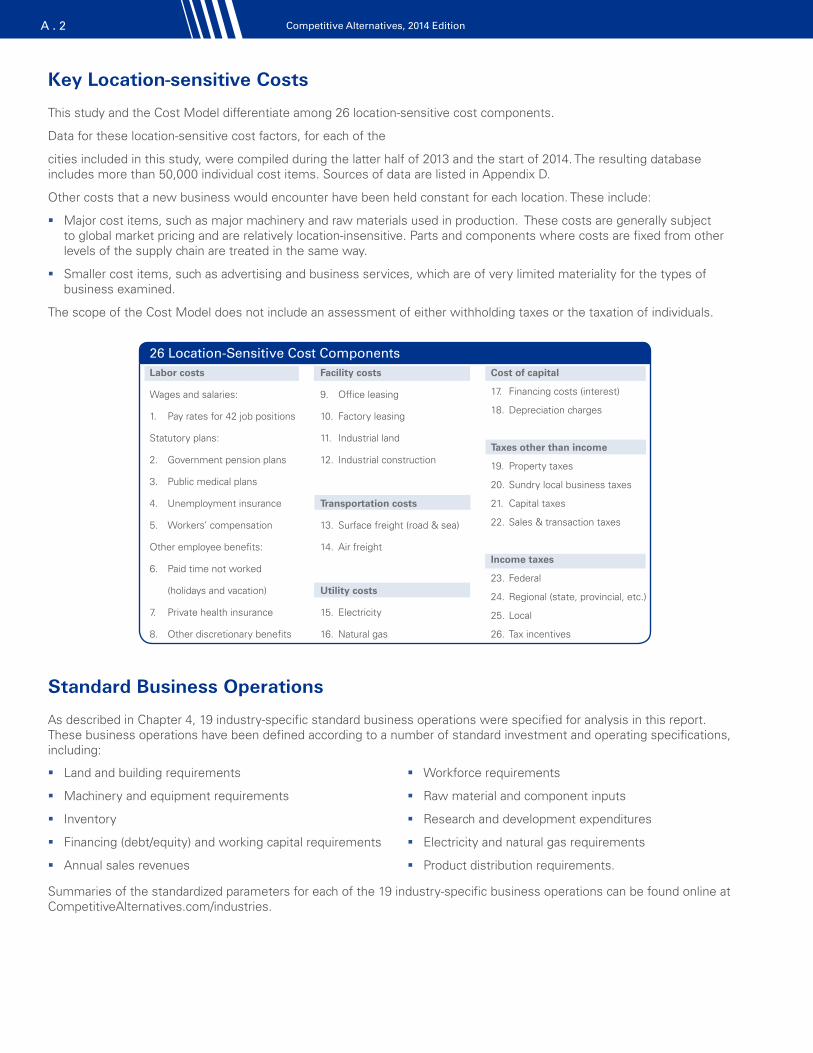

Key Location-sensitive Costs

This study and the Cost Model differentiate among 26 location-sensitive cost components.

Data for these location-sensitive cost factors, for each of the

cities included in this study, were compiled during the latter half of 2013 and the start of 2014. The resulting database includes more than 50,000 individual cost items. Sources of data are listed in Appendix D.

Other costs that a new business would encounter have been held constant for each location. These include:

� Major cost items, such as major machinery and raw materials used in production. These costs are generally subject to global market pricing and are relatively location-insensitive. Parts and components where costs are fixed from other levels of the supply chain are treated in the same way.

� Smaller cost items, such as advertising and business services, which are of very limited materiality for the types of business examined.

The scope of the Cost Model does not include an assessment of either withholding taxes or the taxation of individuals.

Standard Business Operations

As described in Chapter 4, 19 industry-specific standard business operations were specified for analysis in this report. These business operations have been defined according to a number of standard investment and operating specifications, including:

26 Location-Sensitive Cost ComponentsLabor costs

Wages and salaries:

1. Pay rates for 42 job positions

Statutory plans:

2. Government pension plans

3. Public medical plans

4. Unemployment insurance

5. Workers’ compensation

Other employee benefits:

6. Paid time not worked

(holidays and vacation)

7. Private health insurance

8. Other discretionary benefits

Facility costs

9. Office leasing

10. Factory leasing

11. Industrial land

12. Industrial construction

Transportation costs

13. Surface freight (road & sea)

14. Air freight

Utility costs

15. Electricity

16. Natural gas

Cost of capital

17. Financing costs (interest)

18. Depreciation charges

Taxes other than income

19. Property taxes

20. Sundry local business taxes

21. Capital taxes

22. Sales & transaction taxes

Income taxes

23. Federal

24. Regional (state, provincial, etc.)

25. Local

26. Tax incentives

� Land and building requirements

� Machinery and equipment requirements

� Inventory

� Financing (debt/equity) and working capital requirements

� Annual sales revenues

� Workforce requirements

� Raw material and component inputs

� Research and development expenditures

� Electricity and natural gas requirements

� Product distribution requirements.

Summaries of the standardized parameters for each of the 19 industry-specific business operations can be found online at CompetitiveAlternatives.com/industries.

KPMG’s Guide to International Business Location Costs A . 3

Business Model Assumptions

Common Assumptions: Startup Phase � All figures are shown in current US dollars, unless

another currency is specified.

� For each type of facility, the following items are assumed to be identical in each location: - Physical requirements for buildings and land - Machinery and equipment investments - Working capital requirements, including inventory

levels - Cost of equity capital - Debt-to-equity ratio at start-up.

� Expenditures for land (if any) occur in Year 0. Real estate transfer taxes are capitalized in the cost of land.

Common Assumptions: Operating Phase � All figures are shown in current US dollars, unless

another currency is specified.

� There is a ramp-up period of up to four years before operations reach full capacity.

� For each type of facility, the following items are assumed to be identical in each location: - Volume of output - Staffing requirements - Industrial and/or office leasing requirements - Electricity and natural gas requirements - Research and development activities - Cost of equity capital.

� All of the firm’s business income is related to operations.

� For profit center operations, sales revenue is held constant for all locations. For cost center operations, revenue is determined using a “cost-plus” markup approach; with the markup percentage held constant for all locations.

� All revenues earned and expenses incurred in a given period are collected and paid in the same period.

� Net cash flow from operations is added to cash on the balance sheet.

� Additional capital expenditures for retooling are undertaken as required by the type of business operation.

� Costs for materials and other location-insensitive costs are based on a predetermined percentage of sales, split between direct and indirect costs in accordance with general accounting principles. These percentages vary with the business type. For cost center operations, where revenue is a function of costs, location-insensitive costs are fixed in US$ per annum for all locations.

� The firm is a start-up, stand-alone, limited company.

� For the purposes of apportionment of taxable income in North America, the firm is assumed to be eligible to apportion income among states, but not to maintain a substantial portion of its physical business operations in any location other than the location being examined. The firm is also assumed not to be subject to a material level of taxation in any jurisdiction other than its main location.

� For North American operations, the company does not qualify as an S-Corporation in the United States or a Canadian-Controlled Private Corporation in Canada, and does not receive the preferential tax treatment accorded to those categories of company.

� For the purposes of net present value calculations, at the end of Year 10, residual value is measured as: - Current assets (including inventory), at cost; plus - Land, at historical cost; plus - Buildings, at depreciated historical cost; less - All liabilities at face value.

� Machinery and equipment are assumed to have zero scrap value, and no taxable capital gains are realized on the sale of capital assets.

� Calculations over the 10 years of operation are made on the basis of current (2013-14) price levels, exchange rates, tax structures, and cost factors. However, where future tax changes have been announced, such future changes are reflected in the calculations.

� Four depreciable asset classes are recognized: buildings, machinery and equipment, office equipment, and R&D equipment. Major initial investments in all asset classes are made in Year 0.

� An initial investment in inventory is made in Year 0. Average inventory levels are assumed to remain steady over the 10-year period.

� The initial investment is partially financed with debt. Debt servicing costs are treated as expenses in the year incurred. No net principal payments are assumed during the 10-year period, so the level of debt remains constant.

Competitive Alternatives, 2014 EditionA . 4

Transportation/Distribution Costs

A product distribution pattern has been developed for each relevant operation to reflect the characteristics of, and markets for, the goods produced. Product distribution has been based on global, continental, national, or regional markets.

Overseas exports are assumed to be transported by sea freight, except in the case of higher value products with shorter life cycles, in which case air freight may be used.

Food Processing OperationIn developing the product distribution model for the food processing industry, the tendency for food product markets to be somewhat country-specific due to different taste preferences among regions has been considered. As a result, this model assumes that 50 percent of product is sold to distributors in the region in which it is produced, with the remainder being distributed to global markets.

Advanced Batteries, Auto Parts, Metal Machining, Plastic Products, and Precision Components OperationsPlants manufacturing advanced battery systems, auto parts, metal components, plastic products, and precision components are generally producing for industrial customers who will use these components in further value-added manufacturing. Production of such components have become increasingly globalized over the last decade, but still with a tendency for producers to locate close to one or more of their major customers.

In the distribution models for these operations, output is assumed to be distributed to customers globally. Global sales are weighed using Gross Fixed Capital Formation as a proxy for industrial capacity and demand in each country. To allow for the local presence of major customers, this measure is double-weighted on favor of the region of production.

Electronics Assembly, Medical Devices, Pharmaceuticals, Specialty Chemicals, and Telecom Equipment OperationsMarkets for these products tend to be continent-wide, as a minimum, with many firms selling on a global basis In the distribution models for these operations, output is assumed to be distributed to customers globally. Global sales are weighted by a combination of population (to reflect personal consumption demand) and Gross Fixed Capital Formation (to reflect industrial consumption demand). To allow for the local presence of major customers, this measure is double-weighted in favor of the region of production.

Aircraft Parts OperationMarkets for these products tend to be focused on the regions surrounding major aircraft assembly plants, such as the North American Boeing plants in Seattle and Wichita, and Bombardier plant in Montreal; the European Airbus plants in Toulouse, Hamburg, and Broughton; and the Brazilian Embraer plant near Sao Paulo.

Distribution for aircraft parts is assumed to occur on the following basis:

� 60 percent to major aircraft assembly plants in Europe (25 percent), North America (25 percent), and South America (10 percent)

� 40 percent exported equally among eight broad global regions, as parts used by maintenance, repair and overhaul operations.

Other OperationsThe remaining operations are all services operations and have no physical product distribution requirements:

� Biomedical R&D

� Clinical trials management

� Electronics systems testing

� International financial services

� Shared services center

� Software development

� Video game production.

General Product Distribution AssumptionsThe following general assumptions apply to each of the product distribution patterns outlined above:

� The model firms do not have any in-house distribution capability, so all freight movements are handled by third-party logistics providers

� Each firm is able to maximize the efficiency of its distribution patterns, delivering product to its customers in full truckload and/or container-load quantities, or as standardized less-than-load shipments

� The model firms are not selling to customers requiring just-in-time (JIT) or just-in-order (JIO) deliveries

� Intra-continental distribution is by road and/or rail freight (based on the most economical option), except where the use of sea freight is required between countries in Asia (e.g. between Japan and mainland Asia).

KPMG’s Guide to International Business Location Costs A . 5

Labor Costs

To estimate annual labor costs for each facility, employees from different industries and operations have been grouped into a range of generic job positions, based on common levels of skill and responsibility. This approach reflects the nature of data available from different wage surveys, and the number of positions that can be comparably costed across a wide range of locations. By grouping employees into generic positions, the diversity of salary levels that would be encountered in a typical operation has been built into the calculation of annual labor costs. This study uses 42 generic job positions:

� Eight management positions

� Eight production positions

� Five scientific/technical positions

� Ten information technology positions

� Nine sales and administrative positions

� Two facility maintenance positions.

Based on individual job descriptions, typical salary and wage levels have been collected for each position in each city studied. Statutory and employer-sponsored benefits have also been calculated individually, according to the average pay for each job.

Facilities Costs

Facility requirements have been developed based on actual firm data during the process of defining the standard operating parameters for each business operation:

� For service operations, facilities costs include the cost of leasing suitable Class A office space, generally in a suburban area for most business operations but in a downtown location for the International Financial Services operation

� For manufacturing operations, facility costs include the cost of leasing a suitable modern industrial facility in a suburban area.

Costs for land purchase and building construction, and lease capitalization rates are used in some instances to refine values for industrial leasing and property valuation for local tax purposes.

Costs for land purchase, building construction, industrial leasing, and/or office leasing were collected by Colliers International real estate professionals in each local market.

Energy Costs

Energy requirements have been developed based on actual firm and industry average data during the process of defining the standard operating parameters for each business operation. For manufacturing operations, both electricity and natural gas requirements have been considered. For service operations, where energy requirements are far less significant, only electricity requirements have been considered. Based on the identified energy requirements, costs were calculated based on published schedule rates of relevant energy suppliers or reported statistical rate data for industrial and commercial users, as available in each location.

Taxation Costs

Refer to Appendix B for details of taxation methodology.

Interpretation of Results

While great care has been taken in performing this analysis and developing the findings, the resulting comparisons are of a general nature. All cost factors examined in this study are subject to change over time, due to changes in local laws, regulations, and/or market conditions.

The results of this study should not be interpreted as a definitive or final opinion on the merits of locating any specific facility in one jurisdiction over another. Further analysis is required to determine the best site for a specific facility or operation.

Competitive Alternatives, 2014 EditionA . 6

(This page is intentionally blank)

Appendix BTax Assumptions and Comparisons

This appendix presents the tax rate assumptions used in the comparative analysis, along with summary measures of tax burden resulting from the analysis.

In this study, income taxes have been calculated on the “tax payable” basis. Deferred income tax balances (both positive and negative) have been excluded, since these accounting book entries are generally not relevant for location decision making.

All tax rates listed here are current as at January 1, 2014, based on latest information available as at that date. Taxes are grouped based on substance rather than legal form, and legislated names of specific taxes in certain jurisdictions differ from the generic titles used in this study.

Given the broad scope of this assignment, a number of simplifying assumptions have been made with respect to specific taxes. Any simplifying assumptions made are consistent with the business model assumptions set out in Appendix A.

Payroll taxes have been incorporated into statutory benefit costs shown in this report, but are not presented in this table.

These data should not be used to draw definitive conclusions regarding the relative position of any particular jurisdiction with respect to a particular element of taxation. In all circumstances, professional advice should be sought to address any specific taxation issues in any jurisdiction.

Competitive Alternatives, 2014 EditionB . 2

Federal, regional, and local tax rates – In percent

Adelaide Brisbane Melbourne Sydney Footnotes

Corporate Income Tax a a Percentage of taxable income. Minor adjustments required in the calculation of taxable income in each jurisdiction are not individually disclosed. Tax rates shown in this exhibit are for the size of entity examined in this study. Many jurisdictions offer lower income tax rates for small businesses.

b Manufacturing tax rate reductions may reduce on a pro-rata basis where a significant component of a company’s payroll or capital assets are not devoted to manufacturing or processing operations.

c The effective income tax rates for the overall average (services and manufacturing) in this study vary from the combined nominal income tax rates in each location due to the impact of adjustments to taxable income and income tax credits.

d Percentage of taxable capital, determined on the general basis indicated. In many jurisdictions, the general tax base indicated here is subject to minor adjustment.

e Percentage of sales price.

f General rate. Other rates may apply to specified articles.

g The Property Tax category includes all property-based taxes, including the property-based component of multi-base local business taxes. Property tax rates relate to the suburban or urban areas identified in the real estate research for this study as offering sites suitable for the types of operation being examined.

h Percentage of current market value, incorporating current tax rates, assessment factors, base-year price equalization factors, and rental yields (estimated where required).

i Percentage of depreciated value. Special depreciation rates may apply for property tax purposes.

j Percentage of cost.

k Total property-based taxes in US $ per square foot of building space. Property taxes include taxes levied on the value of land and buildings, machinery and equipment, inventory, and other physical assets. For services operations (occupying leased office space), property taxes on facilities are typically levied on the landlord. The amount of tax passed by the landlord to the tenant as part of total rent is captured in leasing costs in this study, but is not separately identifiable.

l Percentage of gross sales.

m Percentage of gross payroll.

n Tax per employee.

o Includes both state land tax (3.70%) and local council rates (0.76%). Land tax represents top marginal rate. Lower rates apply on the first AUD $1.05 million of land value.

p Includes both state land tax (2.00%) and local council rates (0.91%). Land tax represents top marginal rate. Lower rates apply on the first AUD $5 million of land value.

q Includes both state land tax (2.25%) and local council rates (0.92%). Land tax represents top marginal rate. Lower rates apply on the first AUD $3 million of land value.

r Includes both state land tax (2.00%) and local council rates (0.79%). Land tax represents top marginal rate. Lower rates apply on the first AUD $2.48 million of land value.

s State payroll tax of 4.95% (for Adelaide), 4.75% (for Brisbane), 4.90% (for Melbourne) and 5.45% (for Sydney) is not shown here as it is included under statutory plans in the labor analysis.

Federal 30.00 30.00 30.00 30.00

Regional – – – –

Local – – – –

Combined income tax rate 30.00 30.00 30.00 30.00

Manufacturing tax reduction b

Federal – – – –

Regional – – – –

Combined mfg tax rate 30.00 30.00 30.00 30.00

Effective income tax rate, overall average c 24.86 24.30 25.24 24.23

Capital Tax d

Tax based on:

Capital stock – – – –

Net equity – – – –

Total assets – – – –

Debt/borrowings – – – –

Sales Tax e

Refundable GST/VAT:

Federal f 10.00 10.00 10.00 10.00

Regional f – – – –

Non-refundable sales tax:

Regional f – – – –

Local f – – – –

Property Tax g

Land h 4.46o 2.91p 3.17q 2.79r

Buildings h 0.76 – 0.92 –

Machinery & equipment i – – – –

Inventory j – – – –

Total property-based taxes:

Mfg avg (12 operations) k $2.12 $1.75 $1.60 $2.16

Services avg (7 operations) k – – – –

Local Business Taxes

Taxes based on:

Gross receipts l – – – –

Salaries m –s –s –s –s

Employees n – – – –

Australia

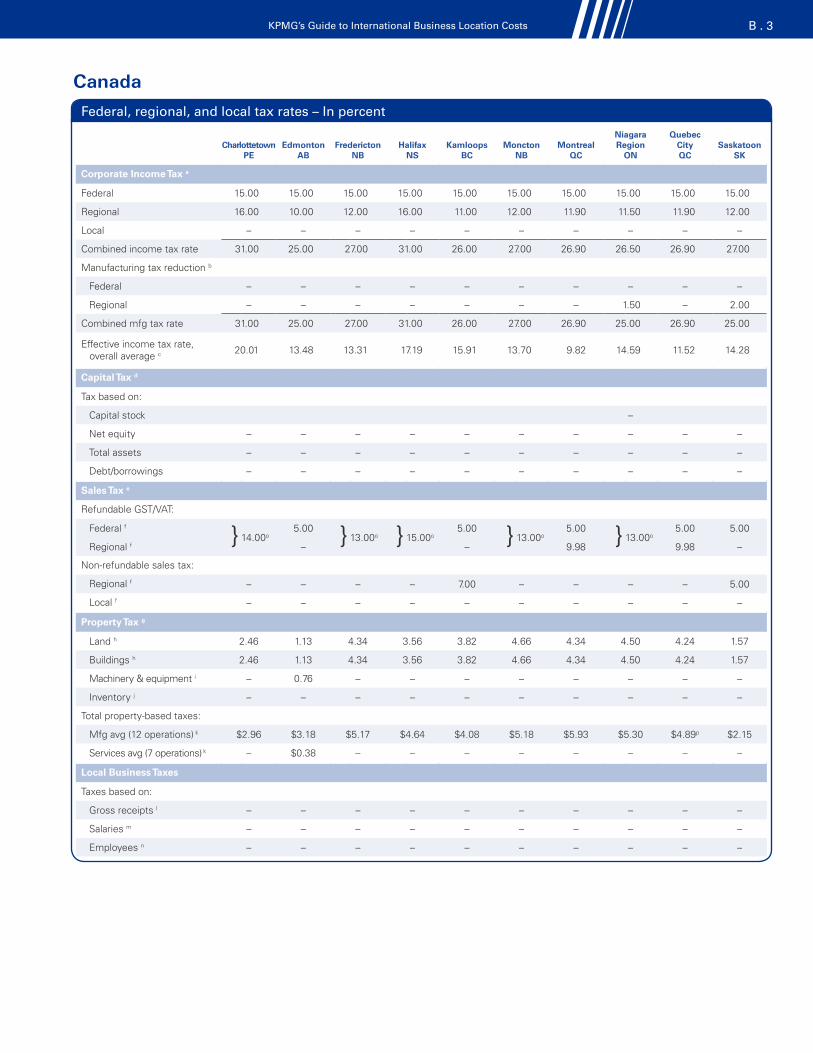

KPMG’s Guide to International Business Location Costs B . 3

Federal, regional, and local tax rates – In percent

Charlottetown PE

Edmonton AB

Fredericton NB

Halifax NS

Kamloops BC

Moncton NB

Montreal QC

Niagara Region

ON

Quebec City QC

Saskatoon SK

Corporate Income Tax a

Federal 15.00 15.00 15.00 15.00 15.00 15.00 15.00 15.00 15.00 15.00

Regional 16.00 10.00 12.00 16.00 11.00 12.00 11.90 11.50 11.90 12.00

Local – – – – – – – – – –

Combined income tax rate 31.00 25.00 27.00 31.00 26.00 27.00 26.90 26.50 26.90 27.00

Manufacturing tax reduction b

Federal – – – – – – – – – –

Regional – – – – – – – 1.50 – 2.00

Combined mfg tax rate 31.00 25.00 27.00 31.00 26.00 27.00 26.90 25.00 26.90 25.00

Effective income tax rate, overall average c 20.01 13.48 13.31 17.19 15.91 13.70 9.82 14.59 11.52 14.28

Capital Tax d

Tax based on:

Capital stock –

Net equity – – – – – – – – – –

Total assets – – – – – – – – – –

Debt/borrowings – – – – – – – – – –

Sales Tax e

Refundable GST/VAT:

Federal f

} 14.00o5.00 } 13.00o } 15.00o

5.00 } 13.00o5.00 } 13.00o

5.00 5.00

Regional f – – 9.98 9.98 –

Non-refundable sales tax:

Regional f – – – – 7.00 – – – – 5.00

Local f – – – – – – – – – –

Property Tax g

Land h 2.46 1.13 4.34 3.56 3.82 4.66 4.34 4.50 4.24 1.57

Buildings h 2.46 1.13 4.34 3.56 3.82 4.66 4.34 4.50 4.24 1.57

Machinery & equipment i – 0.76 – – – – – – – –

Inventory j – – – – – – – – – –

Total property-based taxes:

Mfg avg (12 operations) k $2.96 $3.18 $5.17 $4.64 $4.08 $5.18 $5.93 $5.30 $4.89p $2.15

Services avg (7 operations) k – $0.38 – – – – – – – –

Local Business Taxes

Taxes based on:

Gross receipts l – – – – – – – – – –

Salaries m – – – – – – – – – –

Employees n – – – – – – – – – –

Canada

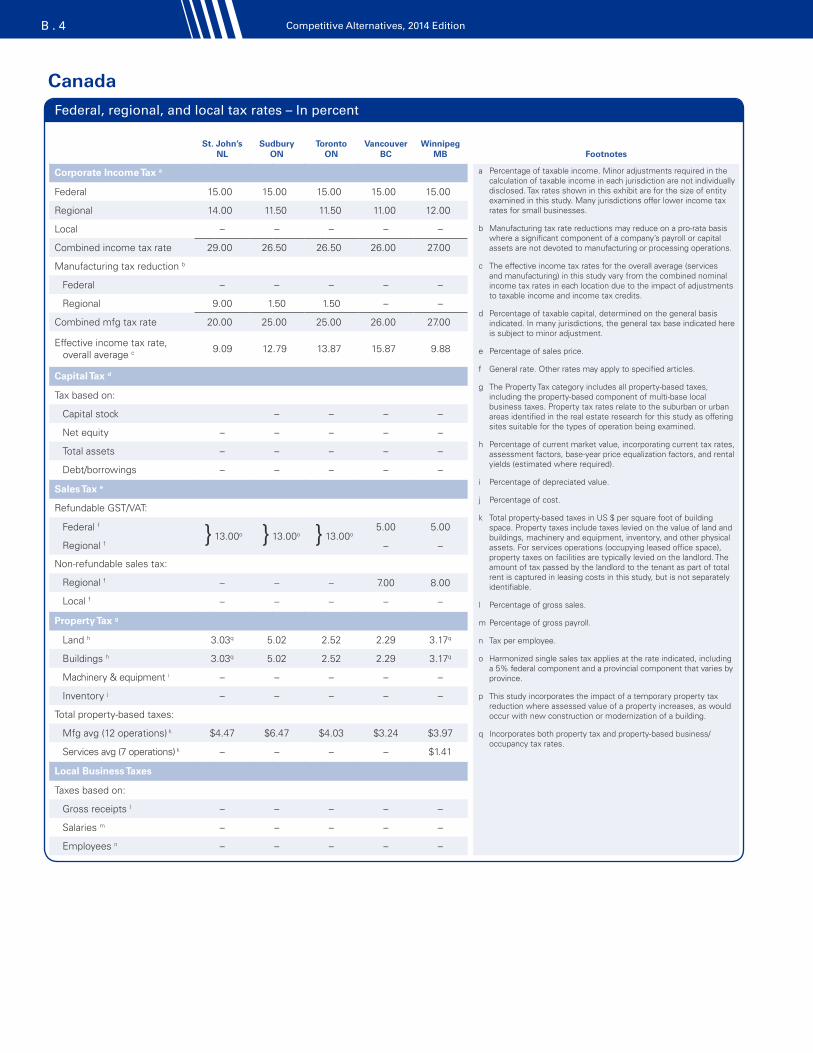

Competitive Alternatives, 2014 EditionB . 4

Federal, regional, and local tax rates – In percent

St. John’s NL

Sudbury ON

Toronto ON

Vancouver BC

Winnipeg MB Footnotes

Corporate Income Tax a a Percentage of taxable income. Minor adjustments required in the calculation of taxable income in each jurisdiction are not individually disclosed. Tax rates shown in this exhibit are for the size of entity examined in this study. Many jurisdictions offer lower income tax rates for small businesses.

b Manufacturing tax rate reductions may reduce on a pro-rata basis where a significant component of a company’s payroll or capital assets are not devoted to manufacturing or processing operations.

c The effective income tax rates for the overall average (services and manufacturing) in this study vary from the combined nominal income tax rates in each location due to the impact of adjustments to taxable income and income tax credits.

d Percentage of taxable capital, determined on the general basis indicated. In many jurisdictions, the general tax base indicated here is subject to minor adjustment.

e Percentage of sales price.

f General rate. Other rates may apply to specified articles.

g The Property Tax category includes all property-based taxes, including the property-based component of multi-base local business taxes. Property tax rates relate to the suburban or urban areas identified in the real estate research for this study as offering sites suitable for the types of operation being examined.

h Percentage of current market value, incorporating current tax rates, assessment factors, base-year price equalization factors, and rental yields (estimated where required).

i Percentage of depreciated value.

j Percentage of cost.

k Total property-based taxes in US $ per square foot of building space. Property taxes include taxes levied on the value of land and buildings, machinery and equipment, inventory, and other physical assets. For services operations (occupying leased office space), property taxes on facilities are typically levied on the landlord. The amount of tax passed by the landlord to the tenant as part of total rent is captured in leasing costs in this study, but is not separately identifiable.

l Percentage of gross sales.

m Percentage of gross payroll.

n Tax per employee.

o Harmonized single sales tax applies at the rate indicated, including a 5% federal component and a provincial component that varies by province.

p This study incorporates the impact of a temporary property tax reduction where assessed value of a property increases, as would occur with new construction or modernization of a building.

q Incorporates both property tax and property-based business/occupancy tax rates.

Federal 15.00 15.00 15.00 15.00 15.00

Regional 14.00 11.50 11.50 11.00 12.00

Local – – – – –

Combined income tax rate 29.00 26.50 26.50 26.00 27.00

Manufacturing tax reduction b

Federal – – – – –

Regional 9.00 1.50 1.50 – –

Combined mfg tax rate 20.00 25.00 25.00 26.00 27.00

Effective income tax rate, overall average c 9.09 12.79 13.87 15.87 9.88

Capital Tax d

Tax based on:

Capital stock – – – –

Net equity – – – – –

Total assets – – – – –

Debt/borrowings – – – – –

Sales Tax e

Refundable GST/VAT:

Federal f

} 13.00o } 13.00o } 13.00o5.00 5.00

Regional f – –

Non-refundable sales tax:

Regional f – – – 7.00 8.00

Local f – – – – –

Property Tax g

Land h 3.03q 5.02 2.52 2.29 3.17q

Buildings h 3.03q 5.02 2.52 2.29 3.17q

Machinery & equipment i – – – – –

Inventory j – – – – –

Total property-based taxes:

Mfg avg (12 operations) k $4.47 $6.47 $4.03 $3.24 $3.97

Services avg (7 operations) k – – – – $1.41

Local Business Taxes

Taxes based on:

Gross receipts l – – – – –

Salaries m – – – – –

Employees n – – – – –

Canada

KPMG’s Guide to International Business Location Costs B . 5

Federal, regional, and local tax rates – In percent

Marseille Paris Footnotes

Corporate Income Tax a a Percentage of taxable income. Minor adjustments required in the calculation of taxable income in each jurisdiction are not individually disclosed. Tax rates shown in this exhibit are for the size of entity examined in this study. Many jurisdictions offer lower income tax rates for small businesses.

b Manufacturing tax rate reductions may reduce on a pro-rata basis where a significant component of a company’s payroll or capital assets are not devoted to manufacturing or processing operations.

c The effective income tax rates for the overall average (services and manufacturing) in this study vary from the combined nominal income tax rates in each location due to the impact of adjustments to taxable income and income tax credits.

d Percentage of taxable capital, determined on the general basis indicated. In many jurisdictions, the general tax base indicated here is subject to minor adjustment.

e Percentage of sales price.

f General rate. Other rates may apply to specified articles.

g The Property Tax category includes all property-based taxes, including the property-based component of multi-base local business taxes. Property tax rates relate to the suburban or urban areas identified in the real estate research for this study as offering sites suitable for the types of operation being examined.

h Percentage of current market value, incorporating current tax rates, assessment factors, base-year price equalization factors, and rental yields (estimated where required).

i Percentage of depreciated value. Special depreciation rates may apply for property tax purposes.

j Percentage of cost.

k Total property-based taxes in US $ per square foot of building space. Property taxes include taxes levied on the value of land and buildings, machinery and equipment, inventory, and other physical assets. For services operations (occupying leased office space), property taxes on facilities are typically levied on the landlord. The amount of tax passed by the landlord to the tenant as part of total rent is captured in leasing costs in this study, but is not separately identifiable.

l Percentage of gross sales.

m Percentage of gross payroll.

n Tax per employee.

o One-time tax on share issuance.

p Includes both Tax on Developed Properties (TFPB) and Contribution for Enterprise Land Value (CFE), both of which are based on property rental value. CFE is levied directly on the lessee of leased properties.

q Contribution for Enterprise Value Added (CVAE), top marginal rate. Lower rates apply to companies with sales turnover of less than €50 million per annum. Tax base is value added, which is calculated as gross receipts less limited specified deductions.

r Total CFE plus CVAE is capped at 3% of value added as assessed for CVAE.

Federal 33.33 33.33

Regional – –

Local – –

Combined income tax rate 33.33 33.33

Manufacturing tax reduction b

Federal – –

Regional – –

Combined mfg tax rate 33.33 33.33

Effective income tax rate, overall average c 16.65 12.71

Capital Tax d

Tax based on:

Capital stock 0.10o 0.10o

Net equity – –

Total assets – –

Debt/borrowings – –

Sales Tax e

Refundable GST/VAT:

Federal f 20.00 20.00

Regional f – –

Non-refundable sales tax:

Regional f – –

Local f – –

Property Tax g

Land h 3.93p 1.68p

Buildings h 3.93p 1.68p

Machinery & equipment i – –

Inventory j – –

Total property-based taxes:

Mfg avg (12 operations) k $3.82r $1.78r

Services avg (7 operations) k $7.69r $10.46r

Local Business Taxes

Taxes based on:

Gross receipts l 1.50q 1.50q

Salaries m – –

Employees n – –

France

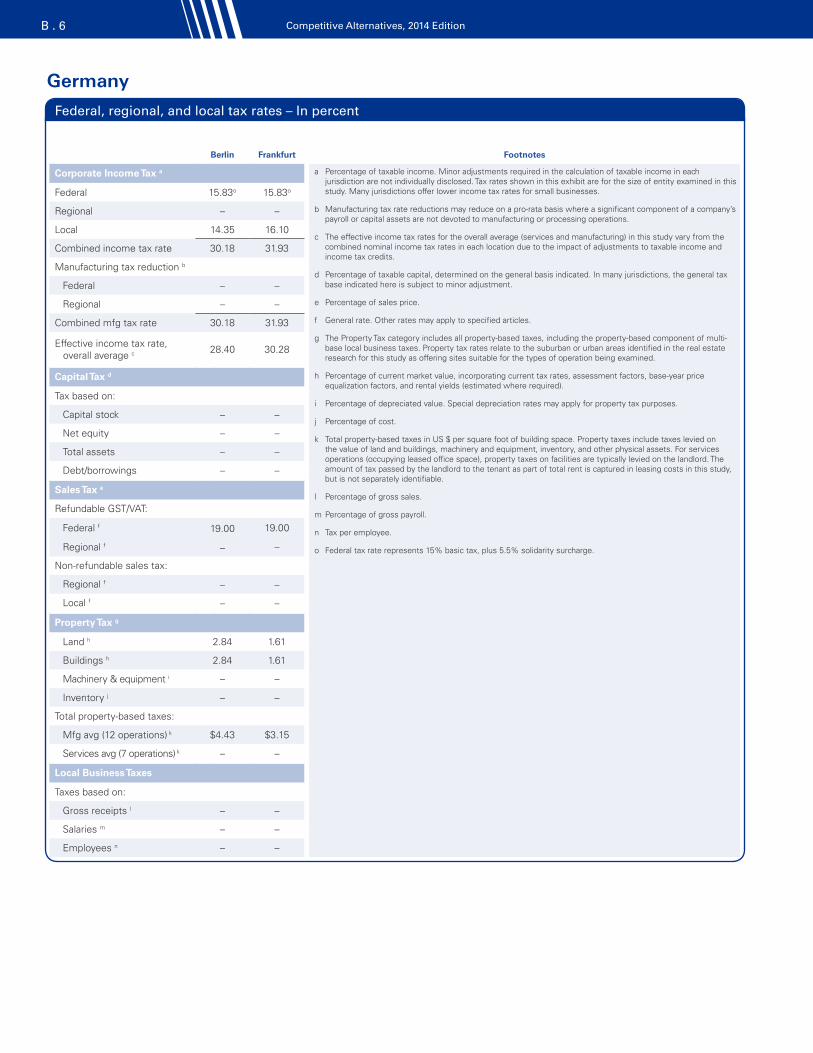

Competitive Alternatives, 2014 EditionB . 6

Federal, regional, and local tax rates – In percent

Berlin Frankfurt Footnotes

Corporate Income Tax a a Percentage of taxable income. Minor adjustments required in the calculation of taxable income in each jurisdiction are not individually disclosed. Tax rates shown in this exhibit are for the size of entity examined in this study. Many jurisdictions offer lower income tax rates for small businesses.

b Manufacturing tax rate reductions may reduce on a pro-rata basis where a significant component of a company’s payroll or capital assets are not devoted to manufacturing or processing operations.

c The effective income tax rates for the overall average (services and manufacturing) in this study vary from the combined nominal income tax rates in each location due to the impact of adjustments to taxable income and income tax credits.

d Percentage of taxable capital, determined on the general basis indicated. In many jurisdictions, the general tax base indicated here is subject to minor adjustment.

e Percentage of sales price.

f General rate. Other rates may apply to specified articles.

g The Property Tax category includes all property-based taxes, including the property-based component of multi-base local business taxes. Property tax rates relate to the suburban or urban areas identified in the real estate research for this study as offering sites suitable for the types of operation being examined.

h Percentage of current market value, incorporating current tax rates, assessment factors, base-year price equalization factors, and rental yields (estimated where required).

i Percentage of depreciated value. Special depreciation rates may apply for property tax purposes.

j Percentage of cost.

k Total property-based taxes in US $ per square foot of building space. Property taxes include taxes levied on the value of land and buildings, machinery and equipment, inventory, and other physical assets. For services operations (occupying leased office space), property taxes on facilities are typically levied on the landlord. The amount of tax passed by the landlord to the tenant as part of total rent is captured in leasing costs in this study, but is not separately identifiable.

l Percentage of gross sales.

m Percentage of gross payroll.

n Tax per employee.

o Federal tax rate represents 15% basic tax, plus 5.5% solidarity surcharge.

Federal 15.83o 15.83o

Regional – –

Local 14.35 16.10

Combined income tax rate 30.18 31.93

Manufacturing tax reduction b

Federal – –

Regional – –

Combined mfg tax rate 30.18 31.93

Effective income tax rate, overall average c 28.40 30.28

Capital Tax d

Tax based on:

Capital stock – –

Net equity – –

Total assets – –

Debt/borrowings – –

Sales Tax e

Refundable GST/VAT:

Federal f 19.00 19.00

Regional f – –

Non-refundable sales tax:

Regional f – –

Local f – –

Property Tax g

Land h 2.84 1.61

Buildings h 2.84 1.61

Machinery & equipment i – –

Inventory j – –

Total property-based taxes:

Mfg avg (12 operations) k $4.43 $3.15

Services avg (7 operations) k – –

Local Business Taxes

Taxes based on:

Gross receipts l – –

Salaries m – –

Employees n – –

Germany

KPMG’s Guide to International Business Location Costs B . 7

Federal, regional, and local tax rates – In percent

Milan Rome Footnotes

Corporate Income Tax a a Percentage of taxable income. Minor adjustments required in the calculation of taxable income in each jurisdiction are not individually disclosed. Tax rates shown in this exhibit are for the size of entity examined in this study. Many jurisdictions offer lower income tax rates for small businesses.

b Manufacturing tax rate reductions may reduce on a pro-rata basis where a significant component of a company’s payroll or capital assets are not devoted to manufacturing or processing operations.

c The effective income tax rates for the overall average (services and manufacturing) in this study vary from the combined nominal income tax rates in each location due to the impact of adjustments to taxable income and income tax credits.

d Percentage of taxable capital, determined on the general basis indicated. In many jurisdictions, the general tax base indicated here is subject to minor adjustment.

e Percentage of sales price.

f General rate. Other rates may apply to specified articles.

g The Property Tax category includes all property-based taxes, including the property-based component of multi-base local business taxes. Property tax rates relate to the suburban or urban areas identified in the real estate research for this study as offering sites suitable for the types of operation being examined.

h Percentage of current market value, incorporating current tax rates, assessment factors, base-year price equalization factors, and rental yields (estimated where required).

i Percentage of depreciated value. Special depreciation rates may apply for property tax purposes.

j Percentage of cost.

k Total property-based taxes in US $ per square foot of building space. Property taxes include taxes levied on the value of land and buildings, machinery and equipment, inventory, and other physical assets. For services operations (occupying leased office space), property taxes on facilities are typically levied on the landlord. The amount of tax passed by the landlord to the tenant as part of total rent is captured in leasing costs in this study, but is not separately identifiable.

l Percentage of gross sales.

m Percentage of gross payroll.

n Tax per employee.

o Deductions for payroll and interest costs are limited for Italian Regional Tax on Productive Activities (IRAP). This results in a higher taxable income base for IRAP purposes than for most other income taxes listed in this Appendix.

p In calculating the combined tax rate, regional tax paid is deductible for federal tax calculations to the extent that regional tax liability reflects non-deductible labor costs. The actual percentage federal deduction for regional tax paid varies by company and by year. The combined tax rate shown assumes a 50 percent federal deduction for regional tax paid. Therefore, the regional tax rate has been reduced by (1 - (federal tax rate x 50%)) to determine the combined rate.

q One-time tax on issuance of medium and long term loans.

r Local tax on immovable property tax (IMU) is intended to be repealed and replaced by alternative forms of local tax as of January 2014. However, as at January 2014 the form of such new taxes is subject to significant uncertainty, so this analysis continues to reflect the IMU tax in effect for 2013. IMU is based on imputed income value of a property as determined by the Immovable Property Registry. The rates shown here represent the estimated tax rate as a percentage of property fair market value, based on the assumption that for owned facilities imputed income represents 1.495% of fair market value. For leased facilities, imputed income is assumed to equal actual lease payments.

Federal 27.50 27.50

Regional 3.90o 4.82o

Local – –

Combined income tax rate 30.86p 31.66p

Manufacturing tax reduction b

Federal – –

Regional – –

Combined mfg tax rate 30.86 31.66

Effective income tax rate, overall average c 27.84 31.07

Capital Tax d

Tax based on:

Capital stock – –

Net equity – –

Total assets – –

Debt/borrowings 0.25q 0.25q

Sales Tax e

Refundable GST/VAT:

Federal f 22.00 22.00

Regional f – –

Non-refundable sales tax:

Regional f – –

Local f – –

Property Tax g

Land h 1.06r 1.06r

Buildings h 0.89r 1.08r

Machinery & equipment i – –

Inventory j – –

Total property-based taxes:

Mfg avg (12 operations) k $1.04 $1.90

Services avg (7 operations) k $3.29 $3.43

Local Business Taxes

Taxes based on:

Gross receipts l – –

Salaries m – –

Employees n – –

Italy

Competitive Alternatives, 2014 EditionB . 8

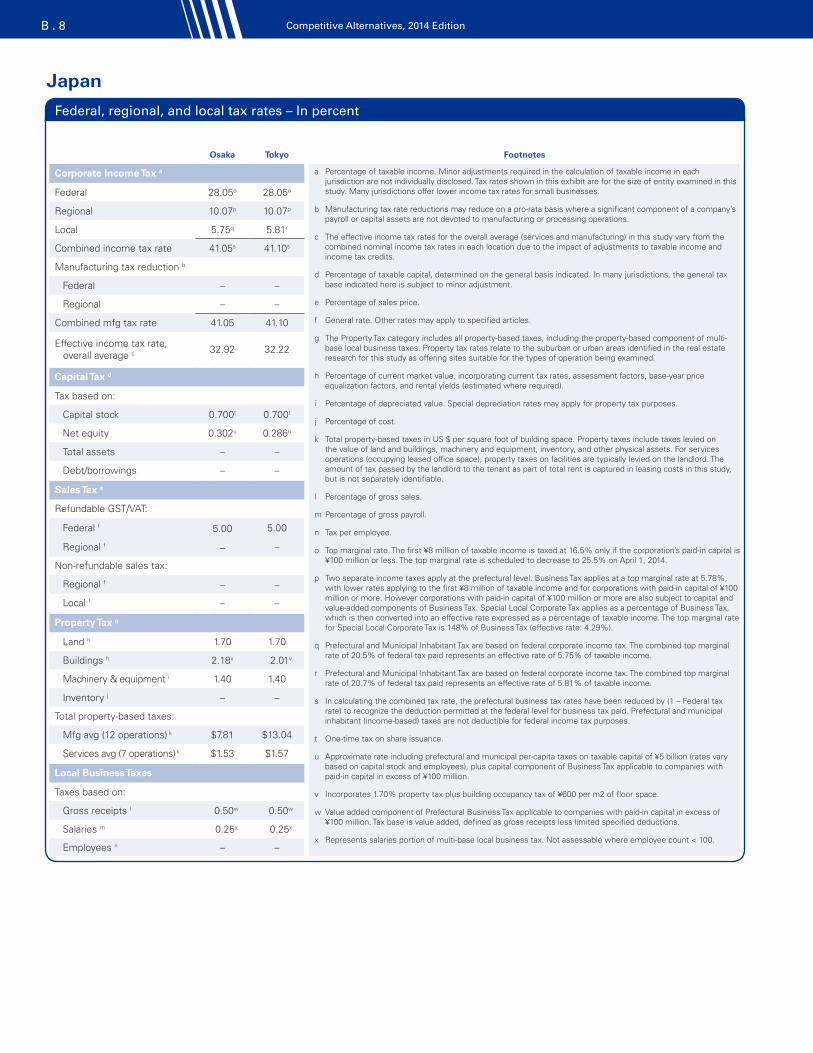

Federal, regional, and local tax rates – In percent

Osaka Tokyo Footnotes

Corporate Income Tax a a Percentage of taxable income. Minor adjustments required in the calculation of taxable income in each jurisdiction are not individually disclosed. Tax rates shown in this exhibit are for the size of entity examined in this study. Many jurisdictions offer lower income tax rates for small businesses.

b Manufacturing tax rate reductions may reduce on a pro-rata basis where a significant component of a company’s payroll or capital assets are not devoted to manufacturing or processing operations.

c The effective income tax rates for the overall average (services and manufacturing) in this study vary from the combined nominal income tax rates in each location due to the impact of adjustments to taxable income and income tax credits.

d Percentage of taxable capital, determined on the general basis indicated. In many jurisdictions, the general tax base indicated here is subject to minor adjustment.

e Percentage of sales price.

f General rate. Other rates may apply to specified articles.

g The Property Tax category includes all property-based taxes, including the property-based component of multi-base local business taxes. Property tax rates relate to the suburban or urban areas identified in the real estate research for this study as offering sites suitable for the types of operation being examined.

h Percentage of current market value, incorporating current tax rates, assessment factors, base-year price equalization factors, and rental yields (estimated where required).

i Percentage of depreciated value. Special depreciation rates may apply for property tax purposes.

j Percentage of cost.

k Total property-based taxes in US $ per square foot of building space. Property taxes include taxes levied on the value of land and buildings, machinery and equipment, inventory, and other physical assets. For services operations (occupying leased office space), property taxes on facilities are typically levied on the landlord. The amount of tax passed by the landlord to the tenant as part of total rent is captured in leasing costs in this study, but is not separately identifiable.

l Percentage of gross sales.

m Percentage of gross payroll.

n Tax per employee.

o Top marginal rate. The first ¥8 million of taxable income is taxed at 16.5% only if the corporation’s paid-in capital is ¥100 million or less. The top marginal rate is scheduled to decrease to 25.5% on April 1, 2014.

p Two separate income taxes apply at the prefectural level. Business Tax applies at a top marginal rate at 5.78%, with lower rates applying to the first ¥8 million of taxable income and for corporations with paid-in capital of ¥100 million or more. However corporations with paid-in capital of ¥100 million or more are also subject to capital and value-added components of Business Tax. Special Local Corporate Tax applies as a percentage of Business Tax, which is then converted into an effective rate expressed as a percentage of taxable income. The top marginal rate for Special Local Corporate Tax is 148% of Business Tax (effective rate: 4.29%).

q Prefectural and Municipal Inhabitant Tax are based on federal corporate income tax. The combined top marginal rate of 20.5% of federal tax paid represents an effective rate of 5.75% of taxable income.

r Prefectural and Municipal Inhabitant Tax are based on federal corporate income tax. The combined top marginal rate of 20.7% of federal tax paid represents an effective rate of 5.81% of taxable income.

s In calculating the combined tax rate, the prefectural business tax rates have been reduced by (1 – Federal tax rate) to recognize the deduction permitted at the federal level for business tax paid. Prefectural and municipal inhabitant (income-based) taxes are not deductible for federal income tax purposes.

t One-time tax on share issuance.

u Approximate rate including prefectural and municipal per-capita taxes on taxable capital of ¥5 billion (rates vary based on capital stock and employees), plus capital component of Business Tax applicable to companies with paid-in capital in excess of ¥100 million.

v Incorporates 1.70% property tax plus building occupancy tax of ¥600 per m2 of floor space.

w Value added component of Prefectural Business Tax applicable to companies with paid-in capital in excess of ¥100 million. Tax base is value added, defined as gross receipts less limited specified deductions.

x Represents salaries portion of multi-base local business tax. Not assessable where employee count < 100.

Federal 28.05o 28.05o

Regional 10.07p 10.07p

Local 5.75q 5.81r

Combined income tax rate 41.05s 41.10s

Manufacturing tax reduction b

Federal – –

Regional – –

Combined mfg tax rate 41.05 41.10

Effective income tax rate, overall average c 32.92 32.22

Capital Tax d

Tax based on:

Capital stock 0.700t 0.700t

Net equity 0.302u 0.286u

Total assets – –

Debt/borrowings – –

Sales Tax e

Refundable GST/VAT:

Federal f 5.00 5.00

Regional f – –

Non-refundable sales tax:

Regional f – –

Local f – –

Property Tax g

Land h 1.70 1.70

Buildings h 2.18v 2.01v

Machinery & equipment i 1.40 1.40

Inventory j – –

Total property-based taxes:

Mfg avg (12 operations) k $7.81 $13.04

Services avg (7 operations) k $1.53 $1.57

Local Business Taxes

Taxes based on:

Gross receipts l 0.50w 0.50w

Salaries m 0.25x 0.25x

Employees n – –

Japan

KPMG’s Guide to International Business Location Costs B . 9

Federal, regional, and local tax rates – In percent

Mexico City Monterrey Footnotes

Corporate Income Tax a a Percentage of taxable income. Minor adjustments required in the calculation of taxable income in each jurisdiction are not individually disclosed. Tax rates shown in this exhibit are for the size of entity examined in this study. Many jurisdictions offer lower income tax rates for small businesses.

b Manufacturing tax rate reductions may reduce on a pro-rata basis where a significant component of a company’s payroll or capital assets are not devoted to manufacturing or processing operations.

c The effective income tax rates for the overall average (services and manufacturing) in this study vary from the combined nominal income tax rates in each location due to the impact of adjustments to taxable income and income tax credits.

d Percentage of taxable capital, determined on the general basis indicated. In many jurisdictions, the general tax base indicated here is subject to minor adjustment.

e Percentage of sales price.

f General rate. Other rates may apply to specified articles.

g The Property Tax category includes all property-based taxes, including the property-based component of multi-base local business taxes. Property tax rates relate to the suburban or urban areas identified in the real estate research for this study as offering sites suitable for the types of operation being examined.

h Percentage of current market value, incorporating current tax rates, assessment factors, base-year price equalization factors, and rental yields (estimated where required).

i Percentage of depreciated value. Special depreciation rates may apply for property tax purposes.

j Percentage of cost.

k Total property-based taxes in US $ per square foot of building space. Property taxes include taxes levied on the value of land and buildings, machinery and equipment, inventory, and other physical assets. For services operations (occupying leased office space), property taxes on facilities are typically levied on the landlord. The amount of tax passed by the landlord to the tenant as part of total rent is captured in leasing costs in this study, but is not separately identifiable.

l Percentage of gross sales.

m Percentage of gross payroll.

n Tax per employee.

o Exemption of 45% applies for new companies for the first year of operation. A further 25% exemption applies in any future year where the number of employees increases by at least 25% compared to the prior year.

p Full exemption applies for new companies for the first four years of operation.

Federal 30.00 30.00

Regional – –

Local – –

Combined income tax rate 30.00 30.00

Manufacturing tax reduction b

Federal – –

Regional – –

Combined mfg tax rate 30.00 30.00

Effective income tax rate, overall average c 30.91 30.81

Capital Tax d

Tax based on:

Capital stock – –

Net equity – –

Total assets – –

Debt/borrowings – –

Sales Tax e

Refundable GST/VAT:

Federal f 16.00 16.00

Regional f – –

Non-refundable sales tax:

Regional f – –

Local f – –

Property Tax g

Land h 0.15 0.20

Buildings h 0.15 0.20

Machinery & equipment i – –

Inventory j – –

Total property-based taxes:

Mfg avg (12 operations) k $0.08 $0.10

Services avg (7 operations) k – –

Local Business Taxes

Taxes based on:

Gross receipts l – –

Salaries m 2.50o 3.00p

Employees n – –

Mexico

Competitive Alternatives, 2014 EditionB . 10

Federal, regional, and local tax rates – In percent

EindhovenTwente Region Footnotes

Corporate Income Tax a a Percentage of taxable income. Minor adjustments required in the calculation of taxable income in each jurisdiction are not individually disclosed. Tax rates shown in this exhibit are for the size of entity examined in this study. Many jurisdictions offer lower income tax rates for small businesses.

b Manufacturing tax rate reductions may reduce on a pro-rata basis where a significant component of a company’s payroll or capital assets are not devoted to manufacturing or processing operations.

c The effective income tax rates for the overall average (services and manufacturing) in this study vary from the combined nominal income tax rates in each location due to the impact of adjustments to taxable income and income tax credits.

d Percentage of taxable capital, determined on the general basis indicated. In many jurisdictions, the general tax base indicated here is subject to minor adjustment.

e Percentage of sales price.

f General rate. Other rates may apply to specified articles.

g The Property Tax category includes all property-based taxes, including the property-based component of multi-base local business taxes. Property tax rates relate to the suburban or urban areas identified in the real estate research for this study as offering sites suitable for the types of operation being examined.

h Percentage of current market value, incorporating current tax rates, assessment factors, base-year price equalization factors, and rental yields (estimated where required).

i Percentage of depreciated value. Special depreciation rates may apply for property tax purposes.

j Percentage of cost.

k Total property-based taxes in US $ per square foot of building space. Property taxes include taxes levied on the value of land and buildings, machinery and equipment, inventory, and other physical assets. For services operations (occupying leased office space), property taxes on facilities are typically levied on the landlord. The amount of tax passed by the landlord to the tenant as part of total rent is captured in leasing costs in this study, but is not separately identifiable.

l Percentage of gross sales.

m Percentage of gross payroll.

n Tax per employee.

o Top marginal rate. The first €200,000 of taxable income is taxed at 20%.

p The benefits provided under the Netherlands’ R&D employee wage tax withholding program are netted into the calculation of effective income tax rate.

q Incorporates real estate taxes levied on both property owners and property occupants.

Federal 25.00o 25.00o

Regional – –

Local – –

Combined income tax rate 25.00 25.00

Manufacturing tax reduction b

Federal – –

Regional – –

Combined mfg tax rate 25.00 25.00

Effective income tax rate, overall average c 18.52p 18.45p

Capital Tax d

Tax based on:

Capital stock – –

Net equity – –

Total assets – –

Debt/borrowings – –

Sales Tax e

Refundable GST/VAT:

Federal f 21.00 21.00

Regional f – –

Non-refundable sales tax:

Regional f – –

Local f – –

Property Tax g

Land h 0.32q 0.54q

Buildings h 0.32q 0.54q

Machinery & equipment i – –

Inventory j – –

Total property-based taxes:

Mfg avg (12 operations) k $0.43 $0.62

Services avg (7 operations) k $0.22 $0.36

Local Business Taxes

Taxes based on:

Gross receipts l – –

Salaries m – –

Employees n – –

Netherlands

KPMG’s Guide to International Business Location Costs B . 11

Federal, regional, and local tax rates – In percent

London Manchester Footnotes

Corporate Income Tax a a Percentage of taxable income. Minor adjustments required in the calculation of taxable income in each jurisdiction are not individually disclosed. Tax rates shown in this exhibit are for the size of entity examined in this study. Many jurisdictions offer lower income tax rates for small businesses.

b Manufacturing tax rate reductions may reduce on a pro-rata basis where a significant component of a company’s payroll or capital assets are not devoted to manufacturing or processing operations.

c The effective income tax rates for the overall average (services and manufacturing) in this study vary from the combined nominal income tax rates in each location due to the impact of adjustments to taxable income and income tax credits.

d Percentage of taxable capital, determined on the general basis indicated. In many jurisdictions, the general tax base indicated here is subject to minor adjustment.

e Percentage of sales price.

f General rate. Other rates may apply to specified articles.

g The Property Tax category includes all property-based taxes, including the property-based component of multi-base local business taxes. Property tax rates relate to the suburban or urban areas identified in the real estate research for this study as offering sites suitable for the types of operation being examined.

h Percentage of current market value, incorporating current tax rates, assessment factors, base-year price equalization factors, and rental yields (estimated where required).

i Percentage of depreciated value. Special depreciation rates may apply for property tax purposes.

j Percentage of cost.

k Total property-based taxes in US $ per square foot of building space. Property taxes include taxes levied on the value of land and buildings, machinery and equipment, inventory, and other physical assets. For services operations (occupying leased office space), property taxes on facilities are typically levied on the landlord. The amount of tax passed by the landlord to the tenant as part of total rent is captured in leasing costs in this study, but is not separately identifiable.

l Percentage of gross sales.

m Percentage of gross payroll.

n Tax per employee.

o Top marginal tax rate applies where taxable income exceeds £1.5 million. If taxable income is below £300,000, the tax rate is 20%, while a pro-rated tax rate of between 20% and 23% applies if taxable income is between £300,000 and £1.5 million.

p The top marginal rate is scheduled to decrease by 2% to 21% on April 1 2014, and then by a further 1% to 20% on April 1 2015.

Federal 23.00o,p 23.00o,p

Regional –

Local – –

Combined income tax rate 23.00 23.00

Manufacturing tax reduction b

Federal – –

Regional – –

Combined mfg tax rate 23.00 23.00

Effective income tax rate, overall average c 12.70 16.36

Capital Tax d

Tax based on:

Capital stock – –

Net equity – –

Total assets – –

Debt/borrowings – –

Sales Tax e

Refundable GST/VAT:

Federal f 20.00 20.00

Regional f – –

Non-refundable sales tax:

Regional f – –

Local f – –

Property Tax g

Land h 4.75 4.71

Buildings h 4.75 4.71

Machinery & equipment i – –

Inventory j – –

Total property-based taxes:

Mfg avg (12 operations) k $9.48 $4.58

Services avg (7 operations) k – –

Local Business Taxes

Taxes based on:

Gross receipts l – –

Salaries m – –

Employees n – –

United Kingdom

Competitive Alternatives, 2014 EditionB . 12

Federal, regional, and local tax rates – In percent

Albuquerque NM

Anchorage AK

Atlanta GA

Austin TX

Baltimore MD

Bangor ME

Baton Rouge

LABeaumont

TXBillings

MTBoise

ID

Corporate Income Tax a

Federal 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o

Regional 7.30s 9.40s 6.00q 0.98q,v 8.25q 8.93q,s 8.00q,s 0.98q,v 6.75 7.40

Local – – – – – – – – – –

Combined income tax rate 38.29z,aa 40.20z 37.60z,aa 34.64z 39.45z 39.89z 36.56z,ac 34.64z 38.46z 38.88z

Manufacturing tax reduction b

Federal 2.85p 2.77p 3.06p 3.06p 3.06p 3.06p 2.82p 3.06p 2.85p 2.83p

Regional 0.61p 0.85p – – – – 0.72p – 0.61p 0.67p

Combined mfg tax rate 34.82 36.59 34.54 31.58 36.39 36.83 33.02 31.58 34.99 35.38

Effective income tax rate, overall average c 23.31 40.30ad 25.20 27.36 28.48 28.89 19.23 27.66 31.59 30.88

Capital Tax d

Tax based on:

Capital stock – – – – – – – – – –

Net equity – – 0.030af – – – – – – –

Total assets – – – – – – 0.300ap – – –

Debt/borrowings – – – – – – – – – –

Sales Tax e

Refundable GST/VAT:

Federal f – – – – – – – – – –

Regional f – – – – – – – – – –

Non-refundable sales tax:

Regional f 5.13 – 4.00 6.25 6.00 5.50 4.00 6.25 – 6.00

Local f 1.88 – 2.75 2.00 – – 5.00 2.00 – –

Property Tax g

Land h 1.73 1.56 1.37 2.41 1.55 1.97 1.06 2.69 1.22 1.82

Buildings h 1.73 1.56 1.37 2.41 1.55 1.97 1.59bk 2.69 1.22 1.82

Machinery & equipment i 1.73 1.56 1.37 2.41 3.43bq 1.97at 1.59bk 2.69 1.22 1.82

Inventory j – 1.56 1.37bp 2.41bp – – 1.59br 2.69bp – –

Total property-based taxes:

Mfg avg (12 operations) k $4.97 $6.30 $3.85 $6.77 $1.92 $2.39 $1.17 $7.47 $3.60 $5.29

Services avg (7 operations) k $0.88 $0.79 $0.70 $1.22 $1.20 $0.12 $0.80 $1.37 $0.62 $0.93

Local Business Taxes

Taxes based on:

Gross receipts l – – – – – – – – – –

Salaries m – – – – – – – – – –

Employees n – – – – – – – – – –

United States

KPMG’s Guide to International Business Location Costs B . 13

Federal, regional, and local tax rates – In percent

Boston MA

Buffalo NY

Burlington VT

Cedar Rapids

IA

Champaign- Urbana

ILCharleston

WVCharlotte

NCCheyenne

WYChicago

ILCincinnati

OH

Corporate Income Tax a

Federal 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o

Regional 8.00 7.10q,r 8.50s 12.00q,s 9.50t 6.50 6.00q,bh – 9.50t –

Local – – – – – – – – – 1.50bo

Combined income tax rate 39.28z 38.69z 39.61z 39.88z,ab 40.27z 38.29z 37.96z 34.00 40.27z 34.99z

Manufacturing tax reduction b

Federal 3.06p 3.06p 2.80p 2.69p 2.77p 3.06p 3.06p 3.06p 2.77p 3.06p

Regional – 1.20bc 0.77p 1.08p 0.86p – – – 0.86p –

Combined mfg tax rate 36.22 34.43 36.05 36.11 36.65 35.23 34.90 30.94 36.65 31.93

Effective income tax rate, overall average c 28.97 29.34 31.50 27.95 31.84 29.01 28.99 27.88 30.31 25.96

Capital Tax d

Tax based on:

Capital stock – – – – 0.100ah – – – 0.100ah –

Net equity – 0.150r – – – 0.100bi – – – –

Total assets 0.260ag – – – – – 0.150bd 0.020 – –

Debt/borrowings – – – – – – – – – –

Sales Tax e

Refundable GST/VAT:

Federal f – – – – – – – – – –

Regional f – – – – – – – – – –

Non-refundable sales tax:

Regional f 6.25 4.00 6.00 6.00 6.25 6.00 4.75 4.00 6.25 5.75

Local f – 4.75 0.67 1.00 2.50 0.50 2.50 2.00 2.31 0.88

Property Tax g

Land h 2.86 3.52 1.87 3.91 2.76 1.73 1.33 0.89 3.12 2.38

Buildings h 2.86 3.52 1.87 3.91 2.76 1.73 1.33 0.89 3.12 2.38

Machinery & equipment i 2.86ar – 1.87 – – 1.73 1.33 0.89 – –

Inventory j – – – – – 1.73 – – – –

Total property-based taxes:

Mfg avg (12 operations) k $3.51 $3.87 $5.54 $3.78 $2.99 $6.10 $3.68 $2.63 $4.21 $2.12

Services avg (7 operations) k $1.45 – $0.95 – – $0.88 $0.68 $0.45 – –

Local Business Taxes

Taxes based on:

Gross receipts l – – – – – 1.00ax – – – 0.26u

Salaries m – – – – – – – – – –

Employees n – – – – – – – – – –

United States

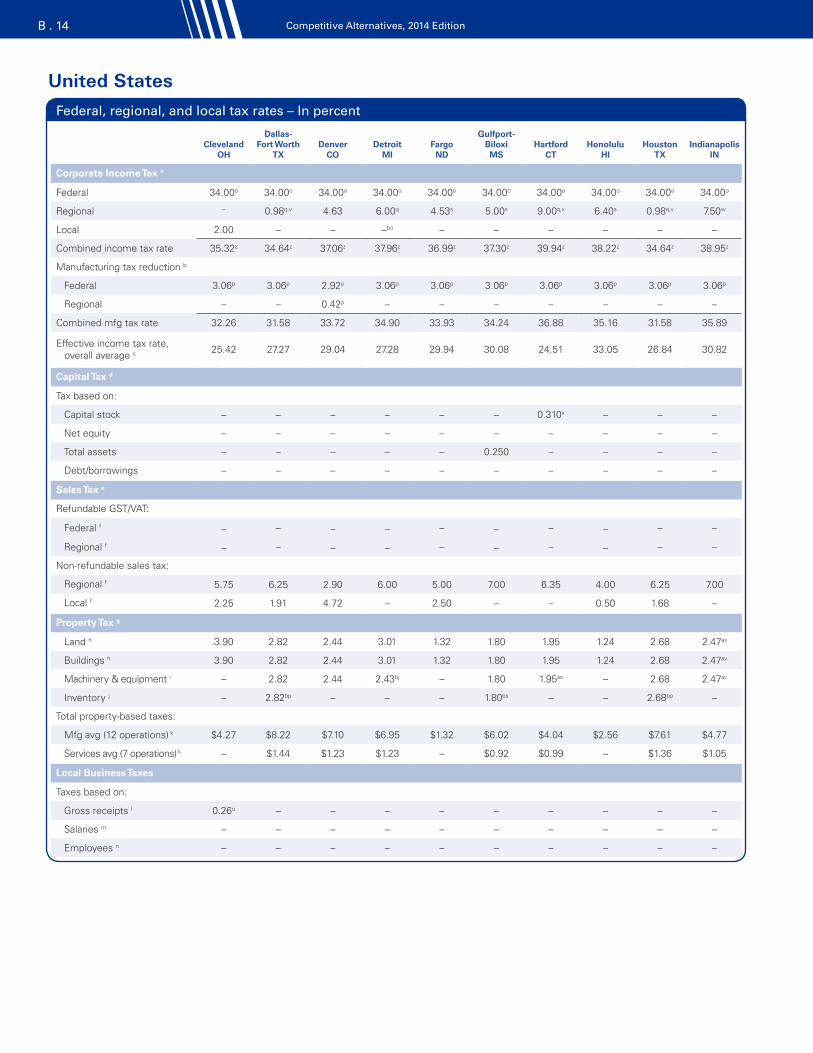

Competitive Alternatives, 2014 EditionB . 14

Federal, regional, and local tax rates – In percent

Cleveland OH

Dallas- Fort Worth

TXDenver

CODetroit

MIFargo

ND

Gulfport- Biloxi MS

Hartford CT

Honolulu HI

Houston TX

Indianapolis IN

Corporate Income Tax a

Federal 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o

Regional – 0.98q,v 4.63 6.00q 4.53s 5.00s 9.00q,x 6.40s 0.98q,v 7.50w

Local 2.00 – – –bo – – – – – –

Combined income tax rate 35.32z 34.64z 37.06z 37.96z 36.99z 37.30z 39.94z 38.22z 34.64z 38.95z

Manufacturing tax reduction b

Federal 3.06p 3.06p 2.92p 3.06p 3.06p 3.06p 3.06p 3.06p 3.06p 3.06p

Regional – – 0.42p – – – – – – –

Combined mfg tax rate 32.26 31.58 33.72 34.90 33.93 34.24 36.88 35.16 31.58 35.89

Effective income tax rate, overall average c 25.42 27.27 29.04 27.28 29.94 30.08 24.51 33.05 26.84 30.82

Capital Tax d

Tax based on:

Capital stock – – – – – – 0.310x – – –

Net equity – – – – – – – – – –

Total assets – – – – – 0.250 – – – –

Debt/borrowings – – – – – – – – – –

Sales Tax e

Refundable GST/VAT:

Federal f – – – – – – – – – –

Regional f – – – – – – – – – –

Non-refundable sales tax:

Regional f 5.75 6.25 2.90 6.00 5.00 7.00 6.35 4.00 6.25 7.00

Local f 2.25 1.91 4.72 – 2.50 – – 0.50 1.68 –

Property Tax g

Land h 3.90 2.82 2.44 3.01 1.32 1.80 1.95 1.24 2.68 2.47av

Buildings h 3.90 2.82 2.44 3.01 1.32 1.80 1.95 1.24 2.68 2.47av

Machinery & equipment i – 2.82 2.44 2.43bj – 1.80 1.95as – 2.68 2.47av

Inventory j – 2.82bp – – – 1.80bs – – 2.68bp –

Total property-based taxes:

Mfg avg (12 operations) k $4.27 $8.22 $7.10 $6.95 $1.32 $6.02 $4.04 $2.56 $7.61 $4.77

Services avg (7 operations) k – $1.44 $1.23 $1.23 – $0.92 $0.99 – $1.36 $1.05

Local Business Taxes

Taxes based on:

Gross receipts l 0.26u – – – – – – – – –

Salaries m – – – – – – – – – –

Employees n – – – – – – – – – –

United States

KPMG’s Guide to International Business Location Costs B . 15

Federal, regional, and local tax rates – In percent

Jackson MS

Kansas City MO

Las Vegas

NVLexington

KY

Little Rock AR

Los Angeles

CAMadison

WIManchester

NHMemphis

TNMiami

FL

Corporate Income Tax a

Federal 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o

Regional 5.00s 6.25q – 6.00q,s 6.50s 8.84 7.90q 8.50 6.50q 5.50q,s

Local – 1.00 – 2.75 – – – – – –

Combined income tax rate 37.30z 37.72z,ab 34.00 39.78z 38.29z 39.83z 39.21z 39.61z 38.29z 37.63z

Manufacturing tax reduction b

Federal 3.06p 2.87p 3.06p 2.88p 3.06p 3.06p 3.06p 3.06p 3.06p 2.89p

Regional – 0.56p – 0.54p – – – – – 0.50p

Combined mfg tax rate 34.24 34.29 30.94 36.36 35.23 36.77 36.15 36.55 35.23 34.24

Effective income tax rate, overall average c 30.03 26.78 27.12 31.89 30.08 28.96 30.25 31.92 30.20 28.57

Capital Tax d

Tax based on:

Capital stock – – – – 0.300 – – – – –

Net equity – – – – – – – – – –

Total assets 0.250 0.013ao – – – – – – 0.250bd –

Debt/borrowings – – – – – – – – – –

Sales Tax e

Refundable GST/VAT:

Federal f – – – – – – – – – –

Regional f – – – – – – – – – –

Non-refundable sales tax:

Regional f 7.00 4.23 6.85 6.00 6.50 7.50 5.00 – 7.00 6.00

Local f – 3.59 1.25 – 2.50 1.50 0.50 – 2.25 1.00

Property Tax g

Land h 2.61 3.28 1.17 1.16 1.35 1.33 2.33 2.44 3.11 2.16

Buildings h 2.61 3.13 1.17 1.16 1.35 1.33 2.33 2.44 3.11 2.16

Machinery & equipment i 2.61 3.21 1.17 0.15 1.35 1.33 – – 2.33 2.16

Inventory j 2.61bs – – 0.49 1.35 – – – – –

Total property-based taxes:

Mfg avg (12 operations) k $8.79 $9.36 $3.48 $1.72 $4.59 $4.50 $2.47 $2.61 $7.21 $6.72

Services avg (7 operations) k $1.33 $1.63 $0.60 $0.07 $0.69 $0.68 – – $1.19 $1.09

Local Business Taxes

Taxes based on:

Gross receipts l – 0.08bt – – – – – – – –

Salaries m – – 1.05 – – – – 0.75bg – –

Employees n – – – – – – – – – $4.50ae

United States

Competitive Alternatives, 2014 EditionB . 16

Federal, regional, and local tax rates – In percent

Minneapolis MN

Mobile AL

Montgomery AL

Nashville TN

New Orleans

LA

New York City NY

North Virgina (Metro DC)

VA

Oklahoma City OK

Omaha NE

Orlando FL

Corporate Income Tax a

Federal 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o

Regional 9.80q 6.50 6.50 6.50q 8.00q,s 7.10q,r 6.00q 6.00 7.81q,s 5.50q,s

Local – – – – – –bo – – – –

Combined income tax rate 40.47z 36.08z,ac 36.08z,ac 38.29z 36.56z,ac 38.69z 37.96z 37.96z 38.54z,aa 37.63z

Manufacturing tax reduction b

Federal 3.06p 2.86p 2.86p 3.06p 2.82p 3.06p 2.88p 2.88p 2.84p 2.89p

Regional – 0.59p 0.59p – 0.72p 1.20bc 0.54p 0.54p 0.65p 0.50p

Combined mfg tax rate 37.41 32.63 32.63 35.23 33.02 34.43 34.54 34.54 35.06 34.24

Effective income tax rate, overall average c 26.19 28.89 29.19 30.54 17.98 27.84 27.94 29.93 22.93 29.15

Capital Tax d

Tax based on:

Capital stock – – – – – – – – 0.150an –

Net equity – – – – – 0.150r – 0.125al – –

Total assets 0.025ak 0.175ai 0.175ai 0.250bd 0.300ap – – – – –

Debt/borrowings – – – – – – – – – –

Sales Tax e

Refundable GST/VAT:

Federal f – – – – – – – – – –

Regional f – – – – – – – – – –

Non-refundable sales tax:

Regional f 6.88 4.00 4.00 7.00 4.00 4.00 4.30 4.50 5.50 6.00

Local f – 6.50 6.00 2.50 4.88 4.63 1.70 3.88 1.50 0.50

Property Tax g

Land h 3.47 1.27 0.73 1.41 1.11 5.34 1.26 1.29 2.20 1.96

Buildings h 3.47 1.27 0.73 1.41 1.66bk 5.34 1.26 1.29 2.20 1.96

Machinery & equipment i – 1.27 0.73 1.06 1.66bk – 2.00 1.62bf 2.20 1.96

Inventory j – – – – 1.66br – – 1.62bp – –

Total property-based taxes:

Mfg avg (12 operations) k $4.02 $3.41 $1.98 $3.22 $1.28 $8.88 $5.38 $2.65 $2.85 $5.65

Services avg (7 operations) k – $0.64 $0.37 $0.54 $0.84 – $1.12 $0.25 $1.12 $1.00

Local Business Taxes

Taxes based on:

Gross receipts l – – – – – – 0.21az – – –

Salaries m – – – – – – – – – –

Employees n – – – – – – – – – $6.16aj

United States

KPMG’s Guide to International Business Location Costs B . 17

Federal, regional, and local tax rates – In percent

Philadelphia PA

Phoenix AZ

Pittsburgh PA

Porland OR

Providence RI

Raleigh NC

Riverside-San Bernardino

CASacramento

CASaginaw

MI

Salt Lake City UT

Corporate Income Tax a

Federal 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o

Regional 9.99q 6.50q,bn 9.99q 7.60s 9.00y 6.00q,bh 8.84 8.84 6.00q 5.00q

Local –bo – – 1.45bo – – – – –bo –

Combined income tax rate 40.59z 38.29z 40.59z 39.97z 39.94z 37.96z 39.83z 39.83z 37.96z 37.30z

Manufacturing tax reduction b

Federal 2.75p 2.86p 2.75p 3.06p 3.06p 3.06p 3.06p 3.06p 3.06p 2.91p

Regional 0.90p 0.59p 0.90p – – – – – – 0.45p

Combined mfg tax rate 36.94 34.84 36.94 36.91 36.88 34.90 36.77 36.77 34.90 33.94

Effective income tax rate, overall average c 27.11 27.62 28.03 31.89 28.64 28.84 29.86 29.28 27.86 28.88

Capital Tax d

Tax based on:

Capital stock 0.067am – 0.067am – 0.025y – – – – –

Net equity – – – – – – – – – –

Total assets – – – – – 0.150bd – – – –

Debt/borrowings – – – – – – – – – –

Sales Tax e

Refundable GST/VAT:

Federal f – – – – – – – – – –

Regional f – – – – – – – – – –

Non-refundable sales tax:

Regional f 6.00 5.60 6.00 – 7.00 4.75 7.50 7.50 6.00 4.70

Local f – 2.20 1.00 – – 2.00 0.50 1.00 – 2.15

Property Tax g

Land h 2.47 2.43 2.34 1.28 2.15 0.94 1.12 1.14 2.66 1.55

Buildings h 2.47 2.43 2.34 1.28 2.15 0.94 1.12 1.14 2.66 1.55

Machinery & equipment i – 2.43 – 1.92 2.98au 0.94 1.12 1.14 1.95bj 1.55

Inventory j – – – – – – – – – –

Total property-based taxes:

Mfg avg (12 operations) k $3.00 $7.08 $2.75 $5.11 $2.71 $2.71 $3.49 $3.52 $5.21 $4.62

Services avg (7 operations) k – $1.13 – $0.98 $1.51 $0.48 $0.57 $0.58 $0.99 $0.78

Local Business Taxes

Taxes based on:

Gross receipts l 0.142be – – – – – – – – –

Salaries m – – – – – – – – – –

Employees n – – – – – – – – – –

United States

Competitive Alternatives, 2014 EditionB . 18

Federal, regional, and local tax rates – In percent

San Antonio

TX

San Diego

CA

San Francisco

CASeattle

WAShreveport

LA

Sioux Falls SD

Spartanburg SC

Spokane WA

St. Louis MO

Tampa FL

Corporate Income Tax a

Federal 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o 34.00o

Regional 0.98q,v 8.84 8.84 – 8.00q,s – 5.00q – 6.25q 5.50q,s

Local – – – – – – – – –bo –

Combined income tax rate 34.64z 39.83z 39.83z 34.00 36.56z,ac 34.00 37.30z 34.00 37.06z,ab 37.63z

Manufacturing tax reduction b

Federal 3.06p 3.06p 3.06p 3.06p 2.82p 3.06p 3.06p 3.06p 2.87p 2.89p

Regional – – – – 0.72p – – – 0.56p 0.50p

Combined mfg tax rate 31.58 36.77 36.77 30.94 33.02 30.94 34.24 30.94 33.63 34.24

Effective income tax rate, overall average c 27.70 29.23 27.66 26.06 19.70 28.11 28.56 27.54 26.06 28.95

Capital Tax d

Tax based on:

Capital stock – – – – – – – – – –

Net equity – – – – – – 0.100 – – –

Total assets – – – – 0.300ap – – – 0.013ao –

Debt/borrowings – – – – – – – – – –

Sales Tax e

Refundable GST/VAT:

Federal f – – – – – – – – – –

Regional f – – – – – – – – – –

Non-refundable sales tax:

Regional f 6.25 7.50 7.50 6.50 4.00 4.00 6.00 6.50 4.23 6.00

Local f 2.00 0.50 1.50 2.93 4.60 2.00 – 2.20 4.20 1.00

Property Tax g

Land h 3.49 1.07 1.21 1.41 1.71 1.81 4.96aq 1.37 3.26 2.05

Buildings h 3.49 1.07 1.21 1.41 2.56bk 1.81aw 4.96aq 1.37 3.26 2.05

Machinery & equipment i 3.49 1.07 1.21 1.41 2.56bk – 4.96aq 1.37 3.34 2.05

Inventory j 3.49bp – – – 2.56br – – – – –

Total property-based taxes:

Mfg avg (12 operations) k $9.60 $3.58 $4.31 $4.53 $1.72 $1.22 $12.17 $4.17 $9.79 $5.78

Services avg (7 operations) k $1.78 $0.55 $0.62 $0.72 $1.30 – $2.18 $0.70 $1.69 $1.04

Local Business Taxes

Taxes based on:

Gross receipts l – 0.035ba – 1.500bb 0.100ay – – 1.500bb – –

Salaries m – – – – – – – – – –

Employees n – – – – – – – – – –

United States

KPMG’s Guide to International Business Location Costs B . 19

Federal, regional, and local tax rates – In percent

Trenton NJ

Wichita KS

Wilmington DE

Youngstown OH Footnotes

Corporate Income Tax a a Percentage of taxable income. Minor adjustments required in the calculation of taxable income in each jurisdiction are not individually disclosed. Tax rates shown in this exhibit are for the size of entity examined in this study. Many jurisdictions offer lower income tax rates for small businesses.

b Manufacturing tax rate reductions may reduce on a pro-rata basis where a significant component of a company’s payroll or capital assets are not devoted to manufacturing or processing operations.

c The effective income tax rates for the overall average (services and manufacturing) in this study vary from the combined nominal income tax rates in each location due to the impact of adjustments to taxable income and income tax credits.

d Percentage of taxable capital, determined on the general basis indicated. In many jurisdictions, the general tax base indicated here is subject to minor adjustment.

e Percentage of sales price.

f General rate. Other rates may apply to specified articles.

g The Property Tax category includes all property-based taxes, including the property-based component of multi-base local business taxes. Property tax rates relate to the suburban or urban areas identified in the real estate research for this study as offering sites suitable for the types of operation being examined.