community webinar independent contractor. insurance forms and endorsements vary based on insurance...

TRANSCRIPT

Community Webinar

Independent Contractor

www.InsuranceCommunityUniversity.com

Insurance forms and endorsements vary based on insurance company; changes in edition dates; regulations; court decisions;

and state jurisdiction. The instructional materials provided by The Insurance Community Center and its authors is intended as

a general guideline and any interpretations provided by The Community do not modify or revise insurance policy language. Information which is copyrighted and proprietary to Insurance

Services Office, Inc. (“ISO Material”) is included in this publication. Use of the ISO Material is limited to ISO

Participating Insurers and their Authorized Representatives. The Insurance Community Center assumes neither liability nor responsibility to any person or business with respect to any loss that is alleged to be caused directly or indirectly as a result of

the instructional materials provided. Insight Insurance Consulting

[email protected]@insuranceacommunitycenter.com www.insuranceacommunitycenter.com

Copyright 2011©

2

www.InsuranceCommunityUniversity.com

Presents Monthly Webinars Free to Community Members.

Community webinars are archived on the Community homepage under the right hand tab titled: Webinar Archive

3

www.InsuranceCommunityUniversity.com

In addition the community has unique business networking opportunities.

Enjoy the Weekly Newsletter on a specific topic with a tip of the week; claim; quiz flash and articles

4

www.InsuranceCommunityUniversity.com

One Flat Fee per Office includes Monthly webinars approved for CE in

California for a total of 28 hours Test and Learn Audio Presentations on insurance topics Checklists Power point presentations for client

and/or peer training

5

When is an Independent Contractor really independent?

www.InsuranceCommunityUniversity.com

Independent Contractor vs. EmployeeHow does it relate to Workers

Compensation?How does it relate to Employment

Practice Liability? Independent Contractor as relates to

the construction industry

7

www.InsuranceCommunityUniversity.com8

www.InsuranceCommunityUniversity.com

An IC is either a person or organization that is hired to perform services under an express or implied contract and is NOT subject to the other party’s control, the manner and means of performing the services

Typically the party engaging the IC is not liable for the acts of the IC Exceptions apply according to case law –

often affects the construction relationship9

www.InsuranceCommunityUniversity.com

An employee is a (natural) person who works in the service of another person under an express or implied contract of hire, under which the employer has the right to control the details of work performance

▪ Black's Law Dictionary

10

www.InsuranceCommunityUniversity.com11

www.InsuranceCommunityUniversity.com12

www.InsuranceCommunityUniversity.com13

www.InsuranceCommunityUniversity.com14

www.InsuranceCommunityUniversity.com15

www.InsuranceCommunityUniversity.com16

www.InsuranceCommunityUniversity.com17

www.InsuranceCommunityUniversity.com

It is important to note that the IRS assumes that a worker is an employee. It is sometimes difficult to determine the status of a worker. If you are unsure whether to classify a worker as an independent contractor or employee, you can file a Form SS-8 to request a determination.

18

www.InsuranceCommunityUniversity.com

Many states have guidelinesExamples:

Oregon typically follows the IRS standards

Rhode Island – an IC must self-certify Massachusetts – has put GC on notice

they are responsible for WC coverage for an IC creating a presumptive employee – employer relationship

19

www.InsuranceCommunityUniversity.com20

www.InsuranceCommunityUniversity.com21

www.InsuranceCommunityUniversity.com22

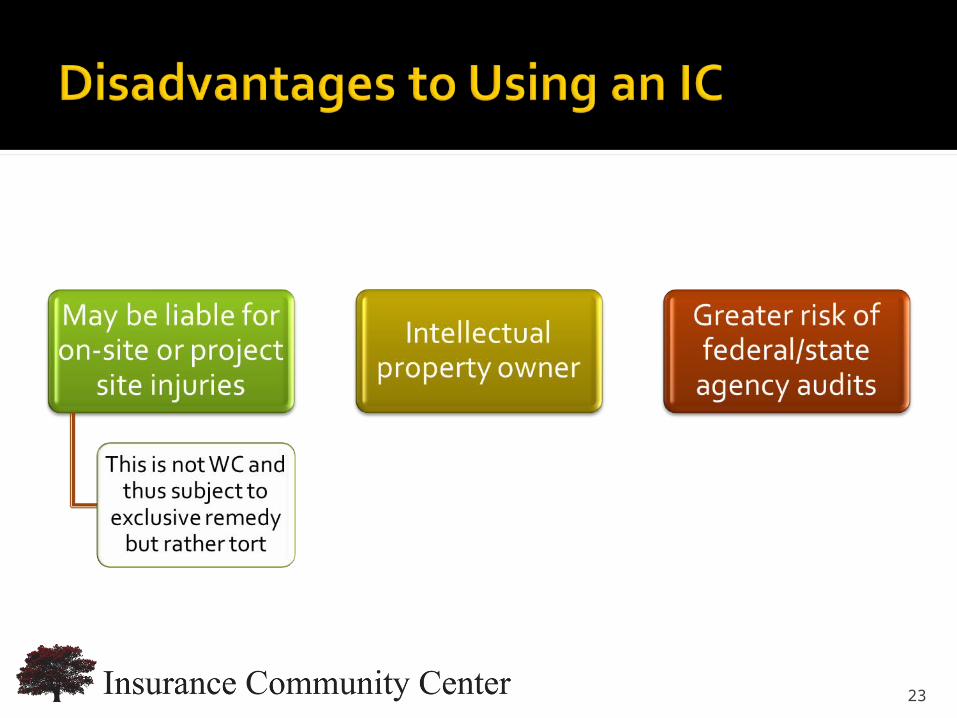

www.InsuranceCommunityUniversity.com23

www.InsuranceCommunityUniversity.com

Oregon typically follows the IRS standards

Rhode Island – an IC must self-certifyMassachusetts – has put GC on

notice they are responsible for WC coverage for an IC creating a presumptive employee – employer relationship

24

www.InsuranceCommunityUniversity.com

NY has stated that if it a reasonable risk that ICs could be misclassified, then it is reasonable for the WC insurer to charge premium to the “employer” unless IC can prove WC coverage

25

www.InsuranceCommunityUniversity.com

California has the following guidelines for ICs: Independent business / holds a business license Control over the work / provides tools or

equipment Is paid by the project (not by time) No fraudulent misclassification Performs services not generally part of business Intends to establish an IC relationship

26

www.InsuranceCommunityUniversity.com

The principal body of law governing retirement, health care, disability and similar types of benefit plans is the Employee Retirement Income Security Act of 1974 ("ERISA"),

The Court has described the common law tests to use

27

www.InsuranceCommunityUniversity.com

An employee: the “conventional master-servant relationship as understood by the common law agency doctrine."

An IC: the hiring party's right to control the manner and means by which the product is accomplished" Did not adopt the IRS “test” but in the

Darden case, identified 12 specific points to determine IC status

28

www.InsuranceCommunityUniversity.com

Skill requiredSource of tools and instrumentalitiesLocation where work performedDuration of relationship of partiesHiring party's right (or lack thereof)

to assign additional projectsHired party's discretion over when

and how long to work

29

www.InsuranceCommunityUniversity.com

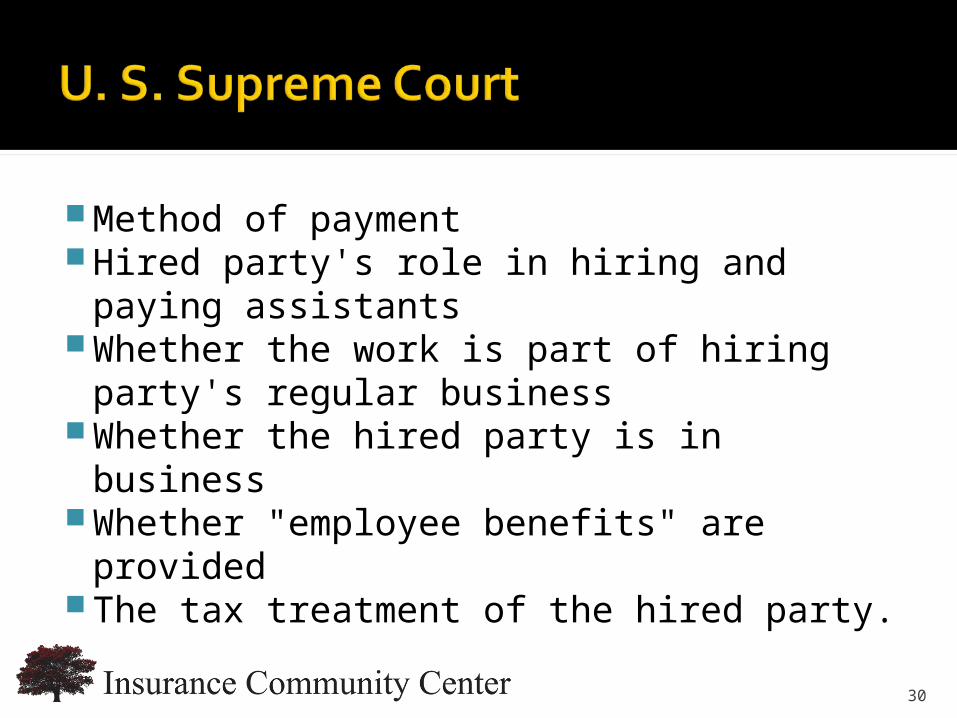

Method of payment Hired party's role in hiring and paying

assistants Whether the work is part of hiring

party's regular business Whether the hired party is in business Whether "employee benefits" are

provided The tax treatment of the hired party.

30

www.InsuranceCommunityUniversity.com31

www.InsuranceCommunityUniversity.com

The 9th Circuit Court of Appeals ruled in this case (and the USSC refused to hear the case) that temporary employees and “freelancers” hired by Microsoft in the late 1980’s and early 90’s were in fact employees at least for their inclusion in the Savings Plus and the Stock Purchase Plan established by Microsoft for its employees

32

www.InsuranceCommunityUniversity.com

Much of the litigation could been avoided if the benefit plans had been drafted differently and if the company had not made a key concession early in the case.

Businesses must review and, where appropriate, amend their benefit plans and forms of contract Legal and accounting advice is critical to

structure properly33

www.InsuranceCommunityUniversity.com

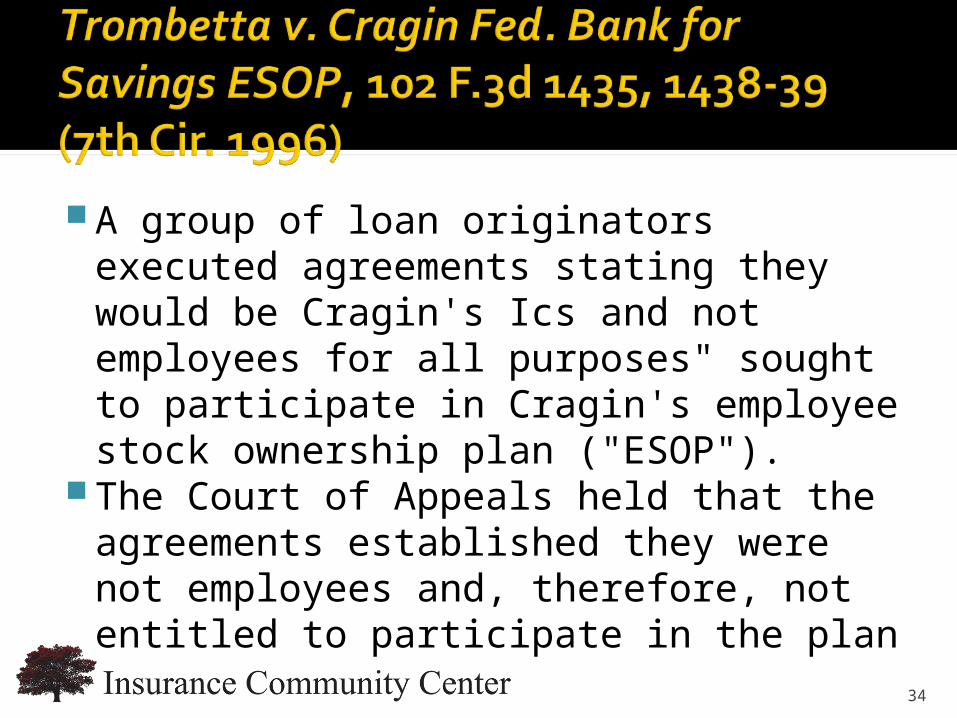

A group of loan originators executed agreements stating they would be Cragin's Ics and not employees for all purposes" sought to participate in Cragin's employee stock ownership plan ("ESOP").

The Court of Appeals held that the agreements established they were not employees and, therefore, not entitled to participate in the plan

34

www.InsuranceCommunityUniversity.com

A group of newspaper carriers who signed IC agreements with no-benefits language were reclassified by the IRS as common law employees for employment tax purposes.

The Court of Appeals upheld their exclusion from the company's retirement plans, finding that the individual contracts alone were a sufficient basis for excluding the workers

35

www.InsuranceCommunityUniversity.com

New York Life was sued by one of their agents who claimed that the company terminated his agency contract in violation of ERISA and ADEA

The agent had to establish that he was an employee and not an IC

After applying the Darden factors to the agency contract, the court concluded that the agent was an independent contractor.

36

www.InsuranceCommunityUniversity.com

The court found some employee related factors Life insurance, pension and 401(k) plans Company trained agent during first 3 yrs Not persuasive

Court found persuasive the signed contract where, in clear language, Barnhart would be an IC, paid commission and claimed self-employment on his tax returns

37

www.InsuranceCommunityUniversity.com

Request and receive W-9 Provide 1099 MiscellaneousRequire copy of business license

38

www.InsuranceCommunityUniversity.com39

www.InsuranceCommunityUniversity.com

Confirm status by creating a written contract that includes the status as IC that includes a statement that the IC assumes responsibility for taxes, withholdings and insurance

Get advice Lawyers IRS can determine if IC by submitting

Form SS-8 – Determination of Employee Work Status

40

www.InsuranceCommunityUniversity.com

Depending on the state – insurer could charge premium based on reasonable expectation of misclassification

Clients should always verify that a hired IC provides WC coverage for employees

41

www.InsuranceCommunityUniversity.com

Most EPLI policies exclude IC from coverage

Include third party discrimination and harassment coverage to fill the gap

42

www.InsuranceCommunityUniversity.com

Majority of forms exclude IC from coverage

43

www.InsuranceCommunityUniversity.com

This area is developing law around the country in both state and federal courts

Help your client understand that just by calling someone an IC doesn’t make it so

Give them insurance guidance but don’t step over the line into the area of law

44

www.InsuranceCommunityUniversity.com

Laurie Infantino [email protected] 714 803 5830

Marjorie Segale [email protected]

m 714 206 9583

45