colorado partnership · colorado partnership or s corporation return of income and composite...

TRANSCRIPT

COLORADO PARTNERSHIPOR S CORPORATION

RETURN OF INCOMEAND COMPOSITE

NONRESIDENT

INCOME TAX RETURN

• Returnisduethreeandone-halfmonthsafterthecloseofthetaxyear.MAIL TO: Colorado Department of Revenue, Denver, Colorado 80261-0006.

• PartnershipsandScorporationswith nonresidentmembersshouldfilea compositereturnforthosemembers. Completelines10-23ofForm106to paythetaxontheColoradosourceincome. >Nootherformsmustbecompleted. >Nospecialelectionorsignatureisrequiredbythememberforinclusion. >MembersdonothavetofileaColoradoindividualreturn.

Inlieuofacompositereturn,therearetwootheroptionsthatpartnershipsandScorporations canusetomeetthenonresidentmemberfilingrequirements.However,theseoptionsrequire additionalformsandcannotbeusedifthememberwillnotbefilingaColoradoindividualreturn. Seepage4fordetails.

(10/28/09)

Modernized e-File (MeF) Partnership/S-Corporation Electronic FilingBoth Federal and Colorado returns

Forinformation,seewww.TaxColorado.com

OnlineServices,Partnershipe-file

Colorado Online Tax PaymentsForinformation,see

www.colorado.gov/paytax

Colorado Department of RevenueTax Forms, Information and E-Services

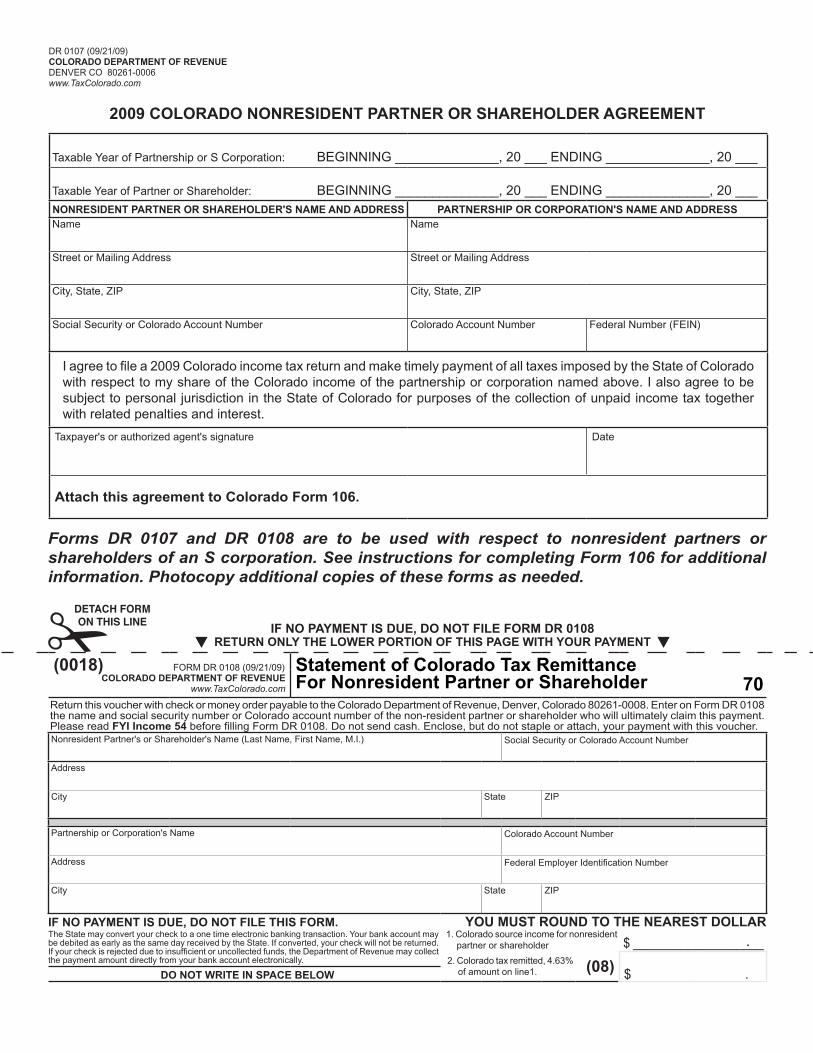

Forms DR 0107 and DR 0108 are to be used with respect to nonresident partners or shareholders of an S corporation. See instructions for completing Form 106 for additional information. Photocopy additional copies of these forms as needed.

DETACH FORM ON THIS LINE

IF NO PAYMENT IS DUE, DO NOT FILE FORM DR 0108 RETURN ONLY THE LOWER PORTION OF THIS PAGE WITH YOUR PAYMENT

(0018) FORMDR0108(09/21/09)COLORADO DEPARTMENT OF REVENUE

www.TaxColorado.com

Statement of Colorado Tax Remittance For Nonresident Partner or Shareholder 70

ReturnthisvoucherwithcheckormoneyorderpayabletotheColoradoDepartmentofRevenue,Denver,Colorado80261-0008.EnteronFormDR0108thenameandsocialsecuritynumberorColoradoaccountnumberofthenon-residentpartnerorshareholderwhowillultimatelyclaimthispayment.PleasereadFYI Income 54beforefillingFormDR0108.Donotsendcash.Enclose,butdonotstapleorattach,yourpaymentwiththisvoucher.NonresidentPartner'sorShareholder'sName(LastName,FirstName,M.I.) SocialSecurityorColoradoAccountNumber

Address

City State ZIP

PartnershiporCorporation'sName ColoradoAccountNumber

Address FederalEmployerIdentificationNumber

City State ZIP

IF NO PAYMENT IS DUE, DO NOT FILE THIS FORM. YOU MUST ROUND TO THE NEAREST DOLLARTheStatemayconvertyourchecktoaonetimeelectronicbankingtransaction.YourbankaccountmaybedebitedasearlyasthesamedayreceivedbytheState.Ifconverted,yourcheckwillnotbereturned.Ifyourcheckisrejectedduetoinsufficientoruncollectedfunds,theDepartmentofRevenuemaycollectthepaymentamountdirectlyfromyourbankaccountelectronically.

1.Coloradosourceincomefornonresidentpartnerorshareholder $___________________

2.Coloradotaxremitted,4.63%ofamountonline1. (08) $ .DO NOT WRITE IN SPACE BELOW

DR0107(09/21/09)COLORADO DEPARTMENT OF REVENUEDENvERCO80261-0006www.TaxColorado.com

TaxableYearofPartnershiporSCorporation: bEgINNINg______________,20___ENDINg______________,20___

TaxableYearofPartnerorShareholder: bEgINNINg______________,20___ENDINg______________,20___NONRESIDENT PARTNER OR SHAREHOLDER'S NAME AND ADDRESS PARTNERSHIP OR CORPORATION'S NAME AND ADDRESSName Name

StreetorMailingAddress StreetorMailingAddress

City,State,ZIP City,State,ZIP

SocialSecurityorColoradoAccountNumber ColoradoAccountNumber FederalNumber(FEIN)

Iagreetofilea2009ColoradoincometaxreturnandmaketimelypaymentofalltaxesimposedbytheStateofColoradowithrespecttomyshareoftheColoradoincomeofthepartnershiporcorporationnamedabove.IalsoagreetobesubjecttopersonaljurisdictionintheStateofColoradoforpurposesofthecollectionofunpaidincometaxtogetherwithrelatedpenaltiesandinterest.

Taxpayer'sorauthorizedagent'ssignature Date

Attach this agreement to Colorado Form 106.

2009 COLORADO NONRESIDENT PARTNER OR SHAREHOLDER AGREEMENT

.

INSTRUCTIONS FOR EXTENSION PAYMENT VOUCHER FOR COMPOSITE FILING

DETACH FORM ON THIS LINE

IF NO PAYMENT IS DUE, DO NOT FILE FORM 158N RETURN ONLY THE LOWER PORTION OF THIS PAGE WITH YOUR PAYMENT

(0049) FORMDR158N(09/21/09)COLORADO DEPARTMENT OF REVENUE

www.TaxColorado.com

Payment Voucher for Extension of Time for Filing a Colorado Composite Nonresident Income Tax Return 70

Forthecalendaryear2009orthefiscalyear:StartDate:_____________ ,2009EndDate:____________.

ReturnthisvoucherwithcheckormoneyorderpayabletotheColoradoDepartmentofRevenue,Denver,Colorado80261-0008.WriteyourColoradoAccountNumberand“2009Form158N”onyourcheckormoneyorder.Donotsendcash.Enclose,butdonotstapleorattach,yourpaymentwiththisvoucher.Name ColoradoAccountNumber

Address FederalEmployerIdentificationNumber

City State ZIP

IF NO PAYMENT IS DUE, DO NOT FILE THIS FORM. YOU MUST ROUND TO THE NEAREST DOLLAR

TheStatemayconvertyourchecktoaonetimeelectronicbankingtransaction.YourbankaccountmaybedebitedasearlyasthesamedayreceivedbytheState.Ifconverted,yourcheckwillnotbereturned.Ifyourcheckisrejectedduetoinsufficientoruncollectedfunds,theDepartmentofRevenuemaycollectthepaymentamountdirectlyfromyourbankaccountelectronically.

AMOUNT OF PAYMENT

(08) $ .DO NOT WRITE IN SPACE BELOW

Coloradoincometaxreturnsareduetobefiledthree-and-one-halfmonthsafterthecloseofthetaxyear.

An automatic six-month extension of time for filing theColorado composite income tax return is allowed for alltaxpayers.However,anextensionoftimetofile isnotanextensionoftimetopaythetax.Ifatleast90%ofthenettaxliability(line15,Form106)isnotpaidbytheoriginalduedateofthereturn,penaltyandinterestwillbeassessed.If90%ormoreofthenettaxliabilityispaidbytheoriginalduedateofthereturnandthebalanceofthetaxispaidwhenthereturnisfiledbythelastdayoftheextensionperiod,onlyinterestwillbeassessed.

Form158Nistobeusedtomakewhateverpaymentmustbemadebytheoriginalduedateofthereturntomeetthe90%requirement.Useform158Nonlytoremitpaymentforthosenon-residentpartnersandshareholderswhowillbeincluded inacomposite return.Withholdingpayments forpartnersandshareholdersnotincludedinacompositereturnmustberemittedusingformDR0108.

Ifaftertheoriginalduedateofthereturnitisfoundthattheamountthathasbeenpaidisinsufficienttomeetthe90%requirement, additional payment should be submitted assoonaspossibletoreducefurtheraccumulationofpenaltyandinterest.MakesuchpaymentonForm158N.

AfederalextensionoftimeforfilingwillnotbeacceptedforColoradopurposes.

SubmitForm158Nwithpaymentto:

TheColoradoDepartmentofRevenue1375ShermanStreetDenver,CO80261-0008

DO NOT SUBMIT FORM 158N WITHOUT A PAYMENT.

besuretoroundyourpaymenttothenearestdollar.Youmustenter00afterthedecimalpoint.Theamountonthecheck and the amount entered on the payment vouchermustbethesame.Thiswillhelpmaintainaccuracyinyourtaxaccount.

ONLINE TAX PAYMENTSYoumaymakeyourextensionpaymentbyecheckorcreditcardatwww.colorado.gov/paytax.Pleasenotethereisanadditionalfeeifyoudecidetousethiselectronicpaymentmethod.ThisfeeispaidtoathirdpartywhoprovidestheseservicesforColorado.gov.Taxpaymentsremittedviaecheck,adirectdebitfromyourcheckingaccount,willbesubjecttoa$1.00administrativeprocessingfee.Theprocessingfeeforcreditcardtransactionsis2.25%ofthetaxpaymentmade,plusanadditional$0.75pertransaction.

WHO MUST FILE FORM 106Anypartnership,jointventure,commontrustfund,limited

association, pool or working agreement, limited liabilitycompanyoranyothercombinationofpersonsorinterests,whichisrequiredtofileafederalpartnershipreturnofincome,mustfileaColoradoForm106 ifanyof thepartnershipincomeisfromColoradosources.

AnScorporationmust fileForm106 for any year it isdoingbusinessinColorado.Doingbusinessinastateisdefinedashavingincomearisingfromtheactivityofoneormoreemployeeslocatedinthestate;orarisingfromthefact that realorpersonalproperty is located in thestateforbusinesspurposes.AcorporationwillbedeemedtobedoingbusinessinColoradoifitisengagedinanyactivitiesinColoradowhicharebeyondtheprotectionaffordedbyPublicLaw86-272.

AnScorporationisacorporationforwhichavalidelectionisineffectundersection1363(a)oftheInternalRevenueCode.IfacorporationisanScorporationforfederalincometaxpurposes it isanScorporation forColorado incometaxpurposes.ScorporationsarenotsubjecttoColoradoincometax.

Achangeorcorrectiononyour returnmustbereportedonacorrectedForm106.ChecktheboxatthetopofthecorrectedForm106.Includepriorpaymentsonline16ofthecorrectedform.

Whenusedinthisinstructionbookletoronthepartnershipforms, the term partnership includes limited liabilitycompanies filing as partnerships for federal income taxpurposes,andthetermpartnerincludesmembersofsuchlimitedliabilitycompanies.

DUE DATES FOR FILING RETURNThereturn isduetobefiled threeandone-halfmonths

afterthecloseofthetaxyearplusanautomaticsix-monthextension. See the extension payment instructions forfurtherinformation.

NONRESIDENT PARTNERS/SHAREHOLDERSA partnership or an S corporation is required to ensure

thatitsnonresidentpartnersandshareholderssatisfytheirColoradoincometaxliabilitiesresultingfromtheColoradosource incomeearnedby thepass throughentity.This isaccomplishedinoneofthreeways:

• Fileacompositereturnonbehalfofthenonresidentmembers.Thetaxdueonthecompositefilingshallbe4.63%oftheColorado-sourceincomeofthepartnersorshareholdersincludedinthecompositereturn.

• ProvideacompletedformDR0107eachyearforeachnonresident partner/shareholder establishing that he/shewillfileaColoradoincometaxreturn,or

• ProvideacompletedformDR0108foreachnonresidentpartner/shareholder. Withhold 4.63% of eachnonresident partner/shareholder's Colorado sourceincomeandsubmitthepaymentwithformDR0108.AseparateDR0108mustbesubmittedforeachpartnerorshareholderforwhomapaymentismade.

YoumustindicateinColumn4ofPartIIIwhichofthesethreefiling requirementshasbeenelectedbyeachnonresidentpartner/shareholder.RefertoFYIIncome54foradditionalinformationoncompositefiling,theagreementtofileformDR0107,andthewithholdingformDR0108.

ADDITIONAL INFORMATION AvAILAbLE

All forms, FYIs and other information are available through theTax Information Index at:www.TaxColorado.comoryoucancallforinformationat(303)238-SERv(7378).

INSTRUCTIONS FOR COMPLETING FORM 106

DECLARATION OF ESTIMATED TAxEstimatedpaymentsarerequiredifthetaxattributableto

anypartnerorshareholderincludedinacompositereturnisexpectedtoexceed$1,000.SuchestimatepaymentsshouldberemittedwithFormDR0106EP.

DISTRIbUTIONSColorado modifications and credits from Form 106CR,

ifany,aretobedistributedtoshareholdersontheirstockownershippercentageandtopartnersontheirdistributivesharepercentage.AdviseeachColoradoresidentpartnerorshareholderofhis/hershareofthepartnershiporcorporationmodificationsandcredits.Adviseeachresidentshareholderofhis/hershareofanyincometaxpaidtootherstatesbythecorporationsohe/shecancompute thecredit for taxpaidotherstates.

APPORTIONMENT OF INCOMEApartnershiporScorporationdoingbusinessinmorethan

onestatemustapportionitsColoradosourceincometoanystatesinwhichtheentity isdoingbusiness.Thisensuresincomeisreportedtothestateinwhichtheincomeisearnedandtaxable.SeeFYIIncome59fordetailsregardingthefollowingapportionmentmethods.

PartnershipsIncomeisgenerallyapportionedinoneoftwoways:

• Singlesalefactor• Colorado–source incomeofnonresident individuals

method

S CorporationsIncome is generally apportioned using the single sales

method.

Not Apportioning Income—ApartnershiporScorporationdoing business only in Colorado will source 100% of itsincometoColorado.

Single Sales Factor—All business income must beapportionedusingasinglefactorsales.Non-businessincomemayeitherbedirectlyallocatedtotheappropriatestateortreatedasbusinessincome,subjecttothesinglesalesfactorapportionment.CompleteandattachPartIvtoyourreturnifyouareapportioningincomeusingthesinglesalesfactorapportionmentmethod.

Colorado Source Income of Nonresident—ColoradosourceincomeapportionedunderSection39-22-109,CRSiscomputedbyincludingincomethatisdeterminedtobefromColoradosources.AttachascheduletoForm106explaininghowColoradosourceincomewasdetermined.ModificationsmaybesourcedtoColoradoonlytotheextentthattheincometowhichtheyrelateissourcedtoColorado.

COMPLETING FORM 106INCOMELINE 1: Entertheordinaryincomeor(loss)fromline1of

federalScheduleK.

LINE 2: EnterthetotalofallotherincomelistedonfederalScheduleK.Forpartnerships,thiswouldbethe

totaloftheamountsenteredonlines2,3c,4,5,6a, 7, 8, 9a, 10and11of federalScheduleK.ForScorporations,thiswouldbethetotaloftheamountsenteredonlines2,3c,4,5a,6,7,8a,9and10offederalScheduleK.Alsoincludeanygainfromthesaleofassetssubjecttosection179thatisnotreportedonScheduleK.

MODIFICATIONS AND DEDUCTIONSLINE 3: Enter the Coloradomodifications that increase

federalincome.

Enter any interest income (net of premiumamortization)fromstateormunicipalobligationssubjecttotaxbyColorado.DonotincludeinterestfromobligationsissuedbytheStateofColoradoorasubdivisionthereof.

LINE 5: Enter the allowable deductions from federalScheduleK.Forpartnerships,thiswouldbethetotaloflines12,13c(2),and13doffederalScheduleK;andforScorporations,thiswouldbethetotaloflines11,12c(2),and12doffederalScheduleK.Donotincludeamountsprovidedforinformationalpassthroughpurposesonly(e.g.domesticproductionactivitiesdeductionamounts).

Charitablecontributions(line13a,ScheduleK,Form1065,orline12a,ScheduleK,Form1120S)andinvestmentinterestexpense(line13b,ScheduleK,Form1065,orline12b,ScheduleK,Form1120-S)maybeincludedonline5ofForm106,butonlyifacompositereturnisbeingfiledforthe4.63%taxofthenonresidentpartnersorshareholders.Donotincludeanycharitabledeductionsforthedonationofaconservationeasementthatqualifiedforthegrossconservationeasementcredit.

LINE 6: Entertotheextentincludedinfederalincomeonline4,anyinterestincomeearnedonobligationsoftheUnitedStatesgovernmentandanyinterestincome earned on obligations of any authority,commission,orinstrumentalityoftheUnitedStatesto theextent suchobligationsareexempt fromstatetaxunderfederallaw.

Enterthemodificationforforeignsourceincomeofanexporttaxpayer.Ifapartnershipqualifiesasanexporttaxpayer,itmayexcludeforColoradoincometaxpurposesanyincomeorgainwhichconstitutes foreign source income for federalincome tax purposes. For purposes of thismodification, an "export taxpayer" means anypartnershipwhichsells50percentormoreofitsproductswhichareproducedinColoradoinstatesotherthanColoradoorinforeigncountries,orifthegrossreceiptsofsuchpartnershiparederivedfromtheperformanceofservices,suchservicesareperformedinColoradobyapartneroremployeeofthepartnershipandfiftypercentormoreofsuchservicesprovidedbythepartnershiparesoldorprovidedtopersonsoutsideofColorado.

Enter to theextent included in federal taxableincome, the excludable Colorado capital gainincomeforpropertyacquiredonorafterMay9,1994andheldforfiveormoreyears.SeeFYIIncome15forinformationonwhatcapitalgainsqualifyforthissubtraction.

NeithertheCcorporationforeignincomeexclusionor the partnership export taxpayer foreignsource income modification may be claimedby an S corporation or passed through to itsshareholders.

COLORADO SOURCE INCOMELINE 9: EntertheColoradosourceincome.Ifpartofthe

income isnotColoradosource income,see theinstructions for Apportionment of Income. TheColorado income tax statute provides that indeterminingthesourceofanonresidentpartner'sincome,noeffectshallbegiventoaprovisioninthe partnership agreement which characterizespaymentstothepartnerasbeingforservicesorfortheuseofcapital.Thuspaymentstopartners,whethersalariesorinterest,shallbeconstruedtobefromColoradosourcesandtaxablebyColoradointhesameratioasistheordinaryincomeofthepartnership.

The partnership will not normally determineincomefromColoradosourcesforanycorporatepartner as the corporationwill include its shareof the partnership's income and factors in itsownincomeandfactorssubjecttoallocationandapportionment.

COMPOSITE RETURN Complete lines 10 through 23 of Form 106 only if

a composite return is being filed for nonresident partners/shareholders.

LINE 10: Enter the Colorado source income of thenonresident partners/shareholders who areincludedinthecompositereturn.

LINE 11: Enter 4.63% of the Colorado source incomereportedonline10.

LINE 12: Enter the taxcredits fromForm106CR thatareallocatedtothenonresidentpartners/shareholdersincludedinthecompositereturn.Donotincludeanygrossconservationeasementcredit,whichmustbereportedseparatelyonline13.

LINE 13: Enter the gross conservation easement creditfromForm106CR,line36,thatwasallocatedtothenonresidentpartners/shareholdersincludedinthecompositereturn.AttachformsDR1303andDR1305tothereturn.SubmitformDR1304underseparatecover.

LINE 16: Enteranyestimatedtaxpaymentsorextensionpayment submitted on behalf of the partners/shareholdersincludedinthecompositereturn.

LINE 17: If 90%of the tax is not paidby theduedate,you must add a delinquent payment penalty.

Thepenaltyis5%oftheadditionaltaxdueforthefirstmonthofdelinquencyand1/2%foreachadditionalmonthuptoamaximumof12%.

LINE 18: Interestisdueonanybalanceoftaxduefromtheduedateattherateof3%(6%ifwebillyouandyoudonotpaywithin30days).

LINE 19: TheestimatedtaxpenaltyiscomputedforeachpartnerorshareholderonForm204.Thispenaltyappliesonlywhenthetaxdueforan individualincluded in the composite filing is more than$1,000.Ifthispenaltyisdue,attachForm204foreachindividualwhoowesthepenaltyandenterthetotalpenaltyonline19.

LINE 20: Enterthebalancedue,includinganypenaltyorinterestduefromlines17,18and19.

LINE 21: Iftheprepaymentsonline16exceedthetaxdueonline15,entertheamountoftheoverpaymentonline21.

LINE 22: Entertheamountfromline21youwanttocredittowardnextyear'sestimatedtax.

LINE 23: Entertheamountfromline21youwishtohaverefundedatthistime.

TheDepartmentcandeposityourrefunddirectlyintoyouraccountataU.S.bankorotherfinancialinstitution(suchasmutualfund,brokeragefirm,orcreditunion)intheUnitedStates.

• Fasterrefund• Saferrefund–Nochecktogetlost.• Convenient–Notriptothebank.

your returnAND use Direct Deposit. get yourrefundintwoweeks.

How do I use Direct Deposit?Completetheroutingnumber,typeofaccountandaccountnumberonline48.

The routing numbermust be nine digits.The first twodigitsmustbe01through12or21through32.Yourcheckmaystatethatitispayablethroughabankdifferentfromthefinancialinstitutionatwhichyouhaveyourcheckingaccount.Ifso,donotusetheroutingnumberinthatcheck.Instead,contactyourfinancialinstitutionforthecorrectroutingnumbertoenteronthisline.Theaccount numbercanbeupto17characters(bothnumbersandletters).Includehyphensbutomitspacesandspecialsymbols.Enterthenumberfromlefttorightandleaveanyunusedboxesblank.Donotincludethechecknumber.

Youshouldcontactyourfinancialinstitutiontomakesureyour deposit will be accepted and to obtain the correctroutingandaccountnumbers.Thisisespeciallyimportantifyouwantyourrefunddepositedtoasavingsaccountatacreditunion.TheColoradoDepartmentofRevenueisnotresponsibleforalostrefundifyouenterthewrongaccountinformation.Anyrefundclaimthat,foranyreason,cannotbedepositedintotheaccountspecifiedwillbeissuedandmailedincheckforminstead.

NameofOrganization ColoradoAccountNumber

DoingbusinessAs

Address FederalEmployerI.D.Number

City State ZIP

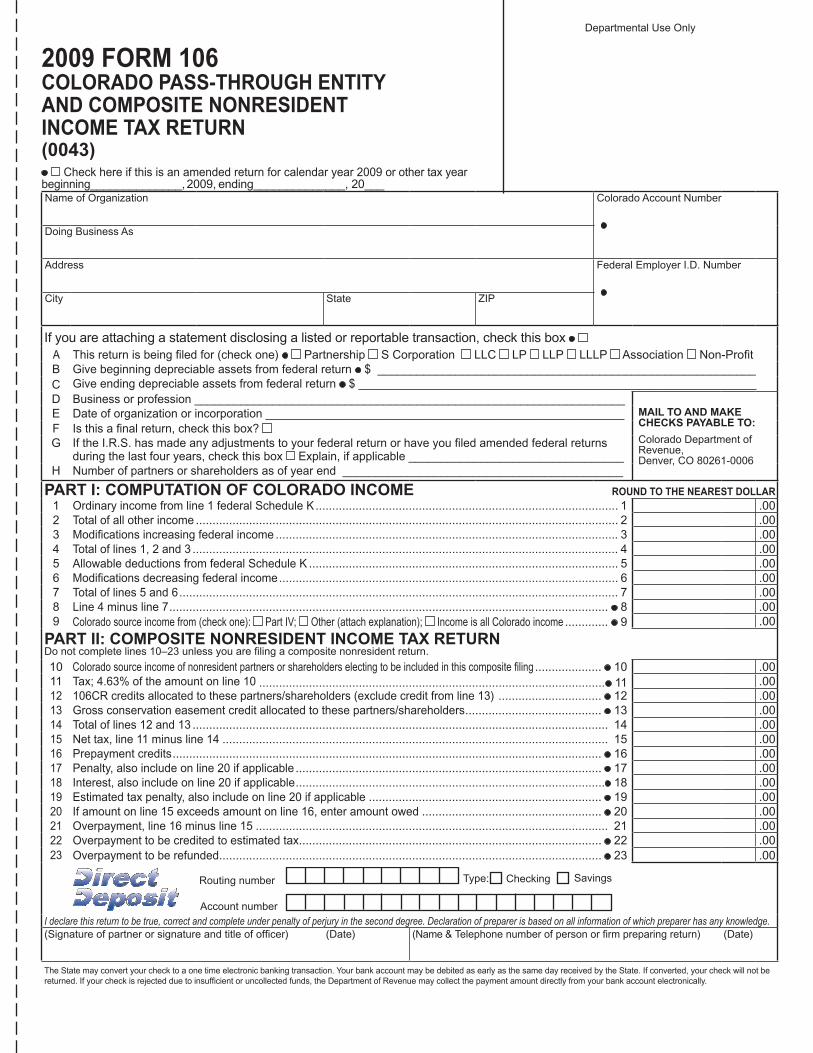

Ifyouareattachingastatementdisclosingalistedorreportabletransaction,checkthisbox A Thisreturnisbeingfiledfor(checkone) Partnership SCorporation LLC LP LLP LLLP Association Non-ProfitB givebeginningdepreciableassetsfromfederalreturn $__________________________________________________________C giveendingdepreciableassetsfromfederalreturn $_____________________________________________________________D businessorprofession__________________________________________________________________

MAIL TO AND MAkE CHECkS PAYABLE TO:

ColoradoDepartmentofRevenue,Denver,CO80261-0006

E Dateoforganizationorincorporation_______________________________________________________F Isthisafinalreturn,checkthisbox? g IftheI.R.S.hasmadeanyadjustmentstoyourfederalreturnorhaveyoufiledamendedfederalreturns

duringthelastfouryears,checkthisbox Explain,ifapplicable_________________________________H Numberofpartnersorshareholdersasofyearend___________________________________________

PART I: COMPUTATION OF COLORADO INCOME ROUND TO THE NEAREST DOLLAR1 Ordinaryincomefromline1federalScheduleK........................................................................................... 1 .002 Totalofallotherincome............................................................................................................................... 2 .003 Modificationsincreasingfederalincome....................................................................................................... 3 .004 Totaloflines1,2and3................................................................................................................................ 4 .005 AllowabledeductionsfromfederalScheduleK............................................................................................. 5 .006 Modificationsdecreasingfederalincome...................................................................................................... 6 .007 Totaloflines5and6.................................................................................................................................... 7 .008 Line4minusline7.................................................................................................................................... 8 .009 Colorado source income from (check one): Part IV; Other (attach explanation); Income is all Colorado income............. 9 .00

PART II: COMPOSITE NONRESIDENT INCOME TAX RETURNDonotcompletelines10–23unlessyouarefilingacompositenonresidentreturn.

10 Colorado source income of nonresident partners or shareholders electing to be included in this composite filing.................... 10 .0011 Tax;4.63%oftheamountonline10........................................................................................................ 11 .0012 106CRcreditsallocatedtothesepartners/shareholders(excludecreditfromline13)............................... 12 .0013 grossconservationeasementcreditallocatedtothesepartners/shareholders......................................... 13 .0014 Totaloflines12and13............................................................................................................................. 14 .0015 Nettax,line11minusline14.................................................................................................................... 15 .0016 Prepaymentcredits................................................................................................................................. 16 .0017 Penalty,alsoincludeonline20ifapplicable............................................................................................ 17 .0018 Interest,alsoincludeonline20ifapplicable............................................................................................. 18 .0019 Estimatedtaxpenalty,alsoincludeonline20ifapplicable...................................................................... 19 .0020 Ifamountonline15exceedsamountonline16,enteramountowed...................................................... 20 .0021 Overpayment,line16minusline15.......................................................................................................... 21 .0022 Overpaymenttobecreditedtoestimatedtax........................................................................................... 22 .0023 Overpaymenttoberefunded................................................................................................................... 23 .00

Type: Checking SavingsRoutingnumber

AccountnumberI declare this return to be true, correct and complete under penalty of perjury in the second degree. Declaration of preparer is based on all information of which preparer has any knowledge.(Signatureofpartnerorsignatureandtitleofofficer) (Date) (Name&Telephonenumberofpersonorfirmpreparingreturn) (Date)

TheStatemayconvertyourchecktoaonetimeelectronicbankingtransaction.YourbankaccountmaybedebitedasearlyasthesamedayreceivedbytheState.Ifconverted,yourcheckwillnotbereturned.Ifyourcheckisrejectedduetoinsufficientoruncollectedfunds,theDepartmentofRevenuemaycollectthepaymentamountdirectlyfromyourbankaccountelectronically.

2009 FORM 106COLORADO PASS-THROUGH ENTITY AND COMPOSITE NONRESIDENT INCOME TAX RETURN(0043) Checkhereifthisisanamendedreturnforcalendaryear2009orothertaxyearbeginning______________,2009,ending______________,20___

DepartmentalUseOnly

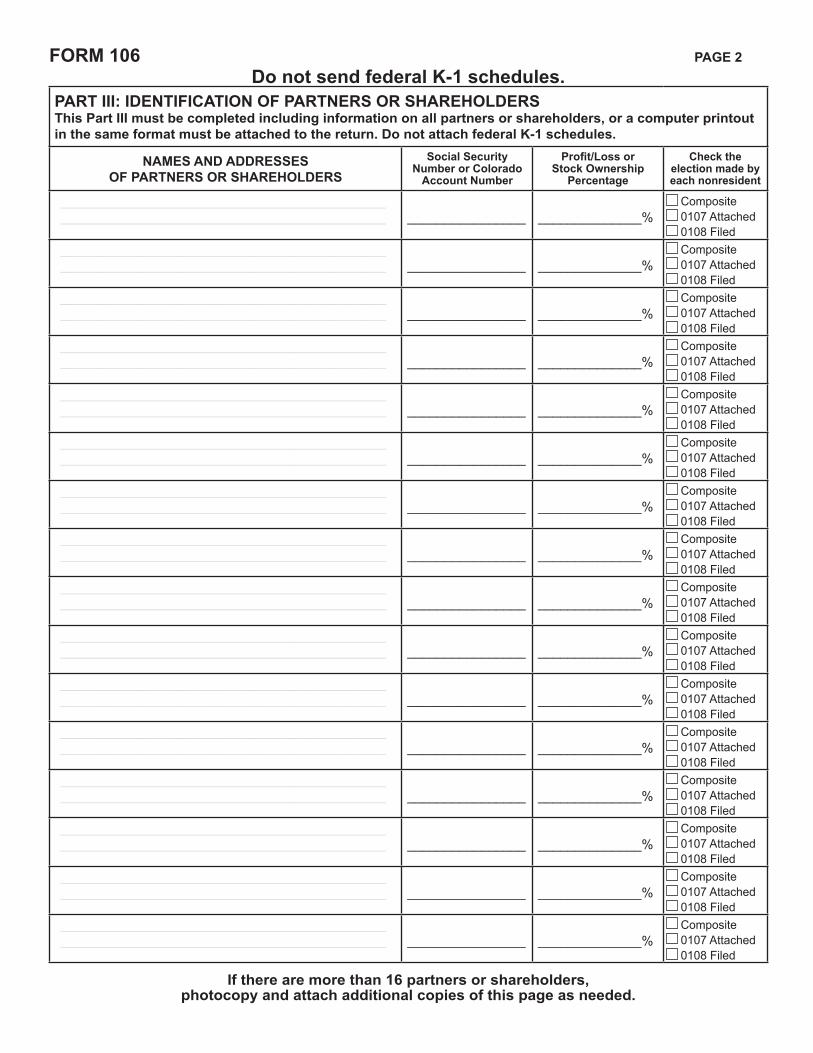

FORM 106 PAGE 2

Do not send federal k-1 schedules.PART III: IDENTIFICATION OF PARTNERS OR SHAREHOLDERSThis Part III must be completed including information on all partners or shareholders, or a computer printout in the same format must be attached to the return. Do not attach federal k-1 schedules.

NAMES AND ADDRESSESOF PARTNERS OR SHAREHOLDERS

Social Security Number or Colorado

Account Number

Profit/Loss orStock Ownership

Percentage

Check theelection made byeach nonresident

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

__________________________________________________________________________________________________ ________________ ______________%

Composite0107Attached0108Filed

If there are more than 16 partners or shareholders,photocopy and attach additional copies of this page as needed.

FORM 106 PAGE 3

PART IV— APPORTIONMENT OF INCOME UNDER THE COLORADO INCOME TAX SINGLE FACTOR FORMULADO NOT SEND FEDERAL RETURN FORMS OR SCHEDULES WITH THIS RETURN

1 Totalmodifiedfederaltaxableincomefromline8,PartI,page1,Form106...................................................................... 1

BUSINESS INCOME APPORTIONED TO COLORADO BY USE OF THE REVENUE FACTORDONOTINCLUDEFOREIgNSOURCEREvENUESMODIFIEDOUTONLINE6,PARTI,PAgE1,FORM106 Colorado Total

2 grosssalesoftangiblepersonalproperty.................................................... 2

3 grossrevenuefromservices........................................................................ 3

4 grossrentsandroyaltiesfromrealproperty............................................... 4

5 grossproceedsfromsalesofrealproperty................................................ 5

6 Taxableinterestanddividendincome........................................................ 6

7 gainfromthesaleofintangiblepersonalproperty..................................... 7

8 Patentandcopyrightroyalties..................................................................... 8

9 Revenuefromtheperformanceofpurelypersonalservices..................... 9

10 Totalrevenue(totaloflines2through9ineachcolumn)....................... ..10

11 Line10(Colorado)dividedbyline10(Total)...................................................................................11 %COMPLETE LINES 12 AND 15 ONLY IF NONBUSINESS INCOME IS BEING DIRECTLY ALLOCATED. IF ALL INCOME IS BEING TREATED AS

BUSINESS INCOME, ENTER 0 (ZERO) ON LINES 12 AND 15.

12 Lessincomedirectlyallocable (a)Netrentsandroyaltiesfromrealortangiblerealproperty.............

NONbUSINESS

INCOME

ONLY

(b)Capitalgainsandlosses.................................................................

(c)Interestanddividends.....................................................................

(d)Patentsandcopyrightroyalties.......................................................

(e)Othernonbusinessincome.............................................................

(f)Totalincomedirectlyallocable(addlines(a)through(e)).............................................. 12

13 Modifiedfederaltaxableincomesubjecttoapportionmentbyformula,line1lessline12.................................................. 13

14 IncomeapportionedtoColoradobyformula,line11timesline13...................................................................................... 14

15 Add income directly allocable to Colorado:

(a)Netrentsandroyaltiesfromrealortangiblerealproperty............

(b)Capitalgainsandlosses................................................................

(c)Interestanddividends....................................................................

(d)Patentsandcopyrightroyalties......................................................

(e)Othernonbusinessincome............................................................

(f)Totalincomedirectlyallocable(addlines(a)through(e))..................................................15

16 TotalincomeapportionedtoColorado,line14plusline15.Enteronline9,part1,page1,Form106................................16

THIS PAGE INTENTIONALLY

LEFT BLANk

FORM 106CR 2009

COLORADO PARTNERSHIP—S CORPORATION CREDIT FORM

OrganizationName ColoradoAccountNumber

CREDIT FOR TAX PAID OTHER STATE BY S CORPORATIONAMOUNTSTObEDISTRIbUTED

1. NameofState.............................................................................. ________________________2. Amountofincomefromsourceswithinstate............................... ________________________3. Amountofincometaxliabilitytostate........................................................................................ 3

THE OLD INVESTMENT CREDIT4. Federalcurrent-yearqualifiedinvestmentinColoradoassets................................................... 4

THE NEW INVESTMENT CREDIT5. Qualifyingcurrentyearinvestment.............................................. ________________________6. 1%oftheamountonline5............................................................................................................. 6

ENTERPRISE ZONE INVESTMENT CREDIT7. Qualifyingcurrentyearinvestment.............................................. ________________________8. 3%oftheamountonline7........................................................................................................ 8

ENTERPRISE ZONE NEW BUSINESS FACILITY EMPLOYEE CREDITS9. Averagenumberofcurrentyearqualifiedemployees.................................................10.Numberofemployeespreviouslyclaimed...................................................................11. Increaseinqualifiedemployees,line9minusline10..................................................12.Numberofemployeesonline11multipliedby$500............................................................... 1213.Numberofemployeesonline11locatedinaruralenterprisezonemultipliedby$2,000....... 1314.Numberofagriculturalprocessingemployeesonline11multipliedby$500.......................... 1415.Numberofemployeesonline14locatedinaruralenterprisezonemultipliedby$500.......... 1516.Numberofhealthinsuredqualifiedemployeestimes$200..................................................... 16

CONTRIBUTION TO ENTERPRISE ZONE ADMINISTRATOR17.Currentyearcashcontributions............................................................................................... 1718.valueofcurrentyearin-kindcontributions............................................................................... 18

ENTERPRISE ZONE RESEARCH AND DEVELOPMENT CREDIT19.Qualifyingcurrentyearexpenditures.................................................. ____________________20.Firstprecedingyearexpenditures....................................................... ____________________21.Secondprecedingyearexpenditures................................................. ____________________22.Totallines20and21........................................................................... ____________________23.One-halfoftheamountonline22....................................................... ____________________24.Line19minusline23.......................................................................... ____________________25.3%oftheamountonline24.................................................................................................... 25

OTHER CREDITS26.Historicpropertypreservationcredit........................................................................................ 2627.Alternativefuelvehiclecredit................................................................................................... 2728.Alternativefuelrefuelingfacilitycredit...................................................................................... 2829.Childcarecontributioncredit................................................................................................... 2930.Childcarecenterfamilycarehomeinvestmentcredit............................................................. 3031.Employerchildcareinvestmentcredit..................................................................................... 3132.Schooltocareerinvestmentcredit........................................................................................... 3233.Enterprisezonejobtrainingcredit........................................................................................... 3334.Enterprisezonevacantcommercialbuildingrehabilitationcredit............................................ 3435.Coloradoworksprogramcredit................................................................................................ 3536.grossconservationeasementcredit....................................................................................... 3637.Contaminatedlandredevelopmentcredit................................................................................ 3738.Low-incomehousingcredit...................................................................................................... 3839.Aircraftmanufacturernewemployeecredit............................................................................. 3940. Jobgrowthincentivecredit...................................................................................................... 40

IN GENERAL. Colorado creditsmay be passed throughfrom partnerships, and S corporations to the partners,or shareholders. Normally the potential credit is passedthroughanditisuptothepartnerorshareholdertodeterminehisorherownlimitations.

Somecreditsmaybeclaimedonlybyindividuals,estatesortrustswhereothersmaybeclaimedonlybyCCorporations.Other credits may be available to all taxpayers. Creditscannot be claimed by some partners or shareholderscannotberedistributedtootherpartnersorshareholders.Forexample,ifapartnershipconsistedofaCcorporationand an individual, the individual partner’s share of thepartnership’snewinvestmenttaxcreditcouldnotbeclaimedbythecorporationeventhoughtheindividualpartnerisnotallowedtouseit.

CREDIT FOR TAX PAID OTHER STATES.ColoradoresidentScorporationshareholdersmayclaim

creditfortheirshareofanynetincometaxpaidtoanotherstate by the corporation when the other state does notrecognizetheScorporationelection.CompleteaseparateForm106CRforeachstatetowhichtaxwaspaid.AdviseeachColoradoresidentshareholderofhisorhershareofthecorporateincomefromsourcesintheotherstateandhisorhershareofthetaxpaid.

THE OLD INVESTMENT TAX CREDIT is10%ofthetentativecurrentyearfederalinternalrevenuecodesection46creditonassetslocatedinColoradoandmaybeclaimedonlybyCcorporations(thiswouldapplyinthecaseofapartnershipwithaCcorporationpartner.)SeeFYIIncome11.

THE NEW INVESTMENT TAX CREDITisbasically1%ofthequalifiedinvestmentintangiblepersonalpropertyusedinatradeorbusinessinColorado.ThiscreditmaybeclaimedonlybyCcorporations.SeeFYIIncome11.

THE ENTERPRISE ZONE INVESTMENT CREDITisbasically3%ofthequalifiedinvestmentintangiblepersonalpropertyusedinatradeorbusinessinaColoradoenterprisezone.Itmaybeclaimedbyalltaxpayers.SeeFYIIncome11.

THE ENTERPRISE ZONE NEW BUSINESS FACILITY EMPLOYEE CREDIT is a credit of $500 for each newjobcreatedwithrespect toaqualifiedenterprisezonenewbusinessfacility.Additionalcreditsmaybeavailable

dependingon the locationof thebusiness, thenatureof the work performed and the benefits provided tothe employee(s). These credits are available to alltaxpayers.

A credit for contributions to enterprise zone administratorstofurthertheeconomicdevelopmentplansofthezoneisallowedtoalltaxpayers.

Acreditof3%oftheincreaseinaqualifiedenterprise zone research and experimental expendituresisavailabletoalltaxpayers.SeeFYIIncome22.

All Other Credits entered on lines 26 through 40 areavailabletoalltaxpayers.SeethefollowingFYIs,availableonlineatwww.TaxColorado.com foradditional informationregardingthesecredits.

Historicpropertypreservationcredit.............. FYIIncome1

Alernativefuelvehiclecredit.......................... FYIIncome9

Alternativefuelrefuelingfacilitycredit........... FYIIncome9

Childcarecontributioncredit......................... FYIIncome35

Childcarecenterfamilycarehomeinvestmentcredit............................................ FYIIncome7

Employerchildcareinvestmentcredit........... FYIIncome7

Schooltocareerinvestmentcredit................ FYIIncome32

Enterprisezonejobtrainingcredit................. FYIIncome31

Enterprisezonevacantcommercialbuildingrehabilitationcredit........................... FYIIncome24

Coloradoworksprogramcredit...................... FYIIncome34

grossconservationeasementcredit............. FYIIncome39

Contaminatedlandredevelopmentcredit..................................... FYIIncome42

Low-incomehousingcredit............................ FYIIncome46

Aircraftmanufacturernewemployeecredit...................................... FYIIncome62

Jobgrowthincentivecredit...ContacttheColoradoEconomicDevelopmentCommision.AcreditcertificateissuedbytheCommissionmustbeattachedtoanyreturnclaimingthiscredit.

INSTRUCTIONS FOR FORM 106CR

COLORADO DEPARTMENTOF REVENUEDENvERCO80261-0006

PRSRTSTDU.S.POSTAgE

PAIDCOLORADODEPTOFREvENUE

FYIs are available at www.TaxColorado.com